Quick Answer

Yes, working capital loans can help freelancers when the gap is temporary and repayment is tied to specific receivables. Use borrowing for short operating needs, not ongoing structural shortfalls, and confirm the cash is expected back inside a short cycle such as 12 months or less. Build a 13-week view, separate essential costs from optional spend, and stress-test collections before drawing funds. If repayment is unclear, improve invoicing and payout timing first.

When a Working Capital Loan Helps#

Freelance businesses can get squeezed when cash leaves before it arrives. Client invoices may settle later than expected while payroll, rent, software, and utilities still hit on time. That kind of pressure does not automatically mean you need debt, but it does mean you need to look closely at payment timing before the gap starts making decisions for you.

A working capital loan is short-term funding used for day-to-day business expenses when cash flow gets tight. PNC frames these loans as a fit for operational needs expected to return value within 12 months or less. That is a useful early boundary. If the cash you borrow will not come back through collections inside a short operating cycle, you are probably using the wrong tool.

The practical issue is usually a cash-timing gap, which Stripe describes as the space between money going out and money coming in. For a freelancer or small operator, it often shows up in a very ordinary way: invoices are approved but unpaid while recurring obligations are already due. In that situation, a cash flow loan can act as a bridge. The danger is using it to cover a gap that is not really temporary, or one where repayment depends on hope rather than a visible source of cash.

That is why this guide treats borrowing as a precision move, not a default response. Before you borrow, you should be able to point to the expected repayment source and explain why it is credible. A good first checkpoint is simple: which receivables, contracts, or near-term cash events are supposed to repay this balance, and do they arrive quickly enough to cover the loan without forcing another draw? If you cannot answer that clearly, the problem may be bigger than timing.

There is also a failure mode worth naming up front: using short-term debt to cover a gap that is not truly temporary. That can relieve this week's pressure while making next month tighter. If the funded activity will not generate cash quickly enough to cover repayment, the loan stops being a bridge and starts becoming rolling debt.

So the goal here is not just to explain working capital loans for freelancers. It is to help you decide with discipline: borrow when the gap is short and repayment is visible, and reconsider spending or payment timing when it is not. That is the lens for the rest of the guide. Use short-term funding only when the timing gap is real, the evidence is specific, and the repayment plan is realistic before cash leaves the account.

What a working capital loan actually is and when it fits#

A working capital loan fits when your gap is short-term cash timing, not a long-term growth bet. It is short-term business funding for regular operating expenses, and it generally fits better when value returns inside a short operating window, such as 12 months or less; short-term repayment schedules are also often within 18 months.

Use this tool when money is going out before money comes in and you can point to a credible operating repayment path. In many cases, lenders assess repayment capacity based on business cash flow, and some facilities may be secured by short-term assets like accounts receivable.

Typical good-fit uses are practical:

- Covering payroll during slower periods

- Managing rent and utilities

- Handling short seasonal demand swings without draining reserves

It is usually a poor fit for long-term expansion, major investments, or routine expense coverage that repeats month after month. If repayment depends mainly on optimistic forecasts rather than clear near-term operating cash, pause and reassess before borrowing.

Map your cash gap before you borrow#

Map the gap first. If you cannot show week-by-week repayment over the next 13 weeks, pause borrowing.

A 13-week cash flow analysis is a recognized near-term planning window. For a freelance business, forecast expected cash in and cash out, then place each item in the week you expect it to hit the bank, including receivables timing.

Build the 13 week view#

List expected inflows from client work, retainers, and other receipts. Then map committed outflows such as rent, payroll, and loan payments, because those obligations continue even when collections are delayed.

| Item | Type | Handling |

|---|---|---|

| Client work | Inflow | Tie to an issued invoice or due date |

| Retainers | Inflow | Tie to a recurring contract payment |

| Other receipts | Inflow | If there is no document or schedule behind it, treat it as timing risk |

| Rent | Outflow | Committed obligation that continues even when collections are delayed |

| Payroll | Outflow | Committed obligation that continues even when collections are delayed |

| Loan payments | Outflow | Committed obligation that continues even when collections are delayed |

Use one control: each collection line should tie to something concrete, like an issued invoice, due date, or recurring contract payment. If an inflow has no document or schedule behind it, treat it as timing risk rather than dependable cash.

Split obligations from optional spend#

After the map is populated, separate baseline obligations from discretionary spend. Baseline costs keep delivery running and the business operating; discretionary spend is what you could pause for a cycle without breaking operations.

Use a working capital loan for timing gaps in necessary operations, not avoidable spend. If most of the shortfall comes from optional costs, cut or defer those first.

Add a downside case and include owner draws#

Do not rely on one forecast. Add a downside case that assumes later client payment and less consistent new revenue, then check whether repayment still clears.

For a self-employed business, model owner's drawings explicitly as cash outflows. If the plan only works because owner draws are quietly reduced, state that directly and decide whether that is sustainable.

Keep both base and downside versions dated and saved so decisions stay traceable if collections slip. Related: Working Capital Optimization for Platforms: How Payment Timing Affects Your Cash Position.

Compare loan and advance options by repayment pressure and control#

Choose the structure that matches your repayment source, not the one that looks fastest. If invoices are clean and collectible, start with invoice financing or invoice factoring. Use an unsecured working capital loan only when timing is urgent and repayment is still clearly covered.

Where repayment pressure changes#

Repayment pressure changes based on what gets underwritten. Invoice financing is designed to free up cash tied up in unpaid invoices, often advancing up to 80% or 90% of invoice value, and underwriting can include invoice quality plus the customer's payment history and ability to pay. Compared with a traditional loan, that can put less weight on your own credit profile.

Working capital loans or lines are different. Public bank materials position lines of credit for short-term operating needs like payroll, and lender disclosures also make clear approval is credit-dependent. If client payment timing slips, repayment pressure still stays on your business.

| Option | Collateralized by receivables | Dependence on credit history | Repayment shape | Customer relationship impact | Operational overhead and reconciliation |

|---|---|---|---|---|---|

| Invoice financing | Yes, against unpaid invoices | Often lower than a traditional loan because underwriting also considers invoice/customer quality | Advance against invoice value (often up to 80% or 90%), then settles when the customer pays | You keep invoice ownership, so you usually keep more direct control | Moderate: invoice tracking, due dates, aging, and payoff matching |

| Invoice factoring | Yes, via sale of invoices | Often tied more to invoice/customer quality than your standalone profile | Cash comes from selling invoices to a third party that collects payment | More customer-facing impact because the third party collects | Higher: assignment tracking, disputes, and matching sold invoices to cash |

| Working capital loan or line | Not necessarily | Higher reliance on credit approval in reviewed public materials | Repayment follows loan terms, not customer payment timing | Minimal direct client impact because invoices are not transferred | Lower invoice-specific admin, but debt schedule and weekly cash tracking still matter |

| Cash advance | Not necessarily | Varies by provider/program | Product-specific; do not assume term-loan or invoice-backed behavior | Verify directly with provider | Variable; confirm reporting treatment of balances, fees, and repayments before signing |

How to choose without losing control#

Use a simple fit rule: when 30-, 60-, or 90-day invoice terms are creating the gap, invoice-backed options usually align better than general debt. They connect funding to the receivable that created the timing problem.

Before you apply, assemble the evidence: issued invoice, due date, AR aging, acceptance/signoff if relevant, and observed payment pattern. If you cannot produce that pack, treat "clean and collectible" as unproven.

Do not generalize market pricing or approval rules from a few lender pages. Public summaries from PNC, Brex, and Fifth Third are useful signals about institution-specific underwriting, not a market-wide benchmark.

Set borrowing rules tied to unit economics#

Keep the borrowing rule simple: draw short-term capital only when the funded work is still expected to clear financing drag, collection slippage risk, and repayment overhead.

Borrow on verified cash performance, not pipeline confidence#

Set your draw limits from collected revenue patterns and overall financial health, since cash flow lenders underwrite those inputs, not sales momentum alone. Use DSCR as a discipline check for repayment capacity, but avoid pretending there is one universal freelancer cutoff across products. The practical test is whether your operating cash flow can cover principal and interest without assuming perfect collections.

| Document | When | Focus |

|---|---|---|

| Receivables aging | Before approval | Receivables |

| Current debt schedule | Before approval | Current debt |

| Expected collection dates | Before approval | Collection timing |

| Gross margin on the funded work | Before approval | Funded-work economics |

Before approval, require one document set with:

- receivables aging

- current debt schedule

- expected collection dates

- gross margin on the funded work

If that packet is incomplete, you are likely financing uncertainty, not a timing gap.

Cap single-client repayment dependence#

If repayment depends mainly on one invoice or one customer, treat it as single-party risk and reduce exposure. Make the rule explicit: if one account is the primary payoff source, cap the draw and require fallback repayment support from other issued receivables with a real collection record.

Do not rely on a fake universal concentration percentage. Set your internal threshold, review it each cycle, and log every exception.

Lock repayment planning before funds are drawn#

No approval is complete without a named owner, a review date, and a stop-loss action if collections slip. Confirm in advance:

- who owns collections follow-up and repayment tracking

- when actual collections will be reviewed against plan

- what spend gets cut, paused, or deferred if cash arrives late

- which fallback receivables or reserves cover the gap

- whether borrowing still improves unit economics after fees and admin load

When evaluating lenders, mirror SBA guidance and compare more than rate: include cash flow requirements, minimum credit score, repayment terms, and other qualifying factors. Keep one exception log with the reason, expected payoff source, review date, and actual outcome so finance, ops, and product can audit whether borrowing improved or damaged unit economics. For a step-by-step walkthrough, see Working Capital Management for Freelancers Who Invoice Clients.

Redesign payment timing and invoicing flow before increasing debt#

Before you add another loan, try to remove the timing gap that created the need. In many cases, the lower-cost fix is tighter execution: invoice sooner, reduce approval lag, and use faster payment rails where they are supported and make sense.

A working capital loan can cover timing pressure, but it does not fix process delay. If delay comes from internal batching, slow client signoff, or payout promises that front-run collections, borrowing can hard-code that weakness into your model.

Tighten the invoicing flow first#

Start with invoicing speed and clarity. Prompt invoices with clear payment terms can improve payment turnaround and reduce the gap between spend and cash receipt.

Trace one live invoice end to end using four timestamps: work accepted, invoice drafted, invoice sent, and payment initiated. If the biggest lag is between acceptance and send, treat it as an operational issue before you treat it as a funding issue.

A common pattern is hidden batching: work is completed throughout the month, then invoices are released late in one batch. That can create an artificial cash trough that gets financed with short-term debt.

Smooth collections with staged billing#

If delivery spans weeks or months, avoid waiting for one month-end invoice. Progress invoicing lets you split one estimate into partial invoices as work progresses, which can smooth collections.

Use staged releases tied to real acceptance events and clear owners. When milestones are vague, disputes and admin overhead can rise, and collection timing does not improve.

More stages can stabilize cash timing, but they also add coordination and reconciliation work. Use only the number of stages your team can execute reliably.

Match payout timing to your cash conversion cycle#

For platform teams, align payout timing to your actual cash conversion cycle (CCC), not to a target schedule that outruns collections. A shorter CCC supports stronger working-capital management, so payout design should follow real conversion speed.

If payouts are consistently earlier than receivable collection, you are taking financing exposure. Compare collection patterns to payout calendars and rail choices, then adjust where needed. Where supported, faster rails such as Same Day ACH can improve liquidity timing versus standard ACH, but speed and economics vary by context.

Decision rule: if invoicing, approval, or payout-timing changes can close most of the gap in the next billing cycle, make those changes before adding new borrowing. Use debt for residual timing risk, not avoidable process drag. If factoring is one of the options you are weighing, see A Guide to Invoice Factoring for Freelancers.

Build payout policy and reconciliation controls before scaling advances#

Before you scale advances, lock your control model so funds become withdrawable only when they are actually available, not just expected, invoiced, or still pending. If your payout policy does not define that boundary, financing can hide settlement problems instead of fixing cash timing.

Define the withdrawable event#

Set explicit states for pending deposits, held funds, and available funds. Pending funds stay non-withdrawable until they settle, held funds need a clear owner and release condition, and returned payouts should move into review instead of back into the normal payout queue.

| Status | Withdrawable | Handling |

|---|---|---|

| Pending deposits | No | Keep non-withdrawable until they settle |

| Held funds | No | Assign a clear owner and release condition |

| Available funds | Yes | Make funds withdrawable only when they are actually available |

| Returned payouts | No | Move into review instead of back into the normal payout queue |

Returned payouts need explicit handling. Review the return reason before reissuing, and fix destination or account mismatches first so exceptions do not become repeat failures.

Reconcile invoices, collections, and payouts every day#

Run daily reconciliation across invoice status, collected cash, and paid-out cash so advances do not mask ledger mismatches. If automatic payouts are enabled, use a payout reconciliation report to match transactions by payout batch and confirm each payout maps to settled collections, not just booked receivables.

Watch for stale status assumptions and duplicate payout retries. Use idempotency keys on payout-creation requests so retries do not create duplicate payouts.

Keep a finance evidence pack#

Tie each funding decision to a compact evidence pack, including:

- an accounts receivable aging report (for example: 0-30, 31-60, 61-90, and more than 90 days)

- a named repayment owner

- exception history (returned payouts, holds, and unresolved reconciliation items)

Use the aging report as a risk check, not paperwork. If repayment depends heavily on invoices in the more than 90 days bucket, treat that as elevated risk.

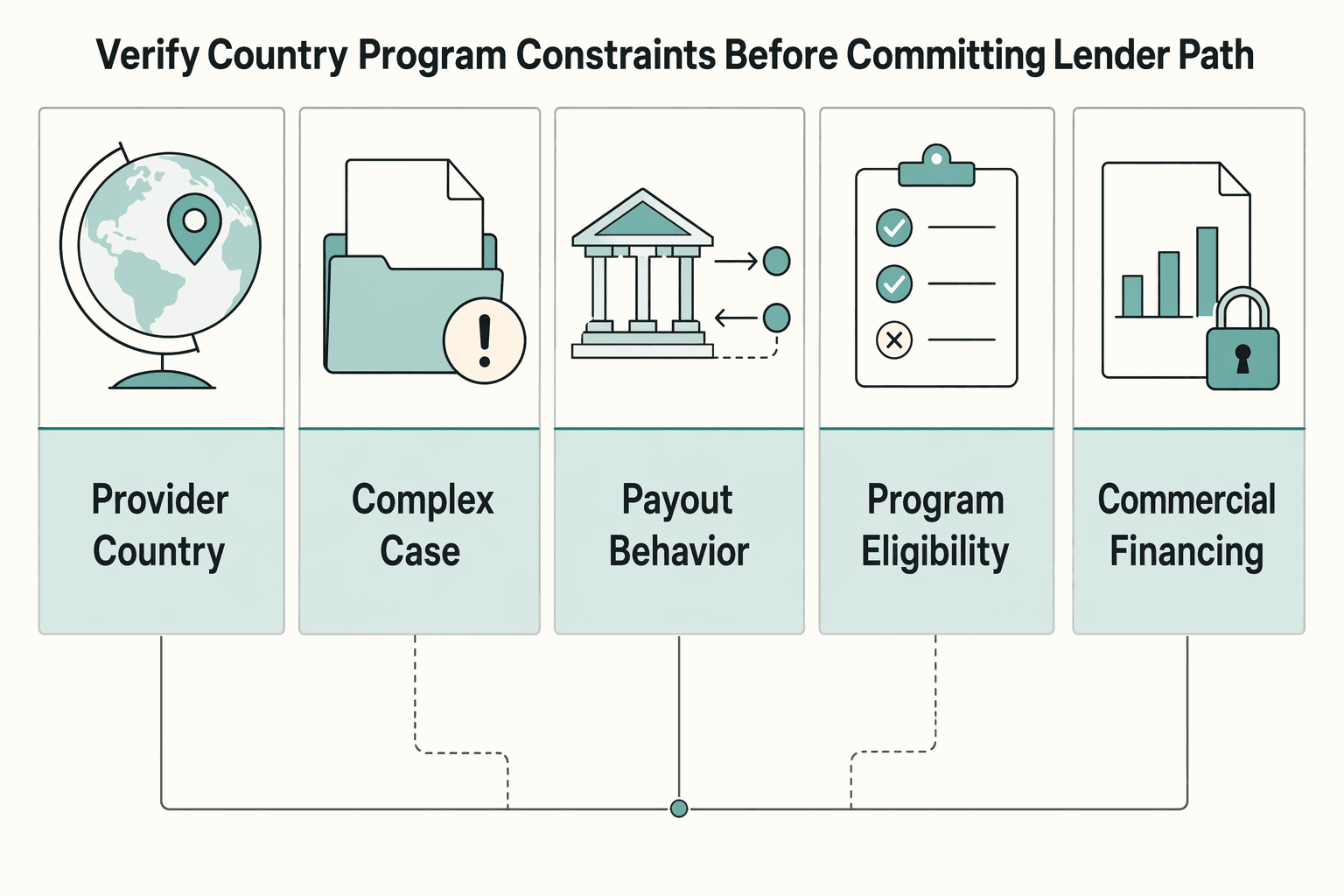

Verify country and program constraints before committing to a lender path#

Verify market and program constraints before you commit to any lender path, because eligibility, disclosures, and payout access are not uniform across countries or providers.

Use this quick check per market before promising funding timelines:

| What to confirm | What can vary | Why it matters |

|---|---|---|

| Provider country support | Supported countries/regions | A global provider still has country-by-country availability limits. |

| Identity and onboarding requirements | Requirements by location, business type, and requested capabilities | Verification steps are not one-size-fits-all. |

| Payout behavior and bank setup | Payout availability by country/industry, and required bank-account details | Funds may not be available on the timeline your plan assumes. |

| Program eligibility for a self-employed business | Program-specific location and operating criteria | A lender path can fail if your business does not meet program rules (for example, SBA 7(a) requires U.S. location). |

| Commercial financing disclosures | Jurisdiction-specific disclosure regimes | Some markets require standardized disclosures (for example, New York rules for certain financings up to $2,500,000). |

Before launch, run a verification checklist across legal review, operations review, and go-live controls for payment rails and payout policy. If coverage is unclear in a target market, treat that as unresolved risk and confirm directly in provider documentation and with compliance before proceeding. Related reading: Form W-9 for Freelancers Working Across Borders.

Conclusion#

The strongest outcome here is not fast approval. It is needing less emergency funding because you fixed payment timing, tightened invoicing, and only borrowed when repayment was already visible in your receivables.

That is the real test in working capital financing decisions for freelancers. This kind of financing is meant for short-term timing gaps, not long-term growth bets or routine expense coverage month after month. If you keep borrowing just to make normal operating costs fit, treat that as a warning sign about your operating model or billing discipline, not as proof that you need a bigger facility.

Process fixes deserve priority because they can remove the gap at its source. A well-managed invoicing process can speed collections and reduce pressure on cash, which is often more durable than adding debt. If you can shorten invoice release lag or reduce approval bottlenecks, do that before taking on a new cash flow loan. Debt should be the backstop, not the first move.

When you do borrow, make the economics explicit. Match the structure to the way cash actually arrives. If your receivables are clean, collectible, and near-term, a receivables-based option may fit because many working-capital lines are tied to short-term assets like receivables. If your repayment schedule is fixed, remember that short-term business loan examples are often repaid on a set schedule, usually within 18 months. If your cash cycle cannot support that cadence without relying on best-case collections, pass.

Control matters just as much as approval. Before funds go out, verify the exact invoices expected to repay the draw, the expected collection dates, and the named repayment owner. After funding, reconciliation is the checkpoint that proves you are still in control: compare the general ledger balance with detailed accounts receivable records, confirm invoice status, and clear exceptions quickly. If you skip that step, you increase the risk of misstated revenue, missed overdue invoices, and bad decisions based on inaccurate cash visibility.

So the practical end state is simple. Borrow only against a credible repayment path, where the downside is survivable and the admin burden fits your operating capacity. Then review results cycle by cycle. If financing reduced stress without masking weak collections, keep it in the toolbox. If it only papered over slow invoicing, thin margins, or repeated timing misses, fix those first and shrink your dependence on debt.

Frequently Asked Questions

Is a working capital loan a good idea for freelancers with uneven income?

It can be, mainly when the problem is timing. Use it for short-term operating gaps with a clear repayment source, not to fund long-term expansion. If repayment depends on optimistic assumptions, fix billing or payout timing first.

How much working capital should a freelance business hold before borrowing?

There is no universal target, but a common reserve guideline is three to six months of business expenses. If you are below that, be stricter about what the money covers and separate owner draw from real operating costs before you borrow. That can help distinguish a true operating gap from a planning issue.

Which costs should short-term funding cover first: payroll, rent payments, or growth spend?

Start with essential operating costs such as payroll and rent payments because those keep the business functioning during a timing gap. Growth spend should come last, especially if the return is uncertain or slow to show up. A simple rule: if the expense does not protect current delivery or collections, it usually should not be first in line for short-term debt.

What are the warning signs that a cash flow loan will make cash flow worse?

A major red flag is repayment that depends on cash you do not control yet. Another is when you cannot map the next few weeks of collections and outflows with confidence, including payout delays. If inflow timing depends on provider schedules, account for that upfront: for example, Stripe typically schedules an initial payout in about 7-14 days after the first successful payment, and timing can vary by country and risk.

When should I choose invoice factoring over a standard working capital loan?

Choose invoice factoring when unpaid invoices are the real funding base and you need cash now rather than in 30, 60, or 90 days. Factoring commonly advances 70% to 90% upfront, with the rest paid later minus a 2% to 5% fee. The tradeoff is real: it can cost more than a conventional loan and can reduce your control over customer interactions.

How do credit history and revenue consistency affect approval odds?

Credit history matters directly. Poor credit history is one of the main reasons small-business loan applications are declined, and some lenders also require minimum business revenue.

What should I verify first when payment and payout rules vary by country or program?

Check country availability, verification requirements, and currency compatibility before you commit to any lender or payout promise. The exact verification requirements differ by country, and payout availability can vary by country and industry as well. A practical checkpoint is to confirm that your account setup, bank account currency, and provider country and currency tables all match before you promise access to funds.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- dfs.ny.gov/reports_and_publications/press_releases/pr20...trusted

- docs.stripe.com/payoutstrusted

- files.consumerfinance.gov/f/documents/cfpb_small-business-lending-rule...trusted

- occ.gov/publications-and-resources/publications/comp...trusted

- sba.gov/funding-programs/loans/7a-loanstrusted

- sba.gov/funding-programs/loans/lender-match-connects...trusted

- stripe.com/resources/more/working-capital-financing-opt...trusted

- stripe.com/resources/more/invoice-financing-loanstrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Embedded Working Capital: Factoring, Financing, or Cash Advance

Treat this as a product design choice first and a funding feature second. The model you pick changes who controls the invoice asset, who collects repayment, what your support team has to explain, and how the economics hold up once disputes and exceptions show up. That is the real lens for embedded working capital.

Working Capital Optimization for Platforms Through Payment Timing Control

Working capital is current assets minus current liabilities. In platform operations, timing controls are a practical lens you can verify: when collection data is posted, when funds are final, and when disbursements are released.

A Guide to Invoice Factoring for Freelancers

**Treat your unpaid invoices as an operating risk first, then choose a funding method that preserves client trust and contract control.** As a business-of-one, your job is to keep cash flow predictable without handing the client relationship to someone else's process.