Quick Answer

Set 31 January as the default filing date, then require legal approval for any local deviation. Under Council Directive (EU) 2021/514, the platform operator holds the reporting duty, so document the Member State of single registration early and keep that decision with authority support. Use a known-versus-unknown timing table, force unresolved points closed in Q4, and submit with a controlled evidence pack that includes scope rationale, seller classification logic, lineage records, filing extract, and submission acknowledgment.

How DAC7 reporting deadlines vary by month#

Treat DAC7 as a year-round control process, not a January filing task. For in-scope operators with EU-resident sellers, the risk is often not awareness of Council Directive (EU) 2021/514. It is whether ownership, evidence, and escalation paths are in place before filing pressure starts.

DAC7 sits within the Directive on Administrative Cooperation, which is built for information exchange between EU tax authorities. That means this is a reporting regime, not a new tax on sellers, and the reporting obligation sits with the platform operator. If teams frame it as a seller-tax issue or a one-time legal memo, late decisions can follow.

The baseline rules are workable if you set them early. DAC7 entered into force on 1 January 2023, reporting is annual, and submission is due by 31 January of the following year. For in-scope non-Union operators, registration and reporting run through one single EU country. That single-registration decision should be documented up front, because confusion there can create duplicate work for one team and missed filings for another.

This guide takes a month-by-month operating view for compliance, legal, finance, and risk owners. It covers who owns scope decisions, when to test seller-data readiness, what sign-offs must be complete before year-end, and what evidence should be ready before submission.

Keep one practical split in mind throughout: confirmed rules versus local open points. Confirmed rules come from the Directive, European Commission DAC7 materials, and published national transposition measures. Open points depend on Member State implementation, including penalty rules and local procedure, so they must be checked at country level. If a country question remains unresolved late in the year, run your plan to the earliest defensible date and record the rationale.

One early control matters more than it looks: confirm the Member State of single registration and document why that choice is correct. In multi-entity groups, unresolved filer-entity questions can surface too late and turn the 31 January deadline into a high-pressure negotiation instead of a controlled delivery date. For related context, see our guide on EU Digital Services Act for Marketplace Operators.

What DAC7 requires and who is in scope#

Start with ownership. DAC7 places the reporting duty on the platform operator, not the seller. If you treat DAC7 as a seller-tax issue, control ownership and filing accountability can land in the wrong team.

| Decision log item | Article detail |

|---|---|

| Platform operator | The entity identified as the platform operator |

| EU or non-EU based | Whether the platform is EU or non-EU based |

| Union activity and seller footprint | Why Union commercial activity and seller footprint do or do not bring the platform into scope |

| Member State for single registration | The chosen Member State for single registration, if applicable |

| Sources used | Commission DAC7 guidance and relevant local tax authority material |

This sits within the Directive on Administrative Cooperation (DAC), a tax-authority information-exchange framework between Member States. Under Council Directive (EU) 2021/514 (DAC7), the obligation is to report information to tax authorities. It is not a new tax, and it does not by itself change sellers' existing tax obligations.

For scope, do not stop at "are we EU-established?" Check both EU and non-EU platform models. Certain non-Union operators can still be in scope where there is Union commercial activity. Where relevant, non-Union operators register and report in one single EU country.

Before you build the calendar, create a short in-or-out decision log and review it with legal and compliance. That log is a control, not a legal filing requirement. It should capture the points in the table above.

As a final check, align that log with the actual contracting and payout model. If your documented operator entity does not match who contracts with sellers or runs marketplace economics, scope disputes can appear late.

Related: DAC7 for Non-EU Platforms: Does Your Marketplace Owe Tax Data to European Authorities?.

How to resolve the deadline ambiguity before it becomes a filing failure#

Treat DAC7 timing as a legal control decision, not a scheduling detail. Set 31 January as the working filing date unless the relevant tax authority has clearly published a different local date, and require a named legal owner to approve any different interpretation.

Separate filing timing from exchange timing#

The first practical step is to separate operator filing from authority-to-authority exchange. EU DAC7 framing sets annual platform reporting at "no later than 31 January of the year following the calendar year." The first exchange for 2023 is described at the end of February 2024.

Ireland shows the same split. Platform operators file by 31 January for the previous calendar year, and exchange follows by end of February, including 28 February 2025 for 2024 data. If "end of February" gets treated as the filing date, your filing prep is already late.

Also isolate the Directive wording on communication "within two months following the end of the Reportable Period." Do not treat that as a general filing extension. First reconcile it against national transposition and local authority guidance.

Build a known vs unknown table#

Build this table from Commission DAC7 materials, the EUR-Lex Directive and transposition records, and relevant Member State authority pages or notices.

| Source | Confirmed timing statement | Known | Unknown (needs legal sign-off) |

|---|---|---|---|

| European Commission DAC7 page | Reporting due "no later than 31 January of the year following the calendar year" | EU-level annual filing framing is end of January | Whether local authority notices create an operational variation |

| Council Directive (EU) 2021/514 | Communication wording says "within two months following the end of the Reportable Period" | A separate two-month communication statement exists | Whether that wording changes filing timing in your jurisdiction |

| Relevant Member State authority page or notice | Ireland: file by 31 January, exchange by end of February, 2023 filing deferred to 7 February 2024 | Ireland separates filing from exchange and has issued a period-specific deferral | Whether current-year local notices change your filing date |

For each entry, save the exact quote, URL, and date checked. Do not carry forward a prior-year deferral as if it were permanent.

Put the two timing statements side by side and name the owner#

Do not leave the two timing statements floating in different workstreams. Create a short memo that presents both together: the end-of-January filing framing and the Directive's two-month communication wording. Assign one legal owner to reconcile them across the jurisdictions you touch.

Record at least:

- jurisdiction or authority interface

- filing date you will operate to

- exact authority source used

- whether exchange timing is separate from filing timing

- named legal approver and approval date

If authorities conflict, run to the earlier defensible date#

When sources conflict, operate to the earlier defensible date and document why. In practice, that usually means keeping 31 January as the target unless a relevant tax authority has clearly set a different local date. For each authority interface, document which source controlled, which date you chose, and what would trigger a change.

Make Q4 the point where ambiguity must end#

DAC7 does not require a Q4 legal checkpoint, but using one can reduce filing risk. Run a legal review in October or early November to refresh the table from EUR-Lex transposition records and current authority pages, lock filing dates by jurisdiction, and escalate unresolved conflicts.

If a country remains unclear, set the earlier defensible date and plan submissions to that date rather than leaving the issue open into January.

Choosing your reporting Member State and setting central ownership#

Once timing is locked, the next control decision is your reporting Member State and who owns that decision end to end. For cross-border operators, a common operating baseline is one reporting Member State with one accountable operating team and one escalation path, unless your legal analysis points to a different structure.

What single registration means in practice#

Under DAC7, operators report EU-resident sellers annually to the tax authority of the Member State of single registration. The framework is meant to simplify compliance, and the Directive allows a reporting platform operator to register with the competent authority of a single Member State.

Treat this as an election backed by evidence, not a portal preference. The Member State you select has to be defensible under your facts and eligibility conditions. Ireland's guidance makes the mechanics clear. If an operator meets conditions in more than one Member State, it must elect one. If it elects another Member State instead of Ireland, it must notify Irish Revenue in writing.

For non-Union operators, the same control logic applies: register and report in one single EU country. Keep the registration rationale, authority source, and registration confirmation together from the start.

Set ownership by decision type#

DAC7 places the reporting obligation on the platform operator, but it does not prescribe your internal split. Define it explicitly:

| Function | Responsibility |

|---|---|

| Legal | Selects and documents the registration rationale for the chosen Member State |

| Compliance | Sets evidence standards and maintains the interpretation record |

| Finance | Owns submission readiness for the selected authority |

| Operations/data | Owns extraction, mapping, and handoff of filing-ready data |

Before you finalize the filing calendar, require a short memo with the selected Member State, selection basis, authority source, and approver. After registration, retain the authority acknowledgment and any issued identifier, for example Ireland's platform operator ID.

Centralized ownership vs fragmented local ownership#

| Model | Practical upside | Main risk |

|---|---|---|

| One central team with one reporting Member State | Clear ownership and consistent execution | Local procedural differences can be missed if no one tracks them |

| Fragmented country-by-country ownership | Faster local inputs early | Conflicting interpretations, duplicate effort, and unclear escalation |

| Central owner with local counsel input | Consistency with local legal input | Requires active conflict-resolution discipline |

A central owner can be more reliable in practice, but it is not a DAC7 legal requirement. Tax authorities in EU Member States automatically exchange reported information with the seller's Member State of residence. Keep local counsel input where registration conditions or procedures differ, but route disagreements to one named decision-maker and document the final position with its controlling source.

Month-by-month DAC7 compliance calendar for marketplace operators#

Use 31 January as your operating filing anchor unless your legal memo for the reporting Member State sets an earlier or more specific date. Do not treat the "within two months following the end of the Reportable Period" wording in Council Directive (EU) 2021/514 as the operator filing deadline without local confirmation from the relevant tax authorities.

This calendar is a control sequence, not a legal script: refresh scope, complete due diligence by 31 December, target filing around 31 January based on your reporting Member State's legal position, then lock post-filing evidence and track exchange checkpoints.

| Month | Primary owner | Core artifact | Done criteria |

|---|---|---|---|

| January | Finance with compliance | Filing-ready return package and submission record | Prior calendar year return is submitted on the reporting Member State timeline, with 31 January as the default operating anchor unless local legal guidance sets a different date. Submission confirmation, file hash or version, and approval record are retained. Failure mode: unresolved December data defects become filing defects. Early catch: first-week blocker review for missing seller identifiers, activity totals, and entity-scope exceptions. |

| February | Compliance | Post-filing evidence lock file | Submission evidence, legal basis, data extract, reconciliation notes, and authority acknowledgments are locked and access-controlled. Track the operational authority exchange milestone by end of February where relevant. Failure mode: filed data gets overwritten by corrected source data and the audit trail is lost. |

| March | Compliance with legal | Filing retrospective and issue log | Each filing defect, late change, or manual workaround is logged with root cause and owner. Failure mode: no retrospective means the same exception logic repeats next cycle without a documented fix. |

| April | Legal with compliance | Scope refresh memo | In-scope analysis is refreshed across cross-border and domestic relevant activities and all DAC7 categories: rental of immovable property, personal services, sale of goods, and rental of any mode of transport. Failure mode: entity or product changes stay unclassified until year-end. |

| May | Operations/data | Seller data completeness report | Required seller fields are tested for completeness and consistency against onboarding and payout records. Done means defects are quantified, owners assigned, and remediation dates set. Failure mode: treating KYC data as sufficient when fields do not match DAC7 reporting needs. |

| June | Compliance with product and ops | Midyear due diligence gap log | Open due diligence items are reviewed against the 31 December completion deadline. Failure mode: waiting until Q4 to collect missing seller data, when response rates are lower and history is harder to reconstruct. |

| July | Finance with data | Pre-close reconciliation design | Transaction, payout, and seller master data are mapped to the year-end reporting extract, and reconciliation logic is tested on year-to-date data. Failure mode: late discovery that payout totals and reportable consideration do not reconcile under extraction rules. |

| August | Legal | Jurisdiction interpretation log update | New guidance from relevant EU Member States is checked against the central calendar and reporting Member State position. Done means open interpretation points are marked confirmed, provisional, or escalated. Failure mode: local guidance shifts but operations is not informed. |

| September | Compliance | Q3 readiness review | Confirm registration status, owner assignments, submission channel readiness, and country-variance notes. Failure mode: portal access, credentials, or local prerequisites are first checked in January. |

| October | Finance with compliance | Pre-close reconciliation pack | Seller counts, activity totals, and exception populations are reconciled on a near-final basis. Done means material breaks are explained or fixed. Failure mode: unresolved Q2 scope decisions distort the population and create Q1 rework next cycle. |

| November | Legal | Formal legal sign-off memo | Deadline interpretation, reporting scope, and Member State position are approved for filing season. If local guidance diverges from the central view, the memo states which rule controls for your filing. Failure mode: operations runs on assumptions that counsel has not signed off. |

| December | Operations/data with compliance | Filing rehearsal and due diligence completion record | A dry run produces a near-final extract, validation results, and escalation list. Seller due diligence is completed by 31 December of the reportable period. Failure mode: rehearsal is treated as optional, so schema or completeness issues appear after year-end. |

| Escalation row | Central legal owner | Interpretation escalation note | If local interpretation in one or more EU Member States diverges from the central calendar, escalate at discovery and resolve before the next gated milestone, especially before November sign-off or January submission. Done means the jurisdiction-specific interpretation log is updated and the calendar is either confirmed or changed with approver names. |

Where this calendar earns its keep#

The highest-value checkpoint pair is April scope refresh plus October pre-close reconciliation. April catches business changes while classification is still manageable. October confirms those classifications are supportable in data. Skip either one, and January turns into a fact dispute you cannot reconstruct cleanly.

The second critical checkpoint is November legal sign-off. This is where you force a decision when a 31 January filing view and local timing language appear to conflict. Do not leave that ambiguity in working notes while operations assumes a later date.

Practical controls and red flags#

Start the evidence pack before January. By midyear, keep a live record of scope decisions, open seller-data gaps, and the extraction logic used to build the filing population. Because DAC7 assigns the reporting obligation to the platform operator, you need to defend both the submitted file and how it was produced.

Treat repeated reminders or unresolved defects after registration as a high-severity signal. Continued non-compliance after two reminders from the Member State of registration is explicitly tied to permanent revocation risk. If the same blocker persists from March into Q4, escalate it as registration risk, not routine backlog.

If you need the legal and scope baseline behind this calendar, see DAC7 Compliance for Platforms: Reporting Rules Deadlines and Implementation.

The evidence pack you should have before any submission#

Before you submit, make sure your evidence pack can recreate what was filed and why. At minimum, it should show how the platform operator set scope, applied due diligence, built the reportable population, validated the output, and proved what was sent to the receiving tax authorities.

Under Council Directive (EU) 2021/514, the reporting obligation sits with the operator, and due diligence must support collection and accuracy of reported EU-seller information. So the pack should preserve both the return file and the procedure trail behind it.

| Artifact | What it proves | Checkpoint before submission |

|---|---|---|

| Scope and population rationale | Why the entity and marketplace activity were treated as in scope, and which seller or activity populations were included or excluded | Confirm it matches the final filing perimeter and reporting Member State position |

| Seller classification logic | How sellers were identified as reportable or non-reportable, including exception handling | Test edge cases against the final extract so classification outcomes match population counts |

| Field lineage and transformation record | Where each reported field came from and what transformations were applied | Trace key fields from source to output, especially seller identifiers and activity totals |

| Filing-ready extracts | The actual reportable dataset used to prepare submission | Verify required seller tax fields are present, including any TIN and each Member State of issuance, or place of birth when no TIN is available |

| Jurisdiction interpretation tracker | Which jurisdiction points were confirmed, provisional, or escalated | Confirm no open timing or scope issue is unresolved at approval |

| Submission confirmations | What was filed, when, how, and by whom | Retain acknowledgment or API, XML, or online submission proof, plus file version, approval record, and timestamp |

Two controls are easy to miss. Keep the filing-ready extract as a controlled output tied to your lineage record, not a last-minute spreadsheet cleanup. Also keep seller-notification evidence. Member States must require operators to inform reportable sellers of reported consideration, so retain the notification copy, delivery record, or both.

Use one simple pre-submit test: rebuild one seller record from source data for each higher-risk population. Check identity fields, reportable activity totals, and any fallback field used when TIN is missing. If one record cannot be explained cleanly, pause submission.

One failure mode is a mismatch between legal position, seller population, and transmitted file. Another is delegated due diligence without oversight evidence. If a third party performed collection or review steps, keep both delegation records and evidence of your control checks.

Retention and access controls#

The evidence pack needs clear retention and access rules, not just a storage folder. Keep it in one controlled location with named access roles. Compliance and legal should be able to reproduce decisions quickly, while broad operational access stays limited because the pack contains sensitive seller data, tax identifiers, and submission records.

| Record point | Requirement |

|---|---|

| Storage and access | Keep the evidence pack in one controlled location with named access roles |

| Retention basis | Do not assume one EU-wide retention period; apply and document the rule for your reporting Member State |

| If Ireland is your filing jurisdiction | Keep DAC7 procedure and evidence records for 6 years from the end of the year the procedures were applied |

| Ireland return proof | Retain proof that the prior-year return was filed by 31 January |

| Ireland seller copy proof | Retain proof that each reportable seller received their information copy by 31 January |

Do not assume one EU-wide retention period. Apply and document the rule for your reporting Member State. If Ireland is your filing jurisdiction, keep DAC7 procedure and evidence records for 6 years from the end of the year the procedures were applied. Also retain proof that the prior-year return was filed by 31 January and that each reportable seller received their information copy by 31 January.

For UK operators, see HMRC Reporting Rules for Platforms for UK Marketplace Operators.

As you finalize your DAC7 evidence pack, align each control owner, audit artifact, and reconciliation checkpoint with your implementation flow in Gruv Docs.

Control owners and escalation points that prevent last-minute surprises#

Last-minute DAC7 risk is usually an ownership problem before it becomes a filing problem. DAC7 makes the platform operator responsible for reporting, but it does not prescribe your internal duty split, so any ownership gap stays your risk.

Anchor your ownership map to the Member State of single registration and the annual 31 January filing deadline for the prior calendar year. If legal, compliance, operations, and finance are not aligned on that same jurisdiction and deadline, deadline risk is already present.

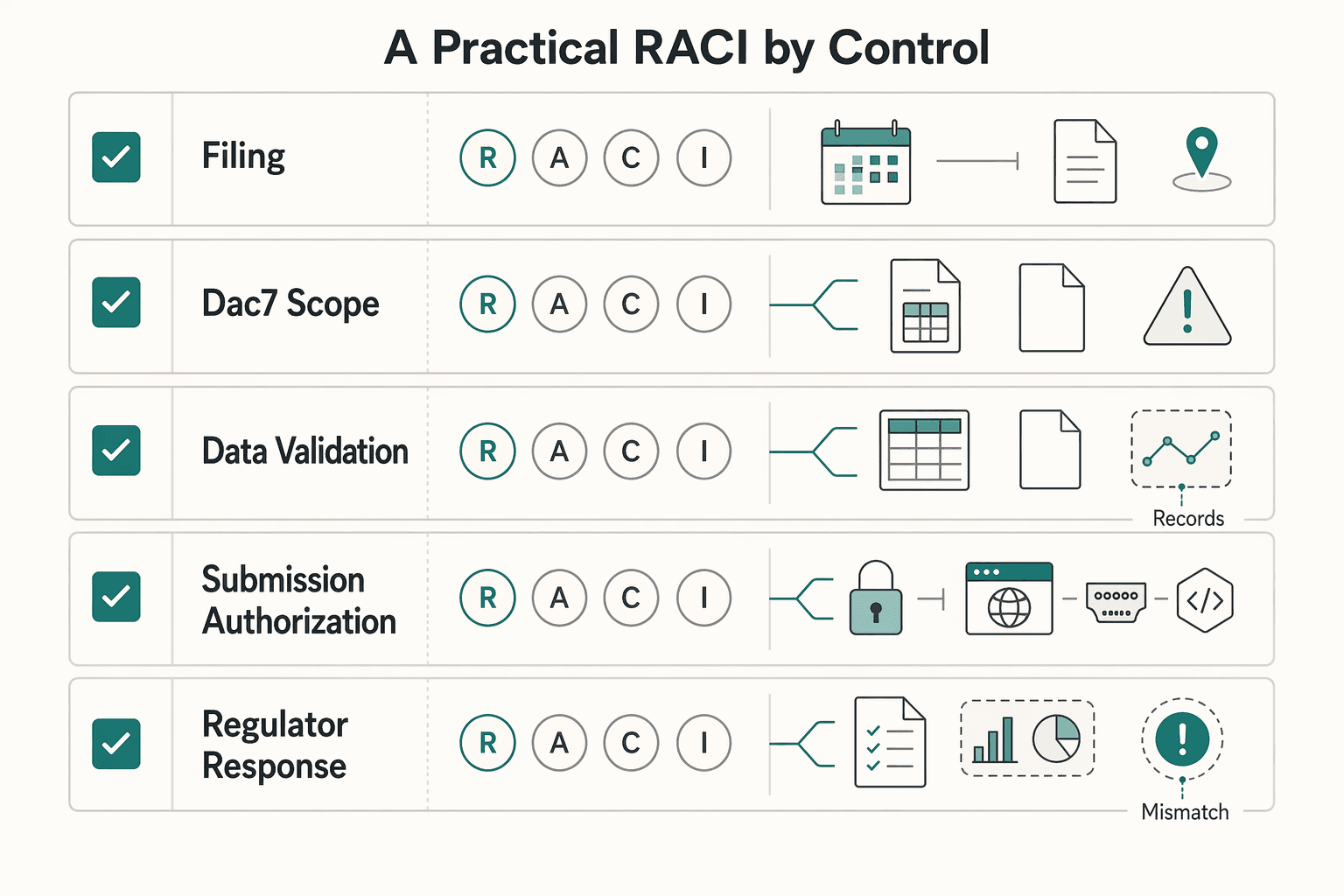

A practical RACI by control#

Use a control-level RACI so each decision, action, and escalation path is explicit. Treat submission-channel readiness as deadline-critical too. Submission routes can differ by authority, for example online, XML, or API, so confirm your filing channel and access early.

| Control | A | R | C | I | Closure evidence |

|---|---|---|---|---|---|

| Legal interpretation of filing timing and local rule variance | Group tax or legal lead | Legal counsel | Compliance | Finance, ops | Written legal position for the filing Member State, including treatment of conflicting guidance |

| DAC7 scope and single-registration position | Compliance lead | Compliance + legal | Finance, ops | Executive sponsor | Signed scope memo and documented registration election where multiple Member States could apply |

| Data validation and seller population accuracy | Operations or data owner | Data team | Compliance | Finance | Validation outputs, defect log, and successful sample rebuilds from source data |

| Submission authorization | Named filing approver | Filing operations | Compliance, legal | Executive sponsor | Final file version, approval record, and confirmed submission route with the authority |

| Regulator response handling | Compliance lead | Compliance + legal | Ops/data | Leadership | Named response owner, response workflow, and access to the evidence pack |

Escalate deadline disputes fast#

Timing disputes should not sit in email threads. If legal and operations disagree on timing interpretation, escalate within one business day to a named decision maker with authority across your in-scope jurisdictions. This is an internal governance rule, not a DAC7 statutory rule.

Keep one distinction explicit in your calendar decisions: the operator filing deadline is 31 January, while separate timelines can apply to authority-to-authority exchange. If that distinction is unclear, escalate and record the conclusion immediately.

Triggers that should force escalation#

Treat any of the following as a control failure until closed:

- unresolved timing interpretation for the filing jurisdiction

- missing or unsigned legal memo for scope or deadline position

- repeated data defects across validation cycles

- unconfirmed submission channel, credentials, or required filing format

- authority query or defect notice without a named response owner

Use a standing cross-functional review cadence before and through filing season with a narrow agenda: open legal points, scope changes, defect trends, submission readiness, and seller-notification status where required. This is more reliable than ad hoc emergency meetings.

Managing country variance and penalties without overbuilding#

The goal is simple: centralize the core process, localize only what the local authority actually requires. Use one country-variance matrix across relevant EU Member States, and adapt only the fields, portal steps, access method, or procedural points that are explicitly jurisdiction-specific. Treat the "about 80% central" split as an internal operating rule, not a legal requirement.

DAC7 is set by Council Directive (EU) 2021/514, but filing channels and procedures are country-specific rather than one EU-wide portal or one uniform procedure. Member States apply national transposition measures, and EUR-Lex indicates that collection is updated weekly, so your matrix should be maintained with current authority links.

| Member State | Filing channel or procedure | Local guidance checkpoint | Timing or change note | Penalty posture signal | Confidence level |

|---|---|---|---|---|---|

| Ireland | Revenue Online Service (ROS); online form, XML, or API | Revenue DAC7 filing guidance | Standard filing by 31 January for prior year; 2023 filing was deferred from 31 January 2024 to 7 February 2024 | Penalty rules are domestic; confirm current position with counsel | High when current Revenue guidance and filing access are confirmed |

| Germany | BZStOnline-Portal with Massendatenschnittstelle activation for mass-data submission | BZSt service description and portal access setup | Mass-data interface activation through BZStOnline-Portal is part of filing setup | Penalties are Member State-defined under DAC7 standards; local legal review required | Medium until portal activation and local interpretation are documented |

| France | DPI-DAC7 declarative procedure | impots.gouv.fr DAC7 and collaborative-economy platform guidance | France replaced the prior Article 242 bis setup; old portal closed on 31 December 2023 | French guidance explicitly addresses sanctions for non-compliance under domestic rules | High when mapped to DPI-DAC7; low if relying on legacy process notes |

Use the confidence column as an internal control signal: settled interpretation versus provisional interpretation. A workable guardrail is to localize transport, credentials, portal activation, and required field handling, then escalate scope, timing, or penalty-interpretation questions to legal before operations treat them as final. EU law requires penalties to be effective, proportionate, and dissuasive, but penalty design remains Member State-level, so record penalty posture as current legal status rather than assumed amounts. Related reading: VAT Reverse Charge Controls for B2B Marketplace Operators.

System and data checkpoints for payout-heavy marketplaces#

For payout-heavy marketplaces, the key question is whether you can reproduce the result. You should be able to trace each reported amount back to source events and regenerate the same extract from the same data cut. Treat that as an internal control standard, not as a DAC7 rule stated in this evidence set.

If you cannot walk a reported seller figure back through the underlying event history and the seller profile state at extraction time, treat it as an internal filing blocker, not a post-filing cleanup task. This mirrors the useful part of OSS operating discipline, where record keeping and audits are explicit parts of scheme operations.

What to verify before filing#

Before you file, run a short internal control set that compliance and finance can apply consistently:

- completeness between reporting extract and payout ledger, with explained differences logged

- duplicate review at seller and transaction level, including retries, reversals, and account merges

- identity consistency review so one seller is not split across multiple profiles, tax identifiers, or country tags

Identity drift can be a high-risk failure mode. Payout events can be correct while the extract still weakens if the same seller appears in legacy and current records, or if profile edits are not historically preserved.

Where Gruv can help operationally#

If you use Gruv, treat product output as operator evidence, not legal interpretation. Audit trails, reconciliation exports, and policy-gated payout flows can support traceability, exception handling, and review records where enabled, but they should sit alongside your legal interpretation log and filing evidence pack.

An OSS-based operating model is useful here. It has one Member State of identification, electronic returns, and onward transmission through a secure communications network. DAC7 is a different regime, but the control lesson still applies. Keep one reproducible extract, one versioned reconciliation, and one retained record trail for audit questions.

Red flags that usually lead to late or defective DAC7 reports#

Late or defective reporting usually starts with unresolved legal assumptions, not formatting errors in the extract. Watch for these signals:

- Unresolved scope status: This evidence set does not resolve EU-versus-non-EU platform scope for DAC7. Treat scope as unresolved until your legal position is documented.

- Single-registration assumption without documentation: In OSS, a taxable person using a scheme registers in one Member State of identification, and returns and payments are transmitted to Member States of consumption through a secure network. Use that as a control analogy only, not as proof of a DAC7 registration position.

- Legal-calendar mismatch: OSS filing cadence is scheme-specific (quarterly for Union and non-Union schemes, monthly for the import scheme). Do not import that cadence into DAC7 deadlines unless your DAC7 legal basis confirms it.

- Template-led false confidence: OSS explicitly covers record-keeping and allows exclusion from a scheme by a Member State. If your DAC7 process has not separately documented record-keeping and exclusion handling, treat templates as incomplete rather than submission-ready.

Where DAC7 ends and other regimes begin#

DAC7 is an EU tax-information reporting obligation for platform operators, not a VAT workflow and not a U.S. account-reporting workflow. These regimes can use some of the same seller data, but the legal basis and authority are different.

DAC7 sits under Council Directive (EU) 2021/514 as part of Directive 2011/16/EU on administrative cooperation in taxation. That framework is for tax-authority information exchange and expressly does not apply to VAT. VAT sits under its own legal framework in Council Directive 2006/112/EC. So even when DAC7 and VAT processes use overlapping source data, do not run them under one owner, one checklist, or one sign-off.

Use a simple routing rule in every procedure note. If it is DAC7, route it through your DAC7 reporting channel. If it is VAT determination, invoicing, or return filing, route it to your VAT owner. Treating a DAC7 seller file as proof that VAT treatment is correct is a control error.

Apply the same boundary to U.S. regimes. FATCA and Form 8938 are U.S. reporting obligations, while FBAR is FinCEN Form 114 filed with FinCEN, not the IRS. Form 8938 and FBAR are separate obligations and do not replace each other.

Add a short not covered by this process block to your DAC7 procedure. This routing note keeps ownership clear:

- VAT registration, VAT rate determination, VAT invoicing, and VAT return filing

- FATCA reporting to the IRS

- Form 8938 assessment or attachment to a U.S. income tax return

- FBAR assessment, including whether foreign accounts exceeded $10,000

- any FinCEN filing

Conclusion#

The practical takeaway is not to memorize one date. It is to run your EU reporting process with a calendar you can defend, named owners for key decisions, and records that show what was decided, when, and why.

This matters most when your platform touches more than one EU Member State. The biggest risk usually appears earlier: scope questions left open, local advice never reconciled into one position, or operations moving on one timing assumption while legal uses another. Treat that split as a control failure, not late-stage cleanup.

Keep a clear line between what must be centralized and what can stay local. OSS shows how registration in one single Member State creates a defined route for returns and payments across Member States. For cross-border operations, choose one accountable route early, record why, and assign one owner for the interpretation log, calendar, and submission path.

You do not need a heavy process. You need a documented timeline, a variance matrix for the countries that matter, and clear escalation rules. Before your reporting window opens, confirm the chosen jurisdiction, the interpretation you are relying on, who holds portal credentials, and where supporting records are retained.

The core tradeoff is control versus sprawl. If you centralize too little, each country becomes its own project with duplicate review and inconsistent evidence. If you localize too much too early, overhead grows faster than your team can sustain. Standardize core controls first, then add local steps only where authority, portal, or guidance requires them.

When interpretations conflict, operate to the earlier defensible point and document the basis. That will not remove every jurisdiction question, but it will lower the chance of a missed or unprovable filing.

Before the next cycle, lock three items in writing so the next filing run starts cleanly:

- your central owner and escalation path across the EU Member States that apply to your program

- your minimum evidence set, including the jurisdiction decision record and proof of submission

- your checkpoint dates for legal reconciliation, data readiness, and final submission authorization

That is the value of a reporting-calendar approach: fewer surprises, clearer decisions, and controls sized to real risk.

If your filing calendar spans multiple EU jurisdictions, use Contact Gruv to confirm market coverage, policy gates, and operational fit before filing season.

Frequently Asked Questions

What is the core DAC7 reporting deadline for an EU marketplace operator?

The core filing deadline is annual and falls on 31 January of the year after the calendar year being reported. The European Commission states reporting must be made no later than 31 January, and Irish Revenue guidance uses the same date for the prior calendar year.

Is DAC7 always filed by end of January, or can a two-month interpretation apply in some cases?

Use 31 January as your baseline deadline unless legal review confirms a different result in your filing jurisdiction. A secondary source describes a two-month window, but that conflicts with the Commission’s 31 January statement. If your team sees both interpretations, work to the earlier date and document the legal basis.

Who must report under DAC7: only EU platforms, or also non-EU platforms with EU-based sellers?

DAC7 is not limited to EU-incorporated platforms. The Commission materials include non-Union platform operators performing commercial activity in the Union, and the reporting obligation sits with the platform operator. For non-EU operators, confirm scope early so registration and filing decisions are made on time.

What does single registration in one EU Member State mean operationally?

Under the Directive, a platform operator may register with the competent authority of a single Member State and report to that state’s tax authority. Operationally, document the chosen Member State, why it was selected, and who owns filing credentials, seller communications, and regulator contact.

What should a compliance team do first if two countries appear to expect different timing?

First, confirm whether there is a true timing conflict or whether reporting should run through the Member State of single registration. Then obtain written legal reconciliation that cites the Commission position, Directive text, and the local authority guidance you are relying on. Until resolved, keep your operating plan on the earlier date and escalate the conflict early.

What evidence should be retained to defend a DAC7 filing decision during review?

Keep evidence showing both why you filed that way and how reportable sellers were identified. Typical records include your scope decision, single-registration rationale, due-diligence procedures, return data used for filing, and submission confirmation. As one benchmark, UK implementation requires relevant records to be kept for five years, while local law may set your actual minimum.

How is DAC7 different from VAT and FATCA-related obligations?

DAC7 is a tax-information exchange regime under Council Directive (EU) 2021/514. It is not VAT, which is a consumption tax, and it is not FATCA, a U.S. foreign asset/account reporting regime. DAC7 reporting does not by itself satisfy FBAR (FinCEN Form 114) or Form 8938 obligations.

Do sellers need to receive anything from the platform?

Check the local rules in your filing route. For example, Irish guidance says a platform operator must provide each reportable seller, by 31 January, a copy of the information included in the return. Where that applies, keep proof of delivery alongside your filing records.

Try a related tool

Rina focuses on the UK’s residency rules, freelancer tax planning fundamentals, and the documentation habits that reduce audit anxiety for high earners.

With a Ph.D. in Economics and over 15 years of experience in cross-border tax advisory, Alistair specializes in demystifying cross-border tax law for independent professionals. He focuses on risk mitigation and long-term financial planning.

Sources

- eur-lex.europa.eu/eli/dir/2021/514/oj/engtrusted

- eur-lex.europa.eu/legal-content/EN/NIMtrusted

- irs.gov/businesses/corporations/foreign-account-tax-...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- sede.agenciatributaria.gob.es/Sede/en_gb/todas-gestiones/impuestos-tasas/d...trusted

- taxation-customs.ec.europa.eu/taxation/tax-transparency-cooperation/admini...trusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- vat-one-stop-shop.ec.europa.eu/one-stop-shop_entrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: