Quick Answer

Start by matching payout design to your current fleet load, not your future roadmap. In U.S. shared bikes and e-scooters, more than 133 million trips in 2023 means small record mismatches scale quickly. Set one hard daily checkpoint: each closed ride, refund, manual credit, and partner adjustment must map to a single finance reference. Add dual-PSP routing or split logic only after that check stays clean.

Where Micromobility Fleet Payouts Get Complicated#

The real payout challenges in scooter and bike-share platforms often start before money ever reaches a payout rail. In shared micromobility, failures can begin when operating events and finance records stop matching. Rides can close late, credits can post without clear references, or partner obligations can sit outside the same transaction view.

- Why this category is different

Shared micromobility covers small, lightweight human-powered or electric vehicles operated at low speeds, including shared e-scooters and bikeshare systems. It is no longer a niche edge case. The U.S. Department of Transportation says riders took more than 133 million trips on shared bikes and e-scooters in 2023, up 17% since 2022 and nearly 10-fold higher than 2013. At that scale, even a small gap between ride events and finance events can quickly turn into settlement noise. The defining constraint is density: most trips are only 15 minutes and average 1.5 miles, so your payout logic depends on high-volume event accuracy rather than a few large transactions.

- Where payout failures actually start

In bike-sharing and shared e-scooters, a common break point is ops and finance drift across station-based or dockless systems, support adjustments, fleet servicing, and city-specific partner arrangements. One warning matters here: micromobility merchants can face challenges with real-time data sharing, and that directly affects transaction tracking and financial transparency. A practical checkpoint is simple: by end of day, you should be able to trace each closed ride, refund, manual credit, and partner-impacting adjustment to a matching finance record with one consistent reference. If you cannot do that today, adding payout complexity will amplify the problem instead of solving it.

- What this article will help you choose

This is a decision guide for founders, finance leads, ops owners, and engineering teams choosing an operating model, not generic PSP advice. The recommendation is straightforward: pick the payout setup that fits your current fleet shape, then lock down controls for transaction tracking, exception handling, and financial transparency before expansion creates noise you can no longer isolate. PSP partnerships matter here, but only when your internal evidence pack is credible: ride IDs, adjustment reasons, payout state changes, and clear ownership for exceptions. If your city launch pace is outrunning your ability to verify those records daily, slow the payout design down and fix traceability first.

Shared bike and e-scooter systems are an increasingly common and important part of transportation. That is why payout operations need to be treated as an operating discipline, not just a payments integration task.

For a step-by-step walkthrough, see How MoR Platforms Split Payments Between Platform and Contractor.

How to choose the right payout setup for your fleet stage#

Choose the simplest payout setup that matches your current operating load and that your team can reconcile every day. If you run shared micromobility services with multi-party payouts, city-by-city policy review, or recurring rider charges from Pay-as-you-go and Subscription billing, prioritize control and traceability over feature count. Overhead is already high in this category, so extra payout complexity should earn its keep.

- For operators with real city-by-city pressure

This section is for teams dealing with different local expectations across jurisdictions. Treat local feasibility documents carefully: the Flagstaff micromobility share feasibility report states it "does not constitute a standard, specification, or regulation." If you treat every local memo as binding, you risk overbuilding controls in some cities and missing the true approval gates in others.

- Not for teams still proving demand

If you are still handling a small set of manual payouts and do not yet have dependable recurring rider volume, keep your setup lightweight. A May 2026 shared-micromobility study highlights that only 18% of income-qualified respondents enrolled in discount ride programs, and that knowledge was the main barrier. The practical takeaway is to avoid locking in a heavy payout stack before demand patterns are clear.

- Choose on four criteria, not feature count

Compare options on onboarding friction, control depth, reconciliation burden, and failure isolation across PSPs and your internal systems. In practice, early payout issues usually come from traceability gaps, not missing features. If a payout fails, you should be able to isolate whether the break came from merchant onboarding, an internal status mismatch, or the provider.

- Set non-negotiables before selecting anything

Assign clear owners for merchant onboarding, payout approvals, and escalation. Keep a minimum evidence pack for exceptions: ride ID, adjustment reason, provider reference, payout state timestamps, and the related ticket or case ID. If your team cannot review that pack consistently, do not add a more complex model yet.

If cross-border payouts are part of your model, How to Hedge FX Risk on a Global Payout Platform covers the FX side in more detail.

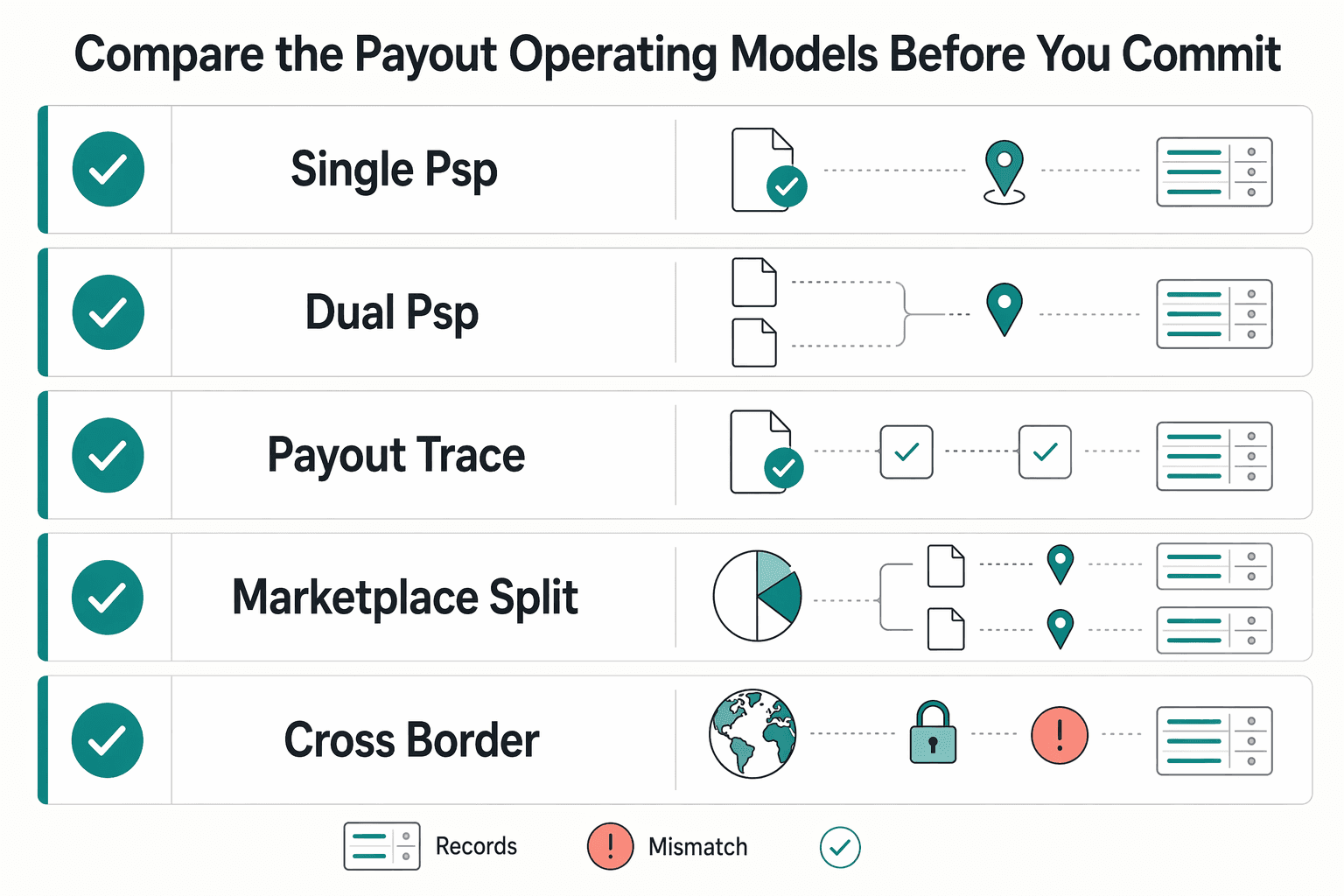

Compare the payout operating models before you commit#

Choose the model that gives you dependable reconciliation and a clear audit trail at your current operating load, then add complexity only when your controls can absorb it.

Shared e-scooters and e-bikes are typically privately operated and city-regulated, so payout operations need to remain explainable across market-by-market differences. In practice, the break usually happens when payment service provider states, ride events, and finance records stop matching.

| Model | Best for | Control level | Implementation load | Main failure mode | Recovery speed |

|---|---|---|---|---|---|

| Single-PSP integrated stack | Teams prioritizing fast launch with one provider | Low to medium | Low | Concentrated dependency on one PSP and weak visibility when provider and internal states diverge | Fast for minor PSP issues, slow when the provider path is blocked |

| Dual-PSP routing | Teams that need provider-level redundancy across markets | Medium to high | High | State normalization drift across PSPs, causing mismatched statuses and exception handling overhead | Faster for single-provider outages, slower if internal routing/reporting is not normalized |

| Internal ledger with external rails | Teams that need one canonical internal record before money moves | High | High | Ledger/event design gaps create internal uncertainty during exceptions | Moderate to fast with clean events; slow if records are incomplete |

| Marketplace split-routing | Fleets with partner payouts or revenue-share splits | High | Medium to high | Split edge cases (adjustments, clawbacks, partial reversals) create manual review load | Moderate; clearer logic helps, but edge cases still take time |

| Cross-border managed payouts | Platforms paying international operators or contractors | Medium to high | Medium to high | Document/compliance holds delay release after operational work is complete | Slower early, steadier once document workflows are reliable |

Use these decision rules when options are close:

- If city expansion speed is higher than finance headcount growth, favor models with stronger reconciliation workflows and audit trail support.

- If you cannot review exceptions daily, avoid dual-PSP routing until you can maintain one normalized view across providers.

- If partner economics change often, keep split logic in your own records instead of ad hoc provider metadata.

- If cross-border volume is rising, prioritize models that make document completeness visible before approval.

There is no reliable public benchmark here for payout SLA variance or provider-level failure rates in scooter-sharing. The June 2025 shared micromobility research is useful for integration pillars (operating concept, physical/digital/tariff integration, communication), but not for payout reliability comparisons. Treat vendor reliability claims as unverified until your own logs show failure isolation, retry behavior, and recovery time in your environment.

Best for early-stage city operators with tight teams#

For one-country scooter-sharing or bike-sharing operators with mostly Pay-as-you-go rides and limited payout edge cases, start with a single integrated payout setup. You want one auditable money trail working end to end before city expansion increases exception volume.

This keeps early operations focused: one payment partner path, one internal product surface, and fewer moving parts to reconcile across teams. It does not maximize customization, but it can reduce avoidable complexity while your operating model is still narrow.

Seattle's rollout context reinforces the point. Seattle is described as an early regulator of ride-hailing and dockless bikeshare, and SDOT created the New Mobility Playbook in 2017. In practice, city-by-city operations already shift quickly, so adding payout-layer complexity too early can make finance and support harder to run.

Use this model when:

- rider revenue is mostly Pay-as-you-go, not a heavy mix of memberships, credits, and partner-funded rides

- partner payouts are limited, with a small number of exceptions

- finance needs dependable daily reconciliation more than routing flexibility

Before go-live, make one checkpoint non-negotiable: every payout or adjustment record should tie back to a ride ID or settlement batch, a provider reference, an internal status timestamp, and an exception owner. Then test three failure cases before launch: one failed payout, one refund after settlement, and one manual ops credit.

Move beyond this setup when exceptions stop getting reviewed the same day, or when finance starts depending on manual spreadsheets to explain provider states. Keep the integrated core, then add structure, for example modular routing or an internal ledger, before reconciliation pain becomes your default.

This pairs well with our guide on Platform Economics 101 for Commission Fees, Payout Costs, and Gross Margin.

Best for scaling fleets that need routing control across cities#

Dual-provider routing is usually the right next step once multi-city launches start running into uneven onboarding and compliance outcomes. A single global payout path can become brittle when one market moves quickly and another stalls, especially under local legal differences and ongoing regulatory complexity.

Shared mobility operators were still describing scaling and regulatory complexity in industry commentary published on February 25, 2026, which is a practical signal that city-by-city variance is still part of normal operations.

Where it earns the extra work#

The core benefit is routing control by jurisdiction. If one city repeatedly stalls in compliance review, you can route onboarding and payouts through the provider that is more reliable for that local context instead of forcing one global default.

The tradeoff is operational weight. You gain failover flexibility and better containment when one provider degrades, but you also take on mandatory dual-provider tracking and status normalization.

What routing control must include#

This model only works if every routed case can be reconstructed end to end. At minimum, track:

| Area | Required detail |

|---|---|

| Location | city and jurisdiction |

| Ownership | operating entity and payout owner |

| Routing | selected provider and routing reason |

| IDs and status | provider reference ID, internal payout ID, and status timestamp |

| Review | compliance or review case ID, latest document-check status, and reviewer |

Without that record, teams lose the ability to explain whether a payout was blocked, rerouted, held in review, or completed.

What breaks if you underbuild it#

The main failure mode is false clarity. If two providers report different states and you collapse them into one generic in-progress label, support and finance lose the truth trail and recovery slows down.

Use a clear trigger for dual routing. Switch when repeated city-level review delays persist on one provider, local legal setup requires jurisdiction-specific handling, or provider degradation in one market starts affecting launch timing or payout recovery in others.

If those conditions already apply, keep one canonical internal status model, route by jurisdiction, and treat local compliance support as a first-class selection criterion. For the full breakdown, read Understanding Payment Platform Float Between Collection and Payout.

Best for marketplace-heavy fleets with partner payouts and rev-share#

Use this model when a single revenue event can owe money to more than one party. If rider fees, partner commissions, contractor earnings, or ad-linked proceeds sit in the same flow, define one canonical payout-ledger event model before you add automation.

This is usually the right fit for marketplace-heavy fleets because it gives you clearer split logic, stronger partner-level settlement control, and better financial transparency for finance and legal review. The tradeoff is operational: if ownership and event records are weak, exception-handling debt builds quickly in reversals, adjustments, and support disputes.

- Contractor split settlements: Track ownership at the event level before netting so support can explain shortfalls, holds, or reversals later.

- Franchise or partner-operator rev share: Link each payable line to the governing agreement and the legal entity carrying liability.

- Mixed rider + advertising payouts: Keep separate event types instead of merging everything into one payout line, then reconcile from your internal ledger and use provider records as confirmation.

In shared micromobility, that governance posture matters. NACTO's Version 2 guidance (September 2019), built from city experience, explicitly includes both fee-related controls ("Insurance, Bonds, and Fees") and data requirements, which aligns with keeping settlement logic and reporting evidence tightly documented.

Before launch, replay a full statement period and confirm partner statements, internal totals, and provider payout references reconcile to the same outcome. The deciding factor is not payout volume; it is whether your model already has multiple claimants on the same revenue event.

Best for cross-border payouts and treasury-sensitive operations#

If your cross-border payout share is growing, prioritize document completeness and traceable payout states over marginal fee savings. The win is not a slightly cheaper rail. It is being able to show why a payout was released or held, and which records supported that decision.

| Area | Key requirement | Specific detail |

|---|---|---|

| Recipient onboarding | KYC requirements must be fulfilled before connected accounts can accept payments and send payouts | If capabilities or required verification data are missing, payouts can remain disabled |

| Payout states | Use explicit internal states and attach each state change to an approver, timestamp, and provider reference | States named: pending documents, under review, payouts enabled, payout held, released |

| FBAR / FinCEN | Where relevant, the trigger is when aggregate value exceeds $10,000 at any point in the calendar year | FBAR is filed on FinCEN Form 114, due April 15 with an automatic extension to October 15, using FinCEN's BSA E-Filing System |

-

Policy-gated recipient onboarding. Treat onboarding as a payout control, not a signup flow. Before connected accounts can accept payments and send payouts, KYC requirements must be fulfilled. Because payout enablement is verification-dependent, payouts can remain disabled even when internal ops marks a recipient as ready if capabilities or required verification data are missing.

-

Traceable payout states with hard holds. Use explicit internal states such as pending documents, under review, payouts enabled, payout held, and released. Attach each state change to an approver, timestamp, and provider reference so finance can quickly see whether a delay came from missing identity data, a tax artifact gap, or a capability issue. The tradeoff is slower rollout upfront and fewer downstream payout holds caused by partial recipient data.

-

Treasury evidence for FBAR and FinCEN workflows where relevant. Not every platform will have FBAR obligations, but if your entity holds relevant foreign financial accounts, the trigger is when aggregate value exceeds $10,000 at any point in the calendar year. FBAR is filed on FinCEN Form 114, due April 15 with an automatic extension to October 15. Keep an evidence pack that ties payout approvals to account inventory, internal balance ownership, and reporting cadence, and use FinCEN's BSA E-Filing System for electronic BSA submissions.

In practice, cross-border payout friction usually starts before the transfer itself, when your records cannot quickly answer who is being paid, whether payouts were enabled, and what evidence justified release. Related: Global Payouts and Emerging Markets: 5 Regions Every Platform Should Prioritize.

Red flags that break payout operations first and what to do#

Once payout gating is in place, the first breaks usually come from reconciliation drift, duplicate retry effects, and untested recovery paths. Fix those before you add another provider or push for faster release times.

- Ops events do not reconcile to finance events. Shared micromobility runs on dense logistics activity, including battery changes, warehouse returns, territorial rebalancing, and maintenance, and those events can affect payables.

Run daily real-time data sharing checks between ops and finance records, and send mismatches to an exception queue instead of letting them age. Use a clear end-of-day rule: each payout-relevant ops event should map to a ledger event or an explicit exception reason.

- Retries create duplicate effects. Timeouts and retries can post the same payout or adjustment twice if your write paths are not replay-safe. Idempotency exists to prevent duplicate side effects, and retry-with-backoff patterns assume idempotent operations to avoid state corruption.

Enforce idempotent retries on every write path that moves money or changes payable balances, and verify both your idempotency key and provider reference before release.

- Leadership tracks approvals but not recoverability. Approval dashboards can look healthy while failed payouts and stale states accumulate.

Run scheduled recovery drills for failed payouts, stuck reviews, and stale transitions so teams can prove continuity under failure, not just track approvals.

External evidence can help you spot patterns, but it does not prove your controls work in production. Validate reconciliation queues, retry behavior, and recovery runbooks in your own environment. For more on this, see Catching Payout Errors Early in High-Volume Platform Operations.

Conclusion#

If you take one thing from these payout decisions, make it this: choose the model that fits your actual fleet shape, then get strict about audit trail, reconciliation, and recovery. In a high-volume category, small payout weaknesses do not stay small for long.

- Match the model to your current operating load

Start with the simplest setup your team can reconcile cleanly every day. As operating complexity grows, that same setup can turn into more manual exception handling than finance teams want to carry. The right choice is not the one with the most payout features, but the one your team can explain, approve, and reconcile without spreadsheet guesswork.

- Protect transaction-to-payout traceability early

This control matters most because it determines whether you can prove what was paid, when, and why. Automatic payouts help because they preserve the association between each transaction and the payout it was included in, and payout reconciliation reports are built to reconcile those transactions as a settlement batch. A practical checkpoint is simple: when you receive payout.paid or payout.reconciliation_completed, retrieve the payout automatically and confirm that one report ties back to the underlying transactions and adjustments. If you rely on manual payouts, you own the burden of reconstructing payout contents later, which is where audit-trail gaps appear.

- Set upgrade triggers before stress exposes them for you

Do not wait for a launch problem or a stale exception queue to decide that your architecture needs to change. Write down the events that force a review, such as meaningful scope changes or payout exceptions that stay unresolved past your normal checkpoint. Keep a consistent evidence pack with settlement outputs and required records so ops and finance can review the same facts. Upgrade because your scope changed or recoverability worsened, not because a more complex payout stack looks more advanced.

NACTO's framing fits here: durable operational models matter. In a category with record demand and ongoing pressure on affordability, operator volatility, and limited resources, aligning ops signals with payout controls early can make issues easier to detect before expansion. To confirm what's supported for your specific country or program, talk to Gruv.

Frequently Asked Questions

What are the most common payout challenges in scooter and bike-share platforms?

Common early problems are reconciliation gaps between operating events and finance records, unclear payout contents when teams use manual payouts, and city-specific compliance rules that do not fit one global process. At shared micromobility scale, with more than 133 million U.S. trips in 2023, even small daily mismatches compound quickly.

How does Pay-as-you-go versus Subscription billing change payout risk and reconciliation effort?

Pay-as-you-go pass models and annual or monthly membership models can create different failure patterns, not a universal winner. Pay-as-you-go can require more event-level matching across rides and adjustments, while subscription products add recurring monthly charges and related adjustments. If you use automatic payouts, the transaction-to-payout link is preserved. With manual payouts, you must prove which transactions were included yourself.

What usually breaks first when fleet operations and payout systems are disconnected?

Reconciliation visibility and clarity usually break first when operations data and payout data drift apart. Operational adjustments can end up without a matching finance event, and teams lose confidence in what should be paid. Make "every adjustment has a ledger event or an exception reason by day end" a hard checkpoint so unresolved items do not age quietly.

When should a platform move from one PSP to a multi-PSP setup?

Move when single-provider concentration risk is creating real operating exposure across cities, not because multi-PSP sounds more advanced. A multi-PSP setup means routing transactions across two or more payment providers using rules you control, which can help when one provider becomes a single point of failure. Do it only after you can normalize provider references and settlement reporting across providers, or you will trade outage risk for reconciliation debt. For a deeper architecture comparison, see Integrated Payouts vs. Standalone Payouts: Which Architecture Is Right for Your Platform?.

What minimum controls should exist before scaling to more cities?

You need a consistent reconciliation routine, automatic payouts where possible to preserve transaction-to-payout linkage, and settlement reports from each marketplace and processor. If you choose manual payouts, accept that your team must reconcile payout contents itself. Before launch, verify that one settlement report can be tied back to underlying transactions and key payout adjustments without spreadsheet guesswork.

How should teams handle market-by-market compliance differences without stalling growth?

Treat each market as a separate requirements set, because program rules can differ even within the same city. One study found 70% of U.S. shared micromobility programs had at least one equity requirement, and those requirements are program-specific. Keep a per-market evidence pack with the active rules, approval status, and settlement outputs, then let product and finance review exceptions locally instead of forcing one generic policy across every launch.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bart.gov/news/articles/2023/news20230426trusted

- bsaefiling.fincen.govtrusted

- bsaefiling.fincen.gov/resources/FinCENFBARHelp.pdftrusted

- democracy.thurrock.gov.uk/documents/g6805/Public%20reports%20pack%2027...trusted

- dot.ca.gov/-/media/dot-media/programs/research-innovati...trusted

- dot.ca.gov/-/media/dot-media/programs/transportation-pl...trusted

- dspace.mit.edu/bitstream/handle/1721.1/162064/joyce%20johns...trusted

- flagstaff.az.gov/DocumentCenter/View/89050/Micromobility-Shar...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Gaming and Esports Platform Payouts for Prize and Creator Programs

Treat payouts in gaming as two separate operating problems from the start. If you are evaluating **gaming platform payouts**, the useful question is not who advertises the fastest cashout. It is which payout lane you are running, in which market, and what has to be true before money can move without creating support debt or breaking user trust.

Integrated Payouts vs Standalone Payouts for Platform Architecture Decisions

**Treat integrated and standalone payouts as an architecture decision, not a product toggle.** The real split is the same one you see in payment processing more broadly: either payments are connected to the core platform experience, or they are not. [Lightspeed](https://www.lightspeedhq.com/blog/payment-processing-integrated-vs-non-integrated) puts that plainly in POS terms: your payment terminal either speaks to your point of sale, or it does not. For platform teams, the equivalent question is whether payment flows run through one connected system or sit in separate lanes you manage independently.

How Platforms Should Prioritize 5 Emerging-Market Payout Regions

If you are choosing where to launch cross-border payouts in 2026, start with what your team can actually run. Too many "top" lists lean on hype or market-cap tables. That may work for headlines, but it does not help with execution.