Quick Answer

Start by choosing for payment reliability, then use yield and promos as tie-breakers. The strongest setup is role-based: a primary operating account, a reserve buffer, and a specialist second path when needed. Bluevine Business Checking is positioned for digital-first operations, Wise Business is positioned for international flows with rail-specific pricing checks, and Chase Business Complete is treated as a branch-access option that requires direct term verification. The practical winner is the one that closes cleanly at month-end and holds up under your real payment mix.

Stop choosing by APY alone#

APY can break a tie. It should not drive your shortlist. If you are comparing the best business bank accounts for freelancers, start with the setup that keeps money moving, records clean, and month-end work manageable.

A dedicated business account does more than separate business and personal activity on paper. For freelancers, it makes day-to-day tracking simpler, keeps owner draws easier to spot, and turns end-of-month cleanup into a review task instead of a reconstruction project. That matters even more when income lands from several clients on different schedules and through different payment methods.

There is no single winning account type. Traditional and digital options can both work, but only when they match how you actually get paid, how often you move money, whether you handle cash, and whether cross-border payments are part of the job. Those details decide fit long before a headline yield does.

| Decision lens | What to check | Why it matters |

|---|---|---|

| Payment rails and limits | Verify how clients pay you and review transfer limits before opening. | A limit mismatch can constrain routine invoicing volume. |

| Verification readiness | Prepare common onboarding documents: EIN, DBA, ID, and proof of business registration. | These documents are commonly required during account opening. |

| Yield in context | Compare APY only after operations and limits fit your process. | Offers like 1.50% APY up to $250,000 help only when money movement already works. |

That order matters in practice. Choosing the highest headline yield first sounds sensible until you find that your main payment rail is awkward, capped, or harder to reconcile than expected. If one client pays by ACH and another pays cross-border, the account has to support both patterns without turning routine payments into exceptions you have to explain later.

Use this rule throughout the piece: if two options are close on fees and APY, take the one with clearer payment handling and cleaner records. That choice usually pays you back in time, fewer surprises, and less friction when a client payment arrives late or differently than expected.

When your client mix changes, run this short implementation pass again before you switch:

- List your main payment methods and your typical invoice flow.

- Confirm your entity details and document pack before applying.

- Stress-test transfer limits against your busiest expected payout week.

- Confirm accounting integration fit before funding the account.

Who this list is for and how accounts are scored#

This list is for self-employed freelancers working across multiple clients who want a clean separation between business and personal finances. It is written for people who want an account that holds up in real use, not just on a comparison page.

The best fit is usually less about marketing extras and more about operating reliability. You need account access that matches how you get paid, month-end records you can actually use, and dependable support when something goes wrong. In that context, support quality and access are operating requirements, not nice extras.

Promotions can help at the margin, but here they are secondary signals. A bonus can make a decent account more attractive. It cannot turn a poor fit into a good one, and it definitely cannot rescue an account that creates friction around payments, reconciliation, or getting help when something breaks.

| Score item | What we check | Concrete anchor |

|---|---|---|

| Service reliability and support | Whether customer support is dependable when questions or concerns come up. | Freelancer banking guidance treats reliable customer service as vital. |

| Ongoing cost discipline | Recurring monthly costs before promotional offers. | Example listing data shows Bluevine Business Checking with a displayed monthly fee of $0. |

| Yield in context | APY as one comparison input, not the only driver of rank. | Example listing data shows 1.30% APY on balances up to $250,000, with terms. |

| Access fit | Online usability plus ATM or branch reach based on your payment pattern. | ATM access is especially relevant when cash deposits are part of your routine. |

| Comparison hygiene | Whether rankings are broad and current enough to trust. | One review reports screening over 30 accounts, and major comparisons are timestamped to March 2026. |

The practical way to use this scorecard is to rank your non-negotiables before you compare products. If your work depends on dependable support, strong ATM access, or a predictable escalation path, those criteria should outrank a slightly better promo number. That keeps the final pick aligned with how your business actually runs instead of how the product page is framed.

APY can still break ties. This list just does not let APY or bonus size decide the ranking on their own. A shown $500 offer can be useful, but it does not replace reliable support, workable access, or manageable recurring cost. Related: The Best Multi-Currency Accounts for Digital Nomads and Freelancers.

Quick comparison table for fast shortlisting#

Use this table to narrow the field quickly, then verify live terms before you open anything. Only Wise Business has row-level pricing support confirmed here, so every other row should be treated as a candidate pending direct confirmation.

| Account | Best for | Pros | Cons | Concrete use case |

|---|---|---|---|---|

| Bluevine Business Checking | Freelancers building a shortlist before live verification | Included in this shortlist for side-by-side comparison | This does not confirm current fees, branch access, transfer limits, or invoicing details | Solo freelancer confirms limits and statement format before switching |

| Wise Business | International client payments and multi-currency inflows | Usage-based pricing with no subscription plan, sending fees can start from 0.57%, and discounts start after 25,000 USD monthly send volume | Receiving USD wire or Swift payments is listed at fixed 6.11 USD per payment; cost depends on payment method; bank vs Money Services Business (MSB) classification is not established here | Consultant paid in multiple currencies checks full receive and conversion cost before choosing rails |

| Relay Business Checking | Small teams adding candidates to a comparison shortlist | Included as a candidate in this article comparison set | This does not confirm current controls, integrations, in-person support limits, or fee mechanics | Small studio validates export and reconciliation behavior before opening |

| Chase Business Complete | Freelancers comparing additional account candidates | Included as a candidate in this comparison set | This does not confirm fee-waiver rules, check-handling details, or escalation outcomes | Freelancer confirms service path and monthly charges before opening |

| Axos Basic Business Checking | Freelancers adding another shortlist option | Included to broaden the comparison set | This does not confirm support quality, cash-handling fit, or current transfer constraints | Solo freelancer validates daily limits and exception handling before funding |

Treat every non-Wise row as a starting point, not a final answer. That habit avoids a common shortlisting mistake: the options look close until payment-method fees, transfer caps, or access gaps show up in real use.

A good way to run the comparison is to hold your invoice sample constant across every account. Use the same invoice size, the same payment rails, and the same expected monthly volume so you are comparing accounts, not changing assumptions. It also helps to record the live terms in one place as you go, because the useful differences are usually in the details you will forget a week later.

Before you choose, run this quick pass:

- Pull each provider fee page and record monthly fee, transfer limits, and receiving-fee lines.

- Price two sample invoices using your real rails, domestic and international if relevant.

- For Wise, test both local receiving assumptions and the fixed

6.11 USDUSD wire or Swift receive fee. - Open the regulator-standardized pricing document when available and compare it with marketing summaries.

- If two options are close, choose the one with clearer month-end records and a workable backup payment path.

With the shortlist in place, the next step is to match each candidate to the kind of work it handles best.

Bluevine Business Checking for digital-first US freelancers#

Bluevine belongs on the shortlist if your business is mostly paid through digital rails and you prefer to manage the account remotely. Bluevine describes itself as a financial technology company, so the appeal is less about branch access and more about whether a remote-first setup covers your day-to-day work cleanly.

For a freelancer who wants one primary operating account, the appeal is straightforward: invoicing and bill pay in one place, with headline terms that are easy to compare early in the search. That makes it a practical first candidate if your routine is already fully digital.

| Signal | What it means in practice | What to verify before opening |

|---|---|---|

Standard plan monthly fee at $0 | Low recurring account cost on paper. | Confirm the exact plan and any conditions tied to that pricing. |

1.30% APY up to $250,000 | Potential yield on operating balances. | Treat as conditional since terms apply and high-yield checking is described for eligible customers. |

Bonus shown at $500 | Possible upside if you already qualify. | Check eligibility requirements before weighting this in your decision. |

Up to $3 million FDIC access via Insured Cash Sweep | May matter if retained cash can exceed basic single-bank coverage limits. | Verify enrollment and disclosures so coverage expectations match your setup. |

If you are considering Bluevine, do not let the APY or bonus do all the work. The material behind this article does not establish faster support escalation for holds or returns, so support quality should stay in the unverified column until you test it yourself.

A sensible trial is to run your normal invoice cycle through the account for one full month before you fully commit. Watch how easy it is to reconcile deposits, identify fees, and close the month without manual corrections. Pay attention to what happens when something ordinary gets slightly messy, because that is where a good-looking account either proves itself or becomes extra admin.

Short version: keep Bluevine on the shortlist when you want a digital-first operating account with low baseline monthly cost and integrated payment tools. Re-compare if you need frequent in-person support or your trial month shows weak handling for delayed or returned payments.

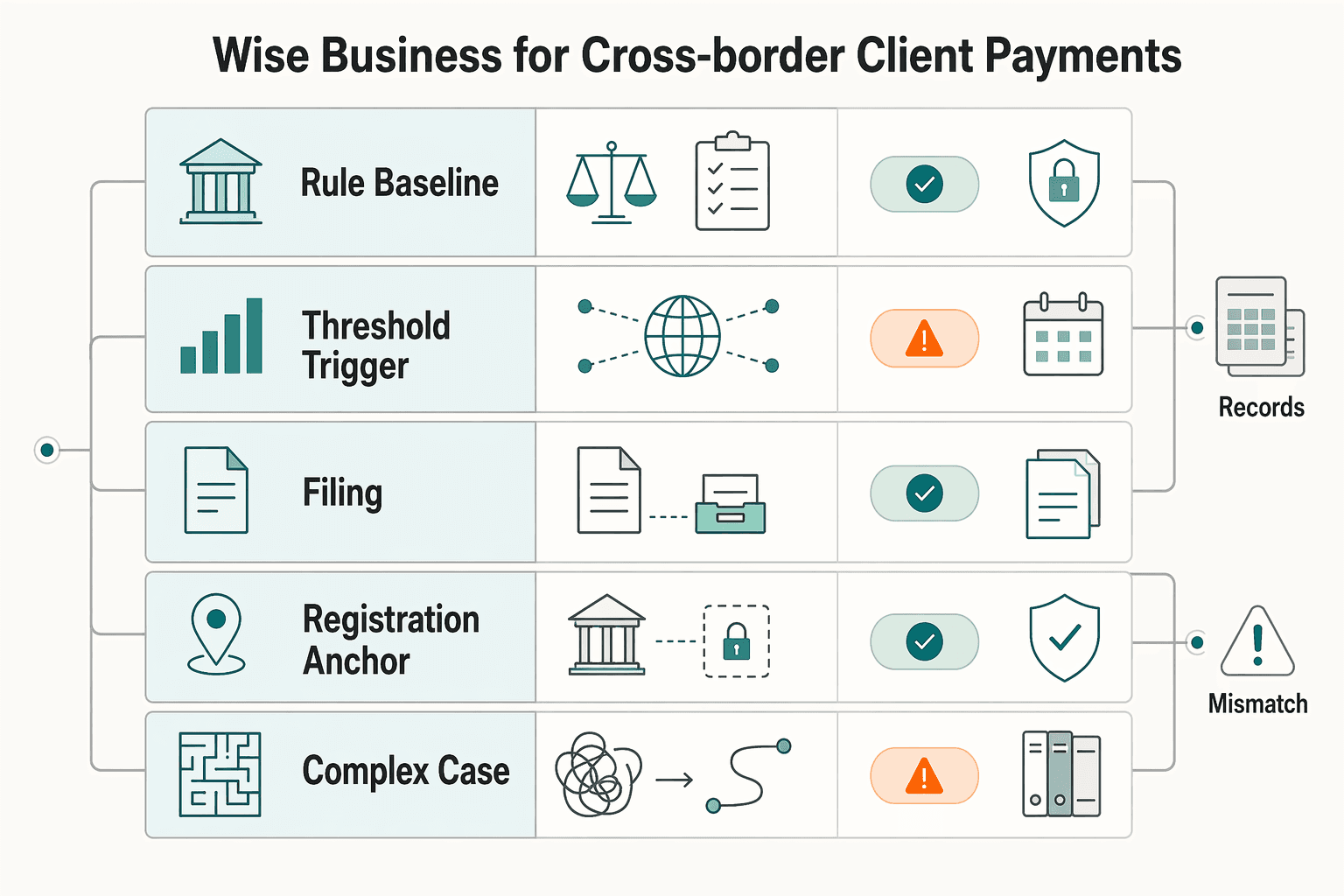

Wise Business for cross-border client payments#

When international invoices become core revenue, this stops being just a banking decision. With Wise Business, tax handling and account classification need to be clear before features start to matter, because the receiving rail, the invoicing setup, and the compliance burden all touch the same record trail.

Whether Wise Business should be treated as a Money Services Business (MSB) or as a bank in your jurisdiction is not established here. Not all Wise-specific product terms are confirmed here either. Treat classification, safeguarding details, and jurisdiction-specific terms as direct checks before you decide where it sits in your account structure, especially if you are considering it for a primary role.

| Cross-border checkpoint | What to verify | Why it changes the decision |

|---|---|---|

| Rule baseline date | EU cross-border B2C VAT rules changed on 1 July 2021. | Older assumptions can produce incorrect invoicing or filing logic. |

| Threshold trigger | Whether the EUR 10 000 EU-wide threshold is relevant to your activity profile. | This can change how VAT is handled across borders. |

| Filing load | OSS returns are quarterly for Union and non-Union schemes, monthly for import, and are additional to regular VAT returns. | This adds recurring compliance work rather than replacing existing returns. |

| Registration anchor | Your Member State of identification and registration path. | A clear anchor reduces admin sprawl. |

| Complex-case backstop | A VAT Cross-border Rulings path in a participating EU country where you are VAT-registered. | This provides an advance-ruling route for edge cases. |

The sequencing matters. If you compare account features before you lock down VAT ownership and filing cadence, you can end up optimizing the wrong thing. A slightly cheaper rail is not a win if it sits inside a setup you have not documented properly or cannot defend later when records need to line up.

Start with compliance clarity, then choose the rails and account role that support that decision. That keeps the banking choice tied to the way you invoice and file, instead of treating payments as a separate problem. In practice, that usually means deciding whether the account is your main international receive path, a specialist second path, or something you only use for certain corridors.

Use this check before making any cross-border account primary:

- Map revenue by jurisdiction and flag invoices that may fall into EU B2C scope.

- Assign ownership for OSS registration, filing cadence, and record-keeping.

- Define a contingency path for voluntary deregistration or exclusion from a scheme.

- Set a trigger for escalating complex VAT treatment through Cross-border Rulings.

- Compare account terms only after these controls are documented.

Use this checkpoint: if international receipts are core revenue, make the VAT pieces explicit before selecting any cross-border account. If classification or filing ownership is still unclear, resolve that first and then choose the account setup.

Relay Business Checking for envelope-style operations#

Relay is strongest when cash segmentation is the main operating problem you need to solve. If one combined balance keeps hiding what is already committed to taxes, payroll, or reserves, Relay can be more useful than an account that looks slightly better on APY but leaves you doing mental math every week.

Finder also lists Relay as its pick for multi-member LLCs, which may matter if ownership structure is part of your decision. Even then, the real question is simpler: does separating cash by purpose remove friction from your actual operating rhythm?

| Item | Brief description | Key differentiator |

|---|---|---|

| Cash segmentation | Relay describes support for up to 20 separate checking accounts. | You can map buckets by purpose instead of tracking committed vs available cash mentally. |

| Auto allocation | Relay describes percentage-based transfers when deposits arrive. | Funds can split into tax, profit, and operating buckets immediately, reducing manual reshuffling later. |

| Spend controls | Relay describes up to 50 virtual and physical cards with per-card limits and category restrictions. | Limits can be enforced at the point of purchase, not only after reconciliation. |

| Transaction fit | Business checking is positioned for deposits, bill payments, payroll, and debit card spend. | The account type lines up with day-to-day operating activity. |

The key caveat is the banking model. Relay states it is a financial technology company, not an FDIC-insured bank. It also states banking services are provided by Thread Bank, Member FDIC, and that pass-through deposit insurance coverage depends on specific conditions. Verify those conditions in current disclosures before making this your primary account.

In practice, Relay is most useful when one general-purpose account hides what is actually spendable. If that is already creating confusion around taxes, payroll, or committed balances, the segmentation itself can be more valuable than chasing a small yield difference somewhere else. It is less compelling if you already keep cash organized and do not need multiple buckets or card-level controls.

Practical takeaway: choose Relay Business Checking when account segmentation and card-level controls are the top need. Before you commit, validate the insurance-condition details and run a test deposit cycle to confirm the allocation rules behave the way you expect.

Chase Business Complete when physical branch support is non-negotiable#

Choose Chase for a concrete reason, usually branch access. Chase Business Complete makes sense when branch-dependent tasks are part of your normal month, not when they are just hypothetical edge cases you might need one day.

That is a fit decision before it is a fee decision. A branch-first setup can reduce friction for cash handling, paper checks, or in-person problem solving. If your business is mostly digital, those same branch advantages may sit unused while a digital-first account gives you a simpler daily setup and fewer moving parts.

Detailed Chase operating mechanics are not confirmed here, so branch and support assumptions should stay in the checkpoint column rather than the guarantee column. That is especially important if you are choosing Chase because you expect a stronger escalation path. Verify the actual tasks you care about, not the general reputation.

Use these checks before you commit:

- Confirm fee-waiver conditions against your real monthly balance and transaction behavior.

- Test branch-dependent tasks you actually use, such as check handling or cash deposit routines.

- Verify the payment and software tools you plan to rely on for your exact account setup.

Choose Chase when branch-dependent tasks are frequent and predictable. If they are only occasional, a digital-first primary account with branch access kept as a secondary path is usually the cleaner setup.

Found, Lili, and Novo for solo operator simplicity#

For solo operators, Found, Lili, and Novo are best treated as low-friction starters rather than guaranteed long-term homes. They can reduce admin load early, which is often the real win when the immediate problem is separating business activity, staying organized for tax time, and keeping routine cash management simple.

This group is especially relevant if you are a first-year 1099 freelancer moving from personal to business banking and still formalizing your tax organization and routine cash management. In that stage, ease of use can be more valuable than feature breadth, as long as you are honest about where the limits might show up later.

| Name | Brief description | Key differentiator |

|---|---|---|

Found | Positioned for solo founders and freelancers, with auto tax set-asides, real-time tax estimates, and Schedule C tools in a September 2025 snapshot. | Strong fit for early tax organization. |

Lili | Listed as an online small-business option in a 2026 comparison. | Keep it on the shortlist, then verify current terms directly. |

Novo | Listed with no monthly fee and strong integrations in a September 2025 snapshot, and no interest payout in that same snapshot. | Useful for a simple operating account with software connectivity, not as a yield-focused choice. |

The point of this tier is simplicity. If the main problem you are solving is basic separation, routine bookkeeping, and getting tax set-asides under control, these accounts can be practical. They are often easier to say yes to because the setup feels lightweight and day-to-day use feels obvious.

The common failure mode is outgrowing them quietly. An account that feels perfect at low volume can become awkward once wires, transaction caps, or cash-access needs start to matter. That is why price and limits deserve direct attention before you open the account, not six months later when changing accounts is more annoying.

A common benchmark range is $0-$30 monthly maintenance, $0.25-$0.50 per transaction after free limits, and $10-$50 per wire, and some accounts also cap transactions. Digital-first options may skip many routine fees, but cash access and branch support tradeoffs are common. Use those numbers as a reality check, not as a reason to stop at the first low-fee option that looks simple.

Run this quick pass before deciding:

- Estimate monthly deposits, withdrawals, and transfers from recent activity.

- Compare expected wires and transaction volume with posted fee and cap rules.

- Confirm cash-access expectations if you may need cash deposits.

- Re-check fit if you later need broader controls or more advanced operations.

Bottom line: choose Found, Lili, or Novo when low day-to-day overhead is the priority. When complexity grows, add a second account instead of forcing one lightweight option to do every job.

American Express, NBKC, and Axos as situational alternatives#

Keep this group in the tie-breaker tier, not the default first pass. American Express, NBKC, and Axos are most useful when your top option is close but misses one requirement that actually matters to how you operate.

These are still serious alternatives. One online-business-accounts roundup says it evaluated 19 options, and another publishes a 12-account list with a stated methodology and a Sep 24, 2025 update date. That is enough to keep them in the conversation. It is not enough to assume any one of them is the universal answer without a direct terms check.

| Account | Brief description | Key differentiator |

|---|---|---|

American Express | Included in a published business-checking roundup as a secondary candidate. | Tagged there as best for member rewards, useful when rewards value is your tie-breaker. |

NBKC | Included in the same roundup as an alternative. | Tagged there as best for add-on services, useful when bundled extras are your deciding factor. |

Axos | Included in the roundup as an alternative. | Tagged there as best for cash deposits, useful if regular cash handling is part of your routine. |

The tradeoff is comparison depth. These labels can point you in the right direction, but they do not tell you enough about operational constraints on their own, and different publishers use different scoring logic. That means you should treat them as focused checks, not broad endorsements.

Use this verification pass before keeping any of these in your final two:

- Define one mission-critical requirement in plain terms.

- Pull current terms and confirm that requirement is met without creating new fee friction.

- Pressure-test expected monthly activity against fee structure and transaction behavior, not marketing copy.

- Keep the option only if it clearly beats your top choice on that one requirement.

Keep American Express, NBKC, or Axos only if one clearly wins on a requirement that materially affects your operations. Otherwise, stay with the core shortlist and keep the decision simpler.

Red flags that create delays and hidden cost#

Most avoidable banking pain starts with setup discipline. The delays and hidden costs that hurt cashflow usually come from boring mistakes: choosing on headline offers, blending business and personal activity, or waiting until a payment path fails before lining up an alternative.

| Red flag | Where the cost shows up | Practical checkpoint |

|---|---|---|

| Choosing on headline offers instead of your real payment profile | Fees can look very different once you price your actual activity. In one non-resident comparison table, listed costs include $15-$50 monthly fees, $15-$30 wire fees, 0.41-2.85% FX fees, and $45 wire costs. | Model expected monthly wires, FX exposure, and transfer count before deciding. |

| Mixing personal and business funds (commingling) | Tracking profitability and expenses gets harder, and tax or compliance risk rises if personal spend is treated as a business deduction. | Use a dedicated business account. If mixing already happened, identify and reclassify transactions, then reimburse or document treatment correctly. |

| Waiting to evaluate alternatives until a payment path is disrupted | Replacement options may involve slower approval and different fee structures. One non-resident guide frames this tradeoff between traditional banks and neobanks or EMIs. | Pre-check at least one alternate account path and its current terms before you need to switch. |

Commingling is the one that tends to snowball. Once records are blended, profitability gets harder to track, expenses get murkier, and tax or compliance risk can rise. Every later reconciliation takes longer because you are no longer reviewing business activity; you are sorting a mixed timeline and guessing intent after the fact. The fix is simple and unglamorous: use a separate business account, then clean up any mixed activity before it spreads across more months.

A backup path matters for the same reason. If you wait until a payment rail is disrupted, you lose the ability to compare calmly and may end up accepting slower approval or worse terms just to keep cash moving. That is exactly when a small amount of advance work saves the most stress.

Working rule: if a change does not improve payment continuity or record clarity, do not adopt it. For a deeper baseline on account separation, see Separating Business and Personal Finances: An Important Step for LLCs.

The 14-day setup checklist after you choose an account#

Once you choose an account, use the next two weeks to prove it works under real conditions. The goal is not just to open it. The goal is to confirm that your payment flow, accounting, and fallback path all hold up before volume grows and before you start relying on assumptions that have never been tested.

- Day 1-3: open and map to your entity records. Open your primary account, map it to your legal and tax entity details, and keep identity information consistent across invoicing and banking profiles. Set accepted invoice payment methods so clients use trackable rails by default, and save the onboarding confirmations somewhere you can find them later.

- Day 4-6: connect accounting and test one full cycle. Connect your accounting stack, create categories for transfer fees, FX costs, and owner draws, then run one invoice-to-settlement test. Confirm each line item posts to the right category and that the exported statement is usable without cleanup you would not want to repeat every month.

- Day 7-10: set reserves and activate a fallback path. Define your tax and dispute reserve policy and keep a second transfer path active across two providers. If

Wise Businessis in your mix, test both domestic non-Swift/non-wire receiving and wire/Swift receiving, since wire/Swift routes can carry fixed per-payment fees, for example6.11 USDfor USD wire or Swift receiving. - Day 11-14: run a dry close and document escalation. Run a mock month-end close from exported statements and accounting entries, verify balances tie out, and log unresolved items. Save support escalation contacts and keep a fee-evidence record that includes the regulator-standardized pricing view so you can compare what you were told with what you are charged.

- Monthly checkpoint: re-validate pricing before it becomes a cashflow issue. Recheck fee changes and reconciliation exceptions. For Wise, monitor when monthly send volume crosses

25,000 USD; discounts apply for the rest of that month and reset on the first.

This sequence works because each step creates evidence for the next one. By day 14, you should know whether the account can handle your preferred rails, whether transactions categorize cleanly, whether your reserve logic is actually usable, and whether the current fee disclosures match what you expected. That is a much better baseline than assuming an account is production-ready because onboarding was easy.

Do not treat the account as fully live unless this checklist produces clean records, predictable settlement behavior, and a tested fallback path. A smooth signup is nice. A boring month-end close is better.

For the entity-setup side of the decision, read Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

Before you lock in your primary and backup rail, run your likely transfer paths through this payment fee comparison tool.

Pick the account that protects your cashflow#

The right account is the one that keeps cashflow steady when client behavior changes, not the one that looks best on a comparison page. Once you have a shortlist, assign each account a clear job and test whether that job still makes sense when payment methods, client mix, or volume shift. That is the thread running through this whole piece: choose for reliability first, then let fees and APY settle the close calls.

- Operating account

Use a primary account for incoming payments, bill pay, and monthly reconciliation. The benefit is simple: cleaner records for bookkeeping and tax planning, plus business statements you may need if you apply for financing. The best operating account is usually the one that makes routine deposits, outgoing payments, and month-end review feel boring. Key differentiator: clear day-to-day visibility on earnings and expenses.

- Reserve account

Keep reserves separate from spending money so delayed client payments are easier to absorb. A business cash management setup can pair an operating account with a reserve account and make internal transfers easier. Some reserve tools may earn a higher APY, but yield should still stay secondary to access and control because reserve money is only useful if you can reach it when the business actually needs it. Key differentiator: buffer discipline without mixing routine spend and contingency funds.

- Specialist second path

Choose this based on your main constraint. For cross-border flows, Wise Business highlights holding 40+ currencies, local account details in 10 currencies, and payouts to 160+ countries, with no monthly fees and no minimum balance, but it also states a key limitation: no cash deposits. If branch access and cash handling matter more, Chase Business Complete is listed at $15 monthly, waivable, and is the better branch-oriented comparison once you verify current terms. Confirm whether Wise Business should be treated as a bank or an MSB in your jurisdiction before deciding how heavily to rely on it. Key differentiator: international digital rails versus in-person branch access and deposit convenience.

Before you treat any setup as stable, run a monthly checkpoint: re-verify current terms, confirm that your payment mix still fits the account's capabilities, and save the latest disclosures. At least one comparison source explicitly warns that some card information may be outdated, so roundup tables should stay a starting point, not your final source of truth.

If Gruv modules are available in your environment, use them for traceability, policy gates, and reconciliation-ready records across collections and payouts. If not, keep the same control discipline with exported statements and a documented review cadence. The tool matters less than the habit of checking that cash movement, fee evidence, and record quality still line up.

Use the final decision rule as a recurring check, not a one-time call. Keep one-account simplicity only when it covers your real constraints under normal volume and changing payment patterns. Add a second path when a known gap remains, such as cash deposit limits or cross-border requirements.

If you need dedicated bank-transfer receiving details with status visibility for cross-border client payments, explore Gruv Virtual Accounts where enabled.

Frequently Asked Questions

What is the best business bank account for freelancers overall?

There is no single best option for everyone. Choose based on payment mix, cross-border needs, and whether pricing is clear before you transact. Opening a dedicated business account is also an important step in separating business and personal finances.

Is `Wise Business` a bank or an `MSB`, and why does that matter?

This grounding set does not confirm a definitive legal label for Wise Business. Treat legal status as a jurisdiction check before making it your primary account. Classification affects which terms and disclosures you should rely on.

Which account is best if most of my clients are international?

Prioritize providers that show rail-by-rail pricing clearly. Wise states it uses the mid-market rate with an upfront fee, and it also lists fixed receive fees for some rails, including 6.11 USD for USD wire or Swift, 2.16 GBP for GBP Swift, and 2.39 EUR for EUR Swift. Model your actual corridors and monthly volume before deciding.

Should I prioritize low fees, APY, or payment reliability first?

Start with payment routes and total operating cost, then use APY as a secondary filter. APY terms can be conditional, so check eligibility details before relying on headline yield numbers.

Do I need a separate business account if I am a `Sole Proprietorship`?

Generally, yes. A dedicated business account helps keep business and personal finances separate, and that separation is explicitly recommended in freelancer banking guidance.

When should I choose `Chase Business Complete` over a digital-first option like `Bluevine Business Checking`?

Use this comparison as a terms check, not a default winner. Bluevine is shown with a $0 monthly fee and a conditional 1.30% APY up to $250,000, while detailed Chase operating terms are not provided here. If you are considering Chase, verify current terms directly before deciding.

Can I run one account only, or should I keep a backup rail?

One account may work if your end-to-end flow is tested and stable. A backup rail can reduce disruption if costs or payment methods change. If Wise is in your setup, remember its monthly volume discount threshold, 25,000 USD, resets on the first of each month.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

The Best Multi-Currency Accounts for Digital Nomads and Freelancers

This shortlist is for cash flow decisions, not brand popularity. It is for freelancers, creators, and lean teams in the United States who need a cross-border payment setup that still works when real work hits: invoices go out, money lands, conversions happen on your timing, and urgent payouts do not depend on luck.