Quick Answer

A platform should stay on the SPI path only while its payment services remain within the Section 6(5) limits discussed here, and it should move to MPI when those limits are exceeded. In practice, that means monitoring transaction volume by service type, combined activity across services, and daily outstanding e-money, then escalating early if forecasts or product changes reduce headroom.

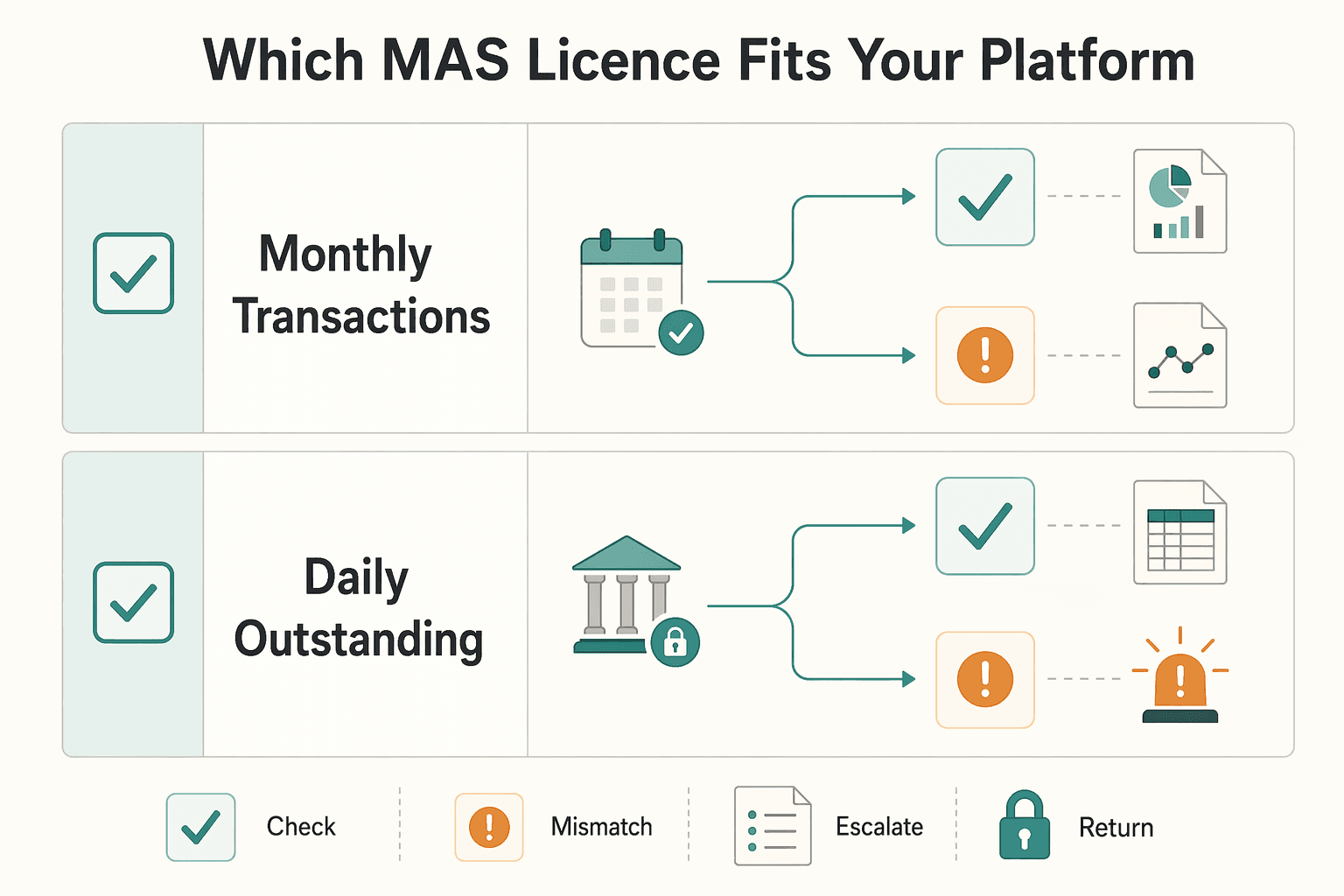

Which MAS licence fits your platform?#

Under Singapore's Payment Services Act 2019, one early licensing decision is practical. Can your platform apply for a Standard Payment Institution (SPI) licence, or should it apply for a Major Payment Institution (MPI) licence? MAS indicates you can apply for SPI if your payment services meet the stated SPI thresholds, and you should apply for MPI if your payment services exceed those threshold limits.

For compliance, legal, finance, and risk owners, this is a control-design decision, not just a licence label. You need clear decision rules, operating checkpoints, and escalation triggers so growth does not force a rushed filing or an unnecessary early overbuild.

MAS confirms that payment service providers can apply for three licence types under the PS Act, and points firms to Section 6(5) for threshold-limit detail. The published SPI threshold signals are:

| SPI threshold signal | MAS-published level |

|---|---|

| Monthly transactions for any single payment service, other than e-money account issuance and money-changing services | S$3 million |

| Monthly transactions for two or more payment services, other than e-money account issuance and money-changing services | S$6 million |

| Daily outstanding electronic money, e-money | S$5 million |

If your forecasts are moving toward these levels, or your service mix is expanding across payment functions, treat that as an escalation trigger. For external status checks, MAS identifies the Financial Institutions Directory as the reference point for listed standard payment institutions in Singapore.

Process execution risk matters too. MAS has published licensing-process revisions effective 26 August 2024, including a legal-opinion submission requirement for mapping proposed business models to regulated payment services, an Independent External Auditor assessment requirement for new and variation applications to carry out DPT services, and a case-on-hold process for reviewed cases that need more applicant resolution time. Because the materials here do not fully set out how every reported change applies across filing types, treat these as filing-specific items to verify before you submit.

Scope boundary matters as well. This article stays grounded in published MAS materials. From the excerpts here, you can rely on the SPI thresholds and the basic within-limits versus above-limits direction. You cannot rely on them for a complete SPI-versus-MPI obligations map, exact MPI quantitative thresholds, full eligibility criteria, or definitive licensing fees and approval timelines.

SPI and MPI at a glance for platform operators#

For platform operators, the core rule is simple. Stay on the Standard Payment Institution (SPI) licence path only while you are within the Section 6(5) of the Payment Services Act limits. If you exceed those limits, MAS says you should apply for a Major Payment Institution (MPI) licence.

| Comparison point | SPI | MPI | Confidence level |

|---|---|---|---|

| Licence intent | MAS says you can apply for SPI if your payment services meet the thresholds. If you only provide money-changing services, MAS says to apply for a money-changing licence instead. | MAS says you should apply for MPI if your payment services exceed the specified threshold limits. | MAS-confirmed |

| Threshold position | MAS points to Section 6(5) and publishes SPI threshold signals: S$3 million monthly for any single payment service, excluding e-money account issuance and money-changing, S$6 million monthly for two or more payment services, with the same exclusions, and S$5 million daily outstanding e-money. | In the MAS material used here, MPI is confirmed as the path when limits are exceeded, but a full MPI threshold and obligations comparison is not set out. | MAS-confirmed for SPI thresholds and the exceed-limits trigger; not fully confirmed here for broader MPI detail |

| Eligibility baseline | MAS states SPI applicants should be a Singapore-incorporated company or Singapore branch of a foreign corporation, have a permanent place of business or registered office where books and records are securely held, and have minimum base capital of S$100,000. | The material here does not fully state MPI baseline criteria. | MAS-confirmed for SPI; limited confirmation here for MPI |

| Governance expectations | MAS states controllers and directors must be fit and proper under FSG-G01, and expects compliance arrangements matched to the business's nature, scale, and complexity. | The material here does not define a complete MPI-specific governance delta. | MAS-confirmed for general expectations; partial for MPI specifics |

| Practical operating impact | Track monthly transactions by service and daily outstanding e-money so you can evidence your SPI threshold position. | If you are near or above limits, MPI can shift from a future possibility to an active licensing and control-planning workstream. | Mixed: threshold direction is MAS-confirmed; readiness timing is operator judgment |

The operational checkpoint is evidence quality. MAS regulates 7 types of payment services under the PS Act, so do not rely only on total volume. Confirm which regulated service types you are providing, and whether you have crossed from one service into two or more. For external verification, MAS identifies the Financial Institutions Directory to check listed standard payment institutions in Singapore.

Operator planning step (not a MAS-stated trigger): if forecasted volume or e-money exposure is close enough that SPI limits are becoming a planning risk, run an MPI readiness assessment before product expansion. That gives you the high-level split. For a broader regional view, see A Deep Dive into the FinTech Network of Southeast Asia.

What MAS confirms today and what is still unknown#

For licensing decisions, use primary MAS text and statute text as decision-grade material. Treat secondary commentary as a prompt to verify, not a substitute for that step.

Confirmed in MAS text#

| Topic | What MAS confirms |

|---|---|

| Offshore-only DTSP scope | From 30 June 2025, DTSPs serving only customers outside Singapore for specified token services require a licence. |

| Licensing posture | MAS says it has set the bar high for licensing and will generally not issue a licence for that offshore-only DTSP scope. |

| Unlicensed activity | MAS says unlicensed in-scope DTSPs will have to cease their regulated activities. |

| Existing licensed providers | For providers already licensed and serving customers in Singapore, MAS says there is no change to what the licensed providers can do. |

| Linked statutes | MAS links digital token services to the Payment Services Act 2019, Securities and Futures Act 2001, and Financial Advisers Act 2001. |

- MAS states that from 30 June 2025, DTSPs serving only customers outside Singapore for specified token services require a licence.

- MAS says it has "set the bar high for licensing and will generally not issue a licence" for that offshore-only DTSP scope.

- MAS says unlicensed in-scope DTSPs "will have to cease their regulated activities."

- MAS says for providers already licensed and serving customers in Singapore, "there is no change to what the licensed providers can do."

- MAS links digital token services to existing statutes, including the Payment Services Act 2019, Securities and Futures Act 2001, and Financial Advisers Act 2001.

Needs direct confirmation from MAS or counsel#

| Topic | Why it needs confirmation |

|---|---|

| SPI/MPI thresholds and obligations | The materials here include secondary SPI/MPI signals, but they do not provide MAS primary-text SPI thresholds or a full SPI-versus-MPI comparison across obligations, governance, safeguarding, reporting, timelines, or fees. |

| Shift from SPI planning to MPI filing | A MAS primary-text explanation of when a firm should shift from SPI planning to MPI filing is not set out in these excerpts. |

| Guidelines on Licensing for Payment Service Providers | The guidelines are not excerpted in this set, so use the current live MAS version directly before relying on any summary. |

If your scope is near a licensing boundary or touches digital tokens, confirm against live MAS materials and counsel before launch or expansion.

Threshold monitoring rules for contractor, seller, and creator platforms#

For SPI operators, threshold monitoring should run as an early-warning control, not only a month-end reporting task. If your legal mapping uses Section 6(5) of the Payment Services Act 2019 for SPI limits, treat that boundary as live and escalate early when growth could outpace licensing preparation.

The point is not false precision. The point is a documented method, repeatable calculations, and a clear escalation path when growth or product changes start to compress your headroom.

Turn legal thresholds into operating triggers#

At minimum, monitor three views together: service volume by payment service type, combined activity across services where aggregation may matter, and e-money exposure, including value stored, held, or redeemed in your platform setup.

| View | Track | Detail |

|---|---|---|

| Service volume by type | Service volume | By payment service type |

| Combined activity | Activity across services | Where aggregation may matter |

| E-money exposure | E-money exposure | Including value stored, held, or redeemed in your platform setup |

Use current statute text and live MAS licensing guidance when finalizing calculation logic. The materials here point to SPI/MPI licensing categories, but they do not provide the full threshold-calculation method or every trigger detail. Keep a dated copy of the source text, or a legal interpretation note, in your threshold file rather than relying on memory.

A practical escalation rule#

Use a forecast trigger, not only backward-looking actuals. As an internal operating rule, if forecast growth shows a realistic chance of exceeding SPI limits within the next two quarters, start an MPI readiness gap assessment and escalate to Legal, Compliance, and the accountable product executive.

Treat that two-quarter trigger as an internal operating rule, not a MAS-quoted requirement. It gives teams lead time for licensing prep, governance evidence, and product-scope decisions.

Where platforms usually get this wrong#

A common failure mode is narrow data scope. Teams may track settled payouts but miss pending flows, held balances, wallet-like value, or DPT-linked activity. That can understate exposure and delay escalation.

For DPT-linked activity, the MAS PSN02 guidance in these materials applies to payment services licence holders carrying on DPT services and should be read with the notice. MAS also states that observance can affect its overall risk assessment, including governance and internal controls. Even where threshold treatment needs legal interpretation, incomplete data coverage is still a control weakness.

Example internal operating cadence (not MAS-mandated):

| Control area | Primary owner | Core data source | Review cadence | Escalation threshold |

|---|---|---|---|---|

| Service-volume monitoring by payment service type | Compliance | Service mapping, transaction ledger, product classification register | Monthly; ad hoc after feature launches | Classification ambiguity, or forecasted SPI headroom compression within two quarters |

| Combined-service exposure review | Finance Ops | Finance warehouse, settlement reports, reconciliations, management forecast | Monthly | Material trend that compresses headroom, or unresolved cross-service reconciliation gaps |

| E-money and held-value exposure review | Payments Ops | Wallet and balance ledger, pending payout queues, reserve and redemption reports | Monthly; weekly watchlist during rapid balance growth | Rising held value, missing pending balances in monitoring, or product changes affecting stored-value behavior |

Keep ownership split: Compliance for interpretation, Finance Ops for completeness and reconciliation, and Payments Ops for money-movement reality. A single-team model can work, but it raises the chance that classification errors persist.

For a US comparison point, read A Deep Dive into California's Money Transmitter License Requirements.

Eligibility and governance baseline before filing#

Before drafting, confirm that your applicant setup is actually licensable. After preliminary threshold monitoring points you toward SPI or MPI, the next gate is practical readiness: clear payment service categorization, a registered Singapore records location, and a resident director MAS can assess as fit and proper.

This work is front-loaded. If you leave it to the form-drafting stage, legal, compliance, and finance can end up in avoidable rework over applicant structure, records ownership, and governance evidence.

| Pre-filing area | Grounded baseline | What to treat as unconfirmed until verified |

|---|---|---|

| Service scope | Determine the exact payment service category under the Payment Services Act before filing. | Treat third-party SPI/MPI threshold summaries (including the S$3M monthly split) as preliminary until confirmed against current MAS materials. |

| Singapore records presence | Establish a registered physical office address in Singapore where regulatory records will be kept. | Do not assume a vague or distributed records location is sufficient. |

| Director baseline | Appoint at least one resident director who meets MAS fit and proper criteria. | Do not treat EP- or PR-linked director assumptions as settled from these excerpts alone. |

| Control readiness | Robust AML protocols and TRM frameworks should be fully operational before launch. | Do not present "controls will be completed later" as launch-ready. |

| Filing mechanics | Submit SPI or MPI applications via the MAS Corporate Services Portal. | Portal submission does not prove substantive readiness. |

What to verify before first draft#

The clearest documentary checkpoint is records governance. Be able to identify the registered Singapore office address where regulatory records are kept, and align finance, ops, and compliance on one consistent records set before filing.

Director readiness needs the same discipline. The materials here support a resident director meeting MAS fit and proper criteria. If your structure depends on EP or PR assumptions, treat that as a verification item and confirm it directly with current MAS guidance and counsel before presenting it as compliant.

Governance should be tested, not narrated#

Complete governance evidence before drafting begins. At minimum, lock down the payment service category, resident director setup, records location, and accountable owners for AML and TRM controls.

A practical failure mode is writing the narrative first and validating governance later. That shows up as conflicting role descriptions, unclear AML and TRM accountability, or inconsistent records-location statements. The materials here say AML and TRM frameworks should be fully operational before launch, so internal sign-off should reject "we will build it later."

Internal sign-off before filing#

Use a three-way sign-off before submission. Legal confirms service category and applicant structure. Compliance confirms fit-and-proper readiness and AML and TRM operating readiness. Finance confirms records location, data completeness, and consistency with threshold monitoring assumptions.

Verdict: treat governance readiness as a filing prerequisite. If resident-director setup, records presence, or fit-and-proper support is still uncertain, pause and close that gap before submitting.

For a step-by-step walkthrough, see 8 Resilient Compliance Controls for Payment Platforms in 2026.

Licensing process changes that now affect execution risk#

After governance readiness, a key execution risk is scope drift, not just form completion. If your application touches Digital Payment Token (DPT) services, plan for additional verification, more document iteration, and a longer path than a stable filing with already-mapped activities.

Under the Payment Services Act 2019, Singapore regulates by activity. The materials here note that 2024 amendments expanded the DPT perimeter. That is why "front-end only" or "non-custodial" product descriptions should not be treated as safe shortcuts without a fresh scope check.

| Application situation | What the pack supports | What to verify before filing | Likely execution effect |

|---|---|---|---|

| Stable application with no DPT expansion | PSA scope can change when product activities change. | Whether any feature now fits a PSA payment-service category. | Lower risk if your service map is current and consistent. |

| New application involving DPT services | DPT scope widened in 2024; exchange-platform functionality is a licensing-scope checkpoint. | Whether your exact model is in scope and what current submission materials are expected. | Higher risk of rework, delay, and added compliance cost. |

| Variation adding DPT-adjacent features | Activity-based regulation means function matters more than labels. | Whether the variation needs refreshed analysis and updated control evidence. | Higher rework risk, especially when product, legal, and compliance describe features differently. |

Where the pressure is highest#

Pressure is typically highest in filings where DPT functionality or exchange-like features are present. Keep a live service inventory mapped to PSA categories, including the seven payment-service categories framing, and rerun it whenever roadmap changes land, not only at drafting time.

One failure mode is treating custody as the only trigger. The materials here support a broader checkpoint: if your platform enables people to exchange virtual currency in Singapore, treat it as a licensing-scope question and escalate early.

Legal opinions and Independent External Auditor Assessment#

For legal opinions and the Independent External Auditor Assessment, the materials here do not support stating that they are universal MAS requirements for these scenarios. Treat them as verification items for your specific filing, not assumptions.

Operationally, confirm early whether additional external analysis or independent review is expected for your model, and align your evidence pack with how the service actually works.

Plan for pause risk in timelines#

The materials here do not give a complete basis for treating any reported MAS hold process as a universal, defined mechanism with fixed triggers. You should still model practical pause risk: applications can stall while scope, documents, or control evidence are clarified.

External commentary cited here reports waits of at least a year in context. That is material for launch sequencing. If DPT scope is near your roadmap, plan around verification gates and scope alignment rather than optimistic submission dates.

For the controls side of ongoing compliance, read What Is an Audit Trail? How Payment Platforms Build Tamper-Proof Transaction Logs for Compliance.

DPT variation applications and scope creep risk#

Treat DPT-adjacent feature requests as an early escalation point, not a routine release decision. In this evidence set, the exact legal trigger for a licence variation is not confirmed. The safer checkpoint is whether the proposed live service still matches your current licence narrative, activity mapping, and customer-facing description.

Recent Singapore fintech activity in tokenised assets and embedded finance, alongside higher fraud/scam pressure in cross-border and AI-driven platforms, is a practical reason to tighten scope checks before launch. A practical decision screen is simple: does this change alter how users access, move, or exchange digital value in your product? If yes, involve legal and compliance before roadmap commitment, not after engineering and commercial plans are locked.

| Product change | Risk signal | What to verify before committing |

|---|---|---|

| UI, reporting, or analytics change with no new user value-movement path | Lower | Product flow and customer description still align with current licensed service position |

| New capability that changes how users route, exchange, or access digital value | Higher | Whether current scope assumptions still hold, and whether a variation assessment is needed |

| DPT-adjacent expansion, for example tokenised issuance or trading, or exchange-like behavior | Highest | Whether scope description, controls, disclosures, and launch plan describe the same real service |

Use existing licensing and customer-protection guidance as review anchors, but do not assume this evidence proves specific variation steps, timelines, or mandatory artifacts. If product, legal, and compliance reviews point in different directions, pause and reconcile before build.

Who owns which control across legal, finance, risk, and engineering#

Use a hybrid ownership model as an internal governance approach. Legal and compliance can make the final licensing call, while finance, risk, and engineering run early-warning signals so scope or threshold issues are caught before filing.

| Control area | Central accountability | Distributed signal owners | What must be checked |

|---|---|---|---|

| Threshold monitoring | Finance | Compliance, Payments Ops, Engineering | Monthly checks against SPI thresholds: S$3 million monthly transactions for any one payment service (other than e-money account issuance and money-changing), S$6 million monthly transactions for two or more payment services (other than e-money account issuance and money-changing), and S$5 million daily outstanding e-money; document assumptions and calculation method; escalate potential threshold exceedance for MPI assessment |

| Application documentation | Legal | Compliance, Finance, Risk, Engineering | Service description matches the live product, entity details are current, books and records are securely held at the permanent place of business or registered office, at least one appointed person is present there to handle consumer queries or complaints, and governance evidence is complete |

| Submission quality control | Compliance | Legal, Finance, Risk | Numbers, scope narrative, customer journey, and control descriptions are internally consistent before submission to MAS |

| Incident and escalation handling | Risk and Compliance | Engineering, Ops, Legal, Finance | Suspected threshold breach, complaint pattern, or recordkeeping gap is escalated promptly and assessed for licensing impact |

Finance can own threshold calculations because the limit test is a licensing control, not just a reporting exercise. Retain source data, calculation logic, and manual adjustments in each monthly pack.

Legal can own the licensing narrative, with cross-functional input. The evidence set should align service scope and governance facts. That includes business location or registered-office recordkeeping arrangements, appointed on-site complaint-handling coverage, and fit-and-proper support for controllers and directors under FSG-G01. If the service is only money-changing, escalate scope classification early because MAS indicates that path should use a money-changing licence.

Engineering can own auditability standards that make compliance evidence recoverable. The excerpts here do not prescribe a specific MAS log format. Set traceable payment-event history and reconciliation-ready records as internal standards that finance and compliance can map back to books-and-records obligations under the Payment Services Act 2019.

Centralized ownership improves filing consistency. Distributed ownership catches product changes earlier. Use an internal release gate so material payment-flow changes are reviewed for licensing impact before go-live.

Evidence and reporting checklist for monthly governance reviews#

Your monthly governance pack should answer two questions up front: are you still within your current licence perimeter, and do you have a clear escalation path if that answer changes.

| Artifact in monthly pack | What it should answer | Verification checkpoint | What to retain | Escalate when |

|---|---|---|---|---|

| Threshold calculations against SPI limits | Are you within SPI limits or moving toward MPI? | Finance prepares monthly calculations; Compliance reviews service-classification assumptions behind the numbers | Source data extract, calculation file, manual adjustment log, reviewer sign-off note | Any service at or above S$3 million monthly transactions, two or more services at or above S$6 million combined, or daily outstanding e-money at or above S$5 million; also when trends indicate likely breach |

| Service-mix mapping | Do current product and payment flows still match the right regulated versus non-regulated scope? | Legal or Compliance checks current flows against First Schedule Part 1 and Part 2 references | Current service map, payment-flow diagram, change log, decision memo | New feature or flow that may change classification, including potential shifts between handling data only and handling money |

| Governance attestations | Are licensing and oversight facts still current across owners? | Control owners submit attestations; Compliance checks completeness and unresolved exceptions | Dated attestations and exception tracker | Unresolved governance gap, recordkeeping issue, or mismatch between live operations and licensing narrative |

| Variation-trigger assessment | Did a change create a licence-variation question under current MAS licensing guidance? | Compliance and Legal review roadmap and production changes against MAS licensing guidance | Monthly variation assessment memo with decision and rationale | Material payment-flow change, new regulated service type, or uncertainty on whether activity remains in current licence scope |

| Regulator-facing reference checks | Are your external status checks and internal guidance references current? | Compliance confirms MAS references used internally | Dated Financial Institutions Directory check and internal guidance note | Directory status inconsistency, outdated internal references, or reliance on third-party summaries over MAS text |

The threshold sheet is the anchor. MAS says firms can apply for an SPI licence when payment services meet the thresholds, and should apply for an MPI licence when payment services exceed specified limits. Keep those threshold numbers explicit each month rather than implied in broader reporting.

Service-mix mapping is the second control that prevents false comfort. MAS also states not all payments-related activities are regulated under the PS Act. Providers that process only payment data and not money may be treated as outsourcing services. That is why scope checks should sit alongside threshold math.

Keep two regulator-facing checks as standing monthly items: a dated Financial Institutions Directory verification and a short internal alignment note to the MAS licensing guidance you rely on. The materials here do not provide a MAS-mandated monthly template, so your internal note should focus on whether current services, entity status, and scope assumptions still match the guidance.

For sign-off and escalation, define an internal matrix and apply it consistently. Escalate to external counsel when you cannot confidently classify a live or planned activity using MAS primary materials. Do the same when operations may be shifting between data handling and money handling, when thresholds are breached or likely to be breached, or when a roadmap change may require licence variation.

Before your next monthly review, map each control owner to implementation evidence and escalation paths in one place. The Gruv docs can help legal, finance, and engineering align on an audit-ready operating model.

High-cost mistakes that create regulatory surprises#

Regulatory surprises often come from a few avoidable mistakes. Teams use secondary summaries as if they were authoritative, wait too long to escalate when they are nearing licensing decision points, or approve DPT-related scope changes before compliance evidence is ready.

| Decision area | Costly shortcut | Stronger check | What fails later |

|---|---|---|---|

| Source of truth | Treating advisory summaries as the decision basis | Validate decisions against MAS primary materials and keep a dated internal note of what MAS text you relied on | Teams discover late that actual flows or scope do not match the summary they followed |

| Threshold management | Tracking only current-month status | Track proximity and trend, not just current position, and escalate earlier when movement is clear | Reclassification and control changes happen under time pressure |

| DPT scope change | Shipping token-related features as normal product work | Require compliance review before roadmap commitment, including service classification and AML/CFT control impact | Licensing and ML and TF risk questions surface after build decisions are already locked |

| Governance evidence | Relying on institutional memory instead of records | Retain dated review evidence, decisions, exceptions, and remediation status | You cannot support your licensing narrative when review or variation questions arise |

Use third-party explainers as prompts, not conclusions. MAS primary materials should be your decision anchor, especially for licensing interpretation and AML and CFT expectations.

Threshold misses are often governance misses, not just math misses. If you are moving closer to your current limits, increase control depth early so escalation is deliberate rather than reactive.

DPT changes deserve earlier escalation#

MAS states DTSPs may be more susceptible to ML and TF risk because the services are internet-based and cross-border. MAS also states it will license DTSPs in a prudent and cautious manner, in extremely limited circumstances, and without a transitional arrangement. Those points do not automatically determine your platform's status, but they do signal that token-scope expansion should never be treated casually.

For token-adjacent changes, keep the evidence pack ready before build approval: product scope, flow mapping, service-classification note, and AML and CFT control mapping. At minimum, that mapping should cover customer and beneficial-owner identification, account review, and suspicious transaction monitoring and reporting where relevant.

Build enough control for your stage, not for a hypothetical future#

Overbuilding too early can slow execution. Underbuilding near key triggers can create expensive rework. The practical approach is to keep controls lean but documented when scope is stable, then increase formality as proximity and scope complexity rise.

MAS notices can change the answer#

Do not assume an earlier analysis remains current. MAS AML/CFT Notices and related Guidelines set requirements and supervisory expectations, so check the latest MAS materials during launch and change approval even when your base licence view appears unchanged.

Scenario recommendations for common platform profiles#

Use a forward-looking lens: decide for the next planning cycle of scope and volume, not only today's footprint. If services and volume are stable and clearly below applicable limits, an SPI-oriented posture may be workable. If growth or scope is moving, start MPI readiness early. Treat SPI/MPI limit assumptions as provisional until you confirm them against MAS primary materials and legal advice.

| Platform profile | Recommended posture | What to verify now | Main failure mode | Practical recommendation |

|---|---|---|---|---|

| Early-stage platform, stable services, clearly below current limits | Stay SPI-oriented | Keep a dated monthly threshold file, service-classification note, and the MAS primary text or legal interpretation you relied on | Teams rely on assumptions instead of evidence and cannot defend the "still below limits" position | Keep controls lean, but make monthly threshold review a Compliance and Finance sign-off |

| Fast-scaling marketplace nearing limits or showing sharp growth | Run parallel MPI readiness | Validate trend, service mix, and scope interpretation against MAS primary materials and counsel | Escalation starts too late, creating rushed governance and launch pressure | Prepare licensing narrative and governance evidence before you are at the edge |

| Platform adding DPT-linked features or front-end trade-arranging capability | Treat as licensing reassessment, not routine feature work | Check whether the flow induces or arranges DPT trades, even if you do not hold DPTs | Product assumes "no custody means no issue" and enters a broader regulated perimeter | Pause launch approval until legal and compliance review the exact flow and control impact |

| Single-function FX or payout product considering multi-service expansion | Keep scope narrow unless expansion is already commercially committed | Confirm which new regulated activities are actually being added | Bundling services early creates rework, heavier evidence demands, and possible licence-path changes | Launch narrow first, then run a fresh licensing review before adding services |

A fast-scaling platform should also treat timeline risk as real. Third-party legal commentary in these materials reports licence processing periods of at least a year, so parallel preparation is usually the safer operating posture.

For DPT-related scope, apply a harder gate. Singapore's regime is activity-based, and 2024 PSA amendments expanded regulated DPT services. Front-end trade-arranging models can fall inside scope even without taking possession of DPTs.

Related reading: Accounting Cycle for Payment Platforms: How to Structure Month-End and Quarter-End Close.

Conclusion#

SPI versus MPI is not just a filing label. In practice, it is an operating commitment you should revalidate as volumes, services, and product scope change.

If you are operating near your assessed SPI thresholds or planning a new payment feature, treat that as an escalation point, not routine monitoring.

| Operating position | What to do now | Keep current | Escalate when |

|---|---|---|---|

| Current model appears within SPI scope | Keep threshold and service-scope checks active | Dated threshold calculations, service mapping, MAS guidance version date, internal approvals | Forecasts move toward limits or a feature changes payment flow |

| MPI may be needed | Start licence-type-change readiness before crossing limits | Gap list, control ownership, dated threshold reference file, counsel question log | You expect to exceed limits, add or remove services, or change licence type |

| DPT-related new or variation application | Plan for higher execution risk and tighter submission quality | Legal opinion and Independent EA assessment where required, plus a complete application evidence set | DPT functionality may bring you into new-licence or variation scope, or MAS follow-up shows the scope or controls need more work |

Process changes effective 26 August 2024 and DPT-related submission requirements can increase execution risk, so treat timeline assumptions cautiously and verify current filing requirements before you submit.

A practical control choice is a monthly threshold review, even though these excerpts do not state a mandatory MAS monthly cadence. The real test is whether you can quickly produce dated records showing why your current licence position is still appropriate.

If your team is designing cross-border payout infrastructure, map these controls into product and finance operations early and confirm Singapore scope and jurisdiction-specific coverage before launch.

If your roadmap could push you from SPI toward MPI obligations, contact Gruv to validate coverage, compliance gating, and rollout assumptions before you lock launch timelines.

Frequently Asked Questions

When should a platform move from SPI to MPI?

Move from SPI to MPI when your activity exceeds the SPI thresholds. If forecasts show you are approaching those limits, start MPI assessment and planning early rather than waiting for a month-end surprise.

What SPI thresholds are explicitly confirmed in MAS materials?

The article discusses SPI threshold signals, but it also says the excerpts used here do not confirm exact SPI threshold figures as primary-text confirmation. What is supported is that SPI and MPI are separated by specified transaction volume and value thresholds, with SPI generally below them and MPI above them. Keep a dated copy of MAS text or a legal interpretation note in your threshold file.

What changed in MAS licensing from August 2024?

These excerpts do not support specific August 2024 licensing-process change claims. For a live filing, verify current MAS application guidance directly and record the version date you used.

Does adding DPT services always trigger extra requirements?

No, a blanket rule is not supported by these excerpts. What is supported is that DPT-related activities are part of regulated-scope analysis, so features involving buying, selling, or facilitating exchange of digital payment tokens should be checked before launch.

Can we rely on third-party MPI summaries for go or no-go decisions?

No. Use MAS primary materials first, including the licensing FAQs, the Payment Services Act, and First Schedule scope checks. Third-party summaries can help with context, but they should not be your decision anchor.

What remains unclear from public excerpts and needs specialist advice?

The excerpts do not provide a full SPI versus MPI obligations map, complete official MPI criteria depth, or dependable timing and fee expectations. Boundary questions can also remain about whether a model is a regulated service, an excluded service, or data-only processing. If your model is near those boundaries or near SPI thresholds, escalate to specialist Singapore counsel.

Asha writes about tax residency, double-taxation basics, and compliance checklists for globally mobile freelancers, with a focus on decision trees and risk mitigation.

With a Ph.D. in Economics and over 15 years of experience in cross-border tax advisory, Alistair specializes in demystifying cross-border tax law for independent professionals. He focuses on risk mitigation and long-term financial planning.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- documents1.worldbank.org/curated/en/099832110082381124/pdf/IDU0d19972...trusted

- home.treasury.gov/sites/default/files/2018-08/A-Financial-Syst...trusted

- mas.gov.sg/regulation/payments/licensing-for-payment-se...trusted

- mas.gov.sg/regulation/paymentstrusted

- oecd.org/content/dam/oecd/en/publications/reports/201...trusted

- sc.edu/study/colleges_schools/law/docs/jilb_vol_19_...trusted

- state.gov/reports/2025-investment-climate-statements/s...trusted

- arnifi.com/blog/fintech-singapore-licensing-mas-approva...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade:

Spain Digital Nomad Visa Guide: Requirements, Application & 2026 Updates

Stop collecting more PDFs. The lower-risk move is to lock your route, keep one control sheet, validate each evidence lane in order, and finish with a strict consistency check. If you cannot explain your file on one page, the pack is still too loose.