Quick Answer

Use a pre-kickoff workflow: send Form W-8BEN-E to the payer, match your UK LTD legal details to the signed contract, and confirm AP onboarding before the first invoice. Then issue invoices with client-required fields and lock payment route details upfront. After payment one, reconcile amount invoiced, amount sent, amount received, and FX evidence so deductions are visible early.

Landing a major US client as a UK creative director trading through a limited company is a real step up. It also changes how you get paid. Cross-border payments tend to break in predictable places: unexpected withholding, invoices blocked by onboarding errors, and margin lost to transfer costs you only notice after the money lands.

The fix is to set the whole payment path up before the work starts. Most expensive problems come from treating tax forms, entity details, and payment instructions as something to sort out later. A one-person company needs a repeatable process from the outset. The three stages below help you get through client onboarding, send invoices that move cleanly through AP, and protect what actually reaches your account.

Stage 1: Onboard to Eliminate Risk Before Work Begins#

Before kickoff, get your tax packet accepted by the client's withholding and AP process so the first invoice does not stall.

| Before-work item | What to send/check | What to confirm |

|---|---|---|

| Entity details | Use your exact legal entity name, country of incorporation, and tax ID details, and match all of it to the exact contract party name | Exact match to the contract party name |

| Onboarding packet | Send the signed contract, your entity details exactly as shown in the contract, and a completed Form W-8BEN-E immediately after signature | Written acknowledgment that onboarding is in progress and the named AP or vendor contact |

| Tax form routing | For a UK LTD, use W-8BEN-E, not W-8BEN, and give it to the payer or withholding agent, not the IRS | Tax form received by the payer or withholding contact, and no additional pre-invoice tax document requested |

| Pre-invoice status | Confirm the form is accepted, the supplier record is live, and there is no open request for missing or inconsistent tax information | All three confirmed before work begins |

Pre-send check, same day the contract is signed: use your exact legal entity name, country of incorporation, and tax ID details. Match all of it to the exact contract party name.

- Send your onboarding packet immediately after signature.

Send it before the first project meeting. Address your day-to-day client owner, and copy AP or vendor onboarding plus legal or procurement if they approve suppliers. Include the signed contract, your entity details exactly as shown in the contract, and a completed Form W-8BEN-E. Before work starts, get written acknowledgment that onboarding is in progress and confirm the named AP or vendor contact.

- Send Form W-8BEN-E to the right place.

For a UK LTD, use W-8BEN-E, the entity form, not W-8BEN, the individual form. Give it to the payer or withholding agent, not the IRS. Before work starts, confirm the tax form has been received by the payer or withholding contact and that no additional pre-invoice tax document is being requested.

- Explain the form in terms the client can act on.

State that it documents foreign entity status and identifies your company as the beneficial owner for withholding purposes. If treaty treatment is being claimed, note that eligibility depends on treaty residence, beneficial ownership, TIN requirements, and limitation-on-benefits conditions. Rates or exemptions vary by country and income type. Keep treaty wording under tax or legal review. For completion detail, use A UK Limited Company's Guide to Filling Out Form W-8BEN-E.

- Use this client-side processing map to preempt common blockers.

| AP/legal blocker | How you preempt it before kickoff |

|---|---|

| Entity details do not match contract party records | Match legal entity details across contract, onboarding records, and W-8BEN-E Part I. |

| Part I identifiers are incomplete | Complete core entity identifiers, including organization name and country of incorporation, before sending. |

| Reduced-rate claim fields are missing | If claiming treaty treatment, complete all fields needed to support entitlement. |

| Information is inconsistent across documents | Cross-check form entries against contract and onboarding data before submission. |

If the client treats payment as U.S.-source FDAP income, withholding can default to 30% (or lower treaty) on a gross basis. The outcome depends on income classification and valid documentation. Before work begins, confirm three things: the form is accepted, the supplier record is live, and there is no open request for missing or inconsistent tax information.

Once onboarding is accepted, the next risk is simpler but just as common: an invoice that no longer matches what the client has on file. If you want a deeper dive, read Understanding the UK's Statutory Residence Test (SRT).

Stage 2: Craft a Bulletproof Invoice That Gets Paid Faster#

Keep the invoice process simple. Start with the compliance basics you can verify: business structure, Self Assessment status, and record-keeping.

| Checkpoint | What to verify | Timing |

|---|---|---|

| Business structure | Confirm whether you operate as a sole trader or limited company | Before sending |

| Sole trader registration need | Check whether sole trader registration is needed, for example if earnings are over £1,000 in a tax year | Before sending |

| Legal business name | Verify the legal business name used in your records | Before sending |

| Record support | Store each invoice with related records, such as bank statements or receipts | Before sending |

| HMRC notification | Tell HMRC by 5 October if you need to file for the previous tax year | 5 October |

| Return filing window | Returns can be filed on or after 6 April after tax year end | On or after 6 April after tax year end |

| Tax payment timing | Self Assessment tax bill is due by 31 January | By 31 January |

Use a pre-send checklist so your records stay consistent and your tax return work does not get delayed later.

Step 1#

Confirm your legal business setup first. The business structure you choose affects how you pay tax and your legal responsibilities. If you operate as a limited company, it is legally separate from the people who own it.

Include and verify these basics:

- Your business structure (sole trader or limited company)

- The legal business name used in your records

- Whether sole trader registration is needed (for example, if earnings are over £1,000 in a tax year)

- A record-keeping routine for invoices and supporting documents

Before you send the invoice, store it with related records, such as bank statements or receipts, so your tax return can be completed correctly.

Step 2#

Set your Self Assessment status before deadlines bite. If you need to file for the previous tax year, you must tell HMRC by 5 October. Telling HMRC after that date can lead to a penalty. If you previously had Self Assessment but stopped filing, reactivate the account before you file to avoid delays.

| Compliance checkpoint | Why it matters | Pre-send check |

|---|---|---|

| Self Assessment registration | Required if you need to file for the previous year | Registration completed by 5 October |

| Existing account reactivation | Filing can be delayed without reactivation | Account status confirmed before filing |

| First-time online filing access | First-time filers must register before using the online filing service | Registration completed before online filing |

Step 3#

Treat VAT wording and client AP fields as case-specific. VAT wording and client routing fields are not universal rules in this guidance. Confirm those details separately for your exact situation before you issue invoices.

Final QA gate before send:

- Self Assessment registration or reactivation status is confirmed

- Records are complete and easy to retrieve

- Filing timing is planned (returns can be filed on or after 6 April after tax year end)

- Payment timing is planned (Self Assessment tax bill is due by 31 January)

Once those checks are clear, move to your payment-operations workflow. For a practical walkthrough, see How a French Micro-Entrepreneur Can Invoice a US Client.

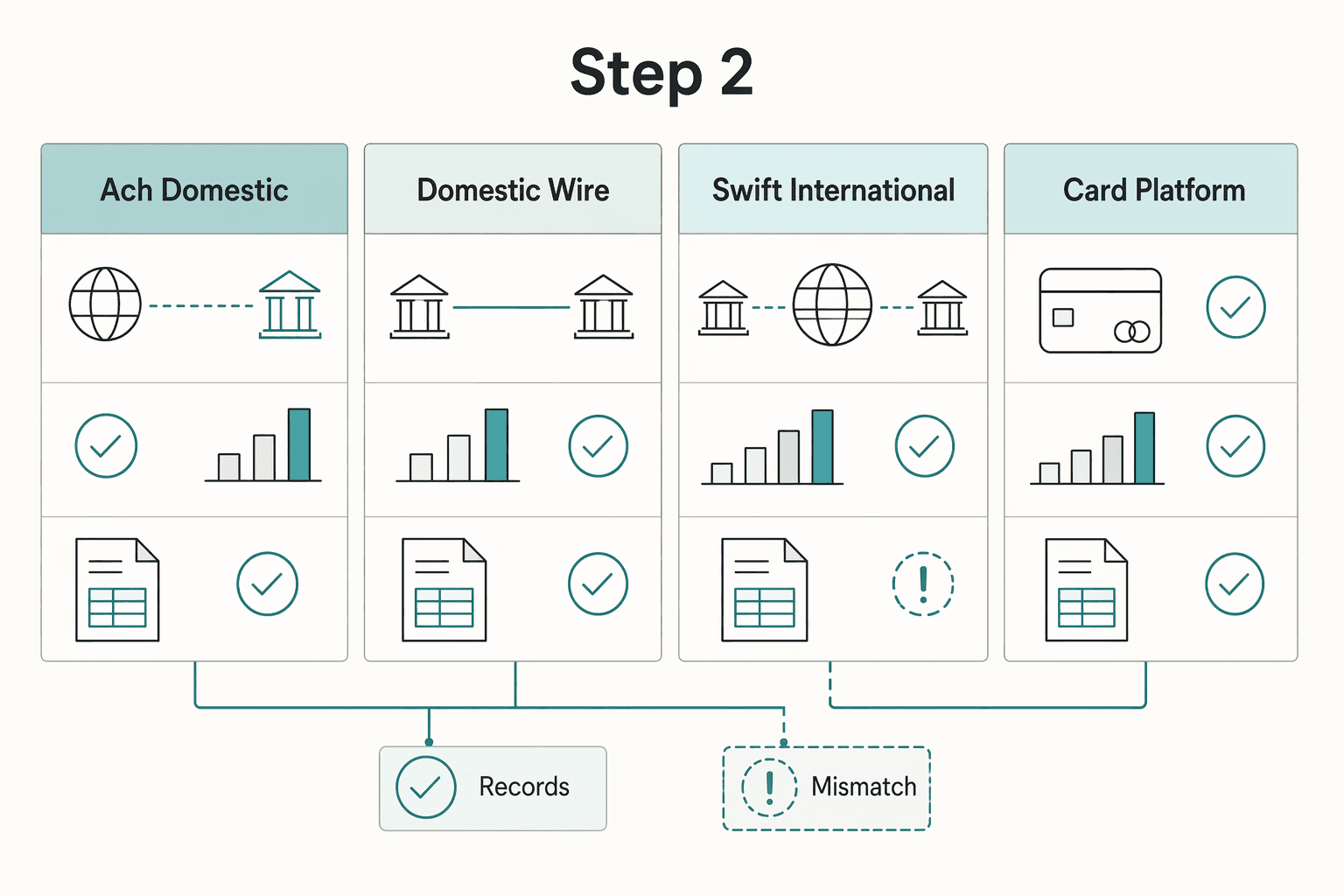

Stage 3: Protect Your Profits from Hidden Transfer Fees#

Once payment is approved, your margin is shaped by the route, the FX treatment, and any deductions along the way. For a UK LTD invoicing a US client, losses can still show up after the client has paid.

| Cost item | What to check |

|---|---|

| FX spread | Markup inside the conversion rate from USD to GBP; use the mid-market rate as your benchmark for hidden markup |

| Platform fee | Provider fee charged by the payment platform |

| Sender fee | Fee charged to the client when they initiate payment |

| Recipient fee | Fee charged on receipt by your bank or provider |

| Intermediary bank fee | Possible deductions on SWIFT or correspondent routes before funds reach you |

| Settlement delay cost | Timing differences that affect cash flow, reconciliation timing, and conversion outcome |

Step 1#

Look at transfer cost line by line, not as one headline fee. Check each payment against six items you can verify on remittance advice, platform reports, and bank statements:

- FX spread: the markup inside the conversion rate from USD to GBP. Use the mid-market rate as your benchmark for hidden markup.

- Platform fee: provider fee charged by the payment platform.

- Sender fee: fee charged to the client when they initiate payment.

- Recipient fee: fee charged on receipt by your bank or provider.

- Intermediary bank fee: possible deductions on SWIFT or correspondent routes before funds reach you.

- Settlement delay cost: timing differences that affect cash flow, reconciliation timing, and conversion outcome.

Typical timing differs by rail. ACH is usually 0-3 working days, domestic wire can be same day or next working day, and SWIFT or international wire is commonly 1-6 working days, with route variation.

Verification point: after the first payment from any new client, reconcile the invoice amount, amount sent, amount received, deductions, and conversion rate used. If you cannot explain the gap line by line, the route is not transparent enough.

Step 2#

Choose the rail based on the invoice, not the client's default habit. Use the method that gives you the best balance of transparent landed cost, predictable payout, and clean records.

| Payment method | Total cost transparency | Payout predictability | Operational friction for US client | Dispute or hold risk | Bookkeeping clarity |

|---|---|---|---|---|---|

| ACH to your domestic USD details | Usually clearer when local USD details and itemized conversion are available | Typical 0-3 working days | Low | Lower card-dispute exposure than card rails | Strong when remittance and FX records are saved |

| Domestic wire to your USD details | Usually clear on sender side; confirm incoming fees on your side | Often same day or next working day | Moderate, bank setup or approval may be needed | Lower reversal risk than card rails once processed | Strong when wire confirmation matches receipt |

| SWIFT/international wire | Lower transparency if correspondent deductions occur | Typical 1-6 working days, uneven by route | Higher, more routing fields | Lower card-dispute exposure, but higher delay and deduction risk | Weaker if landed amount differs from instructed amount |

| Card/platform checkout | Fees and FX components may be split across reports | Can feel fast at capture, but post-settlement risk remains | Low | Higher: disputes can reverse funds; some new PayPal sellers may see holds of up to 21 days | Often messier due to separate fee, dispute, and FX records |

Use this quick rule:

- Recurring retainers: prefer ACH to domestic USD details for repeatable monthly reconciliation.

- Milestone payments: use domestic wire when payout predictability matters and fees are confirmed in advance.

- One-off large invoices: compare domestic wire vs SWIFT on the exact corridor, fee allocation, and provider limits.

Step 3#

Standardize USD-to-GBP reconciliation so every payment is audit-ready. Pick one consistent FX method and one evidence-pack format, and use them for each transaction.

For each payment, save:

- Invoice

- Client remittance advice or payment confirmation

- Bank or platform receipt showing gross amount, deductions, and settlement date

- FX rate source used in your books, for example HMRC monthly table or your chosen method

- Ledger entry mapping USD receipt, GBP book value, fees, and variance notes

Your company must keep adequate accounting records. For corporation tax, HMRC guidance states keeping business records for 6 years from period end; company-law baseline for private companies is 3 years, so use the longer retention standard in practice.

For VAT handling, amounts must be expressed in sterling, and where VAT is payable, the VAT amount must be shown in sterling even if the invoice is in foreign currency.

This gives you a fast, evidence-based answer when a client says they paid in full but your landed amount is lower. For deeper margin control across projects, read The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business.

You might also find this useful: How to Invoice a US Client from Mexico as a Temporary Resident.

Before you lock your payment method into client terms, run your expected USD-to-GBP paths through the Payment Fee Comparison to choose the rail with the cleanest net outcome.

From Invoice Admin to Strategic CEO#

This is not paperwork for paperwork's sake. It is how you make sure the contract, tax setup, invoice, and payment route all tell the same story. When they do, you cut avoidable admin friction and your records are easier to defend if questions come up.

If your HMRC access or filing status is unclear, resolve that before you treat client setup as complete. Then work through the checkpoints below.

Lock the filing checkpoints first#

Start with the UK admin items that can block filing later. If this is your first filing, register for Self Assessment before using the online filing service. If you already had an account but it has been inactive, confirm whether reactivation is required, because HMRC says filing without reactivation may delay your return.

Use UTR status as a hard gate. If you are waiting for your Unique Taxpayer Reference, track HMRC's expected reply timing before you finalize your filing plan. Keep records from day one, including bank statements and receipts, so each payment and expense is supportable.

If you need to file for the previous tax year, HMRC's cited guidance uses 5 October as the notification point, filing on or after 6 April after tax year end, and payment by 31 January. Verify current-year dates before relying on example-year guidance.

Run every client through one standard#

| Workflow point | Reactive habit | Operating standard | Practical outcome |

|---|---|---|---|

| Onboarding documentation | Waiting for requests after work starts | Confirm contracting entity, payee name, and client-requested tax/admin documents before kickoff; mark any gap as [verify current requirement] | Lower risk of onboarding holds |

| Invoice completeness check | Reusing an old edited invoice | Use one approved template and confirm required fields with the client's AP contact or adviser where needed | Smoother approvals |

| Payment-rail selection | Accepting whatever route appears last-minute | Agree currency, remittance details, and payment route before first invoice; run a first-payment check | Lower risk of unexplained deductions |

| Reconciliation follow-through | Matching only what arrived | Reconcile invoice amount, amount sent, amount received, and settlement date; retain supporting records | Clearer records for review |

Keep structure, contract, and money flow aligned#

Alignment matters more than speed. If you invoice through a limited company, use that same company name consistently across the contract, invoice, and receiving account. HMRC's setup guidance frames the tradeoff clearly: a company is legally separate and owner debt responsibility is capped at invested value, but directors must follow rules when taking money out.

Operating standard: no kickoff, no invoice issue, and no repeat use of a payment route until filing checkpoints are clear, onboarding and admin items are complete, and the first payment reconciles cleanly.

Related: UK Creative Director With a US LLC: Filing Readiness, Classification, and Distribution Risk.

If you want a cleaner first draft before sending terms to a US client, build it with the Free Invoice Generator and then add your company-specific compliance details.

Frequently Asked Questions

Do I charge VAT to a US client from the UK?

Do not assume yes or no from a template. Verify VAT treatment and invoice wording with a qualified VAT adviser before you lock your template.

Which form should I send, W-8BEN or W-8BEN-E?

Do not guess. Verify form selection with a qualified adviser. If the adviser confirms W-8BEN-E is appropriate, use A UK Limited Company's Guide to Filling Out Form W-8BEN-E.

How do I avoid being taxed twice between the UK and US?

Do not rely on a blanket treaty answer. Ask a qualified cross-border adviser to review your specific facts before payment starts.

What currency should I invoice in?

Agree currency with your client before the first invoice, then keep your records consistent for each payment.

Can my US client pay my UK company directly into a UK bank account?

Payment setup can vary by client and bank. Confirm payment route details before the first transfer, then reconcile what you invoiced against what you received.

Do I need to do anything with HMRC before filing if this is my first time?

Yes. If this is your first filing, do not leave HMRC setup until the deadline. HMRC says you must register for Self Assessment before first-time filing, and you need your UTR to sign in and file online. If you need to complete a return for the previous tax year, tell HMRC by 5 October, file on or after 6 April after tax year end, and plan to pay by 31 January.

What if I already had a Self Assessment account but have not used it in a while?

Check reactivation before you file. HMRC says you may need to reactivate an existing account, and filing without reactivation may delay your return. Test access early and keep records such as bank statements and receipts ready so your return can be completed correctly.

Does it matter that I invoice as a limited company rather than as a sole trader?

Yes. It affects both tax handling and legal responsibility. HMRC says business structure affects how you pay tax and your legal responsibilities: a limited company is legally separate, while a sole trader has personal responsibility for business debts. Keep your contracts, invoicing, and records aligned to the structure doing the work.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- bis.org/cpmi/publ/swift_gpi.pdftrusted

- bis.org/cpmi/paysysinfo/corr_bank_data.htmtrusted

- federalreserve.gov/paymentsystems/fedfunds_about.htmtrusted

- irs.gov/individuals/international-taxpayers/claiming...trusted

- irs.gov/pub/irs-pdf/fw8bene.pdftrusted

- paypal.com/us/legalhub/paypal/useragreement-fulltrusted

- wise.com/help/articles/2932150/guide-to-usd-transferstrusted

- gov.uk/self-assessment-tax-returns/registeringexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Stop Freelance Profit Margin Erosion Before It Hits Cashflow

Revenue can hold steady while the business underneath it gets weaker. What comes in matters, but what you keep after the work is delivered is the clearer signal of health.

Understanding the UK's Statutory Residence Test (SRT)

Treat SRT like ops, not folklore. You want a repeatable workflow you can run monthly so your tax-year answer is boring, documented, and easy to defend.

How a UK Limited Company Files W-8BEN-E for US Client Payments

How to turn a mandatory compliance document into a practical shield against a 30% withholding tax while keeping payments moving.