Quick Answer

Yes. When consecutive closes depend on spreadsheet bridges for Wire Transfer, PayPal, and eCheck reconciliation, your AP stack is likely past fit. Escalate from patching to an upgrade decision using three gates: control evidence in Ledger Journals, stable ERP plus Webhooks behavior, and near-term pressure from Global Payments or Multi-Entity Support. If two gates fail, move now; if two pass, run a short owner-led optimization sprint and recheck in the next close.

When Your AP Software Starts Holding the Team Back#

If your AP setup still works for one entity, modest invoice volume, and straightforward domestic payments, you probably do not need to replace it yet. Pressure usually starts when teams are supporting payment flows across more countries, more entities, more payment methods, and more people touching the process.

Who should read this closely#

- Scaling platform teams

This guide is for founders, product leaders, Finance and AP teams, Payments Ops, and engineering owners whose payables are no longer just bills in and bills out. Once you are handling suppliers across multiple countries and currencies, or trying to manage AP across domestic and global entities in one place, the question shifts from convenience to operational fit.

- Teams feeling pain beyond invoice entry

Growth does not just affect invoices. It also stretches supplier onboarding, tax identity collection, invoice management, and payments. Several parts of the supplier process can start breaking at once, so if you only inspect invoice capture, you can miss the real bottleneck.

- Operators patching gaps with manual workarounds

A strong signal is when people are keeping the current tool alive with spreadsheets, exports, side trackers, or disconnected tools because the ERP or AP product no longer gives enough visibility. That is often the point where "good enough" accounting software is still fine for basics, but no longer fine for broader operational complexity.

- Teams deciding whether to optimize or replace

Not every business needs an immediate replacement. Some companies can still run well on simpler AP tools, so the useful question is not "is our software old?" but "is our current setup adding avoidable risk as complexity rises?"

Who should probably wait#

If you have a single entity, low invoice volume, and no near-term global payments expansion, you may get more value from tightening process before replacing software. That can mean standardizing supplier intake or improving how data lands in your ERP before taking on a platform change.

How to use the seven signs#

Use the next section as a decision list, not a scorecard for its own sake. Focus on control coverage, visibility, integration fit with your ERP, and evidence from recent close cycles. A practical verification step is to review your last two closes and mark every place work left the AP tool and had to be recreated in spreadsheets, email, or manual ERP entries.

A common failure mode is treating AP pain as a narrow invoice problem when the real issue is broader supplier management and payments visibility. Before you choose between improving the current stack and moving to a stronger one, gather a small evidence pack: a few recent supplier onboarding cases, tax identity collection examples, invoices that needed manual intervention, and the accounting output your team had to fix afterward. That keeps the rest of the review grounded in what is actually breaking.

The 7 signs your platform has outgrown current AP software#

When these signs persist across closes, the issue is usually system fit, not team effort. Use this table to separate a narrow process gap from a broader AP fit problem.

| Sign | Observable symptom | Likely root cause | Business impact | Immediate next action |

|---|---|---|---|---|

| Volume strain | Finance: invoice and payment queues grow faster than team capacity. Engineering: batch jobs, imports, or payment handoffs need ongoing manual watch. | Throughput still depends on people, not AP automation. | Close delays, backlog growth, rising exceptions. | Targeted AP automation if controls still hold; full replacement if approvals, payments, and reporting all degrade together. |

| Manual invoice work | Finance: coding, matching, and status checks happen in email or spreadsheets. Engineering: OCR, intake, or ingestion is inconsistent. | Informal invoice tracking that breaks at higher volume. | Lost visibility, missed due dates, rekeying errors. | Process fix for isolated gaps; otherwise targeted AP automation. |

| Manual interventions | Finance: payment status and reconciliation are repeatedly corrected by hand. Engineering: retries and exception paths are unreliable. | Repetitive back-office work still requires operators. | Higher error rates and heavier month-end cleanup. | Targeted AP automation first; full replacement when manual recovery becomes normal operations. |

| Weak Financial Controls | Finance: approver sprawl, unclear segregation, weak audit trail. Engineering: permission logic is inconsistent across systems. | Access expanded faster than control design. | Approval risk, data integrity issues, harder audits. | Full replacement if controls cannot be enforced in product; otherwise a focused process fix. |

| Supplier friction | Finance: onboarding delays, payment complaints, rising support load. Engineering: fragmented supplier data and payment-method handling. | Supplier processes and payables are disconnected. | Slower daily operations and lower supplier trust. | Targeted AP automation if accounting outputs are stable; full replacement if onboarding, tax identity collection, and payments fail together. |

| Weak Multi-Entity Support | Finance: entity-by-entity workarounds for approvals, coding, and reporting. Engineering: custom branches by entity or country. | Stack was built for single-entity or simple domestic workflows. | Slow consolidation, policy drift, reporting errors. | Usually full replacement; workarounds tend to compound risk. |

| Brittle ERP connectivity | Finance: journals need manual edits after sync. Engineering: integrations fail silently or require frequent patches. | AP, ERP, and payment layers do not maintain reliable shared state. | Reconciliation risk, duplicate work, incident volume. | Full replacement when mapping and sync reliability break across closes. |

Use evidence, not opinions, to confirm the diagnosis. For each sign, trace the same sample flow from invoice receipt to approval to payment to posted entry. Where available, check Ledger Journals for end-to-end source traceability and Webhooks (or equivalent system events) for status consistency. If finance records and system events repeatedly diverge, treat it as a system-design problem, not a training issue.

A process fix is reasonable when the break is narrow. Targeted automation fits when repetitive work is the main drag but controls and ERP output remain trustworthy. Full replacement is usually the right call when failures hit operations, accounting, and engineering at the same time.

You might also find this useful: SaaS Accounting Software Evaluation: What Payment Platforms Need Beyond Standard GL Features.

Signs 1 to 3 show throughput and reconciliation are already breaking#

If these three signs show up across consecutive closes, your AP layer is being held together by workarounds instead of clean in-system execution.

- Volume is outrunning team capacity, so batching stops being optional.

When invoice and payment volume grows and the team keeps adding manual hours for routing, approvals, and settlement, throughput is scaling by labor. At that point, Payout Batches and stronger AP automation are operating requirements, not just efficiency upgrades.

- Manual capture across Wire Transfer, PayPal, and eCheck creates predictable reconciliation drag.

Mixed rails stay manageable only when each payment leaves a clean source record tied to invoice and posting. If your team still relies on email confirmations, portal checks, and CSV stitching, slower close cycles and cleanup work are expected. PayPal also signals that fee and rate details can change via its Policy Updates Page, and its pages were last updated on February 19, 2026 (US consumer fees) and February 9, 2026 (US merchant fees), with separate Domestic and International definitions and a dedicated E-check Fees section. Spreadsheet logic that assumes one static structure across products or markets will create classification fixes at month end.

- Spreadsheet dependence is a clear signal that your reconciliation surface is fragmented.

That is what outgrown systems look like in practice, especially when teams spend more time working around the system than inside it. Use a quick trace: follow three recent invoices from receipt to approval to payment to posted entry, and verify whether finance and engineering are looking at the same status history without manual stitching.

If close timelines keep stretching and workaround effort keeps growing across consecutive closes, stop patching and start a formal upgrade evaluation. Related: How to Handle Mid-Cycle Upgrades and Downgrades Without Double-Charging Customers. If you want a quick next step while you review options, try the free invoice generator.

Signs 4 and 5 reveal control and compliance debt#

If approvals, payouts, and posting outcomes cannot be traced in one record, you have an upgrade problem, not a cleanup task. A platform can still look functional while control risk and compliance debt compound underneath it.

| Artifact | Section detail | Review question |

|---|---|---|

| W-8 | Included where enabled in your setup before first payout. | Was it attached before first payout, and can finance export it without manual stitching? |

| W-9 | Included where enabled in your setup before first payout. | Was it attached before first payout, and can finance export it without manual stitching? |

| Value-Added Tax (VAT) details | Included where enabled in your setup before first payout. | Was it attached before first payout, and can finance export it without manual stitching? |

| Internal Revenue Service (IRS) reporting data | Included where enabled in your setup before first payout. | Was it attached before first payout, and can finance export it without manual stitching? |

| Form 1099 readiness | Included where enabled in your setup before first payout. | Was it attached before first payout, and can finance export it without manual stitching? |

| FBAR tracking support | Included where enabled in your setup before first payout. | Was it attached before first payout, and can finance export it without manual stitching? |

- Access and approvals grew faster than controls.

Start by treating this as a traceability failure. You can see a payout and a journal entry, but you cannot reliably show the approval path, role assignment, or exception decision that produced them in Ledger Journals and consistent Financial Controls.

Run a quick check: trace three recent exceptions from approval to payment to posted entry. If approval evidence lives in chat, email, or a separate admin tool instead of alongside the payment and journal record, the control gap is real. If your setup uses Know Your Customer (KYC), Know Your Business (KYB), or Anti-Money Laundering (AML) gating, confirm where the gate happened, who cleared it, and whether payout was blocked or released afterward.

- Supplier onboarding and payout reliability are slipping even if core AP tasks still run.

When onboarding degrades, payment reliability usually follows. The practical issue is whether supplier records capture required artifacts and gating outcomes before first payout. Where enabled in your setup, that includes W-8, W-9, Value-Added Tax (VAT) details, Internal Revenue Service (IRS) reporting data, Form 1099 readiness, and FBAR tracking support.

Review ten recently onboarded suppliers and ask: were required documents attached before first payout, and can finance export them without manual stitching? If either answer is no, onboarding is already creating payout risk.

FBAR is a useful stress test for record quality. FinCEN defines maximum account value as a reasonable approximation of the greatest value during the calendar year, requires amounts in U.S. dollars rounded up to the next whole dollar, and says non-U.S. currency accounts should use the Treasury rate for the last day of the calendar year. Its example converts $15,265.25 to $15,266.

For most individuals with an FBAR obligation, the due date remains April 15, 2026. A specific cohort with signature authority but no financial interest, for accounts tied to the 2025 calendar year, has an extended due date of April 15, 2027. If your platform cannot preserve that level of account history and context, "functional AP" is no longer enough. Related reading: Best Accounting Software for Small Agencies That Protects Cashflow.

Signs 6 and 7 mean your architecture no longer matches the business#

At this stage, the core issue is architectural fit: if finance and engineering both rely on manual repair to complete normal AP and payout workflows, replacement is usually cleaner than stacking more connectors.

- Sign 6: weak

Multi-Entity Supportturns normal finance work into entity-by-entity patching.

The clearest signal is trust breakdown, not just slower reporting. When teams keep shadow spreadsheets because they do not trust consolidated outputs, your AP and ERP setup is no longer carrying the operating model on its own.

Run a simple check from your last close: trace one supplier paid by more than one entity, or one intercompany allocation, from source record to posted entries. If that path depends on separate exports, side calculations, or spreadsheet-led cleanup journals, you are operating around the system rather than through it.

There is a timing tradeoff. Replacing too early can overbuy software, but waiting too long can lock in ongoing inefficiency. Once entity growth repeatedly pushes work outside the platform, treat that as migration planning territory.

- Sign 7: links between

Accounts Payable (AP),Enterprise Resource Planning (ERP), and payout systems are too fragile for current scale.

This usually shows up first as a trust problem: payout status, AP records, and ERP postings do not line up cleanly without manual intervention. That is the same failure pattern seen in disconnected legacy environments where visibility is limited and scale gets harder.

Check three recent cases: one failed payment, one corrected ERP sync, and one retry flow. Confirm whether one consistent transaction reference is traceable end to end across AP activity, payout processing, and ERP posting, with a clear final economic outcome. If you cannot prove that quickly from records and logs, architecture risk is already present.

A final warning sign is cost without confidence. In one ERP failure scenario, teams were still struggling eighteen months after go-live, with $400,000 implementation cost and consultant spend above $200,000. If your operation is trending in that direction, treat it as a replacement decision, not routine cleanup.

For a step-by-step walkthrough, see How to Handle Client-Paid Software Subscriptions in Your Bookkeeping.

Upgrade now or optimize first with three decision gates#

If architecture issues are already visible, use these three gates to decide timing: failing two is usually a move-now signal, while passing two supports a short, owner-led optimization sprint.

| Gate | What to review | Move-now signal |

|---|---|---|

| Control risk | Test one recent exception end to end: approval trail, source record, posted entry, and supporting supplier or tax record. | If finance still has to reconcile from inbox threads, screenshots, or side spreadsheets, optimization is likely too narrow. |

| Integration risk | Review three real cases: a failed payment, a corrected ERP sync, and a replayed event. | If ERP sync and Webhooks reliability are unstable, treat that as upgrade pressure. |

| Growth risk | If Global Payments or Multi-Entity Support is in your next planning cycle, upgrade before expansion. | Disconnected legacy systems, manual processes, and limited visibility usually get worse under growth, not better. |

-

Gate 1: control risk. If your

Financial ControlsorTax & Regulatory Compliancechecks are failing in live operations, treat that as structural, not just a training gap. Test one recent exception end to end: approval trail, source record, posted entry, and supporting supplier or tax record. If your finance team still has to reconcile from inbox threads, screenshots, or side spreadsheets, optimization is likely too narrow. -

Gate 2: integration risk. If

ERPsync andWebhooksreliability are unstable, treat that as upgrade pressure. Review three real cases: a failed payment, a corrected ERP sync, and a replayed event. The same transaction reference should carry from AP to payout status to final ERP entry, and retries should resolve to one economic outcome rather than creating a second action candidate. -

Gate 3: growth risk. If

Global PaymentsorMulti-Entity Supportis in your next planning cycle, upgrade before expansion. Disconnected legacy systems, manual processes, and limited visibility usually get worse under growth, not better. The risk is not theoretical: one cited ERP case was still struggling eighteen months after go-live despite a$400,000implementation and more than$200,000in consulting spend, and the cited range is that50-70%of ERP implementations fail to meet stated objectives.

Passing two gates does not mean "do nothing." It means run a tightly scoped optimization with named owners, validate it in the next close, and escalate to replacement if the evidence is still weak.

Best upgrade paths by platform profile#

Choose the path based on where exceptions start: invoice processing, payout-state complexity, or both. If your operation is still simple and centralized, a lighter AP-focused move can be enough. If complexity is rising, a modular path is usually safer than forcing everything into one replacement.

| Path | Best for | Key pros | Key cons | Concrete use case tied to payout complexity |

|---|---|---|---|---|

| 1. Stronger AP stack | Teams whose main pain is invoice capture, approvals, ERP posting, and close speed | AI-enabled AP tools are positioned to reduce manual handling, speed approvals, and reduce errors. In one cited view, 63% of teams spend more than 10 hours weekly on invoice processing. | This does not automatically fix payout-state complexity. Limited ERP integrations can still force manual entry and slow close. | A contractor platform paying approved invoices from one entity, where close delays come mainly from invoice handling. |

| 2. AP plus payout infrastructure | Platforms where finance, ops, and engineering all work the same payment exceptions | Brings approval, disbursement status, and reconciliation into a tighter operating flow. | Broader migration scope, with more end-to-end testing across AP, payouts, and ERP sync. | A creator or marketplace flow where approved payables still move through release, failure, reissue, and settlement states before close. |

| 3. Modular stack with Virtual Accounts and Payout Batches | Growing platforms that need to scale components without replacing everything at once | Modular design is commonly used to scale as complexity grows. | Your team owns more integration and reconciliation design across modules. | A platform running high-volume payout batches while separating programs or funds flows with virtual-account-style structures. |

| 4. Merchant of Record (MoR) overlay | Platforms facing commercial and payout-model complexity beyond AP workflow issues | Adds an overlay path when operating-model change is moving faster than internal tooling changes. | Adds a dependency and does not fix broken AP process design by itself. | A cross-border seller or creator model where transaction-model complexity is outpacing current payables setup. |

Use the same four operator checks for every path before you commit:

- Webhooks maturity: verify event catalog, retry behavior, replay handling, and finance-facing status visibility.

- Idempotency behavior: test whether retries or replays can create duplicate action candidates.

- Ledger Journals audit depth: confirm a trace from source record to approval to payout status to ERP entry.

- Supplier Management capability: check onboarding fields, status handling, and retained records for each payee or supplier.

If your main issue is manual invoice work and weak ERP integrations, do not overbuy. If your exception queue spans AP, payouts, and reconciliation, choose for the full transaction lifecycle.

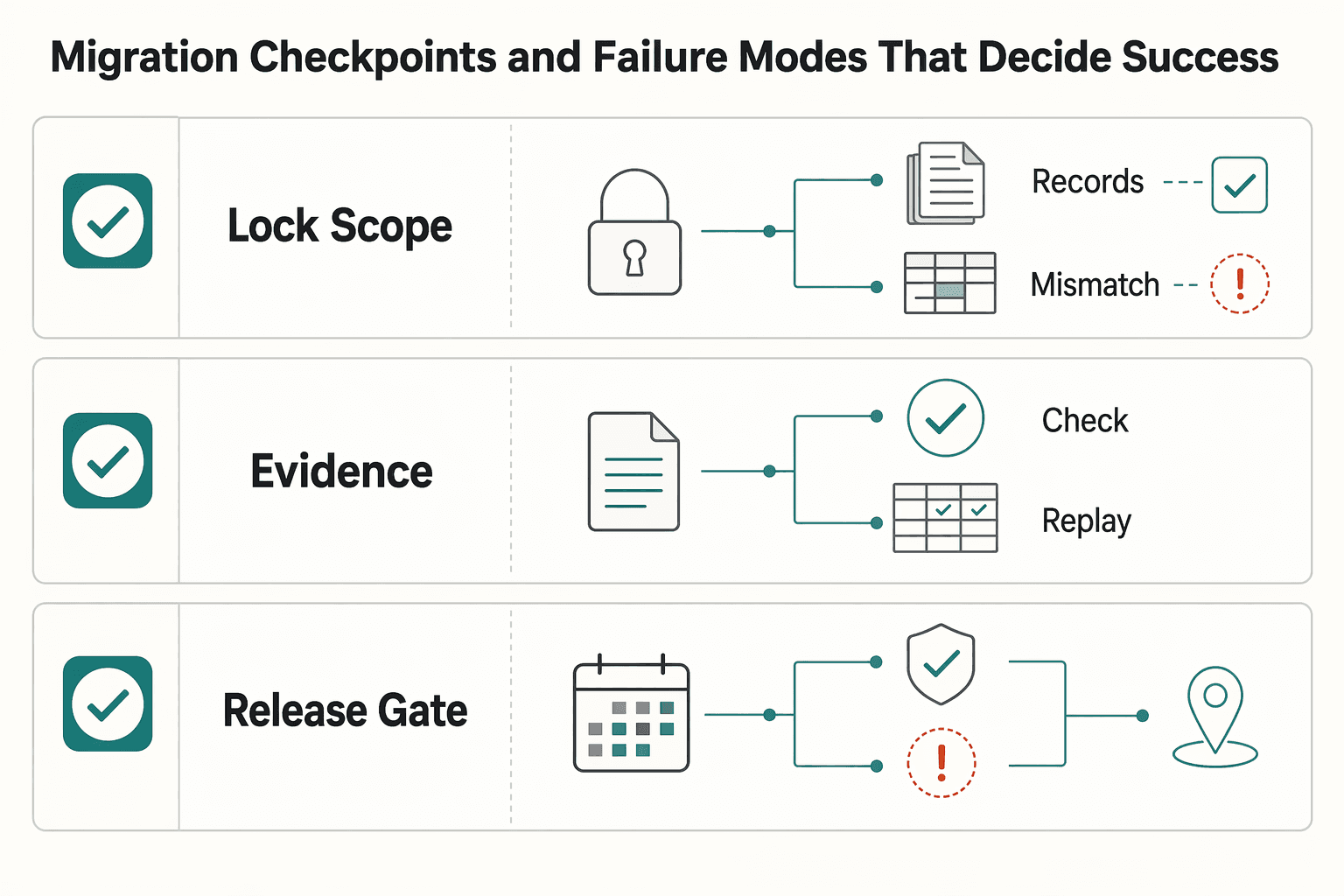

Migration checkpoints and failure modes that decide success#

Migration success is usually decided before go-live: if ownership, evidence, and rollback are not defined for each AP, payout, and ERP touchpoint, cutover risk is still high.

| Checkpoint | What to define | Failure mode |

|---|---|---|

| Lock scope and owners first | Define what is in phase 1 and what is out; assign one accountable owner each for finance, engineering, payments ops, and tax/compliance review. | Shared ownership across supplier onboarding, ERP posting, and payout status handling creates decision gaps during cutover. |

| Design integrations around evidence, not screens | Start from the records you must prove in Ledger Journals, then map APIs, Webhooks, and ERP posting from that evidence requirement. | A feature-rich UI with weak alignment to your close process just relocates reconciliation work. |

| Run parallel paths to build a go-live evidence pack | Compare old and new outputs on real cases before controlled cutover; build a pack with a control matrix, reconciliation proof from Ledger Journals, and named incident ownership by failure class. | Validating only happy-path transactions and missing exceptions that break traceability. |

| Set cutover gates and rollback triggers before launch day | Define stop conditions in advance and who can call rollback. | Deciding rollback in a live incident without pre-agreed thresholds or authority. |

| Test failure handling and document market caveats explicitly | Test retry/replay scenarios for Webhooks, Idempotency, and exception-queue ownership/response expectations; document KYC, KYB, AML, and payout coverage assumptions. | Undocumented assumptions that surface later as onboarding blocks, payout exceptions, or reconciliation cleanup. |

That framing matters. MIT Working Paper CISL# 2013-08 states that software is hard at small scale and even harder to engineer and manage at larger scale, so treat this as a large-scale change program, not a tool swap.

- Lock scope and owners first

Define what is in phase 1 and what is out. Assign one accountable owner each for finance, engineering, payments ops, and tax/compliance review, and tie every migration deliverable to one owner. Failure mode: shared ownership across supplier onboarding, ERP posting, and payout status handling creates decision gaps during cutover.

- Design integrations around evidence, not screens

Start from the records you must prove in Ledger Journals, then map APIs, Webhooks, and ERP posting from that evidence requirement. Keep one stable reference through the lifecycle so finance can trace source record to accounting entry. Failure mode: a feature-rich UI with weak alignment to your close process just relocates reconciliation work. Tool choice is an alignment decision, not only a feature decision.

- Run parallel paths to build a go-live evidence pack

Compare old and new outputs on real cases before controlled cutover. Build a pack with a control matrix, reconciliation proof from Ledger Journals, and named incident ownership by failure class. If your program uses them, include handling checkpoints for W-8, W-9, and Form 1099 artifacts in your own process. Failure mode: validating only happy-path transactions and missing exceptions that break traceability.

- Set cutover gates and rollback triggers before launch day

Define stop conditions in advance and who can call rollback. Keep the rule operational: if reconciliation evidence is not clear on representative traffic, pause expansion and stabilize first. Failure mode: deciding rollback in a live incident without pre-agreed thresholds or authority.

- Test failure handling and document market caveats explicitly

Before launch, test retry/replay scenarios in your own stack for Webhooks, Idempotency, and exception-queue ownership/response expectations. In parallel, document market and program assumptions, since KYC, KYB, AML, and payout coverage can vary by configuration and geography. Failure mode: undocumented assumptions that surface later as onboarding blocks, payout exceptions, or reconciliation cleanup.

Conclusion#

The right call is rarely just "buy new Accounts Payable (AP) software." It is choosing the lowest-risk way to fix three things at once: scale strain, control gaps, and reconciliation reliability. If you only solve one, the other two can resurface during close, vendor support, or the next expansion step.

- Decide from signals, not software age

A mature stack can still be the wrong fit, and an older one is not automatically broken. The useful rule is sign-based: if manual workarounds now carry core finance operations, you have probably outgrown the current tool even if it still works. Age alone is not the decision point. Your checkpoint is simple: trace one real invoice through approval, payment status, and accounting outcome without a spreadsheet bridge. If you cannot, stop debating features and treat fit as the issue.

- Use the three gates to lower execution risk

Warning signs help you spot trouble. The gates help you decide what to do next. If control risk and integration risk are both failing, consider moving now rather than spending another quarter polishing workarounds that only mask the limits. Delaying modernization can raise remediation cost and increase disruption risk later, especially once exceptions pile up across finance and engineering. Before approval, ask for a short evidence pack, not a longer vendor demo: sample transactions, visible status history, accounting outputs, owner list for incidents, and evidence that close can run without side files.

- Match AP decisions to the architecture you are becoming

This is where teams often misstep. A company moving from a simpler accounting setup toward broader Enterprise Resource Planning (ERP), more entities, or more payment complexity should not evaluate AP in isolation. The practical differentiator is fit with the business model you are building next, not just the invoice volume you have today. Evaluation criteria also change by company size, so a team in the 50 to 500 employee range should not buy like a 1 to 50 business, and a 500+ team should not expect entry-level tools to stretch indefinitely.

Outgrowing a tool does not mean it stopped functioning. It means the cost of keeping it may have shifted toward manual effort, weak visibility, and avoidable risk. If your payment complexity is expanding, align the AP decision with your broader accounting architecture before you commit, and make the go-or-no-go decision from observed signs, tested checkpoints, and real operating evidence.

Frequently Asked Questions

What breaks first when a platform has outgrown its AP software?

Usually it is visibility. Invoice and payment status starts getting tracked through email, chat, and spreadsheets, and AP turns into a coordination role instead of a processing function. That may hold at low volume, but one grounded warning is clear: as invoice counts grow, uncertainty grows with them.

When should we upgrade instead of optimizing our current `Accounts Payable (AP)` stack?

Upgrade when the gap between what the business needs and what the tool can deliver has become wide enough that people are compensating with manual workarounds. A strong signal is when your team is buried in spreadsheets and journal entries just to keep the books usable, especially if the current tool is effectively acting like an entry-level accounting system for a business that no longer is. If you are still fixing edge cases with process changes alone, optimize first. If the process now depends on side spreadsheets every close, move.

Which `Financial Controls` are non-negotiable before scaling `Global Payments`?

From this evidence set, the core non-negotiables are clear ownership and reliable status visibility that do not depend on informal tracking. If AP staff spend more time chasing answers than processing transactions, controls are already strained. This grounding does not define a specific global-payments control checklist.

How do we evaluate true `Multi-Entity Support` without overbuying?

Start with your actual structure, not the vendor demo. If you already have multiple entities and still rely on manual financial consolidation, basic accounting tooling is likely the constraint, and that is the specific capability to test first. If you only operate one entity today and have no near-term change, do not buy for hypothetical complexity. If entity count is already growing, make consolidated reporting and inter-entity handling part of the evaluation.

What should we verify between `ERP`, `Webhooks`, and payout systems before cutover?

This grounding does not provide a webhook or cutover checklist. The practical check here is whether AP and accounting outcomes can be reconciled without spreadsheet bridges or heavy manual journal-entry cleanup. If mismatches are mostly resolved through ad hoc coordination, cutover is likely early.

What proof should finance and engineering require before final migration approval?

Ask for proof from real operating work, not just demos: invoice status is visible without informal tracking, and accounting outputs no longer depend on spreadsheet or journal-entry workarounds. For teams already seeing these signs, reducing coordination overhead matters more than adding features.

Try a related tool

Avery writes for operators who care about clean books: reconciliation habits, payout workflows, and the systems that prevent month-end chaos when money crosses borders.

Sources

Includes 1 external source outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

When Platforms Should Move to Payment Orchestration and Multi-Gateway Routing

Payment orchestration can become a practical priority when payment performance and finance operations start limiting growth, not just checkout delivery. A single PSP can be the right setup for a long time. But once approval paths, provider constraints, or reconciliation workload start affecting outcomes, you need a clearer strategy than adding providers ad hoc.

How to Handle Mid-Cycle Upgrades and Downgrades Without Double-Charging Customers

Mid-cycle upgrades, downgrades, and prorated billing stay clean when you pick one timing model and follow it all the way through. The hard part is not the arithmetic. It is choosing one control path for invoice timing, event handling, and customer communication, then using it consistently enough that one plan change does not turn into two charges or a charge plus a stray credit.

SaaS Accounting Software Evaluation: What Payment Platforms Need Beyond Standard GL Features

Choosing accounting software for a payment platform is a controls and integration decision first, not just a General Ledger feature comparison. If your product depends on recurring billing, payment collection, and reporting, a tool that looks complete at the GL surface can still leave rollout gaps. Revenue treatment and exception handling should be tested early.