Quick Answer

Contract compliance tracking works best as a shared operating control that monitors payment-linked deliverables, deadlines, notices, owners, and evidence before issues affect payouts. Start with contracts that can change payment timing, trigger holds, create reporting exposure, or route disputes. Use one shared register, one evidence standard, and risk-tiered escalation so missed milestones become managed exceptions instead of surprises.

Contract compliance tracking that actually prevents payout surprises#

Treat contract compliance tracking as an operating control, not a filing exercise, if you want fewer payout surprises. You want to monitor deliverables, deadlines, and payment-linked obligations early enough that missed milestones become managed exceptions rather than cashflow pressure or audit risk.

Step 1 Define the promise in operational terms#

Start narrow. Focus on obligations most likely to affect payout timing, notices, acceptance, or regulatory exposure. Contract management spans the full lifecycle, not just signing, so your controls need to hold across pre-award, award, and post-award work. A simple filter works well: if an obligation can affect money movement, reporting, or a material dispute path, it belongs in the tracker before it goes late.

Use one verification check for every tracked item: what is due, when it is due, who owns it, and what evidence proves completion. If any of those are missing, the item is not monitorable yet.

Step 2 Name the ownership gap before it creates risk#

Cross-functional handoffs are normal in contract operations, and they are often where blind spots open up. Contracting work is often fragmented across people and systems, with no single point of data or analysis.

That is where payout surprises can start. A deliverable can be done in practice but unsupported in the record. A payment gate can sit in finance logic without a linked contract basis. Or a notice deadline can live in one team's process while another team works from a different tracker.

The stakes are financial, not just administrative. WorldCC has tied contracts directly to revenue and cost flows and estimated almost 9% annual value loss from poor contract management.

Step 3 Set a lean evidence and escalation standard#

The right standard is risk-tiered monitoring with tested controls, not a one-size-fits-all process. Design controls for your highest risks, test whether they work, and tighten them where failures recur.

Make evidence requirements explicit. A status is credible only when a retrievable source record supports it. "Completed" by itself is not evidence.

Avoid parallel legal and finance trackers that share titles but drift on status or due dates. Use one scoped contract list, one evidence standard, and risk-based escalation rules so you reduce surprises without turning contract operations into a heavy compliance build. As Lisa Monaco put it, the real test is "how well the program mitigates the company's most significant risks."

If you manage contractor obligations across markets, How to Build a Global Contractor Payment Compliance Calendar: Monthly Quarterly and Annual Obligations shows how to turn recurring obligations into a usable calendar.

Decide scope and risk tier before you track anything#

Set day-one scope around payment-linked contracts first. Prioritize contractor payments, seller payments, and creator payments where a missed obligation can change payout release, trigger a hold or reserve, or create reporting exposure.

Step 1 Pick the contracts that can move money or block it#

Start with agreements closest to payout operations, not every contract in the lifecycle. Include contracts where deliverables, reporting duties, or other contract conditions can affect whether funds are paid, delayed, or reviewed.

Use this first-pass rule: if a contract can change payment timing, payout eligibility, reserve logic, or recurring reporting, include it. This matters most where your platform has a contractual duty to make payment to participating payees.

Verification checkpoint: for each included contract, identify the exact clause, schedule, or operating rule that links it to payout release, a hold, or reporting. If that link is not clear quickly, it likely is not day-one scope.

Step 2 Tier the obligations by consequence#

Once you know which contracts matter, sort the obligations by what happens if they fail. Treat this as a working prioritization model, not a universal legal taxonomy. Higher-risk items should get stronger monitoring first.

- Payment-impacting

Missed items can delay payouts, pause them, create a reserve, or, in defined contract scenarios, block final payment.

- Regulatory

Missed items can affect required reporting or compliance duties. For US payment-settlement flows where a payment settlement entity is in scope, Form 1099-K reporting is a recurring example because it runs each calendar year.

- Administrative

Important, but less likely to change cash movement or create immediate external exposure.

Step 3 Apply the day one inclusion rule and publish the output#

Track a contract immediately when a missed deliverable could support termination rights, route a dispute into the contract's dispute process, or block payouts. Not every miss will trigger those outcomes, because contract language and governing law control.

Publish three outputs: a scoped contract list, an owner list, and a first-pass risk tier for each contract. The common failure is over-scoping low-value administrative items while missing the few agreements that actually control money movement.

Gather the contract data and evidence you need in week one#

Get the record pack right before you build alerts. In week one, assemble a usable contract file for each in-scope agreement. Define what evidence proves performance, because weak records make payment decisions and later reviews harder to defend.

Step 1 Pull the full contract file from the contract lifecycle#

Use the contract lifecycle as your collection path, not just the signed PDF. Start with the executed contract, then add written changes, amendments, notice artifacts, and the current renewal terms in effect. Treat these as one live agreement record, not side documents.

Do not rely on a folder labeled "latest contract" unless the execution version, most recent written modification, and current renewal position are all visible in the same record set. A tracker can look clean and still fail if a later amendment or notice changed obligations or timing.

Step 2 Build an Audit Evidence Checklist for each contract#

Create an Audit Evidence Checklist for each agreement before monitoring starts. Keep it practical with four fields:

- required proof for each obligation or deliverable

- acceptable source system

- named owner responsible for currency

- retention location for later retrieval

Decide evidence standards up front. If a system record or audit log exists, use it as the primary source instead of informal captures. That preserves event details and identity data for monitoring, investigation, and compliance reporting.

Step 3 Capture clause data as fields, not notes#

If you want consistent reporting and exception alerts, store key clause data as structured fields, not free-text notes. At minimum, capture clause reference, deliverable, responsible party, due date logic, trigger event, notification requirement, and evidence type or status.

This matters most when due dates are relative to contract events. Record both the event and the timing rule so the tracker can evaluate status consistently.

Step 4 Verify ownership coverage and evidence status#

Before you mark a contract ready, confirm mapped contacts across the relevant teams, for example legal, finance, and ops, and confirm a current evidence-status field. This is a practical control for cross-functional accountability, not a universal legal requirement.

Use a quick checkpoint on one payment-impacting contract: legal confirms the current version, finance explains payout impact, and ops points to accepted evidence in the retention location. If any answer depends on guesswork or handoff memory, the file is not ready.

Build a deliverables register that legal, finance, and ops all use#

Where practical, use one shared register as the working record for legal, finance, and ops, then give each team filtered views from that same source. Keep payment timing, acceptance, and notice details in the same record so those fields do not drift.

Step 1 Create one row for each deliverable instance#

Make each deliverable a separate line item in the Deliverables Register, including recurring items as separate instances. If something is due every month, track each monthly due date as its own row so overdue status and evidence are assessed against a specific obligation. Oracle deliverables workflows support this structure with responsible party, deadline, notification, status, and required-document handling.

| Field | What to capture | Why it matters |

|---|---|---|

| Deliverable name | Plain-English obligation title | Keeps the row clear outside legal |

| Due date | Exact date, or trigger plus timing rule | Supports overdue logic and alerts |

| Owner | Named responsible party contact | Makes accountability explicit |

| Dependency | Prerequisite event or task, if used in your process | Explains blocked items |

| Evidence type | Required proof and source system | Ties status to records |

| Status | Current workflow state | Supports escalation and reporting |

Be strict on two points. If timing is relative, store both the trigger event and rule, for example "a week before" the contract event, not only a derived date. Keep status evidence-based, such as submitted, accepted, rejected, or failed where applicable, not just verbal confirmation.

Step 2 Add the commercial fields that explain cash impact#

Basic status tracking is not enough if you need to understand cash impact. Add commercial linkage fields such as Payment Timing Terms, acceptance status, and a Revenue Recognition review flag.

For UCC Article 2 goods contracts, payment timing and acceptance are contract-relevant: payment timing follows contract terms, and accepted goods are payable at the contract rate. Track acceptance separately from delivery so finance is not reconstructing payment position later.

Treat Revenue Recognition impact as a review flag, not an accounting conclusion. Under IFRS 15, recognition is tied to satisfaction of performance obligations through transfer of promised goods or services, not billing alone.

Step 3 Add legal linkage so missed items are reviewable, not just late#

If a row can go overdue, it also needs enough legal context to be reviewed quickly. Add legal linkage fields to each row: governing clause reference, notice requirement, and whether failure may require legal review for Indemnification or Limitation of Liability exposure.

Capture the clause citation that creates the obligation, plus notice method, recipient, and timing rule when relevant. Keep dispute-related flags as review triggers, not conclusions. A missed deliverable does not automatically establish indemnity or liability outcomes.

Also track notice timing carefully. In UCC Article 2 context, breach notice timing can affect remedies, so the register should show when notice is required and whether it was sent.

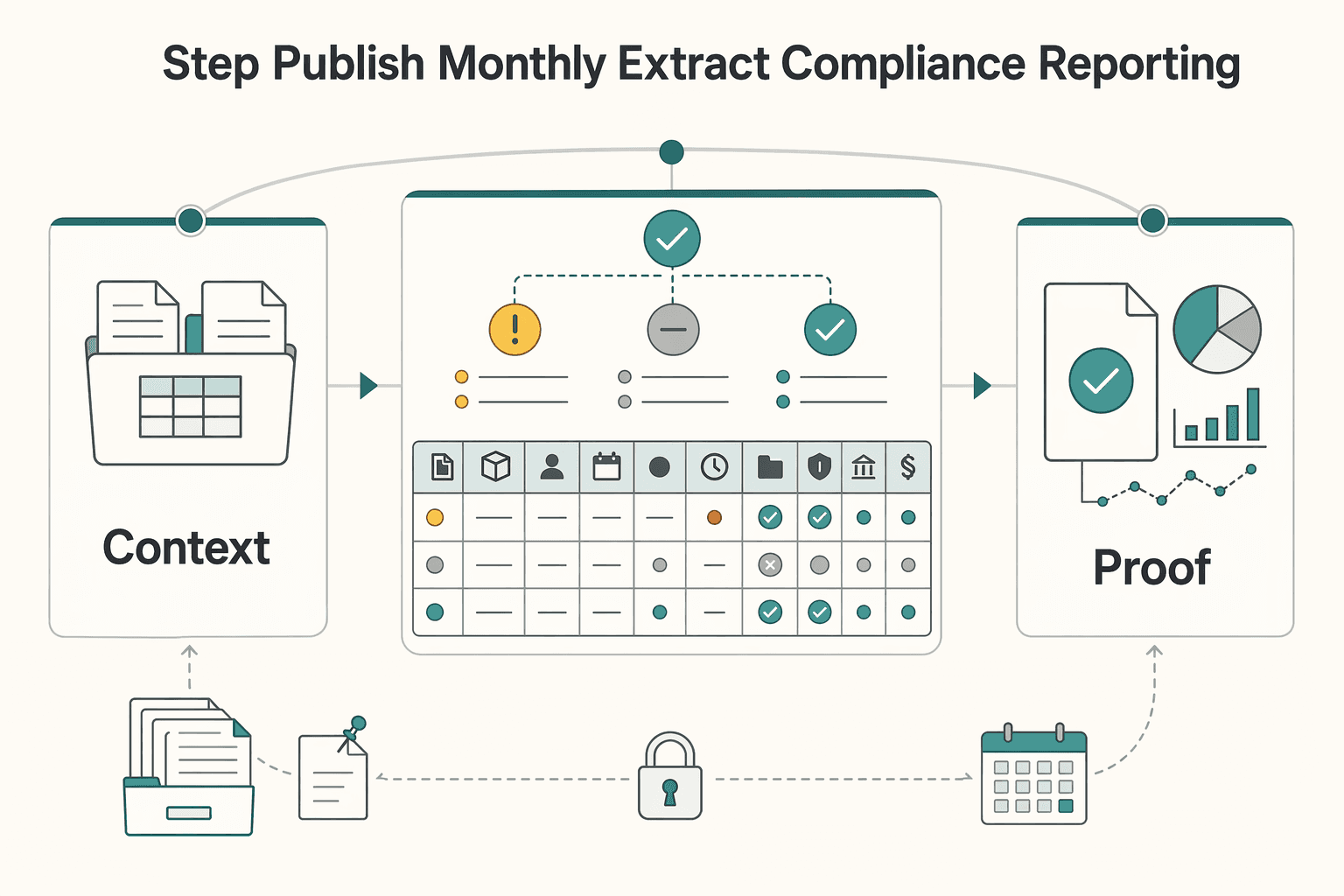

Step 4 Publish a monthly extract for Compliance Reporting#

A monthly extract keeps the register operational and ready for decisions, but it is an operating control, not a universal legal mandate. Include open items, overdue items, and evidence completeness, plus contract, deliverable, owner, due date, status, days overdue if any, evidence on file yes or no, acceptance status if relevant, payment impact, and clause reference.

Where a single system is practical, keep one shared register as the system of record, then let each function consume views from it. In federal procurement, FAR Subpart 42.15 uses CPARS as the official source for past-performance information, which reflects that single-source model in that context.

Final check for each overdue row: owner of recovery, evidence completeness, and whether finance or legal review is required. If those are missing, the extract reports activity but not control status.

For a step-by-step walkthrough, see Project Milestone Tracking: How to Bill Based on Deliverables Not Hours.

Set SLA rules and ownership for deadlines and payment timing#

Turn each deadline clause into an operational service-level agreement rule with a clear timer, cutoff, evidence requirement, and owner. Otherwise the clause is too vague to run.

Step 1 Convert contract text into measurable timer rules#

Start from the contract clause, then map it to execution fields: trigger event, countdown, cutoff, evidence required, and next handoff. SLA rules should use explicit metrics and named responsibilities, not narrative intent alone.

If the clause is already measurable, keep that language. If it is vague, do not invent precision without legal review. A practical structure is trigger, timer, evidence, owner, and escalation. For example: trigger, acceptance recorded. Timer, payment approval starts only after acceptance is on file. Evidence, acceptance record in the approved system. Owner, finance ops. Escalation, legal if acceptance is disputed.

Quick test: can a new operator tell when the clock starts, what counts as complete, and who acts next? If not, the rule is still prose, not control logic.

Step 2 Assign a primary owner, backup owner, and escalation contact#

For each payment-impacting or compliance-impacting deadline, assign a primary owner, backup owner, and escalation contact. This is an operating control to reduce single-point failure, not a universal legal requirement.

The backup should be able to execute the task, not just receive alerts. The escalation contact should be able to unblock work or make a risk call if the first line does not respond.

Watch for false ownership. If the backup cannot access evidence, approve the next step, or send required notice, the process still depends on one person.

Step 3 Tie payout-critical deadlines to approval gates#

If a deadline controls payout release, tie it directly to contractor payments or seller payments approval gates. Do not rely on manual report review to catch blockers.

Where payment depends on delivered and accepted performance, require acceptance evidence before release. Also keep other gating conditions explicit in the rule, such as required tax or compliance information, so teams can distinguish blocked items from ready items.

For each cash-releasing deliverable, confirm the register shows the exact gate, evidence source, and who can place or lift a hold.

Step 4 Apply contract-specific precedence rules and update the tracker#

When SLA wording and contract wording conflict, follow the agreement's stated order of precedence for that contract, and involve legal interpretation when the language is ambiguous. Update the tracker rule as an internal operating discipline.

Do not assume one universal precedence model. Some agreements make SLA terms control only in limited conflict scope, while others rank SLA below other governing documents. Point each rule to the controlling document or clause for that contract.

If the same conflict appears repeatedly, issue one legal interpretation note for that contract family so ops and finance follow a single current rule. For more on payout friction, see Invisible Payouts: How to Remove Payment Friction for Contractors Without Sacrificing Compliance.

Map critical clauses to monitoring triggers#

Once deadline rules are in place, map legal-risk clauses into explicit monitoring triggers. Track Termination, Limitation of Liability, and Indemnification as active records with evidence, owner, and escalation so you catch issues before they become dispute-stage problems.

Step 1 Convert high-risk clauses into clause-trigger pairs#

Do not leave these clauses as passive notes. For each clause, create one monitoring record with clause reference, trigger type, evidence source, owner, and escalation threshold.

| Clause | What to monitor | Evidence checkpoint | Typical first escalation |

|---|---|---|---|

| Termination | Missed deliverable that the contract ties to a termination right, uncured breach notice, unresolved exception tied to a termination right | Contract clause reference, notice record, cure-period tracker, status history in Audit Trail | Legal review if the miss could start or end a cure period |

| Limitation of Liability | Payment mismatch, damages claim, credit request, or exception that may exceed a cap or restricted remedy | Liability cap clause, claim amount, invoice or payment record, approval notes | Finance plus legal review before any concession or payout release |

| Indemnification | Regulatory notice, third-party complaint, security or compliance allegation, or contract breach that could shift loss responsibility | Notice received, underlying event record, required response deadline, supporting documents | Legal review, then outside counsel if the forum or law is unfamiliar |

Treat missed deliverables and missing evidence as separate triggers. One means performance may have failed. The other means you may not be able to prove performance.

Step 2 Add dispute-control fields, not just clause names#

Clause names alone are not enough when you need to route a live issue. Include Governing Law, Forum, Jurisdiction, Venue, and Dispute Resolution as separate fields. Governing law selects which law applies; forum, jurisdiction, and venue help determine where the dispute is heard, so they should not be merged.

Capture required pre-litigation steps, such as amicable-settlement attempts before arbitration or court. In contracts that fall under UCC Article 2, treat notice timing as its own trigger because remedy availability can depend on timely notice under UCC § 2-607(3)(a).

Verification checkpoint: for each contract family, confirm you can answer quickly which law applies, where disputes go, whether ADR must come first, and who can send notice.

Step 3 Standardize trigger types and escalation thresholds#

Use a fixed trigger set so exceptions are comparable across compliance reporting. If outside counsel is a possible path, define that threshold in advance by contract family or jurisdiction.

- Missed deliverable: operational fix first, unless the clause links the miss to termination, indemnity exposure, or payment hold.

- Missing evidence: operational escalation first; route to legal if the gap affects acceptance proof, required notice, or cure response.

- Payment mismatch: finance review first; add legal review when contract liability caps, damages limits, or remedy restrictions may control the outcome.

- Regulatory notice: legal review immediately, because response and indemnity obligations may already be running.

- Unresolved exception: executive review when it remains open beyond practical contract tolerance or blocks payout decisions.

Step 4 Test the mapping against live records#

Validate with live examples before scaling: one missed deliverable, one payment mismatch, and one notice-driven issue. Each record should show clause reference, trigger date, status, evidence link, and escalation path in the Audit Trail.

If one review pass cannot tell you whether an item is an operational fix or a legal dispute, the mapping is still too vague and should be tightened.

Related reading: How to Use Harvest for Time Tracking and Invoicing in a Small Agency.

Run a weekly monitoring cadence across systems and teams#

Use one fixed weekly sequence across teams: refresh statuses, validate evidence, reconcile payment-linked deliverables, then publish exceptions. A set order reduces missed follow-ups and makes reporting easier to read.

Step 1 Refresh statuses from the Deliverables Register first#

Start with the Deliverables Register, not email threads or meeting notes. Update each item to current status, such as done, in progress, blocked, overdue, or awaiting acceptance, then confirm key terms tied to performance, especially deadlines and payment-related conditions.

Do this before evidence and payment reconciliation. If status changes, log who changed it, when, and what record supports the change.

Step 2 Validate evidence before treating a deliverable as complete#

A complete status is not enough without support. For each item marked complete or accepted, confirm required evidence exists in the agreed location and matches the contract requirement.

Use a simple trace test: can a reviewer follow clause to deliverable to supporting proof? If not, keep it in exceptions. Keep missing evidence separate from missed performance so remediation can be assigned clearly.

Step 3 Reconcile payment-linked deliverables against finance records#

After statuses and evidence are current, reconcile payment-linked items against invoice and payment records. This helps keep payment decisions aligned to the latest delivery and acceptance state.

Track a small KPI set that reflects monitoring quality. Set baselines by contract family and watch for trend breaks rather than forcing universal thresholds.

| KPI | What it shows | Watch for |

|---|---|---|

| On-time deliverables | Whether owners meet agreed deadlines | High volume closed, but frequent late delivery |

| Overdue rate | How much work remains past due | Small backlog that stays overdue across cycles |

| Evidence completeness | Whether completed items are defensible | High completion with missing acceptance proof |

| Mean time to resolve exceptions | How fast teams close issues | Older exceptions persisting week to week |

Step 4 Publish the exception list and maintain the Audit Trail#

End each cycle with a short, searchable exception list for compliance reporting: item, contract reference, status, exception age, owner, next action, and whether payment, notice, or dispute exposure is involved.

Tie status changes to an Audit Trail so you can reconstruct history later. At minimum, preserve timestamp and operator action. Adding owner and supporting record can speed review and remediation.

As a verification checkpoint, run a weekly cross-functional review for unresolved high-risk items through established reporting lines. Keep the agenda narrow to items that may affect payout, notice timing, or potential contract risk. If classification is still unclear after one pass, tighten the record facts first.

Escalate exceptions with a risk-tiered matrix#

After you publish the exception list, route each item by severity, not through a single generic path. Classify first, then escalate based on business impact, dispute exposure, and evidence quality.

Step 1 Classify each exception before escalation#

Use an exception taxonomy that matches your risk profile. Compliance guidance emphasizes risk-specific design over rigid, one-size-fits-all models. A practical internal structure can use tiers like:

- Administrative miss

Control issues like status errors, ownership gaps, or filing problems, with no clear payment, regulatory, or dispute impact yet.

- Compliance risk

Missing required support, unresolved clause interpretation, or overdue obligations that weaken your defensible record.

- Payment-impacting issue

Exceptions that may affect payout release, invoice approval, milestone acceptance, or hold decisions under contract terms.

- Potential legal dispute

Facts indicating possible breach, termination, invalidity, or movement toward formal dispute handling.

For each classification, require a short rationale tied to clause reference, current business effect, and known evidence.

Step 2 Publish an escalation matrix with owners, timing, and evidence#

Your matrix should make three points immediately clear: decision owner, response window, and minimum evidence required. That cuts handoff delays across ops, finance, and legal.

| Severity tier | Typical trigger | Response window (example) | Decision owner | Minimum evidence pack |

|---|---|---|---|---|

| Administrative miss | Internal record, status, or control gap | Low-risk window, for example up to 365 days, with earlier follow-up if risk changes | Ops owner | Register entry, status history, corrective action owner |

| Compliance risk | Missing support, interpretation issue, overdue compliance item | Moderate-risk window, for example 90 days, or sooner if contract requires | Compliance or legal ops | Clause reference, due date, missing-evidence list, reviewed records |

| Payment-impacting issue | Deliverable exception linked to payout, invoice, or acceptance decisions | High-risk window, for example 30 days, or sooner if payment timing requires | Finance with legal review | Contract clause, finance record, acceptance state, evidence-gap summary |

| Potential legal dispute | Facts point to breach, termination, invalidity, or formal dispute path | Immediate triage; legal sets timetable | Legal lead, plus finance when payment exposure exists | Contract set, amendments, notices, chronology, preserved evidence |

Use severity windows as internal discipline, not as a substitute for contract deadlines.

Step 3 Set explicit if-X-do-Y rules for common edge cases#

For common edge cases, write the response rule before the first real escalation.

- If facts indicate possible breach, termination exposure, invalidity concerns, or payout-hold implications, escalate promptly to legal and finance under your matrix. If cross-border dispute is reasonably anticipated, start evidence-preservation steps early.

- If evidence is incomplete and no current payment, regulatory, or dispute impact is identified, assign corrective action, keep the item open, and set a defined follow-up date within the assigned risk window.

When clause meaning is uncertain, route interpretation to legal before operational teams act. If additional certainty is needed, escalate for second-opinion counsel before you commit to a high-impact decision.

If your escalation matrix can trigger payout holds, map each severity level to a clear payout approval path. The Gruv Payouts overview is a practical reference for compliance-gated status tracking.

Handle cross-border privacy and records without blocking operations#

For cross-border tracking, keep the operational register lean and keep sensitive evidence in controlled systems. You want to monitor deliverables, deadlines, ownership, and evidence status without turning the register into a full personal-data store.

Step 1 Limit what enters the tracker#

Store only what is necessary for monitoring. In practice, that is often a party reference, contract ID, market, owner, due date, clause reference, and evidence status, rather than full personal records.

This aligns with GDPR data minimisation and Article 25's requirement that only personal data necessary for each specific purpose is processed. A practical check is to sample live rows and confirm teams can still assess status and escalate exceptions without opening full personal files.

Step 2 Keep auditable evidence in protected systems#

Keep audit-ready records in the protected system of record, and keep only references in the operational tracker. That can preserve auditability while reducing unnecessary exposure of personal data.

This supports Article 30 recordkeeping requirements, in writing including electronic form, and Article 32 security expectations for confidentiality, integrity, availability, and resilience. Avoid copying evidence into spreadsheets, email threads, or ad hoc shared folders, because duplicate copies can make access and retention controls harder to defend.

Step 3 Apply stricter local rules where they exist#

Treat third-country transfer as a separate control check. GDPR Chapter V requires transfer conditions to be met, and Member States may introduce more specific provisions in some contexts.

Do not apply one universal retention rule across all markets. Where local law or internal policy is stricter, apply the stricter retention and access controls. Before you use a record in cross-border monitoring, confirm each evidence location has a named owner, defined access controls, a retention rule, and transfer review status.

Fix the common failure modes before they become breaches#

A common control break starts the same way: obligations get tracked, but consequences stay vague. Fix these failure modes first so issues do not turn into payment delays, audit pressure, or avoidable disputes.

Step 1 Tie missed deliverables to payment controls#

When a contract ties payment to proper invoicing, satisfactory performance, or acceptance, a missed deliverable should trigger a control action, not stay a passive status.

Connect overdue items to the approval queue and owner alerts. Do not block every miss automatically, because payment gating depends on contract terms, but where terms support it, finance should see a hold flag before release. Test one overdue item and confirm the approver, legal owner, and operations owner receive the alert.

Step 2 Re-scope to high-impact obligations first#

Tracking everything equally weakens control quality. Re-scope to high-impact contractual obligations first, including payment release conditions, required notices, and obligations that could lead to a dispute.

Use a risk-tiered scope instead of a one-size formula, and align scope to your company's risk profile. If an item cannot materially affect payment, notice timing, reporting, or dispute handling, move it to a lower tier. Your register should show why each tracked item is in scope.

Step 3 Resolve clause ambiguity in writing#

Ambiguity in Jurisdiction or dispute resolution terms is a direct control risk because unclear wording can delay or compromise resolution. When ambiguity appears, document a written clarification and update the tracker fields that depend on it.

Record the clause reference, interpreted forum or process, and escalation owner. If teams are relying on informal email interpretation, standardize it in writing before the next exception.

Step 4 Enforce retrieval-ready evidence#

Evidence is only useful if it can be retrieved quickly. Treat slow retrieval as a control failure, not an admin inconvenience.

Apply the Audit Evidence Checklist as a production control: each item should map to a source record, named owner, retention location, and any required transfer trail. Run periodic spot checks on a small sample to confirm the full evidence pack can be produced without inbox or shared-drive hunting. If retrieval depends on memory, fix indexing before an audit request exposes the gap.

Copy/paste checklist for your first 30 days#

Keep the first month narrow and operational: track what can block payment, affect notice timing, or create dispute exposure, and trim the rest in monthly review.

-

Scope the contracts that can create immediate risk. Start with high-risk agreements tied to payout release, milestone acceptance, invoice support, renewal or termination notice, or active regulatory requirements. For each in-scope contract, assign one primary owner and supporting contacts in legal, finance, and operations. Verification point: each scoped contract has an executed copy, current amendments or notices, and at least one payment-linked obligation written in plain English.

-

Use one shared

Deliverables Register. Keep legal, finance, and operations in the same tracker so status does not drift. A practical starter set is deliverable name, due date, primary owner, backup owner, dependency, evidence type, status, payment linkage, clause reference, notice requirement, and current evidence location. -

Publish

SLArules, escalation paths, and response windows in writing. Turn contract language into clear internal handling rules with owners, backups, cutoffs, and escalation contacts per deadline. If you use KPIs, keep the distinction clear. Where KPIs apply, they should be set out in the contract, so do not present an internal target as a contractual KPI unless signed terms or an amendment support it. -

Map clause triggers before exceptions happen. Connect events like missed deliverables, missing evidence, payment mismatches, regulatory notices, or unresolved exceptions to

Indemnification,Limitation of Liability,Governing Law,Jurisdiction, andDispute Resolution. This keeps response paths clear when issues escalate, including an explicit rule that unresolved disagreement triggers escalation. -

Run weekly monitoring with KPI and evidence checks. Refresh status, verify schedule adherence, reconcile payment-linked deliverables against approvals or holds, and publish the exception list. Keep KPIs short and decision-useful, such as on-time completion, overdue rate, evidence completeness, and time to resolve exceptions. Weekly cadence is an internal operating choice, not a universal legal requirement.

-

Require an

Audit TrailandAudit Evidence Checklistfor every exception. Keep records that reconstruct what happened in sequence, including timestamp, owner, action taken, and source reference. For regulated electronic records, stronger controls can include secure, computer-generated, time-stamped create/modify/delete history. Typical evidence includes executed terms, amendments, notices, acceptance proof, invoice or payment record, submission record, and remediation notes. -

Review monthly and cut low-value tracking. Keep fields and checks that changed decisions on payout, notice rights, or dispute handling, and remove those that did not. This keeps the process lean enough to run and defensible when challenged.

Once your first 30-day controls are live, confirm market and program specifics in the Gruv docs before scaling the workflow.

Frequently Asked Questions

What is contract compliance tracking for deliverables?

Contract compliance tracking means monitoring the commitments that must be honored, not just storing a signed agreement. It focuses on whether contract terms are followed in day-to-day execution, including deadlines, required notices, and retrievable completion records.

Which deliverables and deadlines should we track first?

Track the obligations that can change payment release, notice timing, renewal actions, or dispute handling. Payment-linked items should come first because payment can depend on proper invoicing and satisfactory performance. Your first register is stronger when each high-risk item has a clause reference, due date, owner, and evidence source.

Who should own monitoring across legal, finance, and operations?

Use one primary accountable owner so accountability is clear. Add a designated monitoring role to maintain contract files, status, and supporting records. Legal, finance, and operations can each own their part, but each obligation still needs one named owner.

What KPIs show that compliance tracking is actually working?

Use KPIs that show conformance to requirements, schedule adherence, and cost-control impact. In practice, track on-time completion, overdue items, deliverable completion status, evidence completeness, and time to resolve exceptions. If you have activity data but no explicit KPI set, the control system is likely immature.

What events should trigger immediate escalation?

Escalate when a miss can block payment, jeopardize notice timing, or create a live dispute about performance. Escalate when high-risk records are not retrievable, payment-supporting invoice or performance data conflicts, or clause wording is too unclear to act on confidently. If resolution by mutual agreement looks unlikely, involve legal support.

How do payment terms and renewal terms change monitoring priorities?

They move to the top of the list because both depend on exact timing and documentation. For payment, monitor invoice quality, performance status, and key invoice metadata because due-date calculations can shift, including fallback timing tied to invoice date. For renewals or options, track the written notice window in the contract itself.

When should we involve specialist legal counsel in cross-border disputes?

Involve specialist counsel when dispute wording is unclear, when settlement by mutual agreement is unlikely, or when enforcement may be needed across borders. Ambiguous dispute clauses can delay or compromise resolution, so the language should be reviewed early. Before handoff, prepare a clean package of the executed terms, amendments, notices, dispute language, and timeline.

Asha writes about tax residency, double-taxation basics, and compliance checklists for globally mobile freelancers, with a focus on decision trees and risk mitigation.

With a Ph.D. in Economics and over 15 years of experience in cross-border tax advisory, Alistair specializes in demystifying cross-border tax law for independent professionals. He focuses on risk mitigation and long-term financial planning.

Sources

- acquisition.gov/far/subpart-42.15trusted

- acquisition.gov/far/52.233-1trusted

- csrc.nist.gov/glossary/term/audit_logtrusted

- ecfr.gov/current/title-48/chapter-1/subchapter-E/part...trusted

- federalreserve.gov/supervisionreg/srletters/SR0808.pdftrusted

- gao.gov/greenbooktrusted

- guides.gaoinnovations.gov/greenbook/2025/principle-10-design-control-a...trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-17-evaluate-issues-...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: