Quick Answer

Start with a strict three-record match: Internal Ledger or order data, PSP transaction and payout records, and the receiving statement line. Multi-psp settlement reconciliation works when every posted bundle includes stable join keys, a defined exception policy, and reproducible evidence (raw extract, transformed file, approval record, ERP confirmation). Decompose payouts before GL posting, then block identity and amount breaks while carrying timing-only items with owner, rationale, and date.

Multi-PSP settlement reconciliation without month-end fire drills#

Multi-PSP settlement reconciliation gets easier when you run it like a close discipline, not a reporting exercise. If you use multiple payment providers in parallel, the goal is not a prettier dashboard. It is a faster, cleaner close that finance, ops, and engineering can all verify from source evidence.

Step 1. Confirm that this guide fits your operating reality. This guide is for platform teams working across more than one Payment Service Provider, market, currency, or legal entity. If you have one PSP, one settlement currency, and one payout account, you still need controls, but the reconciliation burden is usually smaller. Once you add multiple providers, the problem stops being just integration work. Operational complexity rises quickly, and different currency support can create close friction before you even get to fees or disputes.

Use one simple checkpoint at the start: list every PSP that can move customer money into a payout or bank deposit today. If your active providers do not all appear in one inventory with their payout destinations, you do not have the baseline for a reliable close yet.

Step 2. Anchor the promise in records that each team can verify. The core promise is straightforward: match your order data to PSP activity, then match that activity to cash movement. In practice, you need one traceable chain from your internal order or ledger record, to the processor-side transaction and settlement record, to the deposit line on a bank statement or equivalent cash account.

That shared trace matters because each team validates a different link. Finance needs posting logic it can defend. Payments ops needs to explain fees, disputes, holds, and timing gaps. Engineering needs to prove which raw file, API extract, or event produced the reconciled line. If one paid order cannot be traced through order ID, PSP transaction ID, payout or settlement reference, and bank statement reference, your month-end problem is already visible.

Step 3. Keep the scope practical, auditable, and narrow enough to execute. This guide stays focused on close operations: decision checkpoints, posting readiness, exception handling, and recovery paths when references break or files arrive late. It is not a vendor comparison, and it does not rely on unverified performance claims. The emphasis stays on evidence you can actually review: raw PSP exports, transformed reconciliation files, bank statement lines, approval records, and ERP posting confirmations.

One early red flag is teams arguing about totals because they are comparing the wrong layer. Merchant processing activity is about settlement, not just customer checkout events. A payout may not equal same-day sales because fees, adjustments, reversals, disputes, and currency timing can affect settlement. If your close still depends on someone "knowing what usually happens" in a PSP dashboard, expect fire drills later.

If you want a deeper dive, read Month-End Close Checklist for Payment Platforms: Reconciling PSP Settlements Bank Statements and Ledger.

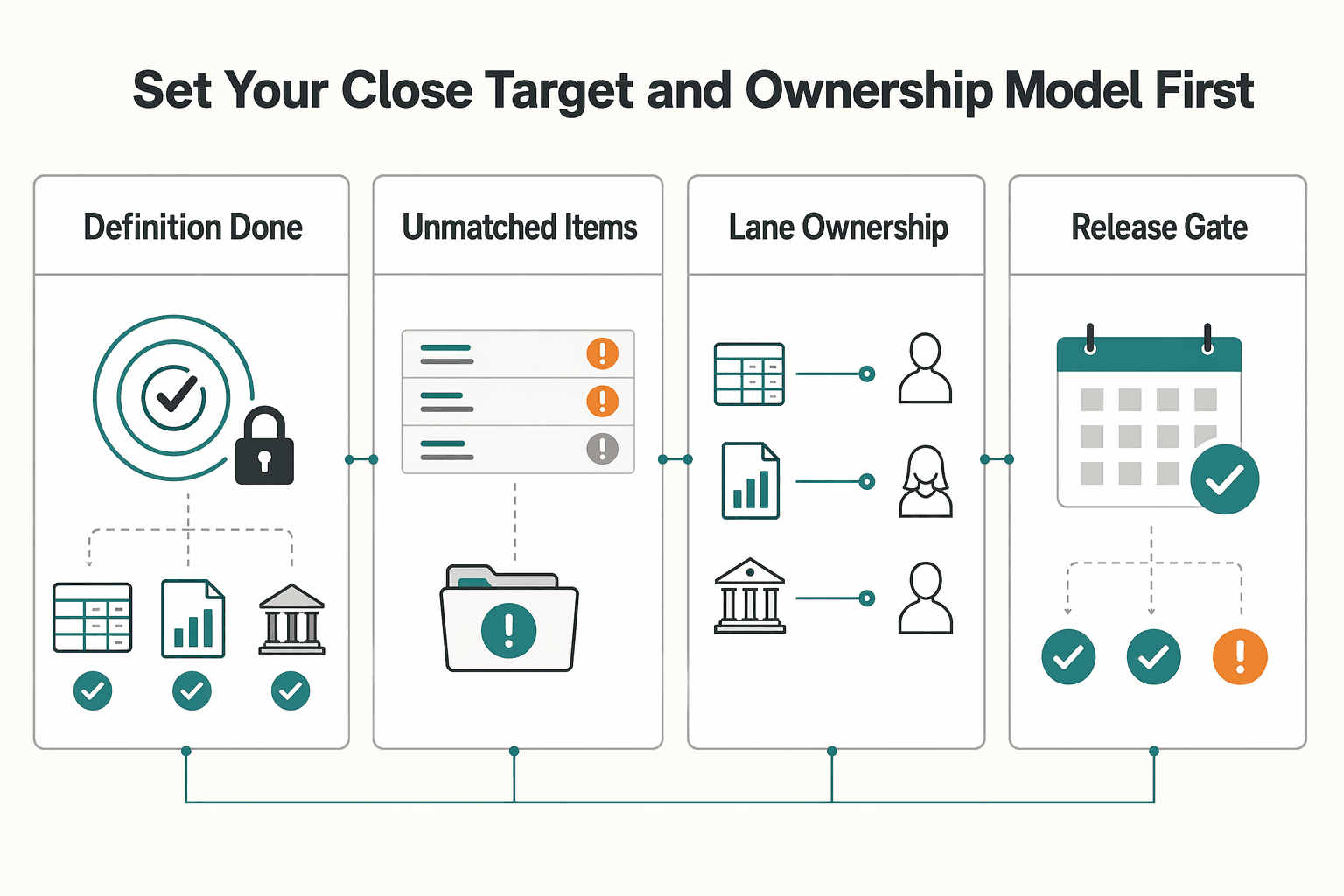

Set your close target and ownership model first#

Set your close target and ownership model before the cycle starts, or reconciliation decisions will drift during month-end.

| Close setup item | What to define |

|---|---|

| Definition of done | What counts as matched across your Internal Ledger, PSP reports, and Bank Statement |

| Unmatched items | How unmatched items are carried as explicit exceptions |

| Lane ownership | Finance owns GL posting rules and ERP posting outcomes; Payments Ops owns PSP exception triage; Engineering owns source completeness and ingestion integrity |

| Approval gates | Who reviews exceptions, who can approve a carry, and who can override unmatched items, including the conditions |

Step 1. Lock one definition of done. Pick one baseline method for this close cycle and document it up front. If you use a 3-way model, define what counts as matched across your Internal Ledger, PSP reports, and Bank Statement, and define how unmatched items are carried as explicit exceptions. Keep the criteria and exception support location written and shared before execution starts.

Step 2. Name one owner for each lane. Use explicit lane ownership so planning, monitoring, and coordination are clear in practice. A workable split is Finance owning GL posting rules and ERP posting outcomes, Payments Ops owning PSP exception triage, and Engineering owning source completeness and ingestion integrity. Avoid dual ownership of the same mismatch, because unresolved items tend to survive into posting.

Step 3. Set approval gates before posting. Decide in advance who reviews exceptions, who can approve a carry, and who can override unmatched items, including the conditions. Use a consistent evidence pack each time: PSP export or API extract, related Internal Ledger entry, Bank Statement line (or documented missing-cash note), and ERP approval record. If that chain is not quickly traceable, tighten the gate before close.

This matters even more across countries, where processor complexity plus country-specific regulation and data-security requirements raise execution risk when ownership is vague.

For a step-by-step walkthrough, see How to Handle Multi-Party Payments: Splitting a Single Transaction Across Multiple Recipients.

Prepare the data and controls before your first clean close#

Before you try to speed up close, make the data boring first: stable IDs, one cutoff rule, and documented status signals prevent most month-end noise.

Step 1. Build a source inventory by PSP and region. Create one inventory for Stripe, Adyen, PayPal, Redsys, Checkout, and Shopify across your active regions (for example North America, Europe, and LATAM). For each entry, record the source record, owner, legal entity, settlement currency, and expected bank account or Bank Statement destination.

For PayPal, record the exact fee page and its update date by market instead of using one global assumption:

| PayPal page | Last updated |

|---|---|

| US consumer fees | February 19, 2026 |

| US merchant fees | February 9, 2026 |

| Iceland consumer fees | 21, April 2025 |

Also keep market context explicit: PayPal defines "Domestic" and "International" by whether parties are in the same market or different markets.

Step 2. Confirm key mappings before automation. Lock your join keys early: order ID, PSP transaction ID, payout ID, currency, legal entity, settlement date, and Bank Statement reference. If any key is missing, treat it as a setup gap, not a reconciliation exception.

Stripe pricing shows why this matters: standard pricing is pay-as-you-go, and additional fees can apply for manually entered cards (0.5%), international cards (1.5%), and currency conversion (1%). If your mapping does not preserve the attributes behind those differences, net settlement variance will be harder to explain at close.

Step 3. Verify compliance status signals that explain timing gaps. Do not infer KYC, KYB, or AML timing rules from policy text. Do require a reliable status field or evidence note when a hold or review affects expected cash movement, so Finance can classify the item correctly.

Step 4. Fix one reconciliation grain and one cutoff standard. Choose daily bundles or intraday matching before the first live close, then enforce one timezone and one cutoff rule across PSP exports and ERP loads. If intraday references are not consistently reliable yet, start with daily bundles and validate a full day from order to payout to Bank Statement before posting.

We covered this in detail in How to Reconcile Multi-Currency Payouts Across Multiple PSPs in One Ledger.

Build a canonical order to PSP to cash mapping model#

Once IDs and cutoffs are stable, do not post from payout totals alone. Build one chain from sales order to PSP event to settlement component to bank cash, and carry that chain into Internal Ledger and GL-ready lines.

Step 1. Define one canonical grain before you map any provider. Use one row logic everywhere: one commercial event, one PSP transaction, one settlement component, one cash outcome. An order can fan out into several lines, but each line should keep the same core join set: order ID, PSP transaction ID, payout or batch ID, currency, legal entity, settlement date, and Bank Statement reference when available. If you skip the component layer and jump from order to net deposit, you lose the reason the math changed.

Your Internal Ledger should answer two questions without manual reconstruction: what happened commercially, and why the bank received that exact amount.

Step 2. Split every payout into posting components before you touch the GL. At minimum, decompose into gross, provider fee, commission, retention, chargeback, adjustment, and net cash. Treat these as separate accounting lines, not memo text on one net line. PayPal US Merchant Fees (Last Updated: February 9, 2026) lists Chargeback Fees, Dispute Fees, and Currency Conversions separately, which is a practical reminder that "fees" are not one bucket.

Stripe shows the same issue in pricing: 2.9% + 30¢ per successful domestic card transaction, plus 0.5% for manually entered cards, 1.5% for international cards, and 1% if currency conversion is required. If your transformed file does not preserve those drivers, similar gross amounts can still produce different net settlement lines.

| PSP | What to record for payout cadence | Reference fields to preserve | Mismatch pattern to normalize |

|---|---|---|---|

| Stripe | Record the actual cadence configured for that account/market | PSP transaction, payout ID, settlement date, currency, bank reference | Add-on pricing drivers can change net outcomes for similar gross amounts |

| Adyen | Record the contracted cadence for the relevant account/entity | PSP transaction, payout or batch ID, settlement date, currency, bank reference | Normalize non-sales and timing components before comparing to order totals |

| PayPal | Record cadence by active market/entity and the fee page version reviewed | PSP transaction, payout or batch ID, settlement date, currency, bank reference, market context | Keep chargeback, dispute, and currency conversion lines separate |

| Redsys | Record the active cadence for the relevant country/entity setup | PSP transaction, settlement or batch ID, settlement date, currency, bank reference | Normalize provider/bank formatting differences before matching |

Step 3. Set hard timing rules for open, escalate, or accrue decisions. Keep an item open when identity is intact and the gap is timing only. Escalate when amounts do not reconcile, key identifiers are missing, or no status signal explains the delay. Accrue only timing items with documented rationale and Finance sign-off.

For PayPal, treat domestic vs. international context carefully: the consumer fee definition ties international transactions to sender/receiver residency in different markets, so market context should be explicit in your rationale when it affects interpretation.

Step 4. Attach an evidence pack to every bundle and make it reproducible. For each posted bundle, keep four artifacts together: raw PSP file/API extract, transformed reconciliation file, approval record, and ERP posting confirmation. The checkpoint is reproducibility: another reviewer should be able to rerun the bundle and reach the same posting result.

You might also find this useful: 3-Way Reconciliation Explained: PSP Ledger vs. Internal Ledger vs. Bank Statement.

Choose your consolidation approach based on constraints not preference#

From the material here, you cannot make a supported choice between Payment Orchestration data unification and EMI payout routing yet. The only evidence in scope is UK Self Assessment registration guidance, which does not provide evidence for payments-consolidation tradeoffs.

Before selecting a path, require documented evidence for each PSP and legal entity: payout destination rules, settlement currencies, payout currencies, account-holder validation requirements, and statement reference fields. Keep the same join keys from the previous section so the close remains testable: PSP transaction ID, payout or batch ID, currency, legal entity, settlement date, and Bank Statement reference when available.

If that evidence is incomplete, keep the decision open instead of forcing a consolidation direction. Proceed only when you can prove an end-to-end match from source payout data to receiving statement lines and posting artifacts for a pilot bundle.

Related: What Is Payment Orchestration? How Platforms Route Transactions Across Multiple PSPs.

Execute the daily close sequence with posting gates#

Once mapping is stable, run the same close sequence every day and treat it as a control, not a preference. The goal is a close you can rerun and explain before you post.

Run intake in one order and keep it fixed#

Use one documented order for each bundle: ingest orders, ingest PSP transactions, ingest deposits, auto-match, route exceptions, approve, then post to ERP. In payment flows, data and funds move through messaging, clearing, and settlement, so loading deposits before the underlying transaction records often creates avoidable noise.

Before you auto-match, confirm each intake file is in scope for the intended settlement date, legal entity, and currency. Confirm the join-critical fields are present and usable, including account identifiers, amount, currency, date, and reference numbers. If a deposit arrives but its corresponding PSP extract is missing, hold that bundle instead of forcing a partial match.

Gate every bundle before posting#

Define three posting gates and apply them to every bundle: your internal match-rate threshold, no unresolved high-risk exceptions, and reviewer sign-off with timestamp. Record all three on the approval record each time.

Treat missing identity fields, amount breaks, duplicates, and legal-entity mismatches as post-blocking until resolved or explicitly carried with ownership. Keep the same approval evidence set for each bundle: raw PSP file or API extract, transformed reconciliation file, approval record, and ERP posting confirmation.

Reprocess safely and publish daily status#

Assume late files and webhook retries will happen. Reprocessing should update the existing bundle identity rather than create duplicate GL impact.

Publish one daily status view by PSP and currency with four states: matched, unmatched, pending, and blocked. That keeps Finance, Payments Ops, and Engineering aligned on what can post now and where intervention is required. Related reading: Invoice Settlement for Platforms That Match Payouts and Close Disputes.

Triage exceptions with a signal-to-action matrix#

Use one signal-to-action matrix so detection leads to a consistent next step, owner, and communication path instead of case-by-case debate.

Classify by operational signal, not ad hoc labels#

Start triage from incident-management signals you can apply every time: what was detected, who is involved, how severe it is for today's close, and whether external communication is needed. This keeps routing consistent and auditable.

| Signal | What to decide immediately | Required output |

|---|---|---|

| Detection signal | Whether the item is an incident for this close cycle | Incident record with timestamp |

| Actors involved | Which team owns investigation and resolution | Named owner |

| Severity for close | Whether to pause posting or continue with controls | Posting decision + rationale |

| Communication need | Whether external communication is required | Communication action or explicit "not required" |

| Recurrence pattern | Whether this is a repeat issue | Problem-management candidate flag |

Route incidents with explicit ownership#

Assign ownership at detection, then route by severity using the same matrix every day. The TARGET participant guide (R2025.OCT) frames incident management around detection, actors, and external communication, which is the right discipline for reconciliation triage.

Convert repeats into problem management work#

Keep a recovery log tied to your Internal Ledger and Bank Statement evidence so repeat failures are visible, not buried in daily commentary. When patterns repeat, move them into problem management and change/release/deployment work rather than treating them as permanent manual exceptions.

Control cross-border and compliance friction before it delays close#

Treat cross-border policy uncertainty as a close risk, not a timing placeholder. If tax scope is unclear for a flow, route it for policy review instead of leaving it in a generic reconciliation queue.

Separate tax-scope decisions from reconciliation mechanics#

In your close policy, require one explicit check per cross-border flow: can the analyst identify the applicable VAT treatment for that flow? If not, escalate before posting decisions are finalized.

For EU cross-border B2C e-commerce, record that VAT rules changed on 1 July 2021. If eligible, online sellers and marketplaces can use the One Stop Shop (OSS) to register in one single Member State (the Member State of identification) for VAT declaration and payment scope.

Make OSS governance explicit in close controls#

If your business is near or above the EUR 10 000 EU-wide threshold, document:

| Control point | What to note |

|---|---|

| EU-wide threshold | Near or above the EUR 10 000 threshold |

| OSS usage | Whether OSS is used |

| Filing entity | Which legal entity owns the filing |

| Member State of identification | Which Member State is the Member State of identification |

| Responsibility owner | Who owns registration, declaration/payment, and record-keeping/audit responsibilities |

| Binding period | Binding for the calendar year of the decision plus the next two calendar years |

If you choose the Member State under the Union scheme, note that the choice is binding for the calendar year of the decision plus the next two calendar years.

Escalate complex cross-border VAT treatment early#

When VAT treatment is complex or unclear, use VAT Cross-border Rulings (CBR) as an advance-ruling path rather than improvising classification during close.

Keep one caveat explicit in the policy: coverage and operational detail vary by market, program, and provider configuration, so controls must follow your documented scope. This pairs well with our guide on Account Reconciliation for Payment Platforms: How to Automate the Match Between Payouts and GL Entries.

Use this checklist to close faster with fewer surprises#

Use this order to keep close moving: completeness, mapping, exceptions, compliance impact, approval evidence, then summary.

| Checklist item | Key points |

|---|---|

| Confirm source completeness | Load Internal Ledger orders, PSP transaction and payout activity, and bank or EMI statement lines; keep a source file or API extract, load timestamp, and date or cutoff basis |

| Validate mapping integrity | Sample matched items across each provider for order ID, PSP transaction ID, payout reference, currency, and legal entity |

| Review the exception matrix | Missing IDs, duplicate events, unexplained amount deltas, and unclear entity or currency context should block posting |

| Verify the compliance impact queue | Review KYC, KYB, and AML holds for payout-timing impact and mark the bundle as pending due to compliance timing when a hold delays release |

| Approve bundle postings with an audit trail | Approval record should show who approved, when, and which evidence pack was reviewed |

| Publish a close summary before moving on | List open risks, unresolved items, and next-cycle owners |

- Confirm source completeness.

For each PSP and settlement currency, load all three records: Internal Ledger orders, PSP transaction and payout activity, and bank or EMI statement lines. Make sure every expected payout bundle has a source file or API extract, a load timestamp, and a clear date or cutoff basis. If a payment is approved but cash is not yet in the account, do not assume ingestion failed. Approved payments can take days to appear in the bank as part of settlement timing.

- Validate mapping integrity.

Before checking totals, confirm IDs link from PSP records to your Internal Ledger and then to ERP posting lines. Sample matched items across each provider for order ID, PSP transaction ID, payout reference, currency, and legal entity. Do not call a bundle matched just because net cash looks right if key identifiers are missing or guessed.

- Review the exception matrix.

Separate blockers from carry items and document the reason for each. Missing IDs, duplicate events, unexplained amount deltas, and unclear entity or currency context should block posting. Carry timing-only gaps only with an owner, dated rationale, and attached PSP and statement evidence. Treat chargebacks explicitly: they are transaction reversals initiated when a cardholder disputes a charge, and once they hit, funds can be pulled quickly and deadlines start immediately.

- Verify the compliance impact queue.

Review KYC, KYB, and AML holds for payout-timing impact, not just operational status. If a hold delays release, mark the bundle as pending due to compliance timing, not as a broken reconciliation item. Do not leave compliance delays in unmatched queues without notes, or they will repeat next close.

- Approve bundle postings with an audit trail.

Do not post in ERP based on verbal confirmation or screenshots. The approval record should show who approved, when, and which evidence pack was reviewed (PSP extract, transformed recon file, statement support, and posting reference). For dispute-heavy bundles, include dispute status and related fees, because fees can continue accumulating even when you win in the end.

- Publish a close summary before moving on.

End with one report listing open risks, unresolved items, and next-cycle owners. Tie each open item to the missing evidence or action needed, such as a late bank line, a mapping defect, or a dispute outcome not yet linked to settlement and fees. Linking dispute outcomes to settlements and fees helps Finance close faster.

Want a quick next step? Try the free invoice generator.

Frequently Asked Questions

What is multi-PSP settlement reconciliation in practical terms for a platform finance team?

It is the process of proving that one sale can be followed from your internal order or ledger, to the PSP activity that processed it, to the actual cash line that landed in your bank or EMI account. In practice, Finance is not just checking deposits. You are validating gross, fees, adjustments, and net cash with enough evidence to post or deliberately carry an item.

What are the three records we must match every day to run true 3-Way Reconciliation?

Match your Internal Ledger or order record, the PSP record, and the Bank Statement or EMI statement cash movement. The daily check is simple: can you trace the same economic event through order ID, PSP transaction or payout reference, and statement reference without guessing? If one of those keys is missing, do not call it matched.

Why does one PSP payout rarely equal the sum of same-day customer sales?

Because payouts are often net of fees, and provider fee schedules can also include separate treatment for disputes, chargebacks, and currency conversion. Provider pricing also varies by payment type and geography. Stripe lists 2.9% + 30¢ for domestic cards, plus 1.5% for international cards and 1% if currency conversion is required, and PayPal shows different headline rates for card processing, PayPal or Venmo, and Pay Later. A common failure mode is comparing same-day sales gross to same-day bank cash net and treating the delta as a data defect.

When should we choose Payment Orchestration over routing to a Multi-Currency EMI Account?

Choose orchestration first when your bigger problem is fragmented data, inconsistent references, or weak visibility across PSPs. If you still cannot normalize order IDs, fee components, and payout references, changing the payout destination will not fix close. Choose EMI routing only when payout endpoints can actually be centralized cleanly and you can still preserve audit traceability.

What conditions must be true before routing Stripe, Adyen, and PayPal payouts into one UK EMI Account?

These fee excerpts do not establish universal eligibility conditions for routing Stripe, Adyen, and PayPal payouts into one UK EMI account. Treat eligibility as provider- and program-specific, and get direct confirmation from each provider for your entity and settlement currencies before centralizing cash.

Which exceptions should block GL posting versus be carried to the next close cycle?

Block posting for identity breaks and amount-integrity issues. That includes missing order or PSP IDs, duplicate events, unexplained amount deltas, and unclear legal entity or currency context. Carry only timing-only items, such as a known payout lag or a late bank line, and only with dated evidence, owner, and rationale attached. If the reviewer cannot explain the variance from raw PSP extract plus statement evidence, it should not post.

Where can FX still hit P&L even after we centralize payout destinations?

FX can still appear anywhere settlement currency, payout currency, and bank statement currency do not match. Stripe explicitly charges 1% when currency conversion is required, and PayPal's fee materials also note that exchange rates or card issuer or bank fees may still apply. The red flag is assuming one UK account removes all currency effects. It only changes where you see them.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- azjlbc.gov/budget/27baselinesinglefile.pdftrusted

- comptroller.war.gov/Portals/45/Documents/defbudget/FY2026/budget...trusted

- ecb.europa.eu/paym/target/consolidation/profuse/shared/pdf...trusted

- icc.illinois.gov/docket/P2023-0082/documents/332931/files/579...trusted

- in.gov/fssa/ompp/files/Anthem124060-010.pdftrusted

- irs.gov/irm/part4/irm_04-001-001trusted

- lf.prospertx.gov/WebLink/DocView.aspxtrusted

- michigan.gov/dtmb/-/media/Project/Websites/dtmb/Procureme...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Month-End Close for Payment Platforms with PSP Settlement Control

Month-end close often breaks down when PSP settlement is treated as a side reconciliation. For payment platforms, settlement is often the clearest record of what cash should have moved, so it should drive the close rather than being checked after journals are drafted. If you run close across multiple PSPs, you need that settlement record to lead the review before your team starts defending journal entries.

What Is Payment Orchestration? How Platforms Route Transactions Across Multiple PSPs

**When orchestration starts to matter** Payment orchestration usually starts to matter when you operate across regions and customer payment preferences, and a single-PSP setup becomes harder to manage cleanly. At that point, you are not just adding another gateway or acquirer. You are coordinating multiple PSPs, routing rules, retries, and failure paths while keeping reconciliation in the flow. A [payment orchestration platform](https://stripe.com/resources/more/what-is-payment-orchestration-what-businesses-need-to-know) is the control layer that centralizes gateways, processors, acquirers, and related providers. It keeps your team from managing each integration in a different way.

3-Way Reconciliation Explained: PSP Ledger vs. Internal Ledger vs. Bank Statement

For platform finance and payments ops teams, 3-way reconciliation is an operating discipline, not a vocabulary exercise. The job is to prove the same money movement across three records built for different purposes: the PSP ledger, your internal ledger, and the bank statement.