Quick Answer

Use a confirmed-or-open launch file first. For Chile, verify three items in order: independent-contractor classification, your CMF and Fintech Act boundary interpretation, and documented RUT account handling for payee checks. After that, pick rail paths by segment (bank transfer, international wire transfer, or digital wallet) and assign owners for initiation, retries, and reconciliation. When any core item is still open, keep the market in validation mode.

What to know before paying contractors in Chile#

Your go or no-go for Chile should rest on operational certainty, not a clean API or polished bank UX. Public materials do show that workable payment infrastructure exists. They do not, on their own, resolve key regulatory-boundary and account-control questions for your specific use case.

That matters early. A provider can advertise strong execution and still leave the hardest launch questions unanswered. For example, Vita Wallet's Business API says businesses can "receive and send 100% automated payments 24/7, including weekends and holidays." It also says businesses can send payouts to 50+ countries with accreditation times of up to 1 business day. Banco BICE's Integrated Report 2024 also points to a live fintech environment, including a section titled "Strengthening the Fintech Network and Strategic Partnerships in 2024." Those are useful signals for payment operations in Chile. They are not proof that your contractor model, regulatory boundary, or account-control design is ready.

Before you start#

Before product or GTM treats Chile as committed, build a small evidence pack your team can actually use. At minimum, include:

- the exact public regulatory text your team is relying on

- the provider documentation for the rail you expect to use

- your contractor use case written in plain terms: who gets paid, from where, in what currency, and into what account type

- the payee fields you plan to collect and re-check before payout

The test is simple: each launch-critical assumption should be tagged either confirmed by source text or dependent on counsel interpretation. If you cannot label an item cleanly, it is still open.

Then follow a practical sequence. First, classify the labor model. If the engagement cannot stand up as an independent contractor arrangement, payment architecture is the wrong problem to solve first. Second, define the regulatory edge of your product: what your platform does directly, what a licensed or regulated partner does, and which parts remain unclear from the public excerpts you have. Only then should you lock in payout rails, retry logic, reconciliation, and payee account checks.

A common failure mode is doing this in reverse. Teams see a promising integration path, assume bank-connected payment tooling answers the launch question, and only later discover that contractor classification, consent surfaces, or payee verification rules were never settled. This guide helps you avoid that mistake. It separates what is confirmed from what is still unknown, then walks through a launch order that keeps legal risk, payment design, and operator controls tied to the same decision record.

For a step-by-step walkthrough, see How Platform Teams Pay Brazil Contractors with Pix.

What to confirm before you scope a Chile launch#

Keep Chile in validation mode until you can mark key assumptions as confirmed or not confirmed, with a source and an owner. Market signals can show activity, but they do not validate your contractor payout model on their own.

| Pre-scope gate | State |

|---|---|

| CMF source saved and reviewed | confirmed |

| Counsel read captured for the current product design | confirmed |

| Payout path selected per segment | confirmed |

| Provider fit checked for that route and entity setup | confirmed |

| RUT account handling status recorded | confirmed |

| Operating controls and audit records assigned to named owners | confirmed |

Build a minimum evidence pack first:

- the current CMF publication your team is using

- counsel's read of the Fintech Act for your product boundary

- a plain-language independent contractor use-case memo (who pays whom, from which entity, in what currency, and into what account type)

Use public signals for context, not proof. For example, Banco BICE's Integrated Report 2024 includes sections like "Regulatory Framework" and risk-governance topics, which supports treating regulatory review and controls as core workstreams.

Map payout paths before discussing scale:

- document whether each segment is planned for domestic bank transfer, international wire transfer, or digital wallet

- for each path, record sender entity, currency, destination account type, required payee fields, and fallback path

Assign ownership before scope is committed:

- onboarding checks

- boundaries for tax-filings guidance

- audit records tied to employee-employer relationship risk

Use the same six gates in the table above and keep them binary (confirmed / not confirmed). If any gate remains not confirmed, do not move Chile to committed roadmap scope.

Step 1 classify the contractor model before you choose payment rails#

Decide the worker model before you choose any payout rail. If contractor status is not clearly confirmed for your setup, treat that as a launch blocker and keep Chile in validation mode.

Use a dated classification record for each contractor segment, with a named legal owner and a simple status (confirmed or not confirmed). Keep the file practical and auditable:

- signed contract terms covering scope, deliverables, and acceptance criteria

- statements of work tied to project outputs

- explicit language on who is expected to handle tax filings and Social Security-related obligations

For cross-border cases, ask counsel whether a bilateral Social Security agreement (totalization agreement) applies in your payment corridor. These agreements are designed to prevent dual Social Security taxation by assigning coverage to one country, and a Certificate of Coverage can serve as proof of exemption from foreign Social Security taxes when home-country coverage applies. Treat that document as a Social Security coverage record, not as a substitute for classification analysis.

For Mexico payouts, read Pay Contractors in Mexico With SPEI for Platform Operators.

Step 2 translate CMF and Open Finance into product boundary decisions#

Set your product boundary conservatively until counsel confirms what your exact flow can do under CMF and Fintech Act interpretations. Keep only the narrowest defensible actions in your platform, and route the rest through a licensed partner.

The current material does not include CMF or Open Finance rule text you can implement directly. Banco BICE's Integrated Report 2024 references a "Regulatory Framework" and "Strengthening the Fintech Network and Strategic Partnerships in 2024," which is useful context but not feature-level legal authority. Treat that as a signal to define boundaries carefully, not as support for consent or payment-initiation assumptions.

Draw the line feature by feature#

Do not scope "payments" as one block. Split the flow and assign an owner for each component:

- collecting contractor onboarding data

- collecting payout destination details

- displaying payout status

- accessing financial account data

- capturing user consent tied to bank connectivity

- initiating a payout or payment instruction

If your legal read is still incomplete, stay on the lower-risk side of this list: calculate amounts, run internal approvals, and pass instructions to a partner. Defer features that make your app the place where bank access is granted or where regulated payment actions are initiated until counsel marks that design as confirmed.

Turn Open Finance into UI and API decisions#

Make boundary decisions explicit in product artifacts. For each bank-connected or payout-adjacent feature, keep a four-field register: feature name, customer-visible surface, legal owner, and evidence. If any field is blank, the feature is not launch-ready.

Review consent and initiation surfaces before build. If UI copy or controls imply your app is directly connecting bank data or moving funds, stop and verify legal ownership of that action.

The common failure mode is adjacency creep: payouts expand into bank data retrieval, reusable permissions, and fallback rails before the evidence pack is complete. If you are still validating Chile scope, launch a narrow partner-routed flow first, log each handoff, and defer bank-data or initiation features until interpretation is confirmed.

If you need a practical next step, Browse Gruv tools.

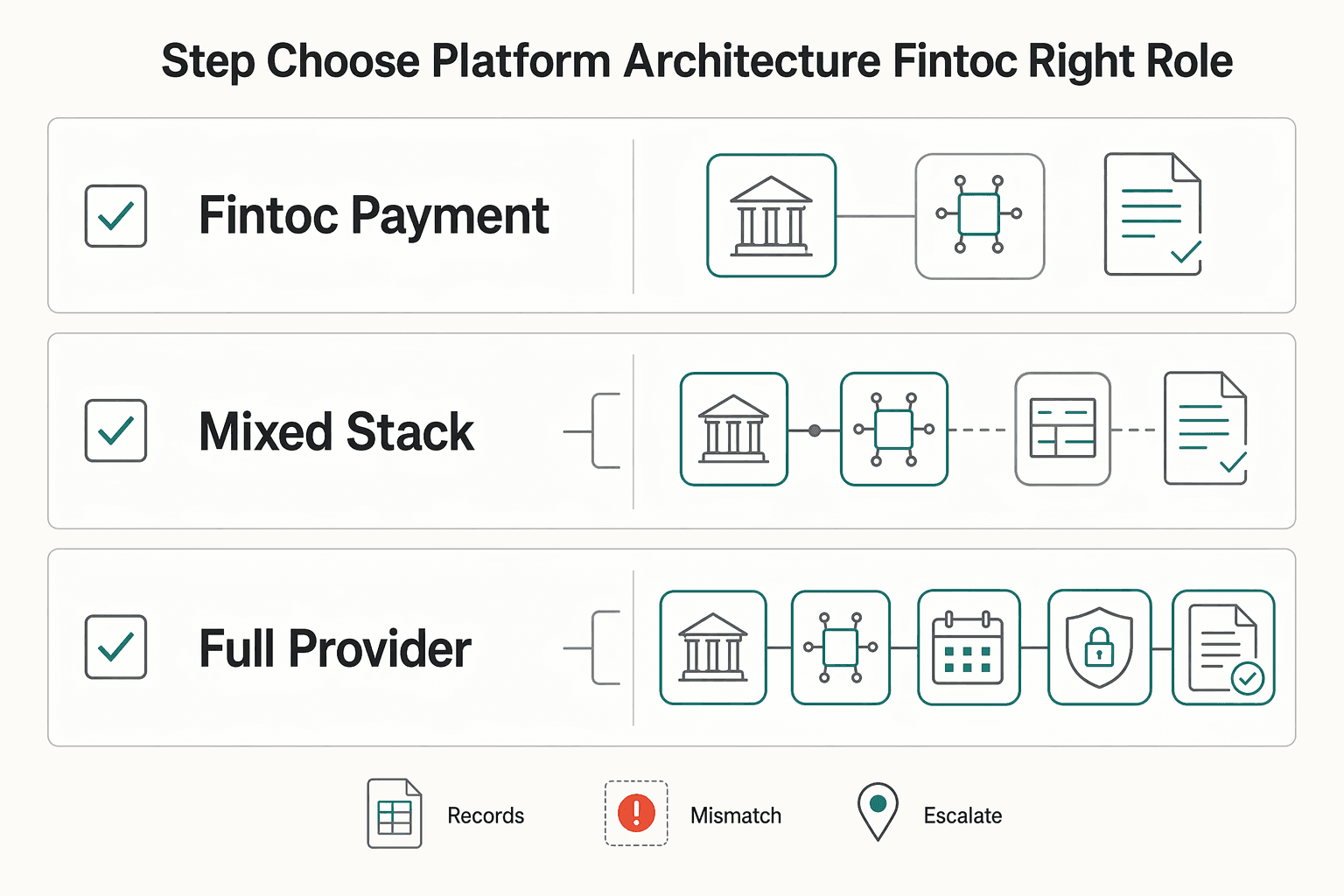

Step 3 choose platform architecture with Fintoc in the right role#

If you need control over routing, retries, and reconciliation, separate bank-facing UX from payout orchestration. The current evidence supports payout-engine capabilities (API, screening, coverage, timing claims), but it does not support assigning contractor compliance ownership to Fintoc or any single provider.

| Architecture option | Best fit | What the current evidence supports | Main risk |

|---|---|---|---|

| Fintoc for payment UX only | You want a bank/card UX layer while payout execution runs elsewhere | The grounding pack does not confirm Fintoc scope details (Paga con tu banco, Tarjeta de crédito o débito, asset standards) | Teams treat UX integration as proof of payout or compliance ownership |

| Mixed stack with separate payout engine | You want to own routing, retries, status mapping, and reconciliation | Vita Wallet docs describe a Business API, restrictive-list screening, 100% automated payments 24/7, and payouts to 50+ countries with accreditation times of up to 1 business day | Boundary errors can create duplicate sends, unclear status ownership, or weak audit trails |

| Full provider-led global payroll software path | You prefer lower internal build effort and accept less control | No grounded evidence here assigns Chile contractor compliance ownership to that provider model | Harder exception recovery and less control over payout logic |

Keep provider roles explicit before build#

Use one architecture sheet with five fields: product surface, who initiates payment, who returns final status, who owns retries, and what document proves each answer. If any field is blank, the design is not ready.

Treat rail choice as a scenario decision, not a default#

For bank transfer, international wire transfer, and digital wallet, choose by contractor segment and exception-handling needs, then verify behavior in provider docs and contracts. The current grounding pack does not provide Chile-specific reliability comparisons across those rails, so treat any rail ranking as a validation task, not a settled fact.

If you are testing wallet fallback for less-banked users, use reaching contractors without bank accounts as the closest design reference. Related: Manufacturing Accounts Payable Automation: How Industrial Platforms Pay Subcontractors and Suppliers.

Step 4 design RUT account and payee verification controls#

Treat RUT accounts and payee verification as an ongoing control surface, not a one-time onboarding check. Until counsel confirms the exact Chile rule set, keep each bank transfer behind repeat verification at payout-critical events and require a documented fallback before launch.

The evidence in hand is narrow: the source pack includes Banco BICE's Integrated Report 2024, a table-of-contents reference to Regulatory Framework, and a package-name listing source that is not payment-control guidance. It does not define RUT validation requirements, profile-versus-destination mismatch procedures, or CMF-specific audit obligations for payee changes.

Use that gap to shape your design:

- Re-check core payee and destination-account fields at payout-critical moments, not only at intake.

- Hold and review cases when profile data and destination-account details do not match before release.

- Make Chile launch conditional if public guidance remains unclear, with counsel-approved handling for unresolved cases.

- Log each payee-change decision with traceable metadata and restrained PII exposure so later review is possible without over-duplicating sensitive data.

We covered related regional control-boundary decisions in How Platform Teams Pay Contractors Across UAE, Saudi Arabia, and Egypt.

Step 5 build payout operations for failures, retries, and reconciliation#

Given the current evidence gap, treat this as an internal control design decision: use one fixed payout sequence, define failure handling before launch, and require a full reconciliation trail for every payout.

The source pack (including Banco BICE's Integrated Report 2024) does not provide Chile-specific retry or reconciliation rules, so keep the workflow explicit, conservative, and provider-agnostic.

Set a strict order before any money moves#

Run each payout in one sequence and do not skip steps for urgent cases:

| Step | Timing | Record |

|---|---|---|

| Payee validation | Before sending | Completed payee check |

| Compliance gate | Before sending | Compliance decision |

| Payout initiation | Before sending | Unique payout instruction ID |

| Provider response capture | After sending | Store raw provider response separately |

| Internal status update | After sending | Keep separate so accepted, settled, and returned outcomes are not conflated |

| Final reconciliation record | Closeout | Link approved payee snapshot, outbound provider reference, and final settlement or return outcome |

Before you send a request, the record should show a completed payee check, compliance decision, and unique payout instruction ID. After sending, store the raw provider response separately from your internal status so accepted, settled, and returned outcomes are not conflated.

Define failures and retries before launch#

Define failure modes in advance, including rejected bank transfer, delayed international wire transfer, unmatched returns, and stale status transitions.

Use idempotent retry keys tied to a single payout instruction. If a request is replayed, return the original attempt or block the duplicate until the first attempt is conclusively failed or reconciled.

Map statuses to actions and ownership#

Use operator-facing states, not raw provider codes. For each state, assign one owner and one recovery action.

A practical minimum is to track states like ready to send, submitted awaiting provider confirmation, requires operator review, returned unmatched, and reconciled closed. Your reconciliation closeout should link the approved payee snapshot, outbound provider reference, and final settlement or return outcome in one traceable record.

Common mistakes that create legal and operational risk#

These controls break down when teams treat unresolved Chile-specific questions as already settled. If labor classification, provider boundary, and account or regulator handling are not documented decisions, launch risk is still open.

Reject copied contractor guidance#

Generic contractor playbooks are not enough for Chile on their own. Do not treat a market-entry memo or provider sales deck as a substitute for a documented local legal review of your contractor model. Before build, keep a record of who reviewed the model, which facts were reviewed, and what would trigger a re-check.

Separate interface comfort from compliance proof#

A clean payment UI, including labels such as Paga con tu banco or Tarjeta de crédito o débito, does not by itself prove end-to-end contractor payout compliance. Keep a boundary memo that states what your team controls, what the provider controls, and who owns each check. Without that memo, operators can assume controls are covered when they were never assigned.

Lock account and regulator assumptions before first payout#

Treat RUT account handling and CMF or Open Finance scope as launch decisions to confirm, not background context. Write explicit rules before the first live payout for required data, mismatch blocks, override authority, and evidence stored with each payout instruction. Patching these rules after failures usually creates inconsistent exceptions that are difficult to unwind.

Related reading: Self-Billing Invoices for Platforms That Pay Contractors.

Conclusion and copy-paste launch checklist#

Do not launch Chile because the story sounds plausible. Launch only when each open issue has written evidence or an explicit approved limitation. If any core item is still marked unknown, keep Chile in validation mode.

One useful discipline is to separate legal interpretation from operating controls. Even in Banco BICE's Integrated Report 2024, the table of contents points to a Regulatory Framework and a Risk Management Model. Your internal launch file should look similar: one section for what you believe is allowed, and one section for how your product, provider, and ops team will keep payouts inside that boundary.

Copy-paste launch checklist#

| Open item | Verification point |

|---|---|

| Contractor classification status | A dated memo or approval note exists, segmented by use case, with a named owner for re-review if role design changes |

| CMF/Open Finance product-boundary requirements | One page clearly states who owns consent surfaces, payout initiation responsibility, and boundary-adjacent controls, with approvals attached |

| RUT account requirements and fallback policy | Payee-change policy, mismatch rules, and override authority are documented with an audit trail |

| Rail decision framework and fallback logic | The launch file shows intended path, fallback trigger, and closure evidence for rejection or delay scenarios |

| Fintoc's launch-architecture role | Provider docs, terms, and implementation notes are attached with a plain-English responsibility split |

| Idempotent retries, failure handling, and reconciliation readiness claims | Sample logs, retry identifiers, and reconciliation records are available and reviewable before first live payout |

- Contractor classification status is unverified in these excerpts.

Keep this as an explicit open item until your own legal review is documented by segment. Verification point: a dated memo or approval note exists, segmented by use case, with a named owner for re-review if role design changes.

- CMF/Open Finance product-boundary requirements are unverified in these excerpts.

Treat boundary assumptions as unresolved until counsel or provider confirmation is documented. Verification point: one page clearly states who owns consent surfaces, payout initiation responsibility, and boundary-adjacent controls, with approvals attached.

- RUT account requirements and fallback policy are unverified in these excerpts.

Do not present this as settled in onboarding or launch docs until confirmed. Verification point: payee-change policy, mismatch rules, and override authority are documented with an audit trail.

- Rail decision framework and fallback logic are unverified in these excerpts.

Keep route-by-segment choices in validation status until tested and approved. Verification point: the launch file shows intended path, fallback trigger, and closure evidence for rejection or delay scenarios.

- Fintoc's launch-architecture role is unverified in these excerpts.

Avoid implied compliance ownership or capability claims without explicit documentation. Verification point: provider docs, terms, and implementation notes are attached with a plain-English responsibility split.

- Readiness claims for idempotent retries, failure handling, and reconciliation are unverified in these excerpts.

Keep these as pre-launch validation items, not completed controls. Verification point: sample logs, retry identifiers, and reconciliation records are available and reviewable before first live payout.

The common failure is not a single bad rule. It is drift: legal thinks the provider owns a control, product thinks ops owns it, and ops finds out during the first payout exception. A strong final check is simple: hand the launch file to an operator who was not in the design meetings. If they cannot tell you what blocks release, who can override it, and what artifact proves the payout is resolved, you are not ready.

For a broader cross-border playbook, read How to Pay International Contractors With Fewer Delays and Disputes.

Frequently Asked Questions

What are the minimum table-stakes to pay contractors in Chile compliantly as a platform?

From the excerpts here, there is no confirmed Chile-specific minimum checklist for compliant contractor payouts. What is confirmed is provider capability: Vita Wallet’s Business API describes 24/7 automated payments, AML restrictive-list screening, and payouts to 50+ countries with accreditation times of up to 1 business day. Treat contractor classification, verification, and payout-control requirements as unresolved until they are documented in current Chile legal guidance and your provider terms.

What misclassification penalties are cited for getting contractor status wrong in Chile?

The current excerpts do not support any specific Chile misclassification penalty amounts, thresholds, or statutory consequences, so do not present a number as settled. The practical move is to get Chile labor counsel to write down the exposure categories and the facts that would trigger a re-review. If you cannot get that memo, treat the contractor model as unresolved rather than estimating risk from generic guides.

Does `CMF` Open Finance regulation directly change contractor payout platform design?

From the excerpts here, no direct CMF Open Finance obligation for contractor payout design is confirmed. That means you should treat data access, consent surfaces, and payout initiation responsibility as open design questions until you have a current legal read. Do not assume the regulatory boundary is settled based on this record alone.

What does `Fintoc` solve in Chile, and what does it not solve for contractor payouts?

These excerpts do not establish any confirmed Fintoc product scope, rail coverage, or compliance responsibility, so you should not assign it a payout or legal role based on this record alone. In practice, ask for current product docs, service terms, and a written responsibility split before treating it as part of your payout stack. If that package is missing, keep Fintoc in the “not confirmed” column.

What is still unknown about `RUT accounts` requirements from current public excerpts?

A lot. The excerpts do not validate a public rule for RUT account requirements, which means you cannot rely on them to define what account data is mandatory, how ownership must be checked, or which mismatches are acceptable. The operator response is to launch only with counsel-approved handling rules, plus stored evidence for overrides and payee edits.

When should a platform use `bank transfer` vs `international wire transfer` vs `digital wallet` for Chile contractors?

The current record does not support a Chile-specific rule for choosing one rail over another, so avoid hard recommendations dressed up as local fact. Make the choice only after you confirm contractor location, destination account type, return and reconciliation handling, and provider coverage. For example, Vita Wallet’s Business API says it supports payouts to 50+ countries, 24/7 automated payments, AML list screening, and accreditation times of up to 1 business day, but those are provider capabilities, not proof that a given rail is the right Chile design.

Try a related tool

Sarah focuses on making content systems work: consistent structure, human tone, and practical checklists that keep quality high at scale.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- ssa.gov/international/CoC_link.htmltrusted

- ssa.gov/international/agreements_overview.htmltrusted

- cdn.sourcecode.ai/pypi_datasets/01.11.2020/package_list.txtexternal

- docs.vitawallet.ioexternal

- pdfcoffee.com/url-4-pdf-free.htmlexternal

- static-sitio-publico.bice.cl/memorias/BICE_Integrated%20Report%202024_ENG...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Paying Unbanked Contractors in Developing Markets: Best Payout Routes for Platforms

If your team needs to send money to contractors, creators, freelancers, marketplace sellers, or other non-payroll recipients across borders, the payout decision can look deceptively simple at first. On paper, you are choosing a payment rail. In practice, you are choosing an operating model that affects onboarding, compliance, support load, engineering effort, treasury visibility, failure recovery, and the degree of legal risk your company is willing to carry.

How Staffing Platforms Automate Healthcare AP for Clinical Contractors

A key distinction matters: the material reviewed here focuses on healthcare AP workflows, not contractor-payout orchestration. If your expansion bet depends on reliable contractor payments, generic healthcare AP language is useful context, but it is not enough on its own.

Manufacturing Accounts Payable Automation for Industrial Platforms Paying Subcontractors

Industrial finance teams do not need another feature checklist. They need a clear way to decide what belongs inside AP automation, what belongs in payout infrastructure, and what needs to stay tied to ERP and production controls so payables do not create downstream delays.