Quick Answer

Start by classifying status as Domestic Tax Subject (SPDN) or Foreign Tax Subject (WPLN), then sort each income line by where the work was actually done. For indonesia tax for foreigners, that status-and-source call drives whether you test PPh 21 or PPh 26 treatment and what filing path to prepare. Keep contracts, invoices, payment confirmations, and NPWP details in one working file before modeling rates or relying on treaty relief.

Why this guide exists for foreign freelancers in Indonesia#

If you are trying to make sense of indonesia tax for foreigners, this guide gives you a practical way to assess your likely tax position. It also helps you organize records in a way that reduces avoidable compliance stress.

This is written for the business-of-one reality in Bali and wider Indonesia, not corporate structuring. Bali is a major expat hub, but the framework here is meant for freelancers and consultants working across Indonesia. Use this guide in this order:

- Decide your status from facts you can document.

- Review each income stream before assuming rates.

- Gather the records you will need to support your position.

- Escalate when one fact pattern could support more than one reasonable answer.

That order matters. Cross-border payments can involve withholding taxes and foreign exchange rules, and contractor payments are often handled in Indonesian rupiah (IDR). How money moved and what records you kept can affect compliance decisions.

Your first checkpoint is evidence, not opinion. Keep contracts, invoices, payment confirmations, and tax identification details together from the start. If you work across Indonesia, keep dates and locations consistent, since operations can span three time zones: WIB, WITA, and WIT.

Treat unclear residency facts, cross-border withholding uncertainty, or conflicting records as escalation triggers. When facts are mixed, take a conservative position and get expert support instead of forcing a confident answer. For location context, see Canggu, Bali, Indonesia: The Ultimate Digital Nomad Guide (2025).

Start with the terms that control everything#

These labels determine which path you test first and which documents you prepare. Use the table below as your first sort.

| Term | Plain-English meaning | Why it matters to you |

|---|---|---|

| Domestic Tax Subject (SPDN) | In the cited secondary guidance, a foreigner whose stay exceeds the stated period is treated as a tax resident. | This status can change the tax treatment you need to analyze. |

| Foreign Tax Subject / Non-Resident Taxpayer (WPLN) | A foreign tax subject receiving Indonesian-source income. | This label appears in treaty and withholding discussions. |

| Indonesian Income Tax Law | The legal framework referenced in Indonesian income-tax guidance. | It is a baseline reference when reviewing residency, withholding, and filing obligations. |

| PPh 21 and PPh 26 | Income tax article references listed in withholding-tax coverage. | These article numbers appear in withholding discussions, including payroll and non-resident contexts. |

The SPDN versus WPLN split is also a practical treaty checkpoint. One explicit treaty-benefit condition is that the income recipient is not an Indonesian resident tax subject, and treaty procedures are set out in DGT Regulation PER-25/PJ/2018. For treaty-benefit claims, WPLN is required to submit SKD WPLN to the tax withholder or collector, with a formal receipt process and information transmission to the tax authority.

On administration, your NPWP number is your taxpayer ID issued by the Directorate General of Taxes (DGT/DJP). In the cited material, not having NPWP is described as triggering a 20% increase under Article 21.

For annual return labels, Form 1770 is described for business or independent-work income. Form 1770S is described for individuals with income from one or more employers, plus certain other income categories. Before filing, classify your income as independent work, employer income, or mixed. We covered this in detail in Malaysia Tax for Expats Who Need a Defensible Filing Path.

Decide your residency status before you calculate any tax#

Decide your status first. Classify as Domestic Tax Subject or Foreign Tax Subject before you calculate anything. That keeps the rest of your compliance path consistent and easier to defend.

Use a decision sequence#

Start with day-count facts from your own records. Build a dated timeline from your travel and presence records. Do not guess from memory. Then review any other residency-related facts in your file. The excerpts used here do not set out a detailed legal test, so treat this as a risk checkpoint, especially if your circumstances changed during the year.

Then classify. If your facts are mixed or changed mid-year, use a conservative classification, document why, and only optimize after that.

In December 2025, DJP issued PER-23/PJ/2025. It replaced PER-43/PJ/2011 and PER-02/PJ/2009, with guidance described as aligned with the Income Tax Law, Job Creation Law, and PMK-18/2021. If your notes still rely on PER-43/PJ/2011 alone, treat them as legacy and re-check.

Compare the two lanes before modeling outcomes#

| Classification lane | Status signals to review | Likely treatment direction | Proof points to keep in file |

|---|---|---|---|

| Domestic Tax Subject | Your fact pattern supports domestic treatment over foreign treatment | Continue with resident-style analysis in later steps | Dated timeline and supporting records, plus a short memo explaining why your facts fit current guidance |

| Foreign Tax Subject | Your fact pattern supports foreign treatment over domestic treatment | Continue with non-resident-style analysis in later steps | Dated timeline and supporting records, plus a memo explaining why domestic treatment was not selected |

| Mixed or changing facts | Mid-year changes, inconsistent records, or facts that support either lane | Use conservative handling until reviewed | Change timeline, reconciliation notes, and a marker that PER-43/PJ/2011 is legacy because it was replaced |

Verification checkpoints before you rely on your classification#

Before you rely on a residency conclusion, make sure your file can tell the story without gaps:

- Timeline records: confirm dates and fix gaps before filing.

- Supporting documents: keep copies that support your timeline.

- Status memo: write a short note with the facts reviewed, the classification chosen, and any unresolved points.

- Legacy cleanup: update older notes that cite PER-43/PJ/2011 without the newer framework.

If your file cannot tell a clean residency story, pause and get case-specific review before you optimize tax outcomes. You might also find Understanding Vietnamese Taxes for Foreigners useful. If your day-count or timeline is messy, run your dates through the Tax Residency Tracker before you lock your status memo.

Classify each income stream before applying rates#

Classify each income stream before you model rates. For a Domestic Tax Subject (SPDN), income is generally assessed on a worldwide basis. For a Foreign Tax Subject, Indonesian-source exposure is the main trigger for Withholding Tax (WHT) and PPh 26 treatment. For some qualifying foreign tax residents, territorial treatment may apply for the first four years, but that treatment is conditional and not automatic.

Offshore payment does not automatically mean foreign source. Indonesian-sourced income can include income paid offshore, so payment origin alone is not a reliable test.

Use three working buckets#

Use these three buckets to sort risk before you get into rates:

- Indonesia-sourced client work

Work facts point to Indonesia activity, so Indonesian-source exposure is the conservative working assumption.

- Offshore-paid work tied to Indonesia activity

Payment comes from outside Indonesia, but services are performed in Indonesia or tied to Indonesia work.

- Clearly foreign-sourced work

Contract scope, work performance, and commercial facts all point outside Indonesia.

These buckets are a practical sorting tool, not a legal formula. The available guidance here does not provide a precise weighting test for payer location, work location, and contract language.

| Income stream pattern | Payer location | Work location | Contract language | Likely treatment under WHT and DTAs |

|---|---|---|---|---|

| Indonesia-facing engagement | Indonesia | In Indonesia | Refers to services or deliverables in Indonesia | Stronger Indonesian-source signal. For a Foreign Tax Subject, WHT exposure is more likely and can fall in the PPh 26 lane at 20% of gross, with possible DTA concessions where available. |

| Offshore payer, Indonesia performance | Outside Indonesia | In Indonesia | Mixed wording or silent on place of performance | Do not assume foreign source from offshore payment alone. Indonesian-source exposure may still apply, and treaty review may matter. |

| Offshore client, offshore performance | Outside Indonesia | Outside Indonesia | Clearly non-Indonesia scope and performance | Cleaner foreign-source pattern on these facts. For SPDN, worldwide-income treatment can still remain relevant. |

If contract and payment flow conflict, prioritize evidence#

When records conflict, lean on written facts you can defend. Start with what work was done and where, then match that to contract terms, invoices, and payment records.

Keep contracts or agreements showing work or business activity in Indonesia for more than 183 days in your file. Those documents matter for both status and downstream tax positioning.

Build a simple source memo before rates#

For each recurring client, keep a short memo with:

- payer entity and country

- where services were physically performed

- contract wording on scope, territory, and performance

- invoice references and payment dates

- payment records tied to invoices

- any withholding documents received

If a third party cannot trace contract -> delivery -> invoice -> payment, your classification is probably still too weak. Related reading: Taxes in Colombia for Foreigners and Remote Workers.

Choose the correct tax path for your status#

Once your income streams are classified, choose your tax path based on status first, then source facts, then article treatment. Treat that as a decision framework, not an automatic rule.

Map status to a likely path#

For a nonresident position, the core question is usually how Indonesia-source income is captured and reported, including withholding where relevant. For an SPDN position, the analysis is usually broader than isolated withholding events and includes annual return treatment.

That distinction matters because Pajak Penghasilan (PPh) is described as self-assessed, so you are responsible for accurate calculation, payment, and reporting. If status and source are misclassified early, the error can flow into withholding assumptions and your annual filing position.

Where treaty relief can change the outcome#

Treaty relief can change the outcome, but only after you confirm that a treaty is relevant to your facts. If you are relying on a DTA, review the primary treaty text directly.

For U.S. taxpayers, use the U.S.-Indonesia Income Tax Convention as the base document. It includes Article 4 (Fiscal Residence), Article 23 (Relief from Double Taxation), and a saving clause in Article 28, paragraph 3. That structure is a useful warning. Treaty benefits may exist, but so do limits and conditions.

The tradeoff is simple. A treaty position may reduce tax exposure, but it can also increase your documentation burden and review risk when the facts are weak or inconsistent.

Keep three short working papers before filing#

Before you file, keep three short internal support notes:

| Working paper | What to include |

|---|---|

| Status memo | Your residence conclusion, supporting facts, and any unresolved ambiguity |

| Income-source memo | Contract and work facts, payer details, invoice and payment trail, and any withholding documents |

| Treaty position memo | The DTA article or articles you rely on, why they apply, and any limits or uncertainty |

If one memo is weak, pause before filing. One provided annual-reporting source says returns are typically due by the end of March every year, and weak execution can lead to penalties and fines. For a step-by-step walkthrough, see Japan Tax for Foreigners Who Work Across Borders.

Understand resident tax mechanics without guesswork#

Do not jump into resident-tax math until status and source are locked. A recurring pitfall in cross-border planning is optimizing a calculation before the legal path is settled, then facing unexpected extra costs and taxes later.

Keep this part practical and high-level. Indonesia-specific bracket, PTKP, or PPh 21 calculation mechanics are not established here, so treat detailed table inputs and labels as a second step after your classification file is coherent. If your facts are mixed or incomplete, fix that first.

| Gather before calculating | Why it matters | What to verify |

|---|---|---|

| Resident-path support | Confirms you should use a resident-style calculation at all | A clear status memo and matching supporting records |

| Annual gross income in IDR | Prevents estimate-driven math | Contracts, invoices, receipts, and conversion method used |

| Personal facts behind any allowance inputs | Prevents unsupported assumptions in the model | Evidence for each personal fact you apply |

| Any adjustment items you plan to include (if applicable) | Reduces mismatch risk between draft math and defensible reporting | Records and a short rationale for each item |

| Withholding already applied | Avoids double counting | Payer documents matched to your own payment records |

Build from documents outward, not from a spreadsheet inward. Confirm annual gross, attach support, then layer in only the inputs you can prove. If any key item is unresolved, mark it unresolved and hold off on bracket optimization until the file is defensible. This pairs well with our guide on Thailand Tax for Digital Nomads Without Residency Mistakes.

Treat the four-year foreigner rule as conditional, not automatic#

Treat the four-year foreigner rule as a conditional exception, not a default. Indonesia's general resident position is worldwide taxation, so this path only works if you clearly qualify.

| Checkpoint | What to document |

|---|---|

| Resident status | Confirm you are actually a resident, for example more than 183 days in any 12-month period |

| Resident start date | Document your resident start date so the four-year window is clear |

| Income separation | Separate Indonesian-sourced and foreign-sourced income with supporting records |

| Skill condition | Document why you believe the skill condition is met |

| Filing checkpoints | Track filing checkpoints, including monthly payment and lodgement deadlines on the 15th and 20th of the following month |

| Unclear items | If any item is unclear, treat the position as unconfirmed |

A limited-period treatment exists under Indonesian income tax rules. Some qualifying foreign tax residents can be taxed only on Indonesian-sourced income for the first four years after becoming tax residents. The qualifier is the key risk point. A "certain skills" condition is confirmed, but a complete official checklist is not established here, so do not self-claim this from summaries, forums, or payroll assumptions. Use the checklist above before you file.

Also flag treaty overlap early. The supported guidance says this territorial treatment may not apply when overseas income is received and an applicable tax treaty is used. A combined position should be reviewed before filing.

When to escalate#

If this rule materially changes your tax outcome, escalate to a licensed advisor before submission. Prioritize review when you have offshore income, mixed-source work, or earlier filings already on record. Returns can be audited, including within a 5-year statute of limitations, so your support file should be built to survive review. Need the full breakdown? Read Taiwan Tax for Foreign Professionals With a Defensible Filing Path.

Build a monthly evidence pack that survives scrutiny#

Build your evidence pack monthly, not at year end. Residency and source positions are facts-and-circumstances calls, so the strength of your filing usually depends on whether your records clearly connect work performed, payment flow, and return treatment.

Authorities may not confirm your status in advance, so document first and decide from evidence. Keep one monthly file that lets someone trace each item from contract to cash to draft return support.

What to keep each month#

| Artifact | What it supports | Monthly control |

|---|---|---|

| Signed contract or statement of work | Client identity, scope, service period, billing terms | Match client name and scope to the related invoice |

| Invoice | Amount billed, period, currency, reference | Keep numbering consistent and avoid duplicates |

| Payment confirmation | Date paid, method, payer reference | Save remittance or receipt when payment lands |

| Bank or payout record | Amount received and payout path | Mark the matching deposit and note fees or deductions |

| Residency-day log | Where you were physically present while work was performed | Update from travel records and work calendar |

| Source-allocation workpaper | How income was allocated by work location | Recalculate monthly and keep the method in the file |

Your day log is one of the strongest controls in the file. When source treatment depends on where work was physically performed, a dated monthly log is much stronger than a reconstruction at filing time.

Tie records to your draft filing position#

As you build the file, tie each record to the return path you expect to take. Start by classifying each period as resident, nonresident, or part-year resident, then document the source-allocation method used. In the California guidance excerpts, this can include a workday ratio approach and Form 540NR controls, including split-income and common-mistake checks.

This guidance draws on California and New York agency material, so treat Indonesia-specific forms, thresholds, and filing positions as unconfirmed in this workflow.

For each income line, note:

- status assumption used for the period

- source classification used

- allocation method used

- supporting files that back the decision

Keep one reconciliation sheet#

Keep one sheet with one row per invoice, mapping classification, treatment, and proof retained. Include:

- invoice number and date

- client name

- service period

- work location, meaning where services were performed

- payer location

- amount billed and received

- payment or bank reference

- source classification

- treatment note and form-control reference

- support file reference

If an invoice does not tie to both payment confirmation and a receipt record, flag it immediately.

Use exports and audit trails without oversharing#

Where supported, platform exports and audit trails can help preserve payout traces and reconciliation evidence. If you use Gruv, export payout history, payment references, and audit-trail records so you can trace billed work through settlement to final receipt.

Keep only what you need to prove timing, amount, counterparty reference, and payout path. Minimize unnecessary personal data so the evidence pack stays defensible and privacy-aware.

Follow a filing sequence that reduces errors#

The cleanest filing is usually the one where key positions are settled before the return starts. As a conservative workflow, confirm status, then source labels, then whether any treaty position is supportable, and only then prepare the return package.

That order helps prevent one bad assumption from flowing through the whole filing. Classification errors can be costly. One Indonesia case showed tax was understated by almost half when resident rates were applied to a non-resident foreign employee. Different facts, same risk. If status is wrong at the top, the numbers below it can be wrong too.

Use this working order#

- Confirm your status for the relevant period from your records.

- Confirm source labels for each income stream using your underlying records.

- Confirm whether your treaty position is supportable, or use domestic treatment.

- Prepare return support for the filing path you expect to use.

Keep filing artifacts aligned#

Treat your annual filing as one connected record set under the Annual Income Tax Return (SPT) and the Directorate General of Taxes (DGT) review context. Keep one folder with:

- draft return package

- reconciliation sheet

- contracts and invoices mapped to each income line

- payment confirmations and bank records

- status and source notes for judgment calls

- consistent NPWP details across documents

This matters if figures are later corrected. The return amount can differ from DGT's calculation and appear in a Tax Assessment Letter (SKP), so each number should be traceable without rebuilding the file from scratch.

Run one pre-file consistency check#

Before submission, do one line-by-line review:

- return totals versus reconciliation sheet

- reconciliation sheet versus contracts, invoices, and payment evidence

- names, dates, currency handling, and duplicate income checks

- NPWP consistency where it appears

Then reverse-test a few items: bank payment -> invoice -> contract -> return line. If the trace breaks, fix classification or completeness before filing.

If a key document is missing, file conservatively and document a correction plan instead of forcing an aggressive position. If your calendar uses a March 31 personal return deadline, do this review early enough to fix gaps instead of patching them at the last minute.

Avoid the mistakes that create expensive cleanup#

Expensive cleanup usually starts when your records tell different stories across status, treaty position, and withholding treatment.

Do not switch status logic midstream and leave old records untouched#

If your status view changes for part of the year, revisit the full affected period, not just current entries. A mixed file where early records follow one logic and later records follow another is hard to defend unless you clearly document why the treatment changed and what you rechecked.

Update related records in one pass: status notes, source labels, reconciliation sheet, and draft return support. If you revise the conclusion but leave contracts, payment records, or return lines on the old logic, cleanup risk rises quickly.

Treaty claims need article support, not just a good outcome#

Treaty relief is not automatic, so do not rely on memory or summary tables. If you use a Double Taxation Agreement, including the US-Indonesia income tax convention, verify your position against the full treaty PDFs and keep those references in your file.

For US-Indonesia positions, anchor your reasoning to the treaty text headings you rely on: Article 4 (Fiscal Residence), Article 7 (Source of Income), and Article 23 (Relief from Double Taxation). Keep in mind the treaty materials also reference a saving clause in Article 28, paragraph 3, and the IRS treaty page includes a Technical Explanation PDF.

The practical test is simple: for each treaty-based line, you should be able to show the article used, the supporting facts, and the matching document trail. If you cannot, use domestic treatment or get professional advice before filing.

Keep PPh 21, PPh 26, and WHT contexts separate in your records#

Do not assume one withholding label fits every payment. If your file includes PPh 21, PPh 26, or Withholding Tax (WHT) contexts, track them separately so treatment stays consistent by line item.

In your evidence pack, map each payment to its source label and tax context. Using one shorthand label across different contexts creates avoidable ambiguity during review.

Admin mistakes still cause real cleanup#

Admin consistency still matters. Keep taxpayer identifiers consistent everywhere and make sure the draft return matches the underlying evidence pack. If you find mismatches, fix them in this order:

- Correct the reconciliation sheet.

- Update the supporting-document index and notes.

- Update the draft return to match those records.

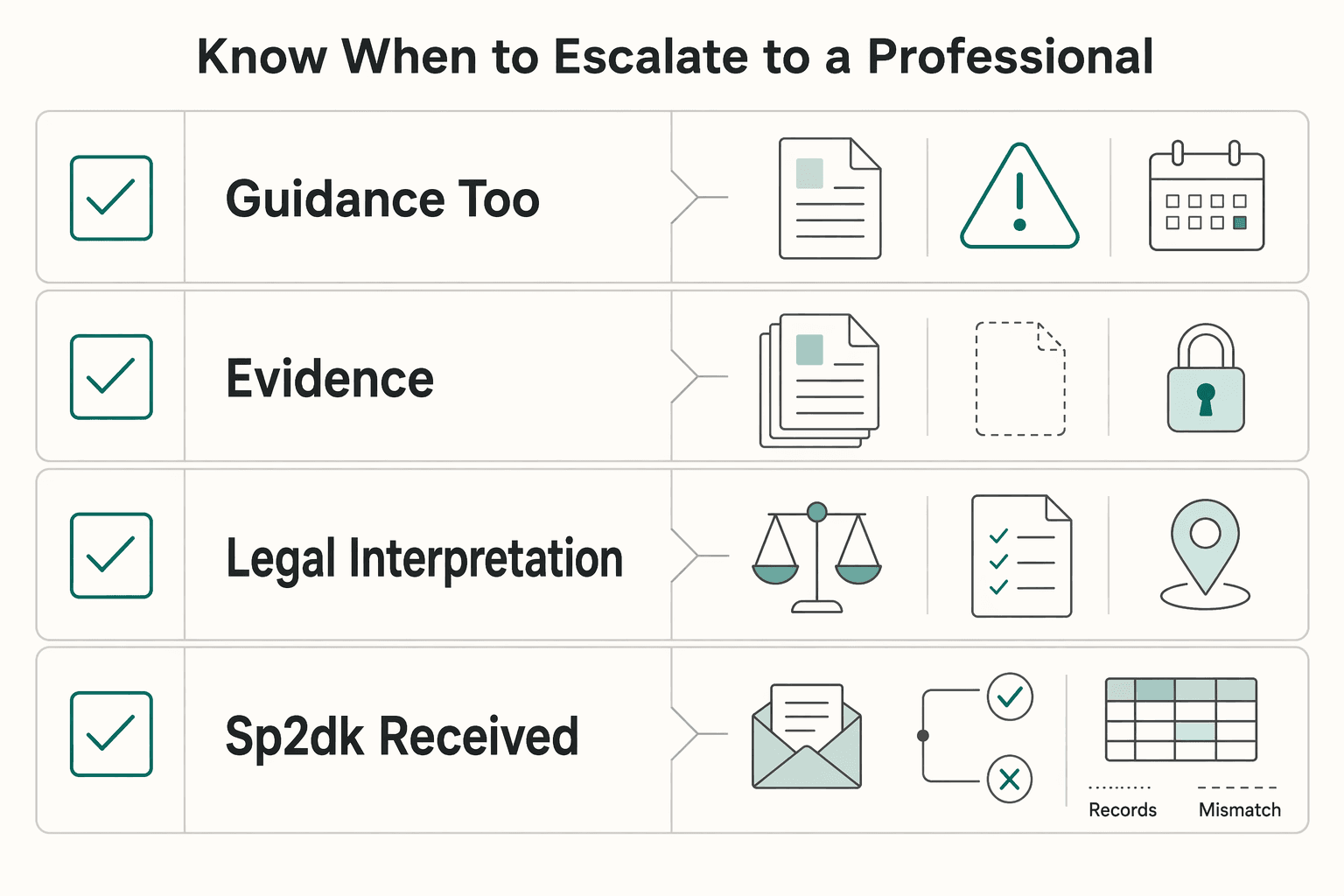

Know when to escalate to a professional#

Escalate early when the filing outcome is sensitive and your evidence is not strong enough to defend your position. Use these as hard triggers:

| Escalation trigger | What the article says |

|---|---|

| Guidance is too general or dated | Use this when available guidance is too general or dated for your specific facts |

| No complete evidence pack | Escalate if you cannot produce a complete evidence pack for your filing position and return support |

| Legal interpretation drives the result | Escalate if your position depends on legal interpretation you cannot clearly tie to your facts and records |

| SP2DK received | Treat this as immediate escalation; the cited practice source says a written response is due within 14 working days |

This is a prudent default, not over-caution. The Deloitte Indonesia tax guide states it is general information only. It advises consulting a qualified professional adviser for decisions affecting finances or business, and it is stated as available only as at 30 June 2023.

If you receive an SP2DK, treat that as immediate escalation. An SP2DK is a formal request for clarification, not a tax penalty, but it is serious. The cited practice source says a written response is due within 14 working days. The DGT may issue it when reported tax data appears irregular, incomplete, or inconsistent. A well-prepared response can close the matter quickly, while ignoring or mishandling it can increase the risk of a longer audit path and possible financial penalties.

Take the low-stress path and document every decision#

The lowest-stress path is simple: confirm your status first, map income sources second, choose your filing path third, and keep the records that support each step. Most problems start when your facts, your forms, and your supporting documents do not match.

If your contracts, payment trail, and filing support do not point to the same story, the stress shows up later. Keep one consistent position and document it clearly.

What to do this week#

- Finalize a one-page status memo.

Write the facts you are relying on, where and when you worked, and the position you are taking. If facts changed during the year, say so directly and explain your decision.

- Build one evidence pack for the year.

Keep contracts, invoices, payment confirmations, bank records, your NPWP record, and other filing documents in one place. Add a simple sheet that maps each invoice to payer so inconsistencies are visible before filing.

- Pre-check filing documents before submission.

Indonesia describes filing the Annual Income Tax Return (SPT Tahunan) every year, and Form 1770 is used by individuals to report personal income. Before filing, align your return with withholding receipts, financial statements if you run a business, and proof of tax payments made during the year.

The paperwork that matters most#

Treat your filing pack as an evidence file, not just a form exercise. Proof of filing can be needed for administrative steps like visa processes or financial services, and weak documentation can create delays or rejection risk. The common failure mode is simple: late filing, late payment, or missing support. Late submissions or payments can result in fines.

Use the defensible option when the stakes are real#

When a rule is unclear or the outcome is sensitive, do not force certainty you cannot support. Choose the position you can defend with documents, then get licensed professional review before submission.

If you want a deeper dive, read Indonesia's B211A Visa: The De Facto Nomad Visa for Bali. If your status, tax position, or filing sequence still conflicts after this checklist, use Contact Gruv to confirm the right next step for your workflow.

Frequently Asked Questions

Do foreigners always pay the same Indonesian tax rate?

No. The rate can change based on your tax treatment, income type, and whether withholding or a treaty position applies. A non-government advisory source also lists Article 21 brackets of 5%, 15%, 25%, and 30%, so a single flat-rate assumption is not reliable.

Is the day-count test based only on consecutive days?

Do not assume that. The exact residency threshold, and whether only consecutive days count, is not settled here. If your status depends on time in Indonesia, verify it against your official travel and permit records before filing.

What changes when I am treated as a Domestic Tax Subject instead of a Foreign Tax Subject?

Your filing approach and tax treatment may change, so confirm status before calculating liability. Keep your status analysis, income-source support, and withholding records aligned to the same position.

Can a tax treaty reduce my Indonesian withholding exposure?

Potentially, yes, but not automatically. The US-Indonesia treaty includes Article 4 (Fiscal Residence) and Article 23 (Relief from Double Taxation), confirming treaty relief as a legal path, but do not assume a specific reduced withholding rate applies. If you plan to claim treaty relief, keep residence evidence and a written position memo, and review How to Legally Avoid Double Taxation: A Freelancer's Guide to Tax Treaties.

Does Indonesia apply local individual income taxes in addition to national rules?

Treat this as a verification item, not an assumption. Confirm whether any local charge applies to your facts before finalizing your filing plan.

Can some foreign residents be taxed only on Indonesian-sourced income for a limited period?

Possibly, but treat it as conditional, not automatic. Eligibility, duration, and self-claim mechanics for any limited-period foreigner regime are not clearly settled. If this position would materially change what you owe, escalate for professional review before filing.

Which forms and records should I prepare first to avoid filing mistakes?

Start with your NPWP and gather the primary forms listed in the provided expat guide: Form 1770 and Form 1770S. Build one working file with contracts, invoices, payment records, bank records, a residency-day log, and your status and treaty notes. If you expect B2B input VAT claims, your NPWP must be recorded on the invoice. If an offshore company is appointed as a VAT Collector, it must submit quarterly reports, and DGT may request a yearly report to validate input VAT credit claims. The same guide excerpt lists the tax year as January 1-December 31 with an individual deadline of March 31.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/104/plaws/publ208/PLAW-104publ208.pdftrusted

- cu.edu/doc/tax-reference-international-visitorspdftrusted

- downloads.regulations.gov/USTR-2025-0016-0161/attachment_1.pdftrusted

- ecfr.gov/current/title-19/chapter-I/part-10trusted

- ftb.ca.gov/file/personal/residency-status/part-year-and...trusted

- ftb.ca.gov/file/personal/residency-status/index.htmltrusted

- govinfo.gov/content/pkg/CHRG-106hhrg60332/html/CHRG-106h...trusted

- govinfo.gov/content/pkg/PLAW-111publ8/html/PLAW-111publ8...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Indonesia B211A Visa for Bali Remote Professionals in 2026

Get the route right before you book anything expensive. Your entry path sets the document load, sponsor coordination, extension pressure, and how much timing risk you carry into the move.

Canggu Digital Nomad Guide 2026 for a Smooth First Month

If you came here looking for a Canggu digital nomad guide, use this as a relocation plan rather than a cafe roundup. The goal is a clean move to Canggu, Bali, Indonesia, with fewer avoidable resets in month one. That only happens if you make decisions in the order they depend on each other, so visas, housing, and work continuity stay aligned instead of colliding later.

How Freelancers Can Legally Avoid Double Taxation With Tax Treaties

Classify the tax problem before you touch a return. If your income is mostly personal service fees across borders, this guide fits. If your issue is C corporation profits and shareholder dividends, you are solving a different problem.