Quick Answer

Payment data can improve contractor matching only when the signals are auditable, comparable by market and job type, and validated against real outcomes. Start with inspectable records from invoice through payment and reconciliation, assign owners for exceptions, keep compliance gates outside ranking logic, and prove lift with controlled side-by-side tests before scaling any signal.

How payment data can improve contractor matching#

Use payment data as verifiable evidence, not automatic proof that matching is better. Most teams can explain how they rank contractors. Fewer can show which payment signals still hold up when you check them against auditable payment and dispute records.

Step 1: Start with auditable payment records#

Before you model anything, make sure each payment event ties back to records an operator can inspect later. A practical checkpoint is 3-way matching: compare the purchase order, invoice, and receiving report before payment is released. If those documents align, the invoice can move to payment. If they do not, you have a clear reason to stop and investigate.

If you cannot trace a signal to standard records like vendor invoices or order receipts, do not use it to drive expansion decisions.

Step 2: Fit the signal to the market context#

A payment signal means little without context. Research on payment-system design frames this as fit to the project environment: project characteristics plus external factors. For platform operators, the practical lesson is straightforward: do not assume one payment signal means the same thing across job types, workflows, or markets.

The same delay can reflect routine verification in one market and an operational breakdown in another. Keep signals out of ranking until you can compare like with like.

Step 3: Build an evidence pack before claiming lift#

Before you change ranking logic, assemble a small evidence pack you can defend later:

- baseline outcomes you already trust

- dispute and payment-exception logs

- document-level examples showing how a payment event was verified

- notes on where records are manual, late-corrected, or missing by market

This matters because manual invoice processing is error-prone and can create delayed payments or disputes. In one case study, PO-invoice mismatches created correction loops that slowed billing and increased administrative workload.

Step 4: Accept the verification tradeoff early#

Verification costs time and effort. Three-way matching and invoice matching can be labor-intensive for both sides, so plan for that resource load before rollout.

Use one rule throughout this guide: if a payment-derived input cannot be checked against trusted records, treat it as non-decision-grade until it is verified. With that rule in place, the next step is making sure your operating trail is complete enough to support a launch.

For more on keeping contractor payment details accurate, see Vendor Data Management: How Platforms Keep Contractor Payment Details Accurate and Compliant.

What to prepare before you change matching logic#

Do not launch a ranking change until your payment trail is inspectable and your exception handling has a clear owner. If you cannot trace how an invoice moved to payment and then to deposit reconciliation, your impact read will rest on partial evidence.

Step 1: Confirm end-to-end payment event access#

Make sure product and ops can see the same event chain from digital invoice through payment and reconciliation. Use concrete checkpoints your systems already expose: digital invoice checkpoints, method-level payment events, including ACH and card, and reconciliation records for deposits that do not line up. If those records are split across tools, document exactly where each event lives before you change logic.

Step 2: Name owners for recurring payment exceptions#

Give clear owners to the exception queues that can distort outcomes. At minimum, that includes late payments, missed invoices, card failures, and deposit reconciliation issues. If ownership is unclear, model decisions and operating decisions will drift out of sync.

Step 3: Build a small, auditable evidence pack#

Keep the pack narrow and reviewable: baseline matching snapshots, payment failure logs, and a few traced examples that show invoice-to-payment-to-reconciliation flow. Favor records an operator can recheck later over derived metrics that cannot be audited.

Step 4: Set launch criteria around benefits, cost, and risk#

Before rollout, evaluate the change with the same discipline you would use for integrated payments decisions: expected benefit, total cost of ownership, and risk. Treat timing and operating effort as first-class constraints, and do not assume success. The goal is not a persuasive upside story. It is a change you can defend operationally.

If your platform uses contractor financial data in California, see CCPA for Platform Operators: How to Handle Contractor Financial Data Under California Law.

Define match quality and prove causality before optimization#

Once the event trail is inspectable, lock down what a better match means and test whether a candidate signal is part of the reason outcomes changed. Correlation alone is not enough to justify a launch.

Step 1#

Define success outcomes before the test starts, then lock each definition so results cannot be reinterpreted later. Keep those definitions consistent across comparison groups.

A compact scorecard helps keep this disciplined:

| Outcome | Definition (locked pre-test) | Baseline (unchanged group) | Decision note |

|---|---|---|---|

| Primary outcome | Team-defined, unchanged during test | Measured before launch | Do not relabel mid-test |

| Secondary outcome | Team-defined, unchanged during test | Measured before launch | Interpret with the primary outcome |

| Risk outcome | Team-defined, unchanged during test | Measured before launch | Worsening can override lift elsewhere |

| Context metric | Team-defined operational metric | Measured before launch | Context only, not causal proof |

Step 2#

Run a side-by-side comparison between the unchanged model and the signal-augmented model, and document assignment rules up front. Keep cohort construction and observation rules stable enough that any difference you see remains interpretable later.

Step 3#

Do not stop at whether outcomes moved. Ask what likely drove the change. In causal decomposition terms, differences between groups may come from differences in mediator distributions, so an intermediate payment signal can be a mediator rather than direct proof that matching improved.

Be careful with restrictive assumptions. Methods that effectively reduce the problem to one mediator, or assume mediators are conditionally independent, can misstate attribution when signals interact.

Step 4#

Stress-test attribution before launch. Sensitivity analysis belongs in this workflow, but keep conclusions provisional unless those checks are strong.

A practical checkpoint is to pair the comparison readout with simulation and applied evaluation, then check whether the conclusion holds when mediators are correlated and interacting. If the story changes materially under those checks, keep iterating before rollout. These methods support attribution testing, but domain-specific validation is still required before treating effects as proven in contractor matching.

Build the payment signal map by market and vertical#

Prioritize market-vertical pairs where payment data is auditable, compliance gaps are explicit, and pricing assumptions are current. Opportunity alone is not enough.

Step 1 Build a rail matrix with facts, unknowns, and owners#

Build one matrix per market with rows for ACH, local bank rails, and Virtual Accounts. Score only what you can verify now. Mark settlement speed and reliability as unknown until provider docs and your own logs confirm them.

| Rail or method | What you can score now | What you must verify locally | Red flag |

|---|---|---|---|

| ACH | If relevant to your flow, Stripe lists ACH Direct Debit at 0.8% with a $5.00 cap | Settlement timing, return behavior, and event coverage in the target market | Assuming US ACH economics or event coverage apply elsewhere |

| Local bank rails | Country-specific payment method pricing may override generic assumptions | Availability, payout timing, exception handling, and ledger joinability | Sales material is the only source |

| Virtual Accounts | Include only if deposits, balance moves, and payouts are traceable end to end | Local availability, reconciliation behavior, and exception visibility | Funds move but the event chain is not auditable |

Revalidate fees before scoring. Stripe states pricing can change, and country-specific payment-method pricing can supersede generic tables.

If you use Stripe Connect with platform-handled pricing, include $2 per monthly active account plus 0.25% + 25¢ per payout in the model. Stripe defines an active account as one that receives a payout in that month, and a payout occurrence is counted each time funds are sent to a bank account or debit card.

Step 2 Map vertical-specific signals before treating them as ranking inputs#

Start with observable payment states only: invoice issued, payment confirmed, funds held, milestone released, payout attempted, payout settled, payout failed, dispute, and reversal. Treat milestone-release or escrow-like events in Stripe-style flows as candidate signals only after they are consistent, comparable, and auditable in that vertical.

Do not port signals across verticals just because they seem intuitive. If two events carry different business meaning, for example managed transaction events versus lead-fee events, treat them as different evidence classes.

Use one hard gate per signal: can this event be traced to both ledger and contractor payout records without manual spreadsheet joins? If not, exclude it from launch prioritization.

Step 3 Add the market overlay for tax and onboarding friction#

Even when payment telemetry looks strong, add a market overlay: VAT treatment status, required contractor documentation, onboarding steps, and exception ownership. If a requirement source is missing or outdated, mark the pair unresolved instead of guessing.

| Setup model | Listed fees | Note |

|---|---|---|

| standard Stripe | 2.9% + 30¢ for domestic cards | Use in the final cost sanity check before ranking |

| Managed Payments | 3.5% per successful transaction, in addition to standard Stripe processing fees | Listed methods may also add 1.5% for international transactions plus 1-2% if currency conversion is required |

| Stripe Connect (platform-handled pricing) | $2 per monthly active account; 0.25% + 25¢ per payout | An active account receives a payout in that month; each payout occurrence counts when funds are sent to a bank account or debit card |

For each pair, keep an evidence pack with current pricing snapshots, provider terms, onboarding document list, payout eligibility notes, and market-specific policy exceptions. Also record the setup model - standard Stripe, Managed Payments, or Stripe Connect (Stripe-handled vs platform-handled pricing) - because the cost stack and ownership differ.

Example cost impact to capture directly in the sheet: Managed Payments charges 3.5% per successful transaction in addition to standard Stripe processing fees, and listed methods may also add 1.5% for international transactions plus 1-2% if currency conversion is required.

Step 4 Score pairs for integrity first and speed second#

Use these as directional triage checks, not fixed thresholds:

- Signal completeness: higher when key events are consistently named and tied to ledger plus payout records.

- Compliance burden: higher when tax, documentation, onboarding, or ownership inputs are unresolved.

- Time-to-value: slower when pricing responsibility, country-specific method pricing, or payout economics still need redesign.

This is prioritization, not proof. If signal integrity is low or compliance inputs are unresolved, defer the pair even if headline opportunity is strong.

Run a final cost sanity check before ranking. Stripe standard pricing lists 2.9% + 30¢ for domestic cards, but total economics can change when layered fees apply or method mix varies by buyer country, for example Klarna ranges of 2.99%-5.99%. The best first-wave pairs are the ones you can explain end to end: events, costs, and unresolved risks.

For a step-by-step walkthrough, see Platform Economy Payment Index for Contractor Payment Quality Across 20 Industries.

Set compliance gates before ranking rules#

Put compliance ahead of ranking. If Form 8938 or related foreign-account reporting status is unresolved, do not let matching boosts override that uncertainty.

Step 1 Define hard-stop gates outside the model#

Treat Form 8938 applicability as a compliance checkpoint before ranking logic runs. Confirm whether the filer is a specified person (including specified individuals and specified domestic entities), and route unclear cases for review before any uplift is applied.

For this gate, define the owner, acceptable evidence, and system behavior while the case is open. If filing status or entity classification is unclear, keep the case in neutral ranking until requirements are documented.

Step 2 Define Form 8938 readiness as states, not assumptions#

Use explicit states for Form 8938: not assessed, not required, required, in progress, filed, or exception-required. This keeps product and ops aligned without forcing ranking logic to interpret tax law.

Do not treat "filed" as complete by default. Track the applicable calendar year or tax year, whether an income tax return is required for that year, and status against the annual return due date, including extensions.

Step 3 Add cross-border reporting flags early#

Add early flags for FATCA-related reporting and Form 8938 implications so sensitive cases route to review lanes before growth ranking rules apply.

| Form 8938 item | Article fact |

|---|---|

| Purpose | Used to report specified foreign financial assets |

| Filing method | Must be attached to an annual return |

| Due date | Filed by that return's due date, including extensions |

| Year reference | Filers must identify the applicable calendar year or tax year |

| No return required | If no income tax return is required for that year, Form 8938 is not required for that year |

| Specified domestic entity thresholds | $50,000 on the last day of the tax year or $75,000 at any time during the tax year |

| Related reporting | Filing Form 8938 does not remove possible FinCEN Form 114 (FBAR) obligations |

Form 8938 is a concrete checkpoint, not a vague risk label. It reports specified foreign financial assets, must be attached to an annual return, and is filed by that return's due date, including extensions. Filers must identify the applicable calendar year or tax year, and if no income tax return is required for that year, Form 8938 is not required for that year.

Keep threshold handling context-specific. IRS materials note higher thresholds can apply in some situations, and for certain specified domestic entities the cited thresholds are $50,000 on the last day of the tax year or $75,000 at any time during the tax year. Also, filing Form 8938 does not remove possible FinCEN Form 114 (FBAR) obligations.

Step 4 Route unresolved cases to neutral ranking#

When filing context is missing, stale, or disputed, default to neutral ranking. Do not apply compliance-derived boosts until filing requirements, status states, exception ownership, and cross-border flags are current and complete.

Choose your infrastructure model for matching quality#

After compliance gates are set, choose the payment model that lets you prove control and traceability first, then optimize for speed. If you are expanding across multiple countries or handling complex tax-document flows, prioritize tighter checkpoints until payout operations are stable.

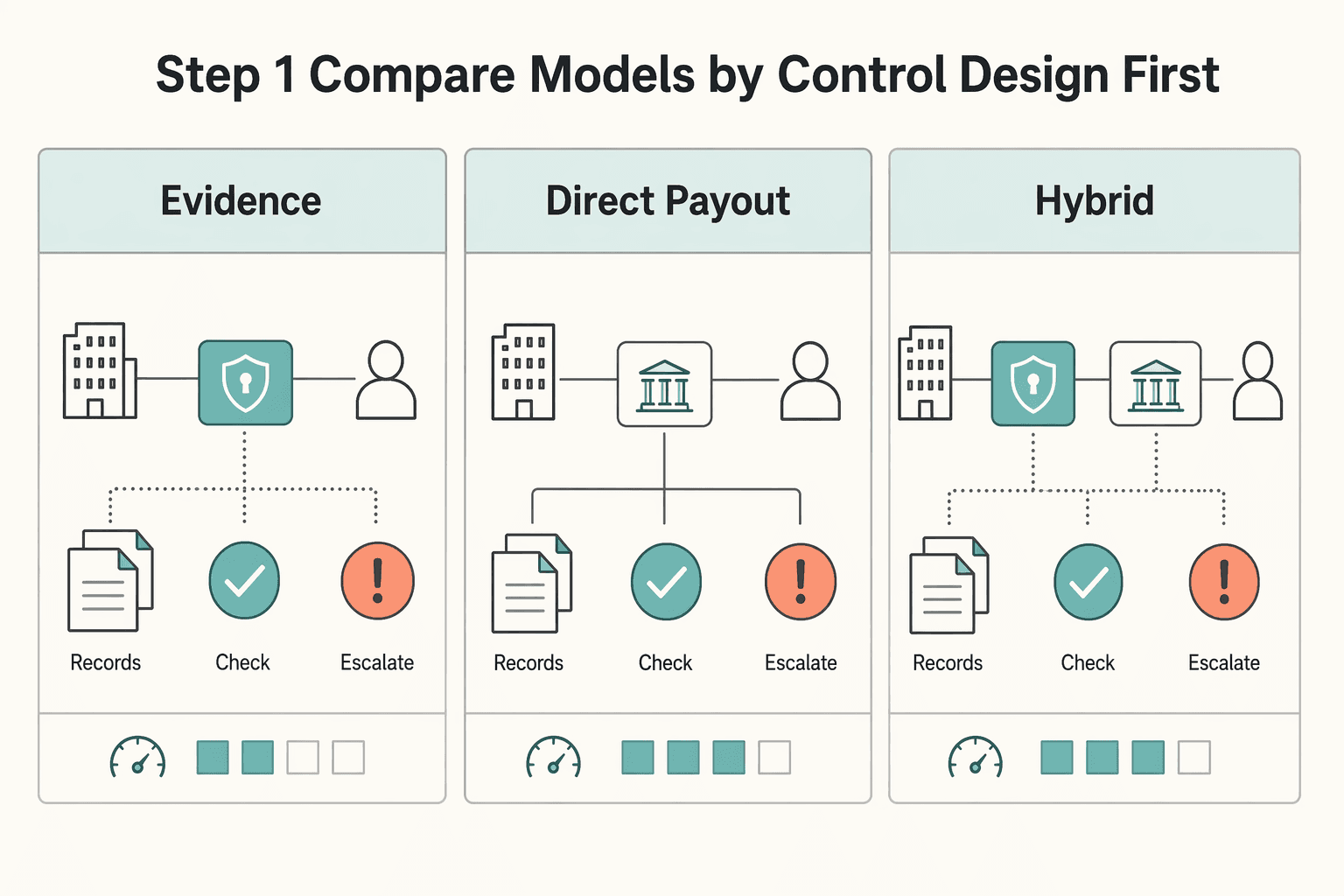

Step 1 Compare models by control design first#

Treat Merchant of Record, direct payout orchestration, and hybrid structures as different control layouts. Use launch speed only as a secondary filter.

| Model | Control posture | Liability surface | Launch-speed tendency | Reconciliation and traceability check |

|---|---|---|---|---|

| Merchant of Record | Define where prepayment and post-payment controls run | Define who owns approvals, holds, and reviews | Validate against pilot timelines and constraints | Confirm payment request, review status, and payout status are visible in an auditable event trail |

| Direct payout orchestration | Define where prepayment and post-payment controls run | Define who owns approvals, holds, and reviews | Validate against pilot timelines and constraints | Confirm prepayment checks, post-payment checks, and exceptions are captured in an auditable event trail |

| Hybrid | Define control handoffs across provider and internal systems | Define ownership at each contract and system boundary | Validate against pilot timelines and coordination overhead | Confirm handoffs are explicit and auditable across systems |

Step 2 Apply a simple decision rule#

If country coverage and tax complexity are high, favor the model where approvals, holds, reviews, and reconciliation are most traceable in practice. Move to a looser structure only after those checkpoints run consistently.

Step 3 Validate payment integrity before scaling matching logic#

Do not judge model fit from conversion signals alone. Include prepayment controls, post-payment controls, exception handling, and end-to-end visibility in the decision. Confirm you can trace events from payment request through payout status with a documented event trail.

Instrument the full data path from invoice to payout#

Instrument payment data end to end before you use it for downstream analysis. If you cannot reliably trace records from invoice and approval flow through payout outcomes, your inputs can drift from operational reality.

Step 1 Define a shared event path your teams can follow#

Define one shared set of payment events across invoicing, approvals, payout operations, and reporting, then map each event to one system of record and timestamp. The exact labels can vary by platform, but consistency matters more than naming style. Finance, ops, and product should be reading the same lifecycle.

That is what keeps remittance timing, payment history, and traceability usable for decisions instead of forcing manual reconstruction.

Step 2 Track retries carefully when they occur#

Payment systems can generate retries or replays. Label those events clearly so reporting does not count repeated deliveries as separate business outcomes. The exact control method can vary by platform, but the goal is consistent interpretation across teams.

Step 3 Reconcile analytics views against ledger records#

Reconcile dashboard-level payment views with ledger-synced records on a regular cadence. Ledger synchronization is a strong control point for data quality, especially when workflows span multiple tools. If totals or statuses do not align, resolve the gap first so reporting stays grounded in auditable records.

Step 4 Reduce fragmentation so audit trails stay complete#

Fragmented approval flows and manual follow-up create delays and weaken audit evidence. Centralizing onboarding, compliance, tracking, and payment workflows helps reduce missed handoffs and incomplete records. Keep downstream analysis focused on payment-state signals that stay traceable through review and audit.

If you are tightening the underlying records first, Vendor Data Management: How Platforms Keep Contractor Payment Details Accurate and Compliant is a useful companion.

Run a controlled rollout by country and contractor cohort#

After you can trace service and payment flows end to end, roll out in a narrow slice first. Start with one vertical, one country cluster, and one bounded contractor cohort before expanding.

Step 1 Bound the test so comparisons stay clean#

Define the cohort before launch and keep operating conditions as comparable as possible. Use a phased test window so legacy and new paths can be compared like for like, without unrelated changes muddying the readout.

Step 2 Set stop conditions and fallback before go-live#

Write fallback triggers in advance, assign ownership, and treat them as operating guardrails, not debate topics. If the new path creates friction, pause the cohort and route it back to the legacy path.

Step 3 Use one shared scorecard for consistent checkpoints#

Compare legacy and test cohorts using one scorecard with the same cohort definitions and source totals. Track outcomes and cost-effectiveness, along with payment-model performance, so gains in one area are not hiding strain in another.

Step 4 Segment results before claiming improvement#

If improvement appears only in a narrow cohort, report it that way and retest before making broader claims. The practical takeaway from segmented service-stream approaches, including the 2019 NEST trial context, is to test by cohort, compare like-for-like groups, and keep a fallback path rather than assuming platform-wide lift.

Common failure modes and recovery paths#

Many failures at this stage are control failures, not signal failures. Treat any apparent lift as unproven until it survives a check against source records.

Step 1 Re-check quality before you trust volume growth#

Higher paid volume is not enough to claim better matching. Before expanding, re-check the same cohort and time window for completion, cancellations, disputes, and payout failures.

Use ledger-linked outcomes, not dashboard totals alone. If paid volume rises while completion is flat or disputes increase, treat it as an operating shift, not evidence of better matching.

Step 2 Audit synced records against the source of truth#

Ranking issues can reflect process friction or poor record quality in synced data, not only model behavior. If you ingest provider syncs, audit them against invoices, contracts, and supporting documentation in source ledgers.

Start with the four most problematic process steps in your own workflow, then fix those before tuning ranking logic.

Step 3 Hold market expansion if tax operations are not ready#

Consider delaying expansion in markets where tax-document operations are not live. If foreign contractor payouts may trigger IRS reporting, confirm your Form 1042-S process is operational before applying ranking boosts.

At minimum, verify ownership for withholding decisions, record retention, and electronic filing readiness under the 2026 instructions, including FIRE retirement and IRIS. If these controls are manual or unclear, treat ranking changes as provisional until the documentation path is stable. For implementation detail, see IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments.

Step 4 Treat vendor claims as prompts, not proof#

Treat PLMBR, Slash, or iWallet claims as hypotheses, not launch evidence. Scale only after your own cohort readout shows matched control windows, outcome deltas, and source-auditable records.

Know when payment data should not drive matching#

If coverage is uneven, payment signals should not be primary ranking inputs. Incomplete capture can create false confidence before it improves matching.

Step 1 Exclude signals when market coverage is not comparable#

Do not rank across markets until key payment data is captured in a comparable way. If one market reports fewer or different fields than another, ranking can reflect instrumentation differences more than contractor quality.

Use a simple completeness grid by market and vertical. Treat consistency as a reporting-discipline check, not a best-effort sync: under MAS, Transactional Data Reporting is mandatory as of Refresh 31, runs through the Sales Reporting Portal, and expects up to 19 elements each month. Even if that rule does not directly apply to your platform, it is a practical bar for deciding whether capture is reliable enough to use in ranking.

Step 2 Downweight markets with unstable reporting#

In early markets, treat incomplete payment-data signals as gating context, not ranking fuel. When coverage and exception patterns are still unstable, those signals can reflect process friction more than contractor fit.

Check stability before volume. If data still shows frequent gaps, inconsistent fields, or unresolved states, keep these signals secondary.

Step 3 Fix data-access bottlenecks before tuning rank#

If data-access issues dominate operations, fix that throughput first. Otherwise, matching changes can make acceptance metrics look better while access bottlenecks remain the real constraint.

Treat apparent lift as operationally confounded until access issues are controlled. Data access problems are a known root-cause risk in payment-integrity work, so fix that layer before claiming matching gains.

Step 4 Prefer rules you can explain and audit#

When finance, ops, or compliance may need to defend ranking decisions, favor simpler, auditable rules over marginal model lift. Tie eligibility and boosts to clear payment states you can trace to source records.

If a boost cannot be explained in one sentence and traced back cleanly, keep the signal secondary until the data path is stable.

For broader market-by-market validation, revisit the Platform Economy Payment Index for Contractor Payment Quality Across 20 Industries.

Use this copy and paste checklist before expansion approval#

Approve expansion only when each item is backed by records, owners, and an audit trail, not confidence in the narrative.

| Approval check | Requirement |

|---|---|

| Baseline/test windows and cohort rules | Defined before lift comparisons, with one scorecard owner |

| Four-question checkpoint | Answerable for sampled payees with current ownership |

| W-9 and TIN Matching controls | W-9 intake sequence, TIN Matching, state controls, and exception ownership are documented |

| W-8, withholding, and 1042-S paths | Documented where relevant and verified against official sources |

| Failed checks | Route to a named, owner-assigned exception queue instead of inbox-only handling |

Step 1 Verify cohorts and ownership before you discuss lift#

If you discuss lift, define baseline and test windows up front, keep cohort rules consistent, and assign one owner for the scorecard.

Step 2 Require record-level auditability before accepting matching claims#

Do not approve matching-related claims unless the team can show auditable records with clear ownership. Use the four-question checkpoint on a sample payee: when the request went out, whether it was submitted, whether it passed validation, and who owns the record now.

Step 3 Confirm tax-document controls are explicit#

For U.S. contractor-pool operations, require this sequence: signed Form W-9 captured, TIN Matching run, then record approved. Keep intake states separate - received, validated, approved - and route failed checks to a named exception queue with an owner.

For W-8 and withholding branches, treat documentation as scope confirmation, not proof that eligibility logic is fully decided. If 1042-S handling is in scope, verify filing details against official sources. IRS Publication 1187 (Tax Year 2025) is an implementation reference, and summary pages are not legal authority.

Step 4 Name ownership boundaries before approval#

Document who owns request delivery, validation, approval, and exception remediation. Do not rely on inbox-only handling for failed checks.

Step 5 Require exception readiness before expansion#

Expansion is not approved if exception handling is informal. Failed checks should route to a named queue with an owner, and teams should be able to answer the four checkpoint questions quickly for sampled payees.

Use this checklist:

- Baseline/test windows and cohort rules are defined before lift comparisons, with one scorecard owner

- Four-question checkpoint is answerable for sampled payees with current ownership

- W-9 intake sequence, TIN Matching, state controls, and exception ownership are documented

- W-8/withholding/1042-S paths are documented where relevant and verified against official sources

- Failed checks route to a named, owner-assigned exception queue instead of inbox-only handling

If any line lacks evidence, treat expansion as not approved.

Review your implementation baseline for audit trails, webhooks, and idempotent retries before locking the rollout checklist. If ownership boundaries are still fuzzy, the breakdown in Building a Multi-Tenant Payment Platform with Defensible Data Isolation may help clarify system responsibilities.

Conclusion#

Payment data can improve matching when events are complete, auditable, and tied to outcomes that remain reliable after errors, delays, and disputes are accounted for. If you cannot explain a ranking signal from source event to business result, do not scale it.

Step 1#

Treat payment signals as context, not magic. Evidence indicates payment-system fit depends on project environment, and in complex environments milestone payment and payment on completion can be more appropriate. A payout pattern is useful only when it matches the work context you are ranking for.

Keep payment data in a supporting role unless that alignment is clear. If the job depends on staged completion, proof points, or a final handoff, use release timing and completion behavior as context rather than standalone proof. If the work is simple and repeatable, structured matching inputs may carry more weight.

Step 2#

Instrument the trail before you trust the signal. A usable signal is not just that money moved. It is an event you can trace from invoice to payment record to accounting ledger, then verify without heavy manual repair. A practical checkpoint is whether deposits can be matched to invoices quickly and consistently.

A known failure mode is keeping payment collection and accounting siloed. When that happens, dashboards can look cleaner than the underlying records.

Step 3#

Test for outcome lift, not operating convenience. Smoother payouts may improve contractor experience, but that alone does not prove better matching. You still need side-by-side cohorts and outcome measures that show the change did more than move friction downstream.

Stay conservative about what the evidence shows. The April 2019 payment-system research is useful for fit and operating logic, but it does not prove platform-wide causality across industries and explicitly calls for further testing. Treat payment signals as a hypothesis to test, not a shortcut to a product claim.

Payment data should complement, not replace, structured matching inputs. Structured job requirements and detailed profiles improve transparency, and payment evidence is strongest when it validates execution reliability on top of that structure.

Step 4#

Scale only after your explanation survives audit and failure review. Before broad rollout, answer four plain questions: what event created the signal, where it is recorded, how it is checked against invoices, and which business outcome it is meant to influence. If any answer is vague, keep the signal out of expansion.

Operational red flags matter as much as statistical ones. Manual invoice handling can create errors, delays, and disputes. When that is true, adding those records into ranking logic will scale process noise, not matching quality.

That is the sequence: gates first, instrumentation second, controlled tests third, scale last. Keeping that order makes payment-data matching decisions easier to defend.

If you still need to confirm market and program coverage before launch, talk with Gruv.

Frequently Asked Questions

Can payment data actually improve contractor matching, or does it mostly improve operations?

Payment data usually improves operations first. Use it for matching only after it maps to measurable marketplace outcomes. If it mainly reveals payout friction or verification gaps, fix operations before making stronger matching claims.

Which payment signals are usually most predictive of match success in contractor marketplaces?

There is no universal list of predictive payment signals. Start with signals tied to execution reliability and payment-schedule fit for the job type, such as milestone, percent-complete, or time-interval schedules when they are comparable and auditable. Treat payout speed as one signal, not proof of match quality.

What metrics should we publish internally before claiming better matching performance?

Publish baseline and test cohort results side by side using the same cohort rules and time windows. Include both matching outcomes and payment-operation outcomes so gains are not just shifted friction. If an improvement cannot be traced to auditable payout records, do not present it as proof of better matching.

How do `KYC`, `KYB`, and `Contractor Classification` rules limit matching strategy in new countries?

Treat KYC, KYB, and contractor classification as eligibility gates before any ranking boost applies. If verification, business checks, or classification review is incomplete, keep exposure neutral until those checks are complete. This matters even more in new countries, where added rails, currencies, tax requirements, and workflows can increase operating load quickly.

When should we prioritize escrow-like assurance over payout speed or payout cost?

There is no universal priority rule. Prioritize assurance-oriented release structures when trust depends on milestone release or staged completion, even if they are slower or costlier. If disputes cluster around completion status, assurance may be worth prioritizing, while stable payout reliability can make speed and cost more important.

How can we test matching changes without exposing the business to compliance or tax risk?

Run tests only on contractors who have already passed the required verification path. Maintain an auditable trail from onboarding through payout outcome before experiment entry, and use code-based account confirmation with required registration fields before activation. If verification or exception routing is still manual, keep that cohort in neutral ranking.

Avery writes for operators who care about clean books: reconciliation habits, payout workflows, and the systems that prevent month-end chaos when money crosses borders.

Sources

- access-board.gov/adatrusted

- acquisition.gov/afars/chapter-5-definitionstrusted

- acquisition.gov/far/part-31trusted

- congress.gov/crs-product/R48296trusted

- department.va.gov/procurement-acquisition-and-logistics/nation...trusted

- dgs.ca.gov/-/media/Divisions/OLS/Resources/SCM-VI---04-...trusted

- ecfr.gov/current/title-13/chapter-I/part-124/subpart-Atrusted

- eda.gov/sites/default/files/filebase/files/tools/gra...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade:

Spain Digital Nomad Visa Guide: Requirements, Application & 2026 Updates

Stop collecting more PDFs. The lower-risk move is to lock your route, keep one control sheet, validate each evidence lane in order, and finish with a strict consistency check. If you cannot explain your file on one page, the pack is still too loose.