Quick Answer

Start by verifying one legal name plus matching TIN, then complete and sign form w-9 for freelancers only when Part II is fully supportable. Send the finalized file to the requester (not the IRS), confirm receipt, and archive the exact version with date and recipient. If identity details, backup-withholding status, or U.S.-person status are unclear, pause before certification and resolve the correct form path first, including whether a W-8 route applies.

Start Here If You Want to Get W-9 Right the First Time#

Treat Form W-9 as an onboarding control point, not an admin afterthought. Before you sign, confirm the identity record you are certifying. This form gives your correct TIN to the person who may need to file an information return with the IRS.

That person is the requester. You give the form to the requester, not to the IRS. In contractor onboarding, this usually happens early, which means mistakes can spread into payee setup, withholding status, and later reporting records.

Focus on the name-and-TIN match, not the PDF itself. The TIN must match the name on line 1 to avoid backup withholding, and Part II is a certification under penalties of perjury that your TIN is correct. If you sign based on a guess, you create a correction loop at the start.

| Choice | Payment setup | Correction loops | Reporting cleanup risk |

|---|---|---|---|

| Submit now with uncertainty | Higher chance the requester sets up your payee record with data you already doubt | More likely to trigger re-requests and explanations after onboarding starts | Higher risk of TIN mismatch issues and backup withholding questions |

| Pause and verify first | Slightly slower upfront, cleaner setup | Fewer re-requests and less back-and-forth | Lower risk of unwinding bad identity data later |

Use this rule: verify the record first, then complete the form from that record. For most freelancers, the highest-value check is whether your line 1 name and TIN come from a current, defensible record, not memory or an old client file.

Run this pre-submit triage#

Before you open the form, do these four things:

| Triage step | What to confirm | Why it matters |

|---|---|---|

| Confirm the scope | The requester actually needs a W-9 for information-return reporting; if U.S. versus foreign tax status is unclear, sort that out first | Helps avoid forcing the wrong form |

| Verify the identity record | The exact name-and-TIN combination you plan to use, against your current record | Part II certifies TIN correctness and backup-withholding status |

| Choose the handoff route | The real requester or payables contact who should receive the form | You give the form to the requester, not to the IRS |

| Create a retention file now | Save the exact version sent, plus the date and recipient, in one folder | IRS guidance says the W-9 should be kept in requester files for four years |

- Confirm the scope

Make sure the requester actually needs a W-9 for information-return reporting. If your U.S. versus foreign tax status is unclear, sort that out first instead of forcing the wrong form.

- Verify the identity record

Write down the exact name-and-TIN combination you plan to use, then confirm it against your current record. This is the key checkpoint because Part II certifies TIN correctness and backup-withholding status.

- Choose the handoff route

Identify the actual requester or payables contact who should receive the form. Do not treat a W-9 as something you file with the IRS.

- Create a retention file now

Save the exact version you sent, plus the date and recipient, in one folder. That makes follow-up easier, and IRS guidance says the W-9 should be kept in requester files for four years.

Stop sign: if you cannot clearly defend the identity record and certification basis, do not sign yet. That is especially true if you are unsure about the TIN, backup-withholding status, or whether a W-9 is even the right form. In some cases, the payer may need to withhold 24% from reportable nonemployee compensation to U.S. persons. That is usually worse than a short verification pause.

Keep that framing in mind. The form is only as strong as the record behind it. If your facts may point away from W-9, confirm the correct form with the requester before submitting. If relevant, this pairs well with our guide on A guide to 'Form 8233' for foreign individuals receiving US scholarship or fellowship grants.

Build the Mental Model Before You Fill Anything#

Think of Form W-9 as an intake record for your identity details, not the reporting form itself. If a payer treats you as an independent contractor, the first step is usually to have you complete Form W-9 so they can collect your correct name and TIN for their records.

Sort the forms by job#

| Form | Who completes it | Primary use in this workflow | When it is used |

|---|---|---|---|

| W-9 | The payee or contractor | Collects the payee's correct name and TIN for payer records | Early in contractor setup |

| 1099-NEC | The payer | Reporting form for qualifying nonemployee payments, not the initial intake form | Later, to report qualifying nonemployee payments made during the tax year, subject to the reportable payment threshold amount |

| W-8BEN | Not covered by this section's approved source material | Do not infer handling from W-9 rules | Separate path. If you are unsure W-9 applies, pause and verify before choosing another form |

One guardrail matters here: 1099-NEC is for certain nonemployee payments, and generally not for employee wages. If a client is blurring worker classification, resolve that first instead of using a W-9 as a shortcut.

Follow the record, not the PDF#

Use a simple sequence: verify your exact legal name and TIN as one linked record, then complete the form from that record so the payer can keep it in their files. Those files may be kept for four years, so intake accuracy matters well beyond setup day.

Run a pre-fill verification check#

Before opening the form, confirm the following:

- The exact legal name you will certify, from your current identity or tax record.

- The TIN that matches that exact name, as one linked record.

- The correct requester contact responsible for payee records.

Use a go/no-go checkpoint here. If you cannot clearly defend the name-and-TIN record and why this is the right certification context, pause before you move to form completion. If you also need banking setup context, see The Best Bank Accounts for Freelancers in the UK.

Decide If W-9 Is Appropriate Before You Submit It#

Use a strict rule: submit only when you can support what you are certifying. If speed and certainty conflict, choose certainty. Form W-9 goes to the requester, not the IRS, and that payee file should be kept in the requester's records for four years.

Use two gates before you submit#

Whether a W-9 is appropriate comes down to two gates:

Gate 1: Verified identity record. You can show one exact legal name and the matching TIN as a single pair. The form is explicit that the TIN must match the name on line 1 to avoid backup withholding.

Gate 2: Supportable certification status. Part II is a perjury-based certification that your TIN is correct and that your backup withholding statement is accurate. If you cannot clearly support that language, stop.

If either gate fails, pause and verify first. If you are a foreign person and beneficial owner, the payer-facing form is generally Form W-8BEN, not W-9.

| Decision | What is true right now | Likely operational outcome |

|---|---|---|

| Submit now | Name and TIN are verified as one pair, and Part II is supportable | Cleaner payee setup and fewer correction loops |

| Pause and verify | Name and TIN are unclear, requester records conflict, or Part II language is unclear | Small delay now, lower risk of mismatch and withholding friction later |

Treat these as hard blockers#

Do not submit yet if any of these apply:

- You cannot confirm your current legal name and matching TIN as one pair.

- The requester's existing payee record shows different identity details.

- You are unsure how to support the Part II certification, including backup withholding language.

- You are not confident W-9 is the correct payer-facing form for your status.

- You are planning to send now and fix it later.

Prevent the correction loop before it starts#

Lock one authoritative version before sending. Complete the form from your verified name-and-TIN record, send that exact copy to the requester, and keep the same version in your own files. If the requester's records conflict with what you submitted, resolve the mismatch directly instead of assuming a new PDF alone will fix it.

That helps reduce later mismatch risk. CP2100/CP2100A notices are triggered when payee name or TIN data is missing or does not match IRS records. Those notices can lead to backup withholding workflows. When backup withholding applies, the payer may have to withhold at a flat 24% rate in specified cases, including when TIN data is not furnished correctly.

If you want a deeper dive, read How to Prepare for an IRS Audit. Not sure whether you should submit a W-9 or use a non-U.S. form instead? Run a quick first pass with Gruv's W-8 Form Generator, where enabled, before you certify anything.

Complete Form W-9 With a Pre-Submit Verification Sequence#

A good W-9 process is simple: verify first, certify only what you can support, then lock the exact file you send. A form that looks complete is not automatically ready for a requester who may use it for an IRS information return on income paid to you.

Use this four-step checklist#

| Step | What to do | Guardrail |

|---|---|---|

| Verify the source record first | Start with one current source record that ties your identifying information to your TIN | Do not combine details from different records or rely on memory or an old PDF |

| Complete the form from that record, then do a sanity pass | Fill out the form from the same verified source | Entries are consistent, optional fields are used only when they apply, and the address is readable for the requester's payee file |

| Treat the certification section as a certification step | Resolve any uncertain certification statement before signing | Do not send first and try to patch uncertainty with email caveats later |

| Create a delivery-ready file and lock the version | Save the exact copy you will send | Keep that exact sent version with recipient and date as the authoritative copy |

- Verify the source record first.

Start with one current source record that ties your identifying information to your taxpayer identification number, or TIN. Do not combine details from different records, and do not rely on memory or an old PDF. If you cannot point to one current record, stop.

- Complete the form from that record, then do a sanity pass.

Fill out the form from the same verified source. Before signing, do a quick operational check: entries are consistent, optional fields are used only when they apply, and the address is readable for the requester's payee file.

- Treat the certification section as a certification step.

If any certification statement is uncertain, pause and resolve it before signing. Do not send first and try to patch uncertainty with email caveats later.

- Create a delivery-ready file and lock the version.

Do a final requester-view review, then save the exact copy you will send. Keep that exact sent version with recipient and date, and treat it as the authoritative copy for later updates.

Before step 2, confirm that you are using the current IRS W-9 package and requester instructions, shown as 03/2024.

Separate cosmetic completion from real readiness#

| Checkpoint | Looks complete | Actually ready to certify |

|---|---|---|

| Name and TIN | Every box is filled | Identifying information and TIN come from one current record |

| Other fields | Optional and required fields are filled | Entries are consistent with your current record, and optional entries are used only when they apply |

| Address | An address is typed in | Address is readable and usable for the requester's payee record |

| Certification section | The form appears certified | Each certification statement is supportable now, with no unresolved question |

| File control | A draft exists | The exact sent version is saved with recipient and date and marked as the reference copy |

Keep adjacent filings out of this step#

Form W-9 has a narrow job: provide your correct TIN to the requester. Keep Form 8938 and FBAR analysis in separate tracks.

Form 8938 is attached to your annual return and filed by that return's due date, including extensions. If you do not have to file an income tax return for the year, Form 8938 is not required. Filing Form 8938 also does not remove any separate FBAR requirement.

When a Form 8938 threshold question is still open, record it as a separate pending check instead of treating it as part of W-9 completion.

Do the final requester-view review#

Before sending, read the form as if you were the payer onboarding a new vendor. If any field requires interpretation, fix it before handoff. Then send the reviewed copy, save that exact version, and label it as the authoritative copy for that requester.

You might also find this useful: A Guide to Form 1099-K for Freelancers Using Payment Apps.

Send, Store, and Update W-9 Like an Operator#

Once you sign, version control can become a major risk. Keep one clear record of who requested your W-9, who received it, which file is current, and where your proof is stored.

Send the signed W-9 to the requester, not to the IRS. The requester is the party required to file an information return, and you are the payee providing your TIN for that process.

Use one controlled handoff#

- Confirm the requester and the exact receiving channel, such as a finance contact, vendor portal, or other controlled electronic channel the requester uses.

- Send one finalized file only: the exact reviewed copy you intend to stand behind, using the current IRS Form W-9 (Rev. March 2024), not draft instructions marked "DRAFT, NOT FOR FILING."

- Save proof of transmission and, when practical, receipt or readability confirmation.

- File everything into one record thread right away.

Use clear file naming so current versus old is obvious, for example: W-9_Rev-03-2024_ClientName_2026-03-25_CURRENT.pdf. If you replace it, mark the prior copy as superseded and keep only one file labeled current.

Define your single source of truth#

Use one folder or client thread per requester as your single source of truth. Keep:

- the current signed file

- superseded files

- send proof and any receipt confirmation

- related payee communications about name, TIN, address, entity classification, or replacement form

This keeps stale copies from circulating and reduces avoidable mismatch issues. The IRS states the TIN must match the name on line 1 to avoid backup withholding, and the cited backup withholding rate is 24%.

| Update method | Clarity | Traceability | Error risk |

|---|---|---|---|

| New complete W-9 through the requester's controlled channel | High | High when sent file and proof are stored | Lowest practical risk |

| New complete W-9 through another controlled electronic handoff, including fax if used by requester | Good when recipient and date are clear | Good when transmission proof is saved | Moderate if storage is inconsistent |

| Edited old PDF without clear current or superseded labeling | Poor | Weak when multiple copies exist | High |

| Email-only change, for example "use my new TIN or address," without an updated signed form | Very poor | Weak and easy to lose | High |

Store it like sensitive data#

Treat W-9 files as sensitive data. Limit access to people handling vendor onboarding or tax records, use controlled sharing channels, and label the current version clearly so stale copies do not keep circulating.

For retention, note that IRS independent-contractor guidance says the W-9 should be kept in requester files for four years; treat that as requester-focused guidance and verify your own applicable retention window.

Related reading: A Deep Dive into Form 5472 for Foreign-Owned US LLCs.

Avoid the Failure Modes That Create Tax Headaches#

Two common W-9 failure modes are stale records and rushed Part II certification.

Audit the two failure points first#

Start by checking whether the underlying record is still current. If your name-and-TIN record is stale, requesters may file information returns from outdated data, and the instructions state that the TIN must match the line 1 name to avoid backup withholding.

Then review Part II before you sign. You are certifying statements that include U.S. person status and backup withholding status. The form says to cross out item 2 if the IRS has notified you that you are currently subject to backup withholding for underreported interest or dividends. If you are unsure, pause and verify before certifying.

Use this self-check: can you explain, without guessing, why your line 1 name, TIN, and Part II certifications all belong on one current record? If not, do not sign yet. Also keep one nuance in mind: for some payment categories, you may not need to sign the certification, but you still must provide the correct TIN.

Do not patch stale data with side notes#

If a record is wrong, do not rely on scattered email fixes. Correct the source once and send one complete corrected W-9 to every requester that has the stale version.

| Correction method | Consistency across requesters | Information-return mismatch risk | Cleanup effort later |

|---|---|---|---|

| Patch by email or notes | Low | Higher practical risk | High |

| Reissue one complete corrected W-9 to all requesters | High | Lower practical risk | Lower |

If you keep getting mismatch requests, stop making ad hoc fixes. Confirm the current record once, distribute the same corrected form, and log who received it and when.

Recovery checklist when something is off#

| Correction step | What to do | Record effect |

|---|---|---|

| Confirm the current line 1 name and matching TIN | Verify the current name-and-TIN pair before correcting anything | The TIN must match the line 1 name to avoid backup withholding |

| Re-check Part II statements | Review whether an IRS notice means item 2 must be crossed out | Pause and verify before certifying |

| Prepare one complete corrected form | Use the current IRS form version, for example, Form W-9 (Rev. March 2024), if that is the version in use | Replace stale records with one complete corrected form |

| Send the corrected version to each requester holding the stale record | Ask them to refresh the payee file | Do not rely on scattered email fixes |

| Save the corrected file, send proof, and a short change log | Keep the correction thread | IRS small-business guidance says requesters should keep W-9 records for four years |

Cross-border context calls for tighter version control, not looser assumptions. The current form includes line 3b for certain flow-through entities with direct or indirect foreign partners, owners, or beneficiaries in specified cases. That is a reason to verify carefully before certification.

Keep the guardrail simple: give the W-9 to the requester, not the IRS; maintain one current version; and replace stale copies with one complete corrected form.

For more on that, read Optionality for Freelancers Who Work Across Borders.

Handle Cross-Border Complexity Without Guessing#

When cross-border facts are in play, keep W-9 in its lane. It is a narrow intake step, not your full analysis. Keep W-9, Form 8938, and FBAR on separate tracks so you do not certify one obligation based on assumptions from another.

| Track | What it does | What it does not do |

|---|---|---|

| Form W-9 intake or certification | Gives the requester your correct TIN and certifications; give it to the requester, not the IRS. | Does not determine Form 8938 or FBAR filing duties. |

| Form 8938 evaluation | Tests whether you must report specified foreign financial assets and attach Form 8938 to your annual return, including extensions. | Does not replace FBAR. |

| FBAR evaluation (FinCEN Form 114) | Tests whether foreign financial accounts trigger a separate FBAR filing. | Is not filed with the IRS and is not replaced by Form 8938. |

W-9 line 3b is limited too. It can indicate certain foreign partner, owner, or beneficiary facts in some flow-through entity contexts, but it is not a full foreign-asset reporting analysis.

Use a sequence, not a guess#

- Confirm filing context first: are you in a U.S. person W-9 requester workflow for this tax year's facts?

- Run the Form 8938 test independently: identify filer category, apply the threshold that matches that category, then document whether attachment to the annual return is required.

- Run the FBAR test independently: determine whether aggregate foreign account value exceeded

$10,000at any time during the calendar year. Do not use account taxability as the trigger. - Pause if residency, ownership, or entity facts are unresolved.

- Certify W-9 only after open items are cleared.

Build a defensible evidence file#

Document the facts you relied on, any unresolved questions, and the timing of your review so a pause is defensible and you avoid retroactive guesswork. Record the filer category and verified threshold basis used for Form 8938, and the foreign-account facts used for FBAR. Also note whether each track resulted in an attachment, a separate filing, or no filing. Once those cross-border determinations are confirmed, keep one current W-9 version aligned across onboarding, payment setup, and tax records.

For a step-by-step walkthrough, see Form T2125 for Canadian Freelancers Without Filing Guesswork.

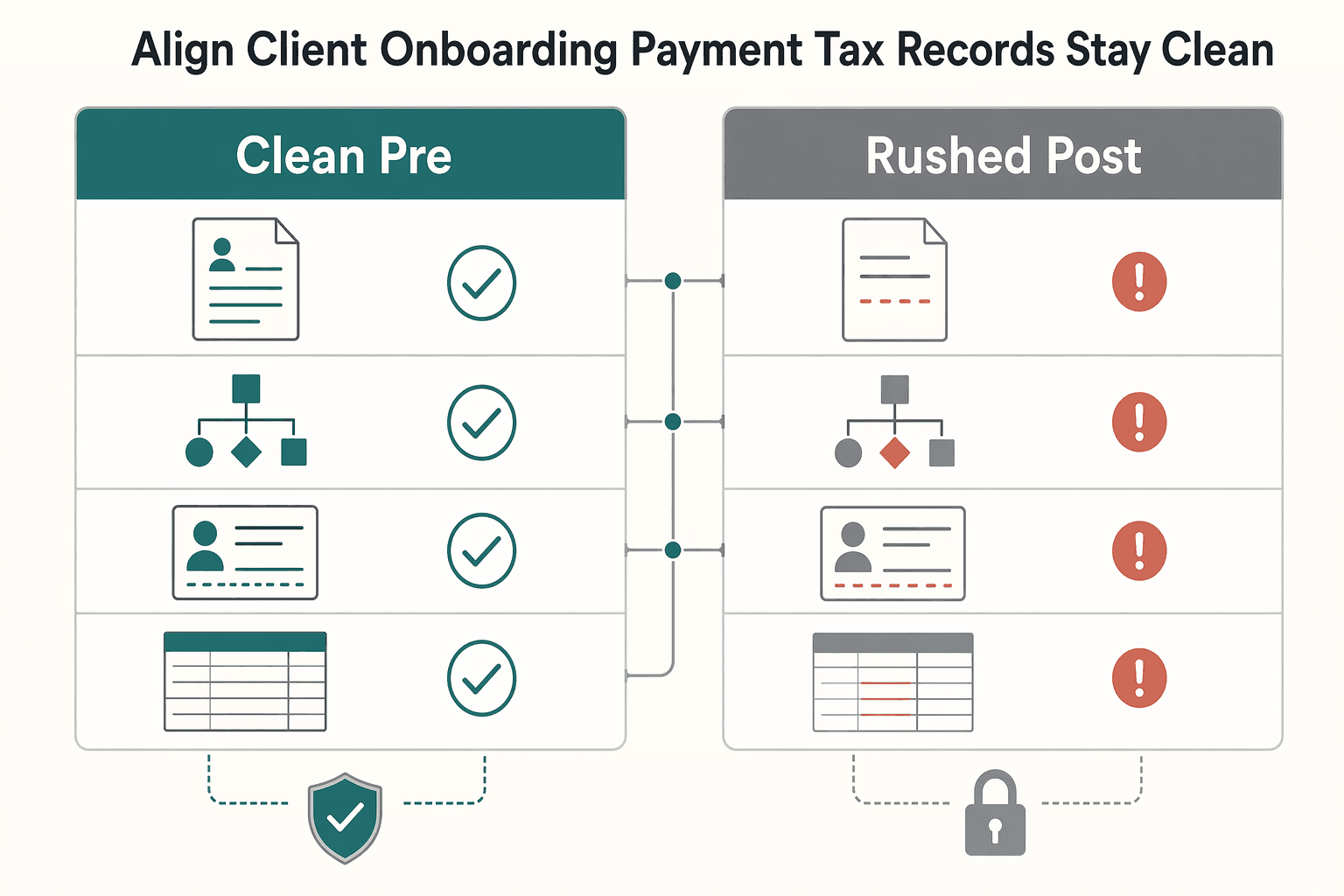

Align Client Onboarding So Payment and Tax Records Stay Clean#

The cleanest setup is to treat tax intake as a pre-payout gate, not post-payout cleanup. If you want payment setup and year-end reporting to stay aligned, provide a completed W-9 before payments begin.

Keep the intake packet practical: a finished W-9 with current taxpayer details such as legal name, business structure, and taxpayer ID information. This is not cosmetic. W-9 data is later used for Form 1099-NEC reporting, so inaccurate payee data can create reporting issues at tax time and extra cleanup work. Proper W-9 management also helps reduce penalty risk and maintain a cleaner audit trail.

| Intake approach | Payment flow | 1099 accuracy | Correction workload |

|---|---|---|---|

| Clean pre-payout tax intake | Payment setup starts after tax intake is complete | Better chance year-end reporting uses current payee data | Lower risk of tax-time fixes |

| Rushed post-payout cleanup | Payment starts before tax intake is complete | Higher risk of payee-data mismatches at year-end | More tax-time cleanup and corrections |

Use this checkpoint before payout setup:

- Complete the W-9 before payment setup.

- Review key taxpayer details for accuracy, especially legal name and taxpayer ID information.

- Submit the completed form to the payer before the first payment.

Keep W-9 information current so payment reporting stays accurate.

The Bottom Line for Low-Stress W-9 Compliance#

Only submit Form W-9 when your identity and certification facts are clear, current, and defensible. If you cannot support your name, TIN, or certification without guessing, pause and verify before you sign.

Use this three-step close every time: verify your source record, send one controlled current version, and reissue a full version when facts change. That is a practical way to avoid cleanup later when your data is used for information reporting, often Form 1099-NEC and in some cases 1099-MISC.

Timing can add pressure. Requesters often ask for this one-page form during onboarding or before first payment, and many send a blank copy to complete. Speed should not replace verification.

| Approach | Stress | Rework risk | Record clarity |

|---|---|---|---|

| Verify, then submit | Lower | Lower | One current file supports the payee record |

| Submit, then fix | Higher | Higher | Old and corrected versions can conflict |

Closeout checklist#

- Verify legal name and TIN against your source record.

- Confirm the certification is still true today.

- Complete one current version.

- Send it through a secure channel.

- If you keep internal records, save the exact copy sent with recipient and date.

- Reissue a new complete version when facts change.

- Mark the prior version as superseded.

If your U.S. person or residency facts are unclear, pause and escalate before certifying. W-9 is generally used for U.S. taxpayers, and foreign contractors may need Form W-8BEN instead. Document what you know, get advice, and contact Gruv before you submit.

For broader workflow ideas, we covered adjacent systems in The Best Zapier Workflows for Freelancers. If you want a repeatable intake process with tax-document workflows and audit-ready records where supported, review Gruv's implementation details in the developer docs.

Frequently Asked Questions

What is Form W-9 for freelancers?

Form W-9 lets a payer collect your correct name and taxpayer identification number for information returns. If you are a U.S. person, including a resident alien, this is the certification document the requester uses for your payee file. Verify your legal name and TIN first, then sign.

Do I send Form W-9 to the IRS or to my client?

Send Form W-9 to the requester, not to the IRS. In most cases, that is the client or team handling information returns. On the IRS independent-contractor page, requester-side guidance says the W-9 should be kept in files for four years.

What information must match on a W-9 to avoid issues?

Your legal name on line 1 and your TIN must match as one linked record. IRS instructions warn that a mismatch can lead to backup withholding, and Topic 307 states withholding is a flat 24% when trigger conditions apply, including not giving your TIN in the required manner. Treat name and TIN as one verification step before you certify anything.

Why does a client ask for Form W-9 before paying me?

A client usually asks for Form W-9 before paying you so they can build a correct payee file before payments start. That file supports later information-return reporting, such as Form 1099-NEC when applicable. Confirm who handles information returns, then send the final version there.

When should I update a previously submitted Form W-9?

Update it when a requester has payee data that is no longer current or correct. Send a new complete Form W-9, then mark the old version as superseded instead of patching a signed file through scattered edits. That can keep recordkeeping clearer and reduce the chance that an outdated copy stays in use. | Checkpoint | New complete W-9 reissue | Piecemeal corrections | |---|---|---| | Current document on file | One signed current version | Old signed form plus separate edits or email fragments | | Version control | Clear current versus superseded copy | Can be harder to confirm which version is current | | Name-and-TIN handling | Name and TIN are revalidated together on one form | Updates can become fragmented across records |

When should a globally mobile freelancer pause and talk to a tax professional?

Pause when you cannot support the Part II certification without guessing. That includes uncertainty about your U.S. person certification, changed residency facts, or unresolved related reporting questions. If you are a foreign person, request the appropriate Form W-8 or Form 8233 path, and keep Form 8938 and FBAR evaluations separate from Form W-9.

Watch

Form W-9 Guide for Independent Contractors

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Prepare for an IRS Audit

Treat an IRS audit as a records check, not a contest. Your job is to show, item by item, how what you filed ties back to the records behind it.

The Best Bank Accounts for Freelancers in the UK

Confirm with each provider directly, as UK bank product details and eligibility requirements can change. Always verify the current terms on official provider pages before applying.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.