Quick Answer

A platform should escalate to formal permanent establishment review when people in one market start negotiating or finalizing contracts, carrying out recurring core business activity from a local place, or acting like dependent agents for the foreign entity. PE is a tax question, not the same as payroll or hiring, and contractors or an EOR do not automatically remove the risk.

When to Move From Monitoring to Formal Review#

Permanent establishment platform risk is often a timing and fact-pattern problem. Operations can look stable, then a small in-market change can turn PE from background tax exposure into a governance decision. Common examples include giving local teams real contract authority or letting a local work location become part of normal delivery.

Permanent Establishment, or PE, is a tax threshold. Broadly, it means an overseas jurisdiction where your enterprise's activities are carried out wholly or partly. When that threshold may be met, the issue shifts from payment operations to potential taxable presence and local corporate tax obligations on income generated in that jurisdiction.

For platform operators, the core risk is that the global model can look lightweight from HQ while local facts look very different to a tax authority. A fixed place of business, a dependent agent acting for the company abroad, or practical authority to sign contracts or make significant decisions can all matter. In practice, PE exposure can show up in day-to-day operations before it is obvious in the legal structure.

This guide helps you spot that shift early without turning every market into a legal project. The focus is on when PE should move from routine monitoring to employer-level governance across compliance, finance, and legal, especially when local activity starts to influence revenue, customer commitments, or recurring in-country delivery.

PE analysis also changes over time. Recent OECD commentary updates in 2025 included updated analysis for remote and home-office fact patterns. The commentary summary included a 50% working-time benchmark in that analysis. That does not create a single global rule, but it does mean cross-border workforce arrangements should be reassessed periodically.

A practical starting control is documentation. If your position depends on activity being auxiliary or lacking real authority, keep detailed records that support it. Misreading PE rules can lead to serious financial and legal consequences, and weak documentation can make PE positions harder to defend.

This is an operator decision guide, not legal advice. PE outcomes depend on local tax law and the wording and interpretation of the relevant treaty. The sections that follow focus on the triggers and escalation points you can control internally, so you know when monitoring is enough and when formal review is overdue.

Related: The 'Home Office as a Permanent Establishment' Risk for Consultants.

Start with the terms that drive the decision#

Define PE terms first, then keep them separate from payroll, hiring, and registration decisions so you can answer the tax question cleanly.

The four terms that matter most#

| Term | Meaning |

|---|---|

| Permanent Establishment (PE) | An ongoing or fixed taxable presence in another country that can trigger local tax obligations |

| Fixed place of business | A physical location, for example an office, branch, factory, or workshop, where business activity is regularly carried out |

| Dependent agent | A person or entity acting for the company abroad whose regular activities can create taxable presence for the company |

| Contract authority | A high-signal agency fact pattern, especially where someone in-market can sign contracts or make significant decisions for the business |

These terms are framed through treaty concepts, often discussed via OECD and UN model conventions, but outcomes still turn on local tax law and should be escalated for local legal/tax interpretation.

PE is not the same determination as foreign entity registration, payroll setup, or broader cross-border employment compliance. Those tracks overlap, but they are not interchangeable.

If PE is found, the consequence chain usually starts with potential corporate income tax obligations and other local compliance requirements.

Known vs unknown#

| Widely accepted starting points | What only local review can confirm |

|---|---|

| PE can arise through a fixed place of business or dependent-agent activity | Whether your exact facts meet that jurisdiction's PE test |

| Regular in-market activity and real contract authority are high-signal facts | How local tax law and treaty wording apply to those facts |

| PE can trigger local corporate tax and compliance obligations | Filing and compliance treatment under local law |

Use this as a practical checkpoint: if your position depends on local activity being auxiliary, keep detailed records of what was done, where, and by whom. A common failure mode is misreading PE rules and lacking evidence when authorities test who actually held decision power.

Map PE triggers by platform operating model#

Map PE risk to operating facts, not platform labels. Use this map as a screening tool, not a jurisdiction-specific legal test. Start with three questions: who negotiates or finalizes contracts, whether business activity is regularly carried out from a local place, and whether local people are acting like dependent agents for the foreign entity.

| Platform model | PE fact pattern to test | Service rendering risk signals to watch | Dependent agent risk signals to watch | Trigger to action |

|---|---|---|---|---|

| Marketplace for sellers | A local market team or local entity moves beyond promotion into core commercial activity | In-country onboarding, merchant management, or revenue-linked support appears tied to core business activity in that market; a recurring local site is used for core activity, not just admin | Local staff or a local subsidiary negotiates or finalizes seller or buyer contracts for the parent, including commission-agent style activity | If local teams start negotiating commercial terms or using a recurring local site for core activity, open tax and legal review |

| Contractor payout platform | The model moves from payout processing into in-market delivery, client handling, or contractor-side service execution | Local personnel handle substantive service issues, coordinate delivery, or run client-facing work that looks like business activity rather than back-office support | A country lead or local representative negotiates client or contractor terms on behalf of the offshore entity, even if final signature is elsewhere | If local roles shift from support to substantive delivery, or they handle contract discussions for the foreign company, open tax and legal review |

| Creator monetization layer | A local monetization team starts generating market revenue from a stable in-country base | Local teams run brand campaigns, creator programs, or recurring in-country activity tied to monetized work | A local partnerships lead negotiates and closes brand or creator deals, or effectively controls commercial decisions for the foreign entity | If local monetization staff gain negotiation authority or run recurring in-country activity tied to revenue, open tax and legal review |

What actually moves the risk up#

Contract authority is a first thing to test. If a local employee, contractor, or subsidiary is negotiating and finalizing contracts for the parent company, you are close to a dependent-agent fact pattern linked to PE findings.

Another signal is whether local teams move from support into substantive commercial activity in-market. If they start carrying core commercial relationships locally, risk can rise.

Recurring local delivery points also matter because PE is not limited to formal branches or offices. If your model relies on a stable local place where business activity is regularly carried out, fixed-place risk becomes harder to dismiss.

The evidence check most teams skip#

The control is evidence, not policy language alone. Keep documentation that shows who negotiated, who finalized, where work was performed, and whether any recurring local location was used for core business activity. That matters because misreading PE rules can create financial and reputational damage, and without clear records it is harder to support a limited-scope activity position.

The commonly cited 2016 Dell Spain and 2010 Zimmer commission-agent examples both show why local contract activity gets attention quickly. A useful test is to compare contract approval records with real behavior. If headquarters signs, but local teams routinely negotiate core terms with minimal challenge, treat that as a review trigger.

Same payment volume, very different exposure#

Payment volume by itself is a poor proxy. It shows where money moves, not where taxable business activity may sit. In one market, negotiations can remain outside the country, local activity can stay administrative, and no recurring local site is used for core revenue activity.

In another market with similar volume, local teams may negotiate terms and run recurring in-country commercial activity. Same throughput, very different PE profile. Use operating facts as your trigger set: contract authority, recurring local business activity, and who is doing the substantive commercial work in-market. When those facts shift, open review early.

Use a clear escalation rule before legal fire drills#

Set an internal escalation rule so monitoring does not drift into late-stage legal triage. A single PE trigger criterion is not established here, so use a documented operating trigger when signals begin to cluster in one market.

This is not a legal threshold. It is an operating trigger that moves the issue out of passive tracking and into documented review.

A practical line in the sand#

An isolated signal can stay in monitoring. A recurring cluster should move to review.

| Signal pattern in one market | Default treatment |

|---|---|

| Isolated or low-impact signal with no repeat pattern | Monitor and log |

| Repeated signal with unclear ownership or inconsistent records | Monitor with tighter checkpoints |

| Multiple material signals appearing together | Escalate to formal PE review |

Keep the lanes separate#

Clear ownership improves review quality. Compliance owns the evidence log: who did what, where, and when, with records that can be verified. Finance models potential exposure ranges so leadership can judge materiality before conclusions are final. Legal validates the position under relevant rules and records assumptions, limits, and next checkpoints.

One simple control helps across all three lanes. Rely on primary records and official documents, not summaries alone, and verify key records against official editions where available.

Understand what contractor models do and do not protect#

Using an independent contractor can change parts of your compliance posture, but it does not automatically remove PE risk.

The label does not decide the tax result#

For PE, authorities look at how work is actually carried out in-country, not just the contract label. If they view your company as a real ongoing enterprise in that market, corporate tax liability can follow.

That is why "they are contractors, so we are fine" is a weak control. Scrutiny has increased in recent years, including focus tied to OECD Action 7, and enforcement also extends to contractor misclassification where people are treated like employees but labeled independent.

Where contractor setups still create PE exposure#

A core exposure path is agency PE. A contractor can still create risk if they function like a dependent agent and act on your behalf to close customer contracts or generate revenue.

Start with one checkpoint: who has real contract authority in that market. Then test the operating pattern around that role. Risk signals can include regular work from the same location and significant economic influence, especially when combined with customer-facing authority.

Contractor hiring and employment are not the same question#

Cross-border contractor hiring and formal cross-border employment are not interchangeable, and they can involve different worker-classification and compliance considerations. But they do not remove the core PE question: are people in-country acting in ways that make your foreign company look like a taxable local enterprise?

A contractor model may change your operating setup, but by itself it is not a PE shield. If a contractor relationship starts to look employee-like, or includes contract-signing authority, escalate classification and PE review together.

One escalation rule worth using#

Treat this as an operating trigger, not a legal threshold. Use combined review early rather than waiting for an inquiry and then defending exposure that may include back taxes with interest, penalties, audits, and reputational damage.

Related reading: How to Build a Risk-Based KYC Framework for Your Platform: Tiering Contractors by Risk Level.

Decide when EOR is useful and where it is not enough#

Use an Employer of Record, or EOR, when you need compliant in-country hiring quickly, but do not treat it as a blanket shield against PE risk.

Use EOR when speed matters more than local employer ownership#

An EOR can be a faster path to legal employment because you can hire without first setting up your own local entity. It also covers local-law employment compliance, payroll, and HR administration, which is useful when hiring must start before entity setup is ready.

EOR and direct entity setup solve different problems. EOR can be a fast operating bridge for employment. Direct entity setup may be a better fit when your model requires deeper local control and a registered long-term local footprint.

| Criterion | EOR | Direct entity setup | What to watch |

|---|---|---|---|

| Speed | Can speed hiring because you do not have to form a local entity first | Entity formation and local setup may come first | Faster hiring does not, by itself, resolve PE exposure |

| Control | EOR handles local employment administration, with role scope documented in localized contracts | Your company manages employment through its own local entity | If local roles need broad authority, structure should match that reality |

| Auditability | Localized contracts, payroll records, and role definitions should be documented | Records sit directly in your own entity structure | In either model, documents must match in-country activity |

| Residual PE exposure | Can reduce setup burden, but PE questions can still arise under local tax law | You are operating through a local entity posture | Choose the structure that matches actual market activity |

What a co-employment agreement can and cannot do#

A co-employment agreement can help allocate local employment administration to the EOR, including payroll and statutory employment terms. That can reduce employment-side confusion.

Its limit is factual, not contractual. PE analysis still depends on what people in-country actually do. If local personnel negotiate or sign contracts, manage clients, represent the business in-market, or operate from a recurring local footprint, including coworking space, PE exposure can still arise under local tax law.

One practical control is to verify that onboarding contracts and role descriptions match real responsibilities. If the paperwork says one thing but the role functions as revenue-facing commercial authority, the agreement will not cure that gap.

The tradeoff rule to actually use#

Use EOR for fast compliant hiring when the role can stay away from core in-market revenue activity. If revenue generation remains in-market, escalate tax review instead of assuming the EOR wrapper resolves PE risk.

Re-check the fact pattern as scope expands over time. Duration also matters in many treaty contexts, often beyond six months, so long-running arrangements should be reviewed again under treaty and local-law analysis.

Keep a compact evidence pack: co-employment agreement, localized employment contract with explicit responsibilities, signer matrix, and a short record of who can negotiate, approve, and sign customer contracts. Then confirm this matches your intended foreign entity registration posture. If those do not align, EOR may be a bridge to registration, not always a substitute for it.

Handle country variance without stalling execution#

Country variance is real, but it should not freeze execution. Treat it as a controlled review sequence, not an open-ended debate. A short written process turns PE uncertainty into a defensible decision.

Use a four-step confirm safely sequence#

| Step | Action | Details |

|---|---|---|

| 1 | Build an internal fact pattern first, not a conclusion | Document the local role, who speaks with customers, who negotiates terms, who signs, where work happens, and whether there is a recurring local place of business; attach the signer matrix, org chart, contract approval path, and any EOR or contractor documents |

| 2 | Send advisors a focused question pack | Request treaty and local-law analysis on your actual facts; ask whether the issue is fixed place of business, dependent agent PE, or both, which treaty article controls, and which facts would change the conclusion |

| 3 | Get a jurisdiction memo | Require a written country position tied to the stated facts, including what is confirmed versus still uncertain |

| 4 | Record the decision and review trigger | Log date, jurisdiction, advisor, facts relied on, decision owner, and the trigger for re-review if scope changes |

- Build an internal fact pattern first, not a conclusion.

Document the local role, who speaks with customers, who negotiates terms, who signs, where work happens, and whether there is a recurring local place of business. Attach the signer matrix, org chart, contract approval path, and any EOR or contractor documents.

- Send advisors a focused question pack.

Request treaty and local-law analysis on your actual facts. Ask whether the issue is fixed place of business, dependent agent PE, or both, which treaty article controls, and which facts would change the conclusion.

- Get a jurisdiction memo.

Require a written country position tied to the stated facts, including what is confirmed versus still uncertain.

- Record the decision and review trigger.

Log date, jurisdiction, advisor, facts relied on, decision owner, and the trigger for re-review if scope changes.

Why the same model can land differently in the US and Germany#

The same operating model can be treated differently across countries, so analogy is not enough. For example, a Germany-based commercial lead under an EOR with no formal signing authority but regular negotiation of core terms can raise PE questions. Whether that creates PE in US-related or Germany-related analysis depends on the applicable treaty text and local interpretation. The pressure point is usually dependent-agent behavior, local business footprint, or both.

Post-2015 PE developments and uneven implementation across jurisdictions increase that variance. US review materials are often organized around explicit treaty sections and treaty-benefit summaries, while Germany-side conclusions still require jurisdiction-specific review of treaty text and local law for the same fact pattern.

What stays unknown until local review#

Keep these items explicitly marked unknown until local review confirms them:

- exact thresholds under the relevant treaty and local tax law

- filing treatment if PE is found

- registration timing and related local compliance steps

Close with a short decision note. The key control is written assumptions. Without them, later scope changes make it hard to prove what was actually analyzed.

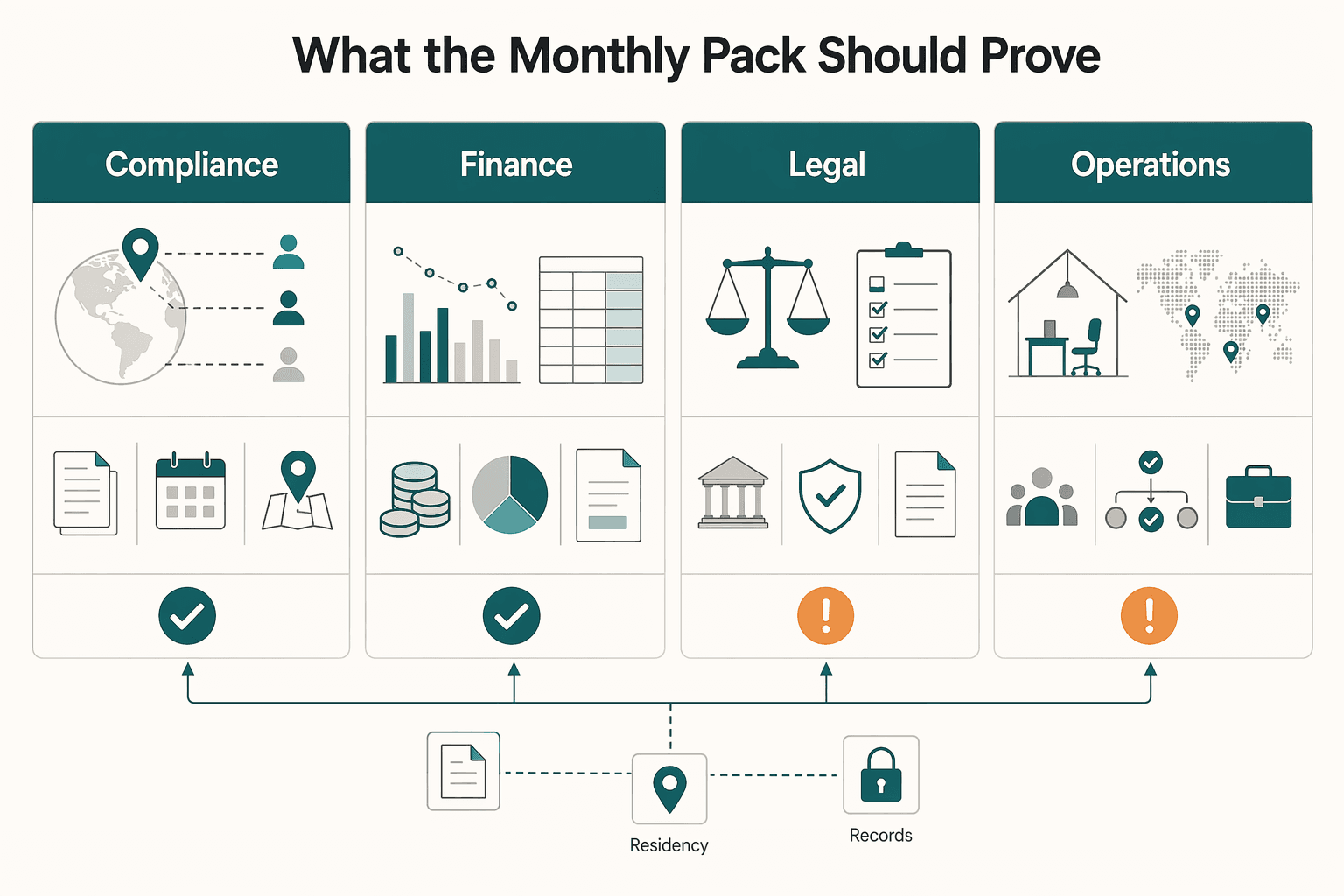

Build the monthly reporting checklist compliance teams can run#

Your monthly control should be a change-focused evidence pack, not a universal legal form. Its job is to keep compliance, finance, and legal aligned on the same current fact pattern so PE risk is assessed from evidence, not memory.

Keep the pack narrow: what changed in local activity, contract authority, and service-rendering footprint. That focus matters because PE can be triggered by a fixed place of business or a dependent agent, and an official office is not always required.

What the monthly pack should prove#

The pack should answer three questions quickly: what happened locally, what it could mean financially, and which legal position you are relying on now. If one of those is missing, review quality can drop and rework can increase.

Use delta reporting. You do not need to rebuild every jurisdiction file each month, but you do need to capture new local roles, shifts in negotiation or approval behavior, and changes in where work is actually performed. Include home-office facts as well, since in some countries a home office may be treated as a fixed place of business.

| Evidence lane | Required artifact | What to capture each month | Owner | Verification checkpoint |

|---|---|---|---|---|

| Compliance | Org chart | Current reporting lines for anyone working in or covering the host country; mark new roles and role changes | Compliance or HR ops | Match against HRIS headcount report and manager approvals |

| Compliance | Local activity log | Actual activities performed locally, especially customer contact, negotiation, delivery support, and recurring in-country work | Compliance | Reconcile to calendars, CRM notes, work tickets, or manager attestations |

| Compliance | Signer matrix for contract authority | Who can approve, negotiate, or sign customer or supplier terms, including practical authority versus formal signatory rights | Legal ops or compliance | Compare matrix to executed contracts and approval-path records |

| Compliance | Service rendering footprint changes | Where services are carried out, by whom, and whether work moved from preparatory or ancillary support into revenue-linked delivery | Operations | Confirm against onboarding records, staffing assignments, and service logs |

| Finance | Corporate income tax exposure scenarios | Current scenario assumptions if PE is found, including low, base, and higher exposure cases | Finance | Assumptions reviewed against latest activity log and jurisdiction memo |

| Finance | Double taxation risk note | Where tax could arise in both host and home jurisdictions and what assumptions are unresolved | Tax or finance | Confirm note aligns with current treaty position and advisor view |

| Finance | Filing calendar assumptions | Working assumptions for likely registration, reporting, and return-prep timing if PE is confirmed | Tax or finance | Date-stamp assumptions and mark them as assumptions, not deadlines |

| Legal | Treaty position notes | Treaty and local-law position relied on, including whether the issue is fixed place of business, dependent agent, or both | Legal | Record the treaty article or commentary used for the position |

| Legal | Foreign entity registration status (where applicable) | Not started, under review, initiated, completed, or not required, by jurisdiction | Legal or entity management | Match to board approvals, formation steps, or local counsel updates |

| Legal | Advisor determinations with timestamps | Latest written advisor view, facts relied on, open questions, and issue date | Legal | Confirm the memo's fact pattern still matches current operations |

| Operations | Payout and onboarding policy changes | Any policy change that affects who engages local users, how they are onboarded, or where activity is handled | Operations or product ops | Monthly signoff against policy repository and release notes |

The finance and legal lanes need explicit assumptions#

Finance should model consequences before an authority inquiry arrives. If PE is triggered, host-country corporate tax and reporting duties may apply alongside home-jurisdiction obligations, so scenarios should be date-stamped and assumption-based, including potential double-taxation exposure.

Legal should keep the governing position auditable. Anchor the file in the treaty analysis and local-law overlay. If OECD commentary is part of the reasoning, record the version used, including whether the 2025 update could change the position for that jurisdiction.

How teams usually get this wrong#

A common failure is collecting policy statements instead of evidence of conduct. A chart showing "no local authority" is weak if logs show in-country personnel habitually acting on the company's behalf in core commercial activity.

Another failure is delaying finance involvement until escalation. That is when penalties and fines can become a surprise instead of a managed risk.

Use one operational trigger rule: if signer authority changes, recurring revenue-linked local work appears, or service rendering shifts into the host country, route the updated pack to legal and finance in that same month. Keep an owner and verification checkpoint on every checklist row so the pack is defensible evidence, not self-reporting.

If you want a deeper dive, read The 'Permanent Establishment' Risk Mitigation Checklist. To operationalize the checklist with policy gates, status visibility, and audit-ready records, review the implementation patterns in Gruv Docs.

Use payments and ops signals as PE early warnings#

Use control and operations signals as reassessment triggers, not as proof of PE. A practical early warning is process drift: operating behavior can change before documented procedures do.

This makes the section a governance extension of your regular review pack: compare current execution with documented process and escalate mismatches.

Watch for repeated process drift#

Repeated deviations from documented procedures are control signals that the approved model may no longer match reality. On their own, they are not legal conclusions under local law or treaty analysis.

If the same deviation pattern keeps recurring, treat it as a procedure-deviation event and route it for review in the same reporting cycle.

Use telemetry as evidence, not legal shorthand#

Use operational telemetry as evidence of how work is actually being performed, then compare it to current documented procedures. If repeated patterns appear in operations but not in the documented file, treat that mismatch as a control risk.

Confirm with a qualified adviser whether payout routing changes, local collection-flow changes, or reconciliation anomalies establish a specific PE trigger.

Set one rule and assign owners#

Keep one governance rule: material procedure-deviation patterns trigger reassessment and documented review. Assign explicit ownership and one program control:

- Operations owners flag recurring deviations and preserve event-level evidence.

- Compliance checks alignment with current documented procedures and records.

- Legal and finance decide whether the current position and assumptions require refresh.

This follows a basic control principle: define roles and responsibilities, keep program controls current, monitor risks when guidance is not current, and escalate when procedures repeatedly deviate from the documented process.

Respond fast when PE risk looks probable#

When PE risk looks probable, treat it as an incident. The immediate goal is to stabilize facts, preserve evidence, and start legal and tax review under local law before operations shift again.

First 72 hours#

Use this as an internal response window, not a legal deadline.

- Consider freezing nonessential changes in the affected market or team, especially around approvals, payout routing, role scope, and customer-facing responsibilities.

- Preserve a dated evidence pack as it stood when the issue surfaced: activity logs, signer-matrix updates, policy or release changes, exception tickets, reconciliation records, and decision history.

- Start legal and tax review under local tax law and the relevant treaty with a short fact memo covering the trigger, jurisdiction, and what changed from the last approved model.

If the concern involves a home office or other local work location, document whether use appears regular and substantial rather than intermittent. The OECD 2025 update introduced an analytical framework for when a home or other location may be a fixed place of business. It includes a 50% of total working time benchmark and a commercial reason test, but local law and treaty analysis still control the outcome. Further OECD mobility guidance is still under discussion, so treat cross-border conclusions as jurisdiction-specific.

Choose a response path#

Pick the branch that matches the facts, not the fastest operational patch.

| Path | Use when |

|---|---|

| Operating-model change | Use when exposure came from conduct you can reverse through authority limits, role redesign, or removing the triggering activity |

| Foreign entity registration | Consider this when sustained in-market activity is now part of the operating model |

| Employer of Record (EOR) | Use when engagement and supervision structure is the core issue, but do not treat EOR alone as resolving PE risk |

Keep the communication chain tight#

Use a clear internal sequence for this incident, for example: compliance, then finance, then legal, then the executive sponsor. This is an internal control flow, not a legal requirement.

Assign one owner for decision logging. Record the trigger, facts reviewed, advisors engaged, options considered, interim controls, and final decision date so the rationale is auditable later.

Verification checkpoint#

Before closing the incident, confirm in writing that updated controls are live, responsibilities are assigned to named owners, and reporting cadence is set for the affected jurisdiction. Then verify the chosen path is operating as documented.

For a step-by-step walkthrough, see A German Freelancer's Guide to Permanent Establishment Risk in the US.

Avoid the mistakes that create preventable PE exposure#

Preventable PE exposure often comes from treating labels as proof instead of testing what people actually do in-country. An independent contractor agreement or a clean policy file does not settle PE if local activity reflects management, contract signing, employees, or operational control.

Do not treat contractor status as a PE answer#

Contractor status does not replace PE analysis. You can still have exposure where someone in-country habitually does business on your behalf as a dependent agent.

Check facts, not titles: who negotiates terms, who commits pricing, who moves deals to signature, and who controls local operations in practice. When those signals concentrate in one local role, escalate PE and worker-classification review together.

Govern de facto authority, not just formal signatures#

PE risk rises when authority is centralized on paper but exercised locally in practice. If local teams effectively set terms, approve exceptions, or commit outcomes before headquarters signs, your operating reality may conflict with your formal model.

Keep evidence that shows where authority actually sits:

- Current signer matrix

- Approval and exception logs

- Customer communication samples

If the model moves into payroll or direct hiring, verify local tax IDs, registrations, and employer accounts before payroll starts.

Tie evidence to the tax position and model downside early#

Policy documents alone are not enough. Maintain a dated memo that links your facts to your tax position and local tax law assumptions, and attach supporting records such as roles, activity logs, approvals, work-location facts, and decision history.

Do not wait for authority inquiries to quantify impact. If PE is triggered, host-country corporate income tax and reporting duties may apply in addition to home-jurisdiction obligations. For large multinational groups, tax authorities may already have jurisdiction-level revenue, profit, and tax visibility through country-by-country reporting, so reactive modeling is a weak control point.

Conclusion#

PE risk is often most manageable when you run it as a control process: monitor triggers, apply clear escalation rules, and keep evidence that reflects what actually happened in-market.

PE is a tax question about whether your business is established enough in a country to be taxed there. If that threshold is met, the impact can move from policy concern to in-country corporate tax exposure, added compliance obligations, and potentially double taxation or heavier administrative burden. Waiting for perfect certainty can leave teams with weaker records and harder decisions later.

Execution discipline often matters more than intuition. Keep three controls active:

- a standing checklist of in-country facts

- a decision log of what changed, who reviewed it, and what was decided

- clear ownership across compliance, finance, and legal

Use that structure to test operating reality, not just policy intent. The same principle applies if you use an Employer of Record. It can support compliant hiring without a local entity, and localized contracts with explicit roles can be useful evidence, but it is not a blanket shield if in-country activity shifts.

A practical next step is to run this trigger map and checklist end to end in one priority market, then expand market by market. If gaps appear, fix the evidence first. If controls hold, repeat the process with the same rigor. That will not remove all uncertainty, but it gives you a defensible position you can explain, test, and update before risk compounds.

If your trigger map indicates probable PE exposure, align your control design to your rollout constraints by speaking with Gruv.

Frequently Asked Questions

What is permanent establishment risk for a platform in plain English?

Permanent establishment risk means another country may treat your platform as having a taxable presence because business activity is being carried out there. If that happens, the issue can move from an internal policy concern to local corporate tax and compliance obligations. The outcome depends on the local facts, treaty text, and local law.

Which activities most often trigger PE for cross-border platforms?

The two main patterns are a fixed place of business and dependent-agent activity. Risk rises when people in-country regularly carry out core business activity from a local place, or when they negotiate, finalize, or effectively control contracts or significant commercial decisions. Marketing-only or other auxiliary activity is not automatically PE, but the facts still need review.

Does hiring independent contractors avoid PE risk?

No. Contractor status alone does not remove PE risk because authorities look at what the person actually does in-country. If a contractor acts like a dependent agent, handles contract discussions, or looks employee-like in practice, PE risk can remain and worker-classification review may also be needed.

What are the first compliance and finance consequences if PE is triggered?

A common first finance consequence is potential local corporate income tax exposure on income generated in that jurisdiction. Early compliance consequences include local tax obligations and related documentation requirements. The downside can also include fines, audits, reputational damage, and possible double taxation exposure.

When should a platform escalate to specialist tax or legal review?

Escalate when local activity moves beyond remote support into real in-country authority or recurring commercial presence. High-signal facts include local contract-signing or negotiation authority, significant decision-making, a regular physical base, or mixed setups where representative-office activity sits alongside contract-concluding activity. If multiple material signals cluster in one market, move to formal tax and legal review.

How does an Employer of Record affect PE risk in practice?

An EOR can help with compliant in-country hiring, payroll, and HR administration, and it may reduce setup burden. It is not a blanket shield against PE because the analysis still turns on what people in-country actually do. If local personnel negotiate or sign contracts, manage clients, represent the business in-market, or work from a recurring local footprint, PE risk can remain.

What should a compliance team document each month to defend its PE position?

Document what changed in local activity, contract authority, and service-rendering footprint each month. Keep dated records showing who spoke with customers, who negotiated or approved terms, where work was performed, and whether a recurring local place was used. If the monthly pack shows drift toward local authority or revenue-linked in-country activity, route it to legal and finance in that same month.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: