Quick Answer

Start by mapping one real transaction from requisition through Purchase Order (PO), invoice handling, and final settlement, then assign named owners at each handoff. For supply chain platforms pay logistics providers po to settlement, the minimum viable design is clear release gates, exception ownership in AP and freight audit queues, and a traceable link from PSP settlements to posted ledger records. Choose narrower P2P first when post-PO execution is the main risk, and expand to broader S2S only when upstream sourcing decisions are driving payment failures.

What PO-to-Settlement Payout Operations Need to Cover#

If you are deciding how supply chain platforms pay logistics providers from PO to settlement, treat it as one operating path from requisition to payment, not a set of disconnected tools. The useful unit of analysis is the full chain, not just the payout rail at the end. A Purchase Order (PO) is the binding buyer-seller document, but the work starts earlier with a requisition that needs approval before the PO exists. At the other end, source-to-settle connects supplier selection, PO creation and management, invoice processing, and payment into one sequence. Expansion can fail at the handoffs, not at the headline feature.

Verification point: by the time you finish this guide, you should be able to describe your real order of operations in plain English and name the owner for approval, invoice handling, and final settlement.

The next move is to use operating evidence before you spend product or go-to-market effort. Generic procurement diagrams are too clean for logistics. They may not show where invoice disputes or manual approvals slow settlement and create exceptions for Accounts Payable (AP). They also do not always tell you which market constraints may force a design change. This guide stays close to the actual path so you can judge whether you need a narrower Procure-to-Pay shape first or broader source-to-settle coverage from day one.

There is a simple red flag here. If your team can describe the market opportunity but cannot produce sample PO records, invoice examples, or the current exception path from AP to payment release, you are not ready to commit build scope. That can mean the hard part is still hidden in operations.

The last foundation is control. The non-negotiables are not abstract governance boxes. In practice, they are the checkpoints that help stop a bad payment from leaving the building: approved requisition, valid PO, invoice review, and a clean handoff into settlement. If you cannot say where those checks happen, who can override them, and what evidence is retained, rollout risk is already high.

A second red flag is treating market summaries as verified operating truth. Some public industry material explicitly notes that public-source data was not independently verified. Market research is still useful, but it is not a substitute for process evidence.

By the end of this article, you should have a decision-ready path. Map the real flow, identify where it breaks, define the controls that must block settlement, and scope expansion only after those constraints are visible.

For a step-by-step walkthrough, see How Podcast Monetization Platforms Pay Hosts, Advertisers, and Network Partners.

What to prepare before you choose a market and build the payment flow#

Do not choose a market or design settlement logic until you have a minimum evidence pack and clear ownership at each handoff. The real path runs from requisition and PO through supplier payment, and teams stall when procurement, finance, and payout operations stay siloed.

Step 1#

Build the minimum evidence pack before any build decision. Gather real PO samples, carrier invoices used for Invoice Matching, and current AP exception logs. If you cannot show how a PO becomes an invoice review case and then either an approved payment or an exception, you are still guessing.

Use one checkpoint: a peer should be able to trace one transaction end to end from those records alone. Flag failure modes early, especially missing references, inconsistent supplier naming, and AP notes that reveal off-process workarounds.

Step 2#

Map system ownership across TMS, ERP, and AR before you scope expansion. The issue is not only tooling; it is how shared systems, data, and processes connect partners and internal teams.

You do not need a perfect architecture diagram yet. You do need explicit owners for who creates the PO, who confirms service or receipt, who approves invoice exceptions, and who releases payment instructions. If ownership is fuzzy, rollout risk is already high.

Step 3#

Set your source of truth before market discussions. If the Ledger is not authoritative for PSP Settlements, pause build decisions and assign reconciliation ownership first.

Then define market decision gates in plain language: required KYC/KYB/AML checks, payout-eligibility criteria, and who can approve exceptions. Keep policies specific enough to assign approvers and evidence retention before launch, without inventing rules too early.

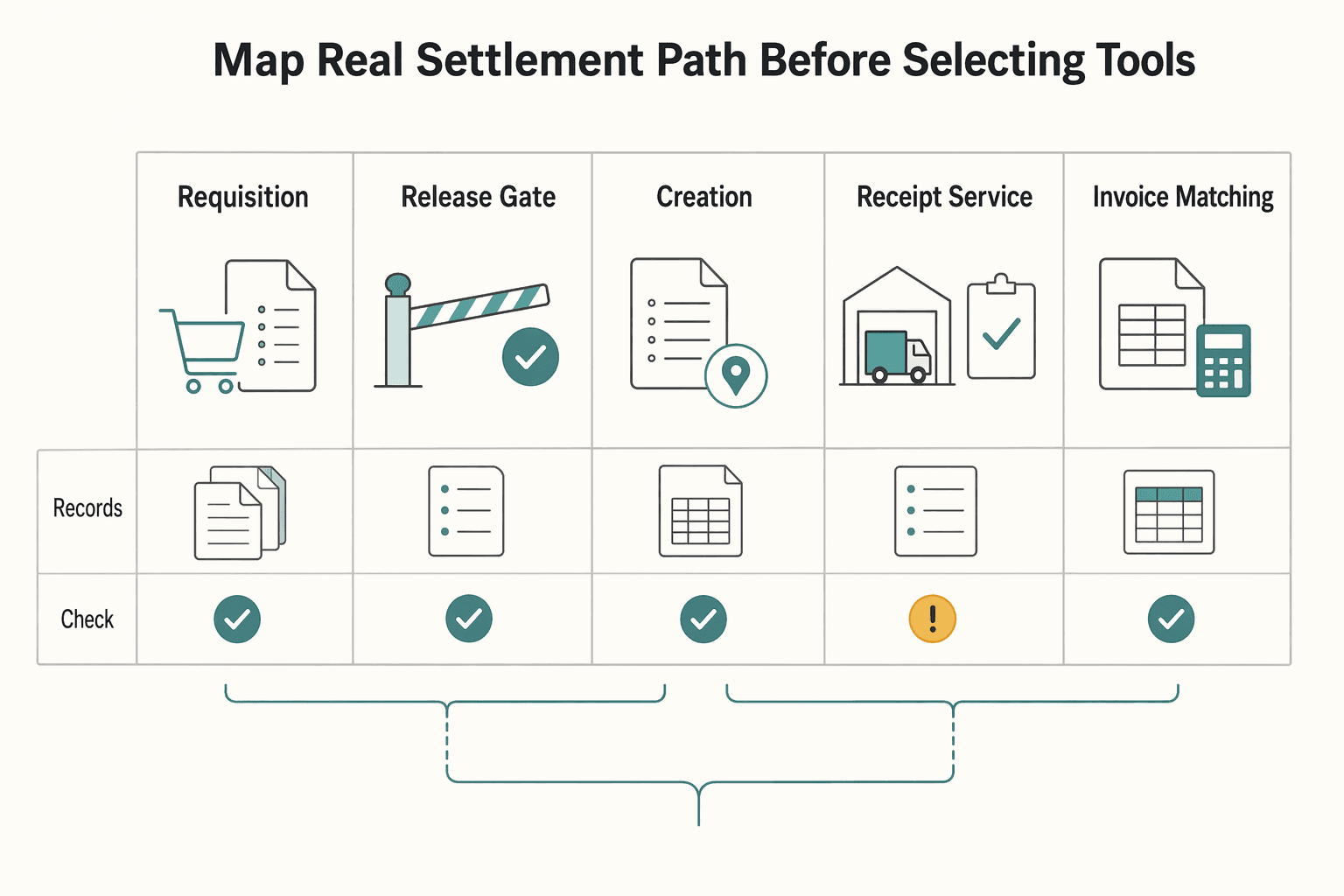

Map the real PO to settlement path before selecting tools#

Before you evaluate vendors, map your real PO-to-settlement flow on one page. Use a traceable path from requisition and approval to PO creation, receipt or service confirmation, invoice matching, and final settlement so you can judge tool fit against actual operations.

| Stage | Key record | Traceability note |

|---|---|---|

| Requisition | Requisition ID | Start with the sequence you actually run. |

| Approval | Approval record | Use the actual flow, not the one remembered in meetings. |

| PO creation | PO number | The PO is the binding record with order details, payment terms, and delivery details. |

| Receipt or service confirmation | Receipt/service confirmation | Downstream events should tie back to the PO. |

| Invoice matching | Invoice number; match result | Make split invoices explicit on the map. |

| Payment approval | Payment approval | If a peer cannot trace the path from records alone, pause tool selection. |

| Settlement | Settlement reference; final posting record | Add status checkpoints into the Ledger so traceability is explicit. |

Step 1#

Start with the sequence you actually run, not the one remembered in meetings: requisition, approval, PO creation, receipt/service confirmation, invoice matching, and settlement. A Purchase Order (PO) is the binding record that carries order details, payment terms, and delivery details, so downstream events should tie back to it.

For one real transaction, document the core references end to end: requisition ID, approval record, PO number, receipt/service confirmation, invoice number, match result, payment approval, settlement reference, and final posting record. If a peer cannot trace that path from records alone, pause tool selection.

Step 2#

Mark every handoff where one operational event can branch into multiple financial outcomes. Make partial shipments, returns, backorders, split invoices, and split payouts in Payout Batches explicit on the map, even if handling is still manual.

Then define which identifier must stay consistent across those branches so finance and operations can reconcile the same transaction without ambiguity.

Step 3#

Add status checkpoints at each transition into your Ledger so traceability is explicit. If Virtual Accounts are in scope, document the statuses your team uses for credits (for example, pending, held, or returned) and who can move each state.

Keep this practical: each status should connect system behavior to policy and risk controls, not just UI labels.

Step 4#

Separate handoffs that can rely on manual review from handoffs that need repeatable system handling. For judgment calls (such as disputed confirmations or invoice exceptions), manual review may be acceptable; for settlement-critical event creation, document controls that prevent duplicate financial outcomes.

Use a simple replay check in test: the same input should produce one intended financial result.

Decide whether P2P is enough or you need S2S coverage#

Decide scope by the control gap you need to close first, not by vendor labels. If your near-term goal is reliable execution from approved PO through Invoice Matching to Settlement, a narrower P2P scope can be the right first move. If sourcing choices, provider terms, and settlement controls must work as one system, plan for broader S2S coverage early, even if rollout is phased.

One caution before tool selection: these terms are used inconsistently. P2P, Source-to-Pay, and S2S are often used interchangeably, so evaluate platforms against your actual business events, not acronym claims.

Step 1#

Anchor the decision to your expansion objective.

- Choose

P2Pfirst when your primary risk is transaction discipline after PO creation: receipt confirmation, Invoice Matching, AP approval, and traceable settlement posting. - Prioritize broader

S2Sgovernance when sourcing and downstream settlement policy need to be coordinated. Some value is described as materializing only in integrated end-to-end setups, and separate sourcing/procurement tools may not be sufficient on their own.

Use a quick checkpoint on recent or expected provider transactions: does breakdown happen mostly after PO issuance, mostly before PO issuance, or across both stages? That answer is a stronger scope signal than category names.

Step 2#

Estimate ongoing burden by function before expanding scope.

- Procurement: Will supplier and terms governance stay stable, or change frequently enough that upstream control must tighten now?

AP: Are exceptions mainly business disputes, or recurring process/data issues tied to matching and approvals?- Payments ops and engineering: Can

ERPandTMScarry stable references from PO to invoice to settlement without manual rekeying?

If broader scope adds surface area without improving record continuity, it adds complexity without adding control.

Step 3#

Include financing in the scope call, but keep it as a separate design question. If provider pressure is about payout timing, evaluate whether Reverse Factoring or broader supply chain finance belongs in your model. If the core problem is inconsistent matching or approval flow, fix that first so financing does not become a workaround for process gaps.

For retention and payout-quality implications, see Bad Payouts Are Costing You Supply: How Payout Quality Drives Contractor Retention.

Design control points that prevent bad settlements#

Set release controls before you automate volume: settlements stay cleaner when payout cannot move ahead of proof, ownership, or policy status.

Step 1#

Gate release on record alignment: approved PO, receipt or service confirmation, and an invoice decision that passes your Invoice Matching rules. If one record is missing or disputed, keep the transaction on hold and route it to a named reviewer.

Use spot checks to confirm traceability on real payouts. You should be able to follow each transaction from PO reference to receipt evidence to invoice decision without manual rekeying across TMS, ERP, and accounting records.

Step 2#

Treat exceptions in Freight Audit and Pay as decision queues, not storage. Give each queue a clear owner and response target so disputed freight charges, missing paperwork, and settlement mismatches do not disappear into a generic backlog.

Keep each item scannable under pressure: age, current owner, blocking reason, next action, and required evidence. If closure does not require a disposition reason, you lose visibility into recurring defects.

Step 3#

Where your product supports payout eligibility and withdrawals, connect policy status to release decisions instead of leaving it as a side alert. Checks such as KYC, KYB, and AML can be applied as eligibility gates according to your market and provider policy.

Also document repeat-request handling before go-live. For suspected duplicates or retries, your team should be able to reconstruct the original request, the subsequent request, the decision taken, and the resulting posting record from one shared transaction reference.

Build the reconciliation chain finance can trust#

A reconciliation chain is trustworthy only when every payout can be traced from PSP Settlements to posted accounting records to the finance export used at close. If that trace breaks, the payout is not reconciliation-ready.

Step 1#

Keep one stable reference chain from provider-facing records to journal entries. If each layer creates its own ID without strict mapping, you will not be able to reconstruct what happened without manual cleanup.

Sample a recent Payout Batch and verify the same reference, amount, currency, and status across settlement records, postings, and finance exports. A status conflict across those layers is a reconciliation break even if summary dashboards look fine.

| Layer | Must carry forward | What to verify |

|---|---|---|

PSP Settlements | Provider reference, batch ID, amount, status, timestamp | Each settlement line maps to one internal transaction reference |

| Posting records | Transaction reference, debit/credit entries, posting status | Posting reflects the settlement event with no duplicate or missing entry |

| Finance exports | Transaction reference, journal line or export row ID, period | Exported rows reconcile back to posted entries |

Payout Batches | Batch ID, included payout lines, confirmation artifact | Batch total matches settlement lines and posting impact |

If you use virtual accounts or similar routing, carry that identifier through the same chain so supplier payments stay linked to shipment, installment, or delivery triggers in both ops and accounting views.

Step 2#

Run reconciliation in two passes: an in-period operational pass and a month-end close pass. The exact cadence can vary, but separating these passes helps catch breaks early and close with fewer surprises.

For the operational pass, compare Accounts Payable (AP), bank movement, and Settlement status side by side. For month-end, confirm every open break is either resolved or explicitly carried with an owner, reason, and accounting treatment. Reconciliation here means confirming consistency and accuracy across internal modules and external systems.

Use a named break path, not a generic queue, with at least:

- transaction or batch reference

- break type (amount mismatch, status conflict, missing bank movement, duplicate posting)

- current owner (AP, payments ops, or engineering)

- cash and period impact

- required evidence to clear the break

When ops and finance statuses disagree, resolve to posted accounting state until the break is cleared. If you need a practical operating model, this is the same discipline behind a month-end close checklist.

Step 3#

Treat the posted accounting record as the authority, and keep an evidence pack for each Payout Batch. Dashboards are useful, but they should be derived from posted state, not used to overrule it.

For each batch, retain:

- matched

Purchase Order (PO), receipt or service confirmation, and invoice decision - related line(s) from

PSP Settlements - posting record(s) tied to those lines

- payout confirmation for the batch

- exception decisions, approval notes, or dispute notes that changed outcomes

Some frameworks report simulated gains in speed, reconciliation accuracy, manual-step reduction, and audit readiness, but those are directional, not guarantees for production. The practical standard is simpler: one traceable reference chain, one authoritative posted state, and complete evidence for each payout. Related reading: How Marketplace Platforms Pay Third-Party Sellers Compliantly.

Handle cross border compliance and tax constraints early#

Treat compliance scope as a launch gate: if required checks, tax documents, and invoice acceptance rules are still unclear for a market, keep payouts out of full automation.

Step 1#

Start each market entry checklist with KYC, KYB, and AML, then map payout operations around that checklist. Provider connectivity and payout speed are secondary if teams cannot align on who is verified, who owns refreshes, and which records must exist before release.

Use one shared checklist and one clear decision owner across ops, finance, and compliance for each target corridor. If those ownership and evidence questions are still open, treat the corridor as not launch-ready.

Step 2#

Define tax document dependencies by provider type before payout mapping. Your matrix can include W-8, W-9, Form 1099, and whether FBAR tracking responsibility may exist for your business.

Where FBAR (FinCEN Form 114) is relevant, be explicit about filing mechanics. The maximum account value is a reasonable approximation of the greatest value during the calendar year, amounts are recorded in U.S. dollars rounded up to the next whole dollar, and foreign-currency conversion uses the Treasury rate for the last day of the calendar year. If a filed report contains errors, file an amended report.

Step 3#

Put VAT Validation in the invoice-acceptance path before settlement approval when VAT treatment affects payout eligibility. That checkpoint should link the invoice, supplier record, and approval decision so finance can explain why an invoice was accepted or held.

Step 4#

If compliance scope is still uncertain, contain risk with a limited Merchant of Record (MoR) setup or a controlled pilot. Keep volume low, log exceptions, and block full payout automation until open compliance items are resolved.

Repeated manual overrides for onboarding or invoice acceptance are an operating-model signal, not just temporary friction.

Common failure modes and how to recover fast#

Recover fastest by stopping questionable money movement immediately, assigning one owner per exception, and restarting only after records are clean.

| Failure mode | Fast recovery action | Restart check |

|---|---|---|

Invoice and shipment mismatch in Freight Audit and Pay | Freeze Settlement, route to the named exception owner, and require refreshed Invoice Matching against current shipment facts. | The hold shows an exception code, linked invoice version, and owner. |

Unmatched inbound credit to Virtual Accounts | Hold funds, investigate reference data and mapping, then post or return based on your configured policy checks. | Each unmatched credit has dated disposition notes before release. |

| Duplicate payouts during retry storms | Enforce idempotency keys, reverse duplicate Ledger postings, and replay only validated requests. | Only requests that match the original instruction set are replayed. |

Month-end breaks between PSP Settlements and accounting | Run a same-day forced-close checklist, publish unresolved items, and pause new automation changes until reconciled. | Finance and payments ops sign off from one unresolved-items list. |

If you need a template, use this month-end close checklist. Related: How Annotation and Data Labeling Platforms Pay Workers Under Piecework and Compliance Constraints.

Conclusion#

The teams that get this right do not start with a broad platform vision. They start with evidence, choose the smallest scope that still controls payout risk, and only then add volume or markets.

Use this copy-and-paste checklist as your final go or no-go pass:

- Confirm ownership across

TMS,ERP,Accounts Payable (AP), andLedger.

Name one accountable owner for shipment facts, one for accounting truth, and one for data movement between the two. Your checkpoint is simple: when settlement status disagrees with the accounting record, everyone should already know who decides the accounting result, who validates the freight record, and who fixes the mapping or retry issue.

- Choose

Procure-to-Pay (P2P)orSource-to-Settle (S2S)based on expansion risk.

If you are entering one market with stable provider contracts, P2P can be a faster operational scope because it stays close to approved Purchase Order (PO), invoice, and payment execution. If you are expanding across markets or changing supplier terms often, S2S is broader by design, from supplier selection through settling financial obligations, but it adds more governance surface that you need to staff and maintain.

- Validate release gates before any provider payment goes out.

Freight payment depends on checking invoice charges against agreed rates and shipment records, not paying from a loose approval thread. The practical checkpoint is that each released payment should tie back to approved purchasing, receiving or service confirmation, the invoice record, and final posting. Red flag: a clean delivery in the TMS but a disputed or stale Invoice Matching result in the payment path.

- Reconcile settlements to the

Ledgerbefore adding markets.

The key is not a slogan about cadence. It is having a reconciliation process your finance team can repeat, explain, and evidence with settlement files, journal entries, batch references, and payout confirmations. A common failure mode is scaling into new corridors while unresolved mapping breaks still sit between settlement status, bank movement, and posted accounting entries.

- Pilot one corridor, measure exceptions, then expand in staged

Payout Batches.

Start where provider contracts, shipment patterns, and invoice logic are easiest to inspect. Track exception rates for partial shipments, split invoices, duplicate retry attempts, and unmatched settlements before you widen scope. If something is still unknown, such as provider file formats, partial payout behavior, or reconciliation exports, document it and require proof before full rollout.

That is the real decision rule: map the flow you actually run, lock the control points you can verify, and treat every expansion step as earned rather than assumed.

Frequently Asked Questions

What is the practical difference between `Procure-to-Pay (P2P)` and `Source-to-Settle (S2S)` for logistics platforms?

For a launch decision, this source set clearly covers the PO-to-payment execution scope: the purchase order process starts when a PO is sent and ends when the supplier is paid. If your pain starts before PO issuance, treat that as upstream process design; this pack does not define a detailed S2S standard. The useful rule is simple: if you need cleaner payment operations this quarter, stabilize PO-to-payment discipline first.

What are the minimum steps from `Purchase Order (PO)` to `Settlement` if we need a launchable process this quarter?

A launchable minimum is an approved PO and a clear, auditable path to supplier payment. Teams often include receipt or service confirmation, invoice review or matching, payout approval, and settlement posting to the accounting record. Common definitions of the purchase order process follow that same arc: it starts with PO issuance and ends with supplier payment. Your checkpoint is whether each payout can be traced back to a PO and a final posted entry.

Why do logistics invoice payments fail even when freight operations look successful?

Because moving freight and proving what should be paid are different jobs. In practice, freight billing and payment are often harder than moving the freight itself, especially when shipment, receipt, and invoice data drift apart across tools. A common failure mode is delivery execution and payment approvals getting out of sync when systems are isolated.

Which controls are non-negotiable before releasing provider payouts across markets?

Do not release funds unless the approved charge basis, receipt confirmation, and Invoice Matching outcome are aligned and traceable. At minimum, keep clear exception ownership and a posting trail that ties the settlement back to the source transaction. Red flag: paying from an email approval when core records still disagree.

How should we split ownership between finance, ops, and engineering for `TMS`, `ERP`, and `Ledger` reconciliation?

Effective execution requires cross-functional collaboration across procurement, operations, logistics, and finance. A practical split is: finance owns accounting truth and reconciliation signoff; ops owns shipment facts and exception evidence; engineering owns data movement and mappings across TMS, ERP, and payment systems.

What remains unknown before selecting a provider stack if benchmarks and architecture detail are missing from market content?

Usually the big unknowns are not headline features. They are operating evidence: sample settlement files, exception handling paths, reconciliation exports, and the ways isolated tools can block information flow. Ask for proof of duplicate handling, invoice version control, partial-shipment handling, and posting traceability before you commit. If provider pressure is really a cash-timing problem rather than a matching problem, you may also need to test whether buyer-led supply chain finance belongs in scope.

Try a related tool

A former tech COO turned 'Business-of-One' consultant, Marcus is obsessed with efficiency. He writes about optimizing workflows, leveraging technology, and building resilient systems for solo entrepreneurs.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- fincen.gov/reporting-maximum-account-valuetrusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/irm/part4/irm_04-026-009trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC10122550trusted

- ripuc.ri.gov/sites/g/files/xkgbur841/files/2026-02/25-45-...trusted

- 3scsupplychain.com/supply-chain-finance/freight-payment-vs-frei...external

- cleo.com/blog/procurement/purchase-order/purchase-ord...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

What Is Reverse Factoring? How Supply Chain Finance Lets Platforms Pay Contractors Early at Low Cost

The core decision is not what you call the model. It is whether you can run a buyer-led financing program on invoices the buyer has confirmed as valid, with approval controls a finance provider can rely on.

Bad Payouts Are Costing Your Supply in Two-Sided Platforms

Payout issues are not just an accounts payable cleanup task if you run a two-sided marketplace. They shape supply-side trust, repeat participation, and fill reliability. They can also blur the revenue and margin signals teams rely on.

Month-End Close for Payment Platforms with PSP Settlement Control

Month-end close often breaks down when PSP settlement is treated as a side reconciliation. For payment platforms, settlement is often the clearest record of what cash should have moved, so it should drive the close rather than being checked after journals are drafted. If you run close across multiple PSPs, you need that settlement record to lead the review before your team starts defending journal entries.