Quick Answer

Start by treating freelancer hiring as an operating decision, not just a talent decision. The benefits hiring freelancers business case is strongest when scoped work can be delivered fast and paid cleanly, with country checks handled up front in the UK, US, and Australia. In practice, that means confirming worker-status logic, collecting required forms like W-9 or W-8BEN where applicable, and proving payout-to-reconciliation traceability before recurring volume.

The real question is not only whether freelancers are cheaper or more flexible#

The real question is not only whether freelancers are cheaper or more flexible. It is whether hiring them can increase output without creating tax, classification, and payment-process issues that slow the business down later. That is the lens for this guide.

There is real upside here. Freelancers can give you flexible staffing when demand moves around, and companies often turn to them when budgets are tight, timelines are short, and a full-time hire is not realistic. But those gains hold only if your team can onboard people cleanly, pay them correctly, and handle the required admin steps without creating a lot of manual work.

That is why this article treats freelancer hiring as an operating model choice across the UK, US, and Australia, rather than a generic talent tactic. The work may look similar in each market, but the administrative burden does not.

In the UK, freelancers and contractors often handle their own tax and National Insurance contributions, yet worker status still matters because employment status affects rights and employer responsibilities. In the US, the IRS says the first step for paying an independent contractor is collecting Form W-9. In Australia, supplier onboarding can become a withholding issue if an ABN is missing. If a supplier does not provide an ABN and the payment for goods and services is more than $75 excluding GST, the payer generally withholds at the top tax rate.

Those are not edge details. They are operating facts that often determine whether a freelancer model stays light or becomes harder to run. A useful early checkpoint is simple: before you approve recurring work, confirm the classification logic, the tax document you need, and the payee details you will rely on for payout. If that evidence pack is incomplete, speed on the front end can become delay on the back end.

So the goal here is practical. We will separate the situations where freelancers are likely to add flexibility from the ones where country-specific admin requirements add coordination overhead and compliance risk. If you are entering one market with tightly scoped work, freelancers can be a strong fit. If you are spreading work across countries without clear document collection, onboarding rules, and ownership of payment exceptions, that flexibility can fade quickly.

Define Benefits in Operating Terms#

A freelancer model is a real benefit only when you can measure it and tie it to a control your team can enforce. Define each upside in operating terms before you use it in planning.

| Benefit category | Measure it with something observable |

|---|---|

| Speed to delivery | Days from approved brief to first accepted deliverable |

| Cost predictability | Variance between quoted cost and approved spend |

| Quality control | Acceptance rate, rework rounds, or defect fixes after handoff |

| Expansion optionality | Time and support effort needed to add another freelancer or market |

After that, map each benefit to the document that protects it. The contract is the legally enforceable promise, while the Statement of Work defines the services or work to be performed. Use both to make deliverables, deadlines, payment terms, and IP expectations explicit. If copyright ownership must transfer, do not assume payment covers it; the transfer needs to be in writing and signed. A Service-Level Agreement covers delivery expectations such as response times and performance standards, and should also state how performance is measured.

Then separate strategic upside from operational readiness: can your team onboard people, run Payouts, and resolve failed payments or scope disputes without adding headcount? A practical gate is simple: do not approve recurring work until the contract, SOW, payout details, and exception owner are confirmed.

Treat SERP snippets as leads, not proof. Search descriptions or cache can be outdated, so any SERP-based claim should remain unverified until someone checks the primary source and records what was confirmed.

Compare Freelancers Against Full-Time and Agencies#

Choose the model based on the kind of capacity you need: if demand is volatile and specialist work is narrow, freelancers usually fit best; if continuity and institutional memory are critical, full-time or a hybrid model is usually stronger.

| Model | Ramp time | Control | Fixed cost | Variable cost | Failure recovery |

|---|---|---|---|---|---|

| Freelancer | Often faster for narrow, scoped work because ramp-up can be lighter than a new hire or a stretched internal team | Lower day-to-day control if you need to stay within contractor boundaries | Low | Active only while work is in scope; cost can stop when the project ends | Can be quick for replaceable tasks, but risky if key context sits with one person |

| Full-time hire | Usually slower to start because hiring and onboarding take time | Highest direct control over priorities, methods, and continuity | Highest | Lower marginal cost once onboarded | Stronger for ongoing ownership and repeated handoffs |

| Agency | Can move quickly when you need an early capacity boost across skills | Indirect control through scope, account management, and service terms | Medium to high | Medium to high, often bundled | Recovery depends on handoff quality and accountability clarity |

Operational control and legal control are not the same. In the US, worker classification is framed around behavioral control, financial control, and the relationship of the parties. If you manage contractors like employees, you reduce the operating upside and increase classification risk.

Financial operations changes the answer#

Even when the delivery model looks right, finance operations can break it.

| Model | Invoicing owner | Payout Batches responsibility | Ledger Journals reconciliation |

|---|---|---|---|

| Freelancer | Your team usually validates invoice-to-scope match | Your team schedules and releases batches | Your team verifies payout and fee entries after settlement |

| Full-time hire | Payroll-led recurring payments | Usually payroll-driven cycles | Usually payroll/accounting-led review |

| Agency | Vendor invoice ownership is often simpler at the surface | Batch handling depends on your payable setup | Reconciliation can be less transparent when charges are bundled |

Keep the checkpoint strict: before you approve recurring external spend, confirm who approves invoices, who releases Payout Batches, and who reviews Ledger Journals. If no one owns payment failures or invoice disputes, the model is not ready to scale.

Coordination risk is real in freelancer-heavy execution. As one marketplace leader put it, "just putting two people to work together is super complex."

Scenario contrast#

For a one-country launch with narrow scope, freelancers can be the cleanest option: defined deliverables, acceptance-based payout, and variable cost boundaries.

For a multi-country rollout with shared API behavior and Webhooks dependencies, continuity usually becomes the constraint. In that case, a hybrid model often holds up better: keep core employees on architecture and incident ownership, then add freelancers or agency support for targeted execution spikes.

For UK-to-US contractor payment mechanics, see How to Pay US-Based Freelancers from the UK.

Choose Markets Where Freelancer Benefits Survive Payment Reality#

Launch markets only where payout operations are predictable end to end. Freelancer economics hold up when corridor coverage, tax onboarding, payout status, retries, and reconciliation are all verifiable.

A model that looks efficient on paper can become expensive quickly in the UK, US, or Australia if you rely on manual bank handling, unresolved tax checks, or opaque payout failures.

Country comparison#

| Country | Payout practicality | Onboarding burden | Tax-document complexity |

|---|---|---|---|

| UK | Viable if the exact corridor is supported and you can use standard Payouts instead of one-off bank transfers. Local currency account infrastructure can reduce setup friction when local receiving details are needed. | Medium. In most cases, the client is responsible for determining worker status under IR35, so onboarding goes beyond identity and bank details. | Medium. The main burden here is status determination, not a long information-return form stack. |

| US | Viable only after explicit corridor verification. Standard Payouts are usually more practical than manual transfer instructions because status visibility is clearer for reporting and exception handling. | High. Form W-9 may be needed to collect a correct TIN, and W-8BEN may be required when requested in some cross-border flows. | High. 1099-NEC filing may apply, so document collection and payer records need to be in place early. |

| Australia | Viable if both Australia and the target corridor are confirmed in platform coverage. Local currency account options can reduce setup friction. | Medium to high. Capture the supplier's ABN early because missing it can change payment handling. | Medium to high. If no ABN is provided and payment for goods and services is more than $75 excluding GST, you generally withhold the top rate of tax. |

Where Virtual Accounts (or similar local currency accounts) and standard Payouts are available together, setup and support friction usually drop. Where teams depend on manual bank transfer flows, support load rises because exceptions turn into case-by-case investigations instead of visible payout states.

Before opening any corridor, run one pilot cycle and confirm:

- Coverage: the sending entity, receiving country, and payout method are supported for that exact corridor.

- Status and retries: payout events are visible and recoverable; if you use webhooks, undelivered events are retried and processed correctly (Stripe retries for up to three days).

- Reconciliation: finance can match each payout outcome to approval and settlement records, including failures and retries.

Do not launch yet if compliance gates or payout success rates are not verifiable. Pause if US flows cannot reliably collect W-9 or W-8BEN where needed, UK IR35 responsibility is unresolved, Australia ABN capture is incomplete, or failed payouts cannot be traced cleanly from event to reconciliation.

Cross-border payments remain structurally friction-heavy, so expansion should follow operational evidence, not market excitement. Related: How to Pay US-Based Contractors from Australia.

Price the Hidden Costs Before You Commit#

Rate cards alone do not tell you whether freelancer hiring is affordable; total delivered cost does. Price the full operating picture up front: sourcing and screening time, coordination across reviews and handoffs, rework from unclear scope or acceptance criteria, delayed releases from stretched feedback loops, and payment operations, including exception handling and reconciliation.

A lower hourly rate is a loss if extra review cycles and rework slow delivery. Marketplace fees also change the math: one major platform shows a 5% service fee on its basic client plan and states that a contract initiation fee is charged per contract, so short engagements can accumulate overhead quickly.

The contract signals that predict cost creep#

Treat contract quality as an operating-cost control, not legal housekeeping. In August 2025, WorldCC reported businesses lose almost 9% annually through poor contract management, with best performers around 3% and worst performers at 15% or more.

Before you launch, check these red flags:

- A

Freelancer Contractwithout clear acceptance criteria in the statement of work (the part that describes the services or work to be performed). - A weak

Service-Level Agreementthat does not define expected performance or what happens when targets are missed. - No named owner for payment exceptions, reissue decisions, and finance follow-up.

Estimate payment operations before volume#

Require a pre-launch estimate for Payouts and Ledger work, not just talent spend. Payment reconciliation means verifying internal records, including journal entries and general ledger records, match external statements for completeness and accuracy, not just confirming a payout was sent.

Use a pilot to measure manual touches per payment from approval to ledger match. If finance cannot trace each payout cleanly from approval to settlement to reconciliation entry, your true operating cost is still unknown. For a step-by-step walkthrough, see Best Business Books for Freelancers Building a Durable Business.

Put Compliance and Tax Gates in Front of Scale#

Scale only after identity and tax controls are complete, and only then enable recurring Payout Batches. If batch payouts go live first, unresolved onboarding checks become recurring payment exceptions.

KYC, KYB, and AML are market- and program-specific controls, not one global checklist. In practice, verify individual identity, verify beneficial owners for legal entities where KYB applies, and confirm AML gating for each target market/program before rollout.

Set one hard gate before batch payouts#

Treat batch eligibility as binary: no freelancer or business enters recurring Payout Batches until required identity and tax states are complete.

| Check | Required state |

|---|---|

| Identity | individual identity verified, and beneficial owners verified for legal entities where applicable |

| Tax profile | tax profile collected and accepted for the relevant payment flow |

| Payout method | payout method approved for that market or program |

Before scaling, test this in a pilot: sample recently onboarded profiles and confirm each can be traced from identity review to tax form to payout approval. If records rely on email attachments, spreadsheet notes, or one-off checks, keep volume gated.

Match the tax artifact to the flow#

| Payment or reporting flow | Required artifact | Operator note |

|---|---|---|

| U.S. person paid by a requester that may file IRS information returns | W-9 | Use Form W-9 to collect the correct TIN from the payee. |

| Foreign individual receiving U.S.-source payments | W-8BEN | Use it to establish foreign status and, where relevant, support treaty-based withholding treatment. |

| U.S. business reporting eligible contractor payments | 1099-NEC | Records should support nonemployee compensation reporting; do not rely on remembered thresholds. |

| U.S. person with foreign financial accounts | FBAR on FinCEN Form 114 | Filing can apply if aggregate account value exceeded $10,000 during the year. Standard due date is April 15, with an automatic extension to October 15. |

| Cross-border support questions on overseas earned income | FEIE workflow, where enabled | FEIE can reduce regular income tax on qualifying self-employment income, but it does not reduce self-employment tax. |

Store the evidence on the profile: verification result, legal name, tax form, and the market/program under which approval was granted.

Apply the same rule to VAT Validation. In the EU, VIES is a search engine against national VAT databases, and validation procedures vary by country. If GTM depends on VAT checks or broader business verification, confirm country- and program-level coverage before launch commitments.

Build a 90-Day Execution Sequence#

After compliance and tax gates are complete, use a three-phase rollout: set written controls first, validate operations in a pilot, then scale only on evidence.

| Phase | Focus | Evidence |

|---|---|---|

| Phase 1 | Set written controls before assigning work | Freelancer Contract, Service-Level Agreement, and acceptance criteria tied to delivery and payout milestones |

| Phase 2 | Run a small pilot cohort through onboarding, work assignment, Payouts, and reconciliation | Verify onboarding completion, event receipt, correct profile matching, and a matching journal entry for amount, counterparty, and status |

| Phase 3 | Scale only after the pilot meets internal thresholds | Use stages such as 1%, 5%, 10%, 20%, then 50%, with written rollback criteria |

Phase 1#

Start with written controls before assigning work. Use a Freelancer Contract to establish project basics and a Service-Level Agreement to define expected service performance.

Then set acceptance criteria tied to both delivery and payout milestones. If a milestone can trigger payment, it should also have a clear, testable completion rule. Keep those rules in the formal workflow, not scattered across chat or email. Do not assume one contract or SLA template works unchanged across markets without local review.

Phase 2#

Run a small pilot cohort through the full path: onboarding, work assignment, Payouts, and reconciliation. The goal is to surface issues early and collect evidence before broader rollout.

Use Webhooks and Ledger Journals as verification points. A webhook gives an HTTPS JSON event when status changes, and a ledger journal entry records the transaction in accounting records. For each pilot payout, verify onboarding completion, event receipt, correct profile matching, and a matching journal entry for amount, counterparty, and status. Do not treat webhook receipt alone as proof of full reconciliation.

Phase 3#

Scale only after your pilot meets internal thresholds for delivery reliability, payment success, and support volume. Define those thresholds before the pilot and assign clear ownership for measurement.

If results are mixed, expand in controlled stages such as 1%, 5%, 10%, 20%, then 50% to limit exposure while monitoring exceptions. Set rollback criteria in writing: pause new onboarding if exception queues exceed internal limits, unresolved payout statuses age without resolution, or support demand outpaces team capacity.

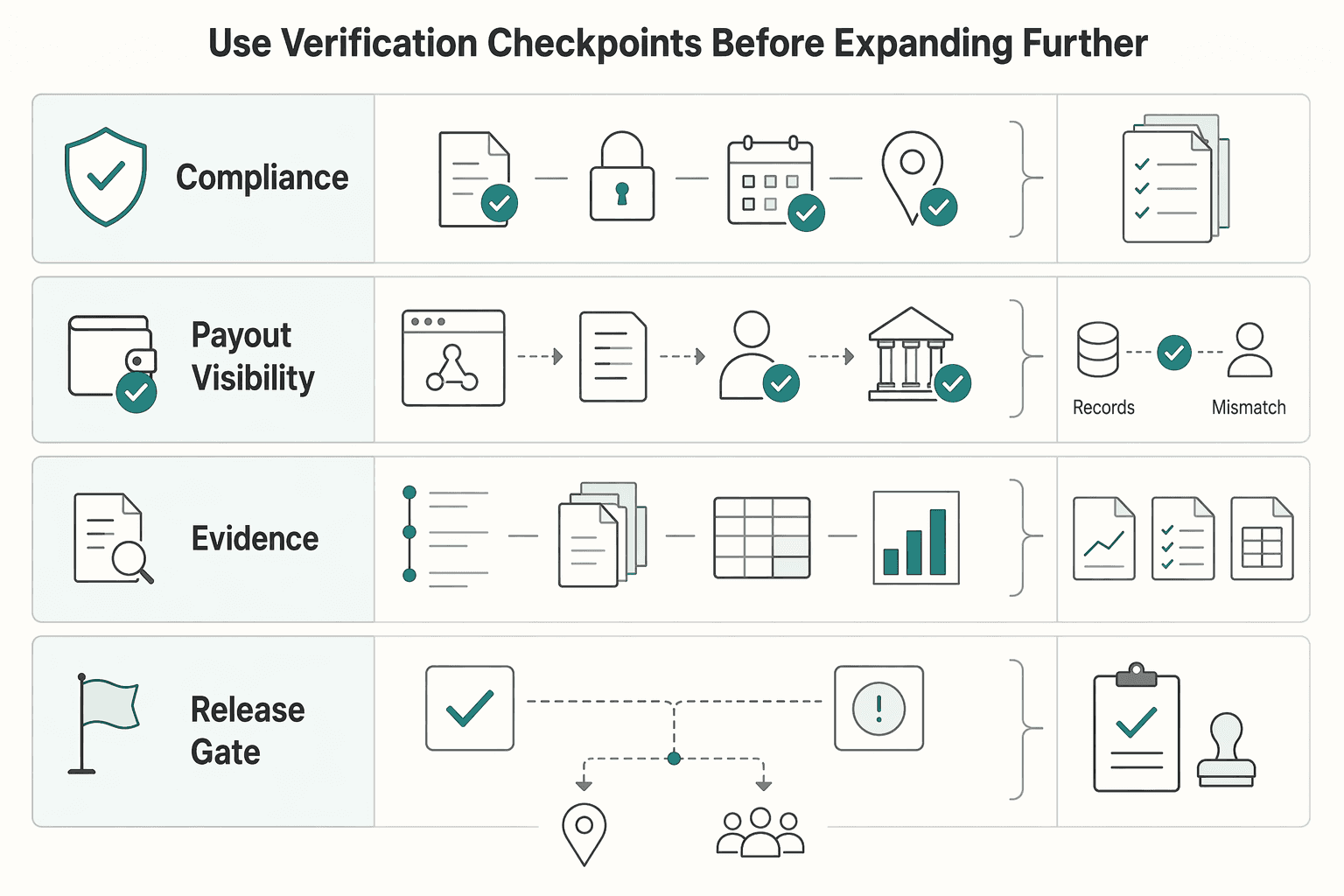

Use Verification Checkpoints Before Expanding Further#

Expansion should be evidence-gated after the pilot. For each country or corridor, run a go/no-go check that confirms compliance completion, payout reliability, usable audit logs, and documented finance sign-off.

| Go/no-go check | What to confirm |

|---|---|

| Compliance | onboarding and compliance checks are complete for the freelancers you plan to pay |

| Payout visibility | recent payouts are completing with enough status visibility to investigate failures |

| Audit records | retained audit logs and records let ops and finance trace what happened |

| Finance sign-off | finance sign-off is documented in your team's actual approval format, not just chat |

Then run a separate technical readiness check. API calls should be idempotent so retries do not create duplicate side effects. Webhook handling should tolerate asynchronous delivery, including late, duplicate, or out-of-order events. For each payout flow, verify you can match the webhook to the right freelancer record, update the correct payout state, and confirm the ledger reflects the final outcome.

Do not treat webhook receipt as completed reconciliation. A common failure mode is receiving the event but missing or misposting the ledger entry, which usually surfaces when finance matches payouts to bank deposits.

Define your internal stop rule before rollout and apply it consistently during canary-style expansion reviews. If checks are missed, pause market adds, fix operations, and re-verify before continuing. Keep the leadership evidence pack lightweight: assumptions, observed outcomes, unresolved risks, and the next verification date.

Conclusion#

The right call is rarely "freelancers are good." It is "freelancers are a fit here, on this corridor, with these controls." Treat cross-border hiring as an operating decision first and a talent decision second if you want the real upside from the business case.

That matters because the payment layer is still uneven. The Bank for International Settlements describes the structural gap clearly: cross-border payments remain more costly, slower, less accessible, and less transparent than domestic payments. The Financial Stability Board frames the same persistent pain points as cost, speed, access, and transparency. The G20 roadmap to improve this has been active since 2020, and most endorsed targets are still aimed at end-2027. Plan around current friction, not future promises.

For operators, the practical implication is simple. Do not approve a new market because the freelance talent looks strong on paper or the day rate looks attractive. Approve it when your payouts actually work with visible status, known exception handling, and finance reconciliation that closes cleanly. If you cannot trace what happened when a payment is delayed, returned, or split across fees and ledger entries, you are not looking at flexibility. You are looking at execution debt.

A good final check is to review one small evidence pack before you commit GTM resources. It does not need to be heavy, but it should be real:

- one live or pilot corridor result showing payout outcome visibility end to end

- the current onboarding and compliance status needed to enable payment

- the finance proof that the payout event and reconciliation record match

- a short list of unresolved route-specific risks, owners, and the next review date

There is also a useful red flag here. Modern tracking and improvement efforts, including tools built to improve speed and transparency, do not make every route behave the same way. Route-level performance still varies significantly. So if your next move is, say, a US corridor, do not assume the results from another country transfer cleanly. Re-test the corridor, then scale.

The strongest teams pair flexible hiring with boring discipline: compliance gates before payment enablement, reliable payouts before recurring volume, and reconciliation before expansion. That is how you capture freelancer speed without letting hidden ops work erase the gain. Keep your next step narrow and concrete: run the market checklist on the next target corridor, gather production evidence, and only then decide whether that market deserves headcount, launch budget, and leadership attention.

Frequently Asked Questions

What are the top business benefits of hiring freelancers?

The practical upside is access to specialized skills, flexible capacity when demand moves around, and potential access to new markets. That can help you test a market or ship a time-bound project without building a permanent team. The catch is that the upside holds only if contracts, onboarding, and payouts are tight enough that ops work does not eat the gain.

Is hiring freelancers actually cheaper for businesses?

Sometimes, but you should price the full operating cost, not just the rate card. Include sourcing time, review cycles, rework, compliance handling, and payment operations before you call it a saving. If lower rates lead to missed acceptance criteria or repeated payout exceptions, the cheaper option stops being cheaper very quickly.

When do freelancers outperform full-time hiring?

They can be a strong fit when the work is specialized, time-bound, or uneven across product phases or countries. They can also help when you need to enter a market quickly without hiring a permanent local team first. If continuity, deep product context, or long-term ownership matters more than speed, full-time or a hybrid model is usually safer.

What are the biggest risks and how do you mitigate them?

The main risks are inconsistent quality, missed deadlines, misclassification, and payout or compliance failures. In the US, misclassification matters because a worker in an employment relationship is entitled to Fair Labor Standards Act wage and overtime protections. Mitigate with a clear service-level agreement, contract scope and acceptance criteria, gated onboarding, and a reconciliation check that confirms the payout status and the ledger entry match.

What should teams check before cross-border freelancer payouts?

Start with whether the target corridor is supported and whether you can see payout states clearly enough to investigate failures. Then confirm applicable due-diligence and AML controls, including beneficial-owner verification where required. Make sure tax documents are collected before payment is enabled: IRS guidance says Form W-9 is the first step for US independent-contractor onboarding, while Form W-8 BEN is submitted by foreign payees when requested by the payer or withholding agent. If a market requires manual chasing of documents or weak status visibility, do not scale recurring Payout Batches there yet.

How should operators prioritize countries for freelancer-led expansion?

Put the next country behind proven production evidence, not just commercial demand. Start where payout rails, compliance coverage, and reconciliation are already working with real freelancers, real exception handling, and finance sign-off. A good checkpoint is simple: if you cannot trace onboarding status, payout outcome, and final Ledger Journals for the corridor, that market is not first.

Can one platform reduce operational overhead across markets?

It can, if it centralizes onboarding controls, Payout Batches, and audit-ready Ledger Journals in one place. The value is not the single login. It is the ability to verify who was onboarded, which tax form is on file, what failed, and what finance should reconcile, especially when 1099-NEC filing has a January 31 deadline in the US.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ato.gov.au/businesses-and-organisations/hiring-and-payi...trusted

- copyright.gov/title17/chapter2.pdftrusted

- dol.gov/agencies/whd/flsa/misclassificationtrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- europa.eu/youreurope/business/taxation/vat/check-vat-n...trusted

- hbs.edu/managing-the-future-of-work/podcast/Pages/po...trusted

- irs.gov/businesses/small-businesses-self-employed/fo...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Pay US-Based Freelancers from the UK

Your ability to attract and keep strong US freelance talent depends less on budget than on how you operate. Strong freelancers often work like serious one-person businesses, and they start evaluating you from the first interaction. Compliance and payment handling are not back-office details. They are early proof that you will be easy to work with, careful with details, and worth prioritizing.

How to Pay US-Based Contractors from Australia

Engaging U.S. talent can be a smart growth move for an Australian business. But paying a cross-border contractor is not just an admin task. If you handle it reactively, you create compliance risk, unnecessary cost, and record gaps that are hard to repair later.

How to Switch PEO Providers

You can switch a Professional Employer Organization cleanly if you treat it as a contract exit and an operating handoff, not a simple vendor swap. To reduce payroll surprises, review your current agreement first, choose a timing window you can actually support, and verify key handoffs before the first live payroll.