Quick Answer

Choose based on corridor reality first: for african gig platform payments mpesa chipper decisions, a Kenya-only domestic launch can stay single-rail, while mixed routes like UK to Nigeria plus Kenya domestic usually justify dual rails earlier. Commit only after a corridor test matrix confirms destination method, settlement expectations, and escalation ownership. Before launch, make retries safe with idempotency and make callback processing verifiable so exceptions do not become duplicate disbursements or reconciliation drag.

How to choose between M-Pesa, Chipper, and local rails#

If you are choosing between M-Pesa, Chipper Cash, and local rails, start with corridor execution, not brand popularity. This list is meant to help you choose the setup you can actually verify by country, payout type, and operating workflow before launch.

It is written for founders, payments ops, finance, and engineering teams planning contractor and creator payouts in markets such as Nigeria, Ghana, Kenya, Uganda, Tanzania, and Rwanda, where coverage can change market by market. Treat each corridor as its own decision. A domestic Kenya flow can differ from a cross-border payout into Ghana or Nigeria.

To keep the decision practical, use three filters, in order.

- Corridor fit

Confirm where money moves first. A TechCrunch profile (December 16, 2019) described Chipper Cash as an African cross-border fintech and listed P2P availability in 6 countries: Ghana, Uganda, Nigeria, Tanzania, Rwanda, and Kenya. Use that as context, not proof of current 2026 coverage for your exact payout flow.

- Execution reliability

Check whether the rail gives your team predictable operations and usable exception handling. Before committing, require a corridor matrix for each launch market with payout method, settlement expectation, and escalation path. Blank cells mean unresolved launch risk.

- Control as you scale

Expansion across African markets involves regulatory fragmentation and low-infrastructure realities. MIT research emphasizes adapting to local constraints rather than exporting one model unchanged, which is why multi-country rollout decisions should be validated corridor by corridor.

Where public information is strong, this list uses it. Where scope or implementation detail is unclear, it flags verification checkpoints instead of guessing. Forbes (June 6, 2022) reported Chipper Cash at 5 million users and framed transnational financial services against a market of 1.2 billion people. But scale alone does not answer the operating questions that matter most. Can you pay the right recipient in the right corridor, what evidence comes back, and what happens when a payout gets stuck?

Related reading: Building a Virtual Assistant Platform Around Payments Compliance and Payout Design.

How this list is scored and who should use it#

Use this list if you run repeat payouts and need predictable operations. Score corridor reality and operational readiness before headline growth claims. That keeps comparisons grounded in what your team can actually run.

| Criterion | What to verify | If unclear |

|---|---|---|

| Corridor fit | Exact launch corridors; regulatory framework, licensing framework, and permissible activities | Do not treat the route as launch-ready |

| Payout method coverage | Recipient reach across the payout methods available in each corridor | Do not assume one payout method will fit all recipients or finance workflows |

| Integration depth | Behavior verifiable in docs or testing | Treat unclear status handling or exception flows as operational risk and expected manual exception work |

| Operator control | Duplicate-prevention and reconciliation controls you can verify | Treat unclear ownership for payout operations and finance reconciliation as operating uncertainty |

- Corridor fit

Score each option by the exact corridors you plan to launch, not continent-wide narratives. Fintech conditions are not uniform across countries, so domestic and cross-border corridors should be treated as separate operating decisions. For each target corridor, document the provider's regulatory framework, licensing framework, and permissible activities before you treat the route as launch-ready.

- Payout method coverage

Score for recipient reach across the payout methods available in each corridor. With digital usage still partial, do not assume one payout method will fit all recipients or finance workflows.

- Integration depth

Score integration behavior only where it is verifiable in docs or testing. If key status handling or exception flows are unclear, treat that as operational risk and expected manual exception work.

- Operator control

Score duplicate-prevention and reconciliation controls based on what you can verify. If ownership for payout operations and finance reconciliation is unclear, treat that as operating uncertainty before launch.

For a step-by-step walkthrough, see How MoR Platforms Split Payments Between Platform and Contractor.

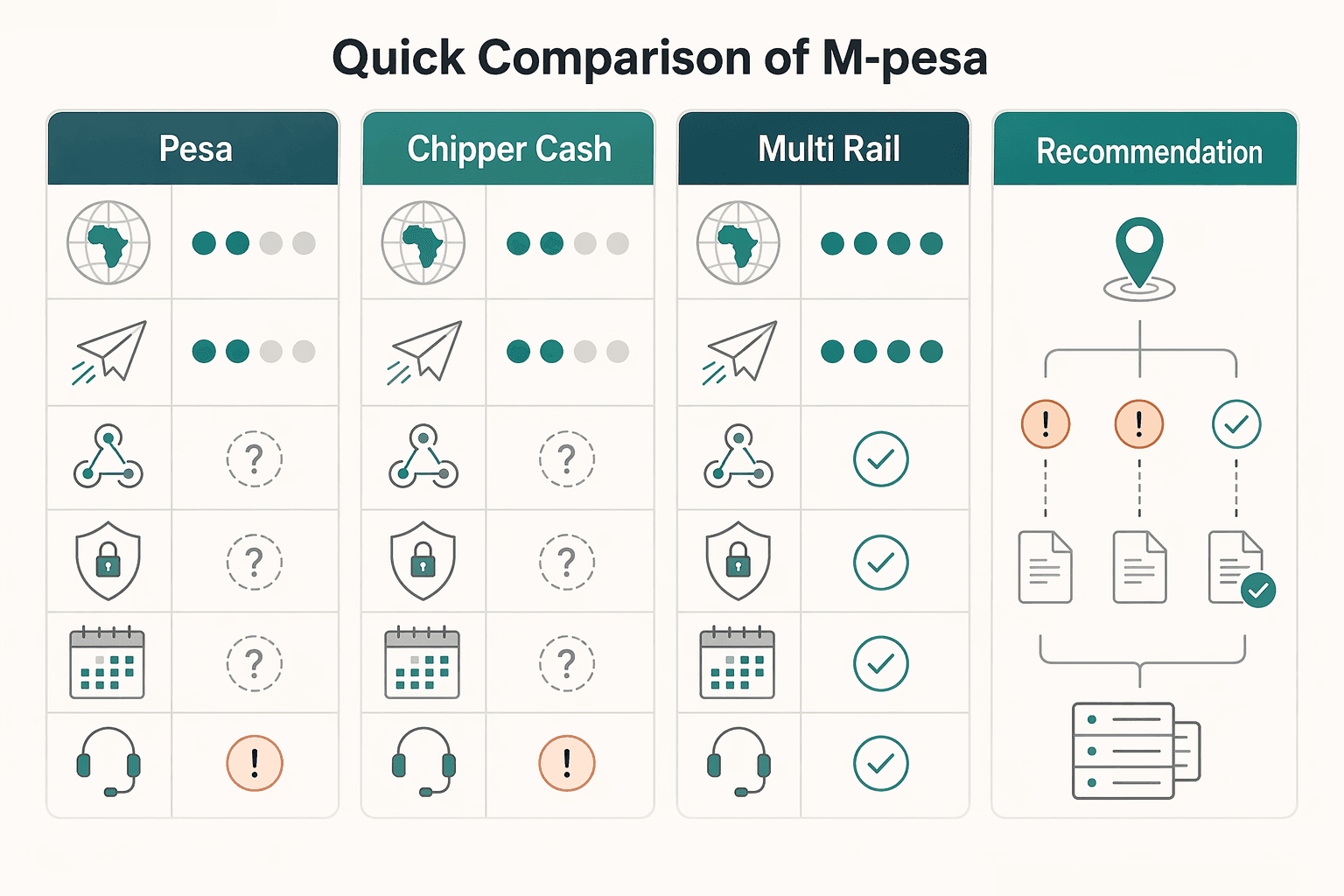

Quick comparison of M-Pesa, Chipper Cash, and multi-rail orchestration#

Use this section as a working map, not a feature race. Based on the available evidence, payout types, corridor depth, webhook behavior, idempotency behavior, SLA transparency, and escalation quality remain unverified for M-Pesa and Chipper Cash. That means your launch decision is mostly about how much unknown risk you are willing to accept.

| Option | Best for | Supported payout types | Cross-border depth | Integration complexity | Control surface | Verification burden | Known vs unknown |

|---|---|---|---|---|---|---|---|

| M-Pesa | Narrow launch scope (one corridor, one payout pattern) | Known: confirm exact payout types with the provider. Unknown: recipient and payout variants in your target route | Known: not established here. Unknown: domestic vs broader corridor coverage | Can be narrower in scope, but actual effort is unknown until first-party review and testing | Known: not established here for webhooks/retries/idempotency. Unknown: practical control behavior in production | High, because surfaced material includes a Scribd overview page for Engineering in Kenya Issue 011 (February 2023, 35 pages) with AI-enhanced metadata | Known: surfaced Scribd material is not authoritative operator documentation. Unknown: SLA transparency, corridor-level payout success, escalation path |

| Chipper Cash | Teams testing one provider first while accepting evidence gaps | Known: confirm exact payout types with the provider. Unknown: mobile money vs bank support by corridor | Known: not established here. Unknown: usable depth by country pair and recipient type | May look lighter than orchestration at first, but real effort is unknown until doc review and sandbox tests | Known: not established here for payout API callback depth or idempotent retry behavior | High, because surfaced material includes a general tech-news feed rather than implementation docs | Known: Wokpa feed is broad tech coverage; one entry provides a timestamp (Sat, 25 Jan 2025 14:43:24 +0000). Unknown: SLA transparency, corridor-level payout success, escalation path |

| Multi-rail orchestration with local payment rails | Expansion planning across multiple countries where you want one internal payout model | Depends on what each contracted rail supports, normalized in your internal layer | Depends on connected providers, not orchestration alone | Highest upfront build and ops design effort | You can define internal webhook handling and idempotency-key rules in your own system, but provider behavior still requires verification | Highest initial setup burden, then ongoing corridor-by-corridor verification | Known: internal control design is in your scope. Unknown: underlying rail SLA quality, corridor success, escalation reliability until verified |

| Recommendation | Use scope to decide complexity | If you truly need one corridor and one payout type first, start simple | If multi-country rollout is near-term, design orchestration readiness early | Single-rail can ship with less surface area; orchestration adds upfront work | Internal controls matter more as countries and payout types increase | Verification remains required in either path | Known: this row is operating judgment, not evidence of comparative success rates. Unknown: best fit until you run a corridor test matrix |

The table gives the high-level tradeoff. The next question is what you should do with it in practice.

- M-Pesa

Choose this path when launch scope is intentionally narrow and you want fewer moving parts to validate first. Collect first-party integration docs, explicit escalation contacts, and run corridor tests before go-live.

- Chipper Cash

Choose this when you want to test one provider first but can tolerate unknowns during validation. The surfaced public material here is a general tech-news feed, which can support a known/unknown log but not payout capability proof. Require corridor-by-corridor confirmation, status lifecycle examples, retry semantics, and escalation handling before relying on it operationally.

- Multi-rail orchestration with local payment rails

Choose this when expansion is expected and you want your own internal payout state model from the start. The advantage is architectural control in your system. The tradeoff is heavier initial implementation and operations design. Keep corridor evidence requirements explicit from day one so orchestration does not mask unresolved provider unknowns.

- Practical recommendation

If your immediate need is one corridor and one payout type, start narrower and verify thoroughly. If your roadmap already includes multiple countries, design for orchestration readiness early, even if you activate only one rail first.

The common failure mode is treating secondary material as production proof. Keep any launch-critical capability in the "unknown" bucket until you have first-party documentation, test evidence, and a real escalation route.

Best for mobile-money-first domestic payouts with M-Pesa#

M-Pesa can make sense when your first phase is domestic payouts in a mobile-money-first market and you are deliberately choosing launch simplicity over feature breadth.

- Best fit: narrow domestic scope

Use this path when you are not trying to solve multiple corridors at once. EY describes M-PESA as an established fintech solution with impact across Africa for over 20 years, and reports double-digit growth in 2024 registered mobile-money wallets to around 1.1 billion accounts in Sub-Saharan Africa. That supports the logic for wallet-first domestic payouts, but it does not prove your exact route.

- Why it may simplify your first release

For marketplaces sending many small domestic payouts, wallet-first flows may be simpler for recipients than bank-detail-heavy flows. In phase one, familiarity with a known payment method may matter more than broad payout-option coverage when your goal is first successful disbursements with fewer moving parts.

- What remains unknown

Confirm current 2026 corridor-by-corridor coverage, cross-border transfer support, payout success rates, SLA commitments, and marketplace-grade Payout APIs behavior for M-Pesa directly with the provider. Webhook depth, idempotency, and retry semantics should also be verified before launch. If your roadmap includes near-term regional expansion or early Bank rails, treat that as an explicit risk to validate, not an assumption.

- Practical use case

An early-stage local services marketplace launching in Kenya with a strict domestic-payout phase could start with M-Pesa first, then add rails later if validation supports it.

- Pre-launch checks

Before you commit, require:

- First-party docs for payout creation, status updates, reversals, and failure codes

- Sandbox or pilot evidence for duplicate-submission handling

- Named escalation contacts and a written incident path for stuck payouts

- Clear payout record requirements for finance (provider reference, internal reference, status history)

Best for cross-border payout corridors with Chipper Cash#

If you are solving cross-border payouts rather than single-country disbursements, Chipper Cash is worth evaluating, but only corridor by corridor.

- Best fit: cross-border need, not domestic optimization first

Use this path when funds need to move across markets, not just within one country. In this context, remittances are only part of the cross-border picture, which also includes trade and intra-African flows, and execution is often fragmented and costly.

- Why it can make an early shortlist

Chipper appears in public discussion around cross-border movement of funds, so it can be reasonable to shortlist for investigation when your use case spans multiple markets. Treat assumptions about launch speed, day-one customization depth, and route coverage as unconfirmed until you test them directly.

- Where evidence is limited

The source set here is mostly leadership commentary and market narrative, not operator-grade integration documentation. It does not verify current corridor coverage, destination-method coverage by corridor, or API, webhook, idempotency, and SLA behavior. Treat those points as unconfirmed until you test them directly.

- Tradeoff to price in before committing

The potential upside may be cross-border focus, but the verification burden is higher. Reporting notes a $150 million Series C extension in 2021 at a $2 billion valuation, followed by a reported 70 percent valuation cut, three layoff rounds, and a pullback from aggressive expansion. Treat that as a signal to validate operational stability and support quality in your exact routes.

- Commit only after a corridor test matrix and escalation path

Before relying on Chipper as your only rail, require a written matrix for each planned corridor and a clear escalation path for stuck payouts. Include sender and recipient route details, recipient type, destination method, onboarding requirements, payout states, failure handling, reversals, and reference fields. Then run live end-to-end tests and failure drills before go-live.

Best for scale control with Gruv plus local payment rails#

Choose this path when multi-country payouts are creating operational exceptions and you need tighter control, not maximum simplicity. Once you move beyond a one-country launch into multiple markets with different recipient preferences, a Gruv-plus-local-rail model can fit. It works only if engineering and finance are ready to own the extra implementation and ops load.

Best fit#

This starts to make sense when single-provider simplicity is no longer enough. The clearest signal is rising exception complexity: different payout methods by market, more failure states, and more pressure on reconciliation and release controls.

The value is control. You can run one internal control layer while routing execution across different rails, but that only works with disciplined ownership across product, engineering, and finance ops.

Why this can win at multi-country scale#

The clearest concrete signal in the available evidence is the "single integration" model and the +400 payment-method claim. That evidence comes from SourceForge related-product marketing copy, so treat it as directional, not operator-grade proof.

A second useful signal is routing neutrality versus PSP routing incentives. In practice, that matters when your payout mix spans different rails and the best path changes by market, recipient type, or failure state.

At this stage, controllability usually matters more than headline transfer fees. Failures, retries, and month-end reconciliation are where the architecture either helps or hurts.

What to verify before committing#

Because evidence is limited, require direct proof in your own flow before committing. Do not infer capabilities from broad product pages alone.

- A provider and payout-method matrix per target market

- Event payload samples and reference fields from payout request to provider result

- Retry and failure behavior for timeouts, duplicates, reversals, and delayed confirmations

- A reconciliation export finance can tie to internal records without manual matching

If you cannot trace request, provider outcome, and event history cleanly, the pain will show up in close and audit workflows first.

The main cost of this choice#

The tradeoff is higher implementation overhead for more control. Engineering must own provider abstraction, webhook intake, retries, and state normalization, while finance or payments ops must own exceptions, approvals, and reconciled exports.

There is also a reliability caveat. The excerpt claims orchestration can reduce single-point-of-failure risk through redundancy. Do not assume failover behavior in your exact payout paths until you test it with live scenarios.

When one rail is enough and when to combine two#

Start with one rail when payouts are concentrated in one country and one method. Add a second rail when corridor coverage and failure handling become operational risk, not edge cases.

| Model | Use when | What the section says |

|---|---|---|

| One rail | Payouts are concentrated in one country and one method | A fast path with lower operating overhead; keep scope tight and verify payout method support, callback fields, settlement behavior, and the provider reference finance will use at close |

| Two rails | You already have two meaningful payout patterns, such as Kenya domestic mobile money and a UK-origin flow into destinations like Nigeria | Different operating conditions, not just different destination labels; validate corridor-by-corridor behavior before rollout |

| Orchestration | Product, engineering, and finance need one normalized event trail and one reconciliation surface across providers | Middleware for controllability and audit consistency; worth it when extra complexity starts paying for itself |

1. One rail for a focused domestic launch#

If most payouts are domestic in one market, use one rail first and get execution quality right. In Kenya, mobile money is already dominant: the Central Bank of Kenya reported 91.32 million registered mobile money accounts in February 2026. In that setup, M-Pesa or one proven local provider can be a fast path with lower operating overhead.

Keep scope tight. Safaricom states M-PESA exists across Vodacom countries as separate stand-alone services, not one uniform cross-border service. If you launch on M-Pesa in Kenya, treat that as Kenya coverage only. Before committing, verify payout method support, callback fields, settlement behavior, and the provider reference finance will use at close.

2. Two rails when you have two real payout shapes#

Move to two rails early when you already have two meaningful payout patterns, such as Kenya domestic mobile money and a UK-origin flow into destinations like Nigeria. Those are different operating conditions, not just different destination labels.

Public data supports that distinction: remittance costs vary by country and transfer method, and Nigeria appears among top UK remittance destinations in recent estimates. UK outbound remittances were estimated at £9.3bn in 2023, while fresh public bilateral splits remain limited. Plan by corridor and method, not broad regional assumptions.

Chipper's public footprint shows why this matters. It advertises direct sends to bank and mobile-money accounts across 21+ African countries, while its help center lists a smaller set of operating countries. It also notes some direct non-Chipper payouts can take up to 4 business days. Treat those as signals to validate corridor-by-corridor behavior before rollout.

3. Add the second rail before failures become structural#

Do not wait for a major incident to add redundancy. Resilience guidance is explicit about avoiding single points of failure, and payout systems can hit that limit when one provider slows or degrades.

Use an internal trigger, not a universal rule. For example, if failed or delayed payouts keep rising faster than your payout volume beyond a short spike, treat that as a signal to plan a second rail before opening new corridors. If timeouts, delayed confirmations, or corridor-specific rejects are compounding, you are likely scaling exceptions rather than scaling payouts.

4. Match the model to the problem#

Use a simple decision rule: single-rail for speed, dual-rail for resilience, orchestration for controllability and audit consistency. Payment orchestration is middleware that coordinates flows across methods, gateways, and institutions. It becomes worth it when product, engineering, and finance need one normalized event trail and one reconciliation surface across providers.

Trigger checklist for moving from one rail to two#

Finance and product should approve the move when most of these are true. This is the point where extra complexity starts paying for itself.

- You have at least two active payout shapes that differ by country or method.

- The current rail cannot prove support for each target corridor with test payouts, expected settlement windows, and clear provider reference fields.

- Failed or delayed payouts are creating recurring manual work for support or finance.

- You need a fallback path when the primary provider is unavailable, slow, or missing a payout method.

- Finance cannot reconcile provider reference, internal payout ID, and final status from one clean export without manual matching.

If this evidence pack is not ready, stay single-rail a bit longer. Moving too early adds overhead; moving too late usually shows up first as reconciliation debt and migration risk.

If your trigger checklist points to dual-rail complexity, use this payouts overview to map routing, statuses, and retry controls before rollout.

Integration order that avoids duplicate payouts and reconciliation debt#

Once you move beyond one rail, integration order matters more than provider count. Build the flow so one logical payout cannot be disbursed twice, and every provider update maps to one internal payout record and one ledger outcome.

If you only harden two controls before launch, make payout creation idempotent and make webhook handling verifiable and replayable. Those two controls help prevent duplicate disbursements and reconciliation drift.

1. Onboard the recipient before payout creation#

Start by creating one recipient record that product, compliance, and payments all use. Store the destination you intend to pay, the country, and the initial provider path.

Do not create payouts from last-step free-text destination input. That increases the risk of duplicate recipient profiles, inconsistent destination formats, and harder reconciliation.

2. Gate payout creation behind KYC/KYB readiness#

Treat KYC/KYB as a precondition, not cleanup after payout creation. For business recipients, include beneficial-owner verification where your policy requires it.

Operationally, no payout object should be created until the recipient is payout-eligible. Keep the compliance decision, timestamp, and evidence reference on the recipient record so ops can explain allow or block outcomes.

3. Create once, submit through Payout APIs, enforce idempotency on create and retry#

Create the internal payout record first with one immutable payout ID, linked recipient ID, amount, currency, corridor, and funding source. Use the same idempotency key for the same logical payout across create and retry paths so retries do not produce duplicate disbursements.

Confirm idempotency behavior per provider before standardizing retry logic, because support is API-specific. If a provider does not support idempotent create behavior, block duplicate submissions by internal payout ID and retry status checks instead of re-creating payouts.

Use provider Payout APIs as execution interfaces, not your system of record. Your internal payout record should remain the source of truth.

4. Process webhooks defensively and make replay routine#

Webhook events should update state, not create truth from scratch. Verify signatures against the unmodified raw request body; payload mutation can break verification.

Design for late and duplicate events. Keep failed event handling in a dead-letter queue, and give ops replay tooling keyed by provider event ID and internal payout ID. Retry windows and mechanics vary by provider, and some providers can automatically resend undelivered events for up to three days.

5. Confirm in the ledger with one internal state model#

Use one internal state model across rails for operations and finance, even if provider labels differ. This is an internal operating model, not a universal provider schema. One workable example:

| Internal state | Ops action and owner | Customer message |

|---|---|---|

| pending | Payout created internally; not yet submitted | Your payout is queued |

| processing | Provider accepted submission; monitor callbacks/status | Your payout is being processed |

| paid | Confirm settled outcome for reporting | Your payout was sent |

| failed | Review failure reason, correct issue, retry safely | Your payout failed and needs attention |

| reversed | Investigate reversal and ledger impact | Your payout was reversed and is under review |

| investigation | Manual review when records are inconsistent or unclear | Your payout is being reviewed |

Keep reconciliation exports deterministic so finance gets the same schema each run: internal payout ID, recipient ID, provider, provider reference, amount, currency, created time, latest state, and event timestamps.

Set a go-live gate as an internal release rule: pass end-to-end tests in your initial corridors before opening additional corridors. Include both happy-path and exception-path coverage from onboarding through ledger confirmation.

Compliance and evidence pack before first live payout#

Treat the evidence pack as a hard go-live gate. If you cannot show recipient eligibility, approver history, provider outcome, and ledger linkage for each payout, do not launch.

| Component | Keep on file |

|---|---|

| Minimum policy pack | KYC policy; KYB policy (where applicable); sanctions/AML operating notes; payout approval matrix; named escalation contacts |

| Corridor readiness sheet per market | Provider; supported payout type; escalation route for failures; expected settlement behavior; callback method; last successful end-to-end test date |

| Finance retention bundle per payout | Provider reference; internal payout reference; webhook or callback event history; reconciliation artifact tied to the ledger entry; exact provider report export where available |

| Audit controls and change tracking | Who can release payouts; who can retry failures; who can override holds; role; approval rule; generated evidence |

- Minimum policy pack

Keep five retrievable, versioned documents: KYC policy, KYB policy (where applicable), sanctions/AML operating notes, payout approval matrix, and named escalation contacts.

Build your evidence pack at provider-onboarding depth. Public Safaricom business onboarding requirements include corporate-entity and ownership evidence. For example, Certificate of Incorporation and beneficial ownership declaration forms, plus company-register recency checks with a 90-day (3-month) validity window. Do not treat that set as universal across all markets, but do treat it as a baseline signal for entity, ownership, and recency controls.

- Corridor readiness sheet per market

Maintain one signed-off readiness sheet per launch corridor, including Nigeria, Uganda, and Rwanda. For each sheet, record: provider, supported payout type, escalation route for failures, expected settlement behavior, callback method, and last successful end-to-end test date.

Country coverage pages are not enough. Public Chipper materials list operations in these markets and reference bank and mobile-money recipient flows, which indicates payout-type variability by corridor. Combine that with country-specific regulatory treatment and FATF's local-circumstances approach. Launch only after corridor-level readiness is documented.

If callbacks are part of your flow, document exactly what is enabled. Daraja notes validation callbacks run only when external validation is enabled, while confirmation callbacks handle payment-completion confirmations.

- Finance retention bundle per payout

Store, at minimum, provider reference, internal payout reference, webhook or callback event history, and a reconciliation artifact tied to the ledger entry. Where available, retain the exact provider report export used for reconciliation.

Make traceability one hop: internal payout ID -> provider reference -> reconciliation artifact. That helps prevent month-end "paid but unprovable" disputes and gives finance a clean proof trail.

- Audit controls and change tracking

Define controls so three actions are unambiguous: who can release payouts, who can retry failures, and who can override holds. For each action, record role, approval rule, and generated evidence.

Use stronger approval paths for higher-risk actions; dual-authorization patterns can appear in onboarding controls, for example requirements signed by at least two directors or shareholders. Then tie the pack to policy-change operations so updates are tracked, not ad hoc. That includes sanctions controls aligned to targeted financial sanctions expectations and your Gig Platform Regulatory Watchlist for Contractor Payments.

Related: How to Write a Payments and Compliance Policy for Your Gig Platform.

Failure modes that break gig-platform payouts first#

The first failures to harden against are duplicate execution, corridor assumptions, status-model drift, and weak escalation paths. These can show up before more abstract scaling issues.

- Duplicate payouts after retry storms

Treat idempotency as mandatory on both create and retry paths, or duplicate payouts become much more likely. Webhook events can arrive more than once, and retry tails can be long, for example every 3 minutes for the first 4 tries, then hourly for up to 72 hours when 200 OK is not returned in a documented Paystack flow. Keep one internal payout ID mapped to one idempotency key and one provider reference across all replays, including manual retries.

- Silent corridor gaps hidden by broad coverage claims

Validate corridor capability market by market before launch, even when provider pages sound broad. Chipper Cash presents different coverage views across operational-country pages and SEND/RECEIVE route guidance, while also supporting payouts to both bank and mobile money destinations. For each corridor, confirm the exact destination rail you need, whether mobile money rails or bank rails, and record the latest successful end-to-end test plus fallback route.

- Reconciliation debt from mixed status models

Use one normalized internal payout state model across rails, or reconciliation work will pile up. API call status and underlying transaction status are not always the same, and M-Pesa exposes separate status-check and reversal capabilities. Map provider-specific statuses into your internal model instead of storing raw provider labels as your source of truth.

- Escalation dead ends on stuck payouts

Define escalation paths before volume increases, because delayed or missing payouts are a known operational case. If your team cannot immediately route by rail with clear ownership, evidence requirements, and provider support channels, incident handling can stall. Keep one investigation path per rail with provider reference, event history, status-check endpoint, and named incident contact.

For a broader payments infrastructure checklist, see How to Scale a Gig Platform From 100 to 10000 Contractors: The Payments Infrastructure Checklist.

Conclusion and next step for your team#

For African gig platform payouts, the practical path is to choose rails based on real corridor and payout-method needs, then add complexity only when your operating data justifies it.

- Choose by corridor reality, not brand visibility

Use published capabilities as a starting point, then verify corridor by corridor and direction by direction before launch. Safaricom publishes M-PESA integration via Daraja 3.0 plus a reconciliation capability, while Chipper publicly positions cross-border transfers and direct sends to bank and mobile money accounts in 21+ African countries. But Chipper public and support sources also show scope differences by context, so treat coverage as a validation task, not a marketing assumption.

- Stage your setup based on control needs

Start single-rail when one corridor pattern and payout destination type dominate early demand. Add a second rail when live demand clearly spans different corridor or destination requirements that one rail does not cover well. Move to orchestration when the core problem becomes retry control, payout-state normalization, and cross-country auditability.

- Make launch approval an evidence-backed internal decision

Before go-live, align product, engineering, and finance on one shared operating pack: corridor matrix, destination coverage by market, payout-state definitions, retry rules with idempotency keys, webhook verification approach, reconciliation outputs, and clear ownership for retry and exception handling. The key test is simple: for any failed payout, your team can trace the internal ID, provider reference, event history, and next authorized action.

- Run a time-boxed pilot, then decide from your own failure data

Use a time-boxed pilot in one or two priority corridors as an internal operating window, not a universal rule. Measure failure classes, manual handling load, unresolved exceptions, and reconciliation quality. If one rail stays reliable with low operational drag, keep it. If failures cluster by corridor or destination type, add dual-rail coverage or orchestration before broader expansion.

For teams weighing build versus buy, see How to Embed Payments Into Your Gig Platform Without Rebuilding Your Stack.

Before your pilot starts, review the API and webhook docs with engineering and finance so failure states and reconciliation ownership are defined up front.

Frequently Asked Questions

Which should an African gig platform start with first, M-Pesa, Chipper Cash, or both?

Start with the rail that matches your first live corridors and destination types, then add the second only when the use case requires it. Chipper’s public materials position it around international transfers and document sends to non-Chipper recipients on bank or mobile money accounts, while M-PESA Global is publicly positioned for global send and receive and the public M-Pesa API portal lists status-query and reversal capabilities. If day-one demand spans multiple corridor types, run both only after corridor-by-corridor validation, because published Chipper country lists and its “over 40 markets” business claim describe different scopes.

How are mobile money rails different from bank rails for contractor payouts?

Mobile money rails pay into a mobile-money account used via mobile phone, while bank rails pay into an account at a bank or other financial institution. In practice, they serve different recipient preferences and operating patterns, so treat them as distinct payout destinations in your routing and reconciliation design. Do not assume identical settlement timing across rails; one documented Chipper non-Chipper flow says funds could take up to 4 business days.

What minimum controls are required before launching live payouts?

Use an idempotency key on every payout create and retry path so retries do not execute the same payout twice. Verify webhook signatures against the unmodified raw UTF-8 request body, and deduplicate already-seen event IDs because duplicate deliveries are expected. Document role separation in writing so critical consecutive payout-control tasks are assigned to different roles.

When should a platform add a second payout rail instead of scaling one provider?

Add a second rail when your required corridors or destination types are no longer covered well by the first rail alone, not just because volume increased. Typical triggers are needing both bank and mobile money destinations across active markets or finding corridor coverage gaps during validation. Before enabling it, keep a corridor test matrix with destination rail, latest successful end-to-end test, and escalation path.

What usually breaks first when payout volume grows quickly?

Focus first on retry safety and event handling: missing idempotency on retries and duplicate webhook processing. Also watch for reconciliation drift when teams treat raw provider statuses as their source of truth instead of mapping to one internal payout state. Because corridor scope can vary by provider and flow, keep status-check and reversal paths operational before queues grow.

How should engineering and finance split ownership of payout failures and retries?

Use documented separation of duties rather than a fixed team template. At minimum, separate technical payout controls (idempotency, webhook authenticity checks, and duplicate-event handling) from approval and reconciliation decisions so one person is not handling consecutive control tasks. Keep one shared investigation path per incident with the internal payout ID, provider reference, and full event history.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- brookings.edu/wp-content/uploads/2022/04/Effective-engagem...trusted

- databank.worldbank.org/metadataglossary/world-development-indicator...trusted

- docs.stripe.com/api/idempotent_requeststrusted

- dspace.mit.edu/bitstream/handle/1721.1/163313/zhu-vicky369-...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ojp.gov/ovc_fmrc_guide_sheet_internal_control_separa...trusted

- remittanceprices.worldbank.orgtrusted

- worldbank.org/content/dam/Worldbank/Research/GlobalFindex/...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Scale a Gig Platform From 100 to 10000 Contractors: The Payments Infrastructure Checklist

If you want to scale a gig platform from hundreds to thousands of contractors, treat payments operations as a launch gate alongside demand, not as a back-office task. Demand can look strong while payout execution, compliance checks, and reconciliation risk build in the background, then surface when you add a country, contractor cohort, or reporting obligation.

How to Write a Payments and Compliance Policy for Your Gig Platform

Treat your **payments compliance policy for a gig platform** as an operating document, not a legal memo. If product, finance, and engineering cannot use it to decide whether a payout is released, held, reviewed, or reported, the policy is not finished.

Gig Platform Regulatory Watchlist for Contractor Payments

Use this watchlist to rank expansion markets by payment operability, not just demand. The real question is whether you can pay contractors with controls that hold up, support costs you can absorb, and evidence you can defend when exceptions or incidents happen. This gives you a decision-ready way to compare regulatory risk, control burden, and operating cost before you commit product, compliance, or GTM resources.