Quick Answer

Build a sequenced control path: onboarding identity and account-intent checks, first-payout tripwires, explainable monitoring rules, and triage thresholds for monitor, hold, restrict, or escalate. Trigger deeper review when first receipt is followed by rapid onward transfer, and keep evidence items tied to each decision. Escalate toward SAR or STR preparation only when identity narrative, source of funds, and transaction behavior still do not reconcile after enhanced review. This keeps FIU-facing files defensible without freezing every payout.

Why Explainable Screening Matters for Money Mule Detection#

Money mule risk can look like a chain, not just a single bad payout. It can start with a plausible account and become clearer only after transaction patterns develop. A money mule is someone who moves illegally obtained money for another person or organization, so the practical question is not just whether one transaction looks bad. It is whether the full account story still makes sense from signup to payout.

- Treat mule risk as a sequence.

If you only look for suspicious behavior after funds move, you may be reacting late. Review onboarding signals, stated account purpose, early payout behavior, and ongoing movement together. A red flag is a signal of potential money laundering, not proof on its own, so each alert should trigger added scrutiny.

- Design controls around clear ownership.

This guide is for compliance, legal, finance, and risk owners who handle contractor, seller, or creator payouts across markets. Use layered controls across onboarding, payout friction, monitoring, investigation, and reporting readiness. For each alert, define who reviews it, what evidence is required, and when the next step is to monitor, hold, restrict, or escalate to an FIU report such as a SAR or STR, depending on jurisdiction.

- Prioritize explainability before complexity.

The goal is fewer AML surprises and controls your team can run consistently, not maximum alert volume. Favor controls that leave an auditable trail: account evidence, analyst notes, transaction context, and documented decision logic. FinCEN's SAR expectations reinforce this approach. Suspicious-activity fields and narrative key terms help make suspicion understandable, even when you are not proving the exact underlying crime.

- Keep obligations local, but operations consistent.

Regulatory duties vary by jurisdiction and program design, so use this article as an operating baseline and align policy with local legal advice. FFIEC Appendix F is a useful reference for recognizing suspicious activity, but it is not exhaustive.

Many AML alert behaviors also overlap with fraud signals, so triage requires careful review before escalation. The downside of getting this wrong is real. AML failures can lead to serious enforcement outcomes, including a 2025 license revocation in Estonia and a recent €25,000 BaFin fine issued to Ratepay for suspected money laundering.

That is the frame for the rest of this guide. Start with controls that produce usable evidence. Treat single red flags as insufficient on their own. Add complexity only when investigators can explain and defend the decision.

We covered this in detail in Device Fingerprinting Fraud Detection Platforms for Payment Risk Teams.

Who this list is for and how to pick controls#

Use this list if your team owns payout-risk decisions across KYC, KYB, CDD, and transaction monitoring, not just one compliance task. Money mule risk can cut across functions, so control ownership should too.

- Cross-functional payout owners

This section is for teams that decide or influence what happens after alerts: monitor, hold, restrict, or escalate. If ownership is split across separate queues with no clear handoff, controls are harder to run consistently and harder to defend later.

- Not for one-model replacement

This is not a playbook for replacing CDD judgment and investigations with a single machine learning model. A practical pattern is automated screening first, then human investigation when alerts trigger. ID verification helps, but it is not enough on its own for mule prevention, including cases where criminals take over an account and activity still resembles a normal customer profile.

- Choose controls with a practical checklist

When you compare controls, ask four questions:

- Does it cover relevant mule behaviors?

- What is the operational cost to run it?

- What false-positive review burden will it create?

- Will the evidence be strong enough for internal review and potential reporting decisions in your jurisdiction?

Keep your taxonomy flexible. Sources use different mule labels, so do not overfit controls to one fixed category set.

- Decision rule before production

If you cannot explain why a control triggered and what action follows, do not deploy it yet. Start with solid data collection and validation, then require a clear evidence trail for each alert and analyst decision.

Use that standard throughout the rest of the list: prioritize controls your team can operate, explain, and audit, not just controls that increase alert volume.

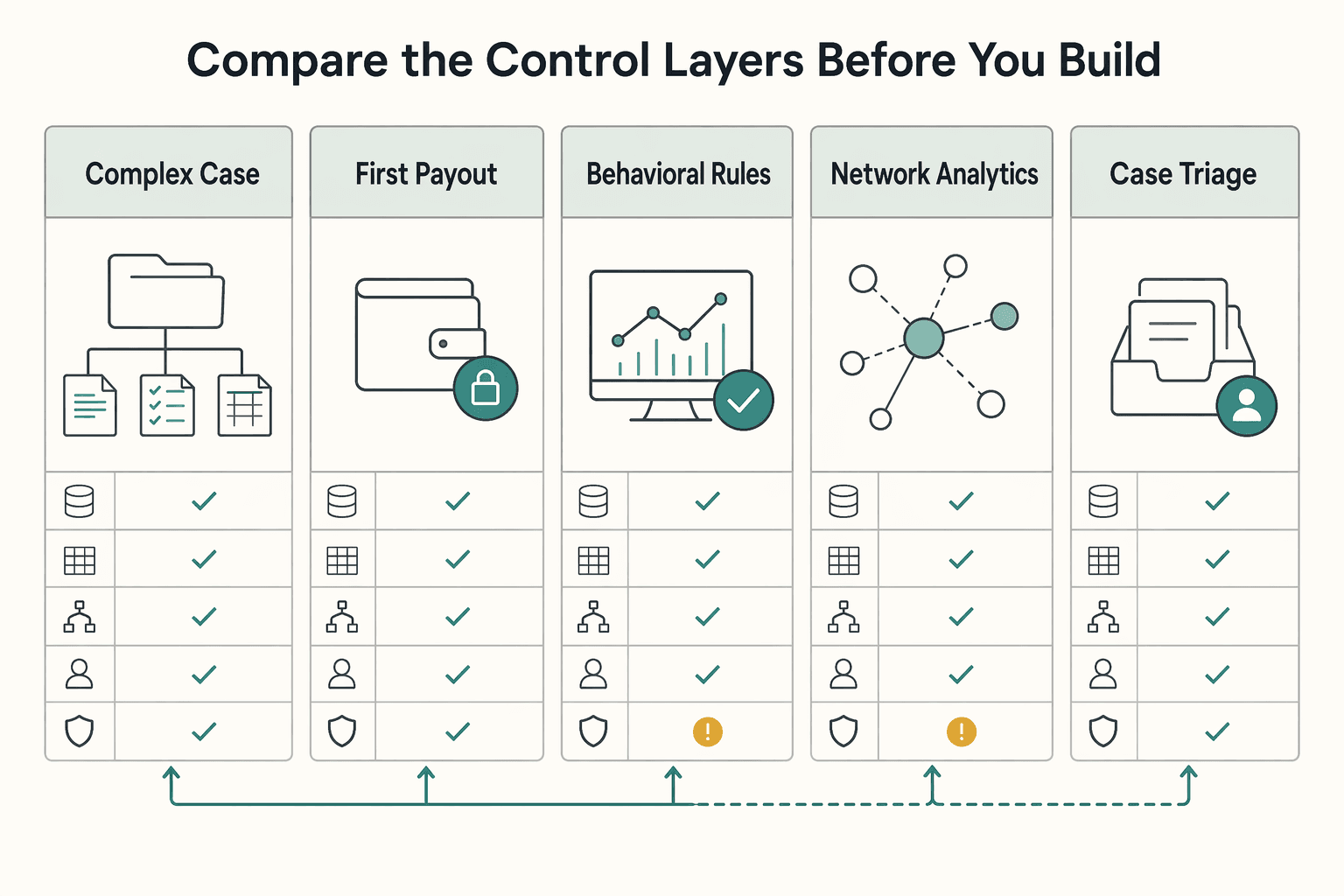

Compare the control layers before you build#

Build the lower-complexity layers that create clear evidence first, then add advanced analytics when your investigation team can support them. Mule activity can start at onboarding, appear early in account activity, and continue through layering, so compare each layer by coverage, tradeoff, and failure mode before you build.

| Control layer | Best for | Key signals | Main tradeoff | Owner team | Required evidence artifact | Failure mode |

|---|---|---|---|---|---|---|

| Onboarding identity checks | Screening account-opening risk before funds move | Identity verification outcomes, sanctions screening outcomes, risk assessment flags | More signup friction and added manual review when thresholds are tight | Compliance ops, onboarding risk, KYC team | Identity verification result, sanctions screening result, risk decision log, analyst notes for step-up review | Synthetic identity can pass when real identifiers are paired with fabricated details; front-account/mule use can remain hidden if checks rely only on onboarding data |

| First-payout friction checks | Testing whether early account activity matches the onboarding profile | Transfers followed by rapid onward movement, including movement across multiple accounts or transfer chains | Slower payout release for some legitimate users and higher support load | Payout risk, AML operations, payments ops | Hold/review trigger log, payout timeline, refreshed CDD request and response, release/reject rationale | Weak follow-up review can let pass-through behavior look routine |

| Behavioral/rules monitoring | Ongoing detection of explainable placement/layering patterns | Transfer patterns, movement between multiple accounts, shell-company indicators | Explainable rules can still miss adaptive behavior and may generate repetitive alerts | AML monitoring, transaction monitoring, risk analytics | Rule definition, alert payload, transaction snapshot, analyst disposition, tuning record | Structured activity can hide the trail if rules are too narrow |

| Network analytics | Finding linked mule networks that single-account rules may miss | Repeated links and movement patterns across connected accounts/entities | Higher model/data complexity and heavier investigation burden | Risk analytics, data science, AML investigations | Link-analysis output, entity-resolution logic, case graph, investigator summary | Weak entity resolution can merge unrelated parties or split linked actors |

| Case triage | Converting alerts into consistent monitor/hold/restrict/escalate actions | Combined alerts from onboarding, payout, and monitoring that remain unresolved | Queue congestion and inconsistent outcomes if triage standards are vague | AML investigations, compliance operations | Case memo, evidence checklist, escalation reason, decision owner, closure rationale | Inconsistent analyst handling weakens defensibility |

Reporting readiness (SAR/STR path) | Preparing a defensible escalation file when suspicion remains | Identity and transaction patterns still cannot be reconciled after review | High documentation effort and legal sensitivity | AML investigations, compliance, legal | Chronology, trigger log, KYC/CDD file, supporting transactions, narrative draft, approval record | Reporting is delayed or weakened when evidence is fragmented |

Use this build-order checkpoint. If a layer cannot produce a clear audit trail of inputs, triggered logic, analyst decision, and final action, do not prioritize it ahead of lower-complexity layers that can. Start with onboarding, first-payout friction, and explainable monitoring. Add network analytics once case quality and review capacity are stable.

If your matrix shows first-payout friction and escalation ownership are the immediate gaps, map those controls to a compliance-gated payouts setup before you add higher-complexity analytics.

Onboarding identity screening and account intent checks#

Start with onboarding. It is a strong pre-funds control for catching likely purpose-opened mule risk before payouts begin. The goal is not to prove a full AML case at signup. It is to confirm that identity and account purpose are coherent and that your approval is defensible later.

Identity verification and KYC checks are core fraud-prevention controls. Keep step-up review targeted to cases where identity, ownership, or funding narratives do not reconcile.

- Identity trace consistency

Check whether identity details align across verification results, account profile data, and linked beneficiary records you already hold. If traces conflict, or the applicant appears duplicative against existing beneficiary identity data, route the case to enhanced review rather than straight-through approval. Keep auditable artifacts: verification result, mismatched fields, analyst notes, and decision log.

- Account intent and source-of-funds clarity

Ask what the account is for and where funds are expected to come from. That matters because mule behavior can involve opening or providing accounts specifically to receive criminal funds. If account purpose and source-of-funds explanations are unclear or do not fit the stated profile, escalate for enhanced review.

- Ownership and control transparency

For entity onboarding, treat opaque ownership disclosures, incomplete control information, or controller contradictions as escalation triggers. Retain the ownership declaration, follow-up responses, review notes, and final release or reject rationale.

Decision rule: if identity traces, ownership disclosures, and funding intent cannot be reconciled at onboarding, escalate before activation. That gives you a defensible audit trail if rapid onward transfers or cash-out behavior appears after onboarding.

This pairs well with our guide on Sanctions Screening for Payment Platforms Before Payout Release.

First payout controls that stop fast pass-through behavior#

First payout is where targeted friction can pay off. Even after clean onboarding, fast pass-through behavior can appear at first receipt or first release. In faster-payment environments, suspicious movement can happen in milliseconds, so post-transaction monitoring alone can leave you reacting after funds have already moved.

- Pre-release first payout gate

Before you release a first payout, score it with evidence you can assess in sub-second timeframes. Prioritize practical inputs: account history, early behavioral patterns, and trusted consortium signals. This is a focused risk check, not a full restart of onboarding.

- First receipt to onward-transfer tripwire

Treat first receipt followed by rapid onward transfer as a separate red flag, even when onboarding was clean. This narrow window is often where laundering velocity matters most, including across ACH, wire, RTP/FedNow, and check-deposit flows where applicable.

- Temporary AML hold with refreshed review

When that pattern appears, apply a temporary AML hold under internal policy and step up review before release. A refreshed review can be appropriate, but it should be a risk-based policy choice, not a universal legal assumption. Keep a defensible evidence pack: first payout details, receipt-to-withdrawal timing, account history, behavioral and consortium signals, analyst notes, and the release or restriction rationale.

The benefit is targeted friction. You can slow immediate laundering velocity without pausing every payout. The tradeoff is customer impact if controls are too blunt.

If you keep one operating rule here, use this: when the first receipt is quickly followed by onward movement that breaks expected account behavior, stop release and review the facts. Do not rely on post-transaction monitoring to recover later.

Transaction monitoring rules that stay explainable#

Explainable transaction monitoring should anchor your ongoing layering controls. A rules-first design is usually a defensible baseline, with behavioral analysis added as a second layer where static logic misses adaptive behavior.

Rule logic matters because it is consistent. When an alert is tied to split movement, unusual dispersion, or activity that breaks the stated account purpose or source-of-funds narrative, investigators can explain what triggered, what they reviewed, and why they released, held, or escalated. That consistency supports day-to-day AML operations and later audit scrutiny.

Build the rules by stage, not by generic "suspicion"#

Build a staged rules table instead of a flat library of generic alerts. It is easier to investigate and tune.

| Stage | Rule description | What the analyst should verify | Key differentiator |

|---|---|---|---|

| Split-transfer patterns | One incoming receipt is followed by multiple smaller outgoing transfers in a short window | Receipt-to-transfer timing, outward leg count, and fit with the customer's stated account purpose | Clear typology coverage for structuring, layering, and smurfing with explainable logic |

| Unusual recipient dispersion | A sharp increase in unique recipients or destinations after stable prior behavior | Whether dispersion is new for this customer and whether counterparties fit the business profile | Surfaces broader risk patterns even when single transfers look ordinary |

| One-off anomaly context check | Activity looks unusual in isolation and is checked against broader customer behavior before flagging | Whether the activity is truly suspicious or a one-off, and how it fits the customer profile | Reduces noise while keeping alert decisions explainable |

| Recurring narrative anomalies | Repeated activity that does not match the original source-of-funds or account-use narrative | Current behavior versus onboarding narrative, prior reviews, and updated customer explanations | Keeps decisions anchored to customer narrative, not isolated events |

Each rule should answer three questions in plain language: what changed, why it may be suspicious, and what evidence would clear it.

Tie alerts back to one customer view#

Monitoring is weaker when transaction alerts are reviewed without customer context. Your investigators need one view of the entity, risks, prior outcomes, and declared narrative so decisions are faster and more accurate.

A practical decision rule is simple: if behavior is unusual but still consistent with the customer narrative, review and document it without automatic escalation. If it is unusual and breaks the narrative, move quickly to refreshed review.

Keep global logic, allow local overlays#

If you operate across markets, a practical model is a shared global typology core plus local overlays for regional requirements. In practice, that means common controls for core typologies, with regional tuning where product mix and reporting expectations differ. That helps you avoid fragmented local rulebooks while keeping controls aligned to local requirements.

Use behavioral overlays to reduce noise, not explainability#

Rules-only systems have a known failure mode: too many false positives relative to true threats. Behavioral context checks can help separate one-off anomalies from genuinely suspicious activity before your analysts get overloaded.

Treat headline performance claims, including figures like 70%, as vendor-stated until you reproduce results on your own closed-case sample. Use a simple standard: better true-case yield without making decisions harder to explain.

Put change control around rule updates#

Rule changes need governance before production release. Use production sandbox testing, compare results against historical outcomes, and require 4-eye approval for material model or rule changes.

For each rule version, keep an audit-ready record: scenario intent, typology coverage, sample alerts, known false-positive patterns, approval trail, and expected action path. Automated audit trails also support downstream SAR and CTR workflows when cases escalate.

If you keep one operating principle here, keep this: start with explainable rules tied to typologies and customer narrative. Then add behavioral overlays only where they improve context rather than obscure it.

For a step-by-step walkthrough, see Fraud Detection on Payment Platforms with Rules and Machine Learning.

Network and behavioral analytics for mule rings#

Use network and behavioral analytics when single-account review is no longer enough to explain movement across multiple accounts or wallets. This layer helps you connect patterns that look low risk in isolation but become higher risk when viewed as a network case.

For mule-ring detection, the practical gain is linkage. Transaction-pattern and behavior analysis can surface hidden links and potential handoffs that a one-account queue can miss. Keep the approach explainable, though. In regulated review, black-box-only outputs can create defensibility gaps, while rules-only controls can miss adaptive behavior.

Before you escalate a network case, require:

- A clear network hypothesis about what appears linked and why.

- Case-level evidence an investigator can read and challenge.

- Model-level and case-level explainability artifacts, including cross-verification of decision logic.

- A documented review path across teams so information silos do not block the investigation.

Use this as an escalation cue: if multiple marginal accounts converge into a common pattern that cannot be explained by available case context, consider treating it as one coordinated case rather than separate low-signal alerts.

Case triage and escalation to regulatory reporting#

Use triage to reach a defensible decision: monitor, hold, restrict, or escalate to reporting. A practical rule is simple: if enhanced review still cannot reconcile the identity narrative, source of funds, and transaction behavior, move from monitoring to formal AML escalation.

The benefit is consistency across analysts and fewer late reporting decisions. The tradeoff is over-escalation. If every unexplained anomaly is escalated, investigations get crowded and higher-risk cases become harder to prioritize.

Build triage around evidence quality#

A red flag should trigger scrutiny, not automatic escalation. FFIEC is clear that a red flag alone is not evidence of criminal activity, and red-flag lists are not exhaustive. In practice, use checklists to guide review, not replace judgment.

Use these checkpoints in every case file. Unresolved gaps should trigger continued review and closer scrutiny; persistent tension after enhanced review supports escalation.

- Does KYC or KYB support the customer's stated activity and expected account use?

- Is the source-of-funds explanation documented and plausible for the observed pattern?

- After closer scrutiny, is there still a reasonable business or legal purpose?

| Severity band | Evidence quality | Typical action | Reporting posture |

|---|---|---|---|

| Low | Single or weak red flag, reasonable explanation still plausible, record incomplete | Continue monitoring and request clarifying CDD evidence | Do not prepare a filing yet; document rationale |

| Medium | Multiple linked indicators, but material facts still missing or explanation partly credible | Temporary hold or account restriction while enhanced review is completed | Prepare a case narrative and evidence set in case SAR review is needed |

| High | Identity narrative, source of funds, and transaction behavior remain unreconciled after enhanced review | Formal escalation to AML investigations, maintain restriction where policy allows | Prepare SAR review package and maintain an auditable record set |

What makes an escalation file credible#

The core artifact is the case narrative, not the alert screenshot. For SAR pathways, FinCEN requests certain key terms in the narrative, so your internal templates should require plain-language documentation of the suspicious pattern before filing review.

A workable evidence pack includes trigger logs, KYC or KYB artifacts, CDD notes, source-of-funds documents, transaction excerpts, analyst reasoning, and the action taken. Build for record retention from the start so the case can be defended during a later audit or investigation.

Common failure modes#

One common failure mode is escalating on volume instead of substance. A burst of transfers can be unusual, but the mere presence of a red flag is not by itself evidence of criminal activity and should trigger closer scrutiny.

The opposite failure mode is waiting for certainty about the exact predicate crime. Escalation should focus on whether activity remains suspicious after closer scrutiny, not on proving the full criminal story before reporting.

Need the full breakdown? Read OFAC, PEP, and Adverse Media Screening Decisions for Payment Platforms.

Evidence packs and governance that survive audits#

If you want decisions to survive audit, optimize for traceability and explainability, not document volume. A strong file lets a reviewer follow the case end to end, from data ingestion to investigator conclusion, and understand why the decision was reasonable at the time.

Recommended baseline pack#

Use this as an internal operating baseline, not a legal minimum.

- End-to-end alert traceability: enough detail to follow the alert from data ingestion to investigator conclusion.

- Pattern and risk comparison: how activity was assessed against expected patterns, risk profile, and known red flags.

- Linked compliance context: relevant context from connected controls like KYC/KYB, sanctions and PEP screening, and ongoing due diligence.

- Decision record: the investigator conclusion and the reasoning that made it defensible at the time.

- Reviewer check: whether a second reviewer can reach the same conclusion from the file alone.

Governance can break when ownership is split but file accountability is not. If compliance, legal, and operations each own part of the work, assign one owner for file completeness and closure so handoffs stay clean.

Before you close a case, run one check. Can a second reviewer compare the activity against expected patterns, risk profile, and known red flags, then reach the same conclusion from the file alone? If not, the pack is not ready. That is also how you balance real-time detection and reporting with fewer false positives and less operational fatigue while keeping cases investigator-ready.

A 30 60 90 day implementation sequence#

Build this in layers: stabilize policy language and case decisions first, then add more advanced detection. Automating before your team can apply the same facts to the same action can create avoidable inconsistency.

Days 1 to 30#

Start by removing ambiguity in language and escalation. If you use labels such as unwitting mule, witting mule, and criminal mule, keep them as internal working shorthand and apply them consistently in alert reasons, investigator notes, QA checks, and escalation templates.

If it improves case clarity, align that vocabulary with Financial Action Task Force (FATF) terminology. Transaction monitoring is a fundamental part of financial-crime compliance, and current monitoring and reporting frameworks still face effectiveness challenges. Terminology drift can become decision drift.

Publish tiered escalation criteria before adding more alerts:

- Monitor with rationale when activity is unusual but still reconcilable with Customer Due Diligence (CDD) and expected account use.

- Hold or restrict and refresh CDD when identity narrative, source of funds, or payout behavior is incomplete or contradictory.

- Escalate for formal AML review and potential SAR or STR preparation when the account story and transaction behavior still do not reconcile after enhanced review.

Days 31 to 60#

Next, deploy controls where intervention can happen early, such as onboarding and first payout. Pair those controls with a tight analyst feedback loop so prompts and workflows improve based on real case outcomes.

Track false positives by segment rather than as one blended number, and refine CDD prompts based on what actually resolves cases. When CDD is refreshed, a second reviewer should be able to see what new fact was obtained and why that fact changed the action.

Days 61 to 90#

Add network-level detection only after baseline rule outcomes, case handling consistency, and evidence quality are stable. Rule-based approaches are easier to implement but can struggle to adapt to new threats, so this is the point to expand detection depth.

Use network and behavioral indicators as investigation prompts, not automatic proof. Examples described in a mule-account detection patent abstract include remote access usage, virtual machine or proxy usage, and a pattern of multiple incoming transfers from multiple countries. Those transfers are followed by one outgoing transfer to a different country.

Introduce a machine learning model only when explainability requirements are clear. Research published on 16 February 2026 reports AML detection F1 scores of 0.54 to 0.63 in synthetic-data experiments, which supports experimentation but not blind deployment. Require both case-level and portfolio-level interpretability.

Verification checkpoint#

Before declaring the rollout mature, test decision consistency. Run retrospective sampling across shifts and regions and confirm that identical facts lead to identical actions when reviewers work from the case file alone.

If outcomes diverge, fix definitions, escalation wording, prompts, or evidence-pack quality before adding complexity. If your program files SARs, also confirm templates can capture authority-specific filing instructions when required, for example when a request specifies required terms in SAR fields and narrative text.

Conclusion#

The strongest approach is not more alerts. It is a staged AML control system with clear ownership, explicit decision rules, and defensible records from first signal to final action.

- Start with controls your team can explain

Build your baseline around KYC and monitoring logic investigators can interpret. Treat red flags as triggers for closer scrutiny, not proof by themselves, and document what was checked, what looked inconsistent, and why the case moved to the next step.

- Add advanced analytics only when operations are ready

Additional analytics can support detection, but they should extend a working baseline, not replace it. Legacy rules built before real-time payments can reduce intervention effectiveness over time, so modernization matters, but only if analysts can still explain why an account was flagged and what action followed.

- Make escalation traceable end to end

Keep a consistent case record: trigger details, KYC review notes, customer explanation updates, action taken, and closure rationale. When suspicion remains unresolved after enhanced review, move from monitoring to formal escalation. Where SAR or STR filing applies, the narrative should clearly reflect why activity remains suspicious.

Remediation and account closure can be costly, so teams may delay action until cases look extreme. A better balance is targeted friction at the right point in the lifecycle, backed by consistent documentation so similar facts lead to similar decisions across reviewers and markets.

When you are ready to operationalize this framework, use the developer docs to map it to your existing risk process.

Frequently Asked Questions

What are the highest-signal red flags of money mule activity on payment platforms?

The strongest signals are usually movement patterns, not one odd payment. Splitting funds into smaller amounts, sending to multiple recipients, or routing money to a crypto wallet can indicate layering behavior. Treat these as investigation triggers, not proof on their own, and test whether the pattern still fits the customer’s CDD profile over time.

How should onboarding checks differ from ongoing transaction monitoring?

Onboarding CDD establishes who the customer is and why the account is being used. Ongoing monitoring checks whether real transaction behavior continues to match that story, including possible layering patterns that are not obvious in a single transfer. A risk-based AML program needs both controls working together, not one in isolation.

When should a platform file a SAR or STR instead of continuing to monitor?

Escalate when review cannot reconcile the customer narrative and transaction behavior. A red flag alone is not enough, but unresolved suspicion after review is where SAR or STR reporting to authorities may be required. At that point, your case record should clearly show what triggered review, what was checked, and why the decision moved from monitoring to reporting.

Why are unwitting mules often harder to detect than criminal mules?

Because surface behavior can look cooperative even when the person does not understand what they are moving. Sources also describe pressure and deception as common factors, especially for vulnerable people, which makes intent harder to infer from surface behavior. Public awareness can be low, with one cited poll noting only about 1 in 4 people recognized money muling as illegal.

What should a minimum viable layered detection stack include?

Start with controls you can run consistently: onboarding CDD, ongoing transaction monitoring, and a clear escalation and reporting path for suspicious cases. Then add behavioral analysis and other security layers as operations mature. This layered approach is more reliable than relying on a single control, especially since rules-only monitoring can fall behind changing crime patterns.

How can teams reduce false positives without weakening AML coverage?

Avoid treating any single red flag as automatic guilt. Review alerts against the customer’s CDD profile and transaction patterns over time, then escalate when suspicion remains unresolved. This keeps coverage intact while reducing avoidable false alarms.

Try a related tool

Yuki writes about banking setups, FX strategy, and payment rails for global freelancers—reducing fees while keeping compliance and cashflow predictable.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- bis.org/cpmi/pietf/fraud_report_2026.pdftrusted

- bsaaml.ffiec.gov/manual/Appendices/07trusted

- cs50.harvard.edu/x/gallerytrusted

- fdic.gov/federal-register-publications/payments-lifel...trusted

- namlcftc.gov.ae/media/nqhlu4av/acpf_dwg_money_mules_mar2025-...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC10311174trusted

- unifiedfireut.gov/wp-content/uploads/UFA-Proposed-Budget-reduc...trusted

- businessscreen.com/resources/top-10-aml-transaction-monitoring-...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade:

Spain Digital Nomad Visa Guide: Requirements, Application & 2026 Updates

Stop collecting more PDFs. The lower-risk move is to lock your route, keep one control sheet, validate each evidence lane in order, and finish with a strict consistency check. If you cannot explain your file on one page, the pack is still too loose.