Quick Answer

Start with facts, not tax optimization: log where you were, where services were delivered, and when income was received, then classify each country by residence and source exposure plus any U.S.-connected filing duty. For digital nomad taxes, the practical control is a monthly evidence cycle using a day map, work-location notes, invoice and payment support, and dated posture labels. If overlap appears, document the exact income line before choosing treaty analysis, FEIE, or Form 1116 credit handling.

Your Digital Nomad Tax Problem Isn't Paying Less-It's Knowing Where You're Taxable#

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Most expensive mistakes start with fuzzy facts. Once you pin down your exposure, later decisions get faster, safer, and easier to defend.

Start with exposure, not optimization#

Use one anchor definition: tax residence is where a country treats you as a tax resident. You will hear the 183-day shortcut a lot. Residence often gets described as kicking in around that mark, but that is not universal, and it does not settle every case. If you are relying on day count alone, read 183-Day Rule Explained: Stop the Tax Myths Before They Cost You first.

A digital nomad works remotely while moving across locations. That mobility can change your tax exposure midyear even if your clients and contracts stay the same.

Also, do not assume your home state is automatically out of scope. Some states may keep taxing you when ties remain, such as property, a driver's license, or bank accounts. Working outside your home state can also create tax implications, and outcomes can vary by income type such as salary versus freelance income.

Separate residence scope from filing scope#

Treat these as separate questions:

- Residence scope: where you may be taxed because of your overall connection.

- Filing scope: where filing exposure may come up based on where you worked and how income was treated.

For most freelancers and consultants, three factual checks can clarify the picture:

| Question you must answer | Why it matters | Evidence to keep tidy |

|---|---|---|

| Where did I spend time? | Time and location can affect residence and filing exposure | Day log, entry/exit records, tickets, lodging or lease records |

| What work happened where? | Helps map where exposure may exist before filing decisions | Calendar notes, project logs, client timeline notes |

| What revenue happened while I was there? | Helps connect income records to your location timeline | Invoices, payment confirmations, monthly ledger |

If those answers are weak, your tax position is weak. A practical test is whether you can open one folder and show support for each answer in under a minute.

For U.S.-connected readers, keep this baseline in view. A U.S. citizen living abroad is still required to pay U.S. taxes on income.

Map filing risk after facts are clear#

Once exposure is mapped, then map filing risk. Do not jump straight to treaties or credits before this step.

If you are dealing with overlapping country claims, treaties may matter, but the exact effect depends on your facts and jurisdictions. If you are already dealing with overlap, use the double taxation guide before improvising.

Researching local laws and keeping logs of your travels is a useful baseline for tracking discipline, especially because state-specific laws can vary significantly.

Proof makes your position usable#

Use one monthly guardrail: review your day log, work-location records, revenue timing, and any continuing home-state ties. If one input is stale, fix it before you start optimizing.

That keeps your filing position defensible and helps you avoid year-end reconstruction. With that base in place, the next step is to separate residence questions from filing questions so you can make decisions from clean facts.

The Mental Model You'll Use All Year: Residency Tax vs Source Tax vs Citizenship Tax (Define the Terms Once)#

For planning, treat different tax hooks as different questions. Separate them once, and you can use the same map all year. Use these three hooks as a recurring check:

Residency taxation applies when a jurisdiction treats you as tax resident under domestic rules. Dual residence is possible, so this is not always a one-country answer.

Source-based taxation applies when income is treated as sourced to a jurisdiction. For employment income, where the work is carried out can be decisive, so work-location evidence matters.

Citizenship- or status-based taxation requires a separate legal check.

Naming the hook changes what you do next. Instead of asking one giant question, break it into the right smaller question for each lane.

| Tax hook | What triggers it | What you do next |

|---|---|---|

| Residency tax | You meet local residence criteria, including possible dual-residence overlap | Identify likely resident jurisdictions and expected filings; check treaty tie-breaker rules if residence conflicts appear |

| Source tax | Income is sourced to a jurisdiction | Separate employment versus independent-service income, and track where work or services occurred |

| Citizenship or status tax | Confirm with the relevant authority | Confirm whether this lane applies before assuming filing obligations |

Run this as a standing monthly check, not a once-a-year exercise. Write one sentence per hook: current status, missing proof, and next action. Short notes are enough, but writing them down keeps subtle travel or work changes from disappearing until filing season.

This model also tells you which records matter most in each lane. Day logs mainly support residence analysis. Work-location notes support source analysis. Status-based lanes, when relevant, need their own jurisdiction-specific evidence set.

A practical benefit is early gap detection. When each document maps to a specific tax question, missing proof can show up earlier instead of the week before filing.

You also see where one record cannot do two jobs. A complete travel log may help residence analysis but still leave source analysis weak if workdays were not tagged by location. The file can look full while still miss the detail that matters.

When residence overlaps across borders, one term comes up often:

Treaty tie-breaker rules are used in double-tax-treaty analysis to resolve residence conflicts. Treat them as a framework, not an automatic answer.

If you see a potential residence or source conflict, capture the fact pattern immediately while memory is fresh: where you were, where work happened, and what type of income was involved. Even when the final conclusion needs advice, early documentation lowers cost and improves accuracy.

When overlap appears, avoid improvisation. Treaty language and the fact pattern both matter, so sequence and context matter. Skip either one, and you can end up with a position that sounds reasonable but is hard to defend.

Now turn that model into an execution step. A short risk screen gives you a defensible status for each jurisdiction and shows where to spend effort first.

Run the 10-Minute Residency & Filing Risk Screen (The Operator Framework That Beats Guessing)#

Use a quick evidence screen to produce a defensible shortlist. Ten minutes will not settle every edge case, and it will not establish legal residency or filing obligations, but it will show where your facts are strong, where they are thin, and where escalation may be worth the cost.

That shift matters because vague concern does not tell you what to do. The screen turns anxiety into triage with working labels: monitor, confirm, and escalate.

The point is not precision theater. The point is to create enough structure that your next decisions rely on current evidence, not memory.

Use the same worksheet each time you rerun it. Consistent inputs make changes visible. If your posture moves from monitor to escalate, you should be able to point to the exact fact that changed.

Treat this as an internal risk screen, not a legal determination. Confirm jurisdiction-specific rules with current official guidance or qualified advice before you file.

Step 1. Choose your "most defensible home base"#

Pick one country you can defend as your strongest ongoing connection. Then write a short statement you can reuse across forms, advisor calls, and your own records.

Good statements are factual. They point to ties you can document, such as housing continuity, core account activity, and where day-to-day life is centered. Weak statements lean on preference language and change every few months.

This is not about picking the country you like most. It is about choosing the country that is easiest to support with documents. If you cannot support the claim quickly, it is not defensible enough yet.

Pressure-test your statement now. Ask: if a reviewer requested proof tomorrow, could you produce it in minutes instead of days? If not, gather the missing records while details are still easy to verify.

Also keep a short list of the documents you would show first. That list can include your strongest housing continuity proof, account activity trail, and day map summary. The goal is not over-collection. It is to avoid hesitation when someone asks how you formed your residence posture.

A stable home-base statement also improves communication. When your explanation stays consistent across advisors, preparers, and forms, you lower the chance of contradictory narratives in your records.

Step 2. Build your day map because this input keeps analysis grounded#

Create a country-by-country log with every entry and exit date for the year. If dates are uncertain, rebuild them now while travel records are still available.

Cross-check dates against official travel records and your own documentation where available. Reconcile border history, tickets, lodging records, and calendar events back to one file.

When a date cannot be confirmed immediately, mark it as unresolved instead of guessing. Then assign a specific follow-up source and close it before month-end. Unresolved days compound quickly and distort later analysis.

Your day map should be your single source of truth. Multiple unofficial versions create mismatches that are hard to unwind later.

If you work while traveling, add workday tagging now instead of later. Different compliance analyses may use overlapping but different facts, and clean tagging helps when you need to escalate.

Step 3. Flag potential dual-residence overlap#

If two jurisdictions appear to have competing residence indicators in your records, treat overlap as possible. Do not wait for filing season to test that assumption.

Mixed facts are common. If evidence points in different directions, do not force certainty. Mark the jurisdiction for confirm or escalate, then strengthen the record before taking a hard position.

A practical discipline is a two-column note: facts supporting each side and facts still missing. If one side is mostly assumptions, do not file a confident narrative yet. Keep the posture at confirm or escalate until your records catch up.

Also note exactly which legal question remains unclear. That keeps escalation focused and reduces advisor time spent re-reading facts you already know.

Step 4. Output your posture without fake precision#

After the screen, assign each jurisdiction one of three labels:

- Monitor: keep records current and recheck monthly.

- Confirm: review local guidance or request targeted filing review.

- Escalate: bring in professional support when overlap or unresolved legal questions appear.

This posture model keeps your response proportional. You avoid overreacting where risk appears low and underreacting where overlap looks material.

It also supports continuity. As travel and contracts change, rerun the same screen and update posture using evidence. You are not starting from zero each quarter.

Keep posture labels time-stamped. A label without a date goes stale quickly, especially when travel plans shift mid-quarter. Date stamps also help advisors see whether they are reviewing current facts or historical ones.

The next shortcut to remove is one-number thinking. Use current records, explicit assumptions, and targeted escalation instead.

Before you move on, turn this risk screen into a monthly operating habit with the tax residency tracker.

The 183-Day Rule Myth Ends Here (And What To Track Instead)#

Treat 183 days as a signal, not a conclusion. In practice, start by defining the exact tax question in each relevant country, then test your facts against that question.

That order matters because the same number can show up in different legal contexts. The exact legal effect is jurisdiction-specific and may stay unclear until reviewed, so a day count on its own is not a complete cross-border answer.

What it actually means#

Day count is useful because it is measurable, so it belongs in your file. But day count alone does not settle your position across cross-border tax questions.

A simple way to work is this: first identify the specific residency exposure question for each country, then match your facts to that question. If you want a deeper myth breakdown, read 183-Day Rule Explained: Stop the Tax Myths Before They Cost You. For overlap handling, see How to Legally Avoid Double Taxation: A Freelancer's Guide to Tax Treaties.

Why it fails in practice#

Most failures start when people stop at the day total. The common mistake is assuming cross-border tax gets simpler, when it usually gets more complex.

You can keep a clean travel log and still miss important cross-border residency exposure questions. Another common failure is category confusion: people hear "183-day rule," treat it as a universal answer, and skip country-by-country review.

If that is your file today, use it as an escalation checkpoint. Speak to a qualified tax specialist in your country of tax residency and in any country where you might unintentionally create one.

What to track instead#

Keep a compact evidence stack that supports a country-by-country review:

| Record | What to include |

|---|---|

| Presence log | Entry and exit dates by country, with retrievable backup |

| Cross-border activity notes | Key facts you may need for specialist review |

| Residency-exposure list | Countries where you may need specialist review |

| Monthly review snapshot | Unresolved dates, open questions, and monitor/confirm/escalate status |

Make the monthly snapshot repeatable. If you could not hand it to an advisor tomorrow without rebuilding the quarter, your records are not ready yet.

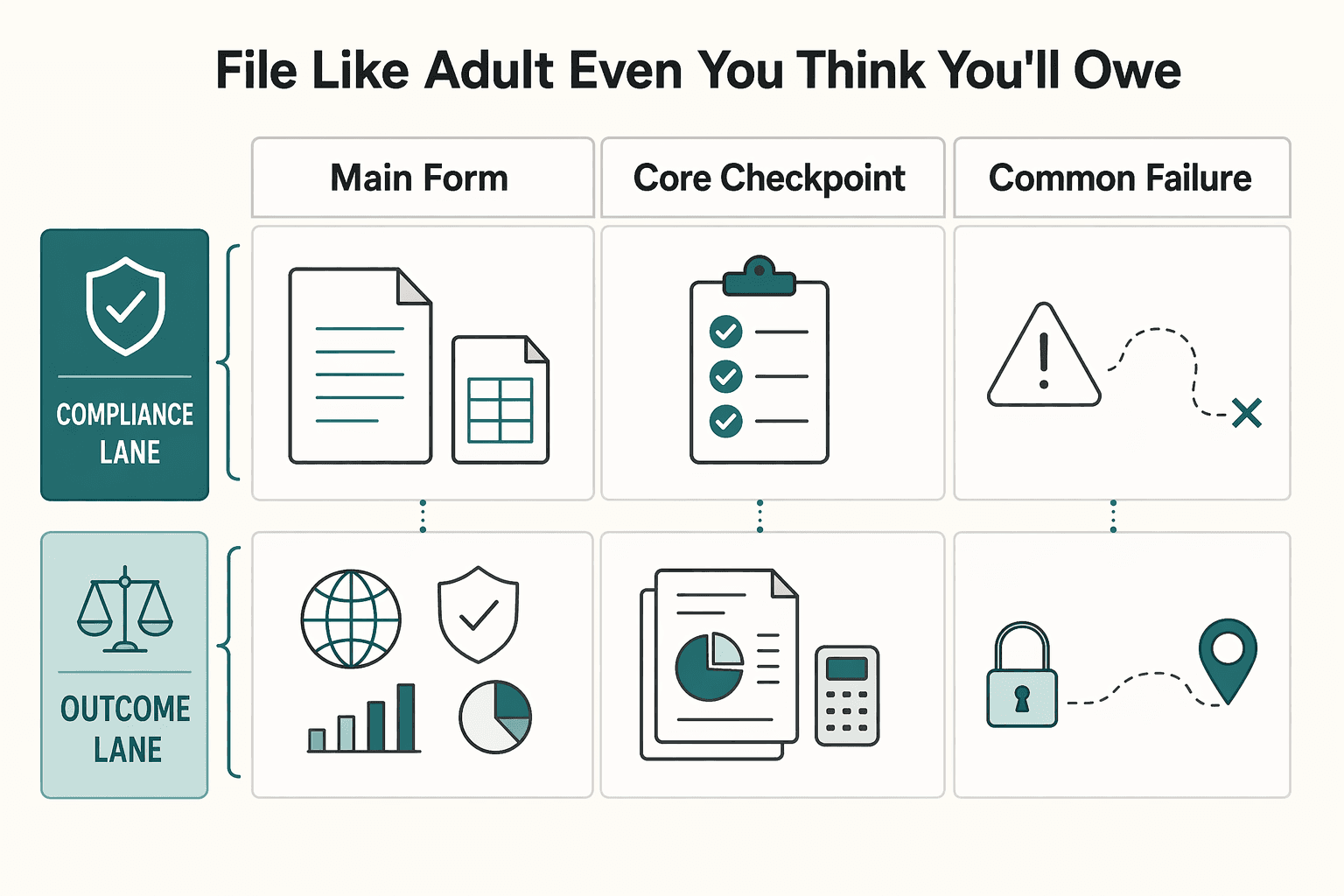

U.S. Nomad Baseline: File Like an Adult (Even If You Think You'll Owe $0)#

For U.S. nomads, filing comes first and tax outcome comes second. Confirm what you must file, assemble the inputs, and only then apply relief tools. U.S. citizens and resident aliens abroad are still taxed on worldwide income, so expecting to owe little or nothing does not remove filing duties.

Keep two lanes separate. The compliance lane is the return and information reporting you may need to file. The outcome lane is what exclusions, credits, or other relief do after the filing facts are established.

If you are deciding between FEIE and FTC, make that decision from your records, not your assumptions. Use this as a quick screen, then go deeper in FEIE vs. FTC: A Strategic Choice for High-Earning US Expats.

| Question | FEIE | FTC |

|---|---|---|

| Main form/workflow | Claimed on your U.S. return after FEIE eligibility checks | Form 1116 |

| Core checkpoint | You must be a qualifying individual with foreign earned income, and your tax home must be in a foreign country | Form 1116 is category-specific |

| Common failure mode | Weak day counting or weak tax-home support | Wrong income-category handling |

FEIE is rules-driven. Under the physical presence test, you need 330 full days during any period of 12 consecutive months, and a full day is 24 consecutive hours beginning and ending at midnight. Missing the count still fails the test, even if the reason is illness, vacation, or employer orders. If you also claim the foreign housing exclusion, compute that first because it limits FEIE capacity.

FTC is process-driven. Form 1116 is category-specific, so use a separate form for each income category, check one category per form, and report amounts in U.S. dollars except where the form says otherwise. In complex cases, category handling discipline matters. That is the overlap flow in How to Legally Avoid Double Taxation: A Freelancer's Guide to Tax Treaties.

Treat self-employment and account reporting as separate controls. Do not assume FEIE or FTC resolves self-employment tax treatment. Verify current rules and form handling before filing. Review account reporting on its own track as well, and verify current filing triggers before you file.

Use this monthly control checklist:

- Update your form-input tracker.

- Refresh your foreign-account inventory, including opens, closes, and balance spikes.

- Maintain an unresolved-items log for tax-home support, FEIE day count, FTC category splits, and foreign-tax payment evidence.

Double-Tax Overlap Playbook: How Treaties, Tie-Breakers, and Credits Help Prevent Double Taxation#

When two tax claims overlap, do not stack relief tools by default. First define the overlap, then choose one primary relief path for that income line, and build the support before filing.

These issues can look similar but require different treatment. A residence conflict, foreign tax paid on income also taxed by the U.S., and FEIE eligibility are not the same problem. If you cannot state the overlap in one sentence with a date range and income line, pause before you file.

Name the overlap before you solve it#

Start with a one-line statement tied to period and income line, for example: "Country A treated me as resident from March through December, and the U.S. also taxed my consulting income for that period."

Then route it: treaty residence question, credit question, FEIE question, or multiple issues handled in sequence. Use a simple control: one overlap, one primary path, then reconcile secondary effects.

When residence conflict points to a treaty tie-breaker#

If both countries treat you as resident, go to the actual treaty text. Treaty tie-breaker details are treaty-specific and are not established in this section. For context before you read treaty language, see How to Legally Avoid Double Taxation: A Freelancer's Guide to Tax Treaties.

Use a compact evidence checklist so the review stays scannable:

- Treaty text: quote or summarize the article language you are applying.

- Supporting facts: facts that point toward one country under that article.

- Contradictory facts: facts that point the other way.

- Proof status: what documentation you have today.

Escalate when facts are mixed. If your facts point in different directions or your proof is thin, treat that as a trigger for professional review before filing.

Match the tool to the job#

Map each income line to the tool doing the work, and keep the paths distinct.

| Primary path | Use when | Must be true first | Does not solve |

|---|---|---|---|

| Treaty position | Residence or taxing-rights conflict under a treaty | You have treaty text and facts that fit the article used | FEIE qualification or tax-paid proof by itself |

| FEIE | Excluding qualifying foreign earned income from U.S. taxation | You are a qualifying individual with foreign earned income, your tax home is in a foreign country, and you meet the relevant test | Treaty residence conflict by itself |

| Foreign tax credit | Potential overlap where foreign tax and U.S. tax both apply to the same income line | Detailed eligibility and computation are not established in this section; confirm separately | Treaty tie-breaker outcomes |

For FEIE, the timing test is strict: 330 full days in a 12 consecutive months period, and a full day is 24 consecutive hours beginning and ending at midnight. If you miss the count, the test is not met. Days in a foreign country while violating U.S. law are not treated as qualifying physical presence.

FEIE also requires that you file a return reporting the income, and your tax home must be in a foreign country. If you claim the housing exclusion, compute housing first because it limits FEIE. For 2026, the FEIE maximum is $132,900 per person; the general housing expense limitation is 30%, or $39,870.

If both exclusion and credit seem potentially relevant to the same income pool, compare deliberately before filing: FEIE vs. FTC: A Strategic Choice for High-Earning US Expats.

Sequence check before filing:

- Assign each income line one primary relief path.

- Check whether that same line appears in a second relief calculation.

- If yes, reconcile the order and logic before filing.

Proof first, then file#

Your overlap position is only as strong as your file. Keep a compact overlap file with these items:

- income-line mapping by period and country

- tax-paid evidence and withholding support tied to those lines

- FEIE support where relevant, including day counts and tax-home support

- a short decision memo explaining why that path was chosen

That structure makes the filing defensible now and easier to support later. Next, turn that into a clean money trail so the agreement, invoice, payment, books, and return stay connected.

The Business-of-One Money Trail: Agreement → Invoice → Payment → FX → Books → Tax Forms (A Practical, Audit-Ready Spine)#

A strong audit defense is a complete chain from economic reality to documented compliance decisions. If one link is missing, review gets slower and your support file gets weaker.

Cross-border digital-nomad work raises questions about applicable employment law, tax jurisdiction, visa requirements, and social security. Contract language alone may not control outcomes, because where work is primarily performed can be a key legal determinant.

Use one repeatable chain for every engagement. It is not a legal checklist, but it can produce clear support:

- Agreement: contract or SOW that specifies approved work locations, tax or social-security obligations, and advance notice requirements for location changes

- Invoice: billed amount, currency, date, and service description

- Payment proof: processor receipt, bank credit, or remittance advice

- Compliance documentation: visas, tax certificates, and location approvals tied to the work period

- Book entry: ledger line tied back to all source records

This chain can solve several problems at once. It can show what was agreed, where work was performed, what was paid, and how the records connect during a compliance review.

When exceptions happen, treat them as first-class records. Credit notes, partial refunds, reversals, and processor adjustments should link to the original invoice and ledger line so the chain still reconciles end to end.

A common failure mode is that agreements and payments exist, but location approvals or tax documentation were never captured. Mistakes here can lead to significant penalties and legal liabilities.

| What you are supporting | Common artifacts to keep |

|---|---|

| Work-location compliance | Agreement terms on approved locations, location-change notices, and location approvals |

| Tax and social-security obligations | Contract obligations plus tax certificates and related records |

| Ongoing audit readiness | Linked agreement, invoice, payment proof, and documented compliance reviews |

Use consistent naming across agreement, invoice, and ledger IDs. Matching IDs can reduce reconciliation errors and make targeted review faster.

In practice, keep one source of truth for each account, set clear communication protocols for location changes, and archive source records in searchable folders. That turns compliance prep into verification, not archaeology.

Another practical gain is continuity across preparers. If your chain is complete, switching advisors is usually easier and less likely to require discovery work from zero.

When the money trail is stable, your broader documentation stack becomes easier to maintain and easier to audit.

The Audit-Ready Nomad Stack: Documentation Kit + Monthly Close (So Tax Season Is Almost a Push-Button Export)#

Tax season gets lighter when evidence is organized by decision type before anyone asks for it. You do not need complicated software. You need consistent categories and a monthly close routine that does not rely on memory.

The goal is simple: each filing question should map to an obvious folder and a clear set of documents. If retrieval is fast, filing risk is easier to manage and advisor time is better spent on technical decisions.

Keep this stack boring by design. Fancy tools are optional. Consistent folder names, month labels, and document IDs do most of the heavy lifting.

Your "Nomad Doc Kit" (what actually matters)#

Do not collect everything. Collect the records that answer recurring tax questions:

- Residency and presence: a day-abroad log plus records that support where you were and when

- Business activity by location: records of strategic decisions, contract signing, and revenue-generating management activity

- Tax exposure notes: advisor notes on where activity may be treated as taxable business presence

- Visa and status records: residency or work authorization documents, with a note that visa status alone does not usually remove business tax exposure

If you are a U.S. taxpayer, keep in mind that U.S. tax still applies to worldwide income.

Consider separating source files from shared files. Keep original statements in restricted storage, and use redacted copies for advisor sharing when possible.

Add a one-page index at the top of the kit with folder names and the question each folder answers. That can save time for you and for any advisor reviewing the file.

Monthly close (the habit that prevents chaos)#

A monthly close can keep small gaps from turning into filing-season blockers. Use a fixed order and do not skip steps. That discipline matters because cross-border mistakes can become structural and hard to unwind, and noncompliance penalties can compound quickly. If taxable presence is asserted, exposure can include corporate income tax, VAT obligations, and payroll withholding requirements.

Run a practical sequence every month:

- Update your day-abroad log and work-location map

- Record where strategic decisions, contract signing, and revenue-generating management happened

- Flag months where activity could be interpreted as taxable business presence

- Capture open compliance questions with an owner, next action, and target date

- Archive the month's key records so retrieval stays fast

If you keep an open-issues log during close, make unresolved items visible with an owner, next action, and target date.

By year-end, this routine should produce a clean evidence stack:

| Stack layer | Output you want at year-end |

|---|---|

| Residency file | Day-abroad log with supporting presence records |

| Business-activity file | Timeline of strategic decisions, signed contracts, and revenue-related management activity by location |

| Tax-exposure file | Notes on possible permanent-establishment exposure and related advisor guidance |

| Risk log | Open questions, decisions, and follow-ups closed or carried forward |

This process can improve advisor efficiency. Instead of spending paid time locating missing records, you can spend more time on technical decisions that may change outcomes.

Run a quick quality check before finalizing the month: pick one meaningful decision and confirm the location record, activity record, and risk notes all line up.

Storage discipline matters too. Use consistent naming, date conventions, and version control for corrected files. When documents need to move quickly, clean naming can save time.

Once this stack is reliable, you can spot potential cross-border traps earlier, often before contract and billing decisions lock in.

The Cross-Border Risk Traps People Skip: PE, VAT, Withholding, and Offshore Structure Noise#

Some of the most expensive mistakes are operational, not technical. They can start when contracts are signed and payments begin flowing before key cross-border checks are done.

Move these checks earlier. When you identify issues up front, you can adjust agreements, pricing, and documentation before they turn into disputes.

Do not rely on the idea that staying under 183 days in one country automatically means you are tax-free. Day-count rules can apply differently and may include multi-year lookbacks, so sub-183 annual presence can still create residency exposure.

These traps look separate, but they often surface in the same records: contracts, invoices, payment details, and work-location history.

Attach a tax-risk note to onboarding so commercial decisions and compliance decisions are made together. Separating them is how preventable exposure gets baked into contracts.

1) Permanent establishment (PE) needs early, jurisdiction-specific review#

Treat PE as jurisdiction- and treaty-specific. Treat it as something to monitor, not something you can close from generic rules alone.

If activity in one market starts to look ongoing, document those facts promptly and request jurisdiction-specific analysis.

Document trigger candidates as they happen, not at year-end. A short monthly PE note can preserve the context for later analysis.

Early analysis matters. PE questions are easier to assess while facts are current than after a full year of mixed activity.

2) VAT and similar consumption taxes need an investigation step#

VAT and similar consumption-tax treatment may vary by jurisdiction, so generic assumptions are risky.

Add a VAT checkpoint to client onboarding and invoicing. Ask early how the transaction should be treated and what documentation is needed. One disciplined check before invoicing is often easier than correcting invoices later.

If your client mix changes, rerun this check. The right treatment for one transaction pattern may not fit another.

Store VAT treatment assumptions next to your invoice templates so billing execution matches the reviewed position.

3) Withholding deserves attention when "net paid" does not match#

Without treaty access, source countries may withhold tax from gross revenue at punitive rates. In practice, mismatches between invoiced gross and paid net should trigger immediate review.

Do not treat net-paid differences as minor bookkeeping noise. Request withholding details, collect the relevant forms, and tie the support to the specific payment line.

Without a formal tax residency certificate, treaty protections may not be available. Also treat missing or invalid tax IDs as an operational risk for payment operations and account continuity.

Treat missing withholding documents as a blocker for close on that payment line. You can still book the cash, but the documentation task should stay open and visible until it is resolved.

This step pays off during year-end analysis. Withholding records linked at payment time are easier to use for credit analysis and easier to explain if questioned.

4) Offshore entities need a written, non-hand-wavy reason#

If the only rationale is to avoid residency everywhere, pause. A legally sound strategy is to deliberately establish tax residency in a jurisdiction that treats foreign-source income favorably.

Require a written rationale tied to commercial and compliance goals before forming any entity. Then map the expected filing impact in plain language. If that map is unclear, you have your answer.

Before formation, write down first-year compliance tasks and who owns each one. If ownership is fuzzy, the structure is probably premature.

The issue is not that entities are always wrong. It is that poorly scoped entities can create ongoing obligations that are costly to unwind.

| Trap | What to watch | Your next action |

|---|---|---|

| PE | Activity in one market that starts to look ongoing, with unclear tax treatment | Log facts and request jurisdiction-specific analysis |

| VAT and similar taxes | Cross-border sales with uncertain treatment | Add a VAT checkpoint to onboarding |

| Withholding | Net payment below gross invoice; missing residency certificate or tax ID | Request withholding detail and required forms |

| Offshore structures | Vague tax-only rationale or "nowhere residency" plan | Define compliance ownership and get qualified advice |

Banks operating under CRS/FATCA are required to identify tax residency, so documentation gaps can become immediate operational problems.

Once these traps are managed, escalation decisions get clearer. The next section covers when to hire help and what to send so paid time goes to strategy, not reconstruction.

When to Talk to a Pro (And the Exact Pack to Hand Them So You Pay for Strategy, Not Archaeology)#

Use professional help where complexity is real: unclear status, uncertain timing, and high-impact filing choices. That is where specialist judgment can reduce risk.

Do not wait for deadlines. Early escalation keeps the focus on analysis instead of reconstructing missing records.

Define the decision you need before booking the call. Clear questions produce strategy. Vague questions produce more fact-gathering.

Book professional help when any trigger is true#

Use these practical triggers:

- You are self-employed abroad and U.S.-connected: if you are a U.S. citizen or resident with self-employment income, U.S. self-employment-tax rules are generally the same whether you live in the U.S. or abroad.

- Your net earnings are at or near the filing trigger: self-employment tax applies when net self-employment earnings are at least $400.

- You are relying on FEIE to remove self-employment tax: claiming the foreign earned income exclusion does not remove self-employment tax on net profit.

- Your residency status changed during the year: income received after becoming a U.S. resident can be subject to self-employment tax.

- You are unsure about form-level reporting: covered self-employment-tax reporting requires Schedule SE (Form 1040) attached to the U.S. return.

- You are in a U.S. territory and assuming income-tax exemption ends the issue: self-employment tax can still apply even when income is exempt from U.S. income tax.

These triggers are not admissions of failure. They are controls that keep technical issues from turning into deadline problems.

If multiple triggers are true, consolidate them into one scoped engagement instead of booking fragmented one-off calls. The facts overlap, and integrated analysis is usually cleaner.

The "Advisor Pack" (send before the first call)#

Quality of handoff drives quality of advice. If you want strategy on the first call, send a clear package before the meeting.

Include these items:

- Timeline of where you lived and when your U.S. residency status changed

- Net self-employment earnings worksheet with gross income, deductions, and net profit

- Draft filing set showing Form 1040 and Schedule SE

- Notes on any FEIE position you are taking

- If applicable, records tied to U.S. territory income treatment

Package files so the naming is self-explanatory and date-sorted. Advisors should be able to see the chronology immediately without decoding custom abbreviations.

| Pack item | What it answers | Why it matters |

|---|---|---|

| Status timeline | Whether and when U.S. residency changed | Timing can change self-employment-tax exposure |

| Net-earnings worksheet | Whether you are at or above $400 | Determines self-employment-tax trigger |

| Draft forms | How self-employment tax is being reported | Catches Schedule SE issues before filing |

| FEIE notes | Whether FEIE is being over-applied | FEIE does not remove self-employment tax |

| Territory records (if applicable) | Whether an income-tax exemption is being misread | Self-employment tax may still apply |

Send this in a structure that is easy to scan. Advisors can give sharper recommendations when the evidence is organized before the call.

A clean pack also helps you compare advice across firms. When each advisor sees the same facts, differences in recommendations are easier to evaluate.

Confirm safely (without outsourcing your brain)#

Even with strong professional support, keep the decision logic explicit. Ask each recommendation to state:

- The U.S. self-employment-tax rule being applied

- The status assumption being used, such as U.S. citizen or resident versus neither

- Form-level impact, such as Form 1040 and Schedule SE

Then request a one-page filings list plus assumptions. Keep that summary with your records and reconcile it against your document kit before filing.

Ask for explicit alternative paths when assumptions change, not just one recommended answer. Contingency guidance makes next-year updates faster and reduces dependency on memory.

That protects continuity. If your status or income mix changes next year, you can update assumptions instead of rebuilding the logic from scratch.

Good advisory relationships still require owner oversight. Your job is to keep the facts clean, assumptions visible, and filing decisions traceable.

Your Safe-Default Nomad Tax Plan for 2026 (Use This Checklist, Then Automate the Routine)#

Run a conservative monthly routine, not year-end guesswork. Re-screen when facts change, document while events are fresh, reconcile on schedule, and escalate before filing when your story is no longer simple.

The core solution#

Set one owner, usually you, for a 20-minute month-end review with four checks: where you were, where you worked, what got paid, and whether your filing posture changed.

If you are a U.S. citizen or resident alien living abroad and expect to claim the foreign earned income exclusion, verify eligibility against records, not memory. You are generally taxed on worldwide income, and claiming FEIE still requires filing a U.S. tax return that reports the income. Foreign-earned income is pay for personal services. Your tax home must be in a foreign country, and the physical presence test requires 330 full days in a 12 consecutive months window, with each countable day a full midnight-to-midnight day abroad. If you do not reach 330 full days, you do not meet that test. Use the IRS Interactive Tax Assistant as a first-pass eligibility check before finalizing positions.

Quick checklist#

- Re-screen monthly: update your day log and re-check FEIE posture whenever your country mix changes. If you still treat simple day-count shortcuts like a force field, reset with 183-Day Rule Explained.

- Document weekly: save passport stamps, flight confirmations, lodging records, calendar entries, contracts, invoices, payment proof, FX support, and foreign tax documents in one dated folder.

- Reconcile monthly: match each payment through agreement → invoice → payment proof → FX support → books. Fix mismatches before the next month closes.

- Verify U.S. filing posture quarterly: review whether your U.S. return and FEIE position still match your records. For threshold-based filings, verify the current filing triggers before you file.

- Escalate early: bring in help when FEIE versus credit choice is unclear, see FEIE vs. FTC, or when part-year qualification means the exclusion must be adjusted by qualifying days. If you are using a housing exclusion route, figure that first because FEIE is reduced by that amount.

Final operator move: when you hand off to an advisor, send a complete pack: day-by-country log, workday tagging, income trail, prior-year return, foreign tax records, account list, and a one-page change memo. Ask for three outputs: a filing list, a position memo with explicit assumptions, and a missing-records list. Save that memo in next year's folder, and carry those assumptions into day-one tracking for continuity.

If you want to implement this routine in a system with compliance gates, audit-ready records, and payout flows where enabled, start with the Gruv docs.

Frequently Asked Questions

Do digital nomads pay taxes?

Often, yes, but outcomes are fact-specific. If you are U.S.-connected, U.S. filing obligations can still apply, so keep a day-by-country log and a clear income trail.

Where do I pay taxes as a digital nomad?

It can be fact-specific and may involve more than one jurisdiction. If you are a U.S. citizen or resident alien, U.S. worldwide-income taxation can apply. FEIE applies only if you are a qualifying individual with foreign earned income, your tax home is in a foreign country, and you file a return reporting that income. See this guide and this guide.

If I don't stay 183 days anywhere, do I owe tax anywhere?

Possibly. This section does not establish a universal 183-day rule. For U.S.-connected FEIE physical-presence analysis, counted days are full 24-hour days (midnight to midnight), and the threshold is 330 full days in a 12-month period. See 183-Day Rule Explained. For mixed-fact cases, use a qualified cross-border tax professional.

Do U.S. digital nomads have to file U.S. taxes?

Many do. U.S. citizens and resident aliens abroad are generally taxed on worldwide income. FEIE applies only if you are a qualifying individual with foreign earned income, a foreign tax home, and a filed return reporting that income. If you are using the physical presence test, keep proof for 330 full days in a 12-month period, with each counted day documented as a full midnight-to-midnight day abroad. The 330 days do not have to be consecutive.

Do digital nomads pay self-employment tax?

Treat self-employment tax as a separate U.S.-connected filing question and confirm the result with a qualified cross-border tax professional.

What records should digital nomads keep for taxes?

Keep proof of presence days and income. A practical baseline is passport and travel logs, calendars that show full days by country, contracts, invoices, and payment records. The key is a defensible timeline that matches where you were to when income was earned and reported.

Can I use an offshore company to avoid taxes?

Not as a blanket answer from this section. Entity structures are mixed-fact cases, and FEIE eligibility still depends on qualifying status, foreign earned income, foreign tax home, and filing a return reporting that income. Keep incorporation documents, service agreements, and evidence of where work was performed, and escalate to a qualified cross-border tax professional.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- esd.ny.gov/sites/default/files/news-articles/Item%20V.%...trusted

- ilga.gov/ftp/legislation/103/HB/10300HB4304.htmtrusted

- irs.gov/individuals/international-taxpayers/self-emp...trusted

- irs.gov/individuals/international-taxpayers/frequent...trusted

- sec.gov/Archives/edgar/data/1756607/0001628280250136...trusted

- sou.edu/olli/wp-content/uploads/sites/37/2026/02/OLL...trusted

- arxiv.org/html/2603.25100v1external

- cambridge.org/core/journals/perspectives-on-politics/artic...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

FEIE vs Foreign Tax Credit for High-Earning US Expats

Start with compliance, then optimize tax. If you are a globally mobile freelancer or consultant filing `Form 1040`, first confirm what you can actually claim and support, then compare the tax result.

How Freelancers Can Legally Avoid Double Taxation With Tax Treaties

Classify the tax problem before you touch a return. If your income is mostly personal service fees across borders, this guide fits. If your issue is C corporation profits and shareholder dividends, you are solving a different problem.