Quick Answer

A payment fee comparison tool should compare total cost and operational fit, not just headline processing rates. For a defensible comparison, normalize volume, average ticket, payment-method mix, geography, and market scope, then preserve dated pricing artifacts. Stripe and PayPal are modelable from public pricing, while key pricing and operational fields for Gruv and Adyen are not established in the cited evidence.

Compare Fees and Operational Fit#

If you run platform finance or payments ops, headline rates are only the first input. The choice that holds up is the one you can still defend when volume grows, payment mix shifts, and month-end close gets more complex.

| Provider | Payment type | Published figure |

|---|---|---|

| Stripe | Successful domestic card transactions | 2.9% + 30¢ |

| Stripe | Manually entered cards | +0.5% |

| Stripe | International cards | +1.5% |

| Stripe | Currency conversion | +1% |

| Stripe | ACH Direct Debit | 0.8% with a $5.00 cap |

| PayPal | Card processing | 2.89% + $0.29 |

| PayPal | PayPal and Venmo | 3.49% + $0.49 |

| PayPal | Pay Later | 4.99% + $0.49 |

| PayPal | Tap to Pay and POS | 2.29% + $0.09 |

This comparison looks at Stripe, PayPal, Gruv, and Adyen across two layers: visible processing fees and the operational cost that shows up later in reconciliation, exceptions, and audit support. A lower posted rate can still end up being more expensive if money movement is hard to trace.

Public pricing shows why context matters. Stripe's standard pricing says there are no setup, monthly, or hidden fees, and lists 2.9% + 30¢ for domestic cards. It also shows uplifts of +0.5% for manually entered cards, +1.5% for international cards, and +1% for currency conversion, plus 0.8% ACH Direct Debit with a $5.00 cap. PayPal's US business pricing page shows starting points such as 2.89% + $0.29 for card processing, 3.49% + $0.49 for PayPal and Venmo, 4.99% + $0.49 for Pay Later, and 2.29% + $0.09 for Tap to Pay and POS. These are useful starting assumptions, not universal outcomes.

What you should compare beyond rates#

Treat processing fees as one line item, not the whole model. When you review Stripe, PayPal, Gruv, and Adyen, pressure-test three things:

- How cleanly transactions map to settlements and payouts

- How clearly your team can explain exceptions and retries

- What evidence behind your assumptions you can preserve for finance, procurement, and engineering review

Use documented assumptions, not memory. PayPal's US business fees page shows Last Updated: February 9, 2026, and the US consumer fees page shows Last Updated: February 19, 2026. PayPal also provides a downloadable printable PDF and directs users to its Policy Updates page for fee and rate changes. Stripe separates standard pricing from custom packages for large-volume or unusual business models, so enterprise terms may differ from public pages. Market coverage, contract terms, and custom enterprise packages can vary.

Do not assume US public rates apply globally. PayPal scopes published rates to residents of the listed market or region, defines domestic versus international by whether parties are in the same or different markets, and notes regional exceptions. For example, some international EUR/SEK EEA transactions on PayPal Iceland are treated as domestic for fee application. Also, even when certain PayPal fees are waived, exchange-rate fees from a customer's card issuer or bank may still apply.

Use public rates as baseline assumptions, then validate operational fit before you recommend a provider.

Stripe vs PayPal vs Gruv vs Adyen at a glance#

Use this as a screening table, not a winner table. Stripe and PayPal can be modeled from public pricing artifacts. Key operational fields for Gruv and Adyen are still unknown in the evidence used here.

| Criterion | Stripe | PayPal | Gruv | Adyen |

|---|---|---|---|---|

| Fee model clarity | Standard pricing is explicit, with no setup, monthly, or hidden fees, but final economics may change under custom or IC+ terms. | Fee pages are detailed and market-scoped rather than one universal rate card. | Not established here. | Not established here. |

| Payment-method coverage | Public pricing explicitly includes domestic cards and ACH Direct Debit. Broader method mix still needs confirmation. | Public fee pages include dispute and chargeback fee categories. | Not established here. | Not established here. |

| Visa | Brand-specific treatment is not broken out in the cited Stripe pricing excerpt. Confirm in contract review. | Brand-specific treatment is not established in the cited PayPal pages used here. Confirm by product and contract. | Not established here. | Not established here. |

| Mastercard | Brand-specific treatment is not broken out in the cited Stripe pricing excerpt. Confirm in contract review. | Brand-specific treatment is not established in the cited PayPal pages used here. Confirm by product and contract. | Not established here. | Not established here. |

| American Express | Brand-specific treatment is not broken out in the cited Stripe pricing excerpt. Confirm in contract review. | Brand-specific treatment is not established in the cited PayPal pages used here. Confirm by product and contract. | Not established here. | Not established here. |

| ACH bank transfer | Explicit: 0.8% ACH Direct Debit with a $5.00 cap. | Not established in the cited excerpts for this section. | Not established here. | Not established here. |

| Card-not-present flows | Baseline is 2.9% + 30¢ for successful domestic card transactions, with +0.5% manually entered, +1.5% international, and +1% currency conversion. | Business fee-page pricing exists, but treatment depends on market scope and selected fee page. | Not established here. | Not established here. |

| Settlement visibility | Not established from pricing alone. Request payout and settlement examples before scoring. | Not established from fee pages alone. Request payout and settlement examples before scoring. | Not established here. | Not established here. |

| Reconciliation effort | Not established from pricing alone. Require sample exports and statement mapping. | Not established from fee pages alone. Require sample exports and statement mapping. | Not established here. | Not established here. |

| Exception handling | Not established in the cited Stripe pricing excerpt for this section. | Fee pages explicitly list both dispute fees and chargeback fees. | Not established here. | Not established here. |

| Audit trail quality | Not established from the cited pricing page alone. | Not established from the cited fee pages alone. | Not established here. | Not established here. |

| Unknowns to clear with sales or contract review | Standard versus custom versus IC+ path, geography-driven uplifts, and reporting artifacts for finance. | Exact market page, product mix, contract terms, and month-end export and statement support. | Pricing model, supported rails, settlement reporting, exception surfaces, and audit evidence require confirmation. | Pricing model, supported rails, settlement reporting, exception surfaces, and audit evidence require confirmation. |

| Quick-read verdict | Strong public baseline for first-pass modeling. Pricing evidence alone does not support an overall winner. | Strong fee-documentation trail for assumptions. This evidence alone does not support an overall winner. | No public verdict is supported from the current evidence. | No public verdict is supported from the current evidence. |

Where the table is already useful#

The table is most useful as a screen for modelability, not as a price ranking. It shows which providers give you enough public structure to build a defensible first-pass model now.

Stripe gives you a clear baseline plus explicit add-ons of 0.5%, 1.5%, and 1%, along with ACH Direct Debit at 0.8% with a $5.00 cap. PayPal gives you a different kind of confidence signal: market-scoped fee pages, dated updates, and downloadable fee artifacts, including a printable PDF. Preserve the exact page, date, and scope behind every assumption.

What not to fake precision on#

Do not treat Stripe's 2.9% + 30¢ as universal when it is scoped to successful domestic card transactions and has listed uplifts. Do not reuse a PayPal figure across markets when published rates are tied to the listed resident market or region.

Keep settlement visibility, reconciliation effort, and audit trail quality unrated until each provider supplies traceable reporting artifacts for finance review. At this stage, the disciplined move is simple: model what is public, log what is unknown, and make contract confirmation part of the comparison.

Related: How to Use Wise to Pay International Invoices with a US Credit Card.

Normalize inputs before you compare anything#

Do not compare providers until your input sheet is normalized. If one provider is modeled on US online card volume and another on mixed cross-border checkout assumptions, the result can look precise without being comparable.

Lock the same fields for every provider: monthly volume, average ticket, payment mix, geography split, and whether you are modeling public standard pricing or a custom contract path.

Keep method-level assumptions separate. Do not blend online card and ACH bank transfer into one average rate, because the fee mechanics are different enough to distort effective cost. Stripe's published structure shows why: 2.9% + 30¢ for domestic cards, +1.5% for international cards, +1% for currency conversion, and 0.8% ACH Direct Debit with a $5.00 cap.

| Input bucket | Keep separate | Why it matters |

|---|---|---|

| Online card | Domestic versus international, and currency conversion exposure | A base card rate alone can understate cost when uplifts apply |

| ACH bank transfer | ACH volume and average ticket | 0.8% with a $5.00 cap behaves differently than card pricing |

| PayPal checkout path | Exact product path in your flow | PayPal shows different published rates across checkout paths and products |

| Geography split | Market page used and domestic versus international treatment | PayPal pages are market-scoped, and some markets are grouped for international calculations |

Use one checkpoint for every assumption row: one source URL, one market scope, and one as-of date. PayPal pages are explicitly timestamped. For example, the US consumer fees page says "Last Updated: February 19, 2026" and the US business fees page says "Last Updated: February 9, 2026." The business fee page also offers a printable PDF snapshot.

If a field is unknown, leave it unknown. Do not back-solve blended rates from statements, and do not infer missing Gruv or Adyen pricing inputs without a confirmed pricing artifact.

Price components that move total cost the most#

Once your inputs are locked, isolate the fee buckets that actually move total cost. The number worth optimizing is your effective rate after each bucket is applied to your real payment-method mix, geography mix, and checkout path.

| Cost bucket | Usually obvious up front | What makes it move | What to verify |

|---|---|---|---|

| Percentage fee | Yes | Card type, channel, and whether pricing is flat-rate or interchange-plus | Exact product path, market, and card-not-present versus other flow |

| Fixed per-transaction fee | Yes | Average ticket and count of successful transactions | Ticket assumptions and whether the model is based on successful payments |

| Plan or platform fee | Sometimes | Plan tier, add-ons, implementation, training, and overages | Contract exhibit, order form, or plan page with as-of date |

| Cross-border uplift and FX | Often partly hidden | International card share and currency conversion exposure | Domestic versus international split and where conversion happens |

| Implementation and scaling costs | Often partly hidden | Integration work, training time, and scaling needs | A standardized comparison artifact that captures costs that show up during implementation |

Stripe is a good example of why this bucket view matters. Standard pricing is pay-as-you-go with no setup or monthly fees, and the visible domestic-card headline is 2.9% + 30¢. But total cost moves with mix: +0.5% for manually entered cards, +1.5% for international cards, +1% when currency conversion is required, and ACH Direct Debit priced at 0.8% with a $5.00 cap.

Headline rate vs effective-rate drift#

A blended headline rate hides the movement that actually matters. More international cards raise cost. Lower average ticket makes the fixed fee matter more. A shift from cards to ACH can materially change economics because capped ACH pricing behaves differently from card pricing.

Fee outcomes vary by transaction context, so a single headline rate is usually not enough for modeling. Keep card type, channel, and successful-transaction assumptions explicit in your comparison.

Why "flat rate" calculators can mislead#

Quick calculators are useful for screening, but they are still assumption-driven. Flat-rate views can hide variability because interchange, assessment, and processor markup are bundled into one number. Interchange-plus can make markup more explicit, but it also passes variable interchange through to the merchant.

Use those tools as a first pass, not as the decision record. If your method mix changes month to month, prioritize fee granularity over one blended rate. Keep one source artifact, one market scope, and one as-of date for every bucket in your model.

Score operational cost, not just processing fees#

After the fee math, operational handling can materially change total cost. Do not let the lowest processing line win by default if reconciliation and close are already painful. For teams under month-end pressure, clearer audit trails and status reporting can be worth a slightly higher nominal fee.

Use an ops scorecard before you pick a winner#

A pricing model can look clean while downstream handling is expensive. The real test is whether your team can reconcile settlements, explain payout movement, and clear exceptions without side spreadsheets. A useful scoring lens is how well the option holds up across policies, internal controls, risk assessment, management reporting, and audit.

| Ops criterion | What strong looks like | What weak looks like | What to verify |

|---|---|---|---|

| Reconciliation complexity | Few joins, stable reference keys, export fields map cleanly to your ledger | Manual matching, changing reference formats, frequent off-platform notes | Sample export and one worked reconciliation example |

| Settlement traceability | You can follow a transaction from request to settlement event to bank movement | Settlements are aggregated with no drillback path | Whether settlement IDs, payment IDs, and timestamps are preserved end to end |

| Payout status clarity | Distinct states with timestamps for initiated, pending, paid, failed, returned | One generic status that hides where the payout stopped | Status definitions and a sample failed payout record |

| Cost monitoring signals | You can spot trends in transactions and interchange, including mix shifts | Mix and interchange trends are only visible after close | Access to trend views by transaction type and geography mix |

| Exception handling visibility | A predictable, reviewable queue with reasons and owners | Exceptions discovered only during close or via bank mismatch | Expected mismatch types and how they are surfaced |

Fee tools can estimate processing cost, but they may not capture all analyst time spent on unmatched deposits or status mismatches between systems. In card flows, interchange is scheme-set and non-negotiable, so optimization usually comes from mix, markup visibility, and operating controls.

Check ledger integrity from request to export#

Ask one core question: can you trace a payment from request, to internal ledger entry, to export, to the bank line where cash moved? If that chain depends on manual naming conventions, you are already carrying operational cost even if fees look lower.

This check matters even more when your workflow spans multiple payment methods and payout cycles. You want IDs and references to stay linked through ingestion, posting, export, and investigation so cash and liability views stay aligned.

Request the same evidence pack from each option before approval:

- One sample payment event record

- One settlement or payout export file

- One failed or reversed transaction example

- One field dictionary for IDs, statuses, and timestamps

If exports cannot map back to originating events and ledger entries, treat that as operational risk, not a documentation issue.

Score failure handling, not just happy paths#

A lot of hidden work shows up in failure paths. Score each option on three things: exception visibility, unmatched-deposit investigation, and trend monitoring.

For unmatched deposits, require a documented investigation path that starts from bank reference, amount, and date, then maps back to settlement or payout identifiers and the underlying transactions. For trend monitoring, make sure your team can track transaction mix and interchange over time so cost shifts are visible early.

Also test by payment method, not only by provider. Transaction and settlement behavior varies by product, and cost and risk patterns differ across card-present, card-not-present, domestic card, cross-border card, and bank-transfer flows.

If close is already a bottleneck, prioritize cleaner exports, preserved IDs, and structured statuses even when another quote is slightly cheaper on headline fees. Small fee deltas are visible early, while reconciliation overhead can build over time.

For a step-by-step walkthrough, see How to Show Fee Transparency to Contractors: Building a Clear Payment Breakdown UI.

Compliance and tax checks that can block go-live#

A lower-fee option is not enough for go-live if compliance and tax ownership are unclear. Treat this as a launch gate: define owners, decision points, and evidence retention before engineering marks the build complete.

Turn compliance into a launch gate, not a later ticket#

Provider-specific KYC, KYB, AML, market-approval, or W-8/W-9/1099 requirements are not established here. Keep those items as internal policy decisions and separate them from FBAR obligations that are supported below.

| Control area | Gate question before launch | Evidence to request | Typical block at go-live |

|---|---|---|---|

| KYC | Not established here. | Internal policy owner and approval record (outside this pack). | Confirm with the relevant authority. |

| KYB | Not established here. | Internal policy owner and approval record (outside this pack). | Confirm with the relevant authority. |

| AML | Not established here. | Internal policy owner and approval record (outside this pack). | Confirm with the relevant authority. |

| Market-level policy gates | Not established here. | Internal policy owner and launch approvals (outside this pack). | Confirm with the relevant authority. |

| Tax document workflow | W-8, W-9, and Form 1099 rules are not established here. | Internal tax workflow owner and controls (outside this pack). | Confirm with the relevant authority. |

| Foreign-account reporting | Does a U.S. person have qualifying authority or interest over foreign accounts, and do aggregate maximum values exceed $10,000 during the calendar year? | Account inventory, maximum-value method, filing owner, receipt archive. | No year-round tracking of account maxima or filing ownership. |

Treat FBAR as an operations requirement when foreign accounts are in play#

If foreign accounts are in scope, FBAR is specific enough to operationalize. A U.S. person (including U.S. citizens or residents and domestic legal entities) may need to file when they have qualifying authority or interest over foreign financial accounts and aggregate maximum account values exceed $10,000 during the calendar year. File electronically through FinCEN's BSA E-Filing System, not with a federal tax return.

| FBAR item | Requirement | Qualifier |

|---|---|---|

| Filing trigger | Qualifying authority or interest over foreign financial accounts and aggregate maximum account values exceed $10,000 during the calendar year | Applies to a U.S. person, including U.S. citizens or residents and domestic legal entities |

| Filing method | File electronically through FinCEN's BSA E-Filing System | Not with a federal tax return |

| Maximum account value | Document each maximum account value as a reasonable approximation of the greatest value during the year | Record the exchange-rate source when Treasury's rate is unavailable and another verifiable rate is used |

| Due date | April 15 | Automatic extension to October 15 |

| Jointly owned accounts | Each person reports the full account value | For jointly owned foreign accounts |

| Item 15a | Can be marked as 'amount unknown' | For filers with fewer than 25 accounts who cannot determine whether totals exceeded the threshold |

| XML submissions | Submissions can be rejected when required elements are missing | Confirm who validates required fields and who monitors rejection notices |

Track this throughout the year: maintain an account inventory, document each maximum account value as a reasonable approximation of the greatest value during the year, and record the exchange-rate source when Treasury's rate is unavailable and another verifiable rate is used. The due date is April 15, with an automatic extension to October 15.

Two filing details matter operationally. For jointly owned foreign accounts, each person reports the full account value. For filers with fewer than 25 accounts who cannot determine whether totals exceeded the threshold, item 15a can be marked as "amount unknown."

FinCEN XML guidance indicates submissions can be rejected when required elements are missing, so confirm who validates required fields and who monitors rejection notices.

Do not assume MoR or VAT validation solves ownership gaps#

MoR-versus-DIY outcomes or VAT-validation requirements are not established here. Do not treat this section as evidence that either model reduces compliance work by default.

Use a narrower internal test instead: who collects data, who validates it, who handles exceptions, and who retains evidence by market. Related reading: How to Calculate Payment Processing Fees: A Total Cost of Ownership Framework for Platforms.

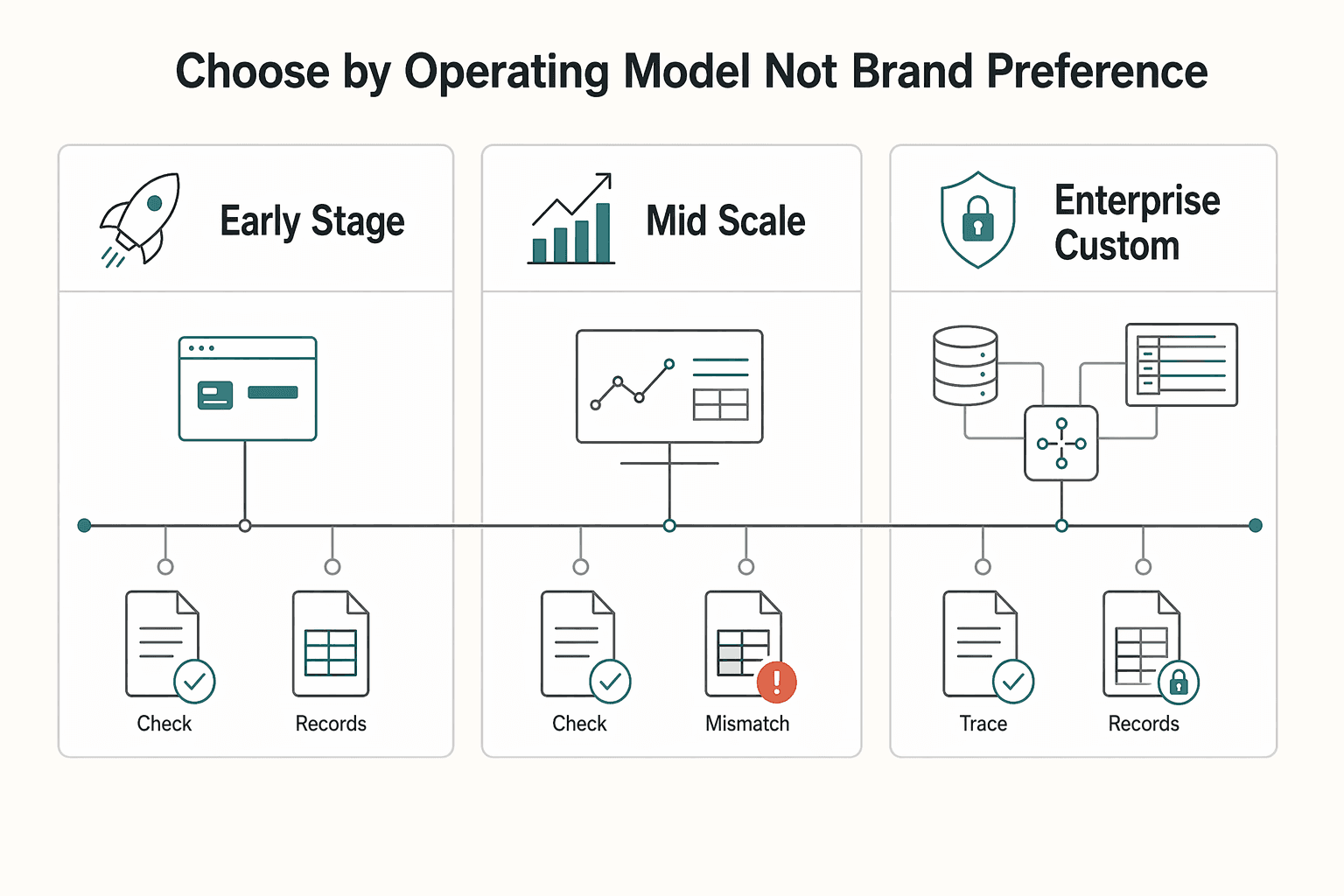

Choose by operating model, not brand preference#

Choose for your highest operating risk, not the brand your team already knows. If your top risk is a fast go-live for standard card acceptance, a checkout-first path is usually the better first step. If your top risk is payout control, reconciled ledgers, and audit evidence, prioritize setups with stronger lifecycle visibility.

| Scenario | Primary decision lens | Practical fit at a glance | Key checkpoint before commit |

|---|---|---|---|

| Early-stage marketplace | Speed to launch standard card acceptance with low upfront engineering overhead | Stripe or PayPal (flow-mix dependent) | Model costs by payment flow and transaction traits, not one headline rate |

| Mid-scale platform with global payouts | Payout lifecycle visibility, reconciliation, exception handling, audit-ready records | Gruv or a deeply integrated enterprise setup, validated directly | Verify concrete payout, ledger, and audit artifacts in product and contract review |

| Enterprise with custom contracting | Negotiated commercial terms, multi-region operating control, explicit ownership | Stripe custom-commercial lane, and assess Adyen explicitly | Document routing, settlement mapping, and contract-change ownership up front |

Early-stage speed and launch-first modeling#

For standard card acceptance, Stripe gives the clearest speed and packaging signal in the material used here: no setup fees or monthly fees, plus prebuilt UI support. Its listed baseline is 2.9% + 30¢ for domestic cards, with 0.5% for manually entered cards, 1.5% for international cards, and 1% when currency conversion is required. If your mix changes, effective cost changes with it.

PayPal can also fit a speed-first launch, but only if the flow mix is explicit. The US business page shows different tracks. Card processing is 2.89% + $0.29, PayPal and Venmo are 3.49% + $0.49, Pay Later is 4.99% + $0.49, and POS starts at 2.29% + $0.09. A single PayPal assumption usually hides real variance.

Mid-scale payout operations with a bias toward control surfaces#

When payouts become core, control quality can matter more than checkout convenience. At that stage, Gruv or a deeply integrated setup can be a fit if you need explicit lifecycle controls, compliance-gated flows, traceable records, and reconciliation-ready outputs.

Keep the decision evidence-based: review sample payout statuses, exception states, and export and audit artifacts before you commit. If those surfaces are weak, plan for manual exception handling.

Enterprise control only works with explicit ownership#

For larger volume or non-standard models, Stripe explicitly offers a custom package. Adyen belongs in the same lane, but the material used here does not provide Adyen pricing or integration specifics, so treat it as a structured fit check, not a default conclusion.

Before comparing enterprise options, normalize by market scope. PayPal states that published rates apply to specific resident markets and regions. It defines domestic versus international by market residency and notes grouped-market behavior that can change fee treatment. Regional exceptions also exist. For example, on PayPal IS, some EEA EUR/SEK cross-border transactions are treated as domestic for fee purposes. Save fee-page PDFs and last-updated checkpoints in your decision file, such as February 9, 2026 on the US merchant fee page and February 19, 2026 on the US consumer fee page.

Common mistakes that make fee tools unreliable#

Fee-tool outputs are unreliable when inputs are not comparable. If your model mixes jurisdictions, blurs payment-method mix, or skips reconciliation checks, treat the output as an estimate, not a decision record.

Price-only comparisons are incomplete too. Use a documented cost model and a complete list of included costs before you compare totals.

Keep AU and US models separate#

Do not combine AU and US assumptions in one model and treat the result as like-for-like unless you have verified the assumptions are directly comparable.

Use one model per resident market. Lock jurisdiction, currency, domestic and international treatment, and rail assumptions at the top so reviewers can verify exactly what was modeled.

Do not blur method mix or plan effects#

If a payment method is material, model it explicitly instead of folding it into one blended payments line. Do the same for plan tiers or custom-commercial lanes. Mark any unconfirmed input as assumed or unknown until it is confirmed in writing.

The practical check is simple: another operator should be able to open the file and see method-level assumptions without asking the model owner.

| Mistake | Why it breaks comparisons | Minimum checkpoint |

|---|---|---|

| Mixing AU and US assumptions | Different market context makes totals non-comparable | One jurisdiction per model |

| Ignoring material methods | Blended rates hide margin-sensitive flows | Method-level rows |

| Accepting calculator totals as final | Exclusions and custom placeholders distort comparisons | Annotate exclusions and unknowns |

| Skipping reconciliation tests | Gaps appear at close, not at approval | Run statement-to-ledger test before go-live |

Normalize exclusions, placeholders, and contract terms#

Treat vendor calculators as estimate tools, not contract summaries. Before you compare totals, normalize exclusions, custom placeholders, and sales-dependent fields across options.

Also review non-fee contract terms. Fee percentages alone are incomplete if fraud or nonpayment risk and dispute allocation differ across agreements.

Reconcile before launch, not at close#

A costly failure is operational: a model gets approved, then statements do not map cleanly to internal ledgers. In distributed fintech stacks, root-cause analysis can be slow once something breaks.

Before approval, run a sample close and verify that finance ops can reproduce totals from provider statements and internal ledger entries. If that fails, the cleaner-looking fee output is not ready for a decision.

If payout rails are part of the decision, see Payout Method Comparison Tool for Platform Operators Across ACH, SEPA, PIX, and UPI.

Build your decision checklist and evidence pack#

Freeze a dated evidence pack before approval. If someone who did not build the model cannot reproduce totals and exception paths from your model, treat the comparison as a draft.

Use four artifacts, and timestamp each one so reviewers can verify what was known at approval time.

| Artifact | What it must contain | What to verify before sign-off |

|---|---|---|

| Normalized input sheet | The shared inputs and assumptions used across the comparison, plus a timestamp | One like-for-like input set, with no hidden logic that changes totals |

| Provider assumption log | Unknowns, vendor-supplied assumptions, and every addendum or revision with date and owner | Revisions are captured as part of the record, not buried in email threads |

| Legal/compliance checklist | Document name, version or date, and the verification path to an official version where relevant | Informational copies are flagged as unofficial, and official versions are checked when needed |

| Verification trail sample | Sample lines and exception handling that let a reviewer trace totals end to end | A reviewer can trace totals end to end and explain unmatched items |

Treat addenda as binding decision inputs, not side notes. If a vendor updates terms or clarifies an assumption, log the change with date, owner, and impact so the evidence pack stays audit-ready.

Require one non-author review before approval. The reviewer should rerun totals and test exception paths, not just the happy path.

For final approval, include sign-off and acknowledgment fields in the approval record, plus unresolved risks and named owners, so accountability is explicit.

Before sign-off, run your assumptions through this payment fee comparison tool so reviewers are working from the same normalized model.

Verify the decision in the first 90 days#

Treat the first 90 days as a validation window, not a final verdict. Re-run live results against the dated assumptions in your evidence pack so you can spot effective-cost drift early.

| Checkpoint | What to track |

|---|---|

| Effective-rate drift | Versus your approved model, broken out by the fee components you modeled |

| One-variable comparison checks | Which single input change is driving movement |

| Reconciliation cycle time | From statement receipt to ledger-close readiness, if this is part of your control plan |

| Settlement mismatch count | Requires manual investigation, if this is part of your control plan |

| Payout exception backlog | Backlog and aging, if this is part of your control plan |

Track these checkpoints on a regular cadence with finance and payments ops:

- Effective-rate drift versus your approved model, broken out by the fee components you modeled

- One-variable comparison checks so you can isolate which single input change is driving movement

- Reconciliation cycle time from statement receipt to ledger-close readiness, if this is part of your control plan

- Settlement mismatch count that requires manual investigation, if this is part of your control plan

- Payout exception backlog and aging, if this is part of your control plan

Set explicit pass/fail thresholds for each checkpoint based on your own transaction mix, contract terms, and control design, not generic benchmarks. If a control misses threshold, trigger a defined remediation path, document the decision, and re-check the model.

Conclusion#

A payment fee comparison tool is most useful when it helps you choose the option that balances fee efficiency with operational fit, controls, and auditability. It can save time and improve pricing decisions, but outcomes are only reliable when your assumptions are explicit and your evidence is preserved.

Before approval, run a normalized comparison table, complete a dated evidence pack, and separate confirmed inputs from unresolved items. Verify key regulatory points against official editions and effective dates, then approve only after compliance checks pass with artifacts that can be checked again later.

If you want to validate market or program coverage and integration fit with an audit-ready process, request access or book a Gruv demo.

If your final decision depends on payout controls, policy gating, and reconciliation clarity, request a coverage and integration review before rollout.

Frequently Asked Questions

What should a payment fee comparison tool include to be decision-ready for platform teams?

A decision-ready tool should use a normalized input sheet and a dated source log, not just headline rates. Lock volume, average ticket, payment-method mix, refund assumptions, and geography so another operator can reproduce the total. Save the exact pricing artifact you used and keep dated change-control checkpoints.

Why do Stripe, PayPal, Adyen, and other calculators produce different totals for similar inputs?

Different totals usually come from unstated defaults, not just math errors. Standardize market scope, domestic versus international treatment, payment-method mix, and whether pricing inputs are published or unresolved. Because PayPal fee pages are market-scoped, different resident-market assumptions can produce different totals for the same volume.

Is the lowest processing fee usually the best choice for finance and operations teams?

Not always. A lower published rate can be outweighed by extra work tracing settlements, matching deposits, and resolving statement-to-ledger breaks. When options are close on price, prefer the one finance can verify and close cleanly with fewer unresolved exceptions.

How do I fairly compare providers when one or more has custom enterprise pricing?

Keep published pricing and custom enterprise pricing separate until custom terms are confirmed in writing. Mark custom items as unresolved instead of filling gaps with assumed numbers. If leadership needs a recommendation now, show a published-terms base case plus an explicit unknowns section.

Which assumptions should I lock before sharing a recommendation with leadership?

Lock jurisdiction first, because fee pages can be market-specific. Then lock payment-method mix, domestic versus international classification, and the exact source artifact used in the model. The article also treats source freshness as a control requirement, and notes PayPal's U.S. merchant and consumer pages are dated February 9, 2026 and February 19, 2026.

What are the first warning signs that a "good" pricing decision is creating reconciliation debt?

The first warning signs are operational drift: effective-rate drift versus the approved model, longer statement-to-ledger-close cycles, more settlement mismatches needing manual review, and a growing payout-exception backlog. Another red flag is when headline results still look acceptable but finance cannot consistently explain why. If spreadsheet fixes or manual deposit matching become routine, revalidate the assumptions and routing.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: