Quick Answer

No, most freelancers and consultants should not rely on tax resident of nowhere as a primary strategy. The article treats it as a narrow edge case and recommends one residency position you can support across filings, invoicing records, and account reviews. It also warns that the common 183-day benchmark is only one input, and overlap situations may require treaty analysis under Article 4 before filing.

Why the 'Tax Resident of Nowhere' Story Fails Under Review#

A "tax resident of nowhere" position may be possible in narrow cases, but it can be hard to defend when your records are inconsistent. The practical target is simpler and stronger: choose one tax residency position you can defend across filings, contracts, and account reviews.

An advisory note dated 21 Oct 2020 says this outcome can be possible and treats U.S. citizens as a separate branch. That framing matters. Edge cases exist, but they do not remove the need for one coherent story in your documents.

For a lower-stress approach, decide early and document continuously. Waiting until filing season creates rushed edits, contradictory declarations, and avoidable disputes with providers that ask for tax-country confirmation.

Use this sequence before making any aggressive move:

- Map your factual ties first, then consider outcomes.

- Pressure test whether more than one country could plausibly claim you.

- Choose the position you can keep consistent across documents.

- Escalate early when facts conflict instead of improvising near deadlines.

Outcome-first narratives tend to underweight documentation quality. If you are a U.S. citizen, treat that as an immediate branch and get country-specific advice before assuming a no-residency path. For everyone else, the same rule applies: pick a setup you can maintain year round with clean evidence.

Read the rest of this article as a set of decision gates. First, confirm what the claim means. Next, test defensibility. Then stress test overlap risk, reporting friction, and record quality. By the end, you should be able to classify your case as defensible now or escalate before the next filing cycle.

What tax resident of nowhere actually means#

A claim like this usually means you are asserting that no country currently treats you as tax resident under its domestic rules. That is a legal-status claim, not just a travel identity.

Tax residency determines which country can tax your income and assets. Physical presence often matters, including the common 183-day benchmark, but day count alone is not the full test. Personal and financial ties can matter too, and residency is not determined by visa type or citizenship by itself.

Most confusion comes from mixing separate questions. Some lifestyle discussions describe perpetual travel without a permanent residence as a real concept. Compliance-focused commentary, however, warns that trying to legally avoid taxes by "living nowhere" is risky and often not viable. Those frames are related, but they are not the same decision.

Keep these checks separate when you assess your position:

- Legal feasibility: can your facts support the claim under domestic rules?

- Defensibility: can your records and reporting support that claim consistently?

- Administrative fit: can you maintain the documentation burden all year?

A quick self-test helps here. If you cannot explain your position in one short paragraph and match each sentence to a document you already hold, your position is not ready. If you can explain it but cannot keep it consistent across tax forms, contracts, invoicing details, and account profiles, it is also not ready.

When defensibility is weak, declarations and records drift apart, creating compliance risk. The lower-risk path is a residency position you can explain the same way everywhere. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Legal possibility is not the same as defensible compliance#

A position can look legally possible in theory and still fail under review if your evidence is thin or contradictory. That is the central distinction, and it is where most avoidable mistakes happen.

Headline answers blur it because they compress complex facts into yes-or-no claims. Use a stricter test for your own case, and do not treat broad internet certainty as proof that your file is review-ready. Ask two questions in order: can this happen, and can you prove it under review.

Based on the material reviewed here, there is not enough reliable support to treat a no-residency position as defensible on its own.

If the second answer is weak, stop and fix the file before you proceed. Defensibility means your records tell one coherent story for the same period.

Use this checkpoint before you commit:

- Write a one-page statement of your current-year position.

- Build a dated movement timeline for the full year.

- Reconcile country and address details across contracts, invoices, account profiles, and tax forms.

- Mark any month where facts changed and explain that change in one sentence.

In practice, weak defensibility usually shows up first in ordinary places. A payout provider may ask for tax-country confirmation. A bank may ask for profile refresh details. A client may request updated forms. If each answer uses slightly different facts, friction can start before any formal dispute.

If you cannot produce coherent evidence for your overall position, do not try to run a nowhere position. Short-term tax reduction can look efficient on paper, but long-term stability usually comes from consistency across banking, invoicing, and filings.

That leads to the next question: once proof quality is central, treaty overlap becomes easier to evaluate without guesswork.

How residency conflicts are actually resolved across countries#

When two countries can both support a residency claim for the same period, treaty tie-breaker criteria become relevant. The outcome is highly fact dependent, and the quality of your file often matters more than your preferred narrative.

A double taxation convention provides the legal method for resolving overlap. In that context, Article 4 addresses residence. Treat it as process guidance, not a guaranteed outcome.

Treaty analysis is generally used when both countries can credibly claim residence for the same period. Treating tie-breakers as a shortcut creates false confidence and weak submissions.

Home Test (plain language): this asks where a genuine permanent home is available to you. For freelancers, one consistent address story across contracts, invoices, account profiles, and tax records is easier to defend.

Vital Interests Test (plain language): this asks where your personal and economic ties are strongest when home alone does not settle the overlap. If records point in different directions, conflict risk rises quickly.

A treaty can resolve overlap, but it may not cure contradictory or incomplete records for the same months. If one set of records says country A and another says country B, tie-breaker language alone may not erase that contradiction.

Run this checkpoint before filing:

- Build a month-by-month timeline of where you lived and worked.

- Reconcile country and address details across contracts, invoices, account profiles, and tax forms.

- Flag any period where facts could plausibly satisfy two countries at once.

A useful stress test is to ask whether a neutral reviewer could follow your timeline without calling you for clarifications. If not, your overlap analysis is still too fragile. If your facts can support two countries at the same time, treat that as escalation territory and get specialist review.

Risk map for globally mobile freelancers and consultants#

For globally mobile independents, risk usually comes from record consistency and jurisdictional accountability, not just travel style. As cross-border activity grows, a no-residency position gets harder to maintain because more records need to support the same story.

| Profile | Main pressure point under tax compliance | What to verify first |

|---|---|---|

| Single-client consultant | One income source can make your jurisdictional ties look concentrated in one place, even with frequent travel. | Track physical presence by calendar year and check whether any country crosses the typical more-than-183-days benchmark used in many jurisdictions. |

| Multi-client freelancer | Revenue may be diversified, but invoice trails and contract timing can still point to multiple jurisdictions. | Reconcile where work was performed and where key contract and payment records are maintained. |

| Incorporated solo business | Personal and company records may drift apart, creating competing narratives about where activity sits. | Keep company admin records, owner residency records, and billing records aligned for the same periods. |

Tax residency, physical presence, and jurisdictional accountability all shape risk. If your filing position changes, your records should show a clear factual break.

Movement pattern is often the practical divider. If you operate mainly from one country, residency ties are usually clearer. Continuous cross-border movement can trigger more complex overlap risk across jurisdictions.

There is also a sequencing effect as your business grows. Early on, you may have one or two clients and one payout channel. Later, you may have multiple contracts, more invoices, and additional financial accounts. Each added surface increases the chance that one field drifts from the rest.

Run this quarterly checkpoint, not just a pre-filing review:

- Update a day-count ledger by country with entry and exit proof.

- Match invoice periods and client contracts to location facts for the same months.

- Confirm declared address and residency fields are consistent across tax forms and financial accounts.

Timing matters here. If you review only at year end, you may find conflicts when deadlines are close and correction time is short. If you review quarterly, conflicts are usually easier to fix before they spread across providers.

The tradeoff is flexibility now versus cleanup cost later. Late compliance pressure usually means more rework when records are weak. If revenue or complexity is rising, prioritize certainty over aggressive gaps.

Red flags that usually break the nowhere strategy#

This strategy usually breaks when your records point to different residency stories in the same year. Once that conflict appears, each additional filing or review can amplify it.

Onboarding and compliance checks often surface mismatches quickly: one tax country in a bank profile, another on a payment platform, and a third in invoice or entity records. The same friction can appear when ownership, address history, or business details are incomplete.

U.S.-linked reporting is another common failure point when you handle records separately instead of as one file. FEIE still requires reporting excluded foreign earned income on a U.S. return, and part-year qualification requires adjusting the maximum by qualifying days. For 2026, the maximum exclusion is $132,900 per person and the general housing expense limitation is 30% ($39,870). A full-year claim with only part-year qualifying days creates an obvious mismatch.

FBAR prep can create avoidable conflicts too. Amounts are recorded in U.S. dollars rounded up to the next whole dollar, and a negative computed maximum account value is entered as zero. If your method is inconsistent, figures may fail to reconcile across records.

These conflicts are rarely isolated. A mismatch in one profile can force updates in several places, and each update can trigger another request for supporting documents. That loop is where many freelancers lose time and confidence.

Use this pre-submission check before filing or replying to remediation:

- Compare declared tax residence across bank, payment, brokerage, and invoicing profiles.

- Reconcile identity fields across account and tax records.

- Validate FEIE assumptions against qualifying days and supporting travel records.

- Apply one FBAR calculation method and keep the worksheet used for conversion and rounding.

Add one more practical check after this list: make sure dates, names, and addresses are formatted consistently across forms and account records. Small formatting differences can trigger follow-up requests even when the underlying facts are correct.

Forum-style loophole advice often fails because it skips document quality. IRS LB&I practice units are not official pronouncements of law. A common failure mode is timing: one review triggers rushed re-documentation across multiple providers at once.

A decision sequence to choose a defensible residency setup#

Use a strict sequence and force a binary output: defensible now, or escalate before the next filing cycle. Anything in between usually means unresolved risk.

| Case | When it fits | Practical output |

|---|---|---|

| Clear single residency | One country has stronger factual ties and records are consistent. | One consistent set of declarations across forms and profiles. |

| Transition year | Facts changed mid year. | Explicit start and end periods in your notes and supporting records. |

| High-conflict case | Two countries have credible claims and facts do not separate cleanly. | An escalation package for specialist review. |

Start with facts before tax outcomes. Build a single-year timeline by country showing where you lived, worked, got paid, and which address appears across contracts, invoicing records, and financial accounts. Then compare those facts to each country's domestic residency criteria.

For this first step, do not try to optimize your tax result yet. Your goal is to make the factual record internally consistent. Optimization before consistency is the fastest way to create contradictions.

Next, map overlap risk and treaty use only if dual residency exposure appears. Domestic rules decide first whether each country can treat you as resident. If both can, treaty residence rules become relevant. In that context, Article 4 provides rules when the same person is treated as resident by both contracting states. Convention scope applies only to residents of the two contracting states.

Use the treaty text and its Technical Explanation together, then test both against your records. The explanation is a guide, but it cannot fix weak facts. If the file shows conflicting addresses, mismatched declarations, or overlapping country claims for the same months, your treaty-residence position is fragile.

Classify the case and act:

- Clear single residency: one country has stronger factual ties and records are consistent.

- Transition year: facts changed mid year, so document clear period boundaries.

- High-conflict case: two countries have credible claims and facts do not separate cleanly.

The practical output should match the category. A clear single residency case should produce one consistent set of declarations across forms and profiles. A transition year should produce explicit start and end periods in your notes and supporting records. A high-conflict case should produce an escalation package for specialist review.

If two countries have credible claims and your facts do not produce a clean treaty-residence result, treat it as a high-conflict case and escalate before filing. Keep your timeline and declarations consistent across tax forms, account declarations, invoice details, and legal address records.

Before filing, run a final yes-or-no check: can a reviewer trace your timeline, follow your declared position, and reconcile your forms without asking for missing context? If not, escalate before the next filing cycle.

Build your residency evidence pack before you need it#

Your position is only as strong as your records. To keep it defensible, maintain one dated, versioned evidence pack that tells the same story across filings, account checks, and payout reviews.

| Bucket | Included records |

|---|---|

| Residential proof | Dated address history, housing records, and entry and exit records that support your residency timeline by period. |

| Economic proof | Contracts, invoices, payment records, and entity records that show where income activity was directed and administered. |

| Administrative proof | Filed returns, declarations, onboarding forms, and account profile snapshots, including submitted versions and confirmation receipts. |

Those three buckets do most of the work. Keep each one current, and add new records as soon as the facts change.

A practical file structure helps. Keep one folder per year, one subfolder per quarter, and clear labels for each document type. Add a short note whenever facts changed during the year so future you can reconstruct the timeline without guessing.

Where relevant, run consistency checks across U.S.-linked records. Your tax forms and account records should not present conflicting identity or residency stories. For FEIE, keep two anchors in the file: excluded foreign earned income is still reported on a U.S. return, and part-year qualification requires adjusting the maximum by qualifying days, with a 2026 maximum of $132,900 per person.

For FBAR prep, standardize valuation before filing. Use a reasonable approximation of each account's greatest value during the year, and value each account separately. Record amounts in U.S. dollars rounded up to the next whole dollar. If you use a non-Treasury exchange rate, keep the source document in the same pack.

Keep response-ready material for routine remediation in the same pack. That includes profile snapshots, confirmation receipts, and the exact forms submitted. When a provider asks for clarification, you can respond with the same fact set instead of rebuilding your case from memory.

Timeline discipline is the key control. Keep records dated to support your bona fide residence or physical presence timeline. Add short notes for unusual events that may affect time-requirement waivers, and verify current IRS waiver countries and effective dates when relevant. Consider a quarterly reconciliation so you fix conflicts before filing pressure. Related: Understanding Indonesian Taxes for Foreign Workers.

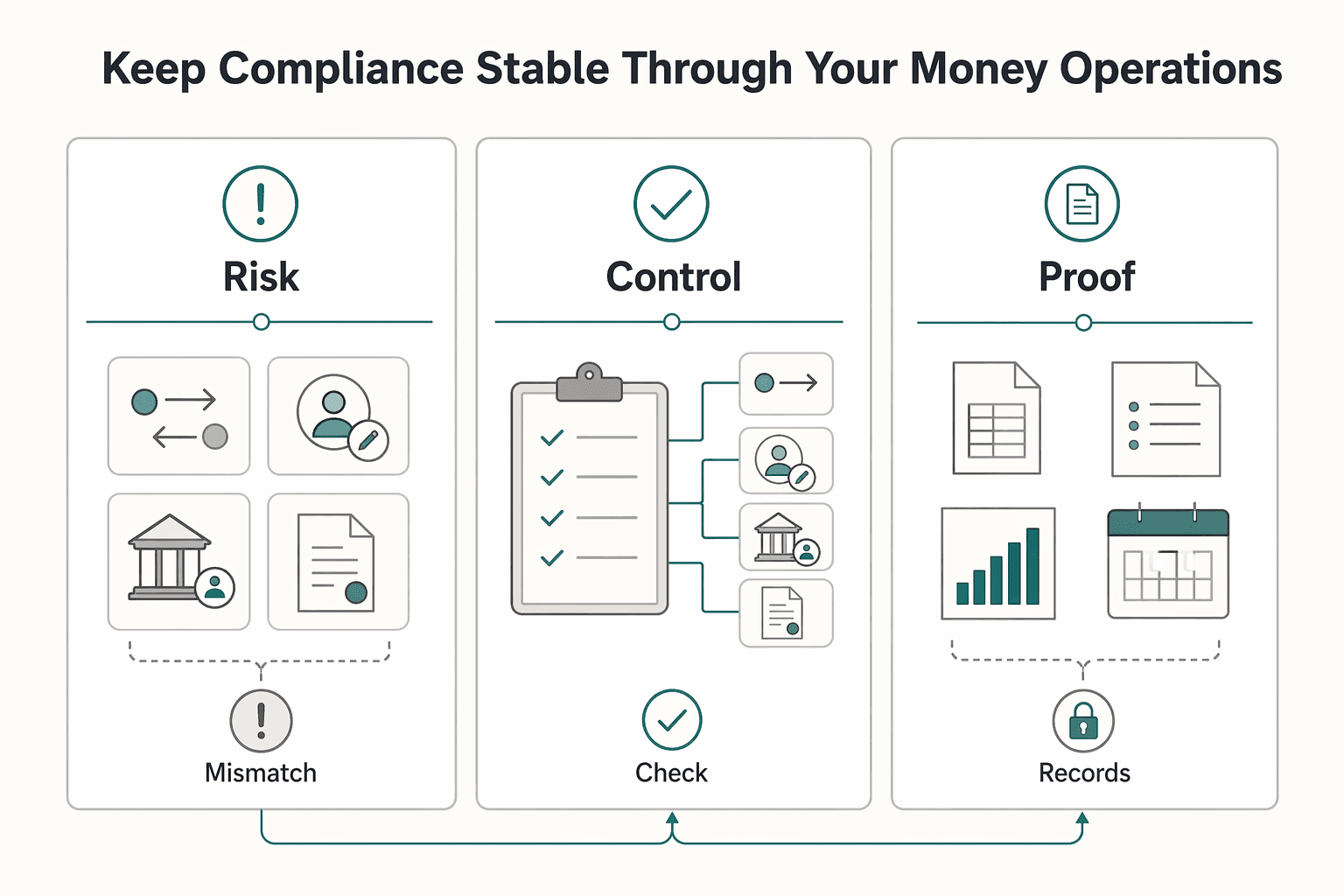

Keep compliance stable through your money operations#

A residency plan only works if your day-to-day money records stay aligned. Routine collections, payouts, and profile edits can trigger additional compliance review points, and mismatched details can slow operations quickly.

Treat reporting visibility as an ongoing consistency check, not a one-time setup. The target is one identity and residency story across invoice headers, payout profiles, account ownership details, and entity records for the same period.

Public narratives are not compliance evidence. Promotional flag theory content can make low-tax outcomes look simple, while forum commentary often mixes broad warnings with narrow technical claims. Use those as prompts to verify your file, not as a basis for filing decisions.

For stacks like Gruv, where supported, set controls before review requests arrive:

- Require approval for high impact edits to tax country, legal name, and ownership fields.

- Keep audit trails for profile and payout configuration changes, including who changed what and when.

- Export regular snapshots of invoices, payout profile data, and ownership records into your evidence pack.

- Reconcile identity and residency fields across providers on a fixed cadence.

- If one provider triggers remediation, run one full consistency pass and reuse the same document set across providers.

A useful operating habit is to treat every profile change as a tax-data event. If legal name, address, or tax country changes in one place, schedule same-week checks across the other platforms that store related data.

Keep the quarterly check binary: compare invoice identity, platform tax profile, and account ownership details line by line, then resolve any mismatch before new forms or onboarding. The tradeoff is clear: low-friction onboarding is faster today, but deeper records can reduce the risk of freezes and repeated document loops later.

When to hire a tax professional and what to bring#

Hire a tax professional early when your facts support more than one plausible residency outcome. Waiting until a filing deadline usually turns an analytical problem into a time problem.

Escalate if these signals appear together:

- Conflicting country ties.

- Uncertain DTAA position.

- Facts that point in different directions under domicile and day-count tests.

Residency calls are multi-factor and fact intensive. Minnesota is a useful example. Residency is tested through both domicile and statutory residency. Domicile is reviewed through multiple presumptions and factors, and statutory residency is tied to being present more than half the year. That is state specific, not universal, but it shows why edge cases need specialist review.

Bring a concise case file so the first meeting can produce decisions:

- A dated movement timeline by country, including entry and exit windows and where you maintained a permanent home.

- Your tax residency hypothesis in one sentence, plus the strongest supporting fact and weakest counter-fact.

- Treaty questions for each country pair where your position is unclear.

- Your current filing posture: filed, pending, and possible amendments.

- Prior tax correspondence or compliance notices that could affect your residency position.

Use the first meeting to set decision outputs, not just discuss background. If the adviser needs follow-up material, agree on exactly what is missing and by when. That keeps the engagement focused and prevents open-ended discovery loops.

Set a clear engagement target: a written decision, a filing plan, and a documentation maintenance plan through the next review period. After you receive those outputs, run a practical implementation pass: update forms, align account declarations, and file the evidence updates in your pack. Advice only reduces risk when it is translated into consistent records.

Conclusion#

The practical win is not nowhere. It is a defensible tax residency position you can prove consistently. A no-residency strategy can be high risk, and day counts alone may not be enough under review.

Treat the 183-day rule as one input, not the answer. Residency analysis can include personal and financial ties, and tax residency can apply without citizenship. That is why a plan that looks simple on a calendar can still fail later.

Use this closeout process before filing:

- Pick one primary residency position for the year and state it clearly.

- Keep dated evidence that supports your core ties and filing position.

- Escalate early when facts are mixed, evidence is thin, or your position depends on one threshold alone.

Cross-border visibility can be high through FATCA and CRS reporting channels. Choose clarity early, maintain records continuously, and get professional review before edge cases turn into compliance problems.

If you want one final quality check, ask two plain questions: does every key document support the same residency story? Could a neutral reviewer follow your timeline without missing context? If both answers are yes, you are in a defensible position. If either answer is no, escalate now, not when a deadline forces rushed decisions.

Frequently Asked Questions

Can you legally be a tax resident of nowhere?

Whether that is legal depends on the jurisdictions and facts involved. Legal possibility is different from review defensibility. Spending fewer than 183 days in one country does not, by itself, guarantee nonresident treatment everywhere. The position has to survive document checks, not just calendar math.

Why is tax resident of nowhere risky for freelancers?

The main risk is proof burden, not theory. A day-count-only strategy can lead to unexpected liabilities and denied treaty protection. Most modern tax tests use criteria beyond days present, so mixed records are hard to defend.

Do I need tax residency somewhere to stay compliant?

For lower-friction compliance, use one clearly supportable residency position unless specialist advice says otherwise. Status can change tax treatment materially. In the U.S. example, resident aliens are generally taxed on worldwide income, while nonresident aliens are taxed on U.S.-source income and certain U.S.-connected business income. If your status is uncertain, resolve that first instead of filing on assumptions.

What evidence best supports my tax residency claim?

Use an organized file that covers days present, personal and economic ties, and filing records. Prioritize records that show where personal and economic ties are strongest, since center of vital interests is a key tie factor. Keep a dated movement timeline and link each key claim to a document you can produce quickly.

How do treaty tie-breakers decide my status?

Tie-breaker analysis is not just a day-count exercise. In plain terms, it looks at tie factors, including where personal and economic ties are strongest. If those facts are mixed, outcomes are less predictable and documentation quality matters more. Treat treaty analysis as a method that depends on strong records, not a shortcut around weak ones.

When should I talk to a tax professional instead of DIY?

Escalate when your position depends mainly on day counts, your tie-factor evidence is weak, or your treaty position is unclear. Bring a concise file with your timeline, filing posture, treaty questions, and core supporting documents. The goal is a written decision and a filing plan you can execute.

Try a related tool

Rina focuses on the UK’s residency rules, freelancer tax planning fundamentals, and the documentation habits that reduce audit anxiety for high earners.

With a Ph.D. in Economics and over 15 years of experience in cross-border tax advisory, Alistair specializes in demystifying cross-border tax law for independent professionals. He focuses on risk mitigation and long-term financial planning.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Indonesia Tax for Foreigners With a Defensible Filing Path

---

How to Invoice as a Freelancer Without Chasing Late Payments

Set one standard from the start: every freelance invoice should identify the client, itemize the work, state agreed terms, and be tracked until funds settle. That habit helps prevent avoidable payment delays and keeps cash flow more predictable.