Quick Answer

To receive international payments in Ukraine, choose the rail you can verify and reconcile first, then test it in a live pilot. SWIFT or wire is usually the cleanest primary path for auditable bank credit, while cash pickup, bank deposit, or wallet routes should stay fallback options until posted receipt, amount, currency, and compliance conditions are proven for your exact corridor.

Treat Ukraine payment receipt as a routing-and-risk decision#

Treat receive international payments Ukraine as a routing-and-risk decision, not a provider-signup task. The key question is which rail you can verify, reconcile, and defend if a transfer fails or a compliance review asks why it was approved.

You are not choosing from one proven path. Start with candidate routes, such as SWIFT, wire transfer, cash pickup, or wallet/account deposit options, and remove anything you cannot verify for your corridor, counterparties, and recipient type.

- Define rail first, provider second.

Set the receiving outcome first: credited bank funds, cash collection, or another deposit path you can evidence after settlement. That choice determines the data you collect, how you reconcile, and which failure modes matter most.

- Separate verified facts from unknowns immediately.

Track two columns from day one: verified in our test flow and still unknown. Include route availability, timing, USD/UAH FX treatment, recipient data requirements, and exception handling. Until you see an end-to-end transfer with a matching posted amount, settlement currency, provider reference, and recipient confirmation, treat the route as an assumption.

- Collect a minimum evidence pack before first transfer.

For account-based routes, capture beneficiary details exactly as provided, intended currency, and your internal reconciliation reference. For cash-style flows, define the release artifact you require, for example a transfer reference or control number, plus recipient confirmation. Reject incomplete payout instructions before funds move.

- Use exact compliance documents, not generic comfort.

OFAC FAQ 1225 references two specific General Licenses: GL 128B and GL 131D. OFAC states they are similar but have different terms and expiration dates. GL 128B was issued on December 4, 2025 and expires on April 29, 2026; GL 131D extends existing authorization until May 1, 2026. This does not mean those licenses automatically cover your Ukraine flow. It means your review should cite the exact document, confirm dates, and check conditions on blocked-person involvement. In the cited authorization, transactions are conditioned on not involving blocked persons beyond the stated LIG exception.

This guide follows that sequence: choose candidate rails, collect evidence, model full USD-to-UAH outcomes, and keep a written boundary between what is verified and what is still unknown.

Set the operating scope before comparing providers#

Define your launch scope before you compare brands, or you will end up comparing offers that lead to different end states.

- Define what "received" means first.

Choose one primary launch outcome: account-based credit into a Ukrainian bank, for example SWIFT or wire-style routing, or a recipient-side outcome such as cash pickup, bank deposit, or mobile wallet deposit that you will verify in your own flow. If you need cleaner audit and reconciliation, prioritize the account-credit objective and treat other paths as fallback until proven. Verification point: record the exact success proof you require, such as posted credit with matching amount/currency or recipient confirmation for collection-style payout.

- Lock first corridors and currencies before naming providers.

For receive international payments Ukraine, set the first sender market and payout currencies up front, commonly USD to UAH for initial modeling, then shortlist Payoneer, Western Union, PayPal, or Xoom. This prevents false comparisons across pages with different market scope. PayPal's US consumer fees page states its published rates apply to US accounts, points readers to Ukraine-specific service details, and shows a last-updated date of February 19, 2026. Use it as a recency checkpoint, not a universal rule.

- Document unknowns before demos shape the decision.

Keep a visible unknowns at launch list: limits, timeline certainty, agent-location usability, availability of bank-account deposit in your tested corridor, and residual FX/card/bank charges even where temporary fee relief is advertised. Red flag: treat marketing claims as non-binding until your test flow confirms path availability, landed amount, and exception handling. Keep sanctions checks tied to the exact OFAC program, since prohibitions vary by program and can apply to certain non-US persons.

Choose the primary rail before you choose the brand#

Choose the rail based on the proof you need operationally, then shortlist brands. If your model depends on auditable account credits and reconciliation, make account-based settlement your primary path, for example SWIFT or wire, and treat cash pickup options as a fallback path to validate, not the default.

If you need a rail-level framework before you narrow providers, pair this article with Cross-Border Payments Guide for Platform Operators and SWIFT vs Local Bank Transfers for Cross-Border Platforms. Those two references help you separate the rail decision from the provider signup flow.

If recipient banking access is uneven, run a dual-path test: keep wire transfer as primary and test an agent-location fallback, for example Western Union, MoneyGram, or Ukrposhta-linked flows, in the same corridor and currency. Judge each path by the receipt evidence it produces, because posted account credit and recipient collection create different audit trails and support burdens.

For PayPal/Xoom, verify recipient-side withdrawal mechanics in Ukraine before you treat them as viable rails. PayPal classifies international status by sender/receiver resident markets, and its fee tables are market-scoped, so US pages are not universal for non-US account residencies. Even where PayPal notes temporary fee waivers for transfers involving Ukrainian PayPal accounts, exchange-rate and card/bank charges may still apply, so sender-side onboarding does not prove landed value or payout reliability.

Use PayPal's US consumer fees page as a checkpoint, not payout proof. As of February 19, 2026, it points to a Ukraine-specific fees page and Help Center update path; keep PayPal/Xoom in the unknown column until your own recipient-side test confirms the exact withdrawal or deposit flow for your corridor.

Compare receiving options on one operator table#

Put every candidate route in one table and rank proof above brand familiarity. If payout mechanics or fee scope for Ukraine are still unclear, keep that route below any path you have already reconciled end to end.

| Route | Recipient method | Required data | Transaction fees | Foreign exchange spread | Proof status | Ops burden | Unresolved unknowns |

|---|---|---|---|---|---|---|---|

| SWIFT via Ukrainian banks | Account credit via bank transfer | Route-specific recipient and transfer fields your flow needs for matching | Confirm with sending and receiving institutions for the exact corridor | Confirm for the exact settlement and conversion path | Unknown until your pilot shows posted receipt evidence and internal matching | Lower when transfer references map cleanly to posted credits | Fee stack, FX handling, field validation, corridor reliability |

| Western Union cash pickup | Cash pickup at agent location | Route-specific pickup and recipient-identification fields, for example control/reference details where required | Confirm for the exact corridor and payout mode | Confirm at quote and collection stages | Unknown for Ukraine corridor unless your pilot verifies it | Higher manual handling at collection and exception points | Location availability, collection-proof quality, exception handling |

| PayPal/Xoom bank account deposit | Claimed account-deposit path; recipient-side mechanics must be proven | Recipient-side deposit/withdrawal fields must be validated in the exact corridor | PayPal states some fees are temporarily waived for transfers involving Ukrainian PayPal accounts; other charges may still apply. Xoom fee scope is not established here | PayPal states exchange-rate or bank/card-issuer charges may still apply | Claimed by provider for fee treatment; payout mechanics remain Unknown for Ukraine corridor | Medium to high until posted-state evidence and recipient flow are proven | Whether funds land as intended, corridor-specific fee scope, withdrawal mechanics, Xoom route behavior |

| Mobile wallet deposit where available | Wallet deposit if the route supports it | Route-specific wallet/account identifiers | Verify in pilot | Verify in pilot | Unknown for Ukraine corridor | Medium if platform evidence is automated; high if recipient confirmation is manual | Availability, eligibility, posted-funds evidence, failed/reversed credits |

Use proof labels strictly:

Verified in pilot: one live transfer with posted receipt evidence, internal matching, and no unresolved recipient-access gap.Claimed by provider: fee pages, help content, or support statements without end-to-end corridor proof.Unknown: any unresolved fee, FX, payout, or access behavior.

For PayPal specifically, treat the U.S. consumer fee page as a checkpoint, not corridor proof. As of February 19, 2026, it says some fees are temporarily waived for transfers involving Ukrainian PayPal accounts, while exchange-rate and bank/card-issuer charges may still apply, and the page is scoped to the U.S. market. Capture the printable PDF as evidence and monitor the Policy Updates Page for timing changes before you change proof status.

Keep compliance uncertainty next to payout uncertainty. OFAC says sanctions prohibitions vary by program and can apply to certain non-U.S. persons. BIS Part 746 is the focal EAR reference for comprehensively sanctioned countries, but it is not route-level approval for a Ukraine payout path. Promote only rows with usable receipt evidence and no unresolved unknowns.

Prepare the recipient evidence pack before first transfer#

Do not release a first live transfer until your evidence pack can prove receipt, matching, and currency outcome for that specific route. Thin recipient records are where pilot-friendly flows fail in real operations.

Step 1 Define the minimum pack by rail#

For SWIFT or wire routes, store the recipient instruction set exactly as provided by the receiving bank or payout provider, the intended receipt currency, and the original source record for those instructions. Keep both the structured fields entered in your payout system and the raw source artifact, for example a screenshot, email, or PDF.

Do not use a generic "Ukraine bank transfer template" as a substitute for route confirmation. The exact beneficiary field set for Ukrainian SWIFT or wire receipt has not been confirmed, including whether extra routing or intermediary-bank details are required. If the full instruction set is not confirmed for the specific corridor, keep it Unknown and stop before funding.

For cash or agent-style collection, keep the pack route-specific and explicit: provider-issued pickup reference, if provided, expected amount, expected currency, submitted recipient name, and selected collection route. Do not assume control number plus amount/currency is universally sufficient for Ukraine collection flows; treat additional pickup fields as Unknown until the provider confirms them.

Step 2 Standardize receipt evidence capture#

Use one evidence bundle per transfer across all rails so finance, ops, and compliance review the same packet.

At minimum, capture:

- posted receipt evidence showing amount and currency received, including USD/UAH outcome where relevant

- provider-native reference from the route used, for example Payoneer, Western Union, or PayPal references

- internal reconciliation notes mapping that external reference to your own invoice, payout, case, or transfer ID

- receipt confirmation owner and timestamp

Keep provider references in original form, then map internally. A common first-transfer failure is not payment loss, but posted funds that cannot be matched back to the correct recipient or expected currency.

If PayPal is in scope, save the policy artifact used during review. The U.S. consumer fees page, last updated February 19, 2026, says some fees are temporarily waived for transfers involving Ukrainian PayPal accounts, while exchange-rate or bank/card-issuer fees may still apply. The U.S. merchant fees page, last updated February 9, 2026, is also a checkpoint. Both pages are U.S.-account scoped and do not prove recipient-side withdrawal mechanics in Ukraine.

Step 3 Add a preflight check that can reject payout#

Your preflight should fail closed: reject any transfer with missing, conflicting, or unsupported route instructions before funds are sent.

Use a simple gate: no payout release unless the route is named, payout instructions are attached, expected amount/currency are locked, source record is on file, and recipient-side mechanics are either pilot-verified or explicitly labeled Unknown. If PayPal route behavior for recipient-side landing in Ukraine is not verified, keep it in pilot status rather than production-ready.

Execute account-based receipt through SWIFT and local banks#

Execution is complete only after beneficiary credit is confirmed and reconciled, not when the wire is marked sent. For account-based receipt, close the loop on beneficiary match, posted amount, posted currency, and internal reconciliation before you treat the transfer as done.

Step 1 Collect bank-issued receiving details#

Use the receiving bank's own instruction set for this exact route. For example, PrivatBank states SWIFT transfers can receive funds from abroad into an individual's account, and it provides payment-details generation in Privat24.

Validate the SWIFT code (BIC) as provided, including format length of 8 or 11 characters. If details are updated, retain prior versions so you can audit exactly which instruction set was used.

If your ops team is still normalizing identifier checks, review What Is a SWIFT Code or BIC for International Payouts and What Is an MT103 and How to Use It to Trace a Wire Transfer before you lock the playbook. They are useful for training reviewers on what they should verify when a transfer exception appears.

Step 2 Send through SWIFT exactly as instructed#

Enter the transfer exactly as shown in the bank-issued details. SWIFT is a messaging network, and payment orders can pass through intermediary-bank processing, so sender-side submission status is not the same as confirmed beneficiary credit.

Before release, run a field-by-field check between your payout entry and the bank artifact on file: beneficiary name, account identifier, SWIFT code, and any other required fields. If your sending workflow cannot represent a required field, stop and resolve it before funding.

Where your bank or intermediary uses extra routing instructions, keep a reference explainer in the runbook. For Further Credit (FFC) Wire Transfer Guide is useful when finance or support teams need to distinguish beneficiary data from downstream credit instructions during exception handling.

Step 3 Confirm beneficiary and currency outcome separately#

Mark success only after you confirm both who was credited and which currency posted. This avoids reconciliation errors where amount and currency assumptions diverge from what actually landed.

If the receiving setup is tied to a hryvnia account, plan for local-currency posting. PrivatBank explicitly advertises auto-conversion from foreign currencies, including USD, to a hryvnia account; that indicates a possible conversion outcome, not a guaranteed rate or cost. Track posted amount and settlement currency, especially USD versus UAH, before closing the case.

Step 4 Require one fully reconciled live wire before production status#

Treat the first live wire as a pilot. Keep the route in pilot status until one live transfer is reconciled end to end with: bank-issued receiving details used, sent SWIFT instruction, external reference linked to your internal transfer ID, and posted receipt evidence of credited amount and currency.

If a transfer is sent but beneficiary credit is not cleanly confirmed and matched, treat it as an unresolved exception rather than a production-ready success.

Execute cash and wallet receipt paths without losing control#

Cash pickup and wallet/account deposit should run as separate receipt paths with separate completion rules. Once you move off direct bank rails, the main risk is handoff control and proof quality, not just field accuracy, so do not close either path from sender-side status alone.

Step 1 Separate the routes before you fund them#

Map cash pickup and deposit routes as distinct ops products, even if the sender sees one brand experience. If you test Western Union or MoneyGram for cash pickup, keep that path separate from any PayPal or Xoom-style bank account deposit or mobile wallet deposit path, because evidence requirements, failure modes, and support load differ.

Before first use, run a route-level sanctions and compliance check for the exact corridor and parties. OFAC states prohibitions and authorizations depend on program documentation, and some financial transactions are prohibited unless authorized or exempted. Use August 21, 2024 as the dated checkpoint for the FAQ set cited here, then confirm whether route-specific rules changed after that date.

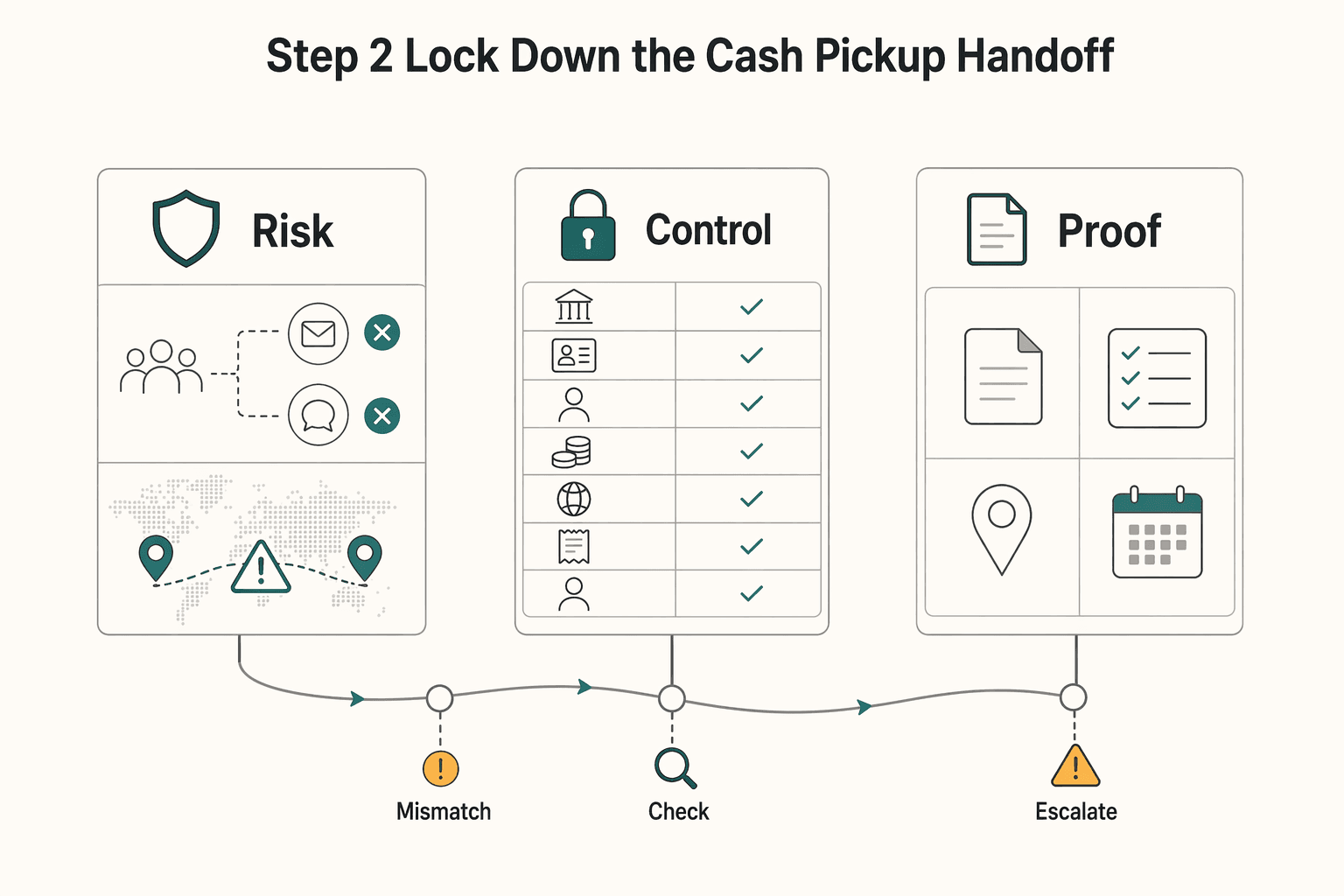

Step 2 Lock down the cash pickup handoff#

For any cash pickup pilot, create a handoff record before release. At minimum, log provider, transfer reference or control number, if used, recipient name as entered, sent amount, sent currency, internal transfer ID, and which staff member shared pickup details.

Keep control-number handling tight. Do not pass it through broad support inboxes or open chat threads; remittance channels are treated as financial-crime risk surfaces in formal U.S. policy discussions, and loose handoff handling quickly increases exceptions. If a route uses agent-location collection, verify the provider's actual identity-check and document rules before launch instead of assuming a standard Ukraine process.

Your verification point is recipient collection evidence returned to ops. That can be provider-issued pickup confirmation, a receipt image, or another artifact tied to reference, amount, and currency. If you cannot match proof to the internal transfer ID, do not mark funds as available.

Step 3 Require posted-state proof for wallet or account deposit#

For PayPal or Xoom-style deposit paths, sender-side "sent" or "completed" status is not enough. Cross-border payments can involve multiple banking partners or financial intermediaries, so sender confirmation does not prove beneficiary credit.

Mark the transfer complete only when you have recipient-side posted-state evidence or a provider artifact showing the deposit landed. The minimum evidence pack should include posted amount, posted currency, posting date, provider reference, and a beneficiary or wallet identifier that matches the intended recipient. If conversion happened before posting, store instructed currency and posted currency so finance can reconcile without a silent FX gap.

A common failure mode is false closure: ops sees a completed notice while the recipient still has no usable funds, or posting details differ from expectations. If posted credit is not provable, keep the case open.

Step 4 Make the tradeoff explicit in your launch rules#

Cash pickup can expand reach when bank access is uneven, but it usually creates more manual exception handling than direct account deposit. The real tradeoff is higher support volume, higher handoff risk, and more case-by-case proof collection.

If your priority is cleaner reconciliation and lower-touch operations, keep account deposit primary and use cash pickup as fallback. If you enable cash, keep it in pilot status until one live transaction is fully evidenced end to end with route approval, handoff log, recipient confirmation, and provider proof matched to your internal record.

Model the true landed cost before rollout approval#

Approve routes on landed cost, not headline fees. For each candidate path, keep one cost row and mark every unsupported field as Unknown until you have a verifiable artifact.

This section is about proving what the transfer actually costs at receipt, not just proving that funds arrived.

Step 1 Build a cost sheet that exposes missing inputs#

Use a USD-origin model with recipient outcome in UAH. Track at least: route name, transaction fees, FX spread, recipient net in UAH, quote timestamp, settlement or posting timestamp, evidence source, and proof status.

Current Ukraine cost figures for Payoneer, Western Union, or PayPal/Xoom are not confirmed, so all cost fields start as Unknown, not estimates.

| Candidate route | Transaction fees | FX spread | Recipient net in UAH from USD-origin payment | Evidence source | Proof status |

|---|---|---|---|---|---|

| Payoneer assumption | Unknown | Unknown | Unknown | Not verified in provided evidence | Unknown |

| Western Union assumption | Unknown | Unknown | Unknown | Not verified in provided evidence | Unknown |

| PayPal/Xoom assumption | Unknown | Unknown | Unknown | Not verified in provided evidence | Unknown |

Only populate a field when you can attach proof, for example provider quote capture, fee disclosure, posted receipt, or reconciled live transfer record.

Step 2 Compare routes side by side, but freeze unsupported assumptions#

Keep the comparison even when rows are mostly unknown. It shows what still must be tested before approval.

For each route, separate these checks:

- What is proven about transaction fees?

- What is proven about conversion into UAH?

- What is proven about recipient posted amount?

Do not merge them into one opaque "cost" value.

For compliance-sensitive decisions, treat legal-source status carefully: FederalRegister.gov is informational and not the official legal edition, and legal users are told to verify against the official edition. Log the official PDF checkpoint and citation metadata, for example 90 FR 1636, when legal conditions are part of route approval. Likewise, eCFR is labeled authoritative but unofficial.

Step 3 Add FX sensitivity before finance sign-off#

Model variance between quote time and settlement or posting time. This isolates FX timing risk from fee effects.

Use one sensitivity block per route:

- Quoted USD amount and quote timestamp

- Quoted FX rate into UAH, if available

- Settlement or posting timestamp

- Settlement FX rate into UAH, if available

- Variance in recipient UAH versus quoted expectation

If live data is missing, keep placeholders and leave unsupported rate inputs unknown.

Step 4 Gate approval on evidence, not spreadsheet completeness#

Require one evidence pack per route before rollout approval: quote or fee capture, transfer reference, recipient-side posted proof, and internal net-UAH calculation tied to those artifacts.

If any artifact is missing, keep the route in pilot.

Set compliance gates for wartime-sensitive operations#

After cost modeling, the next gate is compliance discipline. Do not scale a route until you can prove recipient identity handling, route choice, and exception handling when behavior shifts from baseline.

Step 1 Define escalation triggers before volume starts#

Set escalation rules before launch. At minimum, require a recipient identity check, a route-level risk review when payout behavior changes, and a named owner for exceptions.

Use the U.S. Treasury June 12, 2024 update as a dated checkpoint in your control design. That update announced over 300 new sanctions across Treasury and State, increased secondary-sanctions risk for foreign financial institutions, and described targeting Russia's financial-system architecture. In practice, re-review routes when counterparties, intermediaries, or payout patterns change.

If a payment departs from your approved baseline, pause and review. Verification point: every trigger should map to a saved artifact, not only policy text.

Step 2 Require route-level traceability for every received payment#

Require traceability for every received payment, whether the route is account-based or manual. Store the provider reference, institutions recorded in your payment records, beneficiary record used, and posted or collection proof.

Do not invent required fields you cannot verify. Exact SWIFT field requirements, control-number formats, and Ukraine-specific provider traceability formats have not been confirmed, so policy should require retention of exact provider-issued references and proof artifacts.

Step 3 Publish an explicit unsupported list for commercial teams#

Before market-facing claims, publish a short "verified vs unverified in Ukraine" sheet so commercial teams do not overpromise.

| Claim type | Status labels to use |

|---|---|

| Route claims | Verified in pilot / Claimed by provider / Unknown |

| Timing claims | Verified in pilot / Claimed by provider / Unknown |

| Provider claims | Verified in pilot / Claimed by provider / Unknown |

Be explicit about gaps: exact KYC document requirements, legal payout caps, guaranteed settlement timelines, and provider-specific availability or legality in Ukraine are not confirmed and should be verified with the relevant authority before proceeding.

Step 4 Keep an audit trail that ties route choice to the outcome#

Keep one end-to-end record per payment that links route choice, verification status at approval, exceptions raised, and final outcome. The record should include transfer reference, recipient record used, proof of posted or collected funds, exception reviewer, and route-selection rationale.

For periodic regional context, you can retain the 2025 Ukraine Report artifact labeled Commission Staff Working Document, but do not treat it as a substitute for route-level sanctions review.

Verification point: sample one live payment periodically and confirm a different operator can trace it end to end without asking the original case owner for missing context.

Run a controlled pilot with hard go or no-go checkpoints#

Treat your first Ukraine launch as a controlled test, and expand only on evidence from that test. Do not scale a rail based only on a clean sender-side flow.

Step 1 Pilot two distinct rails in parallel#

Run one account-based path and one alternative path for the same pilot window, where that alternative is actually available to your recipient group. The goal is to test operational resilience, not just compare providers.

Define scope before funds move: recipient segment, geography, USD/UAH cost view, and what counts as a completed receipt. State coverage limits explicitly, since prior reporting on Ukraine noted that some references excluded separatist-controlled areas in Donbas.

Step 2 Gate each rail on three checkpoints#

Approve expansion only if each rail passes all three checks in your own pilot evidence:

- timeliness: observed completion window from your pilot cases

- reconciliation: provider reference matched to your internal payment record

- recipient confirmation: posted-funds proof or collection proof tied to the intended beneficiary

Verification point: for each successful case, a second operator should be able to verify amount, currency, reference, and recipient outcome without asking the original case owner.

Avoid false positives: "sent" status is not enough if you cannot verify recipient access. Historical reporting also documented access barriers to financial institutions for internally displaced persons, so confirmation should be treated as a core gate.

Step 3 Set rollback triggers before increasing volume#

Define rollback triggers up front, then enforce them. Typical triggers include repeated failed credits, unresolved unknowns after provider follow-up, or inability to validate true landed cost in USD/UAH from pilot artifacts.

Keep one evidence pack per test case: provider-issued reference, beneficiary record used, posted or collection proof, exception notes, and calculated net outcome. If cost cannot be reconstructed from artifacts, treat that rail as not launch-ready.

Step 4 Convert pilot evidence into a launch matrix#

Close the pilot with a concise launch matrix signed by product, ops, and compliance. For each rail, record what was verified in Ukraine, what remains unknown, rollback owner, and decision status: approved, limited, or blocked.

Use the Ukraine 2025 Report and Chapter 9 - Financial services as policy-context artifacts only, not as proof that a rail is operational. Go or no-go should come from your pilot evidence.

Handle common breakdowns and recovery actions#

Treat every exception as a scope decision: either you recover it with verifiable evidence or you narrow launch scope. Do not clear cases based only on provider reassurance.

Step 1 Pause release when case data cannot be independently verified#

Pause any collection or release when required payout data is missing or recipient details do not match your beneficiary record. Do not retry until a second operator can re-check amount, currency, recipient details, and payout instructions against the provider reference from the case file.

If the corrected data cannot be confirmed without asking the original handler for interpretation, the case is still not release-ready.

Step 2 Rebuild landed cost from settlement artifacts#

If the landed amount looks wrong, separate transaction fees from FX spread using settlement evidence. Capture quoted amount, settled amount, settlement currency, and recipient net, then rerun route comparison on actuals rather than pre-send estimates.

If you cannot reconstruct the variance from your evidence pack, treat the route as unresolved.

Step 3 Reroute execution failures to a rail already verified in your pilot#

A route marked "where available" is not a guarantee. If that path fails at execution, move the case to a rail already verified in your pilot and mark the failed path as corridor-specific unknown until you have better evidence.

Step 4 Downgrade routes when provider support remains ambiguous#

Repeatedly vague support responses are a launch-risk signal. If support cannot clearly explain whether the issue was data quality, route availability, or settlement handling, downgrade that route from launch scope until evidence quality improves.

Keep one compliance stop condition separate from payout operations: if you are using a License Exception under EAR Part 740, any required EEI filing must include the correct License Code and ECCN. If General Prohibitions Four, Seven, Nine, or Ten apply, no License Exception applies, so treat that as a stop condition, not a recoverable payment exception.

Conclusion#

Launch only when compliance and operations evidence is signed off; a provider shortlist alone is not a go decision.

- Select primary and fallback rails for Ukraine (SWIFT/wire transfer, cash pickup, bank account deposit, mobile wallet deposit).

Treat these as candidate rails until corridor-level pilot checks confirm availability.

- Build and complete the recipient evidence pack, including control number requirements where applicable.

Use rail-specific required fields and reject incomplete instructions before funds move.

- Produce a verified cost table with transaction fees and foreign exchange spread in USD and UAH.

Approve only routes where finance can reconcile amount sent, settlement currency, and recipient net from pilot evidence.

- Run a dual-rail pilot and confirm end-to-end reconciliation before scale.

Do not treat sender-side success as completion without verified recipient credit or collection.

- Publish a signed go/no-go memo listing verified facts, open unknowns, and escalation owners.

State the control context clearly: martial law has applied since 24 February 2022, NBU Resolution No 18 is updated regularly, inbound payments are generally allowed on a usual basis, and most payments from the Russian Federation/Republic of Belarus are generally restricted. If a transaction type has extra conditions, document them, including NBU E-Limits processing where applicable, and assign an owner to re-check them.

If your memo cannot show current restriction checks, unresolved unknowns, and named escalation ownership, treat launch as no-go.

Frequently Asked Questions

What are the main ways to receive international payments in Ukraine?

Main options here are account based wire transfer, including SWIFT linked bank receipt, and bank listed transfer systems. PrivatBank lists PrivatMoney, Western Union, RIA, MoneyGram, and MEEST on its receive/send page. Transfers can be sent and received 24/7, including weekends, but corridor level availability still needs your own pilot check.

What recipient information is required before funds can be collected or credited?

There is no single universal field list to rely on. Treat recipient data as rail specific and keep exact requirements marked unknown until each route is validated in your own flow. Do not mark funds collectible or credited when key case data is missing or cannot be independently verified.

When should operators choose SWIFT and wire transfer instead of cash pickup?

Choose SWIFT or wire when you need account credit traceability and cleaner company to company reconciliation. The article treats wire transfers as one of the most reliable methods between companies in different countries. Keep cash pickup as a separate path that needs corridor proof before launch.

How should teams compare bank account deposit versus mobile wallet deposit in Ukraine?

Compare only routes you can verify in a live corridor test. Keep mobile wallet deposit labeled unknown until you confirm availability and define proof of successful posting and failure recovery. Approve bank deposit routes only when you can reconcile beneficiary, amount, currency, and provider reference end to end.

Which costs matter most beyond headline transfer fees?

Recipient net matters more than the advertised fee alone. Reconcile amount sent, settlement currency, and amount credited or collected using settlement evidence so you can explain any variance. If your team cannot reconstruct that variance, treat the route as not rollout ready.

What should remain labeled as unknown before launch approval?

Keep exact recipient data by rail, real settlement timing, true landed cost, and corridor level route availability labeled unknown until verified. Treat sanctions scope as a live check item, not static text. The cited Eurobank FAQ references announcements dated 03/03/2022 and 09/03/2022, including a SWIFT ban applying to 7 Russian banks and named Belarus banks, but the article says to use that only as a risk signal, not a complete current sanctions map.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- 2009-2017.state.gov/documents/organization/253123.pdftrusted

- 2009-2017.state.gov/e/eb/rls/othr/ics/2013/204754.htmtrusted

- bis.gov/regulations/ear/746trusted

- bis.gov/regulations/ear/740trusted

- congress.gov/bill/119th-congress/senate-bill/1071/text/eahtrusted

- congress.gov/bill/119th-congress/senate-bill/1071/texttrusted

- ecfr.gov/current/title-15/subtitle-B/chapter-VII/subc...trusted

- federalregister.gov/documents/2025/01/08/2024-31486/preventing-a...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: