Quick Answer

Start with a documented decision path for Apple W-8BEN-E UK company filings: confirm whether Form W-8BEN-E fits your facts, decide EIN vs UK UTR based on what App Store Connect actually accepts, and pause if ECI or treaty eligibility is unclear. Keep proof of field labels, submission behavior, and internal approval. If the flow asks for different identifiers or your team disagrees on classification, escalate before submitting. The goal is a defensible record, not fastest completion.

Choosing the Apple tax form for a UK limited company#

For most UK teams, the hard part is not discovering that a U.S. tax form exists. It is deciding what a UK limited company should actually submit when App Store Connect presents tax questions in a way that is operationally vague. This article takes a narrow, practical path through that problem: how to document decisions, and when to stop and escalate before a tax setup issue turns into a payout or audit issue.

That scope matters because a limited company is not just a trading label. It is an incorporated business type and a separate legal entity. In practice, that means the tax profile you build for Apple Developer should follow the company's real legal and tax facts, not whatever seems closest in a platform dropdown. If the screen language and your internal understanding do not match, pause and capture the ambiguity instead of guessing.

The UK side of the picture will feel familiar to finance and compliance teams, but it does not answer the U.S. form question on its own. HMRC's Self Assessment guidance is a useful reminder of how tax administration works in real life. You tell HMRC by registering for Self Assessment, HMRC refers to a Unique Taxpayer Reference (UTR) in account handling, and timing matters.

HMRC says people in scope must tell it by 5 October 2025 for the previous tax year running from 6 April 2024 to 5 April 2025, and warns that notifying after that date could lead to a penalty. GOV.UK also says a return may be delayed if you file it without reactivating an existing account, and that some returns cannot be filed through the standard online service at all. Those are UK administration details, but they point to the same control principle you need here. Treat identifiers, deadlines, and platform acceptance as evidence-backed decisions, not memory work.

So the real question is not just, "Do we have a form?" It is also, "Which form fits the facts, which identifier will the payer accept, and what proof do we keep if that choice is challenged later?" The sections that follow focus on choosing the form and identifier that fit your facts, with clear decision boundaries and escalation points when the evidence is unclear.

One caution up front. Public UK guidance can verify HMRC administration, but it does not resolve Apple-specific steps by itself. Where platform instructions are unclear, the right discipline is controlled verification. Save screenshots, note the date and account used, record who approved the interpretation, and escalate early if tax, legal, and finance are reading the same prompt differently. That is slower than following forum advice, but much cheaper than untangling a bad filing after withholding, rejected payouts, or inconsistent records appear. If you want a related UK company invoicing angle, see How a UK Creative Director Should Invoice a US Client from their LTD Company to Optimize for Taxes.

Define the tax terms before touching Apple settings#

Define each tax label before you touch the platform fields. That makes your filing choices easier to defend later.

| Term | What it is | Handling here |

|---|---|---|

| Form W-8BEN-E | IRS certificate titled "Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting (Entities)" | Use as entity-status evidence for U.S. withholding and reporting; check IRS.gov/FormW8BENE for current instructions (excerpt cited: Rev. October 2021) |

| Effectively Connected Income / gain concepts | Escalation signal, not a quick UI choice | The materials here do not give Form W-8ECI filing criteria; pause and get tax review if there is possible U.S.-connection risk |

| Treaty-gate terms (including Limitation on Benefits) | Technical eligibility questions | The materials here do not define Limitation on Benefits, the active trade or business test, the derivative benefits test, or U.S.-UK treaty qualification rules; do not answer from memory |

| Entity classification (Line 4) | On W-8BEN-E, Line 4 is "Type of entity," and the IRS notes this field was updated | Match the selection to the company's legal records and retain evidence |

- Form W-8BEN-E: This is the IRS certificate titled "Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting (Entities)". Use it as entity-status evidence for U.S. withholding and reporting, not as a blanket conclusion on all U.S. tax questions. Before relying on internal notes, check IRS.gov/FormW8BENE for current instructions (the excerpt here is Rev. October 2021 and directs users to that page for updates).

- Effectively Connected Income / gain concepts: Treat this as an escalation signal, not a quick UI choice. The materials here do not give Form W-8ECI filing criteria, so if your team sees possible U.S.-connection risk, pause and get tax review instead of inferring from platform prompts.

- Treaty-gate terms (including Limitation on Benefits): Handle these as technical eligibility questions. The materials here do not define Limitation on Benefits, the active trade or business test, the derivative benefits test, or U.S.-UK treaty qualification rules, so do not answer from memory.

- Entity classification (Line 4): On W-8BEN-E, Line 4 is "Type of entity," and the IRS notes this field was updated. Match the selection to the company's legal records, then retain evidence such as the submitted screen and internal approver note.

We covered this in detail in Setting Up a UK Limited Company for Freelance Work.

Decide whether you are in W-8BEN-E or W-8ECI territory#

Use Form W-8BEN-E only when your documented facts support foreign-entity withholding/reporting status and your review has not identified a clear effectively connected income concern. If your review raises possible U.S. trade or business exposure or a possible Permanent Establishment issue, pause and escalate before you file.

That scope point matters. The IRS describes Form W-8BEN-E as a certificate of status for U.S. withholding and reporting, not a blanket answer to every U.S. tax question. The same instructions also reference amounts treated under section 864(c)(8) as effectively connected gain and updates tied to section 1446(f), so treat form selection as a documented decision, not a checkbox exercise.

| Decision point | W-8BEN-E | W-8ECI (escalate path) |

|---|---|---|

| Trigger condition | Facts support foreign-entity withholding/reporting status, with no clear ECI signal identified | Facts raise a possible ECI question that needs specialist analysis before filing |

| Decision owner | Internal preparer with documented approver | Tax/legal specialist review before submission |

| Evidence to retain | Entity check, form choice rationale, approval record | Escalation note, fact pattern memo, specialist conclusion |

| If filed on weak support | Withholding/reporting position may not match facts and may require remediation | Filing basis may still need correction and rework |

Before data entry, record the legal entity name, selected form, approver, and why no ECI concern was identified. Then check the latest IRS updates at IRS.gov/FormW8BENE.

If your team's conclusion is still "probably," do not submit yet. Hold filing and complete specialist review first. If you need the company structure backdrop, read Sole Trader vs Limited Company UK for Freelancers.

Set a decision rule for EIN versus UK UTR before submission#

Treat EIN vs UK UTR as a controlled payer-policy decision, not a data-entry choice. For a UK company, record who approved the identifier, what the platform field asked for, and what happened at submission.

The boundary here is narrow and important: GOV.UK supports what a UTR is in HMRC Self Assessment context, including "If you're waiting for a Unique Taxpayer Reference (UTR)" and registration wording around Self Assessment. That evidence does not establish how Apple or IRS platform flows will treat a UTR for this profile.

Treat the identifier as a controlled decision#

Use this rule: if the platform flow accepts a UK UTR with no blocking validation, proceed only after named internal approval and retained evidence. If the flow asks for EIN or blocks UTR, stop and escalate as a tax-policy decision.

Capture evidence at the time of filing: field label, validation behavior, submission result, reviewer name, and date. Prior acceptance is not a standing rule if the UI text or validation behavior changes.

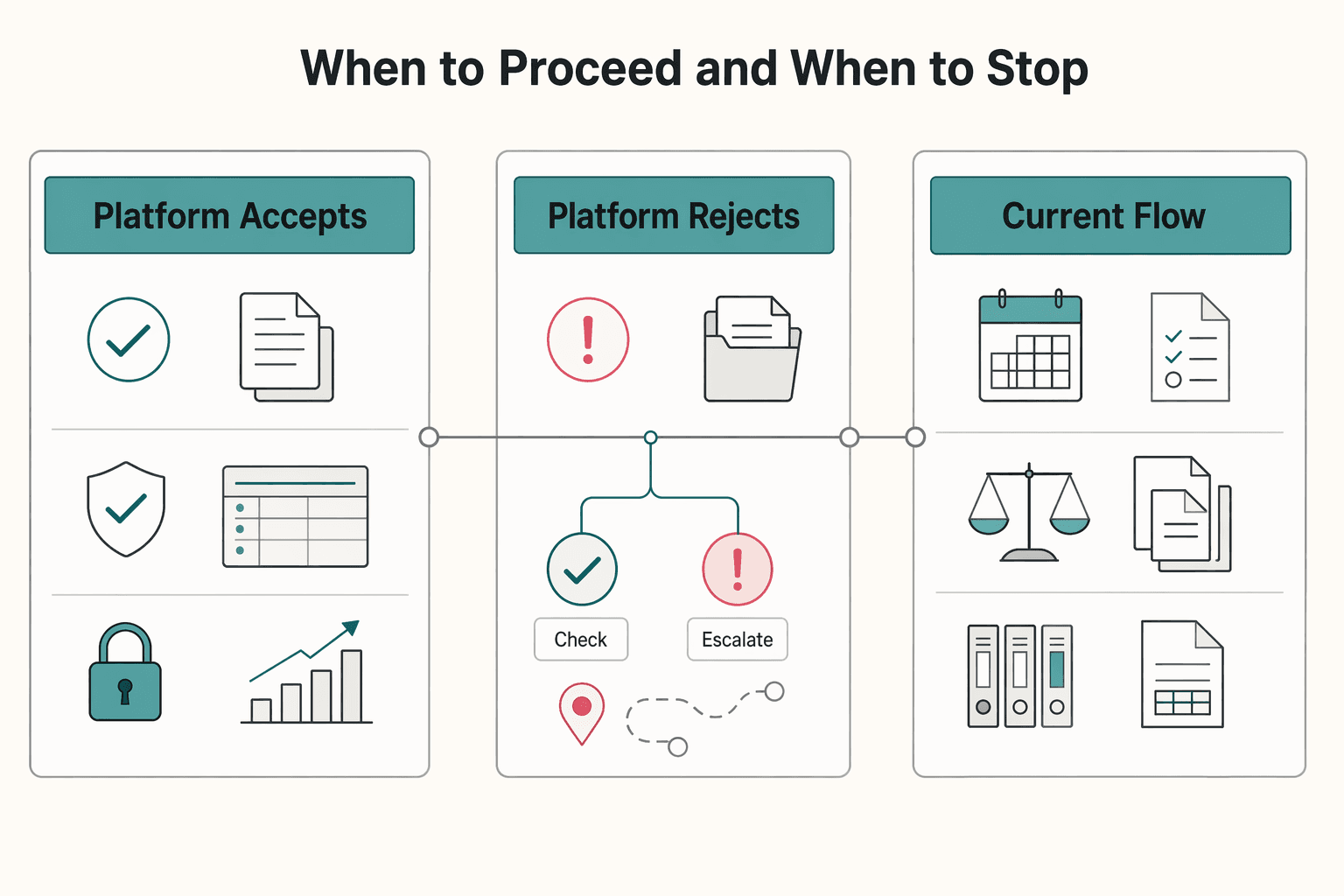

When to proceed and when to stop#

| Scenario | Accepted identifier | Escalation trigger | Retained artifact | Recheck cadence |

|---|---|---|---|---|

| Platform accepts UK UTR and submission completes without blocking validation | UTR for that submission instance | Reviewer cannot confirm fit for the field or later profile mismatch appears | Screenshot of field label, submission state, approval note, dated case record | Next tax-profile edit and after relevant UI/policy changes |

| Platform rejects UTR or explicitly asks for EIN | None until review closes | Inline error, required-field text, support instruction, or blocked submission | Error screenshot, request text, escalation ticket with owner and due date | When payer response or internal tax review lands |

| Current flow differs from prior submission behavior | Do not assume prior identifier still applies | Any change in wording, validation, or requested document set | Before/after screenshots and approval note on whether to reuse or change approach | Immediately before resubmission |

Do not infer Apple identifier policy from HMRC admin deadlines. Dates such as 5 October 2025 (notify HMRC in the cited Self Assessment scenario) and 31 January (paying the Self Assessment bill) explain UK tax administration context, not Apple payer-policy requirements for this filing flow.

For a step-by-step walkthrough, see How to Fill Out Form W-8BEN for a Foreign Freelancer. If you want a quick next step for "Apple W-8BEN-E UK company," try the W-8 form generator.

Complete the high-friction fields without guesswork#

Treat these fields as certification decisions, not simple data entry. If a selection cannot be explained, supported, and approved, pause submission.

Prioritize Corporation entity classification, treaty claim sections, and any Limitation on Benefits selection. For each field, record:

| Checklist item | What to capture |

|---|---|

| Field label | Exact wording shown in App Store Connect |

| Selected answer | The value submitted |

| Business rationale | Why this matches your UK limited company facts |

| Supporting record | Retainable evidence (internal records or documented analysis) |

| Approval | Named reviewer and date |

| Open issue | Yes/no, with owner if unresolved |

When treaty basis is unclear, require written rationale and sign-off before you submit. That includes cases where the active trade or business test or derivative benefits test might apply but the reasoning is uncertain.

Use a hard stop if tax, legal, and finance interpretations conflict. Resolve the inconsistency first so your records stay aligned.

Keep a separate "known unknowns" log for unresolved Apple-specific instructions, including date, screenshot, open question, owner, and next follow-up. Do not substitute forum assumptions for documented decisions. IRS Publication 515 is the relevant withholding subject area and includes Forms 1042 and 1042-S reporting obligations, so incomplete or inconsistent entries can create downstream reporting risk. For more detail, see A UK Limited Company's Guide to Filling Out Form W-8BEN-E.

Build the minimum evidence pack auditors will ask for later#

Once form and treaty decisions are made, freeze the record so a reviewer can see what you submitted, why, who approved it, and which IRS concepts were applied, without reconstructing the story from chat or email.

| Record item | What to include | Notes |

|---|---|---|

| Final submitted Form W-8BEN-E | Final submitted copy | Keep it in one controlled, read-only (or equivalently restricted) case file |

| Decision memo | Form choice, entity classification, treaty position, and any open assumptions | If a position depended on judgment rather than a mechanical rule, state that plainly and note unresolved assumptions |

| Approvals | Named approvers and approval dates | Show who approved the filing and when |

| Supporting records | Records used for the decision | Include the records relied on for the decision |

| Platform submission evidence | Evidence showing final submitted state, if available | Lets a reviewer see what was submitted without reconstructing the story from chat or email |

Keep one controlled, read-only (or equivalently restricted) case file. At minimum, include:

- Final submitted Form W-8BEN-E

- Short decision memo covering form choice, entity classification, treaty position, and any open assumptions

- Named approvers and approval dates

- Supporting records used for the decision

- Platform submission evidence showing final submitted state, if available

If a position depended on judgment rather than a mechanical rule, say that plainly and note unresolved assumptions.

Tie each answer to the Internal Revenue Service concept behind it#

Your memo should map each major selection to the IRS concept behind it. For example, document that Form W-8BEN-E is the certificate of status of beneficial owner for U.S. withholding and reporting (entities), and record the treaty eligibility basis used for the claim.

Also record the instruction set you relied on. The form instructions direct readers to IRS.gov/FormW8BENE for latest developments, and Publication 515 directs readers to IRS.gov/Pub515 for updates. Capture the document version or access date, especially where fields can change; for example, the instructions note that Line 4, "Type of entity," has been updated.

The common failure mode is a file that has the signed form but not the decision logic. A stronger pack lets a reviewer trace the chain from submission record to form/treaty choice to IRS concept to approver. Related reading: US LLC and BVI Company Blueprint for Asset Protection.

Add post-submission controls so one good submission does not decay#

One clean submission is not a permanent control. Revalidate when facts change, and on a simple calendar cadence, so the record does not drift.

| Control | When it applies | What to do |

|---|---|---|

| Event-based review | Ownership changes, entity changes, business-model shifts, rejected payouts, tax-profile mismatches, or unexpected U.S. withholding outcomes | Reopen the file; if new payment patterns raise fresh questions about U.S. source income, U.S. trade or business, or possible Permanent Establishment exposure, escalate for specialist review |

| Calendar-based review | At least an annual check of identifiers, account status, and records | Where relevant, confirm UTR/account status early, keep records such as bank statements or receipts, and avoid late notification risk |

| Exception queue | When payout or withholding issues arise | Keep owner, date opened, affected account, evidence captured, and resolution status so issues are tracked as potential tax-control signals |

For a UK limited company, treat entity changes as hard checkpoints. Business.gov.uk describes a private limited company as a separate legal entity, so ownership, group-structure, or contracting-party changes should trigger a short revalidation memo and approval refresh.

Use two trigger types:

- Event-based review: Reopen the file for ownership changes, entity changes, business-model shifts, rejected payouts, tax-profile mismatches, or unexpected U.S. withholding outcomes. If new payment patterns raise fresh questions about U.S. source income, U.S. trade or business, or possible Permanent Establishment exposure, escalate for specialist review.

- Calendar-based review: Run at least an annual check of identifiers, account status, and records. HMRC says you may need to reactivate an existing Self Assessment account, and filing without reactivation may delay a return. Where relevant, confirm UTR/account status early, keep records such as bank statements or receipts, and avoid late notification risk (HMRC warns that telling HMRC after 5 October 2025 could lead to a penalty in the scenario described).

Keep a lightweight exception queue with owner, date opened, affected account, evidence captured, and resolution status so payout or withholding issues are tracked as potential tax-control signals, not only operational noise.

Connect tax form controls to payout and ledger operations#

Treat unresolved U.S. tax forms as a payout-control issue, not a filing-only task. If a form is missing, under review, rejected, or due for revalidation, move the account into a clear exception state before disbursement. Do not assume Apple provides a payout block for every tax scenario; use your own finance or compliance status model where your stack allows it.

Make the audit trail usable, not just present#

Your record should show a single chain from tax-profile request to approval decision to payout outcome and ledger impact. HMRC's baseline is clear: you need records to complete returns correctly, so form evidence alone is not enough if it is disconnected from money movement. Keep sensitive identifiers out of broad operational surfaces and limit full-value access to the case record.

Reconcile tax decisions to money movement#

At month end, reconcile:

- tax-profile status and approval date

- payout events or holds

- related ledger postings

Investigate date mismatches quickly, especially when payout activity appears before tax-status resolution.

For UK filing operations, keep these timing controls visible:

- First-time filers must register for Self Assessment before using the online filing service.

- Existing accounts may need reactivation, and HMRC warns filing without reactivation may delay the return.

- Online filing opens on or after 6 April following the tax year end.

- Tax due is payable by 31 January.

- Missing the return deadline can trigger a penalty.

For multi-market operations, keep global payout-control rules separate from Apple-specific handling so platform-specific logic stays narrow and easier to govern. If you want a deeper walkthrough of the form itself, see How to Fill Out Form W-8BEN-E for a Foreign Company.

Conclusion#

The practical answer is simple: do not optimize for getting Form W-8BEN-E submitted quickly. Optimize for being able to explain, later, why each answer was chosen, who approved it, and what evidence supported it. For a UK limited company handling U.S. withholding documentation, the trouble spots are usually the same: which documentation path you are on, what position you are asserting, and which tax identifier you are relying on.

That means your standard of completion should be higher than "the screen accepted it." A finished case should include the submitted form, the rationale for the key classification fields, the approver name, and proof of what the platform accepted at the time. If an identifier was accepted, keep the screenshot or export. If a form choice was uncertain, keep the escalation note that shows why you paused rather than guessed.

The strongest control is not a heavy process layer. It is a short, reviewable record tied to the exact decision that mattered. In this work, a good minimum case file is often enough: final form copy, decision memo, acceptance evidence, and the cash-side trail showing what happened after submission. HMRC's own guidance is useful here as a records-discipline prompt, because it explicitly says you need to keep records such as bank statements or receipts. That does not replace U.S. withholding documentation, but it does help you prove the money trail.

You should also expect the underlying guidance to move. The IRS instructions for Form W-8BEN-E point filers to IRS.gov/FormW8BENE for future developments, and those instructions include updates that go beyond a narrow platform use case, including section 1446(f) guidance. So if your team treats tax setup as a one-time task, that is a red flag. Recheck when facts change, when ownership changes, when payout outcomes look different, or when the IRS instructions change.

Keep the UK side current too, because operational delays compound fast when tax administration is neglected. HMRC says you must register for Self Assessment before using its online service if you are a first-time filer. It also warns that filing without reactivating an existing account may delay the return, and points to 5 October and 31 January as key deadlines in the process. The point is not that UK filing rules answer U.S. withholding questions. It is that disciplined records, clear owners, and timely revalidation reduce surprises on both sides without forcing you to build more process than the risk justifies.

Frequently Asked Questions

Do UK Apple developers always need an Employer Identification Number, or can a UK Unique Taxpayer Reference be enough?

The evidence set here does not support a blanket rule that an EIN is always required, and it also does not support assuming a UK UTR will always work. HMRC refers to a Unique Taxpayer Reference and notes that some users may still be waiting to receive one. If App Store Connect accepts the identifier you enter, keep a screenshot or export showing that acceptance. If it asks for an EIN, escalate instead of improvising.

When should a UK limited company use Form W-8BEN-E versus Form W-8ECI?

Form W-8BEN-E is the IRS certificate for entities to document beneficial owner status for U.S. withholding and reporting. These sources do not give Apple-specific rules for when a UK limited company should switch to Form W-8ECI, so do not let the UI make that judgment for you. If the facts suggest possible effectively connected income or U.S. trade or business exposure, stop and get specialist review before you submit.

How should we choose a Limitation on Benefits position under the U.S.-UK tax treaty if the case is not obvious?

Do not pick a Limitation on Benefits answer just because one option feels close enough. This grounding pack does not provide treaty test-selection rules, so the right move is a documented rationale, named approver, and escalation where the treaty basis is unclear. If tax, legal, and finance are split, hold submission until one position is approved and recorded.

What are the biggest mistakes in App Store Connect tax setup that lead to withholding or payout issues?

This grounding pack does not provide a verified Apple-specific mistake list. What it does support is avoiding guesswork: do not choose identifiers, treaty positions, or entity fields for convenience without a documented basis. Keep a record of the accepted App Store Connect form state and the payout or withholding outcome so later changes can be explained.

What evidence should we retain in case Internal Revenue Service questions the filing basis later?

Keep the submitted form, the decision memo, approver names, and the treaty or classification rationale in one case record. Add screenshots or exports that show identifier acceptance and the final form state, plus payout and ledger evidence that shows what happened after approval. HMRC also says to keep records needed to complete returns correctly, with examples such as bank statements or receipts, so retain those where they support the cash trail.

How often should we revalidate our Apple tax profile after the initial submission?

There is no supported one-size-fits-all interval in this pack, so revalidate on fact changes, ownership changes, business-model changes, payout anomalies, or any new request from Apple. Also check the current IRS instructions because the IRS directs filers to IRS.gov/FormW8BENE for updates. Do not leave the UK side until the last minute either. HMRC warns that filing without reactivating an existing Self Assessment account may delay the return, and the tax bill is payable by 31 January.

Try a related tool

Asha writes about tax residency, double-taxation basics, and compliance checklists for globally mobile freelancers, with a focus on decision trees and risk mitigation.

With a Ph.D. in Economics and over 15 years of experience in cross-border tax advisory, Alistair specializes in demystifying cross-border tax law for independent professionals. He focuses on risk mitigation and long-term financial planning.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Fill Out Form W-8BEN-E for a Foreign Company

Start here: Form W-8BEN-E is documentation for a foreign entity, not an IRS filing. You send it to the U.S. payer or withholding agent so they can classify the payment and determine whether they may treat your company as a foreign beneficial owner.

How a UK Limited Company Files W-8BEN-E for US Client Payments

How to turn a mandatory compliance document into a practical shield against a 30% withholding tax while keeping payments moving.

How a UK Creative Director Can Invoice a US Client Through a UK LTD Company

Landing a major US client as a UK creative director trading through a limited company is a real step up. It also changes how you get paid. Cross-border payments tend to break in predictable places: unexpected withholding, invoices blocked by onboarding errors, and margin lost to transfer costs you only notice after the money lands.