Quick Answer

Start with the narrowest control and escalate only when the file shows broader risk. Use a transaction-level hold for isolated anomalies, then move to wider restrictions only if identity or network signals spread beyond that event. Treat timeline examples such as one to seven days or up to 30 days as context, not policy. Every case should record trigger, reason code, approver, provider reference, linked ledger entry, and the exact release condition before funds are restored.

When a Temporary Fund Freeze Makes Sense#

Temporary holds and freezes are useful payment controls, but choosing the wrong one creates avoidable operational stress.

- A payment hold delays access to funds. It does not decide the final outcome.

A payment hold temporarily delays fund availability after a transaction. It can be triggered by a new account, unusual activity, or a sudden large transfer, and is commonly used to screen for fraud, manage chargeback risk, or meet compliance rules. One provider guide describes typical delays of one to seven days, with some flagged accounts, high-limit payments, or B2B transfers taking up to 30 days. In practice, a hold primarily affects when funds become available.

- A hold and a freeze are different actions, so they should be chosen differently.

Merchant account holds and merchant account freezes are not interchangeable. With a hold, sale funds may be set aside until release. With a freeze, the business may also be temporarily limited from processing new card payments. Both affect cash flow, and a freeze is broader. Frequent chargebacks are one pattern that can lead a provider to freeze an account.

- This guide is for teams that need to decide quickly and keep a clear record.

If you own compliance, legal, finance, or risk decisions, the practical question is which temporary control matches the signal in front of you. You also need a clear record of what triggered the control, what was reviewed, and what must be true before release. The sections that follow focus on those decision and release mechanics.

- There is no single timing rule, so policy discipline matters more than folklore.

Hold timelines vary by bank, region, and provider, so universal triggers and release timelines are not reliable. A stronger approach is to document why funds were held, who approved the action, what facts were checked, and what condition supports release. That is what helps keep a control proportionate while reducing unnecessary payout disruption.

If you're tuning the signals that trigger a freeze, see Fraud Detection on Payment Platforms with Rules and Machine Learning.

How to choose a hold control and who this list is for#

Use this list if you set policy gates for platform money movement and need decisions you can document and defend. Do not use it to find a universal trigger or timeline across providers. In this context, treat controls as platform-specific policy choices for your own Payouts, Virtual Accounts, or Merchant of Record (MoR) flows, and do not treat these sources as operational payout-control rules.

- Right audience

This section is for compliance, legal, finance, and risk teams that decide when to delay funds, who approves that decision, and what evidence must be checked before release. The focus is policy and evidence quality, not just reacting to a fraud score.

- Wrong expectation

Do not expect one cross-platform threshold, hold rate, or release timeline that applies cleanly everywhere. If stakeholders ask for a single "normal" trigger, document your own platform-specific matrix instead of relying on market folklore.

- Ranking lens

Compare hold options using internal criteria such as fraud-loss containment, cashflow impact, review effort, and audit defensibility under your KYC, KYB, and AML controls. That lens makes the tradeoffs explicit before you scale a control.

- Escalation rule, as a policy choice rather than a universal standard

If you use a decision rule, define it clearly in policy and apply it consistently. The provided excerpts do not establish a universal escalation formula for hold types. Treasury's February 2022 National Money Laundering Risk Assessment still supports making your rationale explicit: money laundering can facilitate and conceal crime and can distort markets.

One practical legal-source note: if you cite FederalRegister.gov, verify the text against the linked official govinfo PDF. The CFPB final rule page published on 12/10/2024 (89 FR 99582) is a concrete example. The XML rendition is explicitly unofficial and does not provide legal or judicial notice.

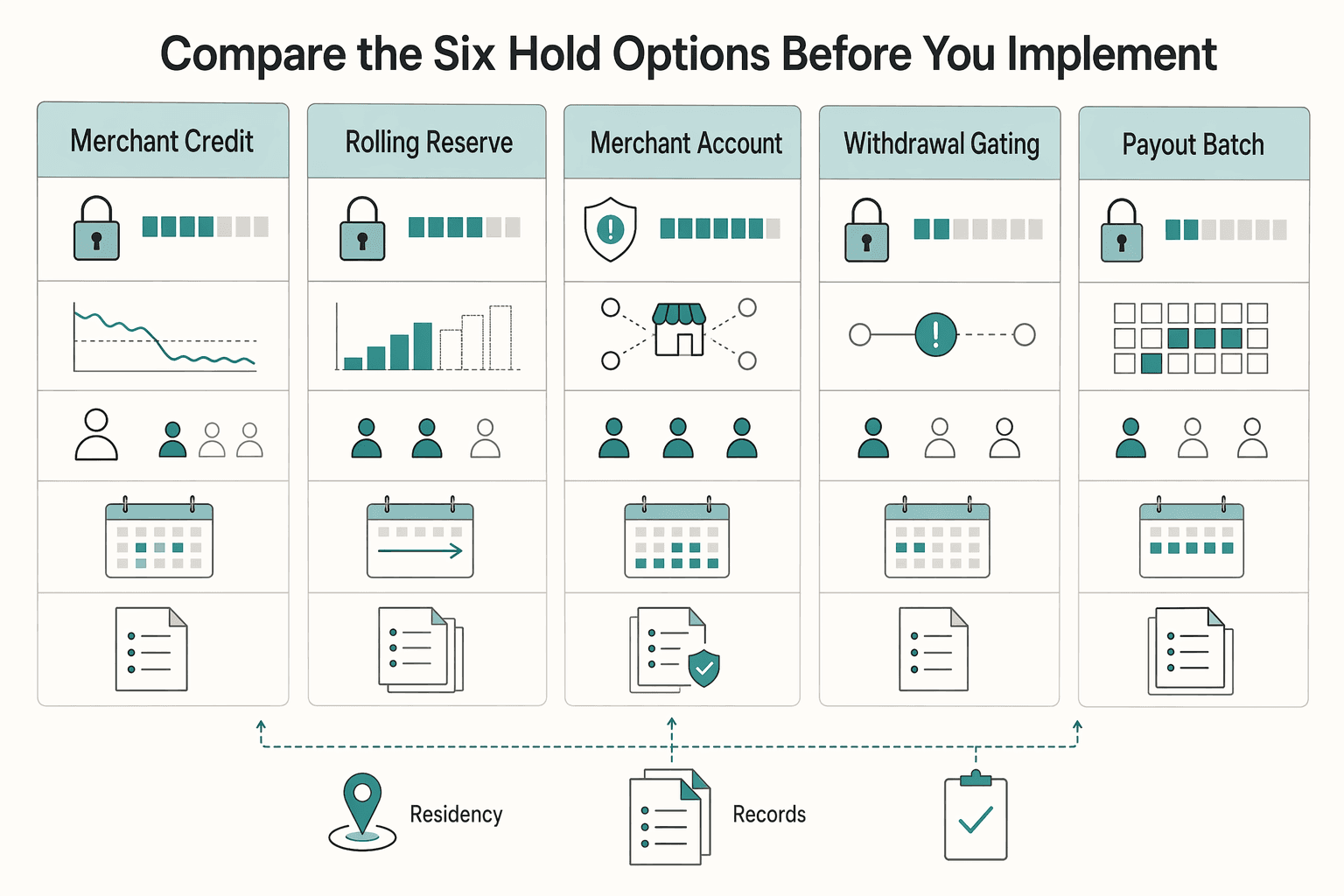

Compare the six hold options before you implement#

Build this matrix before production so fraud containment, cashflow impact, and review workload are evaluated together. Define clear escalation criteria for merchant account freeze so it is used when risk appears broader than a narrow, event-level issue.

The comparison format matters. FCA fraud-controls material is structured for side-by-side control comparison, including "what controls does the firm have in place?" At least one firm also frames fraud controls as a balance between loss reduction, customer impact, and operational demand. Use that same balance as the shape of your own policy.

Use this matrix as a policy-design template, and calibrate the low/medium/high labels to your own risk model and operations.

| Control type | Best for | Blast radius | Release dependency | Cashflow risk to sellers/contractors | Documentation burden | Common failure mode |

|---|---|---|---|---|---|---|

| merchant credit hold for review | Narrow, event-level anomalies | Low to medium, limited to held credits/transactions | Review confirms hold reason and release or return decision | Medium when near-term obligations depend on held funds | Moderate | Review queues run long and a targeted hold becomes broader harm |

| rolling reserve | Ongoing concern where trust is reduced but not broken | Medium, because liquidity is constrained over time | Terms and monitoring checkpoints are met over time | Medium to high due to sustained liquidity drag | Moderate | Reserve persists without clear exit logic |

| merchant account freeze | Broad account-level concern, including identity, behavior, or linked risk | Very high, often account-wide | Senior decision, full remediation review, defensible record | Very high | High | Freeze is applied broadly before scope and duration are clearly justified |

| Withdrawal gating on Virtual Accounts | Funds are credited but still uncertain or under review | Medium, focused on outward movement from affected balances | Payment state is resolved and release decision is documented | Medium | Moderate to high | Legitimate users perceive arbitrary restriction when rationale is unclear |

| Payout batch delay in Payouts | Mixed-risk payout runs | Low to medium if recipients are segmented well, high if the whole run is delayed | Recipient-level review and controlled retry or release flow | Low for clean recipients if partial release works, high if the full batch is blocked | High | Poor status handling causes duplicate, missed, or delayed payouts |

| Enhanced-document hold tied to KYC/KYB | Missing, stale, or inconsistent documentation | Medium, limited to unresolved accounts | Remediation requirements are completed and verified per policy | Medium to high if remediation stays open-ended | High | "More documents needed" loops without a clear sufficiency standard |

Aim to use the smallest control that matches the risk scope, then escalate when evidence shows broader risk. That keeps policy proportionate and defensible instead of defaulting to maximum restriction.

Also separate fraud controls from reliability incidents. Digital payments depend on interbank communications and internet-connected processors, and outages can leave merchants unable to accept electronic payments. The Federal Reserve cites a 2018 Visa outage with 5 million failed transactions over a 10-hour outage. That kind of disruption can be mistaken for fraud at first, so verify whether the issue is fraud risk or operational failure before you decide on release.

Use a transaction-level review hold when risk is narrow#

When the signal is tied to one payment event, consider starting with a transaction-level hold for review instead of a broader freeze. That keeps the response proportionate. You isolate the flagged payment while you review it, rather than pausing payouts and possibly limiting new payment acceptance across the account.

When this is the right control#

Use this hold when the anomaly is specific and recent, with no clear account-wide pattern. Grounded triggers include unusual activity, sudden volume spikes, unusually large single tickets, and incomplete verification details.

A concrete example is an account that usually averages $400 per transaction and then presents a $5,000 payment that triggers review. Treat that as transaction-specific unless evidence starts to show broader risk.

What makes it useful#

The main advantage is scope. A temporary fund hold is a short-term delay while transactions are reviewed, which is generally less disruptive than a full freeze or closure.

It is also easier to defend when evidence is still thin. If your file shows one outlier payment plus unresolved verification details, a transaction-level hold can fit the facts better than an account-wide restriction.

The operator checks that matter#

Do not place this hold on a vague signal. Record a small evidence pack that shows why the event is out of pattern and what clears release. At minimum, capture:

| Check | What to record | Example |

|---|---|---|

| Amount pattern | flagged amount versus recent average ticket | $5,000 versus $400 |

| Documentation issue | specific documentation issue | incomplete verification; mismatched EIN; missing license |

| Provider request | whether the provider has requested more details in the dashboard | requested more details in the dashboard |

| Release condition | what document or confirmation resolves the hold | explicit release condition |

Where it goes wrong#

The common failure mode is scope creep. A narrow hold becomes harder to justify if repeated anomalies appear or documentation gaps spread beyond one event.

When that happens, reassess the control level instead of leaving a transaction hold open-ended. Also treat chargeback signals carefully: one source describes 1% as a review trigger, but that figure is not a universal legal threshold.

Related reading: Account Reconciliation for Payment Platforms: How to Automate the Match Between Payouts and GL Entries.

Use a rolling reserve when disputes are trending but trust is not broken#

This evidence set does not tell you when a rolling reserve should be used. There is no universal threshold, standard percentage, standard duration, or platform-specific trigger you can rely on here.

What this section can support#

The support here is narrow: these excerpts are about source authority and filing metadata, not reserve operations. They do not provide authoritative operating rules for reserve setup, escalation, or release.

Verification standard before policy decisions#

Be precise about source authority. The FederalRegister.gov item (2026-02769, published 02/11/2026) is labeled a Proposed Rule and states that the page is not the official legal edition. It also directs legal research users to verify against an official edition and provides a printed PDF link. The SEC excerpt is a Form F-1 Registration Statement header, confidentially submitted on May 9, 2025, not payment-hold policy guidance.

Practical implication for escalation#

Do not infer a specific escalation rule, hold duration, or release condition from these excerpts alone.

Use a full account freeze only for identity or network-level risk#

A full account freeze is the broadest tool in this set, so use it only when the concern is account-wide and cannot be contained at transaction level. If the issue can still be scoped to one or more transactions, use a transaction-level hold instead. A freeze is a more severe control and can stop access to funds.

Supported reasons for escalation include unusual or suspicious transaction activity, possible money-laundering risk, or a need to protect users while risk is investigated. Do not treat one odd payment as automatic grounds for a full freeze, and do not assume universal thresholds for when to place or release one.

Before you freeze an account, document:

- why a hold on one or more transactions is not enough

- which facts make the risk account-wide

- who owns review and what conditions must be met before access is restored

The main tradeoff is customer harm. A full freeze can unfairly restrict legitimate users from accessing their own money. If the account operates across multiple jurisdictions, document ownership clearly because rules can differ by market.

When a freeze is tied to payout changes or updated bank details, see Wire Fraud Prevention for Platforms: How to Spot Spoofed Bank Details Before You Pay.

Gate withdrawals in Virtual Accounts when inbound funds are uncertain#

When inbound funds are still uncertain, gate withdrawals in Virtual Accounts instead of defaulting to a full account freeze. This keeps funds from moving out while you verify the inbound credit, without treating the whole account as unsafe.

This control is most useful when a credit appears before review is complete. The key point is scope: you are restricting outward movement on unresolved funds, not making an account-wide fraud determination.

Why this is the better middle ground#

A withdrawal gate can buy investigation time with less customer impact than a full freeze. Consumer complaint narratives support the pattern of temporary review states and restricted use during verification, including "account under review" and requests for more identity information. The practical takeaway is that these holds can be precautionary while facts are checked, not proof of confirmed fraud.

What your release check should look like#

Because the grounding here does not provide universal release deadlines or cross-platform thresholds, use a consistent internal checkpoint before release or return decisions, for example:

| Checkpoint | What to confirm |

|---|---|

| Provider reference match | tie the inbound transfer to the correct sender record |

| Ledger posting validation | confirm the current credited, held, or returned status |

| Review note | facts, decision owner, and outcome, whether release, continued gate, or return |

Where teams get this wrong#

A recurring failure mode in complaint narratives is communication, not just the gate itself. Complaint narratives describe users being told a review may take 7-10 business days, then reporting 16 business days with funds still blocked. They also describe support handoff breakdowns between teams, which can make a temporary control look arbitrary.

The user impact can be material: one narrative reports {$600.00} still unavailable to transfer, and another reports lost work opportunity. If you gate withdrawals, keep the customer message precise, avoid timelines you cannot meet, and update the stated reason only if the case file supports that change. For example, move from transfer review to identity verification only when the case file supports that change.

Delay payout batches with partial release instead of platform-wide stops#

If only part of a payout run is questionable, delay that subset and release the clean recipients first. That can contain fraud and funding risk with less user impact than stopping an entire mixed-risk batch.

The limit is evidence: the source guidance supports temporary fund-availability controls, staged release approaches, and data matching, but not a universal split threshold or one prescribed batch method. A practical rule is simple: when risk is recipient-specific or funding-specific, isolate that lane first.

Use it when risk is mixed, not account-wide#

Use partial release when some payees are clear and a smaller group needs review for bank-detail or funding-availability reasons. This matters in ACH flows, where a transfer can be initiated but still be under verification, and funds can appear in total balance while remaining unavailable until cleared. Most ACH transfers settle within 1-3 business days, and same-day ACH can shorten timing in some cases.

What to split and what to keep constant#

Keep payment intent stable and split execution paths:

- move flagged recipients into a delayed lane with its own status, review owner, and release condition

- release clean recipients under a separate payout reference

- keep retry handling idempotent so delayed recipients are not paid twice across separate retries

Your checkpoint should confirm which recipients are tied to a pending ACH or other unresolved funding event. It should also confirm whether funds are visible versus cleared, and the exact link between recipient, funding source, and hold reason. This is where data matching becomes operationally useful.

The main tradeoff is reconciliation discipline#

A key operational risk after the split is state and reconciliation drift. Problems show up when original batches, released subsets, and delayed subsets carry inconsistent statuses, or when retry states blur "not yet released" and "failed, then retried."

Keep a batch-level record of the original batch ID, child payout IDs, affected recipient IDs, funding-source reference, delay timestamp, reviewer, and release trigger.

Operator rule#

If a batch contains both clean and risky recipients, split it and release the clean lane first. Use a platform-wide stop when risk is no longer contained to a subset of payees or funding events.

Related: Airline Delay Compensation Payments: How Aviation Platforms Disburse Refunds at Scale.

Trigger document-driven holds for compliance gaps, not just fraud patterns#

Use a document-driven hold when payout is blocked by a specific documentation deficiency under your own program controls, not by a proven fraud event. That keeps the case narrow: the account is pending required remediation, and release depends on defined artifacts.

Use a deficiency basis, not a suspicion basis#

A defensible document hold starts with a specific gap and a clear release condition. If you cannot name the exact deficiency, the hold is probably too vague.

"Tax profile incomplete" is weak by itself. "Required tax form missing, expired, or inconsistent with account details" is stronger because the remediation path is explicit. Missing tax documentation can justify remediation under your controls, but it does not by itself prove fraud or create a universal freeze rule.

Verify the form logic, not just the story#

Review against concrete artifacts, not narrative explanations. Your record should capture:

- the exact missing, stale, or conflicting document

- the policy or payout condition that requires it

- the reviewer, outreach date, and release condition

FEIE is a good example of why this matters. If a payee says they qualify for the Foreign Earned Income Exclusion, validate the form status and profile details rather than clearing it on self-attestation. The IRS states FEIE applies only to qualifying individuals with foreign earned income and is claimed on Form 2555 or Form 2555-EZ. It also states the physical presence test can require 330 full days in a 12-month period (with a tax home in a foreign country), with each full day defined as 24 consecutive hours (midnight to midnight). The IRS also states income is still reported on a U.S. tax return even when FEIE is claimed.

A common failure mode is the endless hold#

Endless holds can come from unclear ownership or changing acceptance standards. When requests change over time without a final checklist, payout can stay blocked and escalation risk can rise.

Set one consolidated deficiency notice at hold placement: list each required artifact and the exact release test for each. If the case expands beyond documentation quality into broader misuse risk, move it out of the document lane and into your broader risk-hold process.

For a step-by-step walkthrough, see Device Fingerprinting Fraud Detection Platforms for Payment Risk Teams.

Build the minimum evidence pack every hold decision must have#

A hold decision is more defensible when another reviewer can reconstruct both the hold and the release from the file alone. Set one internal minimum record template and use it consistently. Keep coded fields and narrative notes separate so the file shows what happened, what was observed, what was decided, and what must be true before release. Treat this as your program standard, not as a universal legal template.

1) Fix your record set. Use a fixed case structure for every hold so reviewers are not piecing decisions together from scattered notes. Consistency is the control. If the same decision data appears in the same place each time, escalations and re-reviews are faster and more reliable.

2) Tie each claim to a retrievable artifact. For each assertion in the file, store the underlying system artifact, not just a summary note or screenshot. Stable identifiers and official documents are easier to audit later than ad hoc evidence. When you cite legal or regulatory materials, keep the official version in the case file when available:

- FederalRegister.gov states its pages are XML renditions and not an official legal edition, and says legal research should be verified against an official edition

- if you rely on the CFPB entry for Document Number 2024-27836, 89 FR 99582, or Docket No. CFPB-2023-0053, retain the official printed PDF artifact

- if you rely on enacted law status, retain the Congress.gov record showing H.R. 7148 became Public Law No. 119-75 on 02/03/2026

3) Separate facts, uncertainty, and judgment. Write notes so observed facts are distinct from assumptions and reviewer conclusions. If a point is unverified, label it that way and state what would confirm or disprove it. That makes legal and compliance review more credible and easier to challenge-test.

4) Make release a documented checkpoint. Treat release as a second explicit decision, with evidence that the original hold basis was resolved. The file should show why release is now appropriate, not just that time passed or new material arrived. A strong evidence pack is not the longest file. It is the most complete, traceable, and reviewable one.

Turn this checklist into a repeatable runbook with event logs, approvals, and release checkpoints in the Gruv docs.

Set escalation and release governance before the first incident#

If authority, handoffs, and communication rules are not set before a serious hold, decisions can drift and controls can become harder to defend at release.

| Governance area | What to define | Recorded detail |

|---|---|---|

| Authority by control depth | who can place, who can extend, and who can release | approver, timestamp, current rationale, and release condition |

| Handoff path | one internal path with a single current-owner field | what must be true for the next function to act |

| User communications | notice language aligned to the action taken and the facts you can support | template version, sender, and send time |

| Legal-source checkpoints | verify FederalRegister.gov against the official edition | official edition and govinfo PDF in the file |

1. Split authority by control depth (internal policy choice). For each hold type, decide and document who can place, who can extend, and who can release. Keep those approvals explicit in the case file for extensions and releases, including approver, timestamp, current rationale, and release condition. This helps avoid holds staying active without a fresh recorded decision.

2. Fix one internal handoff path for live incidents. This grounding set does not establish a universal sequence, so set one internal path your teams can execute under payout pressure. Use a single current-owner field and require each handoff note to state what must be true for the next function to act. That keeps ownership clear across risk, compliance, legal, finance, and operations when timing pressure is highest.

3. Treat user communications as a control. Keep notice language aligned to the action taken and the facts you can support. If the file supports "under review" or "additional information required," do not overstate the wording. Store each outbound notice in the case record with template version, sender, and send time so you can verify consistency if the decision is challenged.

4. Write uncertainty into policy, and enforce legal-source checkpoints. State this directly in governance: this grounding set does not provide a universal timing benchmark or cross-platform trigger threshold for placing, extending, or releasing holds. Release decisions should rely on resolved facts and documented remediation, not copied timing rules.

When legal interpretation is involved, treat FederalRegister.gov pages as informational. The site states they are not an official legal edition and do not provide legal or judicial notice. Verify against the official edition and retain the govinfo PDF in the file. If you rely on the CFPB item published on 12/10/2024 (89 FR 99582), keep the official PDF artifact. If rationale depends on terms tied to the Bank Secrecy Act or "digital asset service provider" in Public Law 119-27, route for legal review against enacted text.

What to implement first in the next 30 days#

In the next 30 days, prioritize consistency and release readiness over new fraud thresholds, because hold triggers and timelines are not universal across providers.

1. Build one control matrix. Create one matrix for transaction hold, reserve, withdrawal gate, batch delay, and full freeze. For each control, define:

- what risk it addresses

- who can place it

- what evidence is required

- what must be true to release it

A payment hold is a temporary delay in fund availability, not a failed transaction, so reviewers should match control scope to risk scope. If the signal is narrow, use the least disruptive control first.

2. Require one evidence pack and one release checklist. Use one case-file standard for every hold event, regardless of rail or tool. Capture, at minimum:

- trigger event and reason code

- hold type and start timestamp

- approver

- provider reference and related ledger entry

- actions taken and user communication sent

- explicit release condition

Release decisions should be understandable to a reviewer who did not place the hold. Set provider-specific review points, and do not treat generic ranges like one to seven days or up to 30 days as universal policy.

3. Pilot partial release in Payouts and tighten document-hold messages. Pilot partial release logic in Payouts for mixed-risk runs so clean payouts can proceed while flagged items stay contained. One industry example notes that a provider may withhold all, part, or selected payouts. Use that as an operational pattern, not a legal rule.

Track held, released, and retry-eligible recipients clearly to reduce reconciliation and duplicate-payment risk. Pair this with clear compliance-hold templates that state what is under review, what is missing, where to submit it, what activity is affected, and when the next review point is.

4. Escalate legal review when policy coverage is behind risk. Escalate early when cross-market interpretation, restore-access handling expectations, or customer-harm exposure is unclear. If a hold can overreach, legal review should test authority and restore-access handling, not just approve wording.

When reviewing Federal Register materials, treat FederalRegister.gov rendering as informational and verify legal reliance against the official edition and linked govinfo PDF. In the same 30-day window, close any policy gap where hold placement is defined but restore-access handling is not.

For freezes tied to account-opening risk, see What Payment Platforms Must Know About Synthetic Identity Fraud.

If your next 30-day plan includes partial releases and tighter payout governance, review how Gruv Payouts supports controlled disbursement operations.

Frequently Asked Questions

What is the practical difference between a payment hold and a full account freeze?

A payment hold means funds become temporarily unavailable. A broader freeze has a larger operational impact: a third-party Stripe-focused article says payouts can be paused and new payments may also be blocked during review. In practice, the key difference is operational scope.

When can a platform freeze funds for compliance reasons without overreaching?

Public guidance in this pack is limited: PayPal says a hold or account restriction may be used when more information is needed about transactions, business details, or account activity. Beyond that, this pack does not establish a universal legal or compliance rule for when a full freeze is appropriate.

Which events most commonly trigger temporary fund holds in Stripe and Shopify Payments style ecosystems?

In this grounding pack, the clearest trigger examples are from PayPal: first-time seller status, unusual or changed selling patterns, higher-risk items, and multiple refunds, disputes, or chargebacks. A third-party article says Stripe freeze reviews often include an email or dashboard request for more information, but that should not be treated as a universal trigger map for Shopify Payments or all processors.

Who should approve, review, and release held funds inside a platform team?

This grounding pack does not define a specific internal approver hierarchy for placing, extending, or releasing holds. It only supports that holds or restrictions may be used when more information is needed, so exact ownership and approval flow should come from internal policy.

What should a seller or contractor notification include during a compliance hold?

State the action plainly: that activity is under review and what additional information or documentation is needed. A third-party Stripe-focused example says requests are typically sent by email or dashboard notification. Keep wording aligned to what the case file supports, and avoid implying misconduct when the record only supports "additional information required."

How do you reduce fraud risk without creating avoidable chargeback and pre-arbitration spillover?

This grounding pack does not provide quantified evidence on pre-arbitration spillover. The concrete point available is that multiple refunds, disputes, or chargebacks can delay funds availability, so avoid stronger cross-platform claims beyond that.

What is known and unknown about hold timelines and trigger thresholds from current public guidance?

One concrete platform example is PayPal’s statement that funds are usually held for up to 21 days. PayPal also gives a rolling reserve example of 5% held on a 60-day rolling period. What remains unknown in current public guidance is any reliable cross-platform release SLA or trigger threshold for Stripe, Shopify Payments, or similar ecosystems.

Try a related tool

Fatima covers payments compliance in plain English—what teams need to document, how policy gates work, and how to reduce risk without slowing down operations.

Priya specializes in international contract law for independent contractors. She ensures that the legal advice provided is accurate, actionable, and up-to-date with current regulations.

Sources

- cisa.gov/sites/default/files/2022-11/Insider%20Threat...trusted

- congress.gov/crs-product/R48850trusted

- congress.gov/bill/119th-congress/house-bill/7148/texttrusted

- consumerfinance.gov/data-research/consumer-complaints/search/api/v1trusted

- dodcio.defense.gov/Portals/0/Documents/CMMC/AssessmentGuideL2v2...trusted

- ecb.europa.eu/euro/digital_euro/timeline/profuse/shared/pd...trusted

- fac.gov/assets/compliance/2024-Compliance-Supplement...trusted

- federalregister.gov/documents/2024/12/10/2024-27836/defining-lar...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Positive Pay Controls Check Fraud in Digital Payment Platforms

This list is for compliance, legal, finance, and risk owners who need to use Positive Pay without turning it into a bigger build than the risk justifies. The goal is practical: reduce check and electronic transaction fraud while keeping decisions and approvals auditable across products and bank relationships.

Airline Delay Compensation Payments for Customer Experience and Control

If you are evaluating an `airline compensation payments customer experience delays platform`, split the work into three lanes first: legally owed refunds, discretionary compensation, and outsourced claims recovery. Vendor pages often blur these together, but they lead to different policy choices, ledger treatment, and customer outcomes.

What Is Know Your Artist (KYA)? How Music Platforms Stop Streaming Fraud Before It Starts

So this piece stays practical. You will see where basic identity checks end, where KYA adds real value, and where enhanced review is worth the extra operational load. You will also see a failure mode many teams miss: collecting signals without a clear action path. A flag that does not route to a defined approve, hold, or reject decision is not much of a control.