Quick Answer

Yes, you can often pay a Wise transfer with a US card, but only after an eligibility check. To wise pay invoice with credit card, confirm you are in the payer flow, use a supported network (Visa, Mastercard, or some Maestro), and complete 3D Secure. Then screen for named restriction cases such as MYR card limits or a US-issued Visa tied to a non-US Wise account address. If risk is unclear, choose a non-card method before the due date.

What this guide helps you avoid#

If you want to pay a Wise invoice with a credit card, start by choosing the right flow, not the card. The first decision is whether you are paying a supplier or collecting from a customer, because those are separate jobs in Wise.

Identify whether you are paying out or collecting in.

Treat these as two different processes. Paying a freelancer, contractor, or supplier is the payer-side transfer flow. Collecting from a client belongs in Wise Business receiving features.

- If you are paying a supplier invoice, you are in the outgoing transfer flow, where debit or credit card funding is available for most currencies, subject to card rules.

- If you want a client to pay you by card, you are in the receiving flow through business invoices, payment links, or QR codes.

The economics are different too. Card acceptance on the receiving side is presented for 18+ currencies, with published examples such as 2.9% + 0.30 USD for domestic cards and 4.2% + 0.30 USD for international or business cards. That is receiving-side pricing, not the same thing as funding an outgoing supplier payment by card.

Make a go or no-go decision before you try card funding.

For payer-side card funding, make that decision before the due-date window gets tight. Waiting until the invoice is due can turn avoidable failures into late-payment risk. Check the basics first:

- Wise accepts Visa, Mastercard, and some Maestro cards for this flow, and does not accept AMEX.

- The card needs a 16-digit number, an expiry date, and 3D Secure enabled.

- Wise notes that credit or business card funding carries higher fees, and your issuer may add charges.

- If a payment fails, Wise shows an error message, but learning that late can still create deadline risk.

Use one repeatable routine.

A good process here is simple: decide the flow, confirm eligibility, verify the invoice, and keep the record. Use a consistent routine instead of improvising at the last minute.

- Name the flow first: payer-side transfer or business receiving.

- Check card eligibility and cost tradeoffs before payment day.

- Confirm invoice details before submitting.

- Save payment records and any failure message for reconciliation and fast fallback.

Related: Value-Based Pricing: A Freelancer's Guide.

Know which Wise flow you are using before you click#

The cleanest way to avoid payment mistakes is to separate paying bills from collecting money. In Wise, those jobs use different tools and checks.

Classify the payment job first.

Ask one question first: are you paying a vendor, or asking a client to pay you? Paying an invoice is an accounts-payable task, and Wise's invoice guidance describes it as money sent to a vendor, supplier, or service provider. For that payer-side task, available rails can include ACH, credit card, wire transfer, check, or online bill pay.

If you are paying a bill, do one control step before submission: keep the payment confirmation for audit and reconciliation.

Treat client collection as a separate receiving setup.

If you are collecting from clients, move into the receiving tools. Payment links belong on that side, and the account must be upgraded with local account details configured first, available in 8+ currencies.

Timing matters here too. A Single Use payment link expires in one month, so a late client can turn an expired link into a collection delay that looks like a payment issue.

Split ownership before mistakes repeat.

If your team keeps blurring these flows, split them into two SOPs with two owners: one for bills you pay and one for money you collect through payment requests.

That split reduces repeat errors because the risks are different. On payer-side card funding, processing and international costs can outweigh cashback, and a tight credit limit can trigger a refused payment or extra fees. On receiving, common problems include setup gaps and expired links.

Gather what you need before starting payment#

Preparation matters more than speed. It is easier to check requirements before you start than to fix a failed card payment under a deadline.

Confirm your card can be used.

Start with eligibility, because it can block the payment before anything else. Wise says card funding accepts Visa, Mastercard, and some Maestro cards, and your card must have a 16-digit number, an expiry date, and 3D Secure enabled. American Express is not accepted for this flow.

Check this before the due date so you are not troubleshooting at checkout. If the card payment fails, Wise shows an error message and you lose time switching methods.

Prepare the invoice details you will enter.

Keep the invoice open while you pay so you can match the details exactly. Have the vendor name, total amount with currency, invoice number, due date, and payment reference in front of you. Wise invoice guidance also says to confirm amounts, item descriptions, and due date before you pay.

Treat the reference field as a control point. Wise says references are important for many business transfers, and for a business invoice you should use either the invoice number or the payment reference number, not both.

Check country context before payment day.

Base card support is not the only gate. Wise defines an international card payment as using a card issued in a different country from the currency you are paying in, and some restrictions depend on that context. One example in Wise guidance is that a US-issued Visa can be restricted when the address on your Wise account is outside the US.

Keep a backup rail ready.

Do not assume card funding will always be available. Wise says available payment methods can vary by invoice, so check the invoice early and note the non-card options shown there. If card is blocked, move to one of those alternatives instead of burning time on last-minute retries.

For a step-by-step walkthrough, see How Australian Agencies Can Pay US Contractors With Lower Risk.

Run a pre-check on card and corridor eligibility#

Do this before payment day: screen your exact card-and-corridor setup against Wise's stated rules, then switch rails early if anything is unclear. Wise only publishes specific restriction examples, not a complete public pass-fail matrix for every country-currency-card combination.

Map your card against the key eligibility checks.

Document these four inputs first: card network, card-issuing country, Wise account address country, and invoice currency. Wise defines an international card payment as using a card issued in a different country from the currency being paid, which is where extra restrictions can matter.

| Check item | What Wise says | Practical decision |

|---|---|---|

| Card network | Wise says card funding is available for most currencies and accepts Visa, Mastercard, and some Maestro cards. Wise also says it does not accept AMEX. | If your card network is outside Wise's supported set, switch methods now. |

| US-issued Visa card | Wise lists a restriction for US-issued cards if the address on your Wise account is outside the US, and if you're paying with a Visa card. | Treat this as high risk and line up a non-card option before the due date. |

| India-issued cards | Wise says cards issued in India with certain card networks may not be able to make payments outside India due to regulatory requirements. | Check issuer and network rules early. Do not assume all India-issued cards are blocked, and do not assume routine success. |

| Ukraine-issued Visa cards | Wise explicitly lists Visa cards issued in Ukraine as not accepted for this method. | Treat card funding as a no-go and switch methods. |

| Invoice currency vs issuing country | If they differ, Wise treats it as an international card payment. | Flag for extra restriction review, especially if any known restricted card-origin or address rule also applies. |

By the end of this step, mark the exact card you plan to use as yes, no, or risky.

Check Wise's named restriction buckets.

After the table check, verify the restriction buckets Wise calls out directly:

- MYR transfers or MYR top ups: Wise lists any card as restricted.

- Türkiye: Wise lists any card if your address is in Türkiye.

- UAE prepaid cards / AED currency card: Wise lists prepaid cards from the UAE and international payments from an AED currency card as restricted examples.

Do not stop at "supported network plus 3D Secure should work." Corridor and address restrictions can still block payment.

Switch early if anything is ambiguous.

Use one rule: if restriction status is unclear, switch to non-card funding before the due date. Do not rely on a last-minute attempt just because the card meets the base requirements of a 16-digit number, expiry date, and 3D Secure.

Wise says failed card payments show an error message, and its Help Centre advises trying another payment method if troubleshooting does not resolve the issue. In practice, ambiguity is enough reason to move to your backup method early. Make a firm execution choice before payment day: either proceed with card or switch now.

Decide when a credit card is worth it and when it is not#

Use a card for a timing problem, not as the default. If a lower-cost method will still arrive on time, that is often the better choice.

Price the full cost, not just the Wise screen.

Wise says transfer cost depends on the amount, payment method, and exchange rate. It also says payment methods vary in speed and cost. Compare the same invoice in Wise using two options: card funding and your lower-cost alternative.

Then add issuer-side risk. Wise also warns that:

- credit or business cards carry higher fees

- international card payments are charged more

- your bank might add extra fees

- some banks may treat card payments like cash withdrawals

Treat this as a hard checkpoint. If your card issuer country differs from the currency you are paying in, Wise treats it as an international card payment, so review cost more strictly. Before approving, confirm:

- total cost shown in Wise for this invoice with card funding

- whether this is domestic or international for the card and currency pair

- any issuer foreign transaction, conversion, or cash-withdrawal-style charges

Separate card classes in your comparison.

Do not compare all cards as one bucket. Card class changes the economics. The US Wise Business receiving page shows this clearly:

| Card class on US Wise Business receiving page | Fee shown |

|---|---|

| Domestic consumer card | 2.9% + 0.30 USD |

| International consumer card | 4.2% + 0.30 USD |

| Business card | 4.2% + 0.30 USD |

Wise Business defines:

- domestic consumer card: consumer credit or debit card issued in the country where the business is registered

- business card: any business credit or debit card, regardless of issuing country

These are receiving-side examples, not a universal sender fee table. They are still useful because they show how card class and cross-border status can change total cost.

Use a cashflow rule, not a rewards rule.

If card funding protects runway you need right now, the fee drag can be worth it. If timing is flexible and margin is tight, it usually is not.

Wise notes that many business credit cards offer a 30 - 60 day no interest period. That can help when an invoice is due before your receivable arrives. Use this rule:

- choose card when it keeps a critical payment on time and protects near-term cash

- choose the cheaper method when timing risk is low

Add an urgency-versus-cost checkpoint to your SOP.

Pick the method deliberately each time:

- Can the lower-cost method still arrive before the due date?

- Is this an international card payment under Wise's definition?

- Are you using a card type that may change fees?

- Did you check issuer-side fees on top of the Wise quote?

- Is the cashflow benefit worth the incremental fee on this invoice?

This keeps card funding tied to a specific timing need, not to habit.

Before choosing card vs bank rail, run your real invoice scenario through the payment fee comparison tool.

Pay the invoice in Wise with verification checkpoints#

Accuracy matters more than speed at the point of payment. A reliable pattern is to verify the invoice, use an eligible card with 3D Secure, and submit one clean reference.

Review the invoice first, then start from the invoice itself.

Start from the invoice and review it before selecting Pay now. Wise's payer flow tells you to confirm the invoice details first, and the invoice email shows who the invoice is for, what was purchased, and the total amount due.

Before you proceed, confirm:

- recipient name

- total amount due

- currency

- that this is the exact invoice you intend to pay

If anything does not match, stop and resolve it before paying. Also verify the payment options shown on that invoice, since Wise says available methods can vary by invoice. You want to be sure you are paying the correct invoice, to the correct recipient, in the intended currency, from the live invoice flow.

Enter an eligible card and complete 3D Secure.

Use a card that clearly meets Wise's requirements. Wise says most currencies can be funded by debit or credit card, accepts Visa, Mastercard, and some Maestro cards, and does not accept AMEX for this flow.

The card must have:

- a 16-digit card number

- an expiry date

- 3D Secure enabled

If 3D Secure cannot be completed, the card payment may not go through. Treat this as an authentication checkpoint, not just form entry.

Run a final confirmation check before submitting.

Before final submit, do one reconciliation pass against the invoice. Check:

- recipient name

- invoice currency

- total amount due

- funding method

- payment reference

For reference entry, use either the invoice number or the payment reference number, not both. Wise warns that entering both can prevent matching and may block processing. Wise also notes the reference field appears in Step 4 of setup, so treat it as a control point.

If all fields align, submit. If one field is off, correct it before confirming. The goal is one clean payment with the correct amount, currency, and a single reference the recipient can match.

Handle failed card payments without missing the due date#

When a card payment fails, speed matters, but guessing makes things worse. The practical sequence is to read the error, verify the likely cause, retry after a specific fix, and switch methods if the issue persists.

Read the error message and capture it.

Wise says failed card payments show an error message, so start there. Capture the message and log the invoice number, amount, currency, payment reference, timestamp, and card network used.

That gives you a concrete troubleshooting starting point: card type, authentication, or a restriction tied to currency or account context.

Check the eligibility assumption that likely failed.

Check Wise's card-funding rules first. For this flow, Wise accepts Visa, Mastercard, and some Maestro cards, and does not accept American Express. The card must also have a 16-digit number, an expiry date, and 3D Secure enabled.

Then check the restriction patterns Wise lists, including:

- any card when paying for MYR transfers or MYR top ups

- any card if the address on your Wise account is in Türkiye

- US-issued Visa cards when the address on your Wise account is outside the US

- prepaid cards from the UAE, or international payments from an AED currency card

Wise also defines an international card payment as a card issued in a different country from the currency being paid, so card-origin and currency mismatch can be a real cause.

Retry after a specific correction, then change method if needed.

Retry after fixing something concrete, such as moving from AMEX to an accepted network, using a card with 3D Secure enabled, or replacing a restricted card and currency setup.

If it still fails after troubleshooting, switch to another payment method. Wise's guidance is to try another method when card-payment fixes do not work.

Do not rely on cancellation as a fallback. Wise says only uncompleted transactions can be canceled, and debit card refunds are usually returned in 2 to 5 working days. Processing can take up to 10 working days.

Reissue payment and notify the vendor.

If card funding still does not go through, reissue payment using your fallback method. Notify the vendor with the essentials: invoice ID, amount, currency, initiation time, and the new payment reference or confirmation.

Keep the message factual and concise so they can match incoming funds quickly. Related reading: How to Pay International Contractors With Fewer Delays and Disputes.

Know cancellation and refund limits before you rely on them#

Cancellation and refunds are not a good due-date plan. In Wise, they are conditional.

Treat cancellation as conditional.

Wise says refunds happen if a transfer is cancelled or if the recipient bank sends funds back. It also notes some transfers are cancelled for regulatory reasons. So do not assume a submitted payment can always be reversed on demand.

If funds look delayed, check Wise Activity or your home screen for pending tasks or notifications before telling the vendor the payment is being reversed. First confirm whether Wise needs action from you instead.

Keep the refund route clean.

For card-funded payments, Wise sends refunds to the same card used to pay. If that card is expired or cancelled, the refund can still arrive if the linked bank account is open. If that account is closed, the refund may bounce back to Wise.

If Wise asks for refund details, for example through Fix your transfer, provide the account details Wise expects for the refund. Entering different bank details can make the refund fail.

Build timing slack into your AP process.

Set a hard rule: do not schedule card payments so late that cancellation, refunds, or a rail switch have to save the due date. Wise notes most transfers run on working days, and Swift or wire payments can take 2 to 6 working days to reach Wise.

If your card attempt misses your internal cutoff, switch methods the same day and keep proof of payment ready in case funds later need tracing.

Keep an audit-ready payment record each time#

A same-day payment record saves time later. It helps you handle disputes, tracing requests, and month-end reconciliation without rebuilding the story from memory.

Download payment proof after completion.

In Wise, the core receipt is the transfer confirmation PDF for a completed transfer, so download it as soon as the transfer completes and store it with the supplier invoice. Save the transfer number on every payment, and save the banking partner reference number when it appears, since it is only available for some transfers.

If a recipient bank cannot find funds, Wise says the banking partner reference on the PDF is the most useful number to share for tracing. Card statements and email notifications may not include the same tracing identifiers.

Log the exact reference and final outcome.

Record what actually happened, not just what was planned. Log your invoice number, the reference entered at payment, final status, your internal timestamp, and the funding method used.

For invoice payments, use either the invoice number or the payment reference number, not both. Wise warns that entering both can break matching and may stop completion, so your log should show which single reference you used.

| Field to store | What to enter | Why it matters |

|---|---|---|

| Wise transfer number | Transfer ID shown for the payment | Present for every transfer and useful for support and tracing |

| Banking partner reference | Save only if shown | Most useful number for recipient-bank tracing |

| Invoice number or payment reference used | One reference only | Reduces matching failures on invoice payments |

| Status and funding method | Transfer status plus the funding method used (for example, card-funded) | Supports reconciliation and repeatable process |

This gives your team a clean record of which reference was used, how the payment finished, and what to provide if the vendor asks questions.

Export from Transactions, not statements alone.

Use the Transactions export as your working audit record, especially for card-funded payments. Wise states account statements only include transactions made via Wise currency accounts. Transactions exports can be filtered by status, direction, card category, and currency for up to a 365-day period.

If your monthly statement does not show a card-funded transfer the way you expect, use the transfer export as the backup record. Keep one shared template folder and consistent naming so reconciliation stays clean, and review suggested QuickBooks matches before posting.

Use Wise Business receiving tools when you are the one getting paid#

If you are collecting money from clients, run that as a separate receiving procedure. Wise documents receiving and paying invoices as separate workflows, and payment methods can vary by request.

Pick the receiving tool based on client context.

Choose the tool that fits how the client will pay you:

- Invoices you create and send from your business account

- Payment links to request payment directly

- Quick Pay link or QR code for website, in-person, or invoice payments

Before sending, verify which methods are enabled for that specific invoice or link. Do not assume card payment will appear on every request.

Confirm card acceptance before you promise it.

If you plan to accept cards, check eligibility and access in your own account first. Wise says businesses with accounts in the EEA, UK, Australia, Hong Kong, New Zealand, Singapore, Canada, and the US can request card, Apple Pay, and Google Pay receiving. It also says some businesses in eligible regions still may not get access.

If enabled, Wise says card acceptance works with payment links, invoices, and QR codes, and supports 18+ currencies. For single-use payment links, remember they expire after 30 calendar days.

Keep payer-side and receiving-side procedures separate.

Maintain two short procedures:

- Payer-side SOP: how your team pays invoices

- Receiving-side SOP: how your team issues invoices, payment links, and Quick Pay or QR requests

This split prevents policy confusion, like promising methods that are not available on a specific client request or in your region.

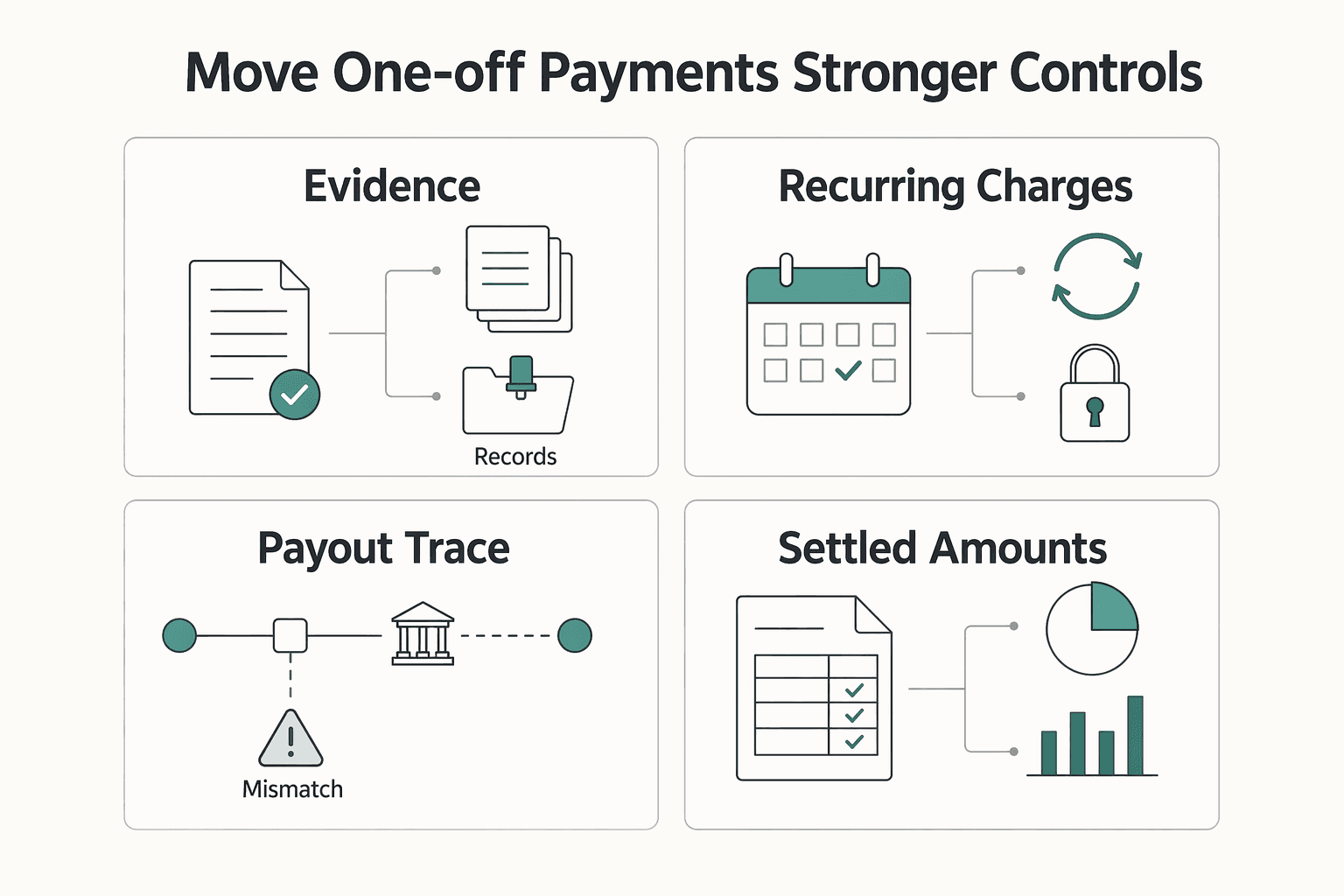

When to move from one-off payments to stronger controls#

Move to stronger controls when ad hoc handling stops giving you clear answers on approval, status, and reconciliation. Instead of using a fixed invoice-count trigger, use the point where tracing a payment from invoice to final funds movement starts taking detective work.

Spot when ad hoc handling is becoming riskier.

Upgrade controls when these issues stop being rare:

- authorization checks are inconsistent or not clearly documented

- recurring charges run without clear authorization transparency

- reconciliation is delayed and clearing or settlement status is hard to confirm

- settled amounts are hard to explain against expected net after fees

Weak processing can increase costs, failed payments, and dispute workload, so waiting for a major failure is usually too late.

Track payments by stage, not just "submitted."

A single submitted status can become insufficient as payment volume or complexity grows. Card processing is commonly framed as a 3-step flow: customer pays, payment is approved, and funds arrive. In practice, track authorization, clearing, and settlement separately.

For each payment, record status by stage plus owner, date, and reference. Authorization is the issuer's approval-or-decline decision. Clearing is reconciliation and transaction-information exchange. Settlement is the movement of funds between banks. This makes timing questions, net-after-fee differences, and "has it actually landed?" much easier to answer.

Keep a repeatable evidence pack for each payment.

Use one standard record per payment so any teammate can verify it without asking the initiator. Include invoice ID, legal counterparty name, currency, amount, approver, payment reference, timestamp, and confirmation evidence.

If you use reconciliation forms, apply them consistently. Where card data touches your process directly, require the relevant compliance artifact, for example a PCI-DSS certification artifact, instead of relying on screenshots or memory.

Choose tools by control quality.

Prioritize tools and procedures that support documented approvals, traceable records, and explicit status tracking. Keep internal policy clear regardless of tool choice: who approves, what evidence is required, and when reconciliation is complete.

If you evaluate Gruv, assess it on compliance-first controls and audit-ready traceability. Keep implementation claims narrow during rollout, since coverage and features vary by market and program.

Copy and paste this risk-first payment checklist#

Use this before any card-funded invoice payment to avoid deadline failures caused by choosing the wrong Wise flow or finding restrictions too late.

- Confirm the flow first.

Paying a supplier invoice is the payer-side Wise transfer flow. Getting paid by a client uses receiving tools like payment links, Quick Pay link, or QR code. Keep them separate, because receiving-side card acceptance does not guarantee outgoing card-funding eligibility.

- Validate card eligibility before payment day.

For payer-side card funding, Wise requires a 16-digit card number, expiry date, and 3D Secure. Wise accepts Visa, Mastercard, and some Maestro, but not AMEX. Check known restrictions in advance, including MYR transfers or top ups, accounts with addresses in Türkiye, Visa cards issued in Ukraine, and US-issued Visa cards when your Wise account address is outside the US.

- Pick method by urgency versus cost.

If timing is critical and added cost is acceptable, card funding can be reasonable. If timing is flexible or margin is tight, consider a lower-cost method. Wise states international card payments cost more, and issuer fees may also apply.

- Run four checks before submit.

Verify recipient, currency, total amount, and payment reference directly from the invoice. Wise emphasizes checking recipient and amount, and notes references are important for many business transfers.

- If card fails, troubleshoot from the error, then switch if unresolved.

Wise says failed card payments show an error message, so start there. Fix a specific cause you can verify, for example 3D Secure or a restricted card and currency context, then try again with corrected details. If issues continue, move to your fallback method without delay.

- Save proof immediately for reconciliation.

Keep the confirmation, transfer ID or reference, invoice ID, timestamp, final funding method, and invoice terms. If you switched from card funding, record that too so later fee and timing differences are easy to explain.

If you are turning this checklist into a repeatable AP process, review the Gruv docs for compliance-gated flows, status tracking, and audit-ready records where supported.

Frequently Asked Questions

Can I pay a Wise transfer with a US credit card?

In many cases, yes, but not in every setup. Wise says card funding depends on currency and region, and it lists specific restrictions, including US-issued Visa cards when your Wise account address is outside the US. If the card was issued in a different country from the currency you are paying in, Wise treats it as an international card payment, so check eligibility before the due date.

Which cards does Wise accept for card payments?

Wise says it accepts Visa, Mastercard, and some Maestro cards for card-funded transfers. Wise also says it does not accept American Express. If the card network is unsupported, the payment will not go through.

Do I need 3D Secure to pay by card?

Yes. Wise says the card must have a 16-digit card number, an expiry date, and 3D security enabled. If 3D Secure authentication cannot be completed, the card payment may fail, so you may need to use another payment method.

Are credit card payments on Wise more expensive?

They can be. Wise says credit card or business card payments are charged at a higher fee, and your bank or card issuer may add extra fees. Check total landed cost, not just the Wise fee.

Can I use any card for MYR or certain restricted corridors?

No. Wise lists a restriction for any card when paying for MYR transfers or MYR top ups. Wise also notes some issuer-country, network, and account-address combinations can be blocked.

Can businesses accept card payments through Wise invoices?

Yes, on the receiving side. Wise says card acceptance works with payment links, invoices, and QR codes, and markets support for 18+ currencies where available. It also lists example processing fees, including 2.9% + 0.30 USD for domestic consumer cards and 4.2% + 0.30 USD for international consumer and business cards.

What should I do if a card payment fails right before the due date?

Start with the error message, because Wise says failed card payments show an error. Check common blockers first, such as an unsupported card network, missing 3D Secure, or a restricted currency and card combination. If the deadline is close, consider another available payment method.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- docs.legis.wisconsin.gov/document/statutes/16.pdftrusted

- federalreserve.gov/publications/fr-y-14-qas/fr-y-14-qas-fr-y-14...trusted

- federalreserve.gov/publications/files/usb_p3.pdftrusted

- financial.ucsc.edu/Pages/Cash_Guide.aspxtrusted

- wise.com/us/business/accept-card-paymentstrusted

- wise.com/help/articles/4qr3kkvIQlHNiD8BegEB4u/getting...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

A Guide to Using Wise for Payroll for International Contractors

**Use Wise as the execution layer for payroll, then wrap it in your own controls so every cycle runs the same way with clearer fees and fewer avoidable delays.**