Quick Answer

Treat currency conversion in your payment API as payment execution, not a rate lookup. Define quote-expiry and retry rules first, then lock the request contract: server-to-server HTTPS POST with JSON where applicable, ISO 4217 currency codes, and amounts sent once as smallest-unit integers such as 10000 for 100.00 USD. Keep sandbox and production fully separated, because the same conversion retried later can legitimately return a different value as rates move.

Where Currency Conversion Fits in Your Payment API#

Currency conversion in production is a payment execution surface, not a simple rate lookup. That distinction changes how you design the entire flow.

In a real currency conversion payment API integration, request shape, authentication, and amount formatting affect outcomes. The same request made twice can also return different values as rates move. You are not integrating a timeless reference tool. You are integrating a service that converts one currency amount to another using current exchange rates.

That point drives decisions teams often leave until later. If your product shows one converted amount and later retries with a fresh request, the response may differ. If you format amounts for display and then send that same display value in the payload, you can create avoidable failures. If you treat retry behavior as a generic API concern instead of a money movement concern, you can turn one customer action into multiple inconsistent outcomes.

The right starting posture is operational, not cosmetic. Treat the request and response flow as part of payment execution from the first design review.

At integration level, the basics are concrete. A provider flow can be server-to-server HTTPS POST with JSON. Requests can require a service_command, a SHA-256 signature, and 3-letter ISO 4217 values for currency and converted_currency. Those are not optional details to clean up later. They are part of the contract that determines whether the request is accepted and whether the resulting record is trustworthy enough to reconcile.

Amount handling deserves special attention because it is such a common failure point. The amount field can be required as a positive integer in the currency's smallest unit, with max length 10. In that model, 100.00 USD is sent as 10000, not "100.00". The practical lesson is simple: serialize source amounts exactly once into the smallest unit, never as floating point and never with display formatting in the API payload.

You also need to design from the start for rate movement and edge cases tied to the rails you use. Repeated conversion calls are not guaranteed to be stable. If rates vary between requests based on market conditions, that is expected behavior, not an exception. Your quote policy, retry logic, operator playbooks, and customer messaging all need to reflect that.

Rounding is another practical issue to settle early. For three-decimal currencies, published guidance tied to Visa transactions says to round the final decimal place to zero to reduce declined-transaction risk. If your product touches those flows, this is not a polishing detail. It is part of reducing avoidable execution problems.

Finally, keep sandbox and production behavior separate in both implementation and logs from day one. Providers can publish distinct endpoints, and environment mix-ups around signing, amount encoding, or routing create discrepancies that are painful to debug later. A clean environment split makes diagnosis much easier. It lets you answer basic questions quickly: which endpoint was called, with which exact payload shape, using which credentials, and under which signing behavior.

Use this guide as an implementation decision guide, not a vendor feature promise. Coverage and behavior vary by provider, market, and program. The safest way to proceed is to lock the decisions that determine money movement, quote handling, audit traceability, and operator recovery before you start coding the happy path. For a related cost angle, see How EOR Platforms Use FX Spreads to Make Money.

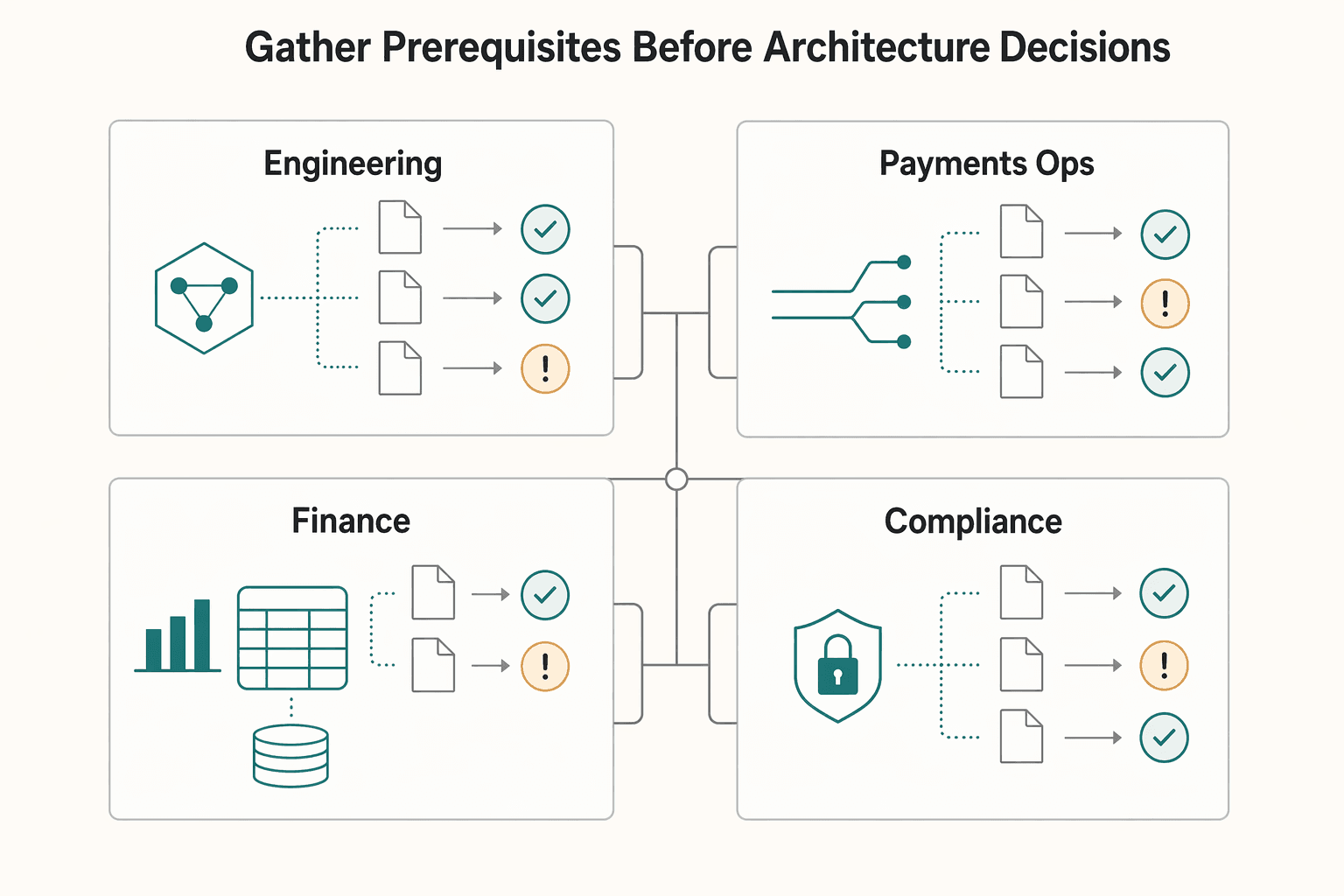

Gather prerequisites before architecture decisions#

Before you compare providers or design endpoints, decide what money movement you are actually building. Routing, transfer checkpoints, and ledger design all depend on that early choice.

| Owner | Primary areas |

|---|---|

| Engineering | request integrity; idempotency behavior; async event handling |

| Payments ops | exception review; transfer-status follow-up |

| Finance | reconciliation rules; export completeness |

| Compliance | review paths for KYC, KYB, and AML evidence or exceptions |

The first step is to pick the money movement shape in plain business terms. Start by naming the flow: Merchant of Record, direct payouts, or Virtual Accounts-led collection. You do not need final implementation detail yet, but you do need one declared shape so the team can define routing decisions and transfer checkpoints clearly.

This is where projects get easier or harder. If one team thinks the platform is collecting funds as Merchant of Record, another assumes direct payouts, and finance expects something closer to Virtual Accounts-led collection, you will not just have terminology drift. You will have different assumptions about when funds are collected, when conversion happens, who is responsible for status confirmation, and what the internal ledger should represent.

Document the flow in a way that forces agreement by specifying:

- where funds are collected

- when conversion happens

- how transfer outcomes are tracked

- how transfer outcomes are confirmed

It is simple, but it removes a lot of ambiguity. When the route is clear, later decisions about request contracts, retry behavior, and reconciliation become more concrete. When the route is vague, every later discussion turns into a proxy argument about what the transaction really is.

Routing is also a reliability decision, not a cosmetic one. It can drive payment failures, so cost and performance need to be weighed together. A route that looks acceptable in a spreadsheet can still create operational strain if it makes exception handling unclear or pushes critical confirmation steps into an ownerless gap between teams.

Use a practical checkpoint here: map one end-to-end transaction from payer to recipient and mark where transfer tracking and confirmation happen. If the team cannot agree on that path, the design is not ready for provider selection or implementation detail.

The next step is ownership. Assign owners to risk before you assign tickets. The purpose is not bureaucracy. It is to avoid predictable failure modes where everyone assumes someone else owns the non-happy-path work.

A simple ownership grid across engineering, payments ops, finance, and compliance is enough:

- Engineering: request integrity, idempotency behavior, async event handling

- Payments ops: exception review, transfer-status follow-up

- Finance: reconciliation rules, export completeness

- Compliance: review paths for

KYC,KYB, andAMLevidence or exceptions

This is a practical operating model, not a universal standard. Team names can vary. The important part is that known risk areas are explicitly owned before implementation starts. Async behavior, reconciliation risk, and compliance controls should never be left as shared concerns with no clear primary decision-maker.

Use another checkpoint here. Every external status change should have one primary owner and one escalation owner. If an external state changes and the team does not know who must act, the process is incomplete no matter how polished the API integration looks.

You also need a minimum evidence pack before build. Keep it specific and tied directly to execution and reconciliation, not to generic planning documents. That pack should include:

- required source and destination currencies

- initial payout corridors

- expected transaction types by flow

- reporting obligations and export consumers

- identifiers preserved from API request to internal record to reconciliation output

This is where the ledger requirement becomes real. If you cannot trace what finance needs to reconcile a converted payment, the design is not ready. A conversion flow is not done when the API call succeeds. It is done when the business can explain what happened, prove what happened, and match what happened across systems.

A useful way to test that is to prepare one worked example from source request through transfer confirmation, ledger entry, and export output. The goal is not to predict every exception. It is to make sure the core recordkeeping path exists before code is written around assumptions that later prove impossible to reconcile.

The final prerequisite is to freeze a few non-negotiables before code. Set policy decisions early for quote expiry handling, stale-quote rejection, and end-to-end audit traceability. You do not need a duration threshold yet, but you do need explicit behavior for what happens when a quote is no longer valid.

Because rates can move between requests, your system needs clear answers to basic questions:

- when is a displayed amount still acceptable

- when is it stale

- what happens if the user or the system retries

- what record connects the original request to the eventual transfer result

Also require traceability across asynchronous steps so teams can connect request, transfer confirmation, ledger entry, and export row without ambiguity. If that chain is broken, finance cannot reconcile, ops cannot investigate, and compliance cannot review with confidence.

A strong checkpoint is a paper test on one hypothetical transaction. Ask whether ops can explain what happened from records alone. If the answer depends on tribal knowledge, Slack history, or someone remembering what the provider usually does, the architecture still needs work.

For a practical breakdown of FX spread, fees, and total landed cost, see How to Calculate the 'All-In' Cost of an International Payment.

Choose the right API class for your payment responsibility#

Choose by responsibility, not brand. First decide whether you need network-context FX, payout execution, or reference-only rates. Then evaluate providers within that class.

| Candidate | Fit | Evidence here | Current status |

|---|---|---|---|

| Visa Foreign Exchange Rates API | Network-context FX option for Visa flows | Returns Visa conversion rates for a currency pair; rateProductCode="A" and "B" are indicative daily rates; transactionType supports Pull/Push Funds; omitted transactionType defaults to Push Funds; for BANK/WALLET flows, eligible Visa Direct clients can receive a reusable quote ID until expiry | Resolve SLA clarity, auth model, webhook/error parity, contract limits, and bundle eligibility before commitment |

| Mastercard Currency Conversion Calculator APIs | Network-context candidate that still needs verification | Confirm with the provider | Keep in evaluation status rather than implementation status |

| Currencycloud Convert Payments API | Payments-native execution candidate to verify if you own conversion execution and payout orchestration | Verify concrete behavior with the provider | Candidate to validate rather than a drop-in answer |

API classes are not interchangeable. Payment gateway and payout APIs solve different problems, so class fit should be your first filter. If you skip that step and compare vendors too early, you can waste time debating surface features while missing the larger issue: whether the provider class even matches your payment responsibility.

A useful way to frame selection is to ask what job the API must do in your system. Do you need network-context FX in payment flows? Do you own conversion execution and payout orchestration? Are you only looking for reference-style rates? Those questions matter more than brand familiarity because they determine the shape of your internal contracts and the operating model around them. Within the evidence available here, the candidates fall into three broad buckets.

Visa Foreign Exchange Rates API#

Treat this as a network-context FX option for Visa flows. The evidence available here is concrete enough to support that classification.

Visa states that it returns Visa conversion rates for a currency pair. rateProductCode="A" and "B" are indicative daily rates. transactionType supports Pull/Push Funds, and omitted transactionType defaults to Push Funds. For BANK/WALLET flows, eligible Visa Direct clients can receive a reusable quote ID until expiry.

That tells you several important things without overreaching:

- it is tied to Visa conversion context

- it has quote behavior that matters to execution design

- transaction type matters

- omission of

transactionTypeis itself meaningful - eligibility and expiry still need to be understood operationally

What still needs to be resolved before commitment is equally important. The open questions listed here include SLA clarity, auth model, webhook/error parity, contract limits, and bundle eligibility. Those are not side questions. They shape how much operator tooling you need, how you model failures, and what you can promise internally about behavior under load or during exceptions.

Mastercard Currency Conversion Calculator APIs#

Treat this as a network-context candidate that still needs verification.

Do not assume parity with another network-context option simply because the broad category sounds similar.

What needs to be resolved before commitment includes SLA clarity, auth model, request semantics, quote behavior, webhook/error parity, and contract limits. In practice, your team should not design around inferred behavior. It should design around verified behavior. Until that verification exists, keep the candidate in evaluation status rather than implementation status.

Currencycloud Convert Payments API#

Treat this as a payments-native execution candidate to verify if you own conversion execution and payout orchestration. The use case fit is clear: you own conversion execution and payout orchestration. Treat it as a candidate to validate rather than a drop-in answer.

The important selection lesson is broader than any one provider. Use candidate names as reminders of responsibility fit, not as shortcuts to architecture decisions. If the evidence available is thin, say so and keep the unknowns visible.

Compare classes without getting distracted#

Once you classify candidates by job, compare them against the flow you documented earlier. Ask:

- does the class match the money movement shape you declared

- does quote behavior fit your stale-quote policy

- does request shape fit your contract discipline

- can you preserve identifiers from API request to internal record to reconciliation output

- does the class support the way you track and confirm transfer outcomes

This sequence protects you from a common mistake: evaluating providers as if all conversion APIs are interchangeable. They are not. One can be suitable for network-context FX in Visa flows, while another is more aligned to owned conversion execution and payout orchestration. A class mismatch can create more downstream complexity than any feature difference on a checklist.

Another useful discipline is to separate what is evidenced from what is still unknown. If a provider's behavior is not evidenced in your material, do not fill the gap with assumptions because another candidate exposes a similar-sounding feature. Unknowns should stay unknown until resolved.

Coverage and behavior vary by provider, market, and program. That is why classification by responsibility should come first. It narrows the field and makes later commercial and technical questions more meaningful.

Set quote policy before writing conversion code and lock request contracts early#

Set quote policy before you finalize UI behavior, retry logic, and conversion code. If you leave it vague, the rest of the build will encode assumptions you later have to undo.

| Part | Requirement |

|---|---|

| Transport | Server-to-server HTTPS POST with JSON |

service_command | Requests can require it |

SHA-256 signature | Requests can require it |

currency | 3-letter ISO 4217 value |

converted_currency | 3-letter ISO 4217 value |

amount | Positive integer in the currency's smallest unit with max length 10 |

| Amount serialization | 100.00 USD is sent as 10000, not "100.00"; never as floating point or display formatting |

Start with the core fact already established: a conversion service is built to convert one currency amount to another using current exchange rates, not to return a timeless reference value. If your product shows one converted amount and later retries with a fresh request, the response may differ. That is not a corner case. It is a basic property of the flow, so you need an explicit quote policy.

At minimum, decide what happens when:

- a customer sees one converted amount but the system needs to submit later

- the original quote is no longer valid

- a retry happens after rate movement

- a repeated request returns a different value

- the product needs to explain the difference to the user or to ops

You do not need to set a duration threshold here, but you do need explicit behavior for stale-quote rejection and expiry handling. "We will decide later" is not a neutral choice. It usually becomes "the front end showed one number, the back end retried with a fresh request, and now finance, ops, and support are all looking at different records."

Quote policy also affects internal expectations. If repeated conversion calls are not stable, engineering cannot assume retry equals replay. Payments ops cannot assume a failed attempt can always be rerun without a value change. Finance cannot assume the displayed pre-execution amount is the same amount that should appear in reconciliation records. Everyone needs the same mental model.

This is where reusable quote behavior, when available, matters. In the evidence provided here, eligible Visa Direct clients in BANK/WALLET flows can receive a reusable quote ID until expiry. That does not mean all flows have that property. It means quote handling must be designed around the actual behavior of the class and provider you choose.

Once quote policy is defined, lock the request contract. The request itself should be treated as a money-moving contract, not just a transport payload.

At integration level, the flow can be server-to-server HTTPS POST with JSON. Requests can require:

service_command- SHA-256

signature - 3-letter ISO 4217 values for

currency - 3-letter ISO 4217 values for

converted_currency

A stable request contract is valuable because it reduces avoidable drift across teams. It gives engineering a canonical payload shape, ops a reliable record to inspect, and finance more confidence that internal records map back to something exact rather than reconstructed.

Amount serialization is the part to lock most aggressively. The amount field can be required as a positive integer in the currency's smallest unit with max length 10. 100.00 USD is sent as 10000, not "100.00".

That has several practical consequences:

- convert display values into smallest-unit integers exactly once

- do not send floating point values

- do not send display-formatted strings in the payload

- do not let multiple services reinterpret the amount independently

Your first verification checkpoint should be simple and strict: serialize source amounts exactly once into the smallest unit, never as floating point and never with display formatting in the API payload.

Why be so rigid here? Because amount bugs tend to look small in code review and large in production. A formatting choice that seems harmless in a demo can produce failed requests, wrong downstream records, or hard-to-explain discrepancies between what users saw and what the system attempted to execute.

This is also the right place to lock idempotency behavior early, even if the exact provider mechanism varies. The goal is not to assume a specific field or vendor-specific design that is not evidenced here. The goal is to define how your system treats duplicate business actions and retries.

If the same business action is submitted twice, you need an explicit rule for whether that is:

- one action being retried

- a second action

- a stale action that must be rejected

- a new conversion that must be clearly separated from the first

Because rates can move between requests, duplicate handling is not just about preventing technical duplication. It is about preventing ambiguity. Without early agreement, one part of the system can treat a second request as a harmless replay while another part treats it as a new conversion with a new value.

Tie your request contract to traceability from the start. The identifiers preserved from API request to internal record to reconciliation output should be selected before code spreads across services. Otherwise you end up retrofitting traceability after the fact, which usually means partial joins, missing context, and hard operator investigations.

A good design review question here is simple: if a conversion is displayed, retried, confirmed, and exported, can the team connect all those states without interpretation? If not, the request contract is still too loose.

For a step-by-step walkthrough, see How to Implement OAuth 2.0 for Your Payment Platform API: Scopes Tokens and Best Practices.

Execute in strict order from quote to ledger posting#

A conversion flow should execute in a strict order that matches how the business explains the transaction. That sequence should run from request and quote handling through transfer confirmation, ledger entry, and export output.

The exact systems can vary, but the discipline should not. If you let the order drift, you create records that are hard to reconcile and even harder to explain.

A practical sequence starts before the API call itself. First, confirm that the flow being executed matches the declared money movement shape. Then make sure the request is being built under the correct environment, with the correct signing behavior, and with the amount already serialized into the smallest unit. Only then should you send the conversion request.

After that, keep the next steps in order:

- create the source request with the exact payload contract

- submit the conversion request in the correct environment

- capture the response and any quote-related outcome that matters to execution

- track transfer progress and confirmation

- post the ledger entry only when the business event being recorded is clear

- carry the preserved identifiers forward into export output

This order matters because each step relies on the previous one being unambiguous. If you skip ahead and post ledger effects before you can connect them back to the exact request and confirmed transfer outcome, finance will later inherit uncertainty that engineering could have prevented.

The guide already gives you a concrete checkpoint for this: prepare one worked example from source request through transfer confirmation, ledger entry, and export output. That single exercise is effective because it exposes hidden assumptions quickly.

For example, can the team answer these basic questions from the worked example alone?

- which exact request was sent

- how was the amount serialized

- what conversion outcome was returned

- where transfer confirmation was recorded

- which ledger entry reflects the event

- which export row finance will use to reconcile it

If any answer depends on memory instead of records, the flow is not ready.

Strict order is also how you keep rate movement from causing silent inconsistencies. Since repeated conversion calls may differ, do not casually replace one request with another and treat the later response as if it represented the same moment. If the business action is a retry, record it as such. If the business action is a fresh attempt after quote expiry, treat it as a new attempt with its own traceable path.

Async behavior deserves special discipline here. The ownership model already assigns engineering responsibility for async event handling and payments ops responsibility for transfer-status follow-up. Use that split to keep the flow understandable. Engineering should make the state transitions visible and reliable. Ops should have enough context to review exceptions and follow up on transfer status without reconstructing history from scattered logs.

The point of strict order is not ceremony. It is explainability. A money-moving system should be able to tell a coherent story about one transaction from start to finish. If the story changes depending on which team is asked, the order is not strict enough.

Related reading: Payment API Rate Limiting: How to Design Throttling Policies That Do Not Break Integrations.

Build reconciliation outputs as product features, not afterthoughts#

Reconciliation should be designed into the product, not added after the API integration appears to work. In conversion flows, reconciliation is not a back-office convenience. It is part of proving that the money movement happened as intended.

The most important principle here is traceability. Preserve identifiers from API request to internal record to reconciliation output. That requirement already appears in the minimum evidence pack because it is the bridge between technical execution and financial control.

If finance cannot connect a converted payment back to the exact request and forward to the export row used for reconciliation, the design is incomplete. A successful API response does not solve that problem by itself. It only creates one piece of the record.

This is why reporting obligations and export consumers need to be identified before build. If you know who consumes the exports and what obligations those outputs support, you can shape the internal records around real downstream use instead of generic assumptions.

A practical approach is to treat export completeness as part of the product surface. That does not mean exposing finance tools to end users. It means acknowledging that the exported record is one of the final outputs of the system and should therefore be designed deliberately.

Use the worked example again here. Start with the source request. Then carry the record through transfer confirmation and ledger entry until you reach export output. Check whether the path remains understandable at each step.

Questions worth asking include:

- can finance match the export row to the internal record without manual interpretation

- can ops use the same identifiers to investigate an exception

- can compliance review the same transaction trail if needed

- can engineering reproduce the sequence in logs without mixing environments

The earlier checkpoint remains decisive: if you cannot trace what finance needs to reconcile a converted payment, the design is not ready.

Audit traceability also matters here. You already set end-to-end audit traceability as a non-negotiable before code. Reconciliation is where that principle becomes testable. A system with good audit traceability should let the team explain what happened from records alone.

That means records should connect:

- the original request

- the transfer confirmation

- the ledger entry

- the export row

Those elements do not have to live in one place, but they do need to connect without ambiguity. If a team member has to infer whether two records belong together, the system is pushing interpretive work onto operations and finance.

Another reason to build reconciliation outputs early is that routing affects them. Since routing is a reliability decision that can drive payment failures, it also affects how exceptions appear in internal records. A route that changes how outcomes are tracked or confirmed can change what finance expects to reconcile. That is another reason to choose the money movement shape first and keep the route explicit.

product completeness for conversion flows includes export completeness. If reconciliation outputs are postponed, you are postponing part of the actual product.

If you want the full breakdown, read How to Build a Partner API for Your Payment Platform: Enabling Third-Party Integrations.

Add compliance gates where conversion and payout risk actually occurs, and plan failure handling#

Compliance gates should be placed where conversion and payout risk actually occurs, not where it is easiest to draw a box on an architecture diagram. The same principle applies to failure handling. Put the decision and recovery points where the transaction actually becomes risky or ambiguous.

The available ownership model already gives you a practical starting point. Compliance owns review paths for KYC, KYB, and AML evidence or exceptions. That means compliance should be engaged around the real transaction checkpoints, not after the fact when a payment has already created downstream confusion.

Start from the flow you documented earlier:

- where funds are collected

- when conversion happens

- how transfer outcomes are tracked

- how transfer outcomes are confirmed

Those are the points where compliance and operational risk become real. If conversion happens at one stage and payout execution risk appears at another, the control points should reflect that instead of relying on a generic pre-launch compliance review as a substitute.

You do not need a universal model here. The guide is clear that this is a practical operating model, not a universal standard. Review paths for evidence and exceptions need to be explicit and owned.

Failure handling should be designed with the same realism. Conversion and payout flows can fail because of routing decisions, environment mix-ups, request-contract issues, stale quotes, or later transfer-status problems. Your recovery path should tell operators what to do without forcing them to guess what the system meant.

Use the ownership grid directly:

- Engineering owns request integrity, idempotency behavior, and async event handling

- Payments ops owns exception review and transfer-status follow-up

- Finance owns reconciliation rules and export completeness

- Compliance owns review paths for evidence or exceptions

That distribution matters most when something goes wrong. A clean failure model lets each team act on its own part of the problem while still sharing the same transaction story.

Use a simple rule here: every external status change should have one primary owner and one escalation owner. That rule turns abstract coordination into something operational. When an external state changes, someone should know they are responsible, and someone else should know they are the escalation path.

Environment discipline is part of failure handling too. From day one, keep sandbox and production behavior separate in both implementation and logs. Providers can publish distinct endpoints, and environment mix-ups around signing, amount encoding, or routing create discrepancies that are painful to debug later.

That separation helps in two ways:

- it reduces the chance of the wrong request being sent under the wrong assumptions

- it makes investigations much easier when a discrepancy appears

A failure plan is not complete unless operators can recover coherently. They should be able to look at a record and answer whether this was a malformed request, a quote issue, a routing issue, a transfer-status issue, or an environment issue. They do not need every answer instantly, but they do need records that support the right path to an answer.

A paper test helps here too. Run one hypothetical transaction through an exception scenario and verify that ops can explain what happened from records alone. That includes who owns the next action and who gets the escalation if the issue remains unresolved.

If currency conversion changes affect request or response fields, this guide on How to Version Your Payment API: Strategies for Backward-Compatible Changes is a useful next step.

Compare commercial constraints before signing#

Commercial comparison should happen after you understand the flow and the provider class, not before. If you compare commercial terms without that context, you risk optimizing for the wrong job.

Begin with what your minimum evidence pack already established:

- required source and destination currencies

- initial payout corridors

- expected transaction types by flow

- reporting obligations and export consumers

Those items define the real scope of the commercial decision. A provider that looks attractive in broad terms may still be a poor fit if the currencies, corridors, transaction types, or reporting needs do not line up with the flow you are actually launching.

The draft also gives you a useful caution: coverage and behavior vary by provider, market, and program. That means a commercial agreement should be tested against actual operating needs, not against generalized expectations.

Use the open questions already surfaced in the candidate comparison as a commercial checklist, not just a technical one. Depending on the candidate, you may need to resolve items such as:

- SLA clarity

- auth model

- request semantics

- quote behavior

- webhook/error parity

- contract limits

- bundle eligibility

These are not all purely technical details. Several have direct commercial impact because they shape support load, operational cost, internal tooling needs, and what your teams can reliably commit to.

Routing should remain part of the comparison too. Routing is a reliability decision, and cost and performance need to be weighed together. That means a cheaper route is not automatically better if it increases payment failures or complicates confirmation and reconciliation. Commercial evaluation should reflect the full operating cost of the route, not just the visible contracted cost.

Also compare candidates against your quote policy and audit requirements. If stale-quote handling is central to your product behavior, the provider's quote behavior becomes commercially relevant because it affects how much complexity you absorb internally. If export completeness is critical for finance, gaps in operational visibility can become a real cost even if they do not appear in the base pricing discussion.

A sound signing decision usually leaves the fewest critical unknowns at launch. If core behavior is still unverified, keep the decision in evaluation until those unknowns are resolved. Commercial progress should not outrun execution confidence.

If you need to document supported currencies, FX behavior, or rate fields clearly, see OpenAPI Specification for Payment Platforms: How to Document Your Payout API.

Run a production readiness test before launch#

Before launch, run a production readiness test that proves the flow works as an operational system, not just as an API integration.

The easiest way to do that is to reuse the same end-to-end checkpoints that appeared earlier and make them concrete under launch conditions. You already know what to test because the architecture work defined it.

Run one transaction from source request through:

- exact payload construction

- amount serialization in the smallest unit

- signing behavior

- environment routing

- transfer tracking and confirmation

- ledger entry

- export output

Then ask the teams to validate their own responsibilities against that single path. Engineering should verify request integrity, async handling, and the records needed to understand retries or duplicates. Payments ops should verify that exception review and transfer-status follow-up are workable. Finance should verify reconciliation rules and export completeness. Compliance should verify that review paths for evidence or exceptions line up with the actual flow.

Keep sandbox and production behavior separate in both implementation and logs while doing this. If the environment split is unclear at launch, the team will lose time investigating problems that should have been easy to isolate.

The final launch test should also prove explainability. Ops should be able to explain what happened from records alone. That was already a paper-test requirement earlier in the design, and it remains the right standard before launch. If a launch candidate depends on unwritten assumptions, it is not production ready yet.

Before implementation freeze, map your quote lifecycle, idempotency keys, and webhook replay behavior against Gruv integration patterns in the developer docs.

Frequently Asked Questions and copy-paste launch checklist#

Is a currency conversion API just a rate lookup?#

No. Request shape, authentication, and amount formatting affect outcomes. Repeated requests can also return different values as rates move.

Why can the same request return a different value later?#

Because the service is built to convert one currency amount to another using current exchange rates, not to return a timeless reference value. If your product shows one converted amount and later retries with a fresh request, the response may differ.

What is the most common payload mistake?#

Amount formatting. The amount field can be required as a positive integer in the currency's smallest unit, with max length 10, so 100.00 USD is sent as 10000, not "100.00". Do not send floating point values or display-formatted strings in the API payload.

What request details should be treated as part of the contract?#

At integration level, a flow can be server-to-server HTTPS POST with JSON. Requests can require a service_command, a SHA-256 signature, and 3-letter ISO 4217 values for currency and converted_currency. Those details should be locked early.

Do I need a quote policy before coding?#

Yes. You do not need a duration threshold yet, but you do need explicit behavior for quote expiry handling and stale-quote rejection. If repeated conversion calls can differ, retry behavior and customer messaging cannot be left implicit.

When should I choose a provider?#

After you decide what payment responsibility you actually have. First decide whether you need network-context FX, payout execution, or reference-only rates. Then evaluate providers within that class.

What should finance insist on before launch?#

Traceability from API request to internal record to reconciliation output. If finance cannot trace what it needs to reconcile a converted payment, the design is not ready.

Where should compliance and ops fit into the design?#

Before implementation starts. Use explicit ownership for engineering, payments ops, finance, and compliance. Every external status change should have one primary owner and one escalation owner.

Why separate sandbox and production so strictly?#

Because providers can publish distinct endpoints, and environment mix-ups around signing, amount encoding, or routing create discrepancies that are painful to debug later. Separate implementation and logs from day one.

Copy-paste launch checklist#

Use this as a final pass before launch:

- Name the money movement shape clearly:

Merchant of Record, direct payouts, orVirtual Accounts-led collection - Document where funds are collected

- Document when conversion happens

- Document how transfer outcomes are tracked

- Document how transfer outcomes are confirmed

- Map one end-to-end transaction from payer to recipient

- Mark where transfer tracking and confirmation happen

- Assign ownership across engineering, payments ops, finance, and compliance

- Confirm every external status change has one primary owner and one escalation owner

- Prepare the minimum evidence pack

- List required source and destination currencies

- List initial payout corridors

- List expected transaction types by flow

- Identify reporting obligations and export consumers

- Decide which identifiers are preserved from API request to internal record to reconciliation output

- Prepare one worked example from source request through transfer confirmation, ledger entry, and export output

- Freeze non-negotiables for quote expiry handling

- Freeze non-negotiables for stale-quote rejection

- Freeze non-negotiables for end-to-end audit traceability

- Treat the request shape as a money-moving contract

- Confirm server-to-server HTTPS

POSTwith JSON behavior where applicable - Confirm required request elements such as

service_command, SHA-256signature,currency, andconverted_currency - Serialize source amounts exactly once into the smallest unit

- Do not use floating point in the API payload

- Do not use display formatting in the API payload

- Confirm

amounthandling as a positive integer in the currency's smallest unit with max length10 - For three-decimal currencies in the relevant Visa context, round the final decimal place to zero to reduce declined-transaction risk

- Keep sandbox and production behavior separate in implementation

- Keep sandbox and production behavior separate in logs

- Confirm your quote policy before finalizing UI and retry behavior

- Classify providers by responsibility before comparing them by brand

- Distinguish network-context FX, payout execution, and reference-only rate needs

- Validate provider behavior only where it is actually evidenced

- Resolve open questions such as SLA clarity, auth model, request semantics, quote behavior, webhook/error parity, contract limits, and bundle eligibility where relevant

- Make sure the execution order from request to transfer confirmation to ledger entry to export output is explicit

- Confirm finance can reconcile from preserved identifiers

- Confirm ops can explain what happened from records alone

- Confirm compliance review paths for

KYC,KYB, andAMLevidence or exceptions - Run one production readiness test that exercises the full flow

- Do not launch until the full transaction story is coherent from request through export output

Next step: take one real planned transaction and run it through this checklist line by line. If the team cannot produce a clear answer for any item from the design itself, resolve that gap before writing more code or signing the final commercial commitment.

If you are finalizing corridor coverage, payout routing, and compliance gates for go-live, talk to Gruv to confirm what is supported for your program.

Frequently Asked Questions

Is a currency conversion API just a rate lookup?

No. Request shape, authentication, and amount formatting affect outcomes. Repeated requests can also return different values as rates move.

Why can the same request return a different value later?

Because the service is built to convert one currency amount to another using current exchange rates, not to return a timeless reference value. If your product shows one converted amount and later retries with a fresh request, the response may differ.

What is the most common payload mistake?

Amount formatting. The amount field can be required as a positive integer in the currency's smallest unit, with max length 10, so 100.00 USD is sent as 10000, not "100.00". Do not send floating point values or display-formatted strings in the API payload.

What request details should be treated as part of the contract?

At integration level, a flow can be server-to-server HTTPS POST with JSON. Requests can require a servicecommand, a SHA-256 signature, and 3-letter ISO 4217 values for currency and convertedcurrency. Those details should be locked early.

Do I need a quote policy before coding?

Yes. You do not need a duration threshold yet, but you do need explicit behavior for quote expiry handling and stale-quote rejection. If repeated conversion calls can differ, retry behavior and customer messaging cannot be left implicit.

When should I choose a provider?

After you decide what payment responsibility you actually have. First decide whether you need network-context FX, payout execution, or reference-only rates. Then evaluate providers within that class.

What should finance insist on before launch?

Traceability from API request to internal record to reconciliation output. If finance cannot trace what it needs to reconcile a converted payment, the design is not ready.

Where should compliance and ops fit into the design?

Before implementation starts. Use explicit ownership for engineering, payments ops, finance, and compliance. Every external status change should have one primary owner and one escalation owner.

Why separate sandbox and production so strictly?

Because providers can publish distinct endpoints, and environment mix-ups around signing, amount encoding, or routing create discrepancies that are painful to debug later. Separate implementation and logs from day one.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/cpmi/publ/d205.pdftrusted

- irs.gov/irm/part2/irm_02-005-003trusted

- occ.gov/publications-and-resources/publications/comp...trusted

- stripe.com/resources/more/money-movement-apistrusted

- stripe.com/ae/resources/more/intelligent-payment-routingtrusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- vat-one-stop-shop.ec.europa.eu/one-stop-shop_entrusted

- vat-one-stop-shop.ec.europa.eu/index_entrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Calculate the All-In Cost of an International Payment

Headline fees can understate true cost. The figure that protects margin is the net amount that lands with the recipient after conversion, transfer charges, and any downstream deductions.

How EOR Platforms Use FX Spreads to Make Money

You can control more of your payout outcome than it first appears. As the CEO of a business of one, separate unavoidable costs from avoidable ones, then manage the compliance exposure that cross-border money movement creates.

Indian Freelancer Payment Analysis That Protects Net INR

For freelancers in India, the number that protects cash flow is the net INR credited to your bank, not the USD amount on the invoice. Start from that outcome and work backward through every payment decision.