Quick Answer

Separate the problem into three lanes immediately: deceptive earnings claims, first-party refund scams, and suspected contractor work falsification. Route any case with consumer-facing claim language plus payment harm to legal under FTC Act and Business Opportunity Rule exposure, and keep anomaly-only files in enhanced monitoring until a second internal source confirms risk. Use one evidence packet per case with claim text, disclosure version, complaint record, payout status, and named approver so finance and compliance can defend the disposition later.

Why this fraud topic is hard for platform risk teams#

This topic is hard because the public evidence is fragmented, while your internal decisions need to be specific, defensible, and fast. If you treat search coverage as a complete map of first-party fraud on gig platforms or suspected contractor work falsification, you will likely build controls for the wrong problem.

Step 1. Treat public coverage as a partial signal#

Public coverage in this pack is incomplete and high-level. It mixes broad gig-economy commentary with material that is not directly usable for enforcement analysis. It does not give you a usable taxonomy for suspected contractor work falsification.

That gap matters because a gig transaction is not a simple buyer-seller exchange. One source in the pack frames platform risk as a network problem rather than a bilateral one and argues that digital trust makes or breaks transactions. That is a reasonable operating assumption for risk teams, but by itself it is not enough to define misconduct categories, thresholds, or case standards.

Your first checkpoint is source quality. Before you let a source shape controls, check whether it is accessible, primary, and relevant to the abuse type you care about. In this pack, one legal source is blocked by a web application firewall, and another scraped source is only an insurance training listing. Those are red flags, not foundations.

Step 2. Separate the business problem from the evidence problem#

The business problem is immediate. The evidence problem takes longer. Public material here does not provide directly usable detail on contractor-side falsified-work patterns. If you blur those together, teams tend to copy controls built for other abuse types.

A practical rule helps here: if consumer-facing claims are involved, assume legal sensitivity. If suspected falsified work is involved, assume evidentiary weakness until you can corroborate it internally. That keeps you from overstating certainty in closure notes or taking punitive action off a single anomaly.

A common failure mode is merging refund abuse, deceptive claims, and contractor behavior into one bucket. You then discover later that none of your records answer the regulator's actual question.

Step 3. Organize around decision checkpoints, not labels#

For compliance, legal, finance, and risk owners, the real job is not naming the fraud perfectly on day one. It is setting decision checkpoints that will still hold up later. You need a clear record of what was alleged, what was observed, what was verified, who approved the next step, and what evidence was missing at the time.

That discipline matters more because the source material treats gig work as mainstream. One article says nearly half of the US workforce is expected to engage in gig work this year and that the market is on track to top $600 billion. Those figures are not regulator-verified statistics, but they do explain why risk teams cannot treat this as a niche edge case.

The next move is to define the fraud surface precisely enough that your controls, escalation rules, and audit trail map to distinct actors instead of one catchall story.

Define the fraud surface before you design controls#

Define the fraud surface first, or your controls will collapse distinct risks into one workflow. Keep these three lanes separate from the start:

Deceptive earnings claims(FTC Act and Business Opportunity Rule exposure)First-party refund scamsSuspected contractor work falsification

If you merge these lanes, case records stop answering core questions: who was harmed, what was misstated, and what evidence is verified.

For deceptive earnings claims, treat the FTC action on Arise Virtual Solutions (July 2, 2024) as a concrete enforcement signal. The FTC said Arise allegedly misled consumers about earnings and marketed a business opportunity without complying with the Business Opportunity Rule, which points to risk around truthful disclosure of the basis for earnings claims. Keep your checkpoint tight in this lane: confirm the issue is tied to consumer-facing representations, not only unusual account behavior.

Use that matter as a signal, not a full taxonomy. The release is in consumer protection, and the settlement terms are proposed, including $7 million for consumer refunds and clearer information. That supports tighter review of work-at-home earnings claims, but it does not define all contractor-side falsified-work patterns.

Document known unknowns in the classification memo:

- No reliable actor-level loss split across customer, contractor, merchant, and platform from the provided sources

- No validated prevalence data for refund abuse from the provided sources

- No mature public taxonomy for contractor work falsification in these materials

If evidence is weak, classify the issue as a monitoring hypothesis instead of a confirmed pattern. This keeps you from overbuilding controls around a pattern your records cannot yet prove.

For a step-by-step walkthrough, see How Platforms Stop Affiliate Fraud Before Commissions Are Paid.

Gather the prerequisites and evidence pack before rollout#

Before you add controls, lock down ownership, records, and escalation proof standards so cases can be reviewed and defended.

| Prerequisite | What to lock down | Key details |

|---|---|---|

| Assign clear owners | Map one named owner to each artifact and decision point, with backups | Complaint interpretation; payout impact review; log retrieval; operational sign-off |

| Build a minimum evidence pack | Start with claim substantiation files, disclosure versions, complaint logs, payout exception logs, and case closure notes | For suspected falsified work, include the underlying work, acceptance, or transaction record |

| Map current gates and record history | Document what KYC, KYB, AML, payout approvals, or virtual account event history capture, who can access it, and how long it is retained | Use this to check whether records can answer core questions during escalation |

| Use one internal evidence standard | Define and train to allegation, corroborated signal, and confirmed first-party fraud | Treat outside commentary as context, not proof |

- Assign clear owners before rollout.

Use a small, decision-capable group and map one named owner to each artifact and decision point, with backups. The goal is practical coverage: complaint interpretation, payout impact review, log retrieval, and operational sign-off.

- Build a minimum evidence pack, not a large archive.

Start with claim substantiation files, disclosure versions, complaint logs, payout exception logs, and case closure notes. For suspected falsified work, include the underlying work, acceptance, or transaction record rather than relying only on summaries. Use a simple file rule: each item should have a date range, source location, and version label.

- Map current gates and record history before adding new ones.

If your workflow already includes KYC, KYB, AML, payout approvals, or virtual account event history, document what is captured, who can access it, and how long it is retained. This checks whether your records can answer core questions during escalation instead of adding friction you cannot later explain.

- Use one internal evidence standard for escalation.

Define and train to three labels: allegation, corroborated signal, and confirmed first-party fraud. Treat outside commentary as context, not proof: the August 2018 paper Trust mechanisms and online platforms: a regulatory response is useful for framing questions, but the series states papers "have not undergone formal review and approval."

Related: Network Effects in Payment Platforms: How More Contractors Make Your Platform More Valuable.

Build an actor-by-actor risk map your team can actually use#

Use a living risk register that separates actor, allegation, owner, evidence, and review hooks, and label any unverified row as an allegation.

| Actor | Working abuse pattern | Control owner | Detection signal to verify | Legal review hook | Payment-state hook |

|---|---|---|---|---|---|

| Customer | First-party refund scam (kept separate) | Risk ops + support | Complaint, refund request, and service/transaction record do not align | Internal Consumer Protection review; add FTC Act or Business Opportunity Rule only after counsel review | Virtual Accounts credit/return history, relevant Payouts state, AML hold outcome |

| Contractor | Suspected falsified work claim (kept separate) | Risk ops + finance + service ops | Work record, service acceptance record, and transaction record mismatch | Internal Consumer Protection review if relevant to consumer harm or misleading representations | Payout release state, reversals, and related AML hold outcome |

| Merchant | Merchant-side complaint or refund mismatch | Partner ops or finance | Payout exception log, complaint log, and closure notes align to one case ID | Internal legal review as needed | Exact payment-event history available in your systems |

| Platform | Disclosure/substantiation mismatch | Consumer Protection counsel + compliance/marketing owner | Complaint language cannot be matched to the disclosure version in force at that time | FTC Act, Business Opportunity Rule, and internal Consumer Protection review flags (as triage prompts, not conclusions) | Add payment context only if it is part of the same file |

Keep first-party refund and contractor falsified-work rows separate even when they touch one case. The refund row tests whether the claim matches the service/transaction record; the contractor row tests whether the work record is reliable.

Use one readiness check for every row: one named control owner and one named evidence source. If either is missing, keep the row in monitoring instead of escalating it.

Treat legal and payment fields as review prompts, not verdicts. If relevant tax documentation appears in the same file, record it exactly: Form 1116 is used by individuals, estates, or trusts to claim the foreign tax credit, and corporations file Form 1118; unused foreign taxes limited by the credit cap may be carried back 1 year and forward up to 10 tax years.

Set the minimum control stack and where to add friction#

Once your risk map is stable, set a minimum stack first, then add friction only where case patterns justify it.

| Layer | Controls | Use notes |

|---|---|---|

| Baseline controls | Earnings-claim substantiation; disclosure governance; complaint triage SLA; immutable audit trail | Start here so the file shows what claim was live, who approved it, which disclosure version applied, and how the complaint moved from intake to closure |

| Transaction controls | Positive Pay-style reconciliation checks; payout velocity checks; idempotent case actions in Payouts | Add these after baseline controls; test replay behavior directly and roll out narrowly if false positives rise |

| KYB/KYC/AML and tax-context friction | Use KYB, KYC, and AML gating as a second layer for higher-risk patterns; use only records already relevant to the case | Examples named in the article: W-8, W-9, 1099, DAC7, FEIE, or FBAR-related records |

Step 1. Put the table-stakes controls in place first#

Start with four baseline controls: earnings-claim substantiation, disclosure governance, a complaint triage SLA, and an immutable audit trail. Your file is only defensible if you can show what claim was live, who approved it, which disclosure version applied, and how the complaint moved from intake to closure.

Keep substantiation caseable. For each material claim, store the supporting record, approver, and publication window together so a reviewer can retrieve the exact claim language and disclosure version tied to a historical complaint.

Treat the complaint SLA as an operating control, not just a metric. Assign a named owner, define intake, and set the handoff point to legal review so support closure and risk review do not drift out of sync.

Step 2. Add transaction controls before broad identity friction#

After baseline controls, add transaction controls: Positive Pay-style reconciliation checks, payout velocity checks, and idempotent case actions in Payouts. The goal is one consistent payment action per case, with a clear event trail.

Test replay behavior directly. If the same case event is sent twice, confirm the system records one action for that case ID and does not stack duplicate holds, reversals, or releases.

Roll out narrowly. If false positives rise, tighten triggers and limit scope to higher-risk markets or programs before expanding.

Step 3. Add KYB/KYC/AML and tax-context friction only when facts support it#

Use KYB, KYC, and AML gating as a second layer for higher-risk patterns, not as default friction for every case. For tax and identity context, use only records already relevant to the case, for example W-8, W-9, 1099, DAC7, FEIE, or FBAR-related records, and avoid over-collecting.

For FEIE-related review, stay precise. The IRS physical presence test uses 330 full days during any period of 12 consecutive months, and those days do not have to be consecutive. The test applies to U.S. citizens and U.S. residents, and FEIE depends on filing a U.S. tax return that reports the income. The maximum exclusion is adjusted by tax year, including $130,000 (2025) and $132,900 (2026).

Do not treat IRS LB&I practice units as binding authority for adverse action logic; the IRS states that material is not an official pronouncement of law and cannot be relied on as such.

Set escalation rules legal and finance can defend#

Escalate quickly when public deception and payment harm appear together, and avoid punitive action when you only have anomaly signals.

Step 1. Define four internal lanes with clear entry criteria. Keep routing consistent so each case has a defensible owner and evidence packet.

| Lane | Use it when | Minimum packet |

|---|---|---|

| Ops review | Facts are incomplete and consumer harm is not yet shown | Case summary, event timeline, payout status, complaint check |

| Legal review | A public claim, disclosure issue, or likely consumer deception appears | Claim screenshot, disclosure version, complaint or refund record, payout impact |

| Executive incident review | The case may affect multiple programs, markets, or senior reporting | Legal memo, loss estimate, affected population, remediation owner |

| Regulator-notification assessment | Facts suggest external inquiry risk or a material consumer-protection issue | Closure-ready chronology, approvers, preserved evidence, draft issue statement |

Step 2. Escalate immediately when deceptive claims and payment harm are in the same file. If misleading public earnings or opportunity claims are tied to monetary harm, route directly to legal. The FTC's July 2, 2024 action against Arise alleged misleading earnings representations and referenced Business Opportunity Rule compliance, and the announcement described a proposed $7 million consumer-refund settlement. Treat this pattern as FTC Act and Business Opportunity Rule exposure, not routine dispute handling.

Before legal accepts the case, confirm the file includes the exact claim language, the disclosure version in force at the time, and the linked payment or refund harm.

Step 3. Keep anomaly-only cases in enhanced monitoring until a second source confirms risk. If you only have behavioral anomalies and no consumer harm, hold the case and require confirmation from your own records before offboarding, clawbacks, or similar punitive action.

For tax-related explanations, verify filings, not notes. Form 1116 is used to claim the foreign tax credit and compute its limit; only certain foreign taxes generally qualify, and each Form 1116 checks only one category box.

Step 4. Log every escalation decision so it is defensible later. Record reason code, approver, date, and closure rationale for every lane change. A closed file should show why it escalated, what evidence was reviewed, and why it closed without relying on side-channel messages.

This pairs well with our guide on Fraud Detection on Payment Platforms with Rules and Machine Learning.

Investigate suspected contractor falsification in a fixed order#

Use one repeatable investigation order for every flagged case. This is an internal control workflow to keep decisions explainable, not a claim of a universal or legally required standard.

Step 1. Freeze the payout path where your controls allow, and preserve payment evidence first. If you use Virtual Accounts and Payouts, retain the full event history for credits, reversals, release attempts, manual holds, and status changes before case debate starts. Your checkpoint is whether a reviewer can rebuild the payout timeline from work completion to release without relying on chat notes or memory.

Step 2. Verify identity and account integrity before judging the work claim. Review the KYC, KYB, and AML record already tied to the account, including identity status, recent profile or entity changes, prior reviews, and open compliance holds. If identity integrity is still unclear, treat that as unresolved and avoid jumping straight to a falsified-work conclusion.

Step 3. Reconcile work evidence to money movement, and document every gap. Match work evidence, service acceptance records, complaint or refund events, and the ledger posting for the same transaction path. A defensible file shows whether work was accepted, reversed, partially refunded, or never accepted, and whether the ledger reflects that sequence.

Step 4. Choose disposition with two yes-or-no checks: is identity integrity unresolved, and is work-to-payment reconciliation unresolved? Use those checks to pick a clear outcome and closure note.

| Outcome | Use it when | Minimum closure note |

|---|---|---|

| Release | Identity is cleared and work, acceptance, and ledger records reconcile | Why funds were released and what evidence cleared the case |

| Partial hold | Some funds are supported, but a defined portion remains unresolved | Amount held, reason, and what evidence is still missing |

| Full hold | Identity or payment reconciliation remains materially unresolved | Exact blocking issue, reviewer, and next review date |

| Offboarding recommendation | The file shows repeated or serious integrity issues your policy treats as exit-level | Policy basis, evidence summary, and approval path |

If you cannot point to preserved payout events, current identity status, and an acceptance-to-ledger match, the case is not ready for final disposition.

Related reading: How Platforms Detect Free-Trial Abuse and Card Testing in Subscription Fraud.

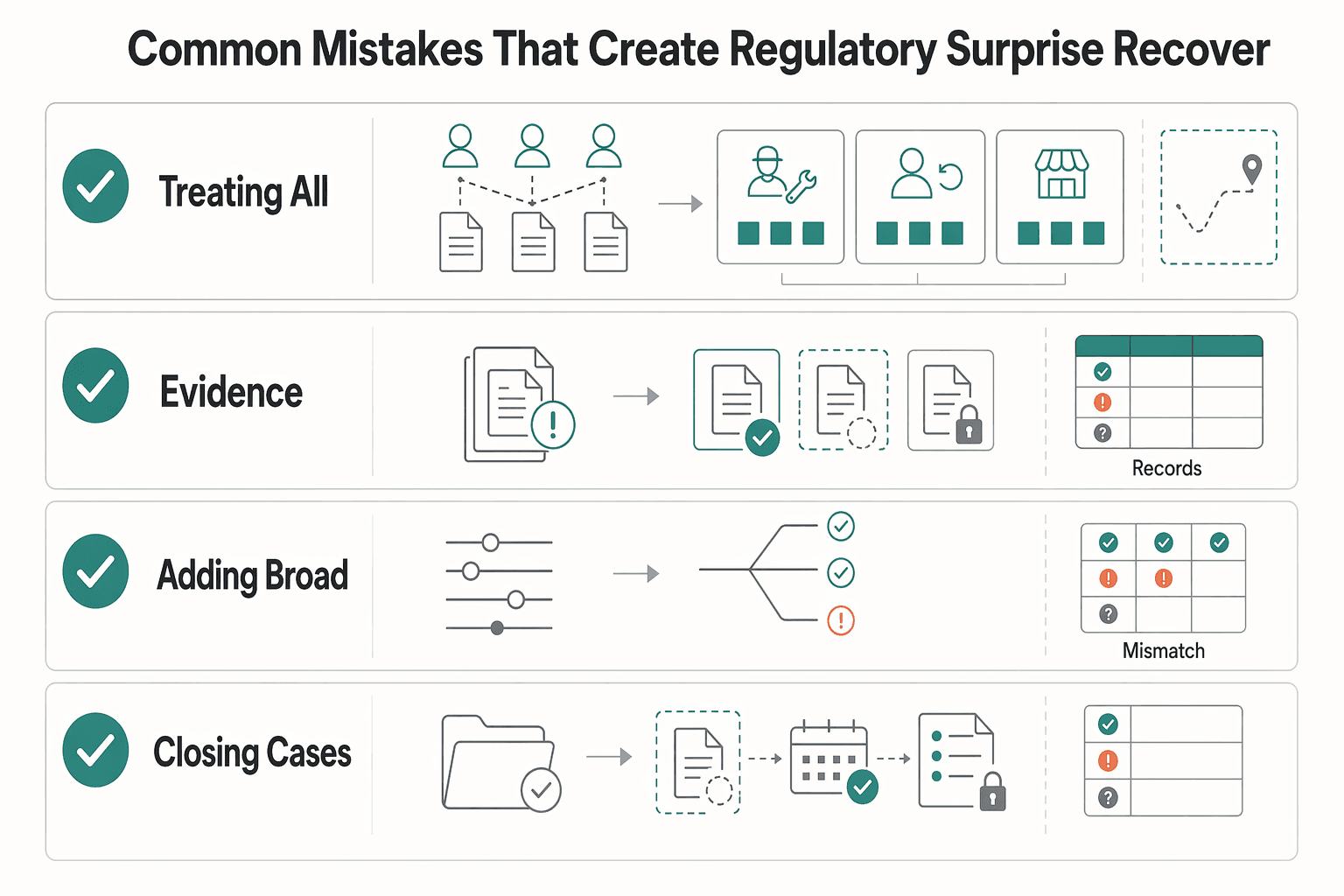

Common mistakes that create regulatory surprise and how to recover#

Regulatory surprise usually comes from weak evidence discipline: teams overstate certainty, apply broad controls, and close files without audit-ready reasoning.

| Mistake | Recovery | What to check |

|---|---|---|

| Treating all first-party issues as one bucket | Split reporting by actor and keep an explicit unknown pattern lane | Who acted, what payment state changed, and what evidence is verified versus missing |

| Filling evidence gaps with generic gig-economy stats | Mark unknowns and keep method limits visible in the case file | Use AI-generated summaries as discovery aids only; the full article remains the authoritative version of record |

| Adding broad KYC, KYB, or AML friction everywhere | Tie added controls to named failure modes in the file | Point to the trigger, the control applied, and the outcome |

| Closing cases with thin notes | Require an audit-ready closure summary every time | Include control decision, legal or policy rationale, evidence relied on, open gaps, reviewer, and follow-up date |

Mistake 1: treating all first-party issues as one bucket. Recovery: split reporting by actor and keep an explicit unknown pattern lane. Track contractor falsification claims, customer refund abuse, and merchant-side exceptions separately so legal and finance can see who acted, what payment state changed, and what evidence is verified versus missing.

Mistake 2: filling evidence gaps with generic gig-economy stats. Recovery: mark unknowns and keep method limits visible in the case file. The Yale Law Journal essay dated 31 January 2025 frames gig-economy harms as requiring legal, regulatory, and policy interventions, but it does not provide a validated fraud-loss split or contractor fraud taxonomy for your cases. Treat AI-generated summaries as discovery aids only; the full article remains the authoritative version of record.

Mistake 3: adding broad KYC, KYB, or AML friction everywhere. Recovery: tie added controls to named failure modes in the file, such as unresolved identity changes, linked business-detail changes, payout-path anomalies, or acceptance-to-ledger mismatches. Your check is simple: can you point to the trigger, the control applied, and the outcome.

Mistake 4: closing cases with thin notes. Recovery: require an audit-ready closure summary every time: control decision, legal or policy rationale, evidence relied on, open gaps, reviewer, and follow-up date. If finance or counsel still needs verbal context to understand the decision, the note is not complete.

Start with this copy-paste checklist for the next 30 days#

-

Publish your fraud-surface definition with explicit known unknowns and owner sign-off. Start with the patterns you can actually observe, for example deceptive claim complaints and suspected contractor falsification, and write down what is still unverified. Name the accountable owner and escalation path so decisions are traceable.

-

Stand up the actor-based risk table before adding new enforcement rules. For each actor row, map the pattern, control, evidence source, and escalation owner. If a row lacks usable evidence, keep it in monitoring status instead of treating it as a confirmed abuse pattern.

-

Implement the minimum control stack, then test two live scenarios. Pressure-test one deceptive-claim complaint flow and one suspected contractor-falsification flow. In both tests, confirm you can retrieve the exact claim/disclosure context, preserve identity and payout event history, and show how the case moved from intake to disposition.

-

Add identity friction only where the trigger is clear and documented. Use targeted checks rather than broad reverification, and log who triggered the step and why. Where enabled, liveness detection helps confirm that a real, live human is physically present during verification; balance that control against user friction.

-

Run a weekly escalation review with legal, finance, and risk, and grade closure quality. Review open escalations, remediation status, and weak documentation, then tighten what failed. A closed case should include reason code, evidence reviewed, approver, final disposition, and follow-up date.

Frequently Asked Questions

What is first-party fraud on gig platforms?

In plain terms, it is abuse by a participant who appears legitimate and uses that legitimate-looking position to cause loss. From the sources here, the best-supported example is deceptive earnings claims in gig-work marketing, along with consumer refund exposure in the proposed FTC settlement. What the public record does not yet provide is a validated taxonomy for contractor-side falsified work, so keep that area labeled as a monitoring hypothesis unless your own case evidence is stronger.

What enforcement signal should risk owners prioritize first?

Start with the Federal Trade Commission signal on deceptive earnings claims. On July 2, 2024, the FTC announced action against Arise Virtual Solutions over alleged deceptive pay representations in gig-work marketing, and the press release describes a proposed settlement that would require $7 million for consumer refunds. That matters because it ties risk to consumer-facing claims, not just internal abuse patterns.

What minimum controls should every platform have?

If resources are tight, start with claim substantiation, disclosure review, complaint monitoring, escalation rules, and an audit trail tied to payment decisions. A simple checkpoint is whether every public earnings claim has a substantiation file, the approved disclosure version, and a named approver you can identify later. A common failure mode is having good transaction controls but no retained basis for what marketing or recruiting promised.

What is still unknown from current public coverage?

Assume three major gaps remain: reliable prevalence, actor-level loss splits, and validated categories for contractor falsified-work behavior. That means you should not pretend the public sources can tell you how much loss sits with customers versus contractors versus merchants. If your dashboard forces a hard classification anyway, use an "unknown pattern" bucket rather than inventing precision.

How should we prioritize controls when resources are limited?

Reduce legal exposure first, then expand abuse controls. In practice, that means fixing consumer-facing earnings claims and disclosures before building broad punitive logic for suspected work falsification, because the FTC action and Business Opportunity Rule context create a clearer enforcement path in the current record. Once that layer is clean, add transaction abuse controls where you can verify the trigger and preserve evidence.

When should legal be pulled in immediately?

Bring legal in as soon as potential consumer deception and monetary harm show up in the same case file. The clearest trigger is a complaint, ad, or onboarding message that may have misstated likely pay, paired with potential refund exposure. That is especially true where Business Opportunity Rule exposure is plausible. For verification, make sure the escalation packet includes the exact claim language, the disclosure version shown, complaint records, and the linked payment or refund history.

Try a related tool

Connor writes and edits for extractability—answer-first structure, clean headings, and quote-ready language that performs in both SEO and AEO.

Sources

- app.mt.gov/cal/attachment/167796trusted

- comptroller.nyc.gov/wp-content/uploads/documents/RFP_NYC-Comptro...trusted

- congress.gov/event/117th-congress/senate-event/331185/texttrusted

- cppa.ca.gov/regulations/pdf/part9_all_comments_combined_...trusted

- downloads.regulations.gov/OCC-2025-0009-0126/attachment_1.pdftrusted

- fdic.gov/formsdocuments/apgm.pdftrusted

- ftc.gov/news-events/news/press-releases/2024/07/ftc-...trusted

- gsa.gov/system/files/Alliant%203%20Master%20Contract...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors

At scale, the hard part is not the acronyms. It is deciding sequence, ownership, and evidence when Form 1099-K, Form 1099-NEC, Form W-8BEN/W-8BEN-E, and DAC7 do not line up cleanly. If you run a high-volume marketplace, put controls in the right order and define clear stop points where legal or tax takes over.

When Contractor Growth Actually Increases Payment Platform Value

Treat network effects as something to verify, not something to assume from user growth or network size. This list is meant to help you test whether expansion is creating real platform value or just adding surface area.

How Positive Pay Controls Check Fraud in Digital Payment Platforms

This list is for compliance, legal, finance, and risk owners who need to use Positive Pay without turning it into a bigger build than the risk justifies. The goal is practical: reduce check and electronic transaction fraud while keeping decisions and approvals auditable across products and bank relationships.