Quick Answer

Build a platform compliance readiness scorecard as a launch gate, not a document checklist. Score governance ownership, control operation, evidence retrieval, exception handling, and monitoring, then require proof for each critical domain before approving exposure. Tie every score to an end-to-end transaction trace from request through ledger and reconciliation records. If a high-risk control lacks current evidence, treat readiness as red and hold full rollout until the missing control proof is produced.

How to assess compliance readiness before a new market launch#

A launch is ready only when your controls hold up under live operations. Teams usually learn that in launch week, when governance, workflows, and visibility all have to work together under real volume and real exceptions. That is the operator problem here: not whether your controls look complete on paper, but whether they work when operations scale.

The practical answer is a readiness scorecard used as a go/no-go method, not a filing cabinet for policy documents. The gap between a clean rollout and a messy one is usually preparation. If you start scaling before confirming that the necessary systems and controls are actually in place, governance gaps show up fast and operational risk follows.

This is written for the people who get called when a rollout stalls, workflows break, or an approver asks for evidence right now. That usually means people across platform, operations, and delivery teams who own execution and oversight. If that is your seat, the scorecard helps you make a defensible decision with facts you can verify, not optimism.

A useful readiness check spans several areas at once. Governance matters because someone has to own the control. Automation and workflows matter because a control that exists only in a policy deck will fail the first time exceptions pile up. Visibility matters because you need to see what happened and pull evidence without a scavenger hunt across three teams. One checkpoint cuts through the noise: can your team retrieve the relevant approval and execution evidence for a sample request on demand? If not, you are not ready, even if the narrative sounds reassuring.

This is also not a vendor feature tour or a product comparison with something called Compliance Scorecard. It is a launch decision method for scaling operations, where readiness varies by workflow, team, and operating context. The point is to pressure-test your launch posture before exposure expands.

The standard is straightforward. You are looking for evidence that the right foundations are in place before you scale. If controls, workflows, and proof retrieval cannot be demonstrated together, treat that as a launch risk, not an admin gap. The next section defines what the scorecard should actually measure so you can separate policy completeness from production readiness. Related reading: Healthcare Staffing Platform Payments Compliance for Safer Rollouts.

What a platform compliance readiness scorecard actually measures#

A platform compliance readiness scorecard should tell you whether controls can be demonstrated as operating effectively, not just whether policy documentation is complete. That is the core difference between launch readiness and a policy or document-management scorecard: policy tools can improve clarity and risk alignment, but they do not prove control execution on their own.

| Domain | Included focus |

|---|---|

| Governance | Ownership and decision rights |

| Control execution | What happens in practice |

| Evidence | Quality and retrieval speed |

| Exception handling | Follow-through |

| Post-launch monitoring | Drift |

Use the scorecard to separate written intent from operating proof. A practical check is whether your team can quickly show who owns a control, what decision rights apply, and the evidence that the control ran as expected. If answers depend on manual spreadsheet tracking and ad hoc follow-up, treat that as a real readiness risk.

At minimum, score these domains:

- Governance ownership and decision rights

- Control execution in practice

- Evidence quality and retrieval speed

- Exception handling and follow-through

- Post-launch monitoring for drift

The non-negotiable is evidence for high-risk controls. If a critical control lacks proof of operation, readiness is red regardless of meeting confidence. No evidence, no go.

The control domains and owners you must lock before launch#

Lock ownership before you score anything. If a domain has no named accountable owner, mark it amber and block production exposure until that gap is closed.

You do not need a heavy RACI artifact on day one, but you do need a clear accountable owner, a usable backup owner, and explicit evidence expectations for each domain. That matches the FedRAMP AC-1 pattern: controls are developed, documented, and disseminated to organization-defined personnel or roles, then reviewed and updated on a defined cadence. In practice, ownership gaps are usually where evidence retrieval and exception handling fail first.

Use 8-12 domains as an operating range, then map each one to the obligations that apply in your program. Typical launch-critical domains include onboarding, payouts, reconciliation, reporting, incident response, access, data handling, and tax-document handling. Where relevant, that mapping can include KYB, KYC, AML, GDPR, and W-8/W-9 workflows. If your operating model changes, revisit domain mapping and ownership because legal, tax, and operational consequences can shift with that architecture choice.

| Domain | Owner | Backup owner | Required control | Required evidence | Launch blocker yes/no |

|---|---|---|---|---|---|

| Onboarding controls | Named role | Named backup | Program-defined onboarding checks (for example KYB/KYC where applicable) | Documented procedure + operational records | Yes |

| Payout controls | Named role | Named backup | Program-defined payout approval/hold controls (including AML/sanctions checks where applicable) | Documented procedure + operational records | Yes |

| Reconciliation controls | Named role | Named backup | Program-defined reconciliation workflow | Documented procedure + operational records | Yes |

| Reporting controls | Named role | Named backup | Program-defined reporting controls | Documented procedure + operational records | Yes |

| Incident response | Named role | Named backup | Program-defined escalation and resolution workflow | Documented procedure + operational records | Yes |

| Access control | Named role | Named backup | Access control policy and procedures assigned to defined roles | Current policy/procedure + operational records | Yes |

| Data handling | Named role | Named backup | Program-defined personal data handling controls (including GDPR where applicable) | Documented procedure + operational records | Yes |

| Tax document handling | Named role | Named backup | Program-defined tax document workflow (including W-8/W-9 where applicable) | Documented procedure + operational records | Yes |

Before launch, run a simple test: pick a domain and ask the owner to produce both documentation evidence and operational evidence in one working session. If the owner can explain the control but cannot produce dated proof, score that domain down.

Also validate backup coverage. A named backup without access, context, or authority is not real resilience. Keep the rule simple: no accountable owner, no launch; no usable backup, limit exposure until fixed. Related: FATCA Compliance for Marketplace Platforms: Identifying and Reporting Foreign Account Holders.

Map controls to the full money lifecycle before you score anything#

Do not score readiness from policy text alone. First map one transaction end to end. If you cannot explain it from request to provider reference to ledger entry to export, treat the launch as not ready.

Walk the lifecycle in the same order that money and evidence move: invoice or payment confirmation, ledger posting, wallet projection, FX quote usage (if applicable), payout initiation, webhook settlement, and reconciliation close. For each step, define one control gate, one detection signal, and one owner responsible for recovery.

Build the lifecycle map around real transaction traces#

Start from a real test or non-production transaction, not a whiteboard flow. Trace it with concrete IDs across systems (for example: internal transaction ID, provider reference, ledger journal ID, payout instruction or batch ID, webhook event ID, and reconciliation/export record). If a handoff depends on someone "knowing where to look," mark it as a readiness risk.

Make verification strict: ask each owner to produce evidence for their step in one working session. If the chain is incomplete, you have a partial story, not a controlled path.

A reactive compliance program often shows up here: teams can assemble screenshots and spreadsheets near an audit, but that is different from staying ready continuously. The more evidence you assemble after the fact, the lower confidence your score should carry.

| Lifecycle step | Control gate | Failure mode | Detection signal | Recovery owner |

|---|---|---|---|---|

| Invoice or payment confirmation | Transaction created and status logged | Duplicate request or missing confirmation | Duplicate IDs, or payment without confirmed status | Product or payments ops owner |

| Ledger posting | Traceable ledger write | Confirmed payment not posted, or posted twice | Count mismatch or duplicate journal pattern | Finance ops owner |

| Wallet projection | Balance update tied to ledger event | Wallet projection diverges from ledger movement | Balance variance or unexplained negative position | Ledger or treasury owner |

| FX quote usage | Quote reference stored with transaction | Stale or missing quote reference | Out-of-window timestamp or missing quote link | Treasury or payments owner |

| Payout initiation | Eligibility check before release | Ineligible or duplicate payout instruction | Pending-review payout or duplicate instruction pattern | Payments ops owner |

| Webhook settlement | Settlement matched to prior request | Delayed, missing, or repeated webhook | Missing expected settlement, late state change, repeated event ID | Engineering or payments ops owner |

| Reconciliation close | Match and exception signoff | Held return or payout exception left open | Open breaks, unmatched lines, aged exceptions | Finance ops owner |

Put hard checkpoints where money can still be stopped#

Place hard gates at the last point where you can still stop a bad release or prove why it happened. If your program uses AML holds before release, make that gate explicit at payout initiation. If your program depends on KYC/KYB status before payout, store that status with the payout decision.

Keep audit trails linked across release, hold, retry, return, and reconciliation/export records so compliance, finance, and ops can answer the same question from their own systems. Watch for common failure patterns: stale FX quotes, duplicate retries, webhook delays, held or returned deposits without clear ownership, and payout exceptions that age without closure. If the team cannot show both detection and recovery ownership for a step, score it down; if you cannot map the full chain, pause the launch.

For a step-by-step walkthrough, see Upskilling Platform Finance Teams for Payments Compliance and Automation.

Set a scoring model that forces a real go no-go decision#

After you map the money path, force a decision with a scoring gate, not a long debate. A strong average should not override one unevidenced critical control.

Use a compact model so owners can score consistently in one review: assign each control domain 0-3, then read that score alongside risk impact from your Risk Matrix Scorecard and open escalations in your Risk Register. If you use a Policy Scorecard or Assessment Scorecard, treat it as supporting context, not the final launch gate.

Use a scale that exposes weak controls quickly#

| Score | Control state | Operational signal |

|---|---|---|

| 0 | Absent or untestable | Current evidence cannot be produced |

| 1 | Exists | Manual, incomplete, or unproven in realistic conditions |

| 2 | Operating | With evidence and explainable end to end, with exceptions managed |

| 3 | Reliable | Clear monitoring and repeatable recovery |

- 0: Control is absent, untestable, or current evidence cannot be produced.

- 1: Control exists, but is manual, incomplete, or unproven in realistic conditions.

- 2: Control is operating with evidence and explainable end to end, with exceptions managed.

- 3: Control is operating reliably with clear monitoring and repeatable recovery.

For each critical domain, require current evidence, the last exception, and related escalation history in the same review. If the score says healthy but escalations are unresolved or unowned, score it down or hold the launch.

Lock stop rules before the review starts#

Set and document stop rules before the meeting:

- Any critical control at 0: no launch

- Any critical control at 1: limited pilot only

- All critical controls at 2+: conditional launch

If you accept faster launch tradeoffs, document residual risk, assign an owner, set a time bound, and require executive sign-off.

| Decision band | Minimum condition | Required approvals | Allowed market exposure |

|---|---|---|---|

| Red | Any critical control scored 0, or critical evidence missing | Launch owner, compliance, and finance acknowledge no-go and log the decision with an audit trail | No live market exposure |

| Amber | No critical 0s, but one or more critical controls scored 1, or residual risk is still open | Domain owners, compliance, finance, and executive sign-off on time-bound residual risk | Limited pilot only, with restricted market scope and heightened monitoring |

| Green | All critical controls scored 2 or 3, and open risks are noncritical, owned, and dated | Launch owner, compliance, and finance approve the decision packet | Conditional launch to planned scope |

Even green should remain conditional and documented. Include the scorecard, evidence links, open exceptions, approvals, and review date so the go/no-go outcome is auditable and repeatable.

We covered this in detail in Country-by-Country Launch Rules for Platform Payout Compliance.

Build the day one evidence pack auditors and operators can both use#

Build the evidence pack at control level so operators can explain day-one behavior and auditors can verify it quickly. For each critical control, keep the same minimum set: policy record, execution log, exception ticket, ledger trace, reconciliation proof, and approval history.

| Control | Minimum artifact set | Primary source system | Named retriever | Response window |

|---|---|---|---|---|

| Payout release gate | Policy record, execution log, approval history, exception ticket if overridden | Risk or payments ops tool | Control owner or backup owner | Set internally before launch |

| Ledger and settlement traceability | Ledger trace, provider reference, reconciliation proof, exception ticket if unmatched | Ledger, provider portal, finance close records | Finance owner | Set internally before launch |

| Tax or identity handling | Policy record, masked document view, approval history, reporting artifact where enabled | Tax doc store or reporting tool | Tax or compliance owner | Set internally before launch |

Make retrieval part of the control, not an admin afterthought. For every artifact, define who can pull it, from which system, in what format, and within what response window. If a complete export cannot be produced on request, treat evidence quality as weaker.

Add cross-reference fields only for discoverability (for example SOC 2, NIST, FTC Safeguards Rule, CIS Control 14), not as proof that a control worked. For sensitive tax and identity records, keep handling PII-safe with masked W-8/W-9 views for routine review and restricted access to full documents. Where enabled, include reporting artifacts for Form 1099, FBAR, and Form 8938 workflows.

For FBAR specifically, preserve the exact page state or notice used at the time because FinCEN posts filing due-date and disaster-related extension updates on its FBAR page. For the full breakdown, read Gruv Platform Payments for Global B2B Payouts and Compliance.

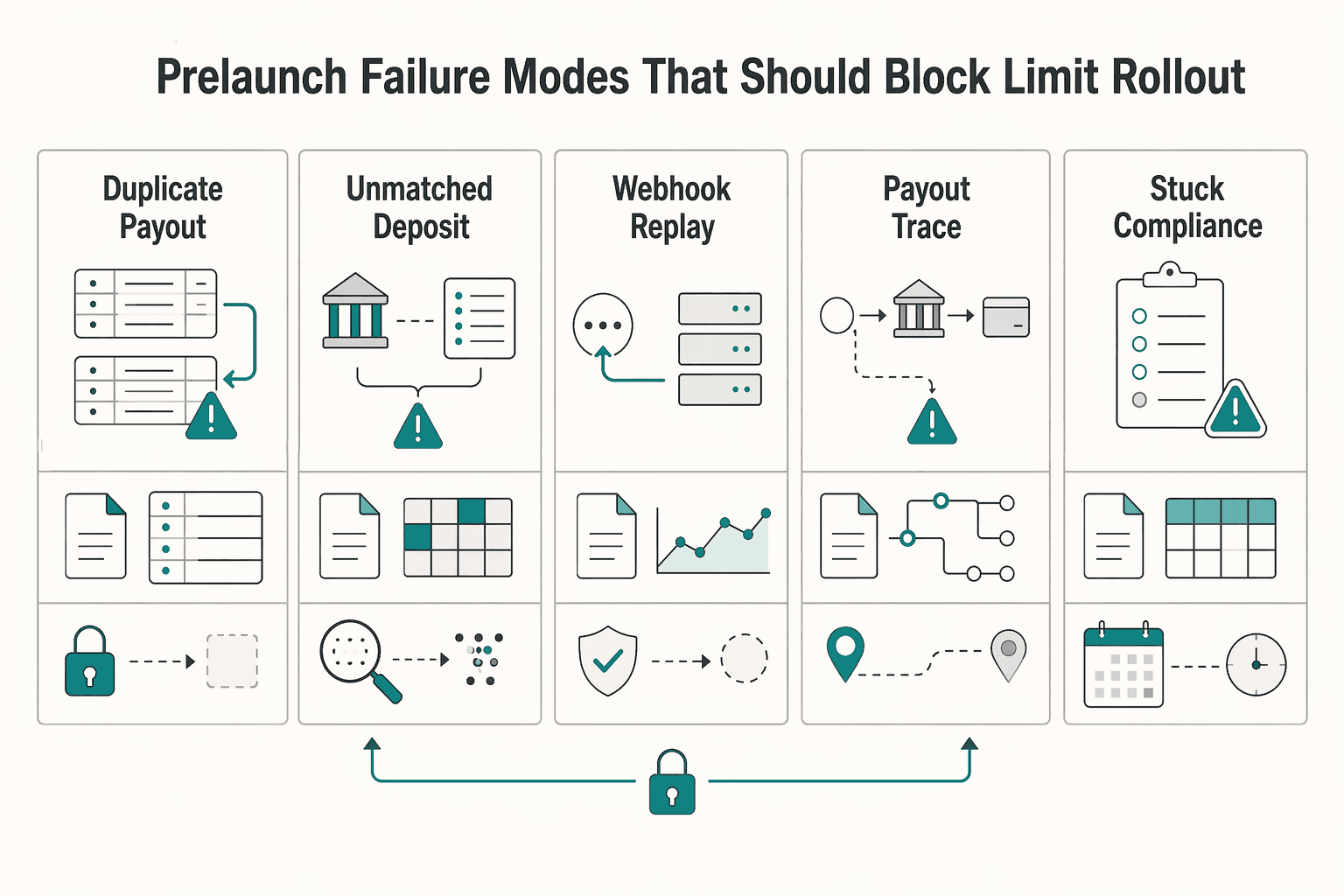

Prelaunch failure modes that should block or limit rollout#

Block rollout when you cannot prove control execution and exception handling, and limit rollout when recovery paths are still manual. A listed control category is not an exemption from review. Check applicable procedures and any extraordinary circumstances before you rely on it.

Run prelaunch drills as a structured process, and use failed or delayed cases to test whether the team can detect, contain, and evidence issues quickly. Keep the decision rule simple: unresolved control gaps are blockers; controlled but unproven operations are pilot-only.

| Failure mode | What to verify before launch | Default launch decision |

|---|---|---|

| Duplicate payout attempt | Retry/idempotency behavior is documented, exceptions are visible, and one case shows how it is handled | Limit if handling is manual; block if handling is unclear |

| Unmatched deposit | A deposit can be traced to the correct record and exception workflow | Block if matching and ownership are not clear |

| Delayed webhook | Source records remain complete when updates arrive late, with a workable fallback path | Monitor if records remain complete; limit if delays break release decisions |

| Failed settlement reconciliation | End-of-cycle reconciliation completes, and repair ownership is explicit | Block if reconciliation cannot close or exceptions cannot be isolated |

| Stuck compliance review | Queue visibility, escalation, and release/reject ownership are defined | Limit if review is manual and aging is not reliably monitored |

Use explicit if-then rules so launch decisions are repeatable. If a release path is manual and untested end to end, keep rollout at pilot volume. If reconciliation breaks at close, pause new payout batches until the break is understood, recorded, and owned.

How to handle country and program variance without slowing every launch#

Do not redesign controls for every market. Keep a fixed global baseline, then add local overlays only when they change data handling, tax reporting, or payout eligibility.

| Area | Grounded note | Action |

|---|---|---|

| Data handling | Local variance changes whether data can be handled the same way | Require legal or compliance sign-off before go-live |

| Reporting duty | Local variance changes reporting duty | Require legal or compliance sign-off before go-live |

| Payout eligibility | Local variance changes payout eligibility | Require legal or compliance sign-off before go-live |

| FATCA-related workflows | Record the exact reporting assumption, filer scenario, and approver for each market or program | If the assumption trail is missing, treat readiness as incomplete |

Variance across GDPR, FATCA, and local KYB programs can change what a launch needs, but your baseline should stay stable: owner assignment, ledger traceability, reconciliation close, approval history, and evidence retrieval. Use overlays for country- or program-specific duties instead of reopening the full control set.

For FATCA-related workflows, record the exact reporting assumption, filer scenario, and approver for each market or program. Form 8938 is attached to the tax return, filing depends on thresholds that vary by filer situation (including higher thresholds for some joint filers and taxpayers residing abroad), and Form 8938 is not required if no income tax return is required for that year. If that assumption trail is missing, treat readiness as incomplete.

Apply one launch rule: if local variance changes payout eligibility, reporting duty, or whether data can be handled the same way, require legal or compliance sign-off before go-live. Keep a dated change log with market, program, approval owner, source document, and any FinCEN-related reporting assumption so approval changes do not drift away from payout logic or reporting evidence.

For contractor and seller data handling, see GDPR for Marketplace Platforms: How to Handle Contractor and Seller Personal Data Compliantly.

Conclusion#

Readiness is not a policy pass. It is the point where you can show, clearly and on demand, that your controls work across your operating workflows. You should be able to show that each one has an owner with decision rights and that the evidence is retrievable when something goes wrong.

That is the value of a compliance readiness checklist or scorecard. It forces the launch conversation away from confidence, slideware, or a clean-looking policy deck and back onto governed workflows, ownership, decision rights, and evidence that can survive contact with live volume. If a control exists only as automation logic nobody can explain, or as a manual step nobody can evidence, you are not ready to scale. Automation helps, but it is not proof by itself.

The practical next move is simple: take one market or one payout program and run it through the scorecard this week. Do not start with your easiest lane. Pick the one most likely to expose ownership gaps, evidence retrieval problems, or unresolved exceptions.

Use these checkpoints as your closeout test:

- Mark every critical control red, amber, or green based on proof, not intent.

- For each red or amber item, record the accountable owner, the missing artifact or broken check, and the exact condition that must be met before launch.

- Write launch conditions in plain language such as "no live payouts until reconciliation close can be demonstrated" or "pilot only until hold-release workflow is tested and approval history is retrievable."

One operator detail matters more than teams expect: test retrieval, not just existence. In the review meeting, ask someone to pull a control trace, an exception ticket, and an approval record from the production-adjacent source you would rely on during an incident. If that takes too long, depends on one person, or produces conflicting records, treat it as a live gap. A common failure mode is assuming evidence can be assembled later, then finding out under pressure that ownership is fuzzy and records live in three different places.

If you need a sensible next step with Gruv, keep it lightweight: talk to sales first to confirm market and program coverage for the countries and payout paths you actually plan to launch. Then put the scorecard into your launch checklist so every new market gets the same ownership, evidence, and launch-condition review before money moves. That is how compliance readiness becomes an operating habit instead of a one-time review.

Frequently Asked Questions

What is a platform compliance readiness scorecard for new market launches?

A platform compliance readiness scorecard is a launch decision tool, not just a policy checklist. It tests whether your controls can be demonstrated clearly and on demand, with evidence that they operate in practice. If the score looks green but a launch-critical control has no proof, the market is not actually ready.

Which controls are mandatory before enabling first live payouts?

There is no universal mandatory set in these sources, so do not borrow one blindly. The practical rule is simpler: every control you classify as critical for launch should have clear ownership, a defined pre-launch check, and retrievable evidence that it operates. Control details can vary by company and market, but the ownership-plus-evidence standard should not.

Who should own each control across finance, operations, and product?

Give each control one accountable owner, with clear decision rights. Ownership can span finance, operations/compliance, and product/engineering, but accountability should be explicit. If a control has shared responsibility but no single accountable owner, treat it as amber until that is fixed.

How do we set an objective go/no-go threshold instead of a subjective review?

Use the same hard-stop logic every time: if any critical control lacks operating evidence, do not approve full launch. Define consistent scoring bands your team uses for no-go, limited rollout, and conditional go-live. A good checkpoint is to request one real artifact per critical control during the review; if the team cannot produce it, score that control lower.

What evidence must be audit-ready on day one?

Keep the evidence pack close to operations: control documentation, records that controls operated, exception records, and approval history. You should also know who can pull each artifact, from where, in what format, and how quickly, because "we can find it later" usually fails when an incident or audit request hits. Include only records that apply to the obligations your market or program actually triggers.

Can we launch if we align to SOC 2 but still have unresolved payout exceptions?

Usually no, not if those exceptions touch a critical launch control. A SOC 2 readiness assessment is a pre-audit step that helps identify control gaps before an official audit, but it does not by itself prove launch readiness. SOC 2 can support your evidence structure and broader control posture, yet unresolved critical exceptions are still a launch risk that needs explicit ownership and a time-bound fix or limited rollout decision.

Try a related tool

Arun focuses on the systems layer: bookkeeping workflows, month-end checklists, and tool setups that prevent unpleasant surprises.

Sources

- cms.gov/Regulations-and-Guidance/Guidance/Transmitta...trusted

- comptroller.war.gov/Portals/45/Documents/defbudget/FY2026/budget...trusted

- dodcio.defense.gov/Portals/0/Documents/CMMC/AssessmentGuideL2.pdftrusted

- dodcio.defense.gov/Portals/0/Documents/CMMC/AssessmentGuideL2v2...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- govinfo.gov/content/pkg/FR-2025-12-19/xml/FR-2025-12-19.xmltrusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/businesses/corporations/do-i-need-to-file-fo...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Prepare Your Payment Platform for Acquisition: Compliance, Technical, and Financial Readiness

Acquisition prep for a payment platform is a cross-functional evidence test, not a finance-only exercise. Frame readiness around whether you can show compliance controls in production, trace money movement, and validate reporting without last-minute rework.

FATCA Compliance for Marketplace Platforms: Identifying and Reporting Foreign Account Holders

For marketplace teams handling cross-border payouts, FATCA work is mostly a control-design problem. You need to decide what to implement first, what evidence to keep, and what to escalate before a payout creates avoidable reporting or withholding risk. The practical question is not whether FATCA exists, but which controls actually reduce reporting errors and potential 30% withholding outcomes.

GDPR for Marketplace Platforms: How to Handle Contractor and Seller Personal Data Compliantly

Treat this as an operating decision, not a policy exercise. If you own compliance, legal, finance, or risk for a platform, your job is to decide who owns each GDPR duty. You also need to define what evidence must exist, what your team reviews on a recurring basis, and which issues need escalation before a launch or vendor change goes live.