Quick Answer

Validate buyer demand first, then complete only the jurisdiction steps required to invoice and stay compliant. For how to start freelance business decisions, use paid signals like discovery calls, proposal requests, or a small paid test before resigning. After that, confirm your first authority action by market: HMRC Self Assessment in the UK, quarterly estimated-tax planning in the US, GST/HST status with CRA in Canada, or permit and licence checks in Dubai. Launch when demand proof, filing readiness, and payment tracking are all in place.

Start your freelance business like an operator, not a hobbyist#

Treat freelancing as a business launch, not a personal identity project. First prove someone will pay for a narrow result. Then add just enough legal and financial structure to stay compliant and keep cash moving.

Define the promise before you touch paperwork#

If you cannot state the buyer, the problem, and the outcome in one or two lines, you are not ready to build anything around it. The fastest way to waste time is to register names, buy tools, and write bios before you know which offer gets replies.

The operator test is simple: can you describe a service someone would reasonably budget for this quarter? The checkpoint is evidence, not enthusiasm. You want actual signals like discovery calls booked, proposal requests, or a small paid test. If your only proof is encouragement from peers or generic forum advice, treat that as noise until a buyer confirms it with money or a clear next step.

Add a lean compliance and cash setup when demand appears#

Add a lean compliance and cash setup once demand starts to show, or immediately if your jurisdiction requires it. Lean matters because overbuilding early burns time, but delaying everything can leave you cleaning up avoidable admin later. That tradeoff is real.

| Market | First checkpoint | Recurring admin | Published detail |

|---|---|---|---|

| US | File an annual income tax return | Pay estimated taxes quarterly | Self-employment tax covers Social Security and Medicare |

| UK | Tell HMRC when you become self-employed | Many self-employed people pay Class 2 and Class 4 National Insurance through Self Assessment | For 2025 to 2026, Class 4 National Insurance is 6% on profits over £12,570 up to £50,270, then 2% over £50,270 |

| Canada | Check whether a GST/HST account is required | Registration depends on what you supply and whether your status requires registration | CRA no longer accepts business number or CRA program account registrations by phone as of November 3, 2025 |

| Dubai | Use the Dubai Development Authority freelance permit route for sole practitioners | Keep permit/licence status current and recheck status by licence number or English business name when needed | Published permit fee AED 7500.00; estimated delivery time 2 working days |

What counts as lean depends on where you operate. In the US, self-employed people generally file an annual income tax return and pay estimated taxes quarterly, and self-employment tax covers Social Security and Medicare. In the UK, you must tell HMRC when you become self-employed, and many self-employed people pay Class 2 and Class 4 National Insurance through Self Assessment. For 2025 to 2026, UK Class 4 National Insurance is 6% on profits over £12,570 up to £50,270, then 2% over £50,270.

In Canada, a GST/HST account depends on what you supply and whether your status requires registration. In Dubai, the Dubai Development Authority offers a formal freelance permit route for sole practitioners, with a published permit fee of AED 7500.00 and an estimated delivery time of 2 working days.

Your verification point here is concrete. Know which authority you answer to first, what registration trigger applies, and what filing rhythm starts once you invoice.

Use checkpoints instead of templates#

Use checkpoints, not templates. A sole practitioner in Dubai, a UK sole trader dealing with HMRC, and a US contractor managing quarterly estimated taxes are not working under the same rules, even if they sell the same service. Canada adds another branch because GST/HST registration depends on supply type and other circumstances, and as of November 3, 2025, the CRA no longer accepts business number or CRA program account registrations by phone.

That is why the rest of this article focuses on decisions and risk, not generic templates. If you cannot absorb delayed client payments and the admin that comes with your market, do not romanticize the jump. Validate demand first, then add the minimum legal and financial structure that protects cash flow and keeps you clean.

Use the same launch test for any early-stage business: prove demand and payment behavior before adding more admin overhead.

Decide if freelancing is economically viable for you#

Treat this as a go-or-no-go decision: if you cannot absorb payment delays and self-managed tax admin yet, do not resign. Keep building pipeline while you still have payroll, predictable pay dates, and employer-managed admin.

Step 1 Account for what your job is currently carrying for you. In the UK, National Insurance is taken from wages before you are paid, and eligible staff are placed into a workplace pension with employer contributions. Gov.uk shows minimum workplace pension contributions of 3% employer, 5% worker, 8% total. That support does not follow you into freelancing.

The same shift shows up in other markets. In the US, self-employed people generally file an annual income tax return and pay estimated taxes quarterly because no employer is withholding. In Canada, gig workers operate as independent contractors and must report and pay tax on self-employment income. In Dubai, the freelancer route is a sole-practitioner permit model, so responsibility sits with you in your own name.

Step 2 Use a blunt timing rule for resignation. If delayed client payments or tax admin would put your cash flow under pressure, treat that as a hold signal and keep validating demand first. Frustration with your job is not the same as operating readiness.

Step 3 Score readiness with a simple operator lens. This is not a validated model; it is just a way to prevent hand-waving. Rate yourself 1 to 5 on:

- Revenue visibility: Do you have evidence like discovery calls, proposal requests, or a paid test?

- Admin tolerance: Can you invoice, track money, and maintain records consistently?

- Compliance complexity: How heavy are your market obligations? In the UK, you can tell HMRC by registering for Self Assessment, and the gov.uk context date shown is 5 October 2025 for required tax-return registration. In the US, net self-employment earnings of $400 can require filing an income tax return.

If any category is a 1 or 2, delay resignation and close that gap first.

Step 4 Set a decision date and trigger condition so this does not drift. Define what must be true by that date: named prospects in pipeline, at least one paid test or active proposal, and your first authority touchpoint identified for your market. If those triggers are not met, stay employed and keep building evidence.

Related reading: How to Create a Business Budget for Your Freelance Business.

Prepare prerequisites and evidence pack before you resign#

Use your employment runway to build operating proof, not just confidence. Before you resign, have a lean launch file and a jurisdiction checklist that makes your first week executable.

Step 1 Build a minimum launch file with four items: a one-sentence offer, a named target buyer list, a weekly outreach cadence, and a weekly rhythm for admin, selling, and delivery. Sanity check: another person should be able to read it and tell who you help, what you sell, and what you are doing next Monday. If the offer is still vague, you are early.

Step 2 Assemble registration and licence requirements before they hold up contracts. In the UK, sole trader registration is required once you earn more than £1,000 in a tax year, late registration can lead to a penalty, and you need a National Insurance number to register for Self Assessment. In the US, registration depends on your location and business structure, and operating under your legal name may not require separate business-name registration. In Dubai, start with the Department of Economy and Tourism process by confirming licence type and setup base first.

Step 3 Create a country-specific tax/admin checklist you can actually follow. In the UK, include HMRC, Self Assessment, and National Insurance tasks. In the US, plan for an annual return and quarterly estimated taxes because no employer is withholding, and track the $400 net earnings filing trigger. In Canada, check GST/HST status against the $30,000 small-supplier threshold rather than assuming immediate registration.

Step 4 Keep a transition memo listing what your employer currently handles that you must replace. PAYE covers Income Tax and National Insurance deductions from wages, and eligible workers are automatically enrolled into a workplace pension with employer contributions. Name each replacement responsibility directly: payroll deductions, pension contributions, filing reminders, and record-keeping.

Validate demand before full legal setup#

Validate demand first: test whether buyers will pay before you add legal, tool, and admin overhead. Use the next 30 to 60 days to collect buyer signal, unless local rules require registration before you can trade, contract, or invoice.

Start with buyer conversations#

Start with conversations, not surveys or more service polishing. Early validation is strongest when you speak directly with likely buyers, hear their problem in their own words, and test whether they will take a paid next step.

Use the offer and target list from the previous section to book short calls. Keep each call practical: what they want to improve, what they use now, what is not working, and what outcome they value. Then offer a small paid first step, such as a tightly scoped project or diagnostic.

Your checkpoint is paid intent, not compliments. Useful signals are booked discovery calls, proposal requests, and paid initial work within that 30 to 60 day window.

Run a focused pipeline sprint#

Run a focused sprint through the channels most likely to convert quickly, starting with your network. One freelancer described the first-client motion this way: "When I started, I wrote personalized emails and LinkedIn messages to my contacts," and said, "This resulted in projects coming my way right away."

Use that as a sequencing lesson, not a guarantee. Start with people who already know your work, make your offer visible to your existing audience, and ask for specific introductions.

Reddit and r/freelance can still be useful for pattern-spotting. Use them to surface common objections and positioning language, not as proof of demand.

Track the sprint in a lightweight pipeline sheet: lead, source, proposal status, follow-up date, expected close date, and next move. Update the next move after each call or email, then review weekly.

Set a threshold for iterating or moving forward#

Set a clear decision rule before you scale admin. If you get conversations but no discovery calls, positioning may be unclear. If discovery calls happen but proposals stall, scope or pricing may be off. If objections cluster around fit, your niche may be wrong.

| Proof artifact | What it usually tells you | What to do next |

|---|---|---|

| Booked discovery calls | Outreach and problem framing are landing | Keep outreach structure, improve call conversion |

| Proposal acceptance pattern | Scope, pricing, or trust signal is working or breaking | Compare accepted vs. rejected proposals for pattern shifts |

| Repeated objections | Buyers are showing the mismatch | Adjust niche, message, or first-step offer before more overhead |

Decision rule: if demand signals stay weak after structured outreach, follow-up, and a real paid offer, iterate the offer before expanding legal/admin setup. If proof artifacts tighten, move forward with more confidence.

Need the full breakdown? Read How to Choose a Niche for Your Freelance Business.

Choose legal and tax setup by jurisdiction#

Choose the minimum setup that lets you work legally and handle tax correctly where you operate. For many one-person freelancers, a sole proprietorship or sole trader setup is enough early on. Revisit structure when contract risk or personal-asset exposure starts to rise.

Map the minimum required setup#

Do not look for one universal setup across the US, UK, Canada, and Dubai. Instead, identify three things for your location: first registration move, tax authority step, and recurring admin you cannot skip.

| Jurisdiction | First registration move | Tax authority step | Recurring admin burden |

|---|---|---|---|

| US | Registration depends on business structure and location, and in some cases you may not need to register. | IRS filing applies early: file an income tax return if net self-employment earnings are $400 or more. | Federal filing plus any state/local registrations, business-name rules, or licenses that apply where you work. |

| UK | If you operate as a sole trader, register for Self Assessment with HMRC, including when you earn more than £1,000 in a tax year. | HMRC Self Assessment is the core step; most self-employed people pay Class 2 and Class 4 National Insurance through it. | Ongoing Self Assessment and National Insurance handling. |

| Canada | A sole proprietorship is an unincorporated business owned by one individual. | Register for GST/HST when CRA conditions apply; small suppliers under the $30,000 threshold may be exempt. | Track gross taxable sales and register once threshold and conditions are met. |

| Dubai | Confirm permit and licence validity before operating; working without a valid permit is illegal in the UAE. | Complete required local tax-registration steps as part of setup. | Keep permit/licence status current and recheck status by licence number or English business name when needed. |

If you are in the US, do not stop at federal guidance. Structure and location drive requirements, so state and local obligations can still apply even without a single federal registration step.

Start lean, then revisit when risk changes#

Start with the leanest structure that fits your current risk, then change it when risk changes. A sole proprietorship is often practical while you are validating demand and handling smaller, simpler contracts.

The tradeoff is liability: sole-proprietor risk can extend to personal property and assets. Use that as your trigger to discuss broader structure options with a local advisor, especially as contract values, commitments, or risk concentration increase.

Use a simple do-now versus do-later rule:

- Do now: filings needed to legally work, invoice, and meet current tax triggers.

- Do later: added entity complexity until revenue and contract risk justify it.

Verify filings before larger contracts#

Before you sign larger contracts, verify your status instead of assuming it. In the UK, that means completing HMRC Self Assessment setup if you are a sole trader and handling National Insurance through that route where applicable.

In Canada, monitor the GST/HST trigger closely. Early low volume does not remove the need to register once conditions are met.

Run one final checkpoint before larger client commitments: confirm required registration and licence status in your jurisdiction, and keep proof in your client file. In Dubai, you can verify licence status by licence number or English business name.

For a step-by-step walkthrough, see How to Choose the Right Business Structure for Your Freelance Business.

Build your pricing and capacity model before you scale outreach#

Before you scale outreach, make sure your pricing can absorb both delivery and the work clients do not pay for directly. If your current rate cannot carry admin, sales time, revisions, and tax overhead, raise the price or narrow scope before adding volume.

Step 1 Calculate your real price floor#

Start with the three common pricing models: hourly, fixed project, and value-based. The model matters less than whether you translated your offer into delivery time, variable cost, and non-billable work.

Use break-even math to set a minimum acceptable quote: Fixed Costs ÷ (Price - Variable Costs) = Break-Even Point in Units. For freelance work, units can be projects, retainers, or booked days. Build a one-page pricing sheet for each offer with:

- scope included and excluded

- expected billable hours

- non-billable time for sales, admin, and client communication

- variable costs (for example, subcontractors or job-specific tools)

- minimum quote that still leaves room for error

Verification checkpoint: compare your estimate with your last two or three real deliveries. If a fixed project regularly takes 8 hours to deliver plus 3 hours of calls and revisions, do not price it as an 8-hour job.

Step 2 Separate billable work from all other work#

Billable hours are only the time you can invoice, and what counts as billable depends on the client agreement. Many freelancers lose margin by quoting from production time only, then absorbing onboarding, proposals, status updates, and collections as unpaid work.

Scaling outreach with a rate that depends on unrealistic utilization creates volume risk. You need more leads just to stay flat, which leaves less room for taxes and compliance costs. In the US, self-employed workers generally owe self-employment tax as well as income tax, and no employer is withholding it for you. Your pricing has to fund that self-managed load.

Step 3 Choose the delivery model you can actually support#

Match your pricing to your operating model before you promise more volume.

| Model | Usually fits | Pricing implication |

|---|---|---|

| Solo freelancer | Targeted, smaller-scope work delivered independently | Price for your own delivery time plus non-billable admin and communication |

| Small team extension | Parallel work across multiple workstreams | Price for coordination, review, subcontracting, and management time |

Stay solo until demand is consistent enough to price management time honestly. If you need extra hands, include that cost before you quote, not after the client says yes.

If you want a deeper dive, read How to Deduct Startup Costs for Your Freelance Business.

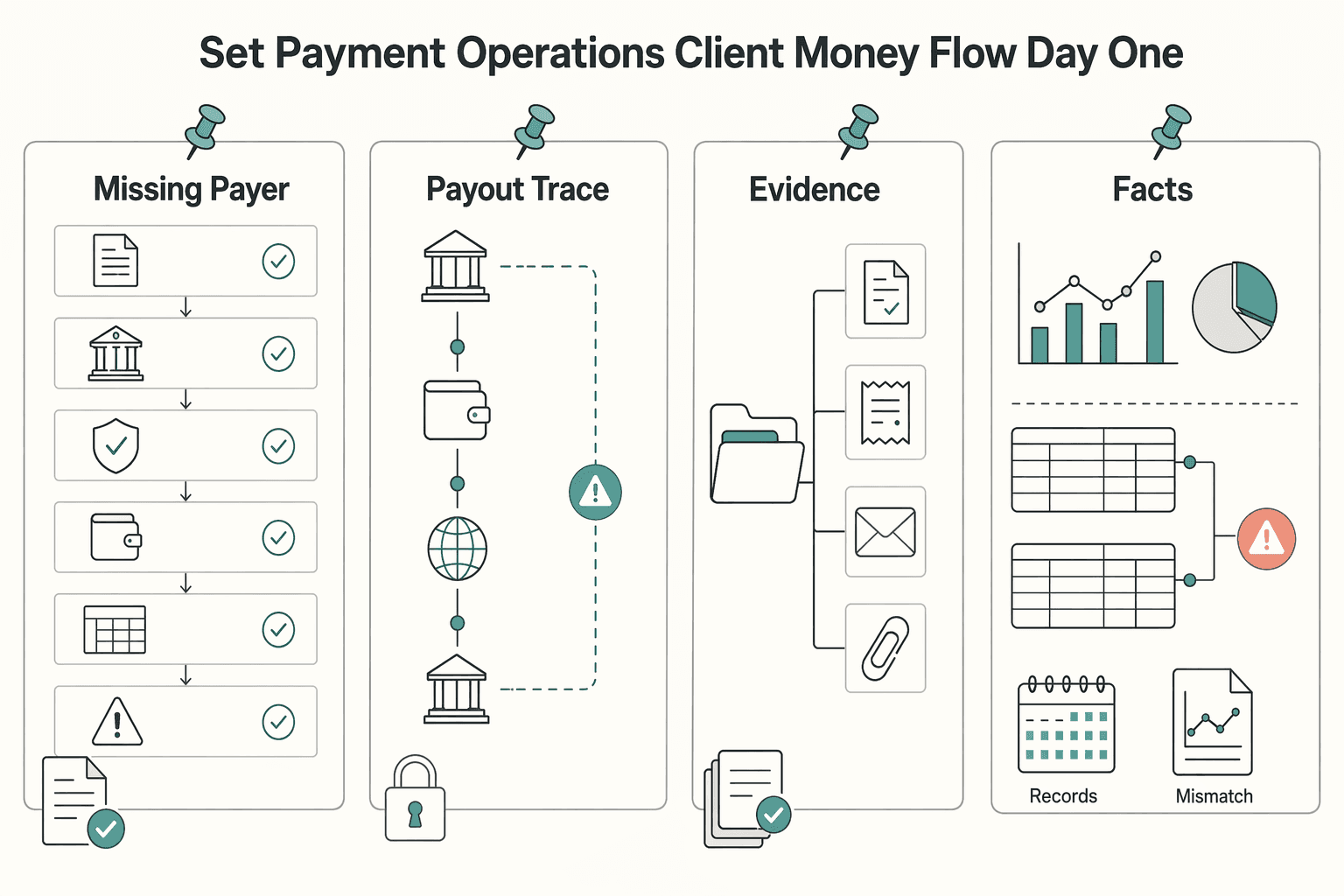

Set up payment operations and client money flow from day one#

Set this up before volume grows: one repeatable money path, early cross-border checks, and records you can trace end to end.

| Step | Focus | Grounded detail |

|---|---|---|

| Step 1 | Define one money path and run every invoice through it | Invoice issued, client payment received, payment confirmed, funds paid out or transferred, transaction reconciled, exception handled |

| Step 2 | Flag cross-border requirements before payment starts | US-to-foreign contractor flows can include Form W-8BEN; validate originator and beneficiary data early |

| Step 3 | Add controls and reconciliation that are audit-ready | Use payout approvals or policy-gated releases where your provider supports them; keep traceable payout records; CHAPS usually operates 6am to 6pm, Monday to Friday |

| Step 4 | Keep a short failure-mode checklist | Missing payer reference or invoice number; wrong rail/currency/window assumptions; documentation gaps; missing reconciliation artifacts |

Step 1. Define one money path and run every invoice through it. Write the flow once and reuse it: invoice issued, client payment received, payment confirmed, funds paid out or transferred, transaction reconciled, exception handled. Keep evidence at each stage. Your system can be simple, but it should clearly show income and expenses and support financial/tax reporting; in the UK, your records should also map cleanly to income, costs, and profit.

Verification checkpoint: for each invoice, you should be able to pull the invoice, payment confirmation, bank or platform receipt, and reconciliation note quickly.

Step 2. Flag cross-border requirements before payment starts. For cross-border clients, collect the required payment and tax details before work begins. In US-to-foreign contractor flows, that can include Form W-8BEN for the payer/withholding agent. Also validate originator and beneficiary data early. FATF Recommendation 16 emphasizes payment-message data quality, and incomplete or mismatched beneficiary/reference details are a common reason cross-border payments get delayed.

Step 3. Add controls and reconciliation that are audit-ready. Use payout approvals or policy-gated releases where your provider supports them, and keep traceable payout records for finance review. Reconcile invoices against confirmations on a fixed routine so exceptions are found early. For UK same-day timing assumptions, account for CHAPS operating hours: usually 6am to 6pm, Monday to Friday. Treat that as an operating window, not a settlement guarantee.

Step 4. Keep a short failure-mode checklist. Review this before chasing late payments or withdrawals:

- missing payer reference or invoice number

- delayed settlement from wrong rail/currency/window assumptions

- documentation gaps (for example W-8BEN or incomplete beneficiary details)

- missing reconciliation artifacts that create month-end and year-end reporting issues

Treat payment operations as part of delivery. If an invoice is paid but not traceable, the work is not operationally finished.

You might also find this useful: How to Pay US-Based Freelancers from the UK.

Common mistakes that stall new freelancers and how to recover#

Most early stalls come from process gaps, not talent: inconsistent follow-up, late filings, and over-reliance on one client source.

Step 1. Replace vague networking with a weekly follow-up cadence. Generic "just network" advice only works if you run a repeatable follow-up system. Treat outreach as a weekly sequence of new contacts, follow-ups, and warm reactivation. By Friday, you should be able to show who you contacted, who you followed up with, and the next touch date for each active lead.

Step 2. Prioritize jurisdiction-critical registration before bigger deals. Handle required registrations, licenses, and permits before contracts get larger. In the US, requirements depend on your activity and location, and many small businesses need a combination of licenses and permits. In Dubai, a formal Freelance License can be part of setup. Before signing, confirm what applies in your jurisdiction and keep filing receipts or approval emails in your launch folder.

Step 3. Put tax on a monthly calendar now, not later. Treat tax compliance as an operating routine from month one. In the UK, you must tell HMRC by 5 October if you need to complete a tax return for the previous year, and most Class 2 and Class 4 National Insurance is handled through Self Assessment. In Canada, GST/HST registration becomes mandatory once you are no longer a small supplier, with the reference threshold at $30,000 ($50,000 for public service bodies) over the last four consecutive calendar quarters and in any one calendar quarter. A monthly bookkeeping, threshold, and deadline check will not guarantee compliance, but it does prevent the predictable scramble.

Step 4. Diversify client acquisition before one channel becomes a dependency. Keep your best-performing channel, but do not let it become your only one. Customer concentration risk is real: reliance on a small number of customers or one source can destabilize revenue and cash flow. Recovery is straightforward: build a second acquisition channel and a referral loop while your first channel is still working.

Related: How to Get a Business License in Dubai as a Freelancer.

Copy and use this 30-day launch checklist#

Use this as a 30-day operating cadence, not a universal legal sequence. Prioritize real buyer signal first, unless your jurisdiction requires registration or a licence before you can contract.

| Stage | Focus | Checkpoint |

|---|---|---|

| Week 1 | Write down one service, one target buyer, one problem, and one concrete outcome. Build a short buyer list and an outreach routine you can run for two weeks | Explain your offer in two plain sentences |

| Week 2 | Run real conversations and capture objections word for word. If prospects are unclear on scope, timing, or value, adjust positioning now instead of masking weak demand with paperwork | Keep an objection log and a short note on what changed in your offer |

| Week 3 | Complete jurisdiction-critical setup. Registration depends on your location and business structure | Save filing receipts, confirmation emails, business name records, and account numbers in one folder |

| Week 4 | Set a pricing model you can defend on an invoice, then define billing timing, payment terms, and receipt confirmation | If a real cycle is not possible yet, simulate proposal → invoice → payment confirmation → reconciliation |

| Final gate | Proceed when demand proof, legal basics, and payment operations are all in place | If one is weak, you are not launch-ready yet |

Week 1: define the offer and your go/no-go rule. Write down one service, one target buyer, one problem, and one concrete outcome. Build a short buyer list and an outreach routine you can run for two weeks. Market research should reduce risk, so decide in advance what counts as viability for you (for example, booked calls, repeated pain points, or prospects willing to review a proposal). Checkpoint: explain your offer in two plain sentences.

Week 2: validate demand before expanding admin. Run real conversations and capture objections word for word. If prospects are unclear on scope, timing, or value, adjust positioning now instead of masking weak demand with paperwork. Checkpoint: keep an objection log and a short note on what changed in your offer.

Week 3: complete jurisdiction-critical setup. Registration depends on your location and business structure. In the US, some people using their legal name may not need formal name registration. In the UK, sole traders use HMRC Self Assessment registration, and late registration can lead to penalties. In Canada, confirm whether you need a GST/HST account; CRA no longer accepts BN or CRA program account registrations by phone from November 3, 2025. Checkpoint: save filing receipts, confirmation emails, business name records, and account numbers in one folder.

Week 4: finalize billing and recordkeeping. Set a pricing model you can defend on an invoice, then define billing timing, payment terms, and receipt confirmation. A defined billing system helps reduce late or missing payments. Track invoices, payments, expenses, and supporting documents from day one; in the UK, an invoice may need to be recorded in one tax year even if cash arrives in the next. Checkpoint: if a real cycle is not possible yet, simulate proposal → invoice → payment confirmation → reconciliation.

Final gate: launch only when all three are working together. Proceed only when demand proof, legal basics, and payment operations are all in place. If one is weak, you are not launch-ready yet. Your evidence pack can stay small: buyer list, objection notes, registration proof, invoice template, and records that clearly show income and expenses.

This pairs well with our guide on How to Build an Antifragile Freelance Business: Financial Core, Compliance Firewall, and Shock Absorbers.

Frequently Asked Questions

What should I do first, find clients or register the business?

There is no universal order, because the right sequence depends on your jurisdiction and the kind of client you want. Start with real client conversations, but if local rules or buyer procurement require registration or a licence before contracting, do that early and keep the filing receipt or approval email in your launch folder.

Can I start a freelance business with no experience if I already have domain skills?

Possibly, but domain skills are not the same thing as proven client delivery. The practical test is whether you can package those skills into a narrow offer, get discovery calls, and convert at least some of them into paid work before you bet your income on it.

Do I need business name registration before I send my first proposal?

Not always. What matters is accuracy: do not present an unregistered business name as if it is already established, and check whether your target client needs formal registration or licence details before onboarding. A common failure mode is winning interest, then stalling because procurement asks for documents you have not started.

How do I decide between staying employed and going full-time freelance?

Compare your current employment package with freelance reality, not just your rate card. If you cannot absorb delayed client payments and jurisdiction-specific tax admin, such as quarterly estimated taxes in the US or self-managed filings in the UK and Canada, keep the job and build pipeline first.

What do I lose when leaving a job with payroll and workplace pension benefits?

In the UK, PAYE is the employer payroll system that collects Income Tax and National Insurance from employment pay. That admin is not on you while you are employed. You may also lose employer pension contributions: under workplace pension rules, both you and your employer usually pay in, with contributions based on earnings between £6,240 and £50,270 in most automatic enrolment schemes.

How should UK freelancers plan for HMRC and National Insurance from month one?

If you are operating as a sole trader, register for Self Assessment when required and do not leave it to year end. HMRC says you must tell it by 5 October 2025 if you need to complete a tax return for the previous year. Most self-employed Class 2 and Class 4 National Insurance is handled through Self Assessment. Your checkpoint is simple: keep proof of registration, a monthly bookkeeping review, and calendar reminders for filing dates.

What changes if I am setting up in Dubai versus the US, UK, or Canada?

The setup path is not equivalent across these markets. In Dubai, one early choice is free zone or mainland, and a free-zone company cannot trade within the UAE without a specific mainland licence. In the US, self-employed workers generally file annually and pay estimated taxes quarterly, with an income-tax return required if net self-employment earnings are $400 or more. In Canada, a GST/HST account becomes mandatory once the CRA conditions for no longer being a small supplier are met, while the UK route usually runs through HMRC Self Assessment and self-employed National Insurance.

Try a related tool

A former tech COO turned 'Business-of-One' consultant, Marcus is obsessed with efficiency. He writes about optimizing workflows, leveraging technology, and building resilient systems for solo entrepreneurs.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- dda.gov.ae/en/registration-licensing/setting-up-a-busin...trusted

- irs.gov/businesses/small-businesses-self-employed/se...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- sba.gov/business-guide/launch-your-business/register...trusted

- sba.gov/business-guide/plan-your-business/calculate-...trusted

- canada.ca/en/revenue-agency/services/tax/businesses/to...external

- canada.ca/en/revenue-agency/services/tax/businesses/to...external

- fatf-gafi.org/content/dam/fatf-gafi/recommendations/Explan...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Deduct Startup Costs for Your Freelance Business

**If you want to claim startup costs safely, run a system that classifies each expense, confirms business start timing, applies startup deduction and amortization rules, and saves proof for every decision.**

How to Get a Business License in Dubai as a Freelancer

Choose your lane first, then compare prices. The right setup depends on four filters: where your revenue will come from, what activity you will be licensed for, which authority will regulate you, and whether you are staying solo or planning a team. A low year-one price can still be the wrong choice if it limits how you contract, expand, or stay compliant later.

How to Pay US-Based Freelancers from the UK

Your ability to attract and keep strong US freelance talent depends less on budget than on how you operate. Strong freelancers often work like serious one-person businesses, and they start evaluating you from the first interaction. Compliance and payment handling are not back-office details. They are early proof that you will be easy to work with, careful with details, and worth prioritizing.