Quick Answer

Route each case by transaction stage: attempt authorization reversal while funds are still authorized, issue a refund after settlement, and move bank-initiated claims into chargeback handling. Then lock ownership across legal, ops, and engineering, capture the exact Terms and Conditions and Refund policy shown at purchase, and require evidence fields such as order ID, payment reference, and timeline stamps. Close only after the incident outcome matches ledger entries and payout effects.

What a Dispute-Ready Refund and Reversal Policy Needs#

By the end of this guide, you should have a refund and reversal policy that legal, ops, and engineering can execute without guesswork. For a marketplace platform, that means more than clean policy text. Support needs clear decisions, engineering needs enforceable transaction states, and finance needs records that still reconcile when a refund, payment reversal, or chargeback arrives out of order.

The hard part is not wording. It is managing tradeoffs. Faster customer resolution can reduce friction now, but rushed decisions create downstream risk when payment status, counterparty responsibility, or ledger impact is unclear. Over-correct for risk, and you may cut immediate exposure while increasing customer frustration and dispute pressure. A workable policy has to balance all three at once: fast customer action, clear chargeback handling, and clean reconciliation.

This guide stays practical by covering both policy design and implementation checkpoints. You are not just deciding what support can say. You are deciding which outcomes exist, who can approve them, what evidence is required, and how the product records each step so the case is still understandable later.

Set the boundaries before you draft.

Set the research boundary first. Otherwise, you will end up debating policy from sources that help with drafting but are not reliable enough for final decisions. This guide covers policy design, ownership, evidence requirements, and product checks that make policy executable. It does not replace legal review. Questions tied to State law (U.S.), card network rules, processor-specific behavior, or partner contracts still require counsel and partner confirmation.

Start with source discipline. If your team researches a federal rule on FederalRegister.gov, treat that page as informational. It states that it is not an official legal edition of the Federal Register and does not provide legal notice to the public or judicial notice to the courts. When you need the official text, use the linked PDF on govinfo.gov and have counsel confirm what applies.

Apply the same caution to the eCFR. 12 CFR Part 1005 is Electronic Fund Transfers (Regulation E), and the eCFR labels its content authoritative but unofficial. The displayed Title 12 text is up to date as of 4/02/2026 and last amended 4/01/2026, which is useful for working analysis. For marketplace cases, though, you still need transaction-type legal analysis before assuming Regulation E governs your specific refund or reversal path.

Use one operating rule throughout: do not approve policy language unless it also names an owner and a recordkeeping expectation. That control exists for a reason. In the IRS refund-offset procedure context, ownership and records are explicitly separated as Roles and Responsibilities and Disclosure and Retention Records. If your draft cannot clearly answer who decides, who documents, and what is retained, it is not launch-ready.

From there, the rest of the guide turns that rule into execution steps: prerequisites, outcome definitions, legal and operational ownership, product-state controls, evidence packs, and reconciliation checks. Every team should reach the same decision from the same facts. The policy should still hold up when a customer, counterparty, bank, or auditor asks what happened.

Gather prerequisites before you draft policy text#

Do not start with clause wording. Start with the documents, owners, and evidence that will make the policy real. Without that baseline, you risk promises support cannot deliver, engineering cannot enforce, or legal cannot approve.

Collect the live governing documents.

Build a versioned inventory of your current Terms and Conditions, Return policy, Refund policy, and the customer-facing copy that creates Sales promises, including checkout, receipts, help-center content, and support macros. Treat this as an operating artifact, not a one-time read.

For each item, capture:

- URL or file location

- owner

- version marker (

last updatedoreffectivedate)

This catches a common failure mode early: obligations can be spread across multiple agreement layers. Map which agreement governs each product flow.

Assign approval owners before editing language.

Set approval boundaries before you edit. At minimum, assign clear legal, ops, and engineering ownership for the policy areas each team must approve.

Map partner constraints at the same time. Your provider may act as a payment facilitator, not a bank, and rely on networks, processors, and acquiring banks, so some outcomes are partner-dependent. If any sentence assumes fixed processor or card behavior, especially card acceptance behavior that can change without prior notice, flag it for review instead of publishing it as a hard promise.

Pull the minimum evidence baseline.

Before you draft policy, pull the minimum records you would need to prove and execute it. Start with payment event logs, customer communication logs, and your current handling rules for Refund method and Time limits.

Run one quick trace test on a recent refund case:

- payment event trail

- customer communication trail

- policy text shown at purchase

If legal research used FederalRegister.gov, verify it against the official legal edition before treating the language as final authority.

Define transaction outcomes before you argue policy#

If refund becomes a catch-all term, teams will choose the wrong path under pressure. Define the outcomes first, then write the customer-facing language around those choices.

Use one decision table with one meaning per label.

Authorization reversals, refunds, and chargebacks are all payment reversals, but they are not interchangeable. Each path has different rules, restrictions, costs, control points, and customer impact.

| Outcome | Who initiates | When it can happen | Expected customer impact | Control and constraints |

|---|---|---|---|---|

| Authorization reversal | Merchant or payment partners, depending on setup | Before the payment is treated as fully settled | Funds are reversed without using the chargeback dispute path | Availability depends on partner and bank or processor handling |

| Refund | Business initiates | After a completed payment when money is being returned | Funds are returned by the business | Your team initiates the return, with downstream handling outside your full control |

| Reversal transaction | Internal umbrella label for a transaction reversal | Use only as temporary classification | Customer impact depends on the actual path used | Must be resolved to a specific path before closure |

| Chargeback | Customer dispute through bank/card rails | After a dispute is initiated through the bank path | Funds are pulled back from the business and returned to the cardholder | Bank and card-network dispute processes govern what happens next |

| Uncertainty row | No single initiator | When partner behavior is not fixed in docs/contracts | Customer timeline is not fully predictable | Resolve to authorization reversal, refund, or chargeback before closure |

Use Card Payment Transaction and Settlement Flow as a checkpoint. Identify whether the payment is authorized, settled, or already in dispute before selecting a path.

Add routing rules based on payment state.

Route by payment state, not by habit. If the payment is still in the authorization stage, attempt an authorization reversal where available. If it has settled, process a refund. If a bank-side dispute has already started, treat it as a chargeback dispute. Early action can reduce merchant cost and lower the chance of a more damaging reversal later.

Keep one limit explicit in policy language: do not promise authorization reversal availability in every case. Partner setup and bank or processor handling can limit what is possible.

Map counterparties so promises match control.

The next step is making sure your promise matches who actually controls the outcome. Map each path to the counterparty that controls what happens next. For authorization reversals and refunds, your team can initiate the action, but external payment partners still affect final outcomes. For chargebacks, control shifts to bank and card-network dispute processes.

Add one plain uncertainty statement in both internal and customer-facing policy copy. Commit to what you control, such as submitting a refund or attempting an authorization reversal when available. Avoid fixed promises on timing, fees, or identical partner behavior.

Related: Late Fee Automation for Marketplace Invoices: Legal Requirements by Country.

Assign legal and operational ownership across parties#

Most case types should have two clear owners: one for funds and one for customer communication. If those owners are not documented for both the marketplace platform and the other side of the transaction, escalations and recovery decisions can drift.

Build one contract-backed responsibility map for each dispute type.

Because risk and policy application are context-specific, treat this map as jurisdiction- and partner-specific rather than one-size-fits-all.

For each path, define who is expected to fund the refund, who communicates with the customer, who handles escalation, and who absorbs downstream balance adjustments or clawbacks, if your model allows them. If ownership changes mid-flow, state exactly when control shifts.

| Case type | Funding owner field | Customer and escalation owner field | Contract checkpoint |

|---|---|---|---|

| Authorization-stage cancellation or reversal attempt | Name the party that covers the return if reversal is unavailable | Name the party that sends the first response and handles follow-up | Seller agreement plus Terms and Conditions language on payment state and timing |

| Post-settlement refund request | Name the party that funds the refund and any offset rule | Name the party that approves exceptions and handles complaints | Refund policy, seller agreement, and payout adjustment clause |

| Chargeback or issuer dispute | Name who bears economic loss pending outcome | Name who submits evidence and who approves settlement decisions | Seller agreement dispute clause and internal escalation policy |

| Misrepresentation, warranty, or listing complaint | Name who funds relief if fault is found or unclear | Name who can suspend listings, approve refunds, or route to legal | Terms and Conditions, listing rules, and seller representations |

Verification rule: every dispute code in support or risk tooling must map to a clause reference, not just an internal owner name.

Tie ownership to the accepted documents.

Tie those ownership fields to the documents customers and counterparties actually accepted: Terms and Conditions, seller agreement, return policy, and refund policy. Be explicit on the clauses teams argue over under pressure, especially Time limits, Refund method, and non-refundable cases.

Also state what payment failure does not do automatically. In the NameSilo example, service commitments do not automatically unwind when a payment fails or is disputed. Your agreement should clearly define what happens to access, delivery, or obligations during a payment issue.

Define ineligible statuses precisely. The same example uses a fraud hold as ineligible for refunds. If you use a similar carveout, put it in customer-facing terms and the corresponding counterparty terms instead of leaving it as an internal label.

Route true edge cases to legal review.

Do not force edge cases through automated ops logic. Route ambiguous U.S. cases to legal review when clause language is unclear, customer promises conflict with checkout or listing copy, or complaints involve warranties, misleading listings, or potentially deceptive practices.

For legal-review packets, include accepted policy and seller-agreement versions, purchase-time checkout or listing copy, payment status, communication history, and the proposed outcome. If federal materials are cited, record source status. FederalRegister.gov says results should be verified against an official Federal Register edition, and its XML text does not provide legal notice. The CFPB item dated 01/14/2025 is shown as a Proposed Rule, with a newer linked withdrawal action dated 05/15/2025 (Docket No. CFPB-2025-0002).

Write policy clauses that reduce ambiguity in disputes#

A good policy is one that produces the same decision across support, finance, and legal for the same fact pattern. Keep clauses plain, specific, and narrow enough that teams do not fill gaps from memory.

Start with the smallest clause set that closes the biggest gaps.

Start with the minimum clause set that removes interpretation gaps:

- Eligibility: which order, service, or item states qualify for a Refund, and which do not.

- Condition standards: what labels like "unused," "not as described," or "damaged" mean in your operation.

- Time limits: when the clock starts, how requests are submitted, and whether windows differ by case type.

- Refund method: whether funds return to the original payment method or another approved path, and who approves exceptions.

- Restocking fees: when they apply, who absorbs them, and when they do not apply.

Avoid open-ended language like "at our discretion" without criteria. If discretion is required, tie it to named exception owners and internal Dispute escalation steps.

Keep policy text consistent across every surface.

Consistency across surfaces matters as much as clause quality. Policy text should match across checkout, receipt email, help center, support macros, and Terms and Conditions. If eligibility, Time limits, Refund method, or Restocking fees differ between surfaces, fix the source text before allowing one-off support replies.

Separate complaint types clearly.

Separate complaint types instead of burying them in general language. You can include a distinct section for non-delivery, misrepresentation, and material-mismatch complaints. State that these cases are reviewed through internal Dispute escalation and, where needed, against applicable Consumer protection laws.

For legal references in policy notes, keep the official PDF on govinfo.gov, not only FederalRegister.gov XML. The Federal Register page for document 2024-07177 (04/26/2024) says legal research should be verified against an official edition. It also says XML does not provide legal or judicial notice. Use eCFR for current drafting context, but treat it as authoritative and unofficial. If a source is labeled Proposed Rule, treat it as monitoring input, not final policy authority.

Keep a policy review log with document number, publication date, and govinfo PDF link. This avoids dependence on live pages, including cases where retrieval fails, such as a 500 Server Error.

State clearly what you cannot promise.

Add one short "what we cannot promise" block. State clearly that you cannot promise exact bank posting speed, exact Card network timing outside your control, or fixed cross-border settlement timing where intermediary processing varies.

Then align receipts and support macros so teams do not promise issuer-controlled or intermediary-controlled timelines.

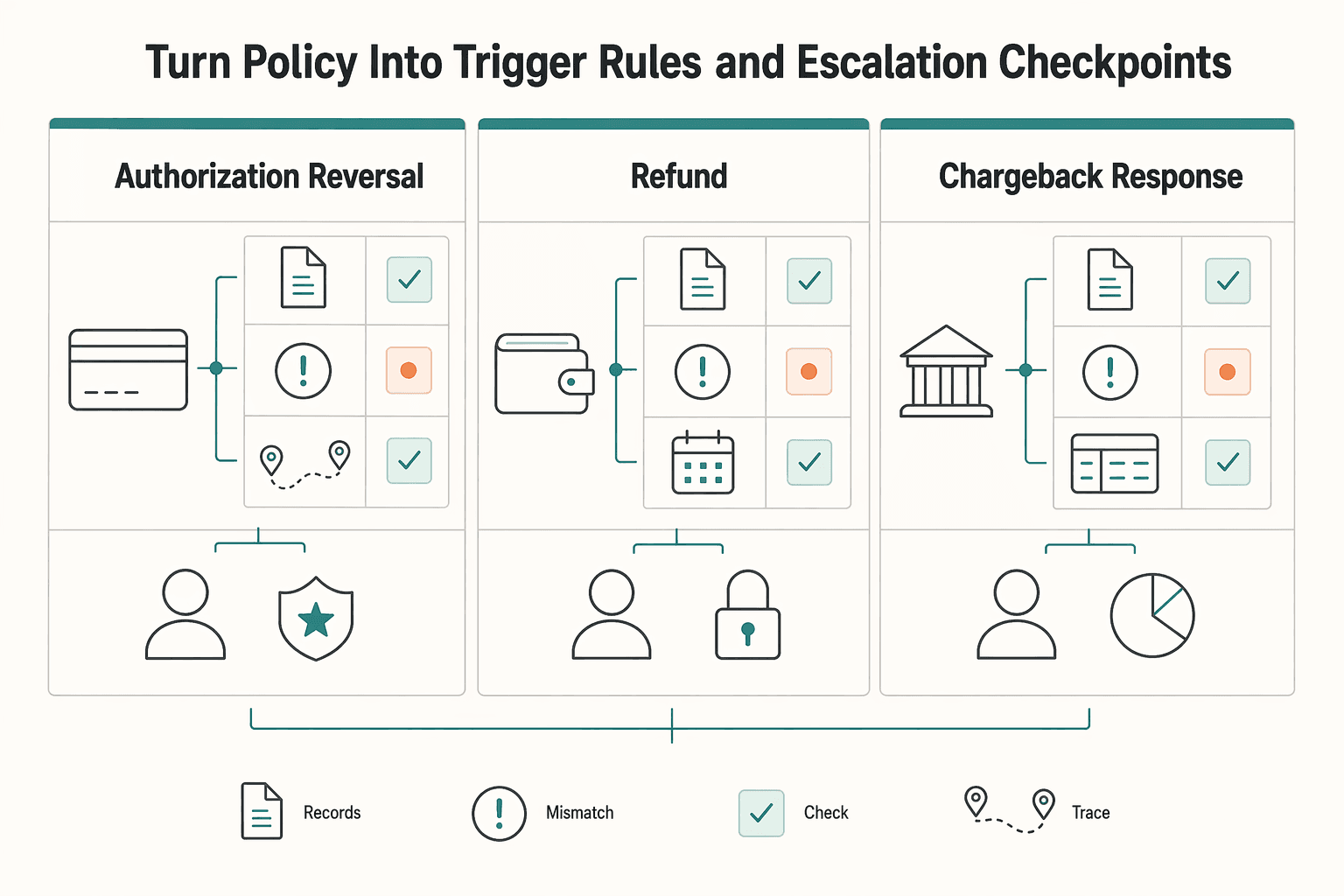

Turn policy into trigger rules and escalation checkpoints#

Policy only works when the same facts lead to the same action. Turn each clause into trigger rules, minimum evidence, and escalation checkpoints before a complaint drifts into a chargeback.

Build one incident tree from intake to a named owner.

Keep it high level. Define what must happen, not every tool click.

At intake, require the same minimum case fields every time:

- order or booking ID

- payment reference or provider transaction ID

- complaint type in the customer's words

- event dates tied to your policy

Time limits - current transaction status from payment records

- counterparty response, if that party is first-line

- policy version shown at purchase, receipt, or checkout

If any field is missing, pause before money movement. This helps prevent weak-record approvals that can fail dispute review.

| Path | Use when your records show | Minimum verification | Primary owner |

|---|---|---|---|

| Authorization reversal | Payment is still authorized and case is approved for return of funds | provider status, order ID, approval reason, timestamp | payments or ops |

| Refund | Payment has settled and policy or review supports returning funds | settlement confirmed, policy clause matched, amount approved, funding owner confirmed | ops or finance |

| Chargeback response | Bank or network dispute is already in motion, or recovery is in dispute channel | dispute notice, payment reference, policy snapshot, customer thread, counterparty evidence | disputes or finance, with legal as needed |

If marketplace and counterparty responsibilities differ by contract, still assign one action owner and one approval owner.

Write rules ops can actually run.

If proof is incomplete, request documents before action. If breach is clear in your records, process the refund before the case escalates. If payment is pre-settlement in provider records, route to the approved reversal path. If counterparty claims conflict with platform logs, escalate to second review instead of debating in email.

An early path is usually less expensive than a reactive one, but speed without evidence raises downstream cost. Use one approval checkpoint: can a second operator understand, from the case file alone, why this path was chosen?

Set escalation points by severity and risk tier.

Set internal SLA checkpoints by severity and risk tier, with explicit escalation points. Low risk means a routine policy match with complete evidence. Medium risk means missing records, disagreement with the other side, or larger amounts. High risk means repeated complaints on the same listing or account, misrepresentation allegations, or a possible conflict between policy language and applicable law.

Escalate to legal when either condition is met:

- an ambiguous clause may conflict with applicable law

- repeated complaints suggest a pattern that may raise consumer-protection risk

Weak routing creates predictable failure modes: long delays, inconsistent treatment, and frustration caused by poor transparency. In one public claims environment, unresolved volume reached nearly 1.2 million cases as of October 26, 2024, and average processing time was more than a year. Build checkpoints early so backlog does not become normal.

Standardize stage communications.

Standardize stage communications so the customer and the other side get the same policy-grounded explanation.

Use templates for: received, evidence requested, under review, approved, denied, escalated. Each template should state the case reason, policy clause applied, what is still needed, and the next step.

Require templates to include the exact clause title used in the decision. Store outbound message IDs in the case record so reviewers can confirm both parties received consistent reasoning. This keeps ops, finance, and legal aligned before the dispute stage.

For a step-by-step walkthrough, see How to Write a Payments and Compliance Policy for Your Gig Platform.

Implement transaction states and idempotent controls in the product#

Your product should enforce one consistent money outcome, even when processing is asynchronous.

Convert policy outcomes into explicit internal states.

Convert policy outcomes into explicit internal states and guard every transition. The provided API excerpts do not define a universal internal state model, so labels such as requested, under_review, approved, refunded, disputed, and closed should be treated as internal implementation choices.

Before any money-moving transition, require core internal fields and confirm at least paymentId plus current provider status. If those are missing, keep the case in review.

Treat payment completion as a hard state boundary.

In documented two-step flows, payment creation and completion are separate, and completion is POST /v1/{merchantId}/payments/{paymentId}/complete.

Do not treat redirect return as final authorization. In 2-step 3D Secure card flows, status can remain PENDING_COMPLETION, and authorization occurs when complete payment is called. Apply the same checkpoint logic to redirect-based completion flows: store paymentId, confirm provider status, then transition internal state.

Make money-moving actions idempotent.

The provided API excerpts do not define idempotency keys or duplicate-prevention behavior for replayed money-moving actions. If replay safety is required, enforce it in your application layer with a stable internal operation ID and deterministic replay handling.

Your validation check is simple: replay the same approved action multiple times and confirm one business outcome, one customer-visible status, and one coherent history with retries recorded.

Reconcile provider events to one internal money record.

The provided excerpts do not prescribe a required internal ledger or wallet architecture. Use provider events as inputs, then reconcile to one internal money record before final internal state changes. If external references are missing or updates are delayed, keep the case recoverable and avoid premature closure.

For resilience, correlate inbound updates to the same paymentId or internal operation ID, and move to closed only when external status and the internal record align. For deeper finance controls, see Refund Reconciliation for Platforms: Matching Returns Reversals and Ledger Entries.

Build an evidence pack that can survive audits and disputes#

Do not close cases just because the queue is empty. Close them when the file can stand on its own. For every refund, reversal, or dispute, the file should answer three questions quickly: what was purchased, what was promised at purchase, and what money event occurred.

Make the minimum case file a closure gate.

Set a minimum case file and make it a closure gate. A practical internal baseline can include the order or booking record, internal case ID, customer communication thread, and a timestamped timeline for request, review, approval, money movement, provider update, and closure.

Map those timestamps to your internal Time limits so reviewers can verify sequence and handling at a glance. If a closed case cannot be reconstructed without Slack threads, inbox searches, or side notes, treat it as incomplete.

Store the exact policy version shown at purchase.

Store the exact policy version shown at purchase, not just today's live page. Preserve the rendered Return policy, Refund policy, Terms and Conditions, and any checkout or receipt copy that carried Sales promises.

When policy language references government notices, keep source quality explicit. FederalRegister.gov states that its XML pages are not the official legal edition and that legal research should be verified against an official edition. Each entry links to the official PDF on govinfo.gov. Keep that official PDF link plus formal identifiers, for example agency or docket, document number, publication date, and citation such as 91 FR 17384 on 04/06/2026, in the case file.

Attach payment evidence by actor.

Attach payment evidence by actor so the money trail is traceable across systems. Keep internal paymentId and any available processor references for each money-moving event, and capture partner-provided dispute details when available.

Treat missing references as an open control issue, not a closed case. If the provider reference or status is missing, keep the case in review until the internal outcome and provider record align.

Apply PII controls as part of evidence quality.

Apply PII controls as part of evidence quality, not as an afterthought. Define masking, access, and retention rules with legal and finance teams, and apply them consistently.

Use a final completeness check before escalation: complete timeline, policy snapshot, payment references, and controlled access. A file that is complete but overexposed, or locked down but missing core evidence, is not escalation-ready.

You might also find this useful: How to Build a Trust and Safety Program for Your Contractor Marketplace.

Reconcile each incident to ledger and payouts before closure#

Do not treat customer communication as the end of the case. Close an incident only when the money movement, ledger entries, and payout impact align.

After the evidence pack is complete, make financial consistency the closure gate. Every Refund or Reversal transaction should map to its ledger entries, and the downstream effect on derived balances and payouts should be verified before resolution.

Reconcile each incident to the full money trail.

Tie the case ID to the payment event, internal ledger entry or entries, and provider reference for the refund or reversal. If you track Authorization reversal, post-settlement Refund, and Chargeback as different outcomes, reconcile them separately.

Use one test before closure: the incident should explain every related debit and credit, with no unexplained ledger rows. If support shows closed but the ledger still has pending or duplicate movement from retries or async callbacks, keep the incident open.

Verify derived balances and payout effects.

Verify derived balances and payout effects, not just core ledger postings. If your product exposes wallet balances or account earnings, confirm those views reflect the reconciled ledger result and that payout status is still correct. A ledger-posted refund that does not flow through to payout handling is not complete.

Document your settlement mapping and checkpoints so they are visible and reviewable, consistent with the control discipline reflected in the OCC [Card Payment Transaction and Settlement Flow](https://www.occ.gov/publications-and-resources/publications/comptrollers-handbook/files/payment-sys-funds-transfer-activities/pub-ch-payment-systems.pdf) area (version 1.0, October 2021).

Set shared close criteria across teams.

Set shared close criteria across finance, ops, and engineering, and enforce them consistently:

- No orphan ledger entries left without an owner and next action

- No unresolved variance between internal and provider records without a documented disposition

- Clear owner for any reserve adjustment or clawback, where applicable

If your platform funds the customer first and expects recovery from the other side later, assign that recovery owner before closure. Keep control intensity risk-based: stricter on higher-risk flows, lighter on lower-risk flows. Use internal risk appetite for variance and aging thresholds, since no universal numeric limit is specified here. For deeper implementation details, see Refund Reconciliation for Platforms: Matching Returns Reversals and Ledger Entries.

Run a monthly control report for finance ops.

Run a monthly control report for finance ops to detect patterns early. A practical report can include:

- Volume by outcome (

Authorization reversal,Refund,Chargeback) - Unresolved exception count

- Aging of open reconciliation items

Use the report to separate isolated errors from recurring control failures, then route recurring issues for remediation. This aligns with the broader control structure that emphasizes internal controls, risk assessment, and Management and Board Reports, with risk tracking across operational, fraud, credit, liquidity, and compliance categories.

Need a concrete reference for webhook states, idempotent retries, and audit-ready records while you build this flow? Read the Gruv docs.

Fix common failure modes before they become chargebacks#

Many preventable chargebacks start before a bank dispute. They can start with merchant-side process mistakes, conflicting promises, missing case evidence, or the wrong transaction path. Fix those upstream before they escalate.

Freeze conflicting support promises first.

If policy and support messages diverge, pause outbound macros first. Then align Terms and Conditions, checkout and receipt language, and support templates with what agents are actually sending.

When legal review is needed, verify FederalRegister.gov text against an official edition before relying on it. After alignment, retrain teams and reopen impacted cases where customer promises did not match the policy shown at purchase.

Block escalation when evidence is incomplete.

Do not allow Dispute escalation with missing case artifacts. Require the case file to include the order record, the policy version shown at purchase, the customer communication thread, payment event references, and timestamps for key events.

Enforce this in tooling with required fields, not agent discretion. If any required artifact is missing, the case should not advance.

Guard the choice between Authorization reversal and Refund.

Guard this choice with transaction state, not memory. Authorization reversal cancels a payment before it happens, while a Refund is a reversal type that happens after a transaction.

Add automated guardrails based on transaction and settlement status so agents are routed to the right action. Alert on mismatches between the chosen action and provider status, because those errors can turn avoidable disputes into chargebacks.

Related reading: How to Build a Spend Control Policy for Virtual Cards on Your Platform.

Roll out in 30 days with legal, ops, and engineering in lockstep#

A four-week rollout can work when each week ends with a clear go or no-go decision, a named owner, and a visible checkpoint. Treat the 30-day window as an internal execution cadence, not a universal legal or network deadline.

| Week | Focus | Checkpoint |

|---|---|---|

| Week 1 | Finalize clause text and ownership | Lock the policy language and ownership map together; verify checkout text, receipt text, Terms and Conditions, and support macros reflect the same outcome |

| Week 2 | Ship the decision tree and escalation routing | Publish one decision path for each outcome your team handles; align templates and escalation routes; run a cross-functional case review |

| Week 3 | Deploy controls in staging | Move approved state handling into staging and validate the controls your team relies on; test duplicates, retries, delayed callbacks, and missing provider references |

| Week 4 | Audit live samples and publish one sign-off | Run a live-case audit sample and reconcile outcomes; publish a single launch-readiness sign-off with owners, open exceptions, and the go-live notice |

Week 1: finalize clause text and ownership.

In week 1, lock the policy language and ownership map together. Confirm who sends customer communications, who approves exceptions, and who owns final case decisions across legal, ops, and support.

Set one internal Effective Date for the package, then verify that checkout text, receipt text, Terms and Conditions, and support macros all reflect the same outcome before moving forward.

Week 2: ship the decision tree and escalation routing.

In week 2, publish one decision path for each outcome your team handles (for example, Authorization reversal, Refund, and Chargeback), and align templates and escalation routes to that path.

Run a cross-functional case review to confirm that legal, ops, and support reach the same resolution and customer message. Keep unresolved legal-exception branches routed to counsel instead of ad hoc agent decisions.

Week 3: deploy controls in staging.

In week 3, move approved state handling into staging and validate the controls your team relies on. If your stack uses them, include idempotent action handling and webhook or state-change checks.

Test failure behavior, not only happy paths. Duplicates, retries, delayed callbacks, and missing provider references should not produce contradictory outcomes.

Week 4: audit live samples and publish one sign-off.

In week 4, run a live-case audit sample and reconcile outcomes before launch. Each sampled case should be complete enough to verify what was promised, what happened, and why the final disposition was chosen.

Publish a single launch-readiness sign-off with owners, open exceptions, and the go-live notice so every team acts from one explicit signal.

Conclusion and copy-paste launch checklist#

Keep one operating rule: your policy text, product behavior, and ledger outcome should match for the same case. Use this checklist as a launch gate.

- Align customer-facing texts before launch.

[ ] Refund policy, Return policy, and Terms and Conditions are aligned across checkout, receipts, and support. Confirm the policy version shown at purchase, not just current site copy. If your Terms and Conditions include dispute limits like binding arbitration or a class action waiver, support should not promise a different dispute path.

- Approve one transaction decision table across teams.

[ ] Decision table for Authorization reversal, Refund, and Chargeback is approved by legal, ops, and engineering. Define trigger, initiator, and expected customer-visible outcome for each path. Validate with sample cases to confirm teams make the same decision from the same facts.

- Make platform-versus-seller ownership explicit.

[ ] Ownership is explicit between Marketplace platform and the other transaction party for funding, communication, and Dispute escalation. Document who funds the Refund, who communicates decisions, and who handles escalation.

- Enforce evidence-pack minimums before closure.

[ ] Evidence pack requirements are enforced before case closure. Case records should show what was promised, what happened, and which path was used, with supporting payment and communication records. For disputed charges, use procedures that include timely notice, a reasonable investigation, and other procedural minimums where applicable.

- Reconcile every incident to ledger and payouts.

[ ] Incident outcomes reconcile to ledger and payout effects with no unresolved variance. Confirm ticket outcome, ledger entries, and payout impact all match. For deeper implementation checks, use Refund Reconciliation for Platforms: Matching Returns Reversals and Ledger Entries.

- Confirm which legal and partner questions still need authoritative answers.

[ ] Team knows which jurisdiction and partner-rule questions require legal or processor confirmation. Do not treat FederalRegister.gov web text as the legal edition. When federal language matters, verify against the official PDF on govinfo.gov linked from the page.

If all six boxes are checked, you have a more operationally consistent launch baseline. If one is unclear, pause launch and resolve it before go-live.

If you want to validate this rollout against your current marketplace stack and compliance constraints, talk to Gruv.

Frequently Asked Questions

What is the practical difference between a refund and a reversal transaction in marketplace operations?

A refund is one type of payment reversal that happens after a transaction. Reversals also include authorization reversals (which cancel a payment before it happens) and chargebacks, which are customer-driven bank disputes that pull funds back from the business. In practice, separate them by timing, initiator, and whether funds have already settled.

When should we use an authorization reversal instead of a refund?

Use an authorization reversal when the payment is still in the authorization stage and can be canceled before it happens. If the transaction has already settled and you are resolving it directly, a refund is the typical path. Making this decision early can help limit downstream cost and risk.

Who is legally responsible for refunds in a marketplace platform model, the platform or the seller?

The provided sources do not establish a single legal rule for platform-versus-seller responsibility across marketplace models. Treat ownership as something to confirm in contracts and with counsel, not something to infer from the word “marketplace.” If responsibility is unclear, resolve it before support or ops handles disputes case by case.

What clauses must every refund policy include to reduce chargebacks and disputes?

The provided sources do not give a universal, legally required clause list for every marketplace. What they do support is the operational goal of following through on promises (for example, delivery and refunds) and avoiding escalation into chargebacks, which are typically the most costly reversal type. Keep policy language and execution aligned so outcomes match what was promised.

How do state-level U.S. rules change refund and return policy design?

These sources do not provide state-by-state rules or federal thresholds. Do not hardcode legal assumptions from this section alone. Route state-specific policy design through legal review.

What records should ops keep for disputes involving issuing banks, card networks, or seller complaints?

Keep records that let a reviewer verify what was promised, what happened, and which path was used: authorization reversal, refund, or chargeback. Include enough payment and case evidence to show initiator, timeline, and final disposition. Clear records support dispute handling across cardholders, banks, and merchants.

Try a related tool

A former product manager at a major fintech company, Samuel has deep expertise in the global payments landscape. He analyzes financial tools and strategies to help freelancers maximize their earnings and minimize fees.

Priya specializes in international contract law for independent contractors. She ensures that the legal advice provided is accurate, actionable, and up-to-date with current regulations.

Sources

- cms.gov/newsroom/fact-sheets/hhs-notice-benefit-paym...trusted

- cms.gov/newsroom/fact-sheets/2025-marketplace-integr...trusted

- dodcio.defense.gov/portals/0/documents/desmf%20edition%20iii%20...trusted

- dos.ny.gov/system/files/documents/2024/05/050824.pdftrusted

- ecfr.gov/current/title-12/chapter-X/part-1005trusted

- ecfr.gov/current/title-45/subtitle-A/subchapter-B/par...trusted

- federalregister.gov/documents/2026/04/06/2026-06600/medicare-pro...trusted

- federalregister.gov/documents/2026/01/30/2026-01907/improving-tr...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Copyright Considerations for Freelance Photographers in the Age of AI

Treat AI photo work as contract-first from day one. It will not give you perfect certainty, but it does reduce avoidable ambiguity by forcing expectations into writing before production starts.

Country Rules for Late Fee Automation in Marketplace Invoices

Late fee automation in marketplace operations is first a legal and accounting control decision, not a convenience feature. When a fee is triggered automatically, you are deciding whether the charge is allowed and how it will be posted, reconciled, and explained later.

Refund Reconciliation for Platforms and Clean Ledger Entries

If you treat commerce orders, payment activity, settlement data, and bank deposits as separate truths, your refund accounting can drift even when each source looks internally consistent. Refund reconciliation is more reliable when you model those records as one connected chain from customer event to payout impact to General Ledger (GL) entry.