Quick Answer

A German freelancer creates U.S. permanent establishment risk only when their work gives the business a meaningful U.S. footing, not simply because the client is in the United States. Risk rises when core billable work is repeatedly done from the same U.S. location, that location is practically available for business use, or a U.S.-based person habitually concludes binding contracts for the business.

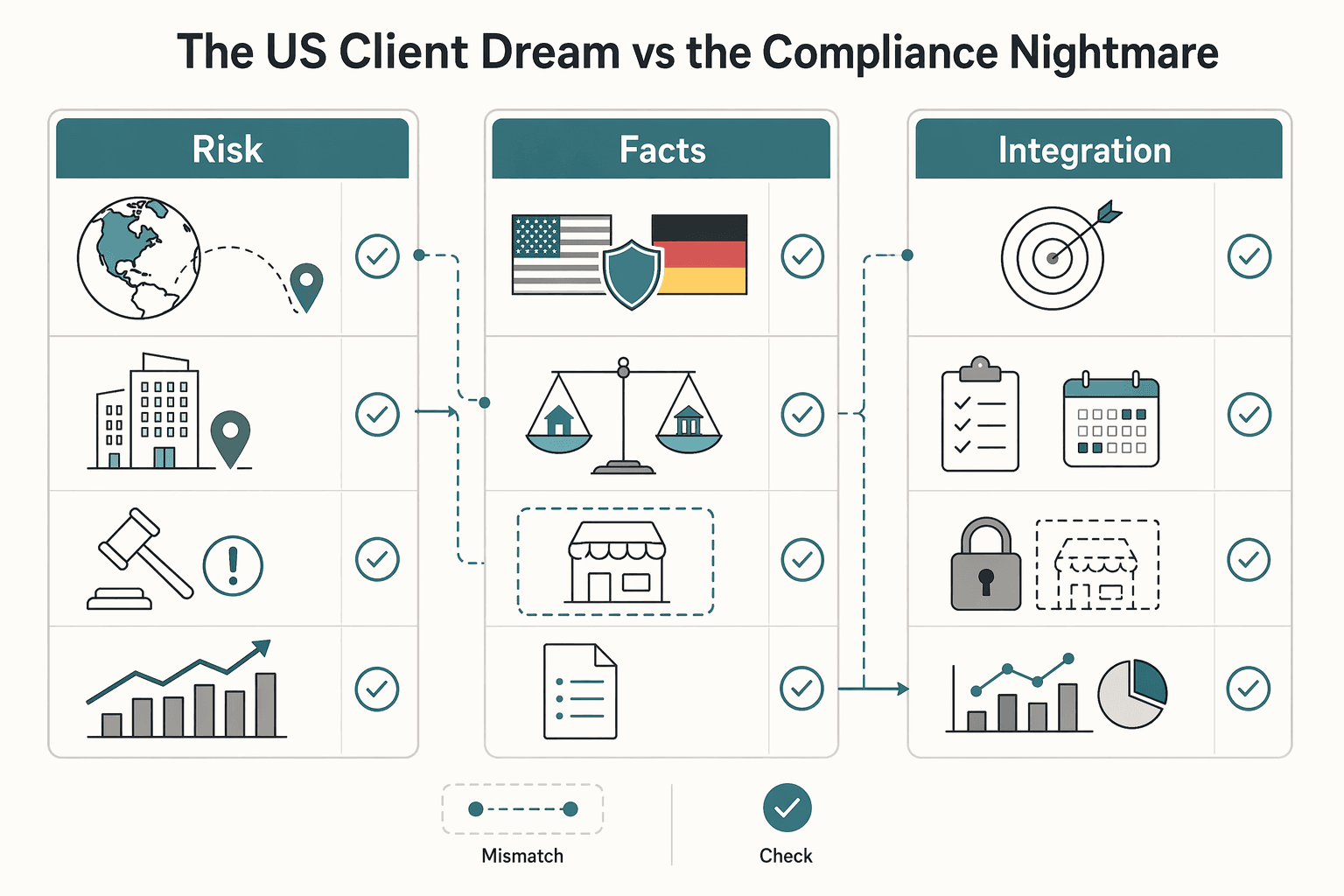

Introduction: The US Client Dream vs. The Compliance Nightmare#

A U.S. client can be a strong growth move for a German freelancer. The real decision is how to take that work without creating avoidable U.S. tax exposure.

In plain language, permanent establishment risk is the risk that your business is treated as having enough U.S. presence for the U.S. to tax profit tied to that presence. Under the U.S.-Germany treaty, business profits are generally taxed only in your home state unless you carry on business in the other state through a permanent establishment. The treaty explanation describes a permanent establishment as a fixed place of business through which business is wholly or partly carried on.

That means the practical test is broader than a simple day count. The IRS also looks at whether you are engaged in a U.S. trade or business. It notes that personal services performed in the U.S. are a common trigger, and says activities must be considerable, continuous, and regular. In practice, check where you work, what you do in the U.S., how often that pattern repeats, and whether you are effectively using a U.S. place as part of your business.

To make that practical, this guide uses a three-phase operating model:

- Diagnose: identify your current risk signals based on presence, activity pattern, and work location.

- Engineer: set contract and operating boundaries before they turn into tax facts.

- Monitor: track drift over time, especially repeated U.S. services and deeper client integration.

Use this as an educational decision framework, not legal or tax advice. The goal is to stay close to treaty and IRS concepts, show you where professional review is warranted, and help you avoid preventable compliance mistakes early. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide.

What is "Permanent Establishment" and Why Does It Matter?#

Permanent establishment is the threshold that can let the U.S. tax business profits attributable to U.S. activity, not just payments from a U.S. client. Under the U.S.-Germany treaty framework, business profits are generally protected unless your business is carried on through a U.S. permanent establishment. If that threshold is crossed, the U.S. can tax the profit attributable to it.

In practical terms, PE is about your business footing in the U.S., not just having a U.S. client. The core test is functional and fact-based: are you carrying on business through a fixed U.S. place, or through a U.S.-based person who habitually binds your business in contracts? Start with two direct tests:

- Fixed-place test: What control or practical access do you have to a U.S. location for doing your work?

- Dependent-agent test: Who can bind your business in the U.S., and is that authority exercised habitually?

| Risk area | Often lower-risk signal | Often elevated-risk signal |

|---|---|---|

| Work location | Work is mainly performed from Germany; U.S. visits are limited and meeting-focused | Core billable work is repeatedly performed from the same U.S. office, desk, or other location available to you |

| Continuity of presence | U.S. presence is occasional and not tied to an ongoing place used for delivery | Your U.S. pattern repeats in a way that may make the location function like part of normal operations |

| Contract-signing authority | U.S. contacts support or coordinate but do not bind your business | A U.S.-based person habitually concludes contracts that are binding on your business |

If your facts point toward PE, treat it as an operating process, not a vague tax warning. The immediate job is to map profit attribution, filing, disclosure, and evidence before the pattern gets harder to reconstruct:

- Determine which profits are attributable to the U.S. presence and document your method.

- Confirm the federal filing path for your legal form. If you operate through a foreign corporation, Form 1120-F may be part of the filing mechanics.

- Check whether a treaty-based position must be disclosed on the affected return.

- Build and maintain an evidence file showing where work was performed, who had contract authority, and what U.S. location was available for business use.

- Verify current form instructions, disclosure mechanics, and filing deadlines before submission.

A common mistake is waiting until the facts have already drifted. A regular client desk, recurring work from the same U.S. location, or a U.S. representative routinely finalizing agreements can change your risk profile over time.

Also keep PE separate from individual residency status. Residency rules classify your individual taxpayer status. PE asks whether your business has developed enough U.S. functional presence for the U.S. to tax attributable business profits.

You might also find this useful: Permanent Establishment Risk: A Guide for US Freelancers with a Single Large Client in Germany.

Phase 1: Diagnose Your PE Risk Profile#

Start by grading your facts, not just counting U.S. days. The key question is whether your working pattern makes it look like your business is carried on through a U.S. place or a U.S.-based person. Publication 901 supports that framing: for business profits, treaty protection turns on whether you have a U.S. PE, and for certain personal-services relief, the 183-day condition is paired with a separate fixed-base condition.

Physical presence#

Your risk is generally lower when U.S. time is occasional and auxiliary, and higher when core delivery repeats from the same U.S. location.

| Check | Meaning |

|---|---|

| Regularity | The pattern repeats |

| Permanence | More than a one-off visit, even if not indefinite |

| At your disposal | The place is practically available for your business use, not just borrowed for a meeting |

Pass if U.S. visits are irregular, temporary, and mainly for meetings or other preparatory or auxiliary activity, while core delivery happens from Germany. Warn if the same U.S. city, office, or client site appears repeatedly and you do meaningful production work there. Escalate if a U.S. location starts functioning like a normal place you work from and is practically available when the project is active.

Use those three checks together. They help you decide whether a place is shifting from a temporary stop into part of normal operations, but they are not bright-line legal tests.

Run a 12-month evidence check across travel logs, calendars, and invoices. If those records tell different stories, fix the drift now.

Client integration#

Treat client integration as an early warning signal. PE analysis is treaty-based, but the more embedded you look, the harder it is to defend a clearly external role. No single indicator below determines PE on its own.

| Signal | Why risk can rise |

|---|---|

| Client-domain email address | It can blur your separate business identity |

| Client-issued laptop, phone, or essential tools | Tool control is one practical independence signal in IRS guidance |

| Persistent badge access or unrestricted office entry | It can support a regularly available U.S. place narrative |

| Presence in org charts, staff directories, or team pages | It can frame you as internal, not external |

| Role titles like interim lead or acting director | It can suggest internal operational responsibility rather than standalone external delivery |

Read these as cumulative signals, not standalone answers. Pass if you mostly use your own identity, tools, and channels, are presented as an external provider, and other risk signals stay limited. Warn if one or two embedded signals exist for convenience but separation is still clear. Escalate if several embedded signals exist at once, especially with on-site core work.

Authority#

This test is narrower than people think. Support in negotiations is not the same as authority to bind your business. Repeated U.S.-based contract closing is a different fact pattern.

Pass if approvals and signatures for contracts, SOWs, renewals, and change orders stay with you in Germany. Warn if U.S. contacts help negotiate terms, but nothing binds until you approve or sign from Germany. Escalate if a U.S.-based person habitually finalizes agreements or signs binding documents for your business.

Documentation matters here. The paper trail should show who approved, who signed, and where that authority was exercised:

- Keep version history, approval emails, signature logs, and executed copies.

- If you use e-sign tools, retain audit trails.

- Keep an internal authority rule showing who can bind the business, and make sure real behavior matches it.

Simply calling someone "independent" does not help if their actual role is dependent and binding.

Revenue concentration#

Revenue concentration is not a treaty PE test by itself, but it can make the rest of your fact pattern harder to defend when presence, integration, or authority signals are already trending up.

Pass if U.S. revenue is diversified and no single client anchors your operating model. Warn if one U.S. client is becoming central to your calendar and delivery pattern. Escalate if one U.S. client effectively anchors the business and that concentration is paired with on-site work or deep integration.

| Risk factor | Lower-risk pattern | Watch closely | Escalate now |

|---|---|---|---|

| Physical presence | Irregular, temporary U.S. visits; mostly meetings or auxiliary activity | Repeating trips tied to delivery work at the same location | A U.S. place functions like part of normal operations |

| Client integration | Own tools and identity; clearly external role | Mixed signals, such as limited internal access or some client tools | Multiple embedded signals plus a visible internal role |

| Authority | Approval and signature stay in Germany | U.S. negotiation support without binding authority | A U.S.-based person habitually concludes binding contracts |

| Revenue concentration | Diversified client base | One U.S. client becoming central | One U.S. client anchors the business, especially with U.S. presence or integration |

If you plan to claim a treaty-based reduction on your return, check whether Form 8833 disclosure applies.

If your profile is mostly low-risk, maintain separation and keep records current. If it is medium-risk, fortify now before patterns harden. If it is high-risk, get cross-border tax advice before expanding U.S. activity. Related: How to Create a Financial Safety Net as a Freelancer.

Phase 2: Engineer Your "Compliance Moat"#

If Phase 1 showed yellow or red, lock the boundary now. Your best protection is a consistent story across contract terms, daily behavior, and legal structure. Treaty treatment for business profits is article-specific and often turns on whether you have a U.S. PE, and IRS guidance is clear that labels alone do not control if the facts point the other way.

Lock down the MSA and SOW stack#

Start with the documents that govern the real work: your MSA, each SOW, and every change order. Keep the paper close to the delivery model you are trying to preserve: core services are performed from Germany, U.S. presence is temporary and limited, and no one in the U.S. habitually concludes binding contracts for your business.

| Clause area | What to state |

|---|---|

| Independent contractor status | Confirm that you control how work is done, use your own methods, and carry your own business risk |

| Place of performance in Germany | State that services are primarily performed from your German business location |

| Limited purpose of U.S. travel | Define U.S. trips as temporary and tied to meetings, workshops, onboarding, or other preparatory or auxiliary activity |

| No contract-concluding authority in the U.S. | State that neither you nor any U.S.-based person for your business habitually concludes binding contracts while in the U.S. |

| Counsel validation | Have cross-border counsel validate the wording before signature |

Then preserve proof that the clauses match reality: executed agreements, version history, approval emails, signature logs, and e-sign audit trails. If treaty-based withholding treatment is requested, keep onboarding documentation aligned with the payee. For an individual, that is typically Form W-8BEN. If you later use a German entity, update the withholding documentation accordingly.

Make operations prove what the contract says#

Contract language helps only when your day-to-day behavior matches it. Convenience drift is the usual failure mode: client email, client devices, persistent access, office routine, and reimbursement patterns can make you look internal.

Set operational controls so they double as proof. Each one should leave a record you can point to later:

- Use your own business identity, including your domain, signature block, and external role framing.

- Use your own equipment and core software accounts where practical.

- Invoice from your German business address with clear service periods and scope.

- Keep travel temporary. Use client sites for defined collaboration, not as a recurring production base.

- Keep internal and client communication consistent with vendor status.

Run a monthly consistency check across travel logs, calendars, badge or access records, and invoices so they all tell the same story.

| Contract says | Behavior must match |

|---|---|

| Services primarily performed in Germany | Delivery pattern and records show Germany as the normal base |

| U.S. travel is temporary and limited purpose | Trips are agenda-based and not recurring on-site delivery cycles |

| Independent contractor using own methods and tools | You consistently use your own identity, tooling, and process |

| No authority to bind business from the U.S. | Binding approvals, renewals, and signatures stay outside the U.S. |

Use structure as a decision gate, not a trophy#

If you operate as a sole proprietor, ask whether risk now depends too heavily on your personal presence. If repeated U.S. travel and deeper client integration are increasing, discuss with cross-border counsel whether using a German entity for contracting would improve legal separation.

But structure does not cure bad facts. Entity separation helps only when contracts, invoicing, authority, and day-to-day conduct all run through that entity consistently. Align payer onboarding, bank account, invoices, and W-8 documentation with the income-earning party.

Run this check before accepting expanded U.S. scope#

Before you accept expanded scope, confirm the points that usually drift first:

- Core performance in the MSA or SOW still sits in Germany.

- U.S. trips remain temporary and clearly defined.

- Your identity, tools, and billing posture stay independent.

- Binding authority remains outside the U.S.

- Calendars, travel records, and invoices still support the same operating story.

- You have re-checked current treaty text and applicable protocols for the relevant tax year.

Escalate to a cross-border tax advisor before signing if any answer is no, or if the scope change creates a repeating U.S. work location, deeper client integration, or a U.S.-based person who habitually finalizes binding terms for your business. If worker-status classification is unclear, escalate that question early (including Form SS-8 where appropriate).

For a step-by-step walkthrough, see A Freelancer's Guide to the US-Germany Tax Treaty.

Before you finalize new client terms, run your clauses through this freelance contract generator and align language with your PE guardrails.

Phase 3: Monitor Your Key Risk Indicators#

You need a simple review rhythm to catch PE drift early, not extra admin. The point is to spot when daily facts start moving away from your documented boundary before they begin to look like a U.S. fixed place of business or a habitual contract-authority pattern.

Patterns matter more than isolated events. One unusual trip on its own may not resolve the analysis. Repeated facts are what change the risk picture. Review what changed, reset quickly where needed, and escalate when the pattern keeps building.

For each review, check your facts against the IRS treaty materials for Germany, including the treaty, technical explanation, protocol, and protocol-related explanation. Treaty tables are useful as a quick index, but the real test is the treaty text against your records.

| KRI | What to track | Risk signal | Safe-default response | When to get professional advice |

|---|---|---|---|---|

| Physical-presence pattern | U.S. trip timing, purpose, site access, calendars, and where delivery work happens | U.S. presence becomes recurring and delivery-heavy, or a U.S. location starts looking continuously available | Reset travel to temporary collaboration windows, move core delivery back to Germany, and update SOW language if scope changed | A client site is functioning like a regular work location, or your position relies on having no U.S. office or fixed base |

| Work-scope drift | Current tasks vs. MSA or SOW, decision rights, and who concludes binding terms | Work shifts from preparatory or auxiliary activity into core operating execution, or contract-concluding authority is habitually exercised in the U.S. | Rewrite scope, pull U.S.-based contract-closing activity back, and document who has authority to conclude contracts and where it is exercised | Your role now looks operational or managerial in practice, or authority patterns conflict with treaty assumptions |

| Economic dependence | Revenue concentration, renewal rhythm, exclusivity, and day-to-day operating independence | One U.S. client dominates while your operating posture looks less independent | Reduce integration signals and rebalance client mix where feasible | Dependence is paired with repeated U.S. presence or embedded client-side working patterns |

| Public representation consistency | Contracts, proposals, profiles, and other role descriptions | Your role is presented as internal client leadership or as holding U.S. contract-closing authority | Correct inconsistent wording promptly and keep dated evidence of corrections | Your documented role and operating facts keep conflicting with your treaty-position assumptions |

Use the table as your quick scan. Then translate each indicator into a practical reset or escalation decision.

Physical-presence pattern#

Track this as your repeat-use footprint in the U.S. The question is straightforward: are trips still temporary and limited, or is U.S. presence becoming a normal delivery base? If the pattern is shifting toward recurring on-site production, treat that as a reset trigger right away.

Work-scope drift#

Track the gap between signed scope and actual work. Ask whether your current work still fits preparatory or auxiliary positioning, or whether it has moved into core execution with habitual U.S. contract authority. If it has drifted, update the documents and escalate before the new pattern hardens.

Economic dependence#

Track how much your practical independence rests on one client relationship. Ask whether concentration plus operating behavior now makes you look less independent in the ordinary course. If yes, reduce embedded behaviors and rebalance exposure where you can.

Public representation consistency#

Check whether your role descriptions match your legal and operational posture. Ask whether your materials and contracts describe a position that is consistent with your treaty assumptions. If not, correct it quickly and preserve the corrected record.

If one or more indicators stay yellow after a reset, move to professional tax or legal review on the facts and treaty application. If interpretation or application is disputed, ask counsel whether escalation through treaty procedures (including MAP under Article 25) is needed. The FAQ covers the tactical questions that usually come next.

We covered this in detail in Home Office Permanent Establishment Risk for Consultants in 2026.

From Anxiety to Advantage: Take Control of Your Global Career#

PE risk is manageable when your travel pattern, signing authority, contract terms, and records all line up. Problems usually start when one of those moves ahead of the others.

That is the point of Diagnose, Engineer, and Monitor. First, diagnose whether your U.S. activity looks like a fixed place of business or a dependent-agent pattern. Then engineer contract and operating boundaries. After that, monitor whether real delivery still matches the paper. For a German resident, Article 7 is the core protection for business profits when income is not attributable to a U.S. permanent establishment, but that protection depends on the facts.

Before you expand scope, run this decision lens first. These questions can help show whether your setup is starting to drift:

- Are U.S. trips becoming frequent enough to change your operating pattern?

- Is the same U.S. workspace repeatedly available to you?

- Has your role shifted from temporary coordination into recurring on-site delivery?

- Are you, or someone acting for you, negotiating or concluding binding terms in the United States?

If any answer is "yes," pause and review before you accept the new setup. One risk pattern is clean contract language that says Germany is primary, while calendars, access records, coworking logs, or message trails show recurring U.S. execution.

These boundaries also help on the client side: clear independent-contractor positioning, predictable scope-change reviews, and written decisions on travel and signing authority. If you take a treaty-based return position that reduces U.S. tax, Form 8833 is generally the disclosure mechanism, and missing required treaty-based reporting can trigger penalties.

Your next operating cycle can stay simple:

- Recheck travel logs, U.S. location use, and the purpose of each trip.

- Confirm who negotiated final terms and who actually signed.

- Compare the contract, SOW, invoices, profile, and email signature against how the work was actually delivered.

- Save evidence now: calendars, tickets, access records, contracts, and key message threads.

- Engage a cross-border advisor when risk signals conflict or facts are incomplete, and review the treaty MAP article before requesting competent-authority assistance.

This also pairs well with our guide on How a German Freelancer Can Handle US Sales Tax with a US LLC.

If you want a cleaner audit trail for travel and presence patterns, keep one source of truth with the tax residency tracker.

Frequently Asked Questions

How long can you work in the U.S. before creating PE?

There is no reliable day-count shortcut. PE risk depends on fixed-place and dependent-agent facts, and U.S. trade-or-business analysis is also qualitative rather than a single threshold. Build a timeline with dates, locations, purpose, and the work actually performed.

Does working from a U.S. home office, client site, or coworking space create risk?

It can, but not automatically. Risk rises when the same U.S. location is effectively available and used as a place your business is carried on. Risk is generally lower when the use is short and limited to preparatory or auxiliary activity.

What is the difference between a dependent and independent agent?

The key issue is authority to conclude contracts that bind your business. A dependent-agent pattern exists when someone in the U.S. habitually exercises that authority for you, while an independent agent acts in the ordinary course of their own business. If the line is unclear, check who set the final terms, who signed, and where that authority was exercised.

How should you structure the client contract and operating reality?

The contract should match the way the work is actually done. State independent-contractor status, a primary place of performance outside the U.S., temporary or auxiliary U.S. travel, and no U.S. contract-binding authority on your behalf. Avoid terms or behavior that create an ongoing U.S. work location, embedded operational control, or a U.S.-based contracting pattern.

What should you do first if your risk no longer looks low?

Start with calm triage and get treaty-specific specialist review quickly. For independent personal services, start from the 30% withholding default and confirm whether treaty relief applies to your exact facts. Gather contracts, SOWs, travel logs, calendars, invoices, access records, profiles, and message trails, then build a dated timeline of U.S. presence, workspace use, and contract activity. Do not assume one treaty article, one day count, or one form resolves everything.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

How to Create a Financial Safety Net as a Freelancer

Your **freelance financial safety net** is more than a savings balance. It is the set of controls that lets you cover fixed obligations on time when receipts are uneven, and it keeps invoiced revenue separate from cash you can actually spend. The goal is not to predict every slow month. The goal is to reduce the chance that one late client payment turns into missed bills, tax pressure, or borrowing.

Permanent Establishment Risk for US Freelancers With One Large German Client

Your client’s concern can be straightforward: the contract says one thing, but the day-to-day record may start showing another. In permanent establishment risk germany, that mismatch can make a file harder to assess quickly and escalate for advice.