Quick Answer

A VAT calculator cannot determine the correct VAT treatment for cross-border services by itself. It helps with net-to-gross and gross-to-net math after you confirm the transaction type, jurisdiction pair, place of supply, customer tax status, and any reverse-charge conditions. If facts or evidence are unclear, treat the result as provisional and hold invoice release.

What a VAT Calculator Can and Cannot Tell You#

Treat a VAT calculator for cross-border services as a control input, not the legal decision. It helps with VAT math, but the legal treatment still depends on jurisdiction, transaction facts, and the rules on where a service is taxed.

That is the tension for finance, legal, and risk teams. You need to keep invoicing and payouts moving without creating avoidable VAT issues in review, filing, or audit. A fast answer built on the wrong assumptions is still an error.

In the European Union (EU), Value Added Tax (VAT) applies to goods and services. Cross-border obligations change based on where the parties are located and whether the transaction is goods or services. For services, place-of-taxation rules drive treatment. In the United Kingdom (UK), services VAT follows its own guidance, including post-transition UK-EU treatment from 1 January 2021.

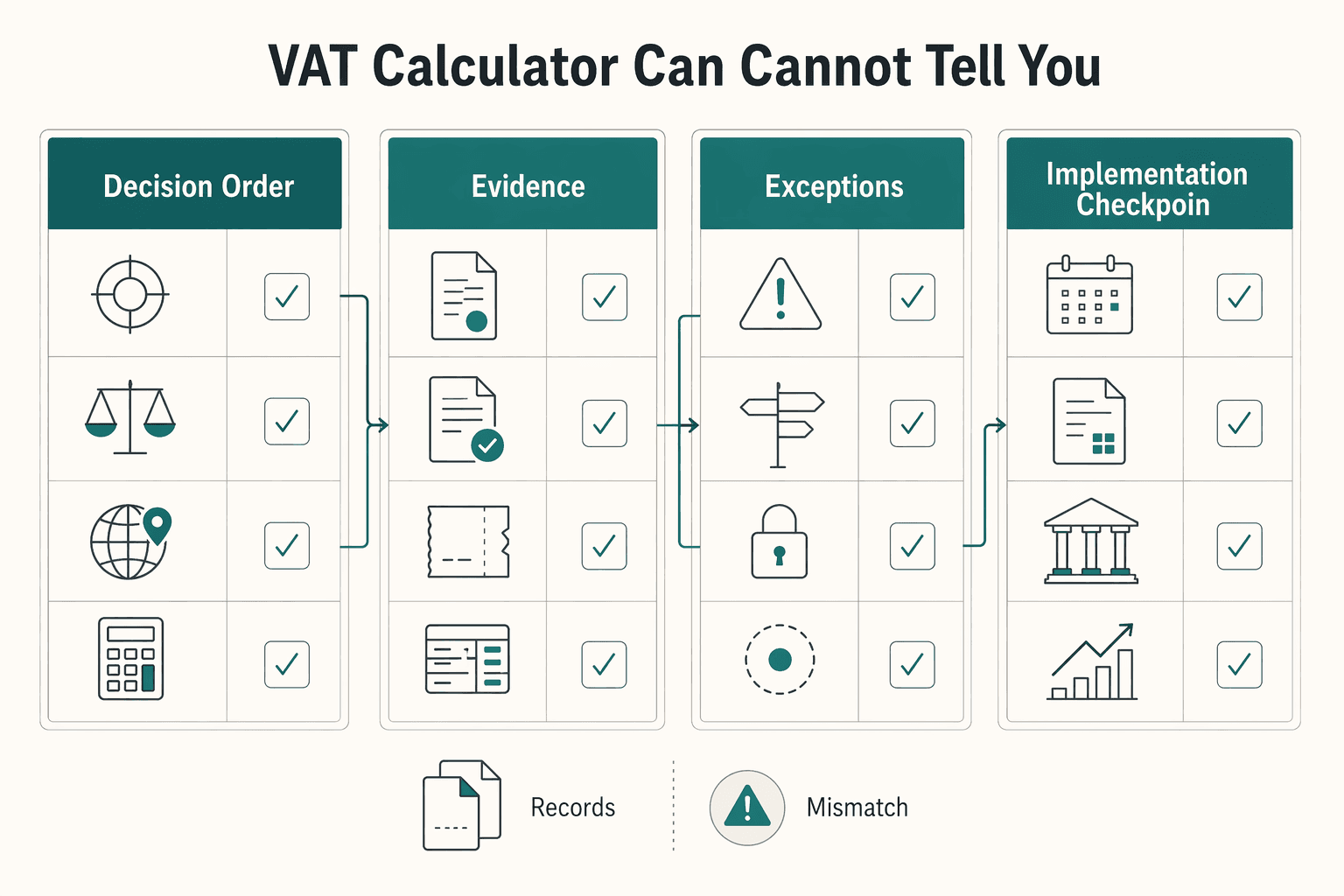

So what is a calculator actually good for? It is useful for net-to-gross and gross-to-net checks once your assumptions are settled. It can produce calculated amounts, but it cannot resolve legal classification by itself. This article gives you a practical sequence before anyone clicks calculate:

- decision order before VAT math

- minimum evidence pack for cross-border services treatment

- escalation points your team should not override

- implementation checkpoints for EU, UK, and other markets with different local rules

Use calculator outputs as provisional until your assumptions are verified. At minimum, confirm the core transaction facts: who is buying and selling, where they are located, whether the transaction is goods or services, and whether rules such as reverse charge may apply.

Scope boundary: this article is about services VAT logic, not goods-import charging. Goods-import regimes can involve both VAT and customs duties and use different thresholds and rules, including EUR 150 in IOSS-related import treatment.

Related: Assessing Services PE Clause Risk Under Tax Treaties for Cross-Border Consultants.

What a VAT calculator can decide and what it cannot#

A VAT calculator can handle the arithmetic, but it cannot make the legal VAT decision for you. VAT is both a calculation task and a reporting and liability task, so the number alone is not the full treatment. Used at the right point in the process, it can:

- convert net to gross

- reverse gross to net

- estimate totals for a chosen rate and assumed B2B or B2C treatment

- produce arithmetic outputs such as VAT = Net × Rate, and Net = Gross / (1 + Rate) with VAT = Gross − Net

But it cannot do the part that usually creates the real risk. A calculator cannot:

- determine place of supply

- confirm final VAT liability by itself

- validate whether reverse-charge treatment is valid in your specific case

The order matters: place of supply comes first, then VAT liability. Reverse-charge outcomes can be conditional, including under EU Article 194, and EU VAT rules may be applied differently across Member States.

Use one operating rule: if any core assumption is unclear, treat the output as provisional and hold invoice release. At minimum, verify and document the supplier's establishment, customer location and status, and service type before you rely on the result. Some calculator providers explicitly frame their outputs as estimates only, and your controls should treat them that way.

If you want a deeper dive, read How to verify a European VAT number using the 'VIES' system.

Why most SERP tools miss cross-border services risk#

Most tools miss the real risk because they are built for a different job. Their math may be fine, but cross-border services VAT starts somewhere else: place of supply and liability.

That is why a clean number can still be the wrong control outcome. HMRC guidance for services focuses on determining place of supply and where the service is liable to VAT. EU guidance separately distinguishes cross-border VAT rules for goods and services. If a tool never asks service-specific questions, it is probably not deciding the key risk part of the treatment.

Foil Drive, SimplyDuty, and Veem show the mismatch. Their positioning is import duty and tax estimation for goods movement, and their inputs include customs-style fields such as HS code, consignment value, and CIF. SimplyDuty also presents itself as an import calculator across over 100 destinations. Those are goods-flow inputs, not service place-of-supply logic.

HS and CIF are quick signals that you are in the wrong tool class. The Harmonized System is for classifying goods for customs and statistics, and CIF is a merchandise-trade valuation concept. Neither is service place-of-supply logic.

| Tool class | Typical inputs | Usually helps with | Misses for service VAT risk |

|---|---|---|---|

| Import estimators (Foil Drive, SimplyDuty, Veem Import Duty and Tax Calculator) | HS code, consignment value, destination, shipping/customs fields, sometimes CIF | Planning duties/taxes before shipping goods | Place of supply of services and related VAT liability checks |

| Generic VAT math tools (Omni Calculator, Wise VAT Calculator) | Amount, VAT rate, include/exclude VAT | Net/gross arithmetic | Whether VAT applies, which jurisdiction applies, who accounts for VAT |

| Broader determination tools (VAT Calc) | Invoice-level determination/reporting-oriented workflows | Broader determination/reporting support than basic arithmetic | Still depends on correct facts and policy setup |

Use a fast checkpoint before trusting any output: inspect the input screen first. If it asks for HS code, CIF, or shipping assumptions, you are in a goods calculator. If it only asks for amount and rate, you are in a math calculator. For cross-border services, anchor your process on place-of-supply facts and the jurisdictional rule applied.

The real danger is false confidence. Goods-oriented inputs or pure VAT math can make an invoice total look settled without a clear basis for VAT treatment. For defensibility, your evidence should tie back to service facts and place-of-supply reasoning.

Related: Cross-Border VAT for Digital Platforms: OSS IOSS and the EU VAT Gap.

Decision order that prevents expensive VAT mistakes#

For cross-border services, decide the legal route first and use calculator output second. Many expensive errors start with misclassification, place-of-supply mistakes, or unsupported customer status before anyone calculates VAT.

HMRC guidance is clear on order: decide place of supply, then VAT liability, and start by identifying the nature of the supply. A clean number from the wrong legal route is still the wrong result.

Use this order by default#

- Classify the transaction type. Confirm what was actually supplied and make sure the contract description and invoice lines match before you set tax treatment.

- Identify the jurisdiction pair. Confirm the legal seller, customer country, and where each party is established for this supply.

- Apply place-of-supply rules. For EU services, Articles 44 and 45 are the general anchors. B2B generally points to where the customer is established, and B2C generally points to where the supplier is established. UK general-rule B2B framing is also taxable where the customer belongs.

- Determine B2B or B2C with evidence. Use taxable-person evidence, not assumptions.

- Test reverse-charge eligibility. Reverse charge is conditional, not automatic, and should only be treated as applicable when the legal conditions are met.

Only after those five steps should you use a calculator for amounts, net/gross math, or invoice totals.

Where the main branches go#

| Route | First legal question | Likely next check | What the calculator can do after that |

|---|---|---|---|

| EU domestic services | Are seller and customer in the same EU Member State for this supply? | Confirm service classification and customer taxable or non-taxable status | Calculate VAT amount after local treatment is confirmed |

| EU cross-border services | Do Articles 44 or 45 place supply at customer or supplier location? | Validate taxable-person status and test reverse-charge conditions, especially where supplier is not established in that Member State | Model VAT-inclusive or VAT-exclusive totals and scenarios |

| UK cross-border services | Is place of supply in the UK or outside it under UK rules? | If place of supply is in an EU country, UK VAT is not due; treatment must then be checked with that country's tax authority | Calculate invoice values after foreign treatment is confirmed |

| Non-EU routes | Is there a local VAT- or GST-type obligation on this service route? | Check whether GST/VAT-type taxes and withholding taxes may both apply to service payments | Support amount calculations, not legal determination |

Controlled exceptions beat ad hoc overrides#

If you cannot validate customer status in time, send the invoice through a controlled exception path and legal review queue, not a manual billing override.

For EU VAT ID checks, VIES is a validation step. Keep the validation evidence in the case file. Where VAT ID validity is part of your treatment decision, keep the associated name and address confirmation too.

Country treatment varies, so document the cases that always trigger specialist review. Build policy on the assumption that edge cases and country-specific exceptions will happen.

Trigger mandatory specialist review when:

- customer status cannot be evidenced in time

- contract, invoice, and onboarding records point to different entities or countries

- service description is too vague to classify confidently

- reverse-charge conditions are unclear

- a non-EU route may involve GST- or VAT-type taxes and withholding taxes in parallel

Minimum data pack before anyone clicks calculate#

Do not trust calculator output until the core transaction fields and evidence are complete. If required data is missing, treat the result as provisional and hold the invoice.

For cross-border services, use this minimum internal pack: legal seller entity, buyer country, buyer tax status, service type, invoice date, currency, and evidence references. It is a practical control set, not a claim that every jurisdiction mandates the exact same list.

| Field | Why it matters | What to verify |

|---|---|---|

| Legal seller entity | VAT treatment can depend on which entity made the supply | Match contract party, invoicing entity, and registered address |

| Buyer country | VAT treatment can depend on customer location in cross-border services | Resolve conflicts across onboarding and billing records before invoicing |

| Buyer tax status | B2B and B2C can produce different VAT outcomes | Keep VAT ID evidence where relevant, or other proof plus verification |

| Service type | VAT invoice rules require a clear description of what was supplied | Align contract description and invoice lines to the actual service |

| Invoice date | VAT invoice requirements include supply/completion timing | Confirm supply or completion date is captured |

| Currency | Needed for invoice display and reporting | For UK VAT invoices, show VAT payable in sterling even if other amounts use foreign currency |

| Evidence references | You need an audit trail, not just a tax flag | Store VAT check records, customer documents, and approval records |

Buyer tax status is often a high-risk field. When EU VAT ID validation is relevant, run a VIES check and keep the result in the case file. Record the VAT number checked, returned status, checked name and address where available, and check date.

Use VIES for what it is. It returns a valid or invalid status at that point in time, and updates can lag national databases. If no VAT ID is available, EU rules allow other proof of taxable status when you perform a reasonable level of verification and record what you relied on.

Mandatory field validation, dual approval for manual overrides, and immutable reason codes are strong operational controls, but they are policy choices rather than explicit EU or UK legal mandates. One hard stop still matters: do not use VIES for UK GB VAT numbers, because as of 01/01/2021 that validation route no longer applies.

For a step-by-step walkthrough, see Digital Rupee Cross-Border Payments for Freelancers in 2026.

Before your team trusts any output, run VAT IDs through a single control point using Gruv's VAT Number Validator and attach that result to the evidence pack.

Verification checks before invoice and payout release#

Release gating is a key control. Before issuing the invoice or approving payout, re-check the invoice total, VAT treatment, and release eligibility under your policy.

Confirm that the invoice still matches the verified inputs: seller entity, buyer country, B2B/B2C status, service type, invoice date, currency, and the evidence record supporting the tax decision. If reverse-charge treatment is being applied, confirm that buyer tax-status evidence is still on file and still usable for the invoice date.

Match the tax decision to what is actually being posted#

Your release check should tie the approval decision to the accounting output so the treatment is explainable later. Keep at least these links reviewable:

- tax decision fields used at approval

- final issued invoice copy

- ledger tax code or posting generated from that decision

- approval log showing who cleared exceptions or refreshed the result

This alignment matters in both EU and UK contexts. UK digital VAT records include time of supply and value of supply, and include reverse-charge transactions in VAT records. EU invoice rules include the date of issue and a unique sequential invoice number. If the invoice, ledger entry, and approval trail do not align, the tax position becomes harder to defend even when the arithmetic is right.

Re-check customer tax status when timing shifts#

If customer tax status may be stale, refresh approval before release. VIES only confirms VAT-number validity for the current day, not past dates, and updates can lag.

So if an EU VAT ID was checked earlier, re-run it close to invoice release and store the result with the check date. For UK (GB) VAT numbers, use the UK checker and keep evidence of when the check was performed.

If a number remains invalid after recheck, route it to review and ask the customer to contact their tax administration to update the record.

Use one hard stop for both invoice and payout#

Use one operational gate for invoice release and linked payout eligibility so tax exceptions do not turn into cash and reconciliation problems.

Practical policy rule: if verification fails, hold invoice release, consider blocking the linked payout batch, and send the case to compliance review with the evidence pack. Include the invoice copy, current validation evidence, approval history, and the field that changed. That record set supports later HMRC checks and, where Article 369k special-scheme standards apply, electronic availability of sufficiently detailed records.

Reporting choices teams confuse most often#

Once the invoice treatment is settled, the next common error is routing it into the wrong reporting path. Similar-looking cross-border invoices should not be forced into the same filing route. Route by jurisdiction and by the scheme that is actually available for that flow.

Direct local filing versus OSS#

For eligible EU flows, OSS (One Stop Shop) can simplify reporting because you register once, file one VAT return, and make one payment through one portal. But OSS is optional, and the OSS return is additional. It does not replace your ordinary VAT return.

Direct local filing remains the right path when a flow is outside OSS scope or your data cannot reliably separate eligible and non-eligible transactions. A practical control is simple: if your team cannot explain why an invoice belongs in OSS instead of a local return, do not centralize that flow yet.

IOSS is not the answer for service invoices#

IOSS (Import One Stop Shop) is for distance sales of low-value goods imported into the EU, up to EUR 150. It is not a general services reporting route.

If a services process is labeled "IOSS," treat that as a routing error unless the transaction is actually an imported-goods flow within that threshold.

EU and UK routes can diverge even when invoices look similar#

EU and UK invoices can look similar while reporting obligations differ. UK VAT MOSS is not available for supplies made after 31 December 2020 and was withdrawn from 1 January 2021.

Keep separate routing logic for EU and UK entities. HMRC OSS guidance in this area is scoped to Northern Ireland to EU distance sales of goods. That is a practical reminder that UK and EU reporting paths are not fully harmonized for all flows.

Reporting artifacts to keep reviewable#

Once routing is set, keep the filing support compact and reviewable so each filed amount can be traced back to an approved tax decision. These are internal controls, not universal legal requirements.

| Reporting artifact | What it should show | Check before filing |

|---|---|---|

| Transaction list | Population included in the return or local filing route | Matches filing period and excludes held or reversed items |

| VAT treatment rationale | Why each flow was routed and treated as recorded | Matches approved invoice decision |

| Evidence references | IDs or links for eligibility evidence used in routing | Evidence is dated and usable for the period |

| Exception logs | Removed, overridden, or manually reviewed items | Unresolved exceptions are not silently included |

| Review sign-off owner | Named owner or function for reporting approval | Ownership is explicit before submission |

Centralization helps only when eligibility and data quality are stable#

Centralization can reduce operational load. In the HMRC Northern Ireland-to-EU distance-sales context, the alternative can mean registrations in up to 27 EU countries. But it works only when eligibility logic and input data are consistently reliable.

Keep tax regimes separate in operations as well. Depending on jurisdiction, cross-border invoices may involve VAT reporting, GST accounting, or withholding obligations, and those should be tracked separately from EU or UK VAT reporting math. For that overlap, see Cross-Border Invoicing: How to Handle VAT GST and Withholding Tax on International Invoices.

Related reading: Choosing a Small Business Lawyer for Cross-Border Freelance Work.

Escalation triggers your team should not override#

Some cross-border service invoices should pause until a human review is complete. If you cannot state the place-of-supply basis, customer status, and reverse-charge basis in one short note, treat the calculation as provisional and escalate.

Use non-negotiable triggers, not "close enough" judgment calls:

- Ambiguous place of supply: if the facts do not clearly show which country's VAT rules apply, do not choose a rate just to keep billing moving. Place of taxation determines which EU country's rules apply, and HMRC guidance says place of supply is decided before VAT liability.

- Conflicting B2B/B2C signals: if the customer says they are B2B but contract or onboarding evidence points to B2C, stop and review. For services, this classification is a core branch in place-of-supply analysis, including in the UK.

- Failed VIES check: an invalid VIES result means the VAT number is not registered in the relevant national database. Treat that as a review trigger, not automatic reverse charge. VIES is a search engine, not a database, and its output alone does not create exemption rights.

- Uncertain reverse charge treatment: in the UK, reverse charge depends on conditions that include recipient status and the place of supply being inside the UK. If either point is unclear, do not label the invoice reverse charge.

One workable operating model is to have finance ops triage and assemble the evidence pack, then route higher-risk cases to a named tax or legal reviewer for final treatment. Keep the pack compact: seller entity, buyer country, service description, tax-status evidence, VIES result when relevant, and a short rationale for the chosen treatment.

Set an internal timing rule as a policy choice: unresolved escalations can pause invoice finalization rather than shipping "temporary" VAT treatment. Keep one additional hard check in place: VIES validation for UK GB VAT numbers ceased on 01/01/2021.

The short checklist for monthly control health#

A monthly control-health check should confirm one thing: your VAT decisions still match current rules and records, and your evidence can support a filing review.

Re-test EU and UK routes separately#

Test EU and UK service routes as separate paths. From 1 January 2021, UK-EU services moved to the UK-to-non-EU framework, so your sample should explicitly cover both routes and can include both B2B and B2C cases.

For each sampled invoice, confirm that stored assumptions still match place-of-supply treatment and customer tax status in your process. Also confirm your controls do not rely on VIES checks for GB VAT numbers, because GB validation in VIES ceased on 01/01/2021.

Read exception logs for root causes#

Treat recurring exceptions as control failures, not admin noise. Missing tax IDs, incorrect customer-status flags, and other data errors can change VAT treatment. That includes cases where an invalid or missing EU VAT ID means VAT is usually charged at the rate applicable in your country.

When you identify an error, correct it and keep a clear record of why it happened, when it was discovered, and the VAT amount involved. If the same cause keeps repeating, fix the upstream rule or data-capture step creating it.

Check reporting-pack evidence before filing#

Before filing, make sure the reporting pack actually supports the return. For OSS flows, ensure records are electronically retrievable without delay and retained for 10 years from the end of the transaction year.

For UK VAT-registered entities, confirm records and filing outputs remain consistent with Making Tax Digital for VAT digital record-keeping and software filing expectations. When a rule changes, record the update, set the cutover date, and re-check transactions around that boundary.

Conclusion#

A VAT calculator for cross-border services is useful for arithmetic, not legal determination. Control quality comes from decision order, verified inputs, and disciplined escalation.

Determine place of supply first, then assess VAT liability, then decide whether reverse charge or another treatment applies, and only then use calculator output. If you reverse that order, accurate math can still produce the wrong VAT result.

The immediate next step is operational: implement a minimum data pack and escalation triggers before adding more automation. Collect core transaction facts and supporting evidence. Where EU VAT ID validation is relevant, keep the VIES result with the invoice record, and document when validation is not possible, for example GB VAT numbers in VIES after 01/01/2021.

Keep the sequence simple:

- Block calculation when required fields or evidence are missing.

- Escalate failed checks, conflicting B2B/B2C signals, unclear place-of-supply outcomes, and uncertain reverse-charge cases.

- Automate release only when the final treatment is traceable to input data, approval, and recorded outcome.

Keep scheme scope explicit. OSS can cover eligible cross-border services to EU consumers through one Member State registration, declaration, and payment path. IOSS is different: it applies to imported goods consignments not exceeding EUR 150, not general services.

Finally, confirm market-specific treatment before scaling. VAT can be applied differently across EU countries, EU Commission VAT guidelines are practical and non-binding, and UK and EU handling diverged in some operational areas after 1 January 2021. Where treatment depends on local interpretation or edge-case classification, route it to specialist review before volume increases.

If you're operationalizing this across EU, UK, and non-EU flows, contact Gruv to confirm market coverage and control design before scaling volume.

Frequently Asked Questions

Can a VAT calculator tell me the correct cross-border services treatment by itself?

No. A calculator can handle VAT arithmetic, but it does not determine place of supply, final VAT liability, or whether reverse charge applies. For EU and UK services, decide where the service is taxed first and assess the VAT treatment second.

What minimum data is required before we should trust a calculator output?

Use enough verified data to determine place of supply and customer tax status before relying on the output. A practical minimum pack includes the legal seller entity, buyer country, buyer tax status, service type, invoice date, currency, and evidence references. If an EU VAT number is relevant, keep the number and its VIES validation result.

When should we apply reverse charge and when should we escalate?

Apply reverse charge only after place of supply is confirmed and you have support that the customer is acting as a business in the relevant jurisdiction. It is conditional, not automatic. Escalate when customer status cannot be evidenced, VIES does not provide what you need, or place-of-supply treatment is still unclear.

How do we avoid mixing import-duty logic with services VAT decisions?

Keep goods and services in separate decision paths. If a tool depends on HS code, CIF, shipment value, or other shipping inputs, it is a goods or import-duty tool rather than a services VAT tool. For services, anchor the process on service facts, place of supply, and VAT liability.

What should we do when customer VAT status is unclear at invoice time?

Do not let the calculator guess. Where relevant, validate the EU VAT number in VIES and keep the result. If VIES still does not provide what you need, contact the relevant national authority; if the customer does not have a valid EU VAT number, you should usually charge VAT at your domestic rate.

How do OSS and IOSS differ, and why does that matter for services teams?

OSS and IOSS have different scopes. OSS can support eligible EU consumer sales, including cross-border supplies of services within the EU, through one registration, one return, and one payment. IOSS is for distance sales of low-value imported goods up to EUR 150, so it is not a general services VAT classification tool.

Does the EUR 10 000 threshold mean our cross-border services team can ignore OSS until we pass it?

No. The EUR 10 000 EU-wide threshold is referenced for certain telecom, broadcasting, and electronic services and intra-EU distance sales of goods, not every service line. If you handle mixed supplies, confirm which flows are actually in scope before using that threshold in reporting logic.

Rina focuses on the UK’s residency rules, freelancer tax planning fundamentals, and the documentation habits that reduce audit anxiety for high earners.

With a Ph.D. in Economics and over 15 years of experience in cross-border tax advisory, Alistair specializes in demystifying cross-border tax law for independent professionals. He focuses on risk mitigation and long-term financial planning.

Sources

- ec.europa.eu/taxation_customs/viestrusted

- elibrary.imf.org/view/journals/001/2025/214/article-A001-en.xmltrusted

- europa.eu/youreurope/business/taxation/vat/check-vat-n...trusted

- europa.eu/youreurope/business/taxation/vat/one-stop-sh...trusted

- irs.gov/individuals/international-taxpayers/nra-with...trusted

- legislation.gov.uk/eudr/2006/112/article/226/adoptedtrusted

- legislation.gov.uk/eur/2011/282/article/18trusted

- oecd.org/en/data/datasets/international-transport-and...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: