Quick Answer

Choose a SEP IRA when you want simpler employer-only funding, and choose a Solo 401(k) when owner-only or spouse-only status plus added contribution levers fit your workflow. Run the decision in this order: hiring outlook, low-month liquidity, contribution classification discipline, and provider-document confirmation. If cross-border facts apply, check Form 8938 and separate FBAR duties before finalizing so compliance issues do not force a midyear reset.

SEP IRA vs Solo 401(k) for freelancers who need steady cashflow#

Pick the plan you can keep funding in weak months, not the one that looks best in a strong quarter. That is the real decision.

For freelancers and self-employed owners with uneven revenue, retirement planning is less about headline limits than about whether the plan still works when invoices land late. Both options can work. The better choice is usually the one that fits your staffing picture, your paperwork tolerance, and the way cash actually shows up during the year.

A straightforward way to decide is to check the constraints in order instead of jumping straight to maximum-contribution math.

- Team shape now and soon. If you expect employees other than a spouse, treat that as a major input. A one-participant 401(k) may stop fitting once non-spouse hiring becomes part of the picture.

- Cash pressure in low-revenue months. Set contributions at a level that still protects core bills when receipts run late.

- Feature need vs upkeep. SEP IRA is employer-contribution-only and usually simpler. A Solo 401(k) can offer more flexibility, but it comes with tighter eligibility and more administration.

- Plan details in writing. Compare tax treatment, contribution rules, withdrawal constraints, and investment options, then confirm provider terms before you open anything.

If you only have one work session to make the call, do not start with the highest possible contribution. Start with whether you can keep contributing during a late-payment month. Then check eligibility. Then compare features. That order usually produces a better real-world answer than chasing the biggest number first.

The tradeoff is practical, not theoretical. SEP IRA usually lowers day-to-day complexity. A Solo 401(k) can give you more levers if you can maintain the records and rules that come with it. Also keep growth in view. SEP contributions are generally applied as a uniform percentage for eligible employees, so what feels simple today can become more expensive as your team changes.

Related: Financial Management for Freelancers: Budgeting, Saving for Taxes, and Retirement.

At-a-glance comparison table you can decide from quickly#

Use this table to sort the two options quickly by eligibility, contribution structure, and execution burden. The point is to get to a sensible first choice without missing a disqualifier.

| Decision checkpoint | SEP IRA | Solo 401(k) |

|---|---|---|

| Eligibility | SEP can be set up using Form 5305-SEP or an IRS-approved prototype SEP plan. | One-participant status applies when the business has no employees other than a spouse and is tied to exemption from discrimination testing. |

| Employee elective deferrals | Not available. | Available through employee salary deferrals. |

| Employer contributions | Yes. SEP IRA is employer-contribution-only. | Yes. Employer contributions can be made in addition to employee deferrals. |

| Catch-up contributions | No separate employee-deferral catch-up structure. | Available for eligible ages, but verify current-year figures before funding. |

| Roth contributions | No Roth version in SEP IRA. | Can be offered as designated Roth contributions if the plan document permits it. |

| Participant loans | Not available. | Can be allowed if the plan is designed to permit loans, and provider terms control availability. |

| Admin burden | Simpler setup and lighter reporting profile. Form 5305-SEP is one documented setup route. | More setup and ongoing administration than SEP IRA. |

| Cashflow fit | This is a planning heuristic, not an IRS category: it can be easier to keep current when you want fewer administration steps. | This is a planning heuristic, not an IRS category: it can fit when employee deferrals matter and you can keep up with added administration. |

| What to verify with your provider and IRS guidance before opening | Confirm document path, where SEP-IRAs will be opened, and setup timing tied to the return due date, including extensions. Then confirm current-year IRS limits before funding. | Confirm one-participant eligibility, whether plan terms include designated Roth contributions and participant loans, and how contributions are classified. Then confirm current-year IRS deferral and combined limits before funding. |

Read it in that order: eligibility and documents first, features second, limits last. If your main goal is low reporting friction and a cleaner opening path, SEP IRA often comes out ahead. If you are truly owner-only or owner-plus-spouse, want employee deferrals, and can handle the added administration, the one-participant plan can be the better fit.

If both columns still look workable, use a simple tie-breaker. Pick the option with fewer steps you are likely to miss in a low-cash month. A plan that is slightly less flexible but consistently funded usually beats a more capable plan that keeps getting skipped.

Once both options pass this quick screen, the next question is whether your current staffing setup actually keeps them open.

Who is eligible now and what breaks eligibility later#

Eligibility is the first hard filter. If the plan does not fit your staffing situation, nothing else matters.

If you are self-employed with no employees other than a spouse, a Solo 401(k) can fit that owner-only structure. If your business has employees beyond a spouse, a SEP IRA is designed to work in employee situations. That is why hiring belongs near the top of the decision, not as an afterthought.

The practical breakpoint is not just who is on payroll today. It is whether your setup is likely to change soon. Once you move from owner-only or owner-plus-spouse into non-spouse employees, your one-participant posture may no longer fit. Recheck eligibility as soon as hiring becomes likely, then confirm contribution handling with your provider before sending more money.

Use this checklist before you compare limits:

- Confirm your current team shape: owner only, owner plus spouse, or employees beyond spouse.

- Confirm near-term hiring plans, not only today's roster.

- If evaluating SEP IRA with employees, confirm you can contribute the same percentage of compensation for all eligible employees.

- Verify provider terminology for Solo 401(k), One-Participant 401(k), or Individual 401(k), since labels vary.

- Keep written confirmation of plan type and employee treatment before the first contribution.

That last point matters more than it sounds. Provider labels vary, but the staffing facts underneath them do not. Naming shortcuts can create confusion later if you assume two products are interchangeable and the documents say otherwise.

Owner-only status also affects operations. In a one-participant 401(k), nondiscrimination testing is generally described as unnecessary because there are no non-owner employees to protect. That simpler posture can change once non-owner employees enter the picture, which is another reason not to treat this as a set-it-and-forget-it decision.

A common planning mistake is to use today's roster as if it will still be true in six months. If you are owner-plus-spouse now and likely to hire next quarter, do not treat current status as permanent. Put that hiring trigger in your notes now so you know exactly when to recheck eligibility before bringing on non-spouse employees.

The practical takeaway is straightforward: choose the plan that still works after your most likely hiring move, not just the one that feels easiest this week.

Once eligibility is clean, contribution structure becomes worth comparing.

How contributions work when your income is lumpy#

When income comes in waves, contribution structure matters almost as much as the annual cap. A plan that looks right on paper can still be the wrong plan if it becomes awkward to fund in a year with slow collections.

A Solo 401(k) has two contribution buckets: employee elective deferrals and employer contributions. SEP IRA uses an employer-only channel. That difference is not just technical. It affects timing, recordkeeping, and how disciplined you need to be about classification when money arrives late in the year.

For 2024, IRS limits include up to $23,000 in salary deferrals for Solo 401(k), with total contributions capped at $69,000 for that year. SEP IRA contributions are up to 25% of net earnings from self-employment, up to $69,000 for 2024. Verify current-year limits before funding.

In practice, the two-bucket structure can help or it can become one more thing to manage. If surplus arrives late and you want more flexibility in how you allocate contributions, the extra bucket can help. If you are trying to simplify decisions during volatile months, one employer-only path can be easier to run.

Use a simple if-then rule when surplus lands late:

- If most surplus arrives late and you want allocation flexibility, a Solo 401(k) can give you more control because it has two contribution buckets.

- If you want simpler execution and fewer classification decisions during volatile months, SEP IRA may be easier to run.

- In either case, higher targets only work if net profit supports them.

That means your contribution schedule should follow cleared business reality, not optimism. A simple cadence for uneven freelance cash flow looks like this:

- January to March: set a conservative target from paid invoices and protect your cash buffer first.

- April to June: if receipts stay uneven, hold or pause contributions and refresh profit estimates.

- July to September: add from cleared surplus only. For a Solo 401(k), decide contribution type before sending funds.

- October to December: increase funding in stronger months if plan terms allow. SEP setup can still be completed by the return due date, including extensions.

The sequencing matters because a common execution mistake is to send money first and sort out the classification later. A safer order is to decide contribution type first, document it, then transfer. For the one-participant plan, log each deposit as employee or employer. For SEP IRA, keep the plan document and contribution worksheet together. That makes year-end review easier and reduces the odds of a correction problem.

Use the same short verification check before each transfer: confirm tax year, entity setup, contribution type, and plan-document terms in writing. It sounds basic, but this is where messy records usually start.

Once you understand how each plan handles real cash timing, the next question is whether the features you want are actually usable when money is tight.

Which features matter when cash is tight#

When cash is tight, treat unverified features as unavailable. That one rule prevents a lot of bad decisions.

It is easy to get drawn toward features that look powerful in a comparison chart. In a down quarter, the only ones that matter are the features your actual plan documents support and the ones you can use without pushing operating cash below your floor. Anything else is wishful planning.

| Feature lens | What is grounded here | Common mistake |

|---|---|---|

| Roth contributions | The grounded tax-side point here is IRA modified AGI phaseout risk. It does not confirm Solo 401(k) Roth treatment for your specific plan. | Treating Roth as a cashflow fix instead of a long-term allocation choice. |

| Catch-up contributions | This section does not establish plan-specific eligibility or limits. | Building a cash-tight plan around catch-up assumptions you did not verify. |

| Participant loans | This section does not establish availability, limits, or terms in your specific plan. | Assuming loan access exists before confirming plan documents and operations. |

That conservative posture is intentional. A feature should not drive your decision until it is confirmed in the actual plan you are opening. That is especially important with loans and Roth treatment, where freelancers often assume a provider supports something because another provider does.

For tax-today decisions, the concrete checkpoint here is IRA rules. For 2025, the IRA contribution limit is $7,000, or $8,000 for age 50+. Traditional IRA deductions can narrow within modified AGI phaseout ranges, and one IRS-described married spouse-covered scenario shows no deduction at modified AGI of $246,000 or more. Roth IRA contribution limits can also phase out by modified AGI.

That does not mean IRA phaseouts should drive this entire choice. It means that if you are counting on a feature for tax treatment, you need to pressure-test the tax side and the plan side at the same time.

Use this checkpoint before feature-driven contributions:

- Check the latest Pub. 590-A updates for the current tax year.

- Estimate modified AGI using year-to-date income and a conservative forecast.

- Confirm each feature in your plan documents, in writing.

- Label each contribution by purpose: tax reduction now, long-term allocation, or cash-buffer protection.

A good down-quarter rule is simple: if using a feature would force you to reduce your operating buffer below your floor, skip the feature and preserve liquidity. You can always revisit feature use after cash normalizes. Cleaning up a rushed contribution decision is usually harder than waiting a little longer.

That same discipline applies to fees, provider restrictions, and correction risk, which are often the real hidden costs.

Hidden costs competitors gloss over#

The biggest hidden cost is usually not the listed fee. It is the cleanup work that follows when you choose before you have the current provider documents in hand.

That is where many clean comparison charts fall short. They make the plans sound more comparable than they are before you know whether your provider supports the design choices you are counting on, what recurring steps the provider expects from you, or how contribution errors are handled in practice.

| Friction lens | SEP IRA | Solo 401(k) |

|---|---|---|

| Setup complexity | Not established here. Confirm exact steps with your provider. | Not established here. Confirm exact steps with your provider. |

| Ongoing administration | Not established here. Confirm required records and recurring actions. | Not established here. Confirm required records and recurring actions. |

| Provider-level restrictions | Feature availability and limits remain unknown until provider review. | Feature availability and limits remain unknown until provider review. |

| Correction risk | Error handling details remain unknown until provider review. | Error handling details remain unknown until provider review. |

That may feel cautious, but it is the right kind of caution. If a feature, fee rule, or correction process is not confirmed in the provider documents, leave it out of your decision model for now.

Two common failure modes to screen for before choosing:

- You choose before reviewing current documents, then discover plan terms differ from your assumptions.

- You choose a design, then later need a feature your provider does not support.

One more caution: this section includes historical hearing material from 2002 and 2005, and it does not replace current provider operating terms. One excerpt also states that the printed hearing record is official and warns that electronic conversion can introduce errors or omissions. Do not use old material as a substitute for current paperwork.

Before opening either account, get written confirmation of:

- Participant loans, if offered in your exact plan.

- Roth contribution availability in your exact plan.

- Full fee schedule: setup, ongoing administration, transaction, and transfer or exit costs.

- Contribution error handling steps.

Do that review before you sign, not after funding starts. A short document pass up front can save a much longer cleanup later if a key feature turns out to be unavailable or more restrictive than you assumed.

Once you understand the hidden friction, you can make a practical first choice based on the kind of freelance business you actually run.

If you are this type of freelancer, choose this plan#

Use this to narrow the field, not to force a false universal answer. Make a provisional choice first, then clear the compliance and document checks before you lock it in.

| Freelancer profile | Practical starting move | Checkpoint before final choice |

|---|---|---|

| Stable profit, low admin tolerance | Start by leaning toward SEP IRA. Keep it provisional until documents are confirmed. | Confirm plan documents and contribution handling in writing before funding. |

| Owner-only, high savings intent, feature-focused | Start by leaning toward Solo 401(k), but treat features as unconfirmed until verified. | Do not assume any plan feature exists in your exact plan without provider confirmation. |

| Planning to hire soon | Favor the option that still works with that hiring horizon in view, rather than treating a one-participant setup as permanent. | Set your hiring horizon first, then choose with likely plan changes in mind. |

| Cross-border U.S. filer concerns | Run compliance review first, then choose. | Confirm whether Form 8938 and FBAR obligations apply, then finalize plan choice. |

These are starting positions, not commitments. The point is to reduce decision noise. If low admin tolerance is your main constraint, the simpler path deserves a hard look. If you are owner-only and expect to use employee deferrals or plan features, the one-participant design may be the better fit, but only after the documents confirm what is actually available.

If you are likely to hire soon, do not decide as if staffing were frozen. Earlier sections already did the heavy lifting here: a plan that fits owner-only status can stop fitting when non-spouse employees enter the picture. That makes the hiring horizon a real decision input, not a side note.

Before you lock anything, run this compliance checklist:

- Confirm whether you are a specified person for Form 8938.

- Use the threshold set for your filing status. The commonly cited $50,000 baseline is not universal, and higher thresholds can apply for joint filers or taxpayers residing abroad.

- If no income tax return is required for the year, Form 8938 is not required for that year.

- File Form 8938 with your annual return by that return's due date, including extensions, and use the correct calendar year or tax year.

- Do not treat Form 8938 as a substitute for FBAR when FBAR is otherwise required.

- If you hold foreign financial accounts or interests in foreign retirement or deferred compensation plans, include those in your Form 8938 review before finalizing.

Think of this section as a first-pass fit test. A provisional choice gives you direction. The compliance and document checks either confirm that choice or stop you before money moves.

The 10-minute checklist before you open either account#

Use this as a go or no-go screen. Open only the account you can fund consistently, document clearly, and report correctly.

- Eligibility check: Confirm eligibility and participant details in writing before opening.

- Cashflow check: Stress-test your worst cash month before committing contributions.

- Feature check: Treat plan features as unconfirmed until provider documents say otherwise.

- Compliance check: If cross-border facts apply, complete Form 8938 and FBAR review before finalizing.

- Provider check: Get written fees, plan documents, deadlines, and support details before funding.

These five checks cover the usual failure points. If any one of them is unresolved, you do not have a ready-to-open plan yet. You have an open issue.

For Form 8938, keep one hard checkpoint in view. Certain U.S. taxpayers with aggregate specified foreign financial assets above a baseline $50,000 threshold must report them, and IRS notes higher thresholds can apply for joint filers or taxpayers residing abroad. Specified domestic entities also have $50,000 on the last day of the tax year and $75,000 at any time during the tax year tests.

The filing mechanics are straightforward even if the threshold analysis is not. Attach Form 8938 to your annual return and file by that return's due date, including extensions. If no income tax return is required for the year, Form 8938 is not required for that year. Filing Form 8938 does not replace FinCEN Form 114 (FBAR) when FBAR is otherwise required, and some accounts maintained by U.S. payers or U.S. institutions are excluded from Form 8938 reporting.

Treat this checklist like a gate, not a reminder list. If any line item is still fuzzy, pause the account opening and close the gap first. That short delay is usually cheaper than fixing a bad setup after funding starts.

For the broader retirement-plan comparison, read The Best Retirement Plans for Self-Employed Individuals.

If cross-border reporting could change your decision, pressure-test that risk early with the FBAR calculator.

Setup order so execution does not fail mid-year#

Execution usually fails because steps happen out of order, not because the basic idea was wrong. The fix is simple: choose plan type, choose provider, complete plan documents, then fund.

That order matters most in a year when cash is uneven. When money finally arrives, it is tempting to rush the deposit and tidy the paperwork later. That is exactly how classification and recordkeeping problems start.

| Setup step | SEP IRA path | Solo 401(k) path |

|---|---|---|

| 1. Confirm fit before opening | Confirm a Simplified Employee Pension design fits and identify each eligible employee. | Confirm it is truly a one-participant 401(k), meaning no employees other than a spouse if you rely on that status. |

| 2. Execute core plan document | Execute a formal written agreement. Form 5305-SEP can satisfy this requirement and is not filed with the IRS. | Execute the plan document and lock plan design choices, including whether to allow loans or hardship distributions, before first funding. |

| 3. Complete required setup actions | Provide required SEP information to each eligible employee and set up a SEP-IRA for each eligible employee. | Complete participant and account setup details before first funding. |

| 4. Lock timing and funding order | SEP setup can be completed as late as the income tax return due date, including extensions. | Set the first contribution date only after documents and recordkeeping are in place. |

IRS reporting notes recurring SEP mistakes in audits and voluntary compliance submissions, so skipped setup details are a known failure pattern. That is why the order above is worth following even if your provider makes the process look fast.

From there, keep one evidence pack from day one so year-end review is easier:

- Entity details and plan effective details.

- Payroll or compensation records used for contribution decisions.

- Contribution log with date, amount, account, and contribution type.

- Year-end verification artifacts for IRS support, including signed plan documents and reconciliation notes.

This is not overkill. It is what lets you answer ordinary questions later without reconstructing the year from scratch. If you need to explain why a contribution was paused, restarted, or classified a certain way, the evidence pack does the work for you.

Use a simple 30/60/90 checkpoint cycle as an internal control, not an IRS requirement:

- Day 30: confirm signatures, required notices, and account setup match plan design.

- Day 60: reconcile posted contributions to payroll and compensation records.

- Day 90: run a year-to-date tie-out and confirm assumptions still hold.

Add one pause guardrail for low-cash months: if projected month-end cash drops below your operating reserve floor, pause that month's retirement funding, log why, and set a restart trigger date. That is an internal operating rule, not an IRS mandate, but it is useful for freelancers whose cash cycles do not behave.

If you have a partner, schedule short check-ins at each checkpoint and review the same evidence pack together. Shared review lowers the chance that a detail slips through and makes later explanations much easier.

With setup handled, the last operating question is when a change is big enough to justify revisiting the plan or switching.

When to revisit your plan and when to switch#

Revisit the plan when the facts that justified it change. Switch only when that change is persistent, documented, and strong enough to matter in practice.

Two kinds of changes matter here. The first is operational: changes in staffing, hiring plans, or cashflow pattern that affect whether the original fit still holds. The second is reporting-related: changes in foreign-asset exposure or filing posture that change the compliance side of the decision. This section focuses on those reporting triggers, because they can alter what a workable setup looks like.

Four changes deserve a fresh review of your foreign-asset reporting exposure:

- Filing status or residency changed: higher thresholds can apply for joint filers and taxpayers residing abroad, so rerun your Form 8938 threshold check.

- Foreign financial assets changed: if your holdings now include interests such as a foreign retirement or deferred compensation plan, reassess whether you have specified foreign financial assets to report.

- Entity classification changed: if you now file through certain domestic corporations, partnerships, or trusts, confirm whether specified domestic entity rules apply.

- Income-tax-return filing requirement changed: if you do not have to file an income tax return for the year, Form 8938 is not required for that year.

For cross-border reporting, keep the checkpoints strict:

- If Form 8938 is required, attach it to your annual return and file by that return's due date, including extensions.

- Filing Form 8938 does not replace FinCEN Form 114 (FBAR) when FBAR otherwise applies.

- If you do not have to file an income tax return for the year, Form 8938 is not required for that year.

- Threshold context changes by taxpayer type. One baseline is aggregate value over $50,000, with higher thresholds in some cases.

- For specified domestic entities, the cited trigger is more than $50,000 at year-end or more than $75,000 at any time during the year.

Use the same evidence pack for this review and keep records of what changed and when. That turns a switch decision into something you can verify instead of something you react to under stress.

A simple way to avoid reactive switching is to keep a short trigger log. When one of these changes appears, note the date, what changed, and which document confirms it. That record gives you a clean basis for advisor review and keeps plan changes tied to facts rather than momentum.

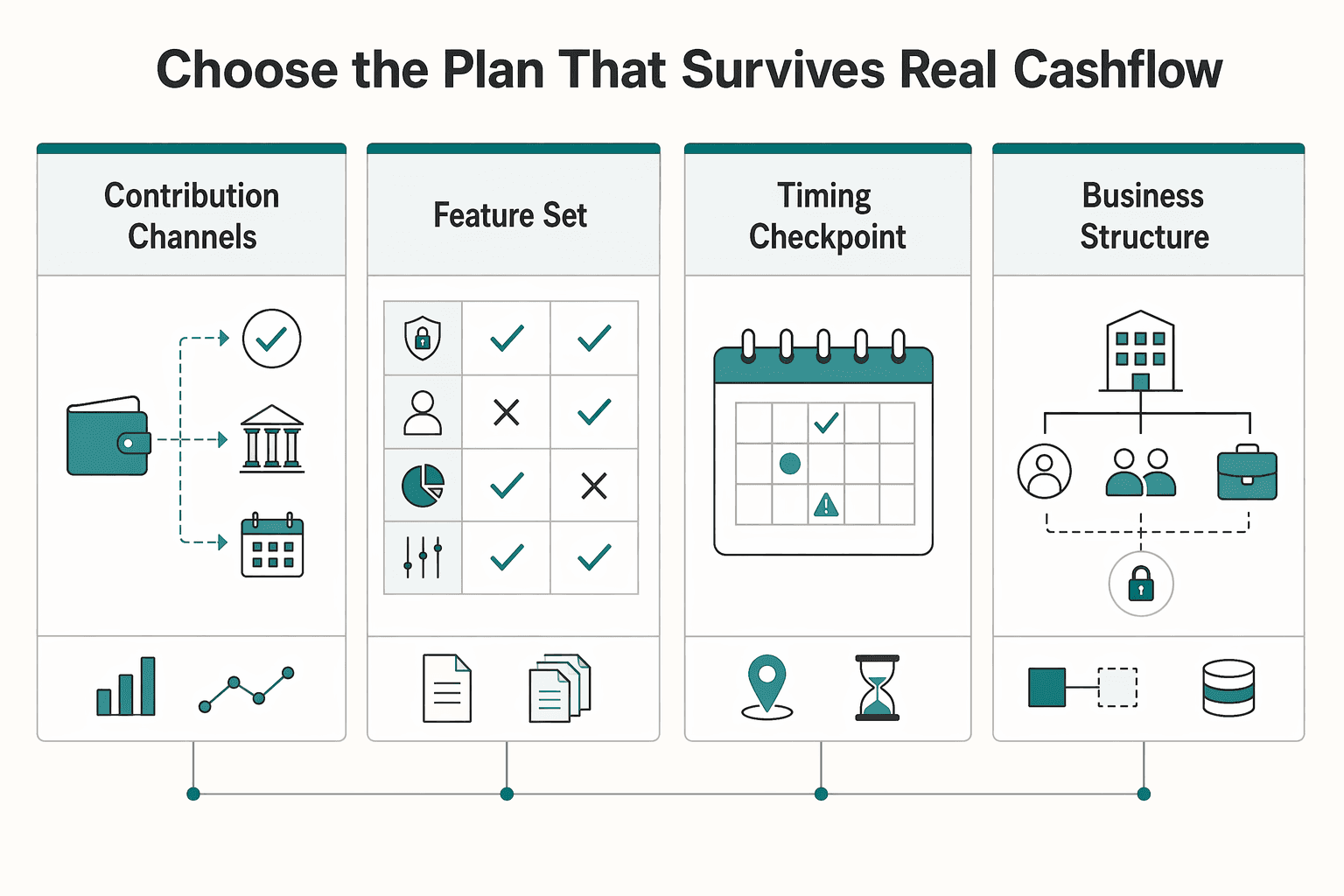

Choose the plan that survives real cashflow, not just a calculator#

The most useful answer is usually the least glamorous one: choose the plan you can keep funding, documenting, and reviewing when revenue is uneven. Maximum theoretical capacity does not help if the plan keeps breaking down in low-cash months.

Start with operating reality, then compare only the levers that change execution.

| Decision lever | SEP IRA (Simplified Employee Pension) | Solo 401(k) | Why this matters in uneven months |

|---|---|---|---|

| Contribution channels | Employer contributions only | Employer and employee contribution channels | Multiple channels can help when surplus arrives at different times, but they also require clearer classification |

| Feature set | No employee contributions, no Roth, no catch-up, no participant loans | Can include Roth, catch-up, and participant loans | Extra options matter only if your exact plan supports them and you can use them without stressing cash |

| Timing checkpoint | Confirm setup timing tied to the return due date, including extensions, and verify current-year limits before funding | Confirm contribution classification, plan terms, and current-year limits before funding | Timing flexibility is useful only when the paperwork and recordkeeping are already in place |

| Business structure fit | Depends on structure and employee situation | Defined for an owner with no employees, or only a spouse employee | A structure mismatch can force avoidable plan changes later |

If your forecast shows repeated shortfalls, favor the option you can fund without draining operating cash. If you reliably finish the year with surplus and will actually use the added flexibility, the one-participant plan may fit better. The real risk is choosing for the theoretical maximum, then missing contributions when cash arrives late or records get messy.

Use the scenario section and checklist in one sitting:

- Review last year's income, balance sheet, and cash flow statements.

- Build a cash flow forecast that includes a late-payment stress month.

- Choose the plan that still works in that stressed month, then confirm contribution timing and feature availability in provider documents before opening or switching.

- Consider having a qualified tax professional review your choice before opening or switching plans.

Final decision rule: if a plan works only when revenue is smooth, it is a weak fit for uneven freelance income. Choose the one you can keep current under ordinary stress, then optimize further only after that baseline is stable.

For edge-case planning after you choose, review Can I have both a SEP IRA and a Solo 401(k)?.

Once you pick a plan, use Gruv's tools hub to tighten the cashflow and compliance process you run each month.

Frequently Asked Questions

Is `SEP IRA` or `Solo 401(k)` better for most freelancers?

This section does not establish a one-size-fits-all winner between SEP IRA and Solo 401(k). If you are deciding between them, rely on your plan documents and current IRS rules.

Can you usually contribute more with a `Solo 401(k)` than a `SEP IRA`?

This section does not support a blanket "usually yes" or "usually no." Compare your own plan terms and official rules before funding.

When does a `SEP IRA` make more sense even if `Solo 401(k)` has more features?

This section does not establish when one option is better than the other. Make that call using plan-specific documentation rather than feature assumptions.

Can a `Solo 401(k)` include `Roth contributions` and `Participant loans`?

This section does not provide support to confirm that. Verify availability in your actual plan document and provider terms before relying on it.

What changes if I hire employees after opening a `One-Participant 401(k)`?

This section does not cover post-hire rule changes for a one-participant plan. Recheck eligibility and contribution handling before making additional contributions.

Can cross-border US freelancers face extra reporting concerns like `FBAR` or `Form 8938`?

Yes. If you are a specified individual and your specified foreign financial assets exceed the applicable threshold, attach Form 8938 to your annual return and file by that return's due date, including extensions. Filing Form 8938 does not replace a separate FBAR filing when FBAR rules otherwise apply. If you are not required to file an income tax return for the year, Form 8938 is not required for that year. Reportable assets can include foreign financial accounts and interests in foreign retirement or deferred compensation plans, and higher Form 8938 thresholds apply to joint filers and taxpayers residing abroad.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Retirement Plans for Self-Employed Individuals

Start with the plan you can actually fund without squeezing the business. Most bad retirement decisions by a self-employed owner do not start with the wrong tax idea. They start with a plan that looks good on paper, then collides with payroll, uneven collections, or a hiring change six months later.

Freelance Financial Management That Protects Cashflow First

Stabilize cash timing first. Perfect budgeting can wait. When payments arrive unevenly, the immediate win is a repeatable way to see what came in, what needs to be set aside, and what is actually safe to spend this week.

Can I have both a SEP IRA and a Solo 401(k)?

Yes, in some situations you can contribute to both a SEP IRA and a Solo 401(k) in the same year. The real question is whether that actually improves the outcome once you account for eligibility, contribution coordination, and extra admin. For many owner-only freelancers, one well-run one-participant 401(k) already gets them where they want to go without adding a second plan to manage.