Quick Answer

Use a split model for Nordic payment platform compliance: one shared control core for ISO 20022 data quality, traceability, and approvals, plus a country variance register for Sweden, Norway, Denmark, and Finland. Escalate legal review before launch when a change could alter disclosures, reporting behavior, or payout eligibility, and keep dated rulebook and scheme references with every control decision.

What Changes Across the Nordic Markets#

Nordic payment platform compliance is a control-design problem, not just a standards exercise. The region is moving toward shared schemes and rulebooks, but legal and operational execution is still uneven at country level.

There is a shared direction. The Nordic Payments Council states a mission to harmonize payments across the Nordics through common rulebooks and standards, with a vision of one Nordic payment area aligned with SEPA. Read that as convergence on data and scheme practice over time, not proof that Sweden, Norway, Denmark, and Finland already operate as one compliance jurisdiction.

That distinction prevents expensive mistakes. Shared scheme messaging or a "Nordic-ready" bank implementation may support processing, but it does not by itself show that local duties are aligned. The cited NPC scheme scope here is also narrower than many teams assume: DKK, NOK, and SEK. If your platform touches Finland, make that a separate checkpoint instead of assuming controls transfer automatically.

In practice, split your model early: keep a common core for structured payment data, evidence capture, and exception handling. Then maintain a country-variance layer for customer treatment, payout eligibility, and legal interpretation. Teams that collapse those layers too early can end up in one of two bad places. They may overbuild approvals for low-risk flows or rely on a thin regional control set that may fail under audit or incident review.

Timing risk matters too. One cited transition snapshot reports no NCT scheme participants yet and estimates first participants in 2027. A later snapshot reports 74 NCT Inst participants as of September 2025, with 54 DKK and 20 SEK. Do not write policy as if every Nordic corridor, bank, and scheme is already live and equivalent.

Use a simple verification habit: for each market, record the exact rulebook or scheme artifact your control relies on, and date-stamp it. For NPC governance artifacts, version control is part of the job: Scheme Management Rules v1.3 is effective 20 November 2024, and it removed the requirement for a board decision to approve scheme adherence applications.

Finally, treat compliance-labeled scheme features as inputs, not substitutes for your controls. NPC transition messaging references a VOP scheme live in October 2025 as a compliance tool. It should inform your design, not replace market-level control decisions.

If you want a deeper dive, read How to Expand Your Subscription Platform to Europe: Payment Methods Tax and Compliance.

Define the terms before you design controls#

Start with source-document definitions. Each control should point to a specific artifact and use that artifact's defined terms, not team shorthand.

The strongest grounded source here is NPC Scheme Management Rules (NPC900-01), Version 1.3, issued and effective 20 November 2024. NPC frames this as internal rules for NPC Scheme Management, including administration, compliance, maintenance, development, and change management. If you rely on NPC artifacts, write controls in rulebook language.

Use Chapter 5 as a drafting checkpoint because it consolidates defined terms. The rulebook also warns that similar terms may not always match meanings used in payment law, so reusing a familiar term without checking the definition can misstate the obligation.

Apply the same discipline to labels like P27, ISO 20022, ISO 20022 XML, and Verification of Payee (VOP). Treat those as dependencies to validate against actual scheme, bank, or legal text, not complete legal or control definitions.

- Verification check: for each control statement, record the source artifact, version, and date used, for example

NPC900-01 v1.3, effective20 November 2024. - Evidence check: store the quoted definition or chapter reference with the control record, especially for capitalized terms.

NPC governance also includes a documented major rulebook change process. If your controls rely on NPC terms, build in an update and approval path, not just first-time implementation.

For a step-by-step walkthrough, see How to Build a Compliance Operations Team for a Scaling Payment Platform.

What is genuinely common across the Nordics today#

The strongest common ground here is operational, not legal. Standardize shared data, traceability, and partner controls, but do not assume Sweden, Norway, Denmark, and Finland already function as one harmonized compliance market.

What the evidence supports#

The clearest common pattern is partnership-led infrastructure. Lunar is described as a fully digital Nordic bank serving Denmark, Norway, and Sweden. Wise says its white-labelled solution is available to Lunar's private and business users in those three countries through Moonrise for local clearing and payments across Scandinavia.

| Entity | Stated fact | Countries/date |

|---|---|---|

| Lunar | Described as a fully digital Nordic bank | Denmark, Norway, and Sweden |

| Wise / Moonrise | White-labelled solution available to Lunar's private and business users; local clearing and payments across Scandinavia; direct connections to six domestic payment systems; over 70 licenses worldwide | Denmark, Norway, and Sweden |

| Nordea | Reports recognition across all four Nordic countries | 12-09-2025 |

Wise also ties performance and reach to concrete implementation factors, including direct connections to six domestic payment systems and over 70 licenses worldwide. That is useful for control design because it points to what you should verify in partner due diligence: actual network access, licensing footprint, and named country coverage.

Another practical signal is regional operating presence. Nordea reports recognition across all four Nordic countries on 12-09-2025. Treat that as evidence of cross-country digital-channel operations, not evidence that legal duties are harmonized.

What to standardize first#

Start with one core control model, then localize where country-level requirements or interpretations diverge. Use one internal payment object and one shared evidence structure for:

- payer and payee identity fields

- remittance and reference fields

- timestamps, status transitions, and provider references

- fee and FX disclosure fields

- exception reasons and manual-review outcomes

When a provider says "Nordics," confirm the exact country list before rollout. The evidence names Denmark, Sweden, and Norway, not Finland.

Operator rule to reduce rework#

Default to one common control design with a visible country-variance register. For each "common Nordic" assumption, log the source artifact, date, and exact countries covered. Also keep evidence for how fees and delivery timing are presented to users, since unclear pricing and timelines are explicitly tied to trust risk.

That common core only works if you are equally clear about where it stops. The next step is to make country differences explicit before they become production assumptions.

Where country differences still drive real risk#

The main risk is treating Nordic modernization as legal harmonization without confirming that assumption country by country. Keep a live country matrix with three buckets: what is confirmed shared, what is country-specific, and what is still unknown pending counsel.

P27 is a practical example of why this matters: one account places the initiative's withdrawal in April 2023 after work since 2018, while another describes a first-transaction target in 2021. That conflict creates rollout risk, not just a documentation issue.

Use a country matrix as a decision record#

| Country | Confirmed shared | Country-specific | Unknown pending counsel |

|---|---|---|---|

| Sweden | Cross-border execution still faces operational and regulatory friction; local legal review is still needed | Active future work is cited around the Bankgirot clearing system and Sweden domestic-payment solutions; Sweden is described as rapidly developing | Whether transition changes affect disclosures, payout eligibility, reporting behavior, or local product handling |

| Norway | Cross-border frictions remain in the region; do not treat Nordic initiatives as completed legal harmonization | Confirm Norway-specific migration details with your provider | Domestic clearing impacts, customer notice duties, reporting behavior, and bank-specific cutover assumptions |

| Denmark | Cross-border frictions remain; local legal review is still needed | Described as a rapidly developing market | Domestic rule changes, local clearing impacts, disclosure effects, and partner-specific migration obligations |

| Finland | Cross-border frictions remain; local legal review is still needed | Described as at a nascent stage of development | Domestic implementation timing, local legal effects, and payout or reporting consequences |

If partner and legal confirmation is missing, mark the item as unknown rather than promoting it to shared.

Sweden is the clearest local checkpoint to verify#

The strongest country-level signal here is Sweden-specific Bankgirot future-solution work after the P27 setback. Use that to justify a Sweden variance entry, but do not project Sweden timing or legal effect onto Norway, Denmark, or Finland.

Treat network labels as routing clues, not legal conclusions#

References such as SEPA, T2, SWIFT, or SWIFT CBPR+ can help identify rails and processing context, but they do not replace country-level legal review. The grounded evidence also notes that some cross-border payments still run over SWIFT. In the cited context, they can take 3 to 5 business days, so product promises should not rely on network labels alone.

Escalate based on customer impact#

Use a clear rule before deployment: escalate to legal review if a change affects customer disclosures, withholding or reporting behavior, or payout eligibility. If a migration claim lacks a country-specific artifact and a named reviewer, keep it out of production logic and leave it in "unknown pending counsel."

Once the country matrix is in place, you can place controls where they matter most: at the point in the payment lifecycle where a bad decision can still be stopped, corrected, or explained.

Place controls by lifecycle stage instead of by regulation name#

Design controls by lifecycle stage, not regulation label, so each control sits where a payment can still be stopped, corrected, or explained. Use the country matrix from the prior section as a constraint layer, then map each stage to two anchors: the data you need and the route you assume.

For data, treat payment-message quality as an operational dependency. For routing, treat shared-infrastructure assumptions as assumptions to validate, not proof that country-level duties disappeared.

| Lifecycle stage | Primary control question | Data or routing dependency | Red flag |

|---|---|---|---|

| Onboarding | Should this customer or payee be allowed to receive payouts? | Identity evidence, KYC/KYB outcome, sanctions result, country variance note | Payout activation before corridor and entity checks are complete |

| Funding | Is the source of funds and balance state clear enough to proceed? | Funding reference, currency, amount, account mapping | Funds move without a traceable source event |

| Conversion | Can FX or amount transformation be explained later? | Original amount, converted amount, rate source, ledger mapping | Posted amount cannot be tied back to request plus conversion event |

| Payout submission | Is the request complete, approved, and non-duplicate? | Parseable payment message, approval record, idempotency key, assumed route | Missing or malformed fields reach live submission |

| Reconciliation | Can external status be matched to internal ledger movement? | Provider reference, network reference, status transitions across payout paths | Conflicting references or unmatched ledger posting |

| Post-event investigation | Can ops or compliance reconstruct the flow end to end? | Event chain from request to posting, manual notes, case record | Team cannot explain failure in one trace |

Onboarding needs a hard activation gate#

Keep onboarding gates consistent across Sweden, Norway, Denmark, and Finland: KYC/KYB decision, sanctions screening, and identity evidence review before payout activation. Do not assume one shared evidence list, legal threshold, or activation rule across all four countries unless counsel has confirmed it.

The World Bank framework is useful here as an operating pattern, not Nordic legal guidance. It separates "CDD/KYC Credential Issuance through TACH" from "Confirmation/Verification of Payee." That distinction helps prevent activation of payouts when the party is onboarded but payee verification is still unresolved.

Use a corridor-level activation check: one named approver, one evidence bundle, one country variance note. If a provider's "Nordic" scope is inconsistent, treat coverage as unverified until resolved.

Submission controls should catch bad data before the rail does#

Submission controls should stop incomplete or conflicting requests before they leave your platform. Use idempotent payout creation to prevent duplicate execution on retries, and keep approvals tied to the payment record.

If required payment-message data is missing, unparseable, or inconsistent with the request, route the payment to an exception queue instead of pushing it to live rails. Preserve the rejected payload, validation output, override identity, if any, and hold reason so the control is defensible later.

Reconciliation and investigation prove whether the design works#

Back-half controls are where you find out whether the design is actually reliable. References may diverge across payout paths, and there is no confirmed single Nordic case-management rule to resolve every conflict, so define internal ownership and handling explicitly.

At minimum, keep request payload, provider or network references, status transitions, ledger postings, and human interventions in one linked case record. Use one hard test: if your team cannot explain a failed payout from request creation to final ledger posting in one trace, the control design is incomplete.

Use ISO 20022 field quality as a compliance control#

Treat ISO 20022 field quality as a pre-submission control, not a formatting step. If identity, address, or payment-purpose data is unclear, reject or hold the payment before it reaches screening, routing, or reconciliation.

In practice, that means strict validation for payment-type, channel, and version-specific ISO 20022 XML fields, with fail-fast rules for defects that would weaken sanctions screening, break traceability, or create avoidable manual review.

Validate by field family and by route#

Define validation by payment type, bank channel, and message version. Channel coexistence is still real. Nordea states Corporate eGateway maintains ISO 2009 while accommodating new address requirements. It also says pain.001 and pain.002 version 2019 messages have been available for Corporate Access users since November 2025.

| Field family | What to check before send | Downstream control outcome | Fail-fast trigger |

|---|---|---|---|

| Payer and payee identity | Name present, entity or individual formatting consistent, account-holder data not contradictory, route-specific identifiers present when required | Stronger sanctions and fraud screening quality | Reject or hold when identity fields are missing, conflicting, or clearly truncated |

| Address elements | Address format matches route rules, and where addresses are used they are structured or hybrid, not a single unstructured line | Lower reject risk and clearer screening data | Hard hold when an in-scope payment still carries an unstructured postal address |

| Remittance and payment reference | Reference present, parseable, and linked to internal payment ID or invoice object | Better reconciliation and less manual investigation | Hold when remittance cannot tie back to the originating request |

| End-to-end references | UETR or other route reference present where applicable | Better traceability across payment processing events | Hold when reference chains are broken before submission |

Address controls deserve a hard gate. Starting 15 November 2026, banks and clearing systems will no longer accept cross-border, SEK, and SEPA payments containing unstructured postal addresses where addresses are used. For Danish payments, Nordea states these address changes come into force in the first half of 2027.

Map defects to business impact#

Map each validation rule to one operational consequence, not just a schema error. Incomplete payee identity is a screening-confidence issue. Malformed remittance is a reconciliation issue. Missing address components that force analyst intervention are a manual-review issue.

This keeps ownership clear across teams. Compliance sees screening risk, engineering sees parser and channel defects, and finance sees unmatched postings.

Make the dashboard shared and version-aware#

Use one shared defect dashboard across compliance, engineering, and finance, segmented by channel, message version, rail, and bank. Aggregate defect rates can hide concentrated problems in one channel or corridor.

Run a weekly verification sample of held and accepted payments to confirm accepted traffic actually includes the structured or hybrid address data, identity fields, and reference chain your downstream controls depend on. If a critical defect makes a payment hard to screen, hard to trace, or likely to bounce, do not push that uncertainty into CBPR+ or SEPA. Reject or hold it with payload, validation output, route, channel or version, and reviewer notes attached for later review.

Field quality is only one part of the move. The next risk is migration itself, especially when external timelines look cleaner than real rollout conditions.

Related: Music Royalty Tax Compliance: How Platforms Handle 1099-MISC vs. 1099-NEC for Artist Payments.

Sequence migration to reduce legal and operational surprises#

Sequence migration in evidence-based phases, not one big cutover. The Nordics are highly digitalized, but payment behavior and infrastructure models still vary across countries, and those differences are tied to available solutions and banking structure.

Phase the move around control evidence#

Use a phased sequence that lets you stop when assumptions break and verify each step before widening scope:

| Phase | Main task | Grounded detail |

|---|---|---|

| Inventory rails and dependencies | Map active payment paths | By country, bank partner, channel, message type, and control owner; separate common solutions from country-specific logic |

| Map process deltas | Document what changes between current and target flows | Include who provides key data and how rejects or returns are handled |

| Run limited parallel testing | Test a narrow set first | Compare acceptance, rejection, reconciliation, and investigation effort across old and new paths |

| Cut over in controlled slices | Move one corridor or segment at a time | Use explicit rollback criteria and a named approver |

| Review post-cutover exceptions before expanding | Check early issues before widening scope | Review early rejects, delays, unmatched postings, and manual cases |

If you align internal planning with external migration programs, treat those milestones as planning inputs, not proof that country obligations or bank behavior have converged.

Keep Sweden assumptions explicit#

In Sweden, make assumptions about bank participation and operating flows visible in your mapping. Even where common solutions are widespread, country setup can still differ, so investigations and reconciliation can depend on different operational handoffs.

Pause expansion when rollout signals conflict#

If vendor, bank, and internal legal or compliance views do not align, pause scope expansion and re-validate current status with banking partners and counsel before go-live. Cross-border differences in digitalization and operating context can materially affect businesses, so use a current evidence pack before approving the next phase.

A phased rollout only helps if teams know how to react when something breaks. That is why escalation rules need to be set before incidents force improvised decisions.

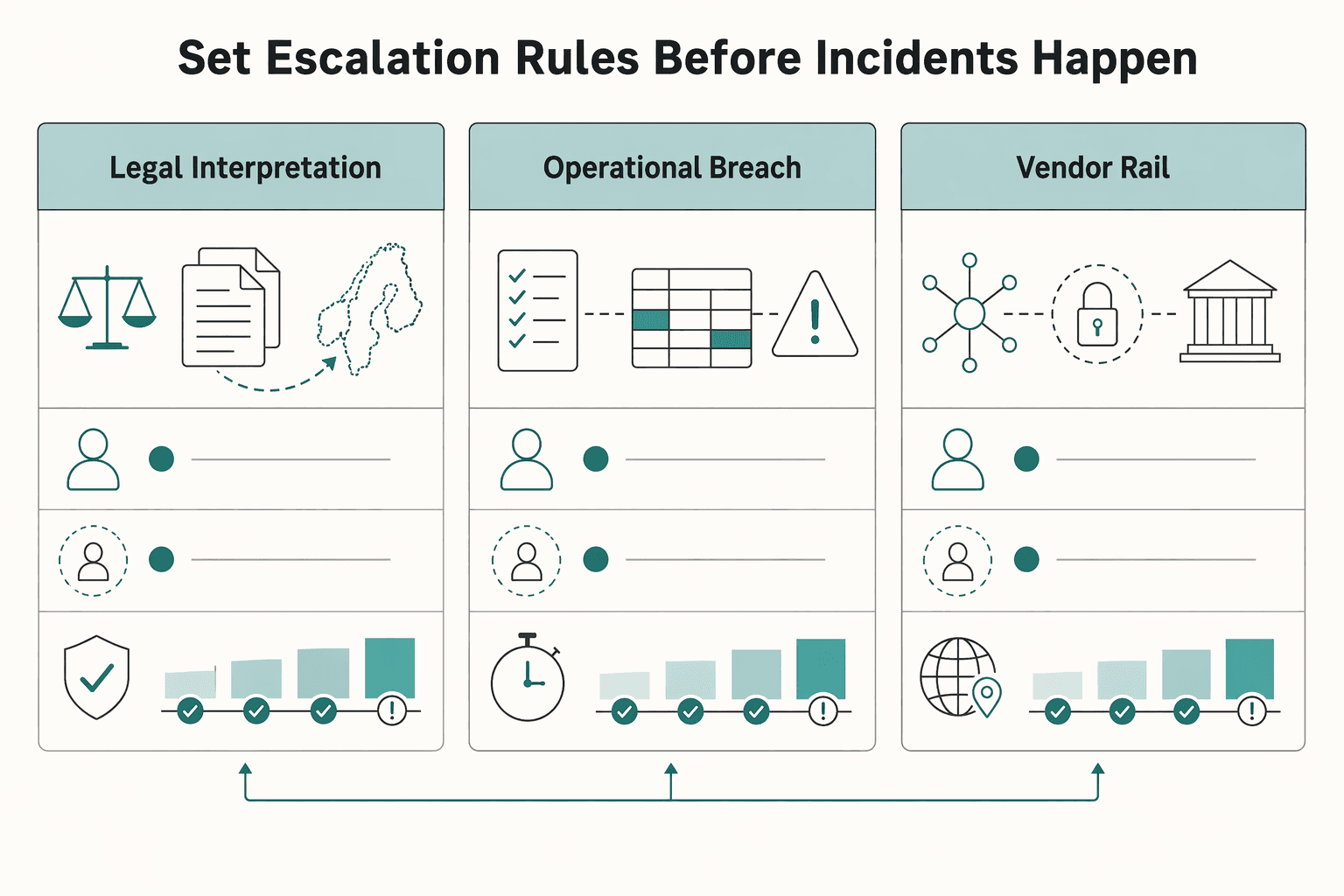

Set escalation rules before incidents happen#

Before volume expands, write escalation rules that separate legal or compliance interpretation from execution failures and concentration outages. Define three lanes in advance: legal interpretation, operational breach, and vendor or rail outage, each with a named owner, backup owner, and severity-based response SLA.

| Escalation lane | Trigger | Primary owner | Minimum evidence to attach |

|---|---|---|---|

| Legal interpretation | A control decision could change how cross-border payments are handled or how AML/CFT risk is treated across Nordic markets | Legal or compliance | Affected markets, affected product or flow, current control, proposed change, impacted customer or payment set |

| Operational breach | The failure is executional, such as rejects from data defects, processing errors, or status/ledger mismatches | Payments operations | Raw request, provider response, status history, ledger impact, sample failed transactions |

| Vendor or rail outage | A provider, processor, or rail is unavailable, delayed, or inconsistent across corridors | Incident manager with vendor owner | Provider notice, affected corridors, start time, fallback path, customer impact estimate |

Use the legal lane early when a decision could change cross-border payment handling or AML/CFT treatment in Nordic flows. Do not treat a policy question as an ops workaround.

Route execution failures to payments ops first. A practical checkpoint is whether you can trace one failed payment from request to provider status to ledger posting without gaps. If you cannot, treat it as an operational breach and preserve evidence before manual retries.

Keep outage escalation separate from routine ops noise. Nonbanks can operate across multiple points in the processing chain, and disruptions at key providers can create wider impact than a single failed transaction set.

Escalation is easier when the underlying record is already in place. That record should be built for real operation, not reconstructed after the fact.

Related reading: KYC Best Practices for Reducing Money Laundering Risks: A Payment Platform Compliance Guide.

Build the evidence pack regulators and auditors will ask for#

Build this as a live operating record. You should be able to show what you decided, what changed, and what happened on a payment without rebuilding the story later. Treat this as your internal minimum evidence baseline, not as a claim about what any single Nordic authority mandates.

Keep five records current together in one operating set:

| Record | What it should prove | Common gap |

|---|---|---|

| Control inventory | Which control exists, where it sits in the payment lifecycle, and who owns it | Policy-level descriptions not mapped to a real stage or team |

| Change log | What changed, why, who approved it, and when it took effect | Release notes with no compliance rationale |

| Country variance register | What is shared across Sweden, Norway, Denmark, and Finland, and what is local or unclear | Local differences buried in email threads or vendor calls |

| Incident log | What failed, when, on which corridor, and how customers or funds were affected | Incidents tracked as ops noise with no control linkage |

| Remediation record | What fix was chosen, how it was tested, and what follow-up evidence was collected | "Resolved" status with no proof the issue stayed fixed |

If a control depends on an assumption or interpretation, record that dependency explicitly. This matters most when teams rely on external standards or market guidance that can be interpreted differently. If guidance is still unclear, keep a documented "known unknowns" list with a named owner and review cadence.

At transaction level, store enough evidence for an end-to-end replay on each payout path: request payload, provider reference, status transitions, and reconciliation outcome. Do not overwrite history when references change across routes. Older systems can flag suspicious activity with no context, so your pack should preserve the context needed to explain the alert.

Stamp each legal, rulebook, or market-guidance reference with a clear "reviewed as of" checkpoint. Point-in-time materials can be authoritative yet presented as unofficial, and they can change over time, so your file should show exactly what version your team relied on. Also log the correct interpretation owner when publisher channels cannot answer content questions.

Use a periodic trace test as an internal verification checkpoint: walk one case per active corridor from onboarding decision to payout completion. If an independent reviewer cannot explain control basis, transaction path, and reconciliation outcome from the record alone, the pack is not audit-ready.

For audit logging and transaction records, read What Is an Audit Trail? How Payment Platforms Build Tamper-Proof Transaction Logs for Compliance. If you need an implementation reference for idempotent payout handling, status tracking, and audit-ready records, review the Gruv docs.

Common failure modes that waste effort and increase risk#

A costly failure mode is treating harmonization progress as if country obligations are already aligned. That turns a strategy assumption into a control decision without proof. A practical check is to keep per-country checkpoints. Even in the ECB's sixth AMI-SeCo monitoring exercise in 2025, compliance was still tracked per market, and single-rulebook work was explicitly continuing into 2026.

Another common miss is managing to migration milestones while ignoring message and data quality defects. A flow can look live and still produce weak monitoring outcomes. Keep the control tradeoff explicit: false positives drive operational waste, and false negatives increase legal and financial risk.

A third failure mode is treating vendor claims as compliance evidence. "Ready" or "compliant" statements are inputs to your assessment, not proof of control effectiveness. Require your own documented review, including document analysis, implementation interviews, and stakeholder surveys or dataset checks before approval.

The last pattern is overbuilding one global process when unmanaged country variance is the real issue. Use a country variance register to separate shared controls, local exceptions, and unresolved points. If a "standard" process depends on side emails, bank-specific caveats, or manual workarounds, document that variance and assign ownership instead of treating it as harmonized.

Those failure modes are easier to fix early. In the first month, focus on making decisions visible and traceable rather than trying to finish the whole model at once.

First 30 days to operationalize the comparison#

In the first month, prioritize control evidence over a perfect end state. The practical goal is to stand up four working artifacts that make decisions traceable, ownership clear, and unresolved points explicit.

| Week | Primary action | Grounded checkpoint |

|---|---|---|

| Week 1 | Publish a variance matrix | Each row includes requirement or assumption, status, market impact, legal owner, operations owner, evidence link, and decision date |

| Week 2 | Define message-field validation and exception routing | Every failed validation creates an exception ticket; every ticket has an owner; every disposition has a timestamp and reason code |

| Week 3 | Dry-run one high-risk payout corridor end to end | Confirm trace from request to final status and reconciliation outcome; run one operational defect scenario and one legal-interpretation scenario |

| Week 4 | Finalize an executive checklist | Controls live, evidence pack complete, unresolved legal questions logged, non-compliance escalation path confirmed, and next review date set |

Week 1#

Publish a variance matrix for the in-scope markets with clear owners and explicit unknowns. Keep each row simple: requirement or assumption, status, market impact, legal owner, operations owner, evidence link, and decision date.

Close each row as one of three outcomes: confirmed shared, market-specific, or unknown pending counsel. If an item could affect customer eligibility, disclosures, or payout handling, assign a named legal owner and prevent silent rollout until a decision is logged.

Record meeting outputs as decision notes or "jointly decided minutes" style documentation. Use those records as governance evidence, not as legally binding language.

Week 2#

Define mandatory message-field validation and exception routing with measurable acceptance criteria. The core control is not perfection on day one. It is a clear rule for what is rejected, held, or passed with monitoring.

Use objective checks: every failed validation creates an exception ticket, every ticket has an owner, and every disposition has a timestamp and reason code. If the team cannot explain why a malformed record was released, held, or corrected, the control is not operational.

Watch for fragmented tooling between payment creation, screening, and reconciliation. If validation is in one system and exceptions are handled in email, fix that gap before scaling volume.

Week 3#

Dry-run one high-risk payout corridor end to end with full traceability. Use provider references from that flow and confirm you can trace from request to final status and reconciliation outcome.

Run escalation drills in the same exercise: one operational defect scenario and one legal-interpretation scenario. The pass condition includes clear escalation ownership, logged decisions, and explicit non-compliance handling, not just payment completion.

Use a simple pass or fail check tied to the trace itself:

- Can you reconstruct the event sequence from request payload, provider reference, status changes, and reconciliation result?

- Can you show who approved each exception and where that approval is stored?

If the answer to either question is no, pause expansion and close traceability gaps before moving further.

Week 4#

Finalize an executive checklist that is short, binary, and reviewable: controls live, evidence pack complete, unresolved legal questions logged, non-compliance escalation path confirmed, and next review date set.

Build the evidence pack from the month's working artifacts: current variance matrix, decision notes, validation rules, exception samples, dry-run outputs, and open-issues log. Keep the governance distinction clear: a checklist shows disciplined management, but it does not by itself settle the legal position.

Conclusion#

The practical answer is a split model: keep one shared control core, and make variance plus escalation ownership explicit. That is usually the difference between controls you can defend and controls you only hope are right.

Your shared core should cover message quality, traceability, approval evidence, incident logging, and change control. Your variance layer should record where local interpretation may differ, where interpretation is still unclear, and who can approve a temporary position.

A reliable anchor is the Nordic Payments Council Scheme Management Rules. Version 1.3, effective 20 November 2024, explicitly covers administration, compliance, maintenance, and change management. Use that governance shape in practice: keep a dated record of the rule or guidance you relied on, classify the issue in your change process, attach your impact analysis, and retain the approval trail.

Do not overcorrect in either direction. If you standardize too aggressively, you can remove local review before the facts support it. If you treat every market as custom, you create a process few teams can run consistently. Standardize controls for data quality, execution integrity, and evidence retention, then localize the points where legal meaning or market practice may change.

If a term in NPC material looks familiar, do not assume it maps cleanly to Payment Services Directive usage. The NPC rules explicitly warn that terms may not always correspond in meaning, so treat that as a legal-escalation trigger in your process.

One final caution: better analytics do not automatically reduce compliance work. Signal quality can improve while review demand still rises, so assign clear ownership for tuning, exceptions, and review load.

If you keep only one operating rule, make it this: one core, explicit variance logging, and a named sign-off owner for every unresolved point. When you are ready to validate local controls and escalation ownership in your payout flow, talk to Gruv.

Frequently Asked Questions

What does Nordic payment platform compliance mean in day-to-day platform operations?

In day-to-day operations, it means running one shared control core while keeping country differences explicit across Denmark, Finland, Sweden, and potentially Norway. Confirm which scheme or rail you are using, validate participation and message assumptions before launch, and log exceptions, approvals, and unresolved legal points. If you cannot show why a payment was accepted, held, or rerouted, the control is not operating reliably.

Is ISO 20022 only a technical messaging upgrade?

No. Treat it as an operations and control question, not just a format question. NPC material states Inter-PSP implementation guidelines are mandatory while Customer-to-PSP guidance is recommended, so do not assume customer-originated data will be as consistent as inter-PSP data.

Does P27 eliminate country-specific compliance obligations in Sweden, Norway, Denmark, and Finland?

No. P27 is described as a pan-Nordic initiative, but that does not equal full legal harmonization, and the cited scope is Denmark, Finland, Sweden, and only potentially Norway. Sweden-specific infrastructure still matters in practice, including Bankgirot as the incumbent real-time clearing provider with Layer 1 and Layer 2 services described as Sweden-only.

Which controls should a platform implement first when timelines and guidance are mixed?

Start with a country variance register, a hard gate for message or instruction quality, and a named escalation owner for unresolved interpretation issues. Then verify dated scheme status before relying on it operationally. For example, NCT and NCT Inst 2025 versions were live on 05 Oct 2025, while other material also says no NCT participants yet and estimates first participants in 2027.

What should trigger legal escalation versus operations escalation?

Escalate to legal when the issue may change eligibility, disclosures, or country-specific obligations. Escalate to operations when the issue is execution against an approved rule, such as malformed messages, routing failures, outages, or reconciliation mismatches. If ownership is unclear between interpretation and execution, pause rollout and get legal review.

What evidence should we retain to defend controls during audits or regulatory reviews?

Keep evidence showing what your team believed at the time, who approved it, and what happened when controls failed. That usually includes a country variance log, dated decision notes, change history, incident records, and proof of current scheme-status checks. If you rely on NPC schemes, retain evidence of scheme adherence because NPC states membership is required to use them.

How should we handle unknowns when market infrastructure is still transitioning?

Do not turn unknowns into silent production assumptions. Record each unknown with an owner, review date, affected country or rail, and temporary control such as hold, manual review, or limited rollout. This is especially important when transition signals conflict, including NCT and NCT Inst 2025 versions going live on 05 Oct 2025 while broader transformation is still described as ongoing into 2027.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- collegecatalog.uchicago.edu/thecollege/economicstrusted

- ecb.europa.eu/paym/target/target-professional-use-document...trusted

- ecb.europa.eu/euro/digital_euro/timeline/profuse/shared/pd...trusted

- ecfr.gov/current/title-12/chapter-II/subchapter-A/par...trusted

- edpb.europa.eu/system/files/2025-06/spe-training-on-ai-and-...trusted

- elibrary.imf.org/view/journals/002/2023/320/article-A001-en.xmltrusted

- europarl.europa.eu/doceo/document/A-10-2025-0133_EN.htmltrusted

- farmingdale.edu/courses/index.shtmltrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Expand Your Subscription Platform to Europe for Payment and VAT Readiness

Treat a European launch as an operations sequencing decision first. Lock VAT, payments, and compliance ownership before you scale localization or acquisition.

Music Royalty Tax Compliance: How Platforms Handle 1099-MISC vs. 1099-NEC for Artist Payments

This is an operating-model decision, not a year-end form choice. A team can ship quickly and still end up with misclassified payouts, correction cycles, and filing risk if the classification logic is weak. If you run creator payouts, you need the classification rule before your first batch, not after your first correction cycle.

What Is an Audit Trail? How Payment Platforms Build Tamper-Proof Transaction Logs for Compliance

For payout risk owners, a useful audit trail is one you can replay under pressure: who acted, what changed, when, and why it was allowed.