Quick Answer

Start with a strict incident taxonomy and run one first-day sequence every time: clean case language, verify state across API, provider, and Ledger, then escalate on missed SLA checkpoints. The marketplace payout error reduction interview shows that complaint signals are useful for symptom mapping, but expansion decisions should depend on whether teams can classify failures, assign owners, and close exceptions with auditable evidence rather than ad hoc retries.

Founders rarely lose a new market because nobody wants the product#

Founders rarely lose a new market because nobody wants the product. They lose when money movement stops behaving the way the launch model assumed. Demand can look healthy right up to the point where sellers, hosts, or contractors start asking why a payout is late, missing, or stuck in review. Then the team realizes it does not yet have a clean answer.

That is the premise of this marketplace payout error reduction interview. The goal is not to retell payout horror stories for effect. It is to turn the anecdotal evidence operators actually see in public marketplace discussions, including interview-style and editorial pieces like Sharetribe's season recap, Stripe Atlas's marketplaces guide with Andrew Chen, and PaymentsJournal's BNPL dispute-prevention coverage, into decisions you can use before committing to a corridor, vertical, or payout setup.

There is an evidence boundary worth stating up front. Public complaints are useful because they show symptoms. People describe delays, unclear status messages, repeated document requests, or support loops that never resolve. They do not prove root cause on their own. A payout that looks "failed" from the user side might be a compliance hold, a profile mismatch, a provider-side reject, a reconciliation gap, or simply a status lag between one layer and another.

That distinction matters because marketplace teams often overreact to the visible surface. They add support headcount before they fix evidence packets. They blame a provider before checking their own beneficiary data. They call a market attractive because supply signs up quickly, then discover that verification, compliance, or payout-data edge cases make payout operations too brittle to scale. Once that happens, the commercial plan is no longer the binding constraint. Operations is.

Here is the practical promise. You should leave with four things you can use right away: an incident taxonomy that separates lookalike payout failures into workable categories, a first-day triage sequence for delayed or failed disbursements, a set of prevention controls to put in place before volume goes live, and a market-by-market checklist for deciding whether to launch, delay, or redesign. If you are evaluating expansion, the useful question is not "Can we turn payouts on?" It is "Can we explain, reconcile, and recover the failures we already know will happen?"

That is the lens for the rest of the piece: less marketplace folklore, more operator judgment. For a step-by-step walkthrough, see Payout Error Rates in Contractor Payroll Teams Can Actually Reduce.

What payout error reduction means in operator terms#

In operator terms, payout error reduction is only real when repeat incidents decline across payout cycles, not when reporting merely looks cleaner. Keep one incident taxonomy and measure outcomes against that same scope every cycle.

Run incident review across separate checkpoints, and do not treat one status as proof of another: API acceptance, payout-partner execution state, and Ledger reconciliation state. Use the same case ID and timestamps so you can trace each delayed case end to end.

Use a strict decision rule in reporting: fewer tickets alone is not operational improvement if unresolved SLA breaches continue to age. Faster first response is helpful, but it is not a substitute for confirmed release, clear reject reason, or a closed reconciliation outcome.

Keep scope broader than technical rejects. Include KYC and AML policy-gate blockers in the same incident set, label cause clearly, and then route prevention work to the layer that actually failed.

With that scope set, the next step is to classify incidents in a way that helps you act before a new market goes live.

Related: How Accommodation Rental Platforms Pay Hosts: Payout Architecture for Short-Term Rental Marketplaces.

Incident taxonomy you can use before entering a market#

Before you enter a market, use an incident taxonomy that starts with observable symptoms and only then assigns root cause. If early cases cluster around profile or data mismatches, prioritize identity and profile normalization before adding another payout rail, provider, or support queue.

Start with observable symptoms#

Start with what you can verify in complaints, tickets, and rejected cases, not with guessed causes. A practical first pass is:

| Incident class | Observable symptom |

|---|---|

| Profile or data-state mismatch | Platform profile, payout beneficiary record, or account state does not line up. |

| Settlement-delay case | Payout appears accepted but misses the expected release window. |

| Support-follow-up failure | Case stalls because current status, owner, or next action is unclear. |

Treat this as a symptom map, not proof of cause. A Facebook Marketplace prompt notes that "many sellers don't mark items as sold," which is a useful reminder that system state can drift from real-world state.

For sampled incidents, compare account identity, beneficiary details, document state, and last status timestamp across product, payout, and support records. If they do not align, classify the incident as mismatch until reconciled.

Split policy holds from data defects#

Keep review and hold categories separate from data defects. In practice, that means distinct classes for verification holds (for example KYC/KYB), policy screening (for example AML or sanctions review), and document-state mismatches, even when the user only sees "under review."

This keeps triage grounded in evidence instead of retries. One marketplace strategy source frames the launch principle directly: trust infrastructure should be designed before launch, not after the first incident.

Keep tax and reporting dependencies separate#

Give tax and reporting issues their own lane. Where relevant, track missing W-8, missing or inconsistent W-9, VAT status mismatch, and dependencies such as Form 1099 setup as separate classes.

| Dependency | Separate class to track |

|---|---|

| W-8 | Missing W-8 |

| W-9 | Missing or inconsistent W-9 |

| VAT | VAT status mismatch |

| Form 1099 | Form 1099 setup dependency |

IRS Publication 5838 (Rev. 10-2025) separates a Quality Review Checklist step from Working Tax Return Rejects; use the same distinction in payout ops so review-state and reject-state issues are not merged into one catch-all bucket. If one market is dominated by profile and document mismatches, pause rail expansion until identity, tax, and document records are normalized.

Once these classes are stable, triage becomes repeatable and launch decisions get clearer. For a category-specific version, see Building a Virtual Assistant Marketplace with Operable Payout and Tax Controls.

The first day triage sequence that prevents repeat failures#

On day one, prevent repeat failures by enforcing three controls before any retry or escalation: shared definitions, named timing checkpoints, and explicit action limits. Without those, teams create avoidable rework and inconsistent case handling.

Freeze action until the case language is clean#

Start by aligning the terminology in the case record. The source material shows why this matters: one source uses Article 2. Abbreviations, Acronyms, and Definitions, and another uses CHAPTER 2 - DEFINITIONS. Use the same discipline in payout triage so every team is working from the same status language.

Before you act, confirm the case includes:

- one current status label

- one owner

- latest timestamped status history

- the exact record version under review (if a profile or document check is involved)

If any item is missing, finish record cleanup first.

Apply timing checkpoints before escalation#

After the status language is clean, route the case by your existing incident classes and work against named timing checkpoints. A useful process model in the source material is 3.2.4 Timing of Enrollment: define when a case is still in normal processing, when it becomes an exception, and when escalation is required.

Enforce action limits for frontline handling#

Use explicit limits for what first-line triage can change or retry, similar to the control pattern in 5.1.3 Procurement Card Dollar Thresholds and Limitations. If a requested action is outside that limit, escalate with a structured evidence pack instead of ad hoc notes.

| Failure signal | Required evidence | Owner | Escalation trigger | Customer-safe status message |

|---|---|---|---|---|

| Status terms conflict across records | Current status, timestamped prior states, assigned owner | Operations triage | Conflict remains after initial reconciliation pass | We are verifying the current processing status before taking the next step. |

| Case record is incomplete | Case ID, current owner, next action, missing fields list | Support operations | Required fields still missing after first review | We are consolidating your case details so the next action is accurate. |

| No state change past named checkpoint | Checkpoint name, current state, last action timestamp | Escalation owner | State unchanged after the documented checkpoint | We are escalating this case because it has passed our normal processing checkpoint. |

| Requested action exceeds frontline limit | Requested action, applicable limit, approval path | Team lead or escalation owner | Action cannot be completed within first-line authority | Your case is being routed for the required review before we proceed. |

If you cannot define the state, point to the timing checkpoint, and show the limit that governs the next action, triage is not ready yet.

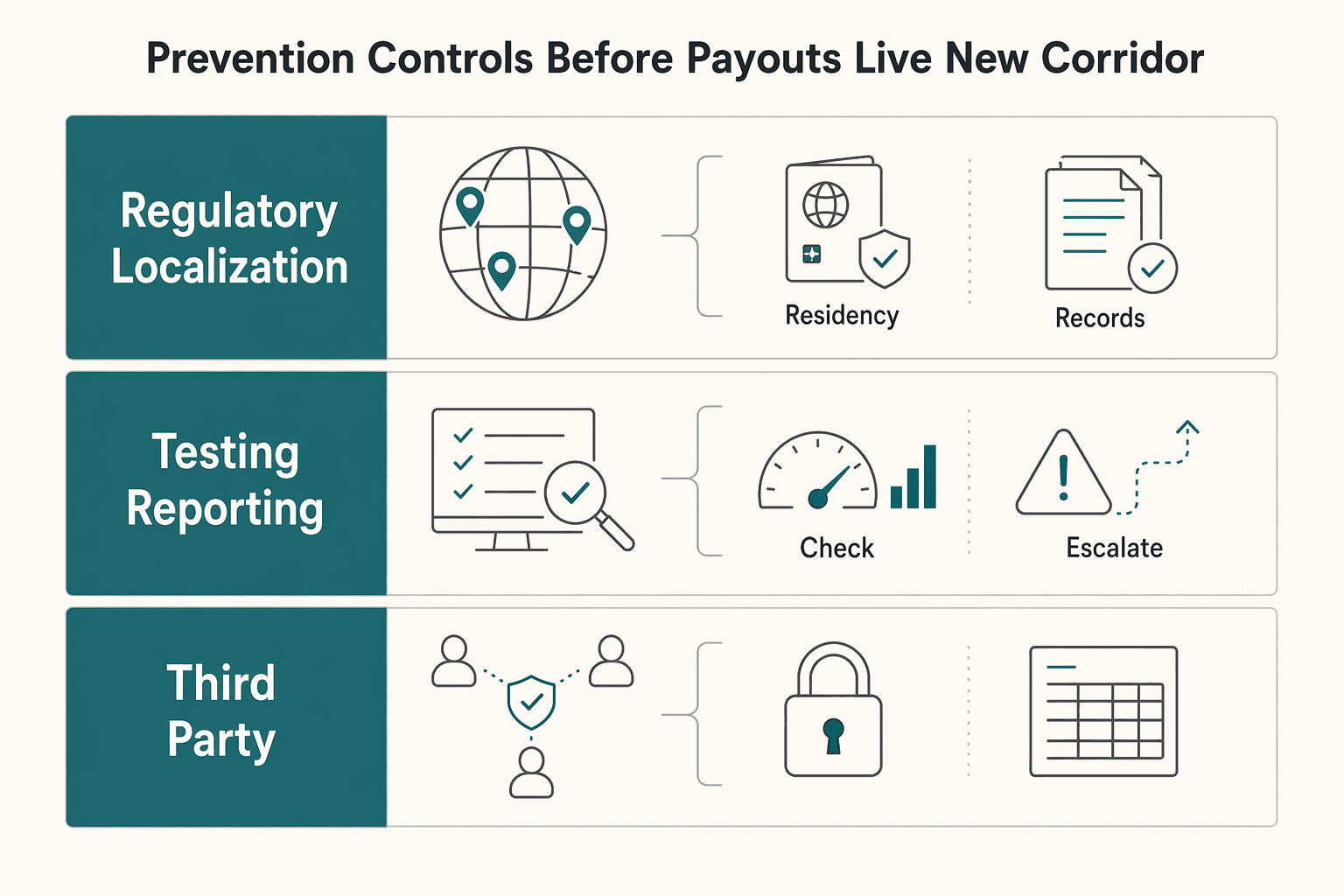

Prevention controls before payouts go live in a new corridor#

Do not scale payouts in a new corridor until you have proven localization, testing, and governance controls with auditable evidence. The 2026 compliance outlook is clear: rules are fragmented across regions, requirements are increasingly local-policy driven, and supervisors expect stronger real-time reporting, testing, and third-party governance.

Before launch, your pre-flight check should confirm:

| Control area | What to prove before broad release |

|---|---|

| Regulatory localization | The corridor-specific control set is defined and enforced, including AML/KYC, sanctions, data-residency, and required tax-profile state. |

| Testing and reporting readiness | You can show documented testing outcomes and reliable reporting for normal payout flow and exception handling. |

| Third-party governance | Provider responsibilities, escalation paths, and closure evidence are explicit for each failure class before volume increases. |

The practical standard is evidence, not confidence. If you cannot show that corridor requirements are operationally covered and exceptions can be closed with a clear owner and audit trail, keep rollout constrained until you can. For third-party seller payouts, see eCommerce Reseller Payouts: How Marketplace Platforms Pay Third-Party Sellers Compliantly.

Expansion decisions by market should be operations-first#

Pick the market you can run reliably, not just the one with the biggest demand forecast. In platform terms, growth and scaling are related but different: growth adds users and value, while scaling means adding revenue without matching cost growth, and that shift requires explicit decision rules.

A practical rule: if a market is likely to add recurring payout exceptions faster than it adds durable revenue, treat it as growth pressure, not a scaling step. That keeps expansion decisions tied to operating reality instead of launch momentum.

Compare markets by operational burden, not excitement#

Compare candidates on three items first: compliance workload, tax-document workflow burden, and support-case complexity. The question is whether most payout issues stay standard and diagnosable, or whether they become ambiguous and investigation-heavy.

Before you mark a market ready, test whether your team can quickly reconstruct payout outcomes from records and statuses with clear ownership. If evidence is hard to retrieve in testing, live exception handling will usually be slower and noisier.

Lower conversion can still be the better launch#

When two markets are close commercially, a lower-conversion market can still be the better first launch if payout operations are more predictable. High demand does not offset chronic exception load if case ownership and closure paths are unclear.

This also aligns with marketplace operating reality: expansion usually depends on building both sides of the market, especially supply, not just pushing demand.

Architecture fit changes the decision#

Architecture should match the market's operational burden. Direct payouts and a Merchant of Record model distribute ownership differently, but neither removes the need for clear controls, traceability, and reconciliation. Where supported, Virtual Accounts help only when credit, hold, and return paths are already proven operationally.

| Market scenario | Gating requirements to inspect first | Likely failure modes | Required staffing shape | Recommendation |

|---|---|---|---|---|

| Moderate demand, predictable workflows | Clear release criteria and stable document paths | Missing docs, standard profile corrections | Named ops + compliance escalation path | Go |

| High demand, heavy review friction | Multi-step checks and branching document states | Chronic holds, repeated follow-ups, aging cases | Dedicated escalation and tighter case ownership | Delay |

| Bank-transfer-led intake (where supported) | Proven credit, hold, and return handling | Funds credited but unresolved return/hold ownership | Finance/treasury + ops + reconciliation coverage | Go only after return-path proof |

For the supply-and-demand pressure behind payout decisions, see Two-Sided Marketplace Dynamics: How Platform Supply and Demand Affect Payout Strategy.

Support design that reduces backlog instead of hiding it#

Design support so the next owner can act without re-investigating the case. If first-response time improves but unresolved aging keeps growing, treat that as a routing and ownership signal first, then revisit staffing.

The market-level implication is practical: more exception classes make vague support more expensive. A queue full of "under review" tickets with weak handoff detail will hide backlog, not reduce it.

Build the escalation packet first#

Require a minimum escalation packet for every payout case instead of free-form notes:

- Case ID

- Exact Ledger reference

- Webhook timeline observed so far

- Current compliance state (for example KYC/AML state, where relevant)

- Prior action log (retries, outreach, and handoffs)

- Current document state (for example VAT, W-9, or Form 1099 status, where relevant)

Use a simple quality check: hand one delayed case to a second team without the full thread. If they cannot quickly identify whether it is a routing failure, compliance review issue, or document-state issue, tighten the packet.

Match external updates to internal checkpoints#

Avoid customer updates that mask inactivity. Tie each customer-facing status to a real internal checkpoint so progress is visible and handoffs stay auditable.

That discipline aligns with IRS Publication 5838 (Rev. 10-2025), which is structured around explicit intake/interview and quality-review steps, including a named "Quality Review Checklist." The takeaway here is process design: named review stages produce cleaner handoffs than one generic review state.

Separate queues by failure type#

Keep these queues distinct because evidence and handlers differ:

- Compliance-review cases

- Payout-routing failures

- Document-state issues

The same pattern appears in IRS Publication 5838's separate "Working Tax Return Rejects" work area: reject handling is separated from standard flow because the work is different.

One caution is worth keeping visible. A Jan 22, 2024 discussion warned that pushing everything into tickets can create "this giant icebox of stuff you'll never do." Use that as a warning sign: if reply speed looks good but aging still climbs, redesign queue boundaries, escalation packets, and ownership before adding headcount.

For dashboard design, see Build a Payout Error Rate Dashboard to Reduce Failed Disbursements.

Verification checkpoints leaders should review every week#

Review one thing first: are payouts getting cleaner at each stage, or are exceptions just moving faster? Closed-ticket volume alone will not show whether expansion risk is actually falling.

Keep the scorecard compact and explicit:

| Review area | What to verify | Why it matters | Expansion gate |

|---|---|---|---|

| API, provider, Ledger stages | Stage-by-stage success and mismatch counts | Upstream success can still fail at reconciliation | Do not expand if one stage is masking another |

| Repeat incidents | Same failure class returning after "resolution" | Closures may be cosmetic instead of durable | Hold launch if repeats cluster in one class |

| Unresolved SLA breaches | Aging cases past internal checkpoint | Signals weak ownership or escalation | No new country or vertical until aging is controlled |

| Compliance friction | KYC/KYB/AML hold-to-release and W-8/W-9 completion | Compliance delays and routing defects have different owners | Review separately before changing payment rails |

For any spike, sample real cases and verify the same escalation packet every time: case ID, Ledger reference, webhook timeline, compliance state, and action log. If leaders cannot confirm the failure path from that packet alone, reporting is too abstract for rollout decisions.

Treat replay safety as a standing audit item#

Audit webhook reprocessing and retry behavior after product changes, not just after incidents. Keep replay checks named, versioned, and hard to skip. Oracle's published approach is a useful benchmark for rigor: a stated 21-point checklist and review across security, functionality, performance, human oversight, feedback, and deployment.

Gate expansion on closure quality, not optimism#

Keep compliance friction on its own line so delays are not misread as rail failures. Then require closure artifacts by exception class before expansion. In practice, this means two controls are always clear: where errors are formally reported (an errata path) and which document/version is authoritative when records differ. If repeated incidents are not declining and aged breaches are not closing with evidence, delay launch.

For a broader marketplace payment setup comparison, see Six Marketplace Payment Setups for Two-Sided Platforms: Checkout, Payout Control, and Reconciliation.

Conclusion#

The main takeaway is simple: complaint-level symptoms are useful only if you can turn them into operator-level decisions before you scale volume, add countries, or widen operations. If you cannot translate "my payout is stuck" into a known failure class, an owner, a checkpoint, and an evidence packet, you are still guessing.

That is the thread running through marketplace interviews and recap commentary. Strong teams do not treat support noise as proof of root cause. They classify what failed, prove the current state from records, and only then decide what to fix first.

In practice, the execution order is straightforward:

- Classify failures first. Separate distinct failure classes so you are not mixing different problems into one backlog.

- Enforce triage discipline. Verify the current state from your own records and event timeline before anyone retries or manually intervenes.

- Harden prevention controls. Keep data-quality and compliance checks upstream, and make retry behavior replay-safe instead of duplicate-prone.

- Gate expansion on proven readiness. Do not launch a new corridor just because demand looks attractive if exception ownership and closure evidence are still unclear.

One useful red flag is simple. If your team says a market is ready but cannot produce a case packet with the case ID, core record references, event timeline, compliance state, and prior action log, that readiness is not verified.

This caution fits a broader lesson from marketplace interviews. A season recap framed as lessons from 11 marketplace experts and related operator commentary both point to the same risk: growth can stall when teams take on more operating complexity than they can control, including overreaching on inventory or supply management too early. A payout launch can fail the same way, not because the market lacks demand, but because the operational layer is still too loose.

The next step should be concrete. Run one market readiness review using the comparison table and the triage checklist from this article. Then make a hard call based on evidence: go if failure classes have owners and closure proof, delay if the basics are still unverified, or redesign if your current payout architecture cannot support the exception load you already see.

Frequently Asked Questions

What causes marketplace payouts to fail most often in practice?

There usually is not one pattern that fits every platform. As you add providers or countries, differences in data models, file formats, settlement timelines, and provider-specific failure modes tend to compound. At that point, reconciliation can quickly become a multi-system puzzle.

How should operators triage a delayed payout in the first day?

Start by checking the Ledger truth before you trust the UI or a provider dashboard. Then verify API acceptance, webhook order, provider status, and current compliance state so you know whether this is a routing issue, a replay problem, or a review hold. Do not manually retry until you confirm idempotency and rule out duplicate posting risk.

When should a payout delay move from support queue to formal escalation?

Move it as soon as the payout state is unchanged past your internal SLA checkpoint. Escalate it when support cannot prove the current state from the case packet alone. A vague note like “pending with provider” is not enough. If the owner cannot show the case ID, Ledger reference, webhook timeline, compliance state, and prior actions, it should be escalated.

How can teams reduce address and profile mismatch errors before payout release?

Normalize profile and beneficiary fields before payout creation, not after a payout fails. The practical check is to compare the beneficiary data in the payout request with the most recent approved profile record and block release if key fields drift. A quiet failure mode is stale seller-status data when marketplace records are incomplete or not updated reliably.

What should founders verify before entering a new country with marketplace payouts?

Check whether your current provider setup, data requirements, and reconciliation process still hold in that corridor. Faster rails may be the market expectation, but speed does not remove operational fragmentation, and reconciliation can become a multi-system puzzle very quickly. If you cannot explain who owns exceptions, how batches reconcile, and what evidence closes a case, delay launch.

How do compliance checks like KYC and AML affect payout error rates?

This grounding pack does not establish a specific error-rate impact for KYC or AML checks. Treat compliance-review holds as a separate delay category from provider execution so users are not left with a generic “payout failed” signal when the issue is actually review-state latency.

What evidence should be included in a payout escalation packet?

Include the case ID, Ledger reference, payout or transfer identifier, webhook timeline, provider status, compliance state, and a clear action log. Add the customer-safe status message already sent so escalations do not create conflicting updates. This packet should let another team verify the issue without re-investigating from scratch.

Try a related tool

Avery writes for operators who care about clean books: reconciliation habits, payout workflows, and the systems that prevent month-end chaos when money crosses borders.

Sources

- acquisition.gov/afars/chapter-5-definitionstrusted

- calbar.ca.gov/sites/default/files/portals/0/documents/rfp/...trusted

- comptroller.war.gov/Portals/45/Documents/afr/fy2024/DoD_FY24_Age...trusted

- congress.gov/committee-report/108th-congress/house-report...trusted

- dhcs.ca.gov/provgovpart/Documents/CalAIM-Eval-Design-App...trusted

- docs.cpuc.ca.gov/PublishedDocs/SupDoc/A2505009/9084/603483158...trusted

- fdic.gov/resources/supervision-and-examinations/exami...trusted

- irs.gov/irm/part4/irm_04-019-014rtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Supply and Demand Dynamics Should Set Your Marketplace Payout Strategy

In a two-sided marketplace, payout strategy is not back-office plumbing. It can shape whether sellers stay active, whether transactions complete reliably, and whether buyers can find supply that is ready to transact.

Host Payout Architecture for Short-Term Rental Platforms

Choose your payout architecture before you pick your next country. The usual break point is where host payments meet local payout-method coverage, identity checks, risk review, and finance close requirements.

How Marketplace Platforms Pay Third-Party Sellers Compliantly

Generic marketplace payout advice usually skips the part that breaks in production. Paying many sellers is not just moving money out. It is deciding who gets paid, when they become eligible, what happens when a buyer disputes a payment, and how finance proves every release later. If you are working on **ecommerce reseller payouts marketplace platforms pay third-party sellers**, this guide is for the marketplace operator, not for solo freelancer banking tips.