Quick Answer

Define stage-based refund rules first, then enforce them with records and ownership. For refund policies service businesses protect, assign a default outcome for pre-work, in-progress, and completed delivery, and require proof of purchase plus acceptance evidence before denial. Store the exact terms version accepted at checkout, not just the current policy page. Include a market review checkpoint for items like California Civil Code section 1723 so legal review is tied to where you operate.

Why this matters for platform teams#

A strong refund policy can reduce avoidable dispute risk without turning every customer issue into a payout loss. For platform teams, the goal is not to be stricter. It is to set a policy you can actually enforce, while keeping enough flexibility to preserve trust when delivery is partial, delayed, or disputed.

Start with the right scope#

Start with the scope. This article is for service businesses and platforms running contractor, creator, marketplace, or embedded-payments flows where money moves before, during, or after work is delivered. It is not about retail returns, warehouse restocking, or unopened goods. If you borrow retail language anyway, you can end up with terms that sound familiar but break down when the dispute is really about milestones, acceptance, or who performed the work.

That distinction matters because service delivery can be harder to prove than product shipment. A customer can accept part of a project, reject the final handoff, or say the work never met the brief. Your policy has to address those stages directly, not hide behind blanket no-refund language.

Treat this as a product and payments problem#

Treat the core tension as a product and payments problem, not just a legal drafting exercise. Customers want a fair way to get money back when something goes wrong. In disputes, outcomes often depend on whether you can show what was promised, what was delivered, and what the buyer agreed to at purchase. If your terms promise broad flexibility but your operations cannot approve, document, and execute that flexibility consistently, you create the worst mix of outcomes: margin leakage and weak dispute defenses.

One practical red flag is promising instant or automatic refunds when your actual payment rails do not support that cleanly. In one published example policy, card refunds can take 10 to 14 business days to appear. The exact timing is not universal, but the lesson is useful. Customer-facing promises need to match execution reality. Before you publish policy text, verify what your processor, ledger, and payout setup can actually complete and how refund status is confirmed after initiation.

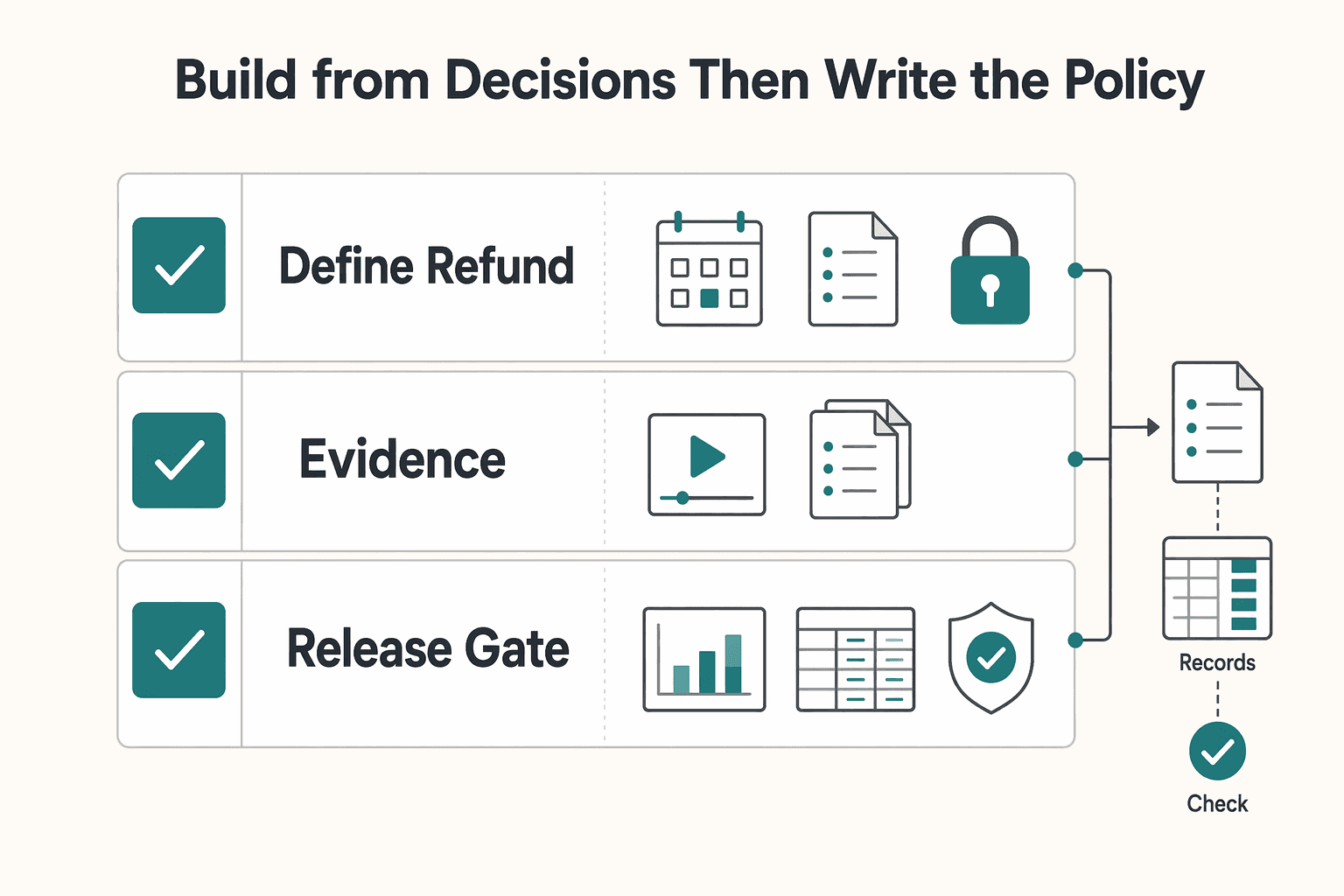

Build from decisions, then write the policy#

Build the policy from decisions first, then turn those decisions into text and operations. Use a simple sequence:

- Define refund outcomes for each service stage, usually full refund, partial refund, service credit, or denial.

- Map each outcome to delivery evidence, such as proof of purchase, milestone acceptance, support messages, or cancellation timing.

- Wire the policy into execution, including approval rules, refund initiation, customer notice, and an audit trail.

If you skip step two, support ends up improvising. If you skip step three, finance or engineering cannot reliably honor what legal or product published. The common failure mode is easy to spot: your checkout says one thing, your agents say another, and the dispute file shows neither side followed a consistent rule.

The rest of this guide follows the same order you'll need in practice: inputs first, then stage-based decisions, then timing, language, approvals, and dispute evidence. For a step-by-step walkthrough, see How to Choose a Corporate Service Provider for Offshore Incorporation.

Gather the inputs before you write policy language#

Start with one clean input set before drafting anything new. Service refund terms get weaker when old promises remain live across checkout, contracts, and support copy.

Collect every live promise#

Pull every customer-facing promise into one review: refund, return, exchange, and no-refund pages, plus terms and conditions, order forms, checkout text, and support macros. Compare them line by line. Mark contradictions directly, especially where one place offers credits, another offers cash refunds, and another says final sale.

Before you draft, ask one question: for each service stage, can you point to one canonical promise and where the customer sees it? If not, fix that first.

Build a market review list#

Create a simple review matrix with market, reviewer, affected pages, and required copy changes in checkout or contracts. If you already track markets that need explicit legal review, include them there; California and California Civil Code section 1723 can be tracked as review items rather than paraphrased from memory.

Also document how users accept terms. Active assent capture, such as an "I Agree" checkbox, is commonly treated as useful evidence of agreement and can support enforceability, but it is not a universal guarantee on its own.

Map payment rails and evidence needs#

List your payment rails and dispute exposure, then make sure policy promises match what your operating flow can actually support. For card-heavy volume, include networks like Visa and Mastercard in that review so policy language and escalation handling stay aligned.

Define the records you require before approving remedies, and confirm you can consistently store them. If your policy depends on evidence you do not retain, close that gap before you publish.

Define refund outcomes by delivery stage#

Define outcomes by stage so your agents can reach the same decision from the same delivery status, policy deadline, and documents.

| Delivery stage | Typical trigger | Default outcome | Minimum evidence to apply it |

|---|---|---|---|

| Pre-work | Customer cancels before work starts and request is inside your policy window | Full refund | Proof of purchase and order timestamp showing work not started |

| In progress | Partial delivery was accepted | Partial refund or service credit | Proof of purchase, scope/contract, accepted milestone or deliverable |

| In progress | Work started but no deliverable accepted | Service credit or denial (per terms) | Proof of purchase, work/scheduling records, customer communications |

| Completed | Service delivered and accepted | Denial (per terms) | Proof of purchase, delivery record, acceptance record |

| Completed with quality defect | Delivered work is materially incomplete, unusable, or does not match agreed scope | Exception path: rework, partial refund, or full refund | Proof of purchase, scope/contract, delivered artifact, defect evidence |

Write the rule logic next to the table in plain language: if work has not started and proof of purchase is valid, default to full refund; if partial delivery was accepted, default to partial refund or service credit; if delivery is complete and accepted, apply your completed-stage outcome unless the quality-defect row applies.

Be explicit about accepted documents. Name the records customers are commonly told to gather: receipts, invoices, contracts, canceled checks, and credit card statements. Keep time limits explicit too, since eligibility is often deadline-based (for example, 30 or 90 days in many return/exchange policies).

Treat final sale and no-refund policy as legal-review terms, not as a shortcut around stage and evidence checks. For defect-style disputes, route to the quality exception row and legal review flags (including implied warranty and Title 1.7 Consumer Warranties) instead of auto-denying. Related reading: How to Build a One-Page Freelance Service Level Agreement.

Set timing windows and acceptance checkpoints#

Your stage table is only reliable if each outcome has a clear time window and a clear proof point. Set request windows around real service milestones, because unclear or overly tight windows can increase dispute risk and push cases toward chargebacks.

Set windows from real milestones#

Define each request window from the delivery stage and the contract milestone tied to payment.

| Scenario | Request window |

|---|---|

| Pre-work cancellations | Window runs until work starts |

| In-progress quality or scope issues | Window runs from milestone delivery |

| Completed-service issues | Window runs from final delivery or final acceptance, based on your contract |

Sanity-check each window against real customer behavior: can the customer review the output, compare it to scope, and contact support in time? You do not need to copy card-network timelines into your policy text, but you should account for the operational cost of avoidable chargebacks.

Require explicit acceptance at each milestone#

If you may deny based on "service delivered," define acceptance so it is provable in the case record.

Use one or more acceptance artifacts per milestone:

- Signed approval in your contract portal

- Email or in-app acceptance confirmation

- Meeting recap with customer acknowledgment

- Delivered work item tied to a timestamped approval action

Store the milestone name, delivery timestamp, acceptance method, and artifact location together. If evidence is scattered across tools, denial decisions become harder to defend.

Route missing acceptance evidence to manual review#

Make this an internal decision rule: if acceptance evidence is missing, do not auto-deny; send the case to manual review and decide from the full evidence pack.

Apply the same discipline to policy versions. Store the refund-terms version shown at purchase, or in the signed agreement, with its timestamp, and show agents both purchased and current terms so they can apply the governing version consistently.

Write customer-facing terms that are clear and defensible#

Make the terms easy to apply in one read: customers should know whether they qualify, how long they have, and what outcome to expect.

Turn internal rules into five public sections#

Convert internal rules into five plain-language sections:

- Eligibility: which orders, service types, and delivery stages can get a full refund, partial refund, credit, or no refund.

- Exclusions: which facts block a refund, such as completed accepted work, customer no-shows, or missing proof of purchase.

- Timelines: which milestone starts the request window.

- Remedies: whether the outcome is money back to the original payment method, service credit, re-performance, or denial.

- How to request support: where to submit the request and what evidence to include.

A quick test: ask a support lead who was not in the policy meeting to resolve three sample cases using only this public text. If they need internal notes, the terms are still too abstract.

Put terms where customers make decisions#

Publish the same core terms at the decision and support points: checkout, service agreement or order form, confirmation email, and the support entry point.

Keep the headline promise, request window, and remedy options consistent across all surfaces. If checkout says one thing and support macros say another, you create avoidable disputes.

Define fees and legal references carefully#

If you charge a nonrefundable amount, name the fee for what it is, for example scheduling, intake, or third-party pass-through, and state when it is charged and when it is not.

Use legal references narrowly and accurately. The CFPB excerpt at 12 CFR 1026.36 is scoped to credit secured by a dwelling, not general refund-policy authority. FederalRegister.gov also states its displayed text is informational and not an official legal edition, and advises legal researchers to verify against an official Federal Register edition. If you review the Transportation Department rule page titled "Refunds and Other Consumer Protections" dated 04/26/2024, verify it against an official Federal Register edition before you rely on it for legal drafting.

Build the internal approval and execution sequence#

Your risk is execution, not wording: a clear policy still fails if ownership, step order, and records are loose.

Assign an owner to each state change#

Assign one owner per state change, not one team for the whole flow. Map ownership from intake to close: Support for intake and evidence collection, Product for policy logic and version mapping, Finance/Ops for approval controls and money movement, and Engineering for automation and status integrity.

For each state, name who can move the case and who reviews exceptions. Keep states explicit: request received, evidence complete, eligibility validated, approved or denied, refund executed, customer notified, audit logged, case closed. FAR Part 7 is not refund guidance, but its focus on responsibilities and general procedures is the right operating standard: if a step exists, it needs an owner.

Lock the order of operations in the case record#

Enforce one fixed sequence in the case file:

- Validate eligibility.

- Verify proof of purchase.

- Check the policy version tied to purchase date.

- Approve or deny.

- Execute refund.

- Notify customer.

- Log audit trail.

Do not execute refunds before the record shows purchase identifier, service milestone, applicable terms version, and decision reason. Keep the exact version the customer agreed to at purchase; "current policy" is not enough when terms changed later.

Control execution so one decision creates one refund#

Build controls so one approved decision creates one money movement. Use idempotent execution, event reconciliation, and ledger-first closure as internal controls.

Idempotency prevents duplicate refunds from retries. Reconciliation ties processor or webhook events back to the case so you can catch gaps like approved-but-not-settled or settled-but-not-posted. Ledger-first closure means the internal reversal is recorded before the case can close.

Route exceptions to humans#

Send exceptions to a queue, not to silent denial. Break automation for duplicate requests, stale status, missing evidence, and payout-rail mismatch.

Track every customer communication and internal handoff in the case history. That record is what lets your team explain the decision path, timing, and ownership when a case is challenged.

Prepare for disputes and chargebacks before they happen#

Assume some denied refunds will become disputes, and make each case defensible from the first response with complete records already attached.

Build a standard evidence pack for each dispute type#

Define one required file structure for the dispute scenarios you actually see, and avoid relying on memory for network-specific details. Your pack should clearly show what was sold, what the customer saw before paying, what they accepted, what you delivered, and what happened after they complained.

| Case file item | Included detail |

|---|---|

| Order ID or invoice number | Proof of purchase |

| Policy or terms version | Tied to the purchase date |

| Checkout or order-form disclosure evidence | Screen, link, or signed contract section shown before payment |

| Acceptance record | Timestamp and user or account identifier |

| Service-delivery records | Tied to milestones, completion, or usage |

| Customer communications | Refund requests, support replies, and any exception approvals |

Use a quick check: pull three recent cases and confirm Finance/Ops can defend each file without asking Support or Product for missing evidence.

Keep visibility and delivery proof in one record#

Keep policy visibility, delivery proof, and customer communication in one timeline-ready record. FTC consumer guidance tells buyers to review a company's return policies and collect related documents before trying to resolve a refund issue, so expect that same document trail to matter in disputes.

The weakest files usually fail on policy visibility and service acceptance. "Policy existed on the website" is weak if you cannot show what the customer actually saw at checkout or in the order flow. "Work was completed" is weak if your file lacks dated acceptance evidence, milestone signoff, usage logs, appointment completion, or another account-linked delivery record.

If a denial depends on a milestone being met, include the timestamped event proving it. If that event is missing, route the case to manual review instead of treating it as ready to defend.

Escalate changed-terms cases early#

If terms changed after purchase and you cannot show customer-level notice, treat the case as elevated risk and escalate early. Do not let Support deny from the current policy page just because it is easier to find.

The key checkpoint is a version match: purchase date, acceptance timestamp, and the policy version in force at that moment. A common failure is submitting today's terms to defend yesterday's sale. If that happens, narrow your response to the original terms if you have them, or move quickly to manual review and commercial resolution instead of overstating a weak position.

Common policy failures and how to recover fast#

Policy failures are recovery work, not drafting work. When teams conflict or complaints keep resurfacing, move fast: set one source of truth, align responses, and verify the fix in live cases.

Freeze contradictions and publish one canonical policy#

If your site says one thing and Support says another, pause discretionary exceptions until wording is aligned. Publish one canonical refund policy version, retrain agents, and re-audit macros, help-center copy, checkout disclosures, and contract snippets so customers see the same rule everywhere.

Your recovery check is simple: compare recent cases against the policy version shown at purchase and the response actually sent. If outcomes still depend on "what we meant," the policy is still not operational. FTC guidance also expects customers to review return policies and gather related documents, so mismatched wording weakens both trust and your evidence trail.

Replace rigid denials where complaints cluster#

Problems and complaints are part of customer relationships, so all-or-nothing denials can create repeat escalations. For high-friction cohorts, use stage-based outcomes: refund before delivery, partial refund during delivery, or service credit after substantial use or completion.

Start with one high-friction cohort rather than every service line at once. Then track whether escalations and manual handling fall after the change.

Rewrite legal-first copy into plain language#

Compliant text still fails if people cannot apply it consistently. Rewrite the live policy in plain language first: who is eligible, what is excluded, when to request, what documents to provide, and what remedy you offer. Then run legal review on that operational draft.

The checkpoint is consistency: a new agent should reach the same answer as Finance/Ops without escalation. Re-audit macros after the rewrite so old phrasing does not reintroduce the problem.

Build a market matrix before you expand#

If you operate across markets, keep a jurisdiction matrix with the approved policy variant, checkout disclosure location, contract language, and legal owner for each market. Roll out updates market by market with cross-functional sign-off, and keep version control tied to market and purchase date.

The recovery check is traceability: for any complaint, you should be able to show which policy version applied and what the customer saw before purchase.

Copy-paste checklist for launching your refund policy#

Do not launch until your team can consistently show what the buyer saw before purchase, what decision was made, and how that decision was executed.

- Define one default outcome per delivery stage.

Map each stage, for example pre-work, in progress, completed, and acceptance milestones, to one default result: full refund, partial refund, service credit, or denial. Sanity-check the table with real recent orders and confirm different reviewers reach the same result from the same facts.

- Make refund terms clear and conspicuous before payment.

Use checkout placement that is clear and conspicuous, not hidden in a footer or only sent after purchase. FTC guidance is explicit that core consumer protection standards apply online and that disclosures should help people understand what they are paying for. Test desktop and mobile, then retain captures of checkout, linked terms, and confirmation states.

- Standardize the evidence file for each decision.

Require the same core records every time: purchase record, applicable policy version, and the service-stage documentation your policy relies on. If key records are missing, route to manual review instead of ad hoc approvals or denials.

- Prepare dispute-response packets before you need them.

Build a reusable packet template for card-payment disputes across your payment rails, including policy version, checkout disclosure capture, transaction record, service documentation, customer communications, and decision log. Align the template with your processor or acquirer guidance so your team is not improvising during a live dispute.

- Anchor legal review in documented markets and verified sources.

Start with jurisdictions you can document and avoid assuming one market's approach applies everywhere. If you use Federal Register material in legal research, treat it as a starting point and verify against an official edition. Assign explicit owners for legal review and policy version control.

- Dry-run refund operations end to end before go-live.

Run test cases through intake, decision, execution, customer notice, reconciliation, and audit logging, and confirm the records stay traceable throughout. If your process handles sensitive customer information, use the Safeguards Rule text itself as the primary source for obligations.

Related: The Best Background Check Services for Small Businesses.

Frequently Asked Questions

What makes a refund policy enforceable for service businesses?

A policy is easier to defend when the customer could see it before paying and understand what it means. Clear wording and clear placement before purchase are the core baseline. California offers a useful visibility benchmark in the retail context. Under California Civil Code section 1723, stores that do not accept returns must clearly display that policy, but that rule should not be assumed to map automatically to every service model or jurisdiction.

Can a service business use a no-refund policy without increasing disputes?

Potentially, but visibility and scope matter. In California consumer guidance, some items can be marked “final sale” or “as is” and treated as non-returnable when those terms are clear. Those labels do not erase every complaint path, and defect or warranty-related issues may still matter. FTC guidance also notes that complaint routes can help people recover money or reach another resolution.

How do clearer refund terms reduce chargebacks in practice?

Clear terms can reduce misunderstandings and leave a cleaner record if a dispute happens. Consistent disclosure before purchase, plus receipt/order documentation, helps support your position. If checkout says one thing and later communications say another, your records can become harder to defend.

What must be disclosed before purchase to lower legal and dispute risk?

Disclose whether refunds/returns/exchanges are allowed and whether any limited or no-return terms apply. California Department of Justice guidance is direct: know the return and exchange policy before you buy. If you require receipt documentation, say that upfront as well, since many retailers require the original receipt for returns.

What should we do if policy terms changed after the customer paid?

The grounding pack does not provide a specific rule for post-payment policy changes in service contracts. A safer approach is to keep dated copies of the policy shown at purchase and avoid applying stricter terms unless they were clearly disclosed and accepted. If you cannot show what the buyer saw before payment, disputes are more likely.

What if the customer paid by card and disputes even after we follow policy?

Respond with records, not summaries: proof of purchase/receipt and the policy terms that were visible before purchase. If key records are missing, reassess before escalating. FTC guidance says complaint routes can help people recover money or reach another resolution, so negotiated resolution may still be practical.

Try a related tool

Ethan covers payment processing, merchant accounts, and dispute-proof workflows that protect revenue without creating compliance risk.

Sources

- acquisition.gov/far/part-7trusted

- acquisition.gov/far/part-52trusted

- cbp.gov/trade/automated/ach/refundtrusted

- consumer.ftc.gov/node/77484trusted

- consumer.ftc.gov/articles/solving-problems-business-returns-r...trusted

- courts.delaware.gov/forms/download.aspxtrusted

- ecfr.gov/current/title-47/chapter-I/subchapter-B/part-64trusted

- federalregister.gov/documents/2024/04/26/2024-07177/refunds-and-...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Price a Bookkeeping Service for Small Businesses

**Step 1. Reset what a bookkeeping price is supposed to do.** A usable price is not just a number that sounds competitive. It should reflect the work required and how the engagement will actually run. Market comparisons help with context, but they do not replace a pricing strategy built around the real workload.

How to Vet Contractors and Global Partners With a 3-Tier Screening Process

Start by deciding whether you need formal screening at all. If the contractor will do low-sensitivity work with least-privilege access and no control over money, customer data, production systems, or live client relationships, Tier 1 may be enough. If any of that changes, or you expect to use a formal third-party background study or screening report, stop and move the case to Tier 2.

The Best PEO Services for Small Businesses

Many **best peo services** pages are just comparison lists. They help you spot names, but they usually do not answer which provider fits your hiring model, your risk tolerance, or how much HR admin your team can realistically absorb.