Quick Answer

Yes. A US LLC plus BVI company setup can be workable when each entity has a narrow role and your paperwork tells one consistent story. The article’s go/no-go test is operational: the contract party, invoice issuer, bank account holder, and signer authority must match before the first payment. It also calls for early checks on Form 5472 exposure, FinCEN Report 114 recordkeeping, and registered-agent files so compliance does not get bolted on later.

Why this structure attracts serious independent professionals#

A US LLC with BVI company blueprint is worth considering only if you treat it as a disciplined operating choice, not as a shortcut around tax, reporting, or legal obligations. If you want a magic offshore outcome, this is the wrong place to start.

This structure can appeal to experienced independent professionals because it can separate roles more clearly. A US LLC can sit closer to day-to-day operations in the United States, while a BVI company may make sense when ownership, holding, or cross-border structuring needs are real. In practice, that can mean clearer role separation on paper, but also more moving parts, more documentation requests, and less room for vague answers.

This article gives you three practical tools. First, decision rules for whether the combined model even fits your business. Second, a setup order you can review with counsel in the United States and the British Virgin Islands. Third, a maintenance checklist so the structure stays explainable after formation, not just on incorporation day. If you are already speaking with advisors, this should help you ask better questions and spot gaps earlier.

An early checkpoint is whether you can keep the basic identity facts consistent across every document set. In real filings, that starts with plain fields such as the state or other jurisdiction of incorporation or organization and the named agent for service. Those details sound administrative, but they are often where sloppiness shows up first. If your formation records, contracts, onboarding forms, and banking files do not point to the same legal reality, you create friction before you create protection.

Another boundary matters just as much. One IRS audit technique guide excerpt dated 5/2009 explicitly says it is not an official pronouncement of the law and that no guarantees are made about technical accuracy after publication. That is a good reminder for this whole topic. Treat articles, checklists, and even some government training materials as orientation tools, not final authority for your personal facts.

Use this as an operator guide, then validate the parts that touch your life with licensed advisors in each relevant jurisdiction. A BVI company is not just an "offshore" label. In formal disclosure, the organizing jurisdiction is stated plainly. For example, British Virgin Islands appears because jurisdiction is a legal fact with consequences. If your goals, ownership, residence, clients, or banking footprint are unclear, pause there first. Serious structures reward clarity and punish improvisation.

Build the mental model before you form anything#

Use this rule first: if you cannot explain each entity's job in one sentence, do not incorporate yet.

| Pre-formation check | Article detail |

|---|---|

| One-line purpose for each entity | If you cannot explain each entity's job in one sentence, do not incorporate yet. |

| Organizing jurisdiction | Keep it consistent with fields like "State or other jurisdiction of incorporation or organization" and "State of Incorporation." |

| Who signs contracts | Sanity-check this before formation so documents point to one legal reality. |

| Bank account holder | Sanity-check this before formation so documents point to one legal reality. |

| Agent for service | Where relevant; example: COGENCY GLOBAL INC. |

A US LLC is usually the onshore operating entity in the United States. A BVI Business Company (BVI BC) is often used only when you have a real cross-border holding, ownership, or investment purpose.

Keep this distinction clear: offshore company describes jurisdiction, while LLC or IBC describes legal form. They are not interchangeable. In formal disclosure, that separation appears in fields like "State or other jurisdiction of incorporation or organization" and "State of Incorporation." One filing shows Cayman Islands as jurisdiction; another shows Delaware and separately lists IRS Employer Identification No. 86-1032927.

Before formation, sanity-check that your documents point to one legal reality:

- one-line purpose for each entity

- organizing jurisdiction

- who signs contracts

- bank account holder

- named agent for service where relevant (for example, COGENCY GLOBAL INC. appears in one New York service-of-process disclosure)

The common failure mode is role mixing, not complexity. If a BVI holding vehicle appears in service contracts, invoices, or onboarding files without a clear reason, you create confusion before protection.

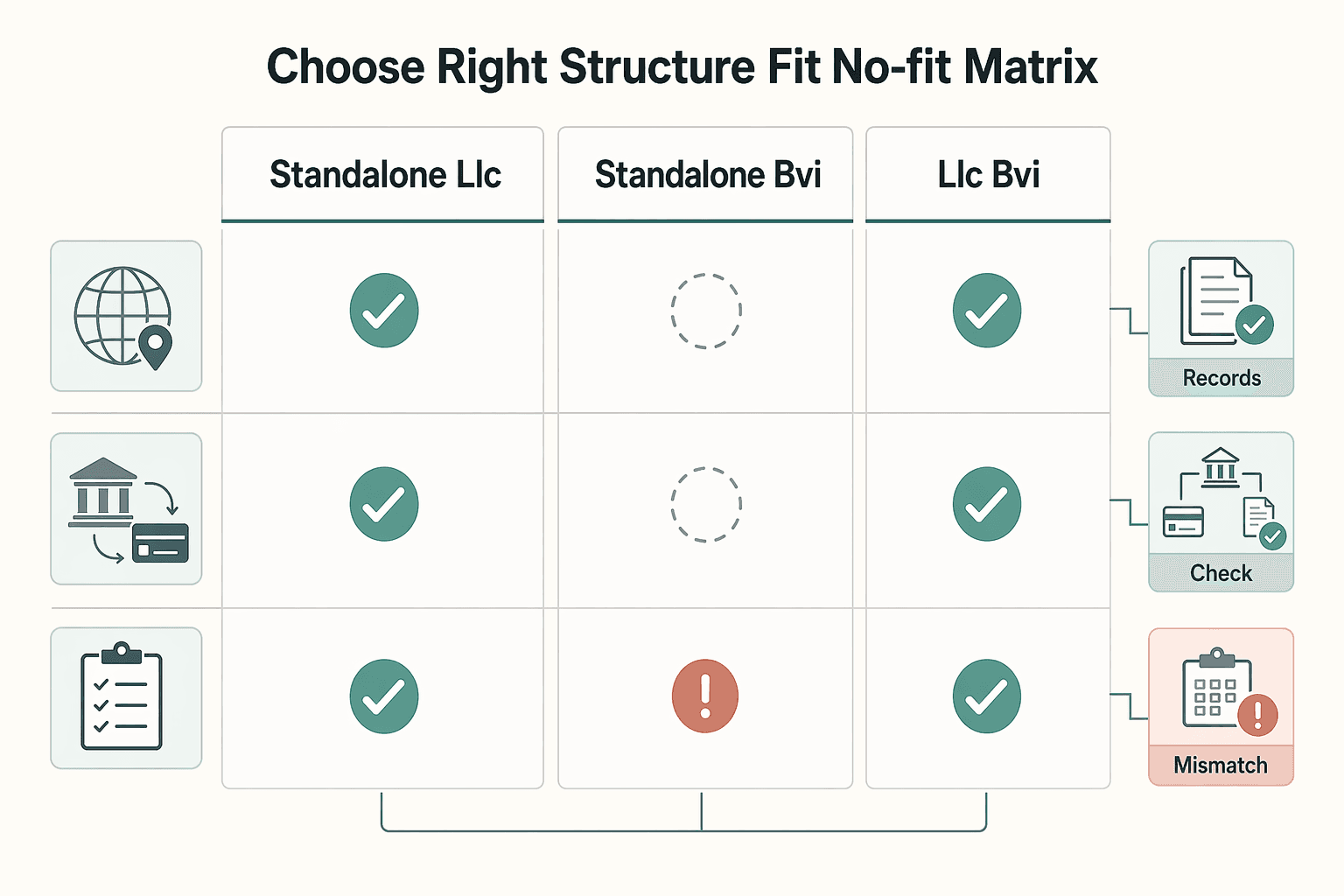

Choose the right structure with a fit and no-fit matrix#

Start with the simplest structure that matches how you actually operate. If your clients, revenue, and day-to-day work are mostly in the United States, a single US LLC is usually the cleaner default. Add a BVI company only when you can document a real cross-border ownership, banking, or investment need and define each entity's job clearly.

| Path | Usually fits when | No-fit signals | What to verify before filing |

|---|---|---|---|

| Standalone US LLC | Revenue and contracts are mainly US-based, and you want fewer moving parts. | You are adding international complexity before the business needs it. | Your US jurisdiction of incorporation or organization, who signs contracts, and which entity holds the operating bank account. |

| Standalone BVI company | Ownership and counterparties are genuinely cross-border, and you do not need a US operating shell as the main contracting entity. | Most work is still US-centered, with no clear reason to run operations through a second jurisdiction. | Whether the BVI entity will actually be used in contracts, invoices, and onboarding, not kept as a disconnected paper entity. |

| US LLC + BVI company | You can clearly split roles (for example, US operations vs. cross-border holding/ownership) and both entities solve real needs. | Low revenue, low complexity, no international expansion plan, or no documented reason for the second entity. | Ownership chart, contract flow, bank flow, and signing authority for both entities before launch. |

Before choosing a combined setup, pass three checkpoints. First, map client geography. Second, confirm banking and payment flow so the invoicing entity, account holder, and contract party line up. Third, be realistic about compliance tolerance, because two entities mean two maintenance tracks.

Then choose jurisdictions with paperwork discipline, not branding logic. Public filings show Delaware and British Virgin Islands in the field labeled "State or other jurisdiction of incorporation or organization," which is how regulators and counterparties read legal structure. If you choose Wyoming, Delaware, or British Virgin Islands, confirm the records, roles, and named agent for service are consistent from day one.

Use one red-flag test before you proceed: if you cannot state which entity signs client contracts and which entity receives funds, do not use the combined route yet.

If ongoing filings already feel hard to sustain, simplify now. A USVI public notice states that failure to pay franchise taxes or fees and file annual reports for five or more years can lead to administrative dissolution, and the entity name can become available to others. That notice is not a BVI rule, but it is a practical reminder that each added entity increases maintenance risk. Related: What is FinCEN? A Guide for Freelancers and FinTech Users.

Pick ownership and control logic that survives scrutiny#

Your ownership and control chain should be explicit on paper, not implied. If you cannot show who owns the US LLC, who controls the BVI Business Company (BVI BC), and where that authority was approved, stop and fix it before contracts or banking.

Control failures are not theoretical. A Delaware opinion describes a CEO initiating a sale process without board authorization and giving the board incomplete information about back-channel communications. Different context, same operational lesson: unclear authority creates avoidable risk.

| Pattern | What to lock down first |

|---|---|

| Holding company model | Document who owns each entity, who can approve major decisions, and who can sign for each company. |

| Investment vehicle model | Separate operating authority from investment authority in writing, and map both to named decision-makers. |

| Trust-owned company | Use a plain ownership-and-control chart that shows legal ownership and practical decision control, then align company documents to it. |

| Limited Partnership (LP) | Show who controls the LP, how that control flows into any company interests, and who can bind each entity. |

Choose one control chain and write it down#

Use one consistent chain across all documents. If the BVI company owns the LLC, the LLC documents and BVI approvals should both say that clearly, and signer authority should match.

If one person is involved across both entities, still document each legal capacity. Signing as LLC manager is a different capacity from signing as BVI director unless the records authorize both roles.

A practical cross-check is to mirror the clarity seen in standard filing headers: "State or other jurisdiction of incorporation or organization" and "agent for service." For example, filings can list British Virgin Islands in that jurisdiction field. Your internal records should be at least that clear on legal home, contact point, and authority chain.

The hard stop rule#

If beneficial ownership is unclear on paper, stop and resolve it before launch.

Build a minimum evidence pack that can be reviewed quickly:

- One-page ownership and control chart (all entities plus human decision-makers).

- Written approvals/resolutions for ownership, control, and signing authority.

- Role definitions for registered agent/agent for service, directors, members/managers, and day-to-day operators.

A combined structure works when the chart, approvals, contracts, and jurisdiction details tell the same story.

Execute incorporation in the right order#

Use this launch order: define roles, form the US LLC, form the BVI company through a registered agent, then align contracts, invoicing, and payment rails before go-live.

Form only after each entity has one clear job#

Set each entity's role in writing first, then build the documents in that same order. For the US side, keep the formation document, operating agreement, beneficial ownership records, and authority resolutions aligned. For the BVI side, keep incorporation records, registered-agent paperwork, beneficial ownership records, and director or board resolutions aligned.

Before launch, run a simple consistency check: legal name, signer title, and ownership position should read the same way across the ownership chart, resolutions, contracts, and invoice setup.

Build compliance gates before money moves#

| Compliance gate | What to review |

|---|---|

| Form 5472 review | Identify potential filing triggers early, especially before related-party flows begin. |

| FinCEN/FBAR step review | Identify who may have a filing obligation and set recordkeeping from day one. |

| BVI substance review | Confirm whether planned activity may fall under economic substance rules and what local evidence should be retained. |

On the US side, identify potential Form 5472 triggers early, especially before related-party flows begin. Do the same for FinCEN/FBAR: identify who may have a filing obligation and set recordkeeping from day one. FinCEN's FBAR materials state that each account is valued separately, maximum account value is a reasonable approximation of the greatest value during the year, and amounts are recorded in U.S. dollars rounded up to the next whole dollar (for example, $15,265.25 becomes $15,266). FinCEN also maintains an FBAR due-date resource and publishes event-based extension notices.

On the BVI side, confirm whether planned activity may fall under economic substance rules and what local evidence should be retained.

Final checkpoint before go-live#

Before sending the first invoice, confirm the legal entity providing the service is the same entity named in the contract and invoice flow. If those do not match, fix the documents and authority chain before funds move.

Run ongoing compliance like an operating system#

Once the entities are live, drift is the main risk, not formation. Treat recurring compliance as an operating routine so your US LLC and BVI company stay usable under review.

Use your own monthly, quarterly, and annual checklist as a control tool, then map each item to real legal deadlines confirmed by your tax advisor, registered agent, company secretary, or local counsel. Your internal cadence keeps execution on track; the actual filing and renewal dates still depend on your facts and jurisdictions.

| Internal cadence | What you check | Evidence to save |

|---|---|---|

| Monthly | Bank or payment account changes, new signers, related-party transfers, ownership or role updates, statements needed for FBAR tracking | Statements, account-opening records, signer lists, transfer support, updated ownership chart |

| Quarterly | Form 5472 input status, related-party agreements, director/member decisions needing written approval, policy exceptions | Draft agreements, approval notes, resolutions, exception log |

| Annual | Filing calendar, corporate renewals, authority records, and final FinCEN/tax reporting evidence pack | Renewal confirmations, final resolutions, advisor checklist, year-end audit folder export |

For FinCEN Report 114, keep the FBAR record trail current all year. FinCEN says the maximum account value is a reasonable approximation of the greatest value, and periodic statements may be used when they fairly reflect that maximum. Track each account's high-water value, keep the source statements, and note account currency so conversion can be done with the Treasury's Financial Management Service rate. When values are reported, they are rounded up to the next whole U.S. dollar (for example, $15,265.25 becomes $15,266).

Keep one audit folder for the full structure, not scattered records across inboxes and drives. At minimum, store meeting notes, ownership changes, related-party agreements, policy exceptions, account statements, signer approvals, and member/director resolutions. Your verification standard is simple: if someone asks who approved a signer or why a transfer happened, you can show one document immediately.

Set one hard decision rule: if compliance tasks are repeatedly late, simplify before scaling revenue. If Form 5472 inputs, FinCEN evidence, or approvals are consistently missed, your structure is likely too complex for current capacity.

Design money movement so audits are easy#

Design the flow before volume starts: each payment should be traceable from invoice to collection, FX conversion, and payout, and tied clearly to the correct US LLC or BVI company.

| Flow stage | Record it this way | Exception owner |

|---|---|---|

| Client invoice | Entity named, invoice ID, contract match | Person who confirms entity and contract alignment |

| Collection | Provider reference, date, payer, amount | Person who resolves unmatched deposits |

| FX conversion | Conversion reference, source/destination accounts, internal rate snapshot | Person who approves rebooking if quotes expire |

| Payout | Approval record, beneficiary, purpose, final ledger posting | Person who handles payout exceptions |

Where your providers support it, use compliance gates instead of informal transfers: complete KYC/KYB checks before new payees, require explicit approvals before inter-entity payouts, and keep the approval trail with provider confirmations.

Define failure handling in advance so exceptions do not become ad hoc decisions: unmatched deposits stay unresolved until invoice/entity matching is complete, AML-related holds pause downstream movement, and stale quotes or payout failures are logged with the final action and approver.

Keep records as searchable working documents, organized by entity and month, so they are easy to reference during review. For both United States and British Virgin Islands activity, reconciliation is complete only when one transaction can be traced end to end with consistent entity, amount, and purpose.

Catch the red flags before they become expensive#

Treat this first as a compliance design issue, not a tax outcome. In an onshore-offshore structure, the offshore entity does not remove reporting work, and your records still need to stand up when a bank, accountant, or regulator asks questions.

| Red flag | What to check |

|---|---|

| FinCEN Report 114 mechanics | Show each account valued separately, the maximum account value captured as a reasonable approximation of the year's highest value, and amounts recorded in U.S. dollars rounded up to the next whole dollar. |

| Entity mismatch without documentation | If the BVI company is on the contract but funds move through a different entity, create and store a written rationale before the first payment. |

| Strategic drift | If you cannot explain the advantage over a single US LLC in two or three concrete sentences tied to real banking, ownership, or cross-border needs, simplify first. |

If foreign financial accounts are involved, pressure-test your process against FinCEN Report 114 mechanics. You should be able to show each account valued separately, the maximum account value captured as a reasonable approximation of the year's highest value, and amounts recorded in U.S. dollars rounded up to the next whole dollar. For non-U.S. currency accounts, your conversion method should align with the Treasury Financial Management Service rate.

A second red flag is entity mismatch without documentation. If the BVI company is on the contract but funds move through a different entity, create and store a written rationale before the first payment. Put it in your contract set, intercompany documentation, or approval record so your team can explain who earned the income and why another entity handled cash.

A final red flag is strategic drift: no clear reason this setup beats a single US LLC at your current stage. If you cannot explain the advantage in two or three concrete sentences tied to real banking, ownership, or cross-border needs, simplify first.

Related reading: The Global SaaS Founder's Blueprint: Combining a Delaware C-Corp with a Stripe Atlas Account.

Use complexity only when it buys real operational advantage#

Use a second entity only if it makes your operating model easier to explain and maintain over time. The durable version is compliance-first: clear role separation, documented control, and ongoing filings that stay current.

Start with proof, not theory#

Your fit test should be simple: can you state each entity's role in one clear sentence and keep that same logic across your documents and operations? If that story shifts between records, the structure is not ready.

Before launch, finalize a document pack that makes control and role assignment easy to follow without guesswork. The key checkpoint is consistency from entity records to contracts, banking responses, approvals, and payment flow.

Validate assumptions before you scale it#

Once the structure is documented, validate your assumptions with qualified advisors before money starts moving. Ask for written edits to the core documents and compliance calendar, not only verbal feedback.

If your reviewers cannot align on control, role assignment, or how the model should be described to counterparties, pause and resolve that first. Scaling disagreement creates avoidable review risk later.

Build controls around the lookback, not the launch#

Ongoing evidence matters more than setup day. In a SEC annual report, the filer had to attest to required filings over the preceding 12 months, confirm required Interactive Data Files in that same period, and confirm it had been subject to filing requirements for the past 90 days.

Use that operating lesson directly: build controls that stay explainable over time, not just at incorporation. Keep one audit trail for filings, approvals, account records, and exceptions so your model remains defensible as complexity grows.

Frequently Asked Questions

What is a US LLC with a BVI company blueprint in plain terms?

A us llc with bvi company blueprint is a two-entity setup often used to separate roles: one entity for active operations and another for holding or cross-border activity. The key idea is role clarity, not paperwork avoidance. If you cannot explain each entity’s purpose in one clear sentence, you are not ready to add the second company.

Who is a strong fit for a combined US LLC and BVI company structure?

This is generally a better fit when there is a real cross-border operating need and a clear reason for role separation. Structure choice can affect tax strategy, operational autonomy, and market approach, so fit should follow the business you are actually running today. Before filing, make sure your ownership map, authority decisions, and contract flow align.

When should I stay with only a US LLC instead of adding a BVI company?

Stay with one LLC if your business is still mostly domestic and you do not yet need a separate offshore role. A common red flag is adding a second entity because it sounds more protective or more global without a current business reason. If you cannot defend the extra entity in plain language, keep it simple.

What minimum compliance steps should I complete before launch?

Do not send the first invoice until your core documents are complete and consistent across entities. At minimum, your records should clearly show ownership, control, who signs contracts, and which entity receives funds. A common failure mode is documents saying one thing while contracts and payments show another.

Which ongoing obligations are easiest to miss for US persons?

The easiest issues to miss are recurring filing, reporting, and fee deadlines when no one clearly owns the calendar. Keep one compliance calendar and one audit folder for approvals, agreements, and key records. Long periods of missed reports can lead to serious consequences in some jurisdictions, including administrative dissolution after years of noncompliance.

How do I choose between Wyoming, Delaware, and a British Virgin Islands setup?

Start from operating facts, not jurisdiction labels. An offshore company is simply a legal entity formed outside your principal country of residence or primary business activity. From there, choose the structure that best matches your real operations and can be maintained with consistent ongoing compliance.

What are the main tradeoffs between simplicity, cost, and cross-border flexibility?

A single US LLC is usually simpler to run and explain. Adding a BVI company can improve role separation for cross-border activity, but it also adds ongoing compliance work and more opportunities for contradictions across contracts, payments, and governance. If you are on the fence, choose the structure you can keep current, documented, and defensible a year from now.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- bsaefiling.fincen.gov/docs/FinCENFBARElectronicFilingRequirements.pdftrusted

- commerce.gov/sites/default/files/2026-02/DOCFY2025AFR_508...trusted

- courts.delaware.gov/Opinions/Download.aspxtrusted

- energy.gov/sites/default/files/2025-12/NPC_Permitting_r...trusted

- fincen.gov/reporting-maximum-account-valuetrusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/pub/irs-utl/constructionindustry_atg.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

What Is FinCEN for Freelancers and FinTech Users

If you are asking **what is fincen**, focus first on the decision in front of you. FinCEN, the Financial Crimes Enforcement Network, is tied to FBAR filing through FinCEN Form 114 when foreign financial accounts create reporting duties. By the end, you should know whether to act now, gather records, or escalate.

How to Incorporate a Company in the British Virgin Islands (BVI)

A BVI company can be useful for a solo operator, but only in a narrow set of circumstances. If your business is genuinely cross-border, your clients are comfortable contracting with an entity, and you are prepared for real compliance and documentation work, it can be a strong tool. If you are looking for a shortcut on tax, admin, or banking, it is usually the wrong one.