Quick Answer

Start by deciding whether the invoice is owner-linked or entity-linked, then run controls to that classification. For invoice sole proprietor vs company, a sole proprietor file can pass when owner identity, DBA mapping, and beneficiary naming align, while company-labeled files need supportable entity records plus acting-person linkage. In U.S. review, Schedule C context and SSN/EIN posture are matching signals, not stand-alone approval rules. If tax identity or naming cannot be reconciled, hold the case and escalate before payout.

Classify the counterparty before accepting the invoice#

When comparing invoice sole proprietor vs company, start with who is legally behind the obligation, not how polished the invoice looks. That is where payout acceptance risk usually splits.

A sole proprietorship is the same legal person as its owner, so business debt or lawsuit exposure can reach personal assets. An LLC or incorporated company is a separate legal entity. For compliance, legal, finance, and risk teams, that distinction changes counterparty risk even when an invoice appears valid.

This guide is for operational acceptance decisions across the United States, Canada, and United Kingdom. The goal is practical: what to verify, what to document, and when to escalate.

Use these two early checks:

- Entity evidence quality: A DBA explains a trading name, but it does not create a separate entity. Treat DBA documents as name evidence only, and keep the owner identity tied to the invoice record. If a supplier claims company status, require records that support it.

- Tax identity context: In the US, a sole proprietor may report business activity on IRS Form 1040 Schedule C, and businesses with employees need an EIN. These are useful signals, not universal shortcuts.

Keep a strict line between confirmed facts and local-rule assumptions. Do not assume a universal standard for invoice fields, tax-ID display, or VAT/GST-style checks across the US, Canada, and UK without local review.

The operating rule is simple: treat legal form as one risk input, not the whole decision. If owner identity is clear and naming is consistent, standard controls may be appropriate. If the file depends on a DBA, unclear tax identity, or unsupported entity claims, pause and escalate before funds move.

We covered this in detail in When a DBA Works for a Sole Proprietor and When to Move to an LLC.

At-a-glance comparison for invoice acceptance risk#

Start with who is legally and operationally behind the invoice. Formatting comes after that. Acceptance risk mostly turns on evidence quality, name consistency, and tax-identity consistency.

| Checkpoint | Sole proprietorship | Single-member LLC | Corporation | Practical recommendation |

|---|---|---|---|---|

| Legal separation | Owner and business are the same legal person. | Treat legal separation as supportable only when entity-status evidence is clear in records. | Incorporation can establish a separate legal and financial entity when the claim is supportable in records. | Use legal form as one input, then confirm evidence quality before release. |

| Identity evidence quality | Supported business-name evidence plus personal identity tied to the payee. | Entity-status evidence plus entity records, tied to the acting person. | Incorporation/entity evidence plus entity records, tied to the acting person. | Accept with enhanced review when the file is mainly name evidence plus personal identity. Accept with standard controls when entity records and person-to-entity linkage are clear. |

| Verification depth | Match owner identity, invoice name, and payout beneficiary. | Match entity existence, acting person, invoice name, and beneficiary. | Match entity existence, acting person, invoice name, and beneficiary. | Escalate when the claimed payee cannot be consistently tied across records. |

| Tax-ID handling | Do not treat EIN presence as a shortcut. If SS-4 support exists, use Line 7b or 9a (taxpayer ID) and Lines 9a, 13, 14, 15 (entity/employee context) for consistency checks. | Same SS-4 consistency checks apply; the LLC label alone is not enough. | Tax identity should stay consistent with corporate name and records. | Accept with standard controls only when tax identity aligns with the legal/entity story; otherwise accept with enhanced review or pause for legal/tax escalation. |

| Invoicing name rules | Invoice name should map to owner or supported trade name, then to beneficiary. | Invoice name should map to legal/trade name, then to beneficiary. | Invoice name should map to legal/trade name, then to beneficiary. | Any unresolved name mismatch is a hold point. |

| Escalation triggers | Unclear owner identity or unresolved name-to-beneficiary mapping. | Entity label present but entity evidence is missing or inconsistent with tax support. | Incorporated claim present but entity or tax support is contradictory or suspicious. | Pause for legal/tax escalation when entity status or tax paperwork cannot be independently supported. |

| Operator impact (payout routing and controls) | Baseline KYB with stronger exception handling and clear owner-level audit notes. | Baseline KYB plus entity-and-actor linkage checks; route exceptions for manual review. | Baseline KYB with cleaner routing when records are consistent; maintain full decision trail. | Route clean files after artifacts are attached; keep an audit trail from acceptance decision to payout release. |

How to read the table#

Sole proprietor files are not automatically unacceptable, but they are more sensitive to evidence quality because owner identity and business identity are closely linked. Single-member LLC and corporation files can be handled with standard controls when entity records, acting-person linkage, tax identity, and payout details stay consistent. If those elements conflict, treat it as a verification problem and escalate before payout.

Related: How to Register for a Business Number (BN) in Canada.

Legal separation changes who carries invoice risk#

The key split is legal separation. A sole proprietorship is the owner. An LLC is a separate entity when that status is supported in records. In invoice review, that changes who you treat as the accountable party and how strictly you handle mismatches before payout.

When the file is a sole proprietor, a business name on the invoice alone does not establish a stand-alone company profile. The invoice name, submitting person, and payout beneficiary should all map back to the same owner story.

What changes in review#

| Structure shown in the file | Separation status you can rely on from this section | Who the invoice file should point to | Main review consequence |

|---|---|---|---|

| Sole proprietorship | No legal separation from the owner | The individual owner behind the invoice | Name, identity, and beneficiary mismatches are owner-level risk and need tighter review |

| Limited liability company (LLC) | Separate business from the owner, if the entity claim is supportable | The entity, plus the person acting for it | Review entity identity and actor authority separately, and require evidence for both |

| Other company-style label | Do not rely on the label alone here | Hold until entity status is independently supported | A company-style label by itself is not enough to lower onboarding risk |

If things go wrong, exposure sits directly with the owner because there is no entity shield. A cited failure mode is that creditors may reach personal assets such as homes and savings. That does not make sole proprietor invoices unacceptable, but it does raise the cost of owner-level verification mistakes.

With LLC files, the risk picture improves only when separation is real in the records. Treat the entity claim as meaningful only after you can connect the invoice name, entity evidence, acting person, and receiving account. If records look mixed between personal and business use, keep controls tight.

Why DBA evidence needs caution#

A DBA or local business license can explain a trading name, but by itself may not demonstrate legal separation. Being able to invoice and being low-risk to onboard are different decisions.

| Artifact or signal | What it can support | Caution |

|---|---|---|

| DBA | Can explain a trading name | Does not by itself demonstrate legal separation |

| Local business license | Can explain a trading name | Does not by itself demonstrate legal separation |

| DBA plus personal identity | Can be checked so the DBA maps cleanly to the owner and then to the payout beneficiary | Enhanced review is usually the safer posture |

| LLC filing-formality signal ($50-$500) | Gives you more to verify | Is not proof of a clean file |

If the package is only a DBA plus personal identity, enhanced review is usually the safer posture. Check that the DBA maps cleanly to the owner and then to the payout beneficiary, and treat business-style presentation without entity-grade support as a red flag.

LLCs also carry a formality signal, including cited state filing fees in the $50-$500 range. That added formality gives you more to verify, but it is not proof of a clean file. Accept sole proprietor invoices when owner-level evidence is coherent. Require independent support before relaxing controls on any file claiming a company posture.

This pairs well with our guide on How a UK Creative Director Can Invoice a US Client Through a UK LTD Company.

Tax identity on invoices by country#

Use tax identity as a matching control, not a formatting test. First confirm whether the invoicing party is an individual owner or a separate company in your file record. Then reconcile tax signals to that party, and leave invoice-field rules to local-law review.

| Country | Sole-owner invoicing check | Company invoicing check | Tax registration signal to reconcile | Must confirm locally |

|---|---|---|---|---|

| United States | Anchor review to owner-level tax identity; use IRS filing context such as Schedule C (Form 1040) when classification is unclear. | Anchor review to entity-level tax identity, separate from the acting individual. | Resolve SSN and EIN posture from the full file record, not invoice layout alone. | Whether invoices must show SSN, EIN, both, or neither, and any mandatory invoice fields. |

| Canada | If the file is owner-level, reconcile the invoicing party to any claimed BN or GST details. | If the file is entity-level, reconcile legal entity identity to any claimed BN or GST details. | Treat claimed BN and GST details as signals to verify, not stand-alone proof. | Whether BN must appear, GST thresholds, and required GST invoice elements. |

| United Kingdom | If your file classifies the payee as an individual sole trader, keep checks tied to that individual. | If your file classifies the payee as a limited company, validate company identity separately from the submitting person. | If VAT is claimed, reconcile it to the invoicing party and supporting records. | VAT registration evidence standards and mandatory UK invoice fields. |

United States#

For U.S. sole proprietors, IRS reporting context is a grounded anchor: business income or loss is reported on Schedule C (Form 1040).

| U.S. signal | What the article says | Review use |

|---|---|---|

| Schedule C (Form 1040) | Business income or loss is reported here for U.S. sole proprietors | Use as a grounded anchor when classification is unclear |

| Schedule SE (Form 1040) | Net self-employment earnings of $400 or more trigger it | Use as a classification clue, not an invoice acceptance threshold |

| Withholding posture | Payers generally do not withhold tax from payments to self-employed individuals | Keep owner-level tax-identity controls tight |

For self-employment tax context, the IRS states that net self-employment earnings of $400 or more trigger Schedule SE (Form 1040). Use this as a classification clue, not as an invoice acceptance threshold.

Also avoid assuming the payer already handled withholding. The IRS says payers generally do not withhold tax from payments to self-employed individuals. For owner-level files, keep owner-level tax-identity controls tight.

Canada#

In Canada, reconcile any claimed BN or GST detail to the actual invoicing party in your file. That check is useful. Guessing missing-rule details is not.

Treat claimed BN and GST details as verification items. Confirm BN display requirements, GST thresholds, and mandatory GST invoice fields with the CRA or a qualified adviser, and escalate when the claim does not match the invoicing party.

United Kingdom#

In UK review, keep identity checks aligned with the payee classification in your records (individual vs company). If VAT is claimed, verify that claim against the invoicing party before payout.

Do not import EU VAT invoicing assumptions into UK review. UK mandatory-field rules vary by country, so keep those as local confirmation items.

For cross-border Social Security claims involving U.S. coverage, use a separate evidence lane. Totalization agreements are meant to prevent dual Social Security taxation. A U.S. Certificate of Coverage is the concrete proof artifact when exemption is claimed.

Related reading: BVI vs Cayman Islands for an Investment Holding Company in 2026.

Build the minimum KYB evidence pack before first payout#

Before first payout, build a lean KYB/KYC pack that shows who you are paying and how the invoice, onboarding profile, and bank payee connect. If that payee story is not clear from reliable, independent documents, pause release for review.

What the minimum pack should prove#

KYB/KYC should answer one question: is the person or company really who they claim to be, based on reliable, independent information or documents? Build the file around the invoicing party type, then add only the evidence needed to explain naming and payout.

| Checkpoint | Sole proprietorship or sole trader | Registered business or company | Operator rule |

|---|---|---|---|

| Primary identity anchor | Individual identity evidence for the payee | Legal-entity identity evidence for the payee | Validate against the invoicing party, not only the submitter |

| Trading name evidence | If a trading name is used, include evidence linking it to the verified payee | If a trading name is used, include evidence linking it to the verified entity | Do not treat a trading name alone as full entity proof |

| Profile alignment | Names and profile details align to the verified payee | Names and profile details align to the verified entity | Hold when records point to different parties and the gap is unexplained |

| Tax footprint | Claimed tax identifier, if collected | Claimed tax identifier, if collected | Use as a matching signal, not stand-alone proof |

| Payout readiness | Bank payee supports the same verified payee story | Bank payee supports the same verified payee story | No payout until unresolved name mismatch is explained |

This is also a core KYB risk control: do not pay a paper-only business profile that cannot be tied to a real counterparty.

Make name matching a release gate#

Name reconciliation can be a release gate. The invoice name, onboarding profile, and bank beneficiary should resolve to one credible payee story. Exact character matching is not always realistic, but the file should explain the relationship without guesswork.

Use a simple handoff test: can a second reviewer quickly see why the names belong together? Straightforward digital checks can take a few minutes, while more complex investigations can take several business days or more.

Add tax signals only where they actually help#

Tax identifiers help only after you have verified core identity. If your program collects tax identifiers, reconcile each claim to the same invoicing party reflected in the name and bank evidence.

If a tax claim points to a different party, treat it as a risk signal and escalate. Tax identifiers can strengthen a file, but they do not replace core identity evidence.

Keep full identifiers out of day-to-day tools#

If your process handles sensitive identifiers, use masked values in operational tools and keep full documents in restricted, auditable systems.

Approve first payout only when identity evidence, name matching, and payee logic are coherent. If the case depends on unexplained name gaps or unsupported tax claims, escalate before funds move.

If you want a deeper dive, read The Best Business Bank Accounts for Canadian Sole Proprietors.

Use decision rules for accept escalate or block#

Use evidence quality as the primary rule in this review. Source-quality checks are supported here, but accept/escalate/block thresholds are not established on their own.

Let the file drive the decision#

Build your matrix around what is verifiable in the file, then map that to your internal policy path. Entity type can still help sort the queue, but entity type alone should not drive outcomes.

| Evidence state | What is true in the file | Decision path (internal policy, not excerpt-derived) |

|---|---|---|

| Reproducible and current | Source can be reopened, the record is current, and the payee story is coherent across invoice/profile/payout records | Consider standard handling under your policy |

| Incomplete but fixable | Core proof is missing or unclear, but the gap may be resolved with additional documentation | Consider escalation and temporary hold per policy |

| Unsupported or unusable | Source cannot be retrieved, is too broad to verify the claim, or conflicts with the case record | Treat as unresolved until the claim is verified or removed |

Verify the source, not just the summary#

Capture source metadata showing what was actually checked. For example, FAR Part 31 shows FAC Number: 2026-01 and Effective Date: 03/13/2026, and DOSAR Part 652 shows its authority plus Source: 53 FR 26177, July 11, 1988.

If a page returns An error occurred, please try again., treat that as unavailable evidence. Also distinguish broad search results from narrower chapter-level checks when confirming a specific claim.

Keep controls proportional#

Keep baseline controls for all files, and reserve enhanced review for records with unresolved evidence problems. Overbuilding every queue slows work without improving decisions.

If you define escalation owners or response windows, treat them as internal operating policy rather than excerpt-derived requirements, and document them clearly in your process.

For a step-by-step walkthrough, see Sole Trader vs. Company: A Guide for Australian Freelancers.

If your escalation matrix is defined but execution is still manual, map it to a payout workflow with explicit statuses and retry-safe controls in Gruv Payouts.

Run invoice intake in a fixed order to reduce rework#

A fixed intake sequence can cut rework. These cases often loop across teams when checks happen out of order and a basic mismatch appears only after payout prep has started.

This matters because the work is cross-functional, and break points in multi-step flows can hide leakage that top-line metrics do not fully capture. A fixed order gives each team clearer ownership and cleaner handoffs.

| Intake stage | What you are deciding | What should be attached or logged before moving on | Common rework if you skip the stage |

|---|---|---|---|

| Entity type classification | What kind of payee the file claims to be | Claimed entity type, source reviewed, retrieval date, and any uncertainty note | Teams request the wrong evidence later or apply the wrong review path |

| Identity match | Whether invoice, profile, and payout details tell one coherent story | Name-match note, any mismatch flag, and the artifact used to confirm or question the match | Payment setup starts while naming issues are still unresolved |

| Tax registration validation | Whether claimed registration status was checked under your program rules | Validation result, masked reference where appropriate, and unresolved issues clearly marked | Tax follow-up reopens a file that looked complete |

| Payment execution readiness | Whether the case is ready for release | Explicit approval status, reviewer identity, timestamp, and release condition met | Premature payout, duplicate handling, or last-minute manual holds |

Start with classification, not payment setup#

If classification is not reliable, stop there. As a process control, do not begin identity exceptions, registration checks, or payout preparation until the case record clearly states what is being reviewed.

This step is not about resolving every legal question. It is about choosing the right downstream evidence path so later teams do not inherit avoidable ambiguity.

Gate release on artifacts, not memory#

As a process control, do not release payout based on informal confirmation. Hold release until verification artifacts are attached and approval status is explicit in the case record.

At minimum, keep the reviewed record, retrieval metadata, mismatch notes, and named reviewer in the file. Without that, later challenges can force reconstruction from partial notes.

Make retries harmless#

If retries or out-of-order events occur, your process should handle repeated events without creating duplicate approvals or duplicate payout instructions.

In practice, tie approvals and payout actions to a unique case action key, and treat repeats as no-op updates unless the underlying state changed.

Add one hard checkpoint before funds move#

Before release, require one final checkpoint: required evidence complete, no open mismatch flags, and auditable reviewer sign-off. If any checkpoint item is missing, hold release and return the case to the failed stage. That helps keep cross-functional ownership intact and can reduce late-stage payout errors.

Catch the failure modes competitors gloss over#

Most repeat failures are not exotic. They are completeness and review-gating failures that turn into avoidable delays.

| Failure mode | What it looks like in review | Why it fails later | What to do before release |

|---|---|---|---|

| Incomplete submission package | Required accompanying information is missing or submitted in fragments | Approval is delayed when required materials are not submitted together | Hold the case until the required package is complete in one record |

| Review started before the package is complete | Due diligence begins while required information is still incomplete | Due diligence on a partial file drives delay and rework | Gate review so due diligence starts only after required accompanying information is complete |

| Invoice/KYB identity or tax conclusions without primary support | Identity consistency or tax treatment is inferred from labels or partial records | Confirm invoice/KYB sufficiency rules with the relevant authority before drawing conclusions | Treat these conclusions as unverified until supported by applicable primary policy/legal sources |

| Legal-source reliability gap during escalation | A non-official rendering is used as final legal support | Escalation decisions rest on text that may not provide legal or judicial notice | Verify against an official edition of the Federal Register before closing the issue |

If you tighten only one control, make completeness and source reliability a hard release condition. Do not release while required information is incomplete, invoice/KYB conclusions are still unverified, or legal support has not been checked against official text.

Choose controls by scenario not by ideology#

Set control depth by exposure, not preference. Use a lean baseline for high-volume, low-ticket files. Use stronger upfront review when payouts are high-value or recurring and the file is presented as a company record, especially a Corporation label.

| Scenario | Default control depth | First checkpoint | Escalate when |

|---|---|---|---|

| High volume, low ticket, individual payee | Lean baseline | Confirm the file is complete and the payee record is coherent across invoice, profile, and payout details | Any name mismatch, entity-label conflict, or unclear country signal |

| High-value or high-frequency payouts, company-labeled record | Stronger upfront review | Verify the claimed company form has supporting entity evidence before approval | The invoice uses a company label but the file cannot support that status |

| Ambiguous country or entity signals, any payee type | Pause, do not force-fit | Hold the case until jurisdiction and entity form are resolved in one record | Approval would depend on assumption rather than evidence |

For the lean lane, keep speed but do not lower release gates. Reserve enhanced review for files that break coherence, and stop low-touch handling when labels start mixing individual and company signals.

For corporation-labeled files, front-load entity-status checks. A corporation is described as a separate legal entity. The incorporation excerpt identifies three checkpoints in that record trail: filing Articles of Incorporation, a directors' meeting, and a shareholders' meeting. You do not need that same depth in every case, but a corporate label without incorporation support is a red flag.

When country or entity signals are ambiguous, pause and escalate instead of forcing a lane decision. Jurisdiction-specific control requirements are not established here, so avoid jurisdiction assumptions. The same scenario logic applies to speed-versus-cost choices: invoice financing can improve working capital and provide up to 85% of invoice value upfront, but it can be expensive and third-party involvement may complicate customer relationships, so it is best suited to specific business models.

Use this reporting checklist for audit-ready operations#

A file is audit ready when it can trace one invoice decision through payout and reconciliation without guesswork. Use one consistent case record for every approved, conditional, escalated, or blocked invoice.

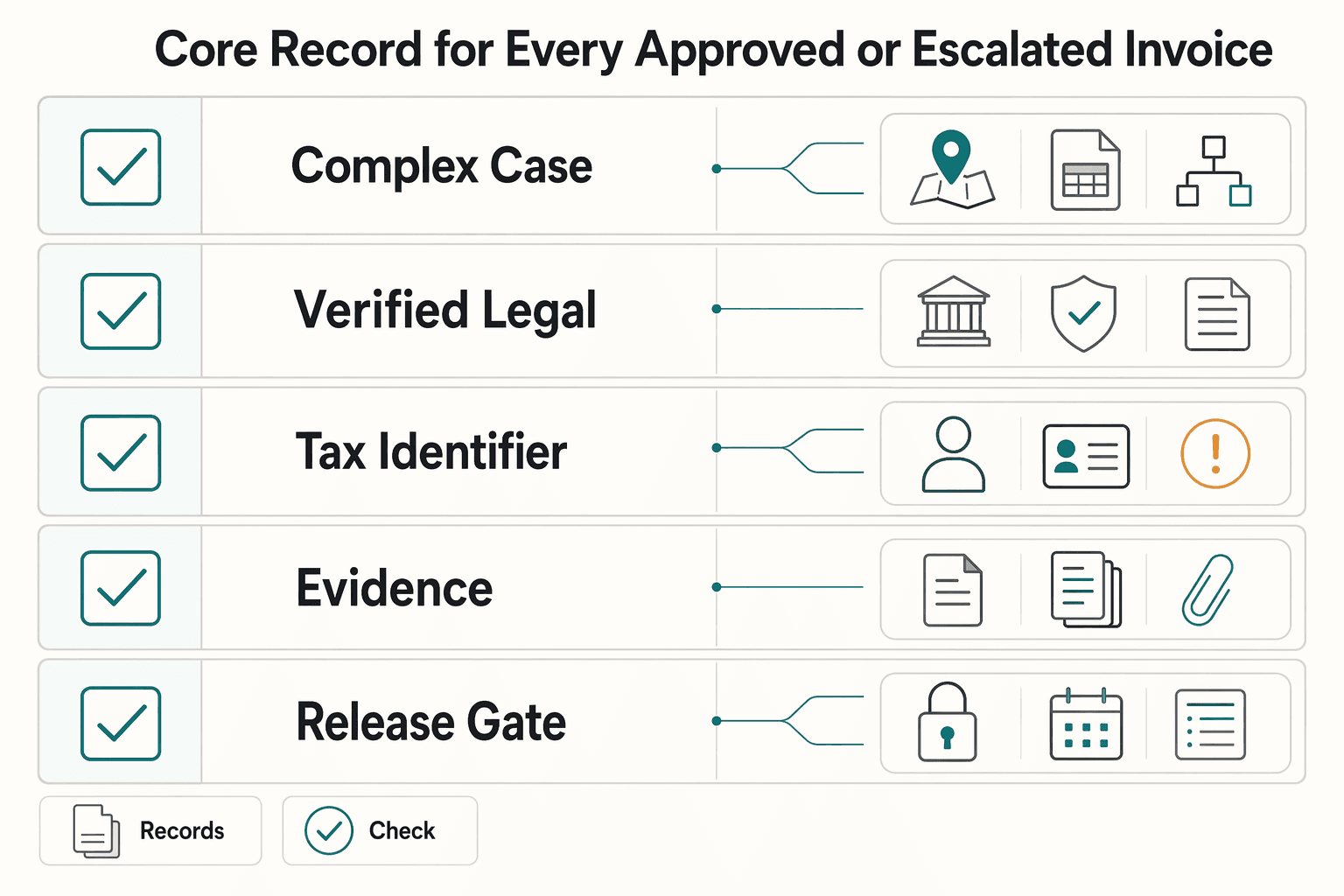

Core record for every approved or escalated invoice#

Use controlled fields so another reviewer can replay what was verified, what stayed unresolved, and why funds moved or did not move.

| Field | What to record | Operator note |

|---|---|---|

| Entity type | Claimed and verified form (for example sole proprietorship, single-member LLC, corporation, sole trader, limited company) | Keep entity form separate from trade name |

| Verified legal name | Exact legal name used for approval | Match invoice, onboarding profile, and payout beneficiary |

| Tax identifier status | Status only: provided, verified, pending review, or unresolved; include identifier type where known (for example EIN) | Avoid vague entries like "tax checked" |

| Registration evidence | Artifact reviewed, or "none provided" | Capture business registration, DBA, or incorporation support here |

| Approval outcome | Approved, approved with conditions, escalated, or blocked | Use controlled values, not free text |

| Escalation notes | Why escalated, owner, next review date | Keep unresolved issues in-record, not chat/email |

| Reviewer identity | Named reviewer or approval queue | Missing reviewer weakens defensibility |

| Decision timestamp | Date/time of approval or escalation | Prefer system timestamp |

| Payout trace | Payout event ID, batch ID, or provider reference | Links decision to funds movement |

| Reconciliation artifact | Reference that ties payout to expected account trail | Bank deposit match or reconciliation file is the anchor |

| Known vs unknown | Confirmed facts vs items pending local counsel/tax review | Prevent assumptions being logged as facts |

Trace the decision to reconciliation#

Your report should work in both directions: invoice to payout, and payout or bank deposit back to approval. Tie together the invoice, payment records, and bank statements showing deposits. Where relevant, also point to filed tax returns and supporting documents.

Treat missing reconciliation evidence as an incomplete case, even when entity review passed. A payout that looks valid in the payment tool but does not match the bank trail is a proof gap, not just operational noise.

Monthly exception report#

A monthly exception report is an operating control, not a universal legal requirement. Use it to surface control failures before they spread across payout batches. Review groups like these, and for each exception record aging, owner, and payout-hold status so the report does more than count cases.

| Exception group | Examples | Track for each case |

|---|---|---|

| Unresolved record mismatches | Name mismatches, entity-label conflicts, missing registration evidence, or approvals with open questions | Aging, owner, and payout-hold status |

| Tax-identifier status gaps | Expected tax identifier remains unverified (for example EIN), or local invoice/registration questions remain unresolved | Aging, owner, and payout-hold status |

| Repeat failure patterns | Recurring payout-to-bank mismatches by queue, country, provider path, or payee type | Aging, owner, and payout-hold status |

Keep known facts separate from legal unknowns#

Keep known facts separate from legal unknowns by adding a short "known vs unknown" block in each report.

- Known: verified facts, such as legal name matched, payout reference documented, and bank deposit reconciled.

- Unknown: unresolved legal or tax questions, such as local invoice tax-ID display expectations or adequacy of registration evidence.

If local counsel is needed, state that directly. This separation helps in cross-border files, where local entity, tax-registration, and invoice-format rules may differ.

Retention and retrieval#

Keep case records and supporting artifacts long enough to defend the decision later. Retention is jurisdiction-dependent. General guidance often starts at 5-7 years from the end of the tax year for basic records. Contracts may run 7 years after contract end. Asset records may run for the life of the asset plus 5-7 years.

Digital records are commonly workable if backups and retrieval are reliable. Storage is usually cheaper than reconstructing records later. If a case cannot show who approved it, what evidence supported it, when funds moved, and what reconciled later, the reporting design is not finished.

You might also find this useful: Sole Trader vs. Limited Company: A Guide for UK Freelancers.

Conclusion#

For invoice sole proprietor vs company, treat entity form as a risk input, not a payout decision on its own. The practical advantage is an acceptance process that ties each approval to evidence quality, clear escalation triggers, and a review record another reviewer can replay.

A sole proprietorship is not legally separate from the owner, while an LLC or incorporated company is legally distinct from its owner. That changes liability exposure, but it still does not determine whether a specific invoice should be paid. Sole proprietors can be legitimate even when records are thinner or state registration is absent. Registered entities often provide stronger verification artifacts, such as registration records, formal filings, and owner or officer disclosures.

Use this simple decision sequence:

- Classify the claimed form: sole proprietorship or registered entity.

- Verify against the strongest checkpoint available for that form: owner-linked records and DBA details, where relevant, for sole proprietors; registration and formal entity records for registered entities.

- Treat missing or limited records as a risk flag that needs deeper investigation, not an automatic rejection.

- Approve payout only when the file records what was verified, what remains unknown, and who approved.

This avoids two common errors: treating naming evidence alone as legal-entity proof, and inferring tax treatment from the entity label alone. Standardize what you can, escalate what is country-specific, and document each decision so the result is defensible.

For upgrade timing and liability tradeoffs, read When Should a Freelancer Upgrade from Sole Proprietor to an LLC?. Before rolling this framework across countries, validate coverage and compliance assumptions for your specific program by contacting Gruv.

Frequently Asked Questions

Can a sole proprietor legally issue invoices to business clients?

Use a local-law answer, not a generic yes or no. The source guidance defines a sole proprietorship as an unincorporated business run by one individual, but it does not establish country-specific invoicing legality or required invoice fields. For multi-country operations, confirm local rules before proceeding.

What is the practical difference between invoicing as a sole proprietorship and as an LLC or corporation?

The core difference is legal separation and liability exposure. A sole proprietorship has no legal separation from the owner, so the owner is personally liable for business debts and legal obligations. An LLC is a legally separate entity created under state law, and formation evidence, such as articles of organization, is a practical verification checkpoint. Confirm corporation-specific invoicing rules with the relevant authority.

Should invoices show an SSN or EIN in the United States?

This guide does not support a blanket SSN-versus-EIN invoice-display rule. It does support that sole proprietors report business income on IRS Form 1040 Schedule C, so tax-identity handling is still a review point. If your team cannot confirm identifier display requirements, escalate instead of approving on assumption.

Does entity type change VAT, GST, or sales tax handling on invoices?

Do not infer VAT, GST, or sales tax handling from the entity label alone. The grounded sources do not support a rule that sole proprietor, single-member LLC, or company status by itself determines tax treatment. If treatment is being inferred rather than verified, pause and confirm country-specific tax requirements.

When should a platform escalate an invoice for legal or tax review?

Escalate when claimed status cannot be verified with available documentation, or when tax handling is assumed instead of verified. Examples include an LLC claim without state formation proof (such as articles of organization) or missing required city/state licenses and permits where applicable. In practice, the risk signal is the evidence gap, not the label by itself.

Is a DBA enough to verify a business for cross-border payouts?

Do not treat a DBA alone as sufficient verification. A DBA is a name-registration step. It does not create legal separation and does not convert a sole proprietorship into an LLC. Use it as one file artifact, then verify the underlying owner or legal entity separately.

What records should we keep to defend invoice decisions in an audit?

This guide does not define a mandatory record set or retention period. Keep records that let another reviewer replay the decision, including claimed entity type, registration evidence reviewed, and who reviewed and when. Add a short known-versus-unknown note so assumptions are not logged as facts.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/dosar/part-652%E2%80%94solicitation-provisio...trusted

- acquisition.gov/far/part-31trusted

- business.gov.au/planning/business-structures-and-types/busin...trusted

- dfpi.ca.gov/wp-content/uploads/sites/337/2020/11/PRO-02-...trusted

- docs.legis.wisconsin.gov/document/administrativecodearchive/659/remov...trusted

- fac.gov/assets/compliance/2024-Compliance-Supplement...trusted

- federalregister.gov/documents/2022/09/30/2022-21020/beneficial-o...trusted

- finance.senate.gov/download/made-in-america-effect-of-the-us-ta...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Business Bank Accounts for Canadian Sole Proprietors

If you want the right setup, start with your payment pattern, not the monthly fee. If most of your activity is in CAD, one domestic hub can be enough. When foreign receipts become meaningful, add an international gateway instead of forcing one account to handle both jobs poorly.

How to Register for a Business Number (BN) in Canada

--- Getting control of your operation starts with the right question: not whether you might eventually need a Canadian Business Number, but when it becomes worth setting up. This is less about bureaucracy than about operating cleanly, reducing onboarding friction, and avoiding rushed compliance work later.

Sole Trader vs Limited Company UK for Freelancers

If you need a practical starting rule, choose sole trader for a faster start and lighter admin. Choose a limited company when legal separation and company-level compliance are worth the extra work.