Quick Answer

Form W-8EXP is a payer-side certificate used to support withholding treatment for certain foreign governments and other foreign organizations, but it does not automatically eliminate U.S. withholding. A withholding agent should accept it only when the payee clearly fits an IRS-listed category, is the beneficial owner of the income, and provides a complete, signed, current form supported by the record.

How Form W-8EXP Affects Withholding Decisions#

Treat Form W-8EXP as a payer-side control document, not just another upload. A withholding agent still has to apply withholding rules when paying income to foreign persons.

This guide takes that operator view so compliance, legal, and finance owners can:

- separate likely eligible entities from misrouted submissions,

- define the minimum evidence pack to collect, and

- escalate when the facts are unclear.

The IRS scope is specific. Form W-8EXP is the certificate for certain foreign governments and other foreign organizations for U.S. withholding and reporting. It is used to establish non-U.S. status, claim beneficial ownership of the income tied to the form, and claim a reduced rate or exemption when the Code allows it.

A signed form is not the decision. IRS instructions indicate that withholdable payments are generally subject to withholding unless the entity establishes a valid chapter 4 exemption status. In practice, the key checkpoint is whether the submission supports the status and withholding treatment you plan to apply.

That matters because the default withholding backdrop is strict. The instructions reference a general 30% withholding rate on specified U.S.-source payments to foreign persons, with a 4% rate called out for certain foreign private foundations under section 1443.

This article stays within IRS form-purpose and instruction signals, including the IRS Form W-8EXP page and Instructions for Form W-8EXP (Rev. October 2023). The IRS page shows a recent review date of 30-Mar-2026. Confirm you are using the current revision before relying on older intake templates.

This is not line-by-line tax advice, and it does not assume Form W-8EXP automatically removes U.S. withholding in every case. Where facts are ambiguous, including special cases such as a withholding qualified holder claiming section 897(l) treatment under section 1445, escalate for specialist review.

Need a related tax-form primer? Read A Deep Dive into the Foreign Tax Credit (Form 1116).

What Form W-8EXP actually certifies#

Form W-8EXP supports a specific withholding position, not a blanket exemption from U.S. withholding. It is the Certificate of Foreign Government or Other Foreign Organization for United States Tax Withholding and Reporting, and it works only when the entity and payment facts fit.

It is used to certify core points:

- the payee is not a U.S. person,

- the filer is the beneficial owner of the income tied to the form, and

- the filer is claiming a reduced rate or exemption only within listed categories, such as foreign governments, international organizations, foreign central banks of issue, foreign tax-exempt organizations, foreign private foundations, or governments of U.S. territories.

For section 1445, a withholding qualified holder may also use Form W-8EXP to establish non-foreign treatment and claim a section 897(l) withholding exemption where applicable.

For withholding decisions, the form is evidence, not automatic clearance. You still need a defensible classification that lines up the entity category, ownership claim, and payment facts with the treatment you plan to apply.

Use a simple checkpoint: confirm the submission fits an allowed W-8EXP category and that your records support that fit. Validate against current IRS instructions, including Rev. October 2023.

A common failure is treating a signed upload as automatic withholding relief. IRS instructions indicate withholding generally applies unless the entity establishes an exemption based on a valid chapter 4 status. If category fit or ownership is unclear, pause and escalate before releasing payment.

Who should use W-8EXP and who should not#

Use Form W-8EXP only when the payee clearly fits an IRS-listed category, or the limited section 1445/section 897(l) special case. If the facts do not clearly fit, verify eligibility in the current IRS instructions before you accept the form.

The IRS lists these categories for this form: foreign government, international organization, foreign central bank of issue, foreign tax-exempt organization, foreign private foundation, and government of a U.S. territory. IRS instructions also include a separate "When not to use Form W-8EXP" section, but the full disqualifying detail is not covered here.

| Entity type | In scope for Form W-8EXP | What to verify before acceptance | Evidence to request and retain | Caution |

|---|---|---|---|---|

| Foreign government | Yes, if the entity fits this category and owns the income covered by the claim | Category fit and beneficial owner claim | Signed form and any supporting information required by current IRS instructions | Public excerpts do not provide the full legal test; validate against current IRS instructions |

| International organization | Yes, if the entity fits this category and is the owner of the income | Category fit and beneficial owner claim | Signed form and any supporting information required by current IRS instructions | Category definitions are not fully detailed in the excerpts |

| Foreign central bank of issue | Yes, if the payee is this entity type | Category fit and beneficial owner claim | Signed form and any supporting information required by current IRS instructions | Do not rely on label similarity alone |

| Foreign tax-exempt organization | Yes, where the entity qualifies and is claiming appropriate treatment | Category fit and beneficial owner claim | Signed form and any supporting information required by current IRS instructions | IRS instructions (Rev. October 2023) note revisions tied to section 501(c)(3) supporting information |

| Foreign private foundation | Yes, if the entity fits this category | Category fit and beneficial owner claim | Signed form and any supporting information required by current IRS instructions | This form does not always mean zero withholding; IRS instructions reference 4% under section 1443 for certain payments |

| Government of a U.S. territory | Yes, if the payee fits this category | Category fit and beneficial owner claim | Signed form and any supporting information required by current IRS instructions | Public excerpts do not provide full boundary detail |

| Qualified foreign pension fund (special case) | Limited case in the section 1445 context | Confirm the filer can claim treatment as a withholding qualified holder under section 1445 and section 897(l)-related exemption treatment | Signed form and any supporting information required by current IRS instructions for the section 1445/897(l) claim | Not a general shortcut; instructions note updates tied to December 2022 (87 FR 80042) final regulations |

The core control is simple. If legal name, claimed category, and ownership representation do not line up for the income stream, do not approve the form yet.

A signed form alone is not enough for withholding treatment. IRS instructions state withholdable payments are generally subject to 30% withholding unless an exemption is established.

For a step-by-step walkthrough, see Who Should Use Form W-8EXP for U.S. Tax Withholding.

How W-8EXP compares with other W-8 forms#

Use this as an intake classification check. Ask whether the form matches the payee type and payment facts, not just whether a W-8 was provided.

| Form | Filer type lane to test | Core claim to validate | What the U.S. withholding agent can do |

|---|---|---|---|

| Form W-8EXP | Special-tax-treatment lane, confirmed from payee facts | The payee is claiming status-based withholding treatment | Validate the claim and supporting record before applying reduced or exempt treatment |

| Form W-8BEN | Individual lane, confirm from payee facts | The payee is documenting foreign status for withholding treatment | Classify and process under the individual documentation path |

| Form W-8BEN-E | Entity lane, confirm from payee facts | The entity is documenting foreign status for withholding treatment | Process under the entity documentation path |

| Form W-8ECI | One of the five W-8 forms; confirm fit from payee facts and income type | The submitted form matches the payee and payment facts | Route for tax review before final withholding treatment if fit is unclear |

| Form W-8IMY | One of the five W-8 forms; confirm fit from payee facts and income type | The submitted form matches the payee and payment facts | Route for tax review before final withholding treatment if fit is unclear |

Operator rule: if the submitted form does not clearly match filer type, income type, and any special-tax-treatment claim, pause and validate form selection before accepting it.

Intake can fail when a W-8 form is accepted before filer type and payment type are clearly mapped. Because W-8 forms are submitted to the payer or withholding agent, intake is the control point. If required documentation is missing, withholding can default to 30%. For a related walkthrough, see Mechanical Royalties Explained: How Streaming Platforms Calculate and Pay Mechanical Rights.

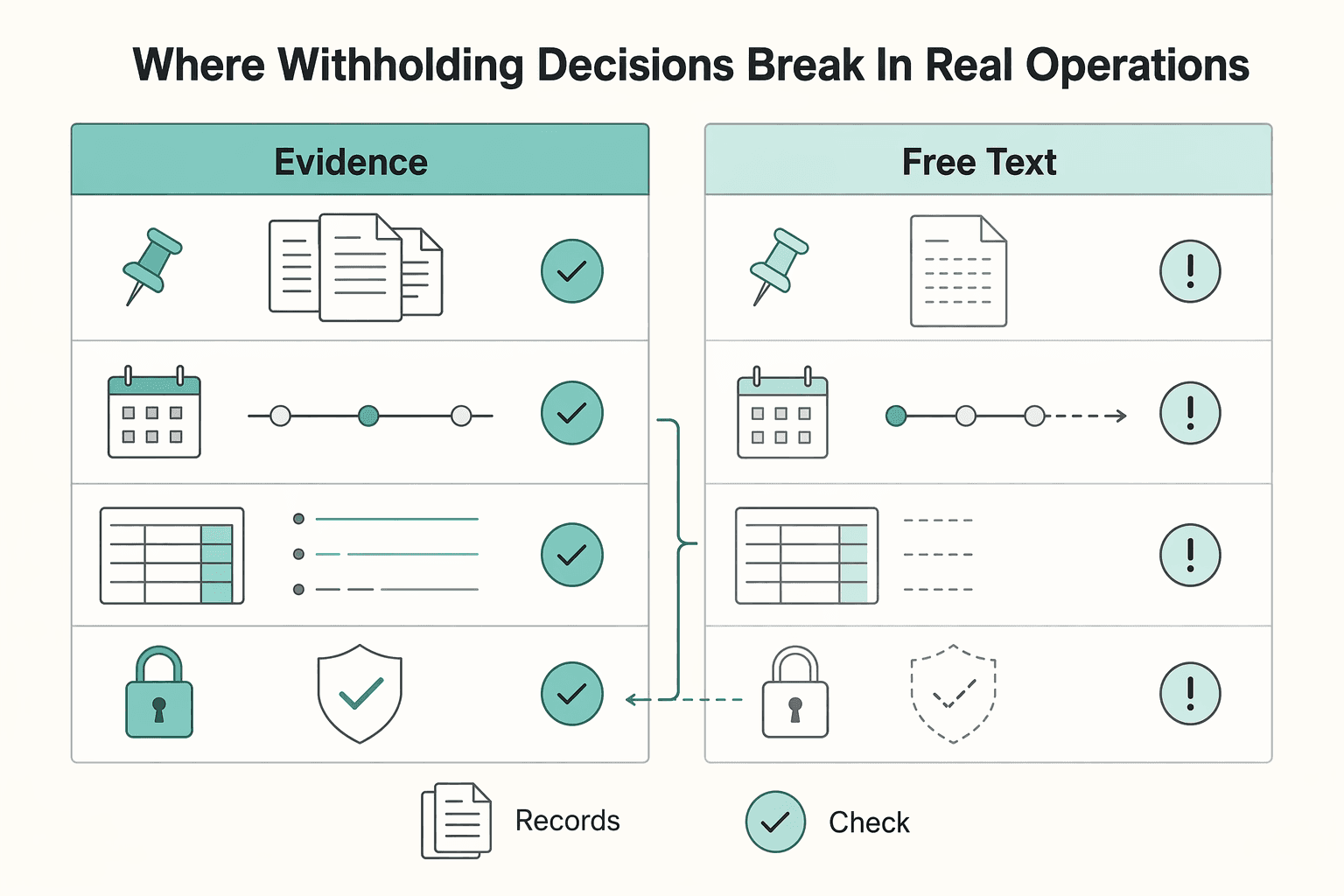

Where withholding decisions break in real operations#

Most breakdowns happen at intake, not in the rule itself. Teams can treat "document received" as "withholding approved." If payee facts are ambiguous, pause disbursement and require compliance sign-off instead of allowing a manual override.

| Break point | What happens | Response |

|---|---|---|

| Payout moves before the evidence is ready | Payment is queued as soon as a withholding document is uploaded, but later review shows the file was not ready | Distinguish an approved withholding record from only an uploaded form |

| Free-text intake drives the wrong form path | Fields like "foundation," "ministry," or "agent" can route the payee into the wrong lane | Require structured intake facts before assigning withholding treatment |

| Stale records get reused after status drift | An older status assumption keeps getting copied forward while entity facts change | Recheck current guidance instead of treating older summaries as final decision authority |

That lines up with the Publication 515 decision sequence: Identifying the Payee, When to withhold, Determination of amount to withhold, and the withholding agent's Liability for tax. In practice, payout timing can take priority before payee identity and withholding support are actually locked.

Payout moves before the evidence is ready#

A common failure is queueing payment as soon as a withholding document is uploaded. Later review then shows the file was not ready for the treatment that was applied.

The control question is binary: do you have an approved withholding record, or only an uploaded form? If your payment logic cannot distinguish those states, you have a release-control gap.

Free-text intake drives the wrong form path#

Another failure mode starts with description fields like "foundation," "ministry," or "agent." Teams then accept the first form submitted and route it into the wrong lane.

Publication 515's operational guardrail is still clear: Identifying the Payee is a separate step. Require structured intake facts before you assign withholding treatment, and do not let free text decide payee classification.

Stale records get reused after status drift#

A quieter failure is record reuse. An older status assumption keeps getting copied forward while entity facts change. Without revalidation, your withholding decisions inherit stale logic.

Version discipline matters here. IRS bulletin synopses are reader aids and are not authoritative interpretations, so older summaries should not be treated as final decision authority without rechecking current guidance.

Install this control now#

Separate "document received" from "withholding approved." For ambiguous cases, hold disbursement until compliance signs off on payee identification and amount-to-withhold determination. A compact evidence pack is usually enough:

- final withholding documentation on file

- reviewer note for payee identification and classification

- dated guidance reference used for the decision

- reporting linkage for Forms 1042 and 1042-S obligations

Intake sequence from request to approved withholding record#

Close the release-control gap by separating received from approved. As an internal control, keep payment on hold until the W-8EXP submission is approved as a withholding record.

| Step | Action | Control point |

|---|---|---|

| Collect and classify | Collect the tax package and classify the payee into the correct form lane using structured intake facts, not free text | If the profile is an organization but the submission is Form W-8BEN, stop the flow |

| Validate reviewability | Check completeness and internal consistency against your intake checklist | If the file is not decision-ready, reject it with structured reason codes |

| Approve and lock | Use operations plus tax or compliance approval as an internal control choice and record exactly which submission version was accepted | Keep a short decision note |

| Bind approval to payout | Only approved records should be release-eligible | Received, incomplete, rejected, or pending review should remain blocked |

| Log the trail | Record every state change with timestamp, reviewer identity, reviewed version, and payout-hold transitions | Treat record history as a standing control |

- Collect and classify before payment is even eligible.

Collect the tax package and classify the payee into the correct form lane using structured intake facts, not free text. If the profile is an organization but the submission is Form W-8BEN, stop the flow, because W-8BEN is for individuals.

- Validate reviewability, then reject with reason codes when needed.

Check completeness and internal consistency against your intake checklist. Treat W-8EXP-specific field, eligibility, and signer checks as internal policy decisions here. If the file is not decision-ready, reject it with structured reason codes so it gets corrected once instead of being informally rerouted.

- Approve with dual control, then lock the approved version.

Use operations plus tax or compliance approval as an internal control choice, then record exactly which submission version was accepted for the U.S. withholding agent decision. Keep a short decision note so later reviewers can reconstruct the rationale without redoing intake.

- Bind approval state to payout state.

Only approved records should be release-eligible. received, incomplete, rejected, or pending review should remain blocked. This also reduces downstream exposure where missing or incorrect TIN data can trigger separate withholding consequences. Publication 1281 lists a 24% backup withholding rate for subject payments after December 31, 2017.

- Log a full, replayable event trail.

Record every state change with a timestamp, reviewer identity, reviewed version, and payout-hold transitions. Treat record history as a standing control, consistent with IRS instruction themes such as "Change in circumstances" and "How long to keep the certifications."

If you are wiring these controls into release logic, map approval states to compliance-gated disbursements in Gruv Payouts.

What evidence to retain for a defensible position#

Retain a decision packet that explains both what you approved and why you approved it, so finance, risk, auditors, or partner banks can reconstruct the withholding position without rerunning intake.

Build one packet per approved decision#

Treat this as an internal control choice, not just document storage. Keep one packet with the items below.

| Evidence item | What it should show |

|---|---|

| Final approved form and withholding record | The exact version tied to the approved withholding record |

| Verification support | Required verification artifacts, including certifications of compliance where applicable |

| Withholding and reporting analysis | How due-diligence, withholding, and reporting obligations were evaluated |

| Decision memo | Treatment applied, approver(s), authority used, and decision date |

A form image alone is often not enough if the follow-up question is why that form and treatment were accepted.

Record the legal anchor you actually used#

If you relied on Code sections (for example, section 1446(f), where relevant), tie the citation to the facts reviewed in the memo. Avoid shorthand-only notes with no section reference or dated reasoning.

Where you use IRS instructions, be explicit about the authority level: section references are to the Internal Revenue Code unless otherwise noted.

Date policy and interpretation changes#

Store the policy version and instruction set in force at the time of approval. If internal guidance changes later, keep the dated trail so reviewers can see what standard was applied when the decision was made.

When section 1446(f) is relevant, keep the transaction-date checkpoint used in the analysis (including the January 29, 2021 and January 1, 2023 applicability dates noted in the instructions).

Do not treat Internal Revenue Bulletin highlight text as final authority. IRB 2017-5 states its synopses "may not be relied upon as authoritative interpretations," so keep underlying primary authority with any IRB pointer.

Make retrieval part of the control#

Index packets so teams can retrieve the full record quickly by entity, payee ID, form type, approval date, reviewer, and cited Code section. A practical check is whether someone outside tax can pull the approved form, verification support, and decision memo from one place without rebuilding the file.

This pairs well with our guide on IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments.

Renewal, revalidation, and change-event controls#

Use two controls together: a scheduled renewal check and a trigger-based revalidation check when facts or law change.

Separate the calendar check from the fact-change check#

IRS requester instructions support both lanes: "Period of Validity" for fixed-cycle review, and "When To Request a New Form W-8" plus "Changes in circumstances for chapter 4 purposes" for trigger-based revalidation.

| Control lane | Grounded anchor | Operational use |

|---|---|---|

| Fixed-cycle renewal | Period of Validity | Set and track a next renewal review date |

| Trigger-based revalidation | When To Request a New Form W-8; Changes in circumstances for chapter 4 purposes | Re-check reliance as soon as relevant facts change |

A form can still be inside your review cycle and still be unsafe to rely on if you now have conflicting information. That is the core stale-form risk under due-diligence and reason-to-know concepts.

Use conservative reminder logic when timing is not clean#

Do not force one blanket validity period across programs when timing is uncertain. Set internal reminders conservatively and require active confirmation before expiry-sensitive payouts. If confirmation is not complete, hold release until you either confirm continued reliance or obtain a new form.

Build change-event checks around the legal basis you approved#

For entities using Form W-8EXP, base revalidation on the legal basis documented in the approval memo, not on document presence alone. Keep the re-review packet tight: prior approved form, prior withholding memo, the change trigger, and the updated conclusion.

Also treat legal or treaty changes as change events, even when payee data is unchanged. Publication 515 shows this risk directly. It notes cases where withholding agents may not accept certain treaty claims, including a suspension context with withholding treatment shifts beginning on or after August 16, 2024, effective December 17, 2024, and a statutory 30% withholding requirement in that context.

When to escalate to specialist tax counsel#

Escalate when the file does not support a clear, defensible withholding decision under your own approved policy. If you are in a "maybe" state, pause approval and route to specialist review.

Use that escalation lane in cases not resolved here, including:

- the same facts could plausibly fit

Form W-8EXP,Form W-8BEN-E, orForm W-8IMY - ownership status is unclear from the file

- the withholding position depends on detailed

Internal Revenue Codeanalysis not covered in your internal notes - payout timing, SLA pressure, or partner requirements are pushing a tax decision before the classification is settled

Use referral logic, not local guesswork#

IRM 21.3.11.4.2 explicitly includes "Referring Customers to Other Areas and Resources." Treat that as the operating principle here. When first-line review cannot resolve the issue, refer it instead of forcing a conclusion. The same IRM framework also includes a TAS escalation path.

When you escalate, send a tight packet:

- received form and any alternate form proposed

- payment description and relevant contract excerpt

- entity status or formation support

- signer authority support

- prior withholding memo, if any

- one short statement of the exact ambiguity

Hard-stop signals#

Treat inconsistency or suspicion in identity or EIN documentation as a hard stop. IRM 21.7.13.2.2.1 isolates "Frivolous/Suspicious Forms SS-4" as separate handling, and IRM 21.7.13.2.8 includes TAS guidance.

Also treat withholding-certificate execution issues as escalation candidates rather than quick fixes. The IRSAC discussion of electronic-signature alignment for withholding certificates is a practical signal that these processes can be technically detailed. Use a sober specialist review process when classification is uncertain.

How to implement this in Gruv controls without overbuilding#

Keep the implementation narrow: use a formal intake checkpoint, a payout gate tied to document state, a reconstructable event trail, and an exception lane for unresolved conflicts. Treat these as Gruv control choices, not IRS-mandated Form W-8EXP requirements. Neither W-8EXP-specific eligibility rules nor a required Gruv control architecture are established here.

Gate payout on approved document state#

Use a clear document-state flow (requested -> received -> under review -> approved/rejected -> superseded) and release payout only when the current state is approved. Also require a formal receipt checkpoint before a submission is treated as accepted, so intake does not become usable before review.

Where tax-document processes are enabled in Gruv, keep sensitive fields in restricted storage and expose masked views for broader operations.

Make the trail reconstructable from intake to release#

Record explicit events from request to decision to payout, and keep clarifications in written case notes. If the classification or decision changes midstream, capture who changed it, what changed, and what decision followed.

Where payout flows are ledger-backed, tie approval, hold, rejection, and release events to the same payout reference so reconciliation does not depend on manual stitching.

Make retries harmless and mismatches obvious#

Design status writes so retries can be replayed safely instead of creating duplicate approvals or conflicting states. If systems diverge, for example, a tax case is approved but payout is still pending, or payout is released while the case is unresolved, route the item to an exception queue for manual resolution before funds move.

Keep baseline controls global and local changes explicit#

Define one global baseline, then add market-specific or program-specific variants only where they are actually enabled. Because operational rules and payout parameters can change, document each local override with an owner, effective date, and exact deviation from baseline.

30-day implementation checklist for compliance and finance owners#

Use the first 30 days to make classification, evidence, and revalidation decisions explicit internal controls, not IRS-mandated sequencing. The practical risk is reliance. If your team cannot show why it accepted a valid Form W-8EXP, the payment can fall back to general withholding treatment, which IRS instructions describe as generally 30% on withholdable payments to a foreign entity.

| Week | Focus | Key checks |

|---|---|---|

| Week 1 | Publish triage criteria for Form W-8EXP | Hold the file for review before payout release if entity facts do not clearly support this certificate |

| Week 2 | Deploy a minimum evidence pack and a formal review step | Keep the completed form, a short classification note, and support for non-U.S. status, beneficial owner claim, and any chapter 4 status or exemption claim |

| Week 3 | Enable revalidation triggers for incomplete, conflicting, or stale records | Trigger fresh review instead of reusing prior acceptance when entity facts or claims change |

| Week 4 | Run a sample audit on recent payouts | Reconstruct each decision from request to release and confirm document completeness, written withholding rationale, and any documented escalation outcomes |

Week 1#

Publish triage criteria for Form W-8EXP and the withholding documentation your intake team already handles. Keep the first checkpoint simple: does the payee fit the certificate scope for foreign governments or other foreign organizations for U.S. withholding and reporting purposes? If entity facts do not clearly support this certificate, hold the file for review before payout release.

Week 2#

Deploy a minimum evidence pack and a formal review step for each withholding decision. At minimum, keep the completed form, a short classification note for why this form type was accepted, and support for the core certifications you are relying on: non-U.S. status, beneficial owner claim, and any chapter 4 status or exemption claim.

As a process check, confirm reviewers are using the current instruction set (Rev. October 2023) and flag section 1445 and section 897(l) claims for separate review.

Week 3#

Enable revalidation triggers for incomplete, conflicting, or stale records. Changes in entity facts or claims should trigger fresh review instead of reusing prior acceptance. This is where stale reliance creates preventable risk.

Week 4#

Run a sample audit on recent payouts and reconstruct each decision from request to release. Confirm document completeness, written withholding rationale, and any documented escalation outcomes. If you cannot rebuild that trail quickly, treat it as a control gap even when the form itself appears valid.

Related reading: Form 3520 Playbook: A 3-Step Framework for Foreign Trust Transactions and Foreign Gift Reporting.

Conclusion#

Treat Form W-8EXP as a controlled withholding decision artifact, not a one-time upload. The highest-value controls are eligibility triage, evidence retention, and change-triggered revalidation.

This form is narrow by design and should be accepted only for the listed filer groups: foreign governments, international organizations, foreign central banks of issue, foreign tax-exempt organizations, foreign private foundations, and governments of U.S. possessions. Operationally, classify first, then accept. The instructions distinguish who must provide Form W-8EXP from when not to use it. If the entity is acting as an intermediary, route to Form W-8IMY. If an owner is only claiming foreign status or treaty benefits, route to Form W-8BEN or Form W-8BEN-E.

Before payout release, validate the basics in order:

- Confirm the entity fits a W-8EXP category.

- Confirm Part I owner identification details are present and match your payee record.

- Confirm the form is complete under your current controls.

Then retain a defensible file: final form, classification rationale, supporting review evidence, and a brief approval note. Revalidate on change in circumstances, and pause reliance on the existing certificate until review when key entity facts or claimed status change.

Keep the baseline tight and escalate edge cases. Do not guess when the fact pattern is ambiguous across W-8 forms or ownership status is unclear. Keep the form with the withholding agent or payer, not filed with the IRS. Start with intake, validation, and revalidation checkpoints, then tighten ambiguous cases with counsel. When your policy needs market-specific confirmation before rollout, use Contact Gruv to validate coverage and control design.

Frequently Asked Questions

What is Form W-8EXP and what does it certify?

Form W-8EXP is the IRS certificate for certain foreign governments and other foreign organizations for U.S. withholding and reporting. It is used to establish non-U.S. status, certify beneficial ownership of the income tied to the form, and support a reduced rate or exemption when the Code allows it. For payer-side controls, treat it as evidence for a withholding position, not an automatic tax waiver.

Who should use Form W-8EXP instead of Form W-8BEN-E?

Use Form W-8EXP when the payee clearly fits an IRS-listed category for this certificate, such as a foreign government, international organization, foreign central bank of issue, foreign tax-exempt organization, foreign private foundation, or government of a U.S. territory, or in the limited section 1445 and section 897(l) special case. This guide does not establish a full rule set for every W-8EXP versus W-8BEN-E fact pattern. If the entity does not clearly fit the W-8EXP categories, escalate classification before payout instead of guessing.

Does Form W-8EXP automatically eliminate U.S. withholding?

No. Withholding still depends on the income type, the support for the exemption claim, and whether the claimed chapter 4 status or other basis is valid. IRS instructions state foreign persons can be subject to 30% U.S. tax on covered U.S.-source payments, and certain foreign private foundations can be subject to 4% tax under section 1443.

What changed in the latest IRS instructions relevant to Section 1445 and Section 897(l)?

The Rev. October 2023 instructions say they were updated to reflect final regulations published in December 2022. They also state that a withholding qualified holder under section 1445 may use the form in connection with non-foreign treatment and to claim a section 897(l) exemption where applicable. The same revision updated supporting information requirements for entities qualifying under section 501(c)(3) that represent non-private-foundation status.

What happens if a payer has no valid Form W-8EXP on file?

Without a valid form on file, the payer may not have a clear basis to rely on the claimed status or exemption. Treat the record as invalid if the form is expired, incomplete, or unsigned. Withholding outcomes can depend on several factors, not just whether a form was submitted.

Who should sign Form W-8EXP for an organization?

The form should be signed by the beneficial owner claiming the status on the certificate. This article does not provide a reliable entity-by-entity list of acceptable signer titles. If signer authority is unclear from your records, escalate before relying on the form for payment release.

How long can a Form W-8EXP be relied on before revalidation is required?

This article does not treat a single rule of thumb as definitive for W-8EXP revalidation mechanics. Operationally, rely only while the form remains unexpired, complete, and signed, and confirm current IRS instructions when timing affects a live payout. Revalidate sooner when facts or law change.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: