Quick Answer

Yes: payment tokenization replaces a card’s PAN with a token so your app can run checkout, one-click, and recurring charges without storing raw card numbers in normal paths. In what is tokenization payments terms, the core boundary is simple: your systems keep token references while the token vault keeps PAN mapping. It reduces exposure, but it does not make PCI DSS obligations disappear. For platform teams, the practical decision is token model plus portability terms before launch.

Why Tokenization Matters#

Tokenization solves a practical platform problem: you can accept cards and run card-on-file flows without using or storing raw card numbers in your normal application paths. In operator terms, it replaces the primary account number (PAN) with a token, so your systems work with that tokenized reference instead of the real card data.

If you are building checkout, subscriptions, one-click payments, or repeat billing, that is usually the real question behind "what is tokenization payments." You need to know where card details enter, where the token is created, and whether sensitive card data stays with the processor or tokenization service. Your team should be reusing tokens for future charges, not handling raw card data.

A token is a random string that stands in for sensitive payment information. The basic flow is simple:

- Collect card details at checkout.

- Generate a replacement token.

- Store sensitive card data securely with the processor.

- Complete the transaction using the tokenized reference.

That is why tokenization matters for repeat purchases, subscriptions, and one-click checkout. A useful first checkpoint is to map every downstream path, then confirm those services use tokens rather than raw values or retained copies.

Two cautions matter from the start. Coverage is not automatic, and partial coverage is a common failure mode. Portability is also a real constraint, so choices you make now can affect how easily you can migrate later.

What follows is practical: clear definitions, the checkout-to-reuse lifecycle, and the main operator decisions, including launch checks, day-two operations, and where provider setup can change what is available.

What payment tokenization means in operator terms#

In practice, tokenization means your product uses a token instead of the raw Primary Account Number (PAN) in normal application paths. Card data is captured and replaced with a payment token. Your platform then runs authorizations, retries, and card-on-file charges against that tokenized reference.

The control that matters most is the storage boundary. Your systems keep the token, while the real PAN stays in a secure token vault operated by a tokenization provider. That provider handles token generation, storage, verification, and lifecycle management. Your first practical check is coverage: confirm that downstream services, including retries, support tooling, and exports, reference tokens rather than copied PAN fields.

The terms that matter#

| Term | Definition | Use |

|---|---|---|

| Payment token | Unique random value | Stands in for sensitive card data. |

| PAN | Actual card number | Identifies the cardholder account and issuer. |

| Token vault | Secure store | Keeps the PAN-to-token mapping, including usage parameters. |

| Network token | Token model | Managed by card networks. |

| Card-on-file | Stored payment credentials | Used for repeat purchases, recurring payments, and one-click flows. |

A single PAN can map to multiple tokens based on channel or use case, so do not assume one token works everywhere.

What tokenization does and does not buy you#

The main benefit is reduced exposure. Fewer internal systems handle raw card data, which can reduce PCI DSS risk by minimizing where cardholder data is stored or transmitted. It does not make you automatically PCI compliant, and it does not remove all security and compliance responsibilities.

A common operational failure mode is partial coverage. If logs, analytics payloads, support screens, or failure paths still capture full card numbers, the design is only partly tokenized.

How tokenization works across a real transaction lifecycle#

The lifecycle only works if the same data boundary holds from checkout through reuse. Card details are captured at checkout or wallet entry, converted by a tokenization service, and later payment operations run on the tokenized reference instead of raw PAN data.

From checkout to first authorization#

The first decision is where raw card data enters your stack. At checkout or wallet entry, card details are sent to a tokenization service. The service stores the original card data in a secure PCI DSS-compliant vault and returns a payment token for future transactions.

From there, the live payment path should keep using that tokenized reference through authorization and downstream operations such as settlement and refunds. If any internal path still captures raw card numbers, the boundary is incomplete even if the main flow is tokenized. Before go-live, test the full tokenized flow, not just token creation.

Reuse for one-click and recurring payments#

This is where tokenization earns its keep. After first use, you can reuse the token for future charges without exposing card data again, which enables one-click payments and subscription billing flows.

In some network-token setups, tokens can be updated when cards expire or are reissued, which helps keep recurring payments active. At the same time, plan for token sprawl and portability limits across providers.

Keep records reconcilable across teams#

Reduced card exposure does not remove the need for clean internal records. Your teams still need to follow the same transaction across authorization, settlement, and refunds.

Before launch, validate the full tokenized flow in your own stack, including how shared references appear in support, finance, and engineering tools.

Tokenization and encryption solve different risks#

Use both controls for different jobs. Encryption protects sensitive data you still store or transmit, while tokenization can remove PAN from many application surfaces by replacing it with a payment token.

Encryption turns readable data into ciphertext and makes it readable again with the right decryption key. Tokenization swaps PAN for a token with no standalone value, while the PAN-to-token mapping stays in a token vault. In operator terms, encryption protects data where it exists. Tokenization changes where real card data exists.

| Approach | Data location | Reversibility | Key management burden | Blast radius if app data is exposed | Impact on PCI compliance |

|---|---|---|---|---|---|

| Encryption only | Encrypted PAN can still live in systems that process or store it | Reversible with the decryption key | Higher, because key handling is an ongoing operational responsibility | Can be wider because PAN is still present where encrypted data is retained | Protects data, but does not by itself remove PAN from your environment |

| Tokenization only | App stores payment tokens; PAN mapping stays in the token vault | Token is not PAN; access depends on vault mapping controls | Lower in the app boundary, but vault access control still matters | Can be smaller across app surfaces because exposed tokens have no standalone value | Commonly helps reduce PCI-related burden by minimizing sensitive-data handling |

| Tokenization plus encryption | PAN can stay in the vault; retained sensitive fields can be encrypted where needed | Token path is indirect; encrypted retained data is reversible with keys | Shared burden: vault controls plus encryption key management for retained fields | Better containment when app paths avoid PAN and retained sensitive data is encrypted | Strong combined control set, but not automatic PCI compliance |

A practical architecture is to tokenize card-entry paths and then encrypt any sensitive fields you still need. That can keep PAN out of much of your application boundary without pretending encryption is no longer necessary.

Use a concrete launch check. Confirm card entry happens inside a secure iframe or equivalent hosted capture boundary, and verify card data is encrypted in transit with TLS before it reaches the token vault. Then verify application-controlled systems are handling tokens rather than decryptable PAN. If an application-controlled system still stores decryptable PAN, the tokenization goal is not met.

Treat the tradeoffs as design inputs, not absolutes. Encryption can add key-management and speed overhead. Token-vault designs can introduce single-point-of-failure, latency, and provider lock-in risk in some implementations. The practical rule is still straightforward: keep PAN in the vault where possible, keep tokens inside the app boundary, and encrypt only the sensitive remnants you still need.

Related: What is an IBAN and How is it Different from a SWIFT Code?.

Choosing network tokens or processor tokens without regrets#

Treat this as an operating-model decision, not just a security choice. If you may change processors, add routing logic, or expand coverage, decide early how you will avoid lock-in and what credential-migration options exist if needed.

Gateway choices shape retries, declines, outages, regional coverage, PCI scope, and checkout performance. Token strategy sits inside broader business risk. The important caution is simple: integration decisions can be hard to unwind, and processor outcomes can vary enough that one may approve what another rejects.

The practical judgment#

Do not assume one token path is always better. Choose the option that fits your routing and processor strategy, then verify migration terms before volume builds.

A constrained payment environment is a security benefit when a token is compromised. That same boundary can become an operational problem when portability and migration support are unclear. Before committing, confirm and document:

- which token types are returned for your card-on-file flows

- whether stored credentials can be migrated, under what conditions, and on whose timeline

- whether your contract explicitly covers export and assisted migration support

- whether your internal payment-method model can handle token-reference changes over time

Decision table#

| Decision area | What is grounded | What you should verify before choosing |

|---|---|---|

| Portability risk | Integration choices can create lock-in that is hard to unwind. | How each option handles credential migration and whether token reuse is possible across processor changes. |

| Routing flexibility | Processor behavior can differ for the same payment. | Whether your token approach supports planned routing, retries, and fallback patterns. |

| Outage resilience | Outages are a practical gateway checkpoint. | What happens to stored-payment flows during provider incidents and recovery. |

| Contract dependency | Gateway setup is also a business decision, not only technical. | Exact contract language for migration rights, assistance, timelines, and limits. |

| PCI and checkout impact | PCI scope and checkout performance are explicit evaluation checkpoints. | The real scope and performance impact in your own implementation. |

| Claimed performance uplift | One source reports 4 billion network tokens tied to a 28% fraud drop and 3% approval lift. | Whether those reported outcomes apply to your stack, geographies, and routing setup. |

If orchestration is already on your roadmap, make portability requirements explicit now and avoid hard-coding one provider path as your only long-term option. For a deeper routing lens, see Payments Orchestration: What It Is and Why Every Platform Needs a Multi-Gateway Strategy. For ACH-specific tradeoffs, see What Is ACH? The Automated Clearing House Explained for Platform Operators.

Designing for marketplace and embedded payments realities#

In marketplace and embedded setups, tokenization protects card credentials, but it does not define the rest of the operating model. You still need clear boundaries for who a token belongs to and which payment context can use it.

Map token boundaries by actor#

A token is only useful if its ownership and context are clear in your own data model. In a tokenized setup, your system stores the token while the original card data stays in the token vault, and the processor maps the token back to the underlying data during processing. In practice, every token reference should carry clear actor context. At minimum, store enough context to distinguish:

| Context field | What it captures | Grounded example |

|---|---|---|

| Payment method entry | Who entered the payment method | Store who entered the payment method. |

| Seller or sub-merchant context | Which payment context it belongs to | Store which seller or sub-merchant context the payment belongs to. |

| Processor account or merchant configuration | Which setup created the token | Store which processor account or merchant configuration created the token. |

| Token type | Which token model you have | Network token or vault/PSP token. |

Vault/PSP tokens can reduce merchant PCI DSS scope, but they may have weaker lifecycle intelligence and portability than network tokens. A network-level token is restricted to a specific device, merchant, or domain, so do not assume cross-context reuse without validating that path in your own setup.

Card rails and bank-transfer rails need separate handling#

A unified product surface can make very different payment rails look similar. Embedded payments keep payment actions inside the platform workflow, and APIs or SDKs can connect that same surface to card networks, banks, and wallets. The user experience may look unified, but the backend objects and controls are not.

For card flows, tokenization replaces the PAN with a token, supports recurring reuse, and may include automatic network-token updates when cards expire or are reissued. For bank-transfer flows, treat those references and traces as bank-rail objects, not as card-token lifecycle events.

| Rail | Primary object | Practical implication |

|---|---|---|

| Card flows | Payment token | Design around token context, recurring reuse, and token lifecycle behavior. |

| Bank-transfer flows | Bank transfer/reference records | Define separate records and lifecycle handling for bank rails instead of reusing card-token logic. |

Keep payout-state logic explicit#

Do not let collection success stand in for payout readiness. Exact payout gating rules are not defined here, so model and expose payout status explicitly in your own system.

Define the mixed-flow order before launch#

Before launch, document one clear payment-flow sequence and exception path. The exact collect-to-payout rules are product-specific and not defined here, so make that sequence explicit instead of leaving it implicit across teams.

For a step-by-step walkthrough, see What Is an e-Payable? How Virtual Cards and Digital Payments Replace Paper Checks in B2B.

Go-live checklist that product, engineering, and finance can sign off#

Do not launch on tokenization alone. Launch when engineering, security, finance ops, compliance, and vendor-readiness checks are all signed off. Use the checklist below as the sign-off frame.

| Area | Verify before launch | Evidence to keep | Red flag |

|---|---|---|---|

| Engineering | Idempotency on create, charge, and refund paths. Webhook handlers stay safe under duplicate, late, or out-of-order events. Token lifecycle states are explicit in the model. | Replay test results, webhook replay logs, token lifecycle/state diagram. | Retries create duplicate charges, refunds, or state transitions. |

| Security | PAN-adjacent fields are masked in logs, exports, and admin views. Residual sensitive data is encrypted. Token access is restricted to required services/roles, with audit logging. | Masking examples, access-control settings, audit-log samples. | Raw card-adjacent details still leak through support or debug paths. |

| Finance ops | Processor events reconcile to ledger journals with shared references. Exception queues are documented and owned. Subscription billing close is tested for reuse, failures, retries, refunds, and card-update behavior. | Reconciliation sample, exception runbook, close dry-run output. | Processor outcomes exist, but journal posting depends on manual repair. |

| Compliance | Map the deployed architecture to actual PCI DSS scope. Vault/PSP tokens can reduce PCI DSS scope, but they do not remove all obligations. Record market/program caveats where requirements differ. | Current architecture and data-flow diagrams, written scope decision. | "Tokenized" is treated as full compliance without scope validation. |

| Vendor | Confirm token export or migration rights in writing before scale. Confirm whether terms differ for network tokens versus vault/PSP tokens. | Contract terms, product docs, written provider confirmation. | Portability is assumed, but migration rights are undefined. |

Run failure-path tests, not just success paths. Replay requests with the same idempotency key, replay webhooks, and confirm customer, payment, and ledger states remain consistent.

For subscription flows, verify lifecycle behavior in your actual provider integration. Network tokens are described as adding domain controls and automatic lifecycle updates, but feature support can vary across processors and programs.

Be explicit about jurisdiction. In one India example, card-on-file tokenisation was required as an alternative to card storage, and the deadline was extended to September 30, 2022. Treat that as market-specific, not a global default.

Keep one go-live sign-off pack: replay proof, webhook duplicate-handling proof, reconciliation sample, current scope diagram, and written migration terms. If one is missing, you still have launch risk.

Before rollout, map your token lifecycle, webhook retries, and reconciliation checkpoints against your implementation plan in the Gruv docs.

Failure modes that break trust and how to contain them#

The risk is not just technical failure. When tokenization fails, the current payment can fail, and ad hoc handling of sensitive payment data can increase risk.

The first place to watch is the tokenization request, where you send payment data to a processor or third-party vendor. If this step fails, treat it as both a transaction risk and a trust risk, not just a temporary error.

Keep the storage boundary clear in your system: your business stores the token, while the original PAN stays in the tokenization service vault. That lowers exposure to card data, but you still need clean internal handling of token records so failures do not spill into customer-facing issues.

Recurring payments raise the stakes because the same token can be reused over time. That means a token-handling error can carry into later transactions. There is no mandated incident-response checklist specified here, so treat the sequence below as an internal operating pattern:

- Detect the failure signal quickly, for example a tokenization failure at the request step.

- Contain or pause the affected flow before retries or manual workarounds expand impact.

- Communicate clearly to customers about what failed and what happens next.

- Reconcile payment outcomes with internal records before closing the issue.

- Harden the control that failed so the same pattern is less likely to repeat.

What tokenization does not solve for compliance#

Tokenization reduces exposure to card data, but it does not make compliance work disappear. In normal handling, it replaces a visible Primary Account Number (PAN) with a payment token, while compliance still needs separate review beyond token basics.

That distinction matters in practice. Tokenization and compliance are related, but they are not the same question.

The boundary that helps, and the controls that still matter#

The architecture helps only if you can prove the boundary in practice. First checkpoint: confirm your application database, logs, support tooling, and finance exports contain tokens or masked values, not raw PAN.

If you cannot prove that boundary, your compliance position is weaker than your architecture suggests. A potential failure mode is a tokenized flow that still exposes card details through error logs, screenshots, support notes, or one-off exports.

Tokenization alone does not answer access-control, logging, or incident-response questions. If a payment token is exposed, that is not the same as a leaked PAN, and the token alone cannot be used for fraudulent purchases. You still need to investigate access, linked records, whether real card data was exposed, and whether the same gap exists elsewhere.

Residual responsibilities across engineering and finance#

This is not only an engineering concern. Finance, support, and operations may also handle exports, reconciliations, chargeback packs, refund research, and customer communications, and those steps can expand where token-linked records live. For compliance reviews, keep three questions explicit:

- Where can sensitive payment-related records appear, even when PAN is tokenized?

- Who can access those records across engineering, finance, and support?

- How do you detect, review, and respond when handling goes off script?

Data retention is part of the same control surface. Tokenization by itself does not define what records, tickets, logs, or archives you keep. You still need documented rules for retention, storage, approvals, and review or removal of stale data.

Why blanket compliance claims are risky#

Blanket claims create avoidable risk. Tokenization lowers PAN exposure, but obligations can still vary by integration pattern, market, and program. That is why "we use tokenization, so we are compliant" is an overreach.

A safer statement is simpler: "We use tokenization to reduce PAN exposure." Then document what remains in scope for access, logging, retention, and incident processes. Compliance answers should map to your actual integration, not a generic vendor promise.

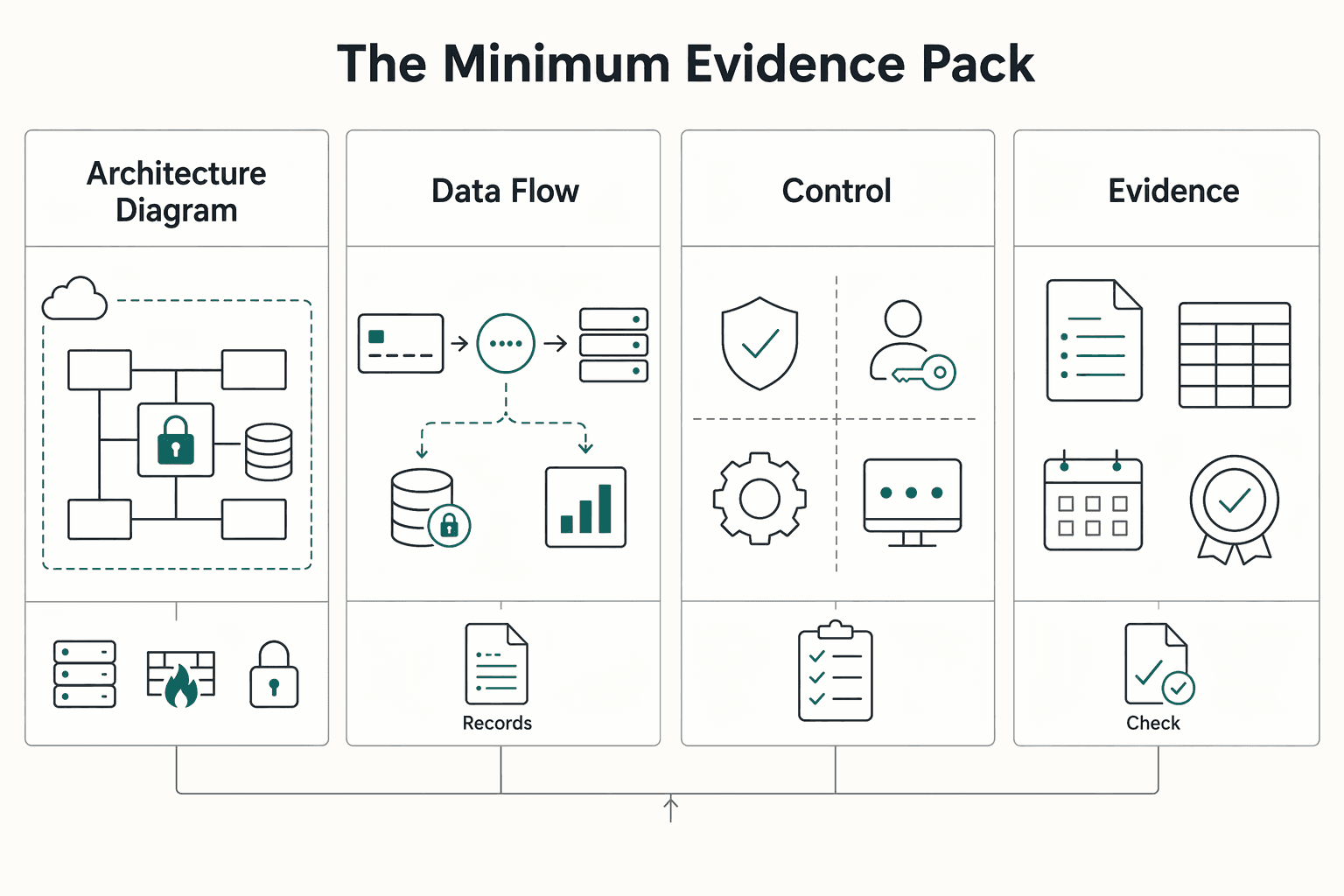

The minimum evidence pack#

Keep a compact evidence pack that proves the boundary in practice:

| Artifact | What it should show | Article examples |

|---|---|---|

| Architecture diagram | Where PAN can appear, where only tokens are stored, and which services or teams can access each layer | Access by services or teams. |

| Data-flow map | Card capture through token creation, authorization, storage, retries, refunds, and reporting | Include logs and exports. |

| Control ownership list | Owners for access reviews, log reviews, retention decisions, incident handling, and change approval | Named control owners. |

| Periodic verification records | Checks that prove the boundary in practice | Log spot checks, sample export reviews, and access review sign-offs. |

If you keep only one artifact, keep the data-flow map. It is often the fastest way to find where tokenization reduced exposure in the main path but side channels still create compliance work.

Planning migration early so tokenization does not lock you in#

Plan migration before launch, because tokenization can still create lock-in when token portability and detokenization paths are unclear. Use your data-flow map to answer migration-critical questions early: where PAN can exist, where only tokens exist, and which tokens are tied to which provider or context.

A payment token can be unusable outside its payment system. Some network-level tokens are limited to a specific merchant, device, or domain. Portability limits need to be explicit before you scale card-on-file. Before signing or going live, get written answers from each processor on:

- Whether stored tokens can be exported, and in what format.

- Whether detokenization is allowed, and under which conditions.

- What migration support is available during a provider switch or portfolio move.

- Which token type your records will rely on: network-level, merchant-level, or both.

Inside your product, keep the business concept of a saved payment method separate from processor token IDs where possible. Use your own payment method ID as the stable reference, and treat provider token fields as replaceable mappings. If you make a processor token the canonical ID, retries, subscriptions, support workflows, and finance outputs can be harder to move cleanly.

If payment orchestration is on your roadmap, define routing and outage failover rules now. An orchestration engine can serve as a single connection point and improve flexibility across providers, especially when your token model and failover behavior are designed together.

Before full cutover, run a limited card-on-file migration dry run. Validate token mapping, retry behavior, and reconciliation outputs, compare old versus new provider results, and document rollback steps plus findings.

Conclusion#

Tokenization is a core control for modern card acceptance, but the result depends on architecture choices and operating discipline, not the token alone.

In a sound setup, your business stores the token while the tokenization service stores the original card data in its vault. The token can be reused for recurring payments, and if intercepted during payment it is described as useless to fraudsters. Treat that boundary as something to verify in your real implementation, not something to assume.

Tokenization and encryption are different controls, not substitutes, so keep both in scope when you design how payment data moves through your systems. The practical path is four decisions in order:

- Define your token model and storage boundary. Be explicit about where PAN appears, where it is replaced, and which system owns vault storage.

- Choose token type with clear tradeoffs. Network tokenization is managed by card schemes such as Visa and Mastercard; provider-issued models are another option to evaluate.

- Build for day-two operations before scaling. Confirm how your team will handle payment-state edge cases and recurring flows without creating operational confusion.

- Validate finance and compliance evidence early. Make sure ownership, controls, and traceability are documented before volume grows.

Run one cross-functional review with product, engineering, and finance ops before committing your production path, then confirm provider-specific coverage and constraints in writing. If your team is weighing portability, compliance gates, and payout operations across markets, talk through your target architecture with Gruv.

Frequently Asked Questions

What is payment tokenization in one sentence?

Payment tokenization replaces sensitive payment data, such as a card’s Primary Account Number (PAN), with a unique token so real card details are not used directly. In card-on-file flows, you store and reuse the token for future transactions instead of the raw card number.

Is tokenization the same as encryption?

No. They are different controls, and tokenization does not mean encryption is no longer needed. A payment token does not contain the real payment details.

Who stores the real card number after tokenization?

In gateway-vault setups, the provider stores credentials in its vault while your system stores tokens. But this is not universal: some gateway models allow a merchant to store either PAN or a network token. Confirm your actual storage boundary in your architecture and provider documentation.

Does tokenization mean we are automatically PCI compliant?

No. PCI DSS still applies wherever your organization transmits or stores cardholder data. Tokenization can reduce exposure, but it does not remove PCI responsibilities on its own.

Should we choose a network token or a processor token first?

Start with your operating model and integration constraints, not just speed to launch. Direct network-token integrations can require scheme-by-scheme API work and ongoing maintenance. If your provider offers a single API abstraction, verify exactly what it covers for your use case.

Can we move tokens if we switch payment providers?

Sometimes, but never assume portability. Whether tokens can be moved depends on your provider and tokenization setup. Get provider-specific confirmation before committing.

Is tokenization enough for marketplaces that also run payouts and compliance checks?

No. Tokenization addresses payment-data handling, not the full payout and compliance stack. You still need separate controls for payout operations and checks such as KYC, KYB, and AML.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- middlebury.edu/sites/default/files/2025-01/PCI-DSS-v4_0_1.pdftrusted

- sec.gov/files/ctf-written-sec-submission-fcck-compan...trusted

- sec.gov/files/ctf-written-input-daniel-bruno-corvelo...trusted

- stripe.com/resources/more/payment-tokenization-101trusted

- stripe.com/resources/more/payment-tokenizationtrusted

- airwallex.com/us/blog/how-tokenization-worksexternal

- bluefin.com/bluefin-news/tokenization-vs-encryption-choo...external

- corefy.com/blog/payment-tokenization-explainedexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: