Quick Answer

For most freelancers comparing sole trader vs company australia, the practical answer is to choose the structure you can operate cleanly right now. Sole trader usually fits fast setup and lighter admin, while a company can fit better as liability exposure, reporting obligations, and contract complexity increase. The strongest approach is a staged one: decide for the next 90 days, run clear controls, and switch only when your risk and operating model justify it.

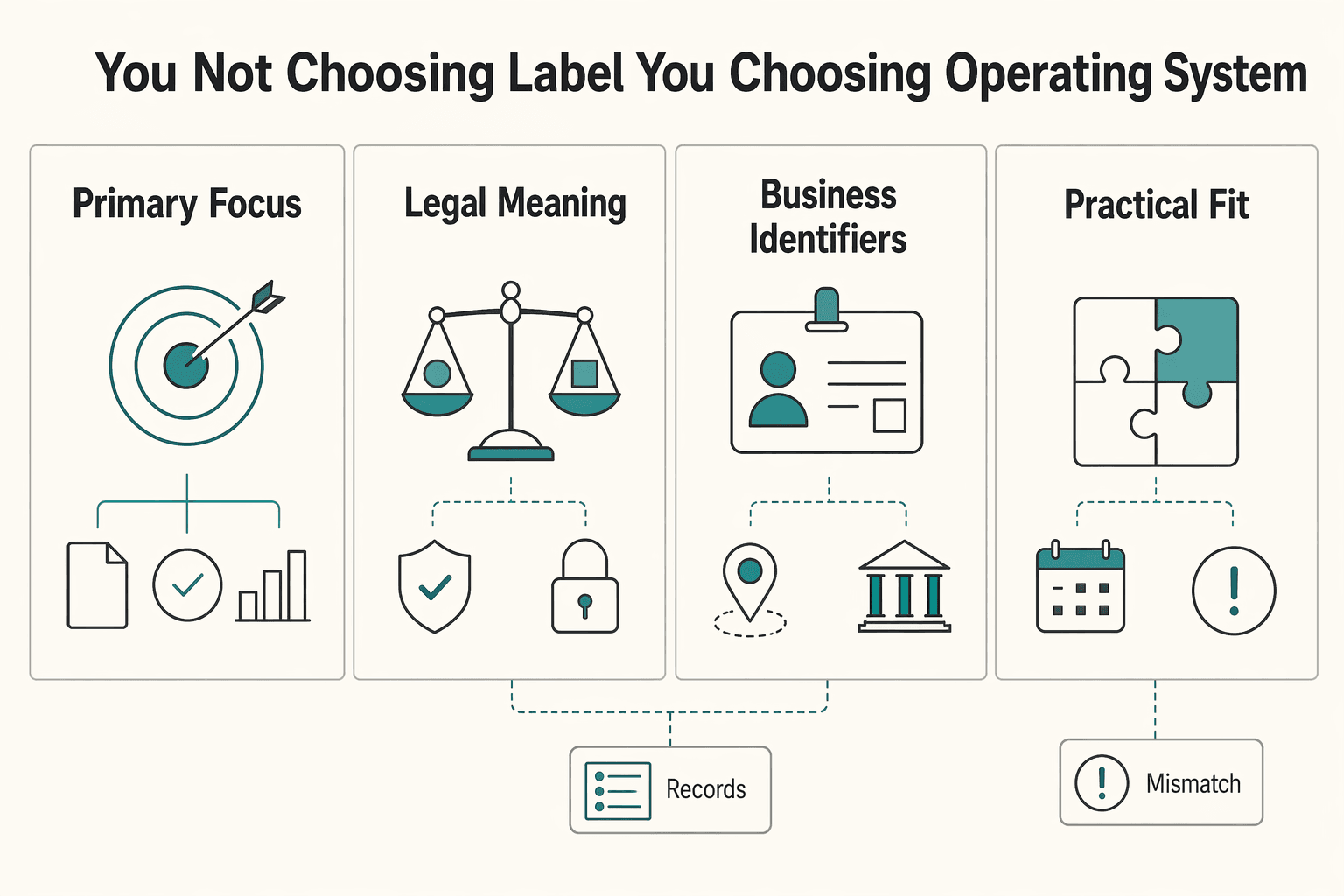

You are not choosing a label you are choosing your operating system#

In a sole trader vs company decision in Australia, you are choosing a system, not just a label. Your structure affects contracts, tax, personal asset protection, and investment readiness.

If you are freelancing in Australia, starting fast as a sole trader can feel like the obvious move. Sometimes it is. The trap is treating that first decision like a label, then getting forced into a rushed rebuild later when contracts tighten, compliance expectations rise, or you take on bigger obligations.

If you want a quick decision framework, use the table below to pick the system you can actually run.

| Decision lens | Sole trader path | Company path |

|---|---|---|

| Primary focus at the start | Get operating quickly and keep setup manageable | Build a formal structure from day one |

| Legal meaning | Not a separate company structure | In Australia, "company" has a specific legal meaning and is treated as a separate legal entity when registered |

| Business identifiers | An ABN is used for tax purposes across many business types | Companies usually use both ACN and ABN. ASIC handles ACN registration, and ATO handles ABN issuance |

| Practical fit | Works when you want fewer moving parts early | Works when you want a formal company structure for bigger obligations |

The core tension for a business-of-one is simple: speed now versus structure now.

- A sole trader setup can work when your priority is starting quickly and keeping administration manageable.

- A company setup can work when you want a formal structure in place earlier.

This guide is clear about its limits. It does not claim exact tax rates, guaranteed tax outcomes, detailed reporting thresholds, or precise fee totals. Those details depend on your facts and who is advising you. The goal is to help you choose a direction before you lock in the mechanics.

If ABN setup is your immediate blocker, use A Guide to Australia's ABN for Sole Traders alongside this decision.

Use this operator check:

- Which structure can you run monthly without missed records?

- Do your target clients expect a company counterparty?

- Is your risk exposure increasing through bigger obligations?

- What trigger will move you from sole trader to Pty Ltd?

Imagine you win a larger ongoing contract that asks for formal entity details and sign-off controls. With this framework, you already know your next move. That is the outcome: fewer surprises, cleaner compliance, and an Australian business structure that scales without rework.

Which structure wins for your situation right now?#

For many operators, starting as a sole trader is the simpler, faster path. Moving to a company can make sense later as risk and operational complexity rise.

You have the operating-system lens. Now make the call you can run cleanly this quarter, then put a review date on it.

| Criteria | Sole trader | Company |

|---|---|---|

| Legal separation | You and the business operate as one. | You run through a separate company structure with different obligations. |

| Liability exposure | You carry unlimited liability, so business problems can put personal assets at risk. | You operate under a different legal structure than a sole trader, but do not assume absolute protection. |

| Setup effort | Fast and low-friction setup. | More formal setup path than sole trader. |

| Admin load | Lighter at the start for a business-of-one. | Higher ongoing discipline and process needs. |

| Tax treatment framing | You use an ABN and TFN, and income flows through your personal tax return. | You follow company tax and compliance obligations. Do not assume better tax implications by default. |

| Growth readiness | Strong for testing services and building early momentum. | Often considered as operations become more complex and structured. |

Safe default for early-stage Australian freelancers: Start as a sole trader when you need quick market entry, simple administration, and a clean way to validate demand before you add complexity.

Upgrade path when complexity rises: Move earlier to a company when obligations, risk profile, and operational complexity rise beyond what you can comfortably hold personally.

| Choose this if | Sole trader | Company |

|---|---|---|

| Risk profile | You can accept personal exposure while work stays straightforward. | You want tighter separation as obligations become heavier. |

| Growth intent | You are validating a niche and keeping scope narrow. | You expect larger or more structured engagements. |

| Admin capacity | You need minimal process overhead right now. | You can run stronger recurring controls each month. |

If your risk profile and obligations increase, choose the company path earlier. Your structure should match the work.

Practical verdict: start as a sole trader if speed and simplicity are your priority today. Switch to a company when risk and operational complexity increase. That gives you a decision you can use now, without pretending the first choice has to be permanent.

Related: A Guide to Tax Residency in Australia for Digital Nomads.

What liability exposure are you actually taking on?#

When you compare a sole trader and a company in Australia, liability should be part of the decision once obligations start to grow.

You can pick a structure that looks neat on paper and still carry more risk than expected. Pressure test your choice so you do not confuse easy setup with lower risk.

For a sole trader, you and the business are closely tied in practice. You keep full control and minimal compliance overhead, but you also carry unlimited personal liability. Risk can move beyond business operations into your personal position, and sole trader business income is taxed at personal income tax rates.

A company structure, including a Pty Ltd proprietary limited company, can reduce personal risk concentration in normal operations, but do not treat that as absolute protection.

| Risk lens | Sole trader exposure | Company exposure framing |

|---|---|---|

| Personal liability | Unlimited personal liability sits with the owner | Personal risk concentration can be lower in normal operations, but not eliminated |

| Tax and pay setup | Business income is taxed at personal income tax rates | Structure choice can change tax position and how you pay yourself |

| Growth and perception | Choice still depends on goals and risk profile | Structure can influence customer and investor perception as plans scale |

Rule to run: both structures can work. Choose based on your goals, risk profile, and growth plans, then revisit the decision as obligations change.

What does setup and ongoing cost really look like in year one?#

In year one, cost depends less on headline setup spend and more on whether you can run the structure cleanly every month.

Now turn that risk view into a practical operating budget you can execute without surprises.

Start with the structure, then complete the setup steps that apply.

- For a sole trader, that usually means securing an Australian Business Number (ABN) and, if needed, handling business name registration.

- For a Pty Ltd path, plan a more formal company setup with additional registration and ongoing compliance work.

| Cost lens | Sole trader | Company (proprietary limited company) |

|---|---|---|

| Visible setup items | ABN and possible business name registration | More formal company setup and registration tasks |

| Hidden setup load | Basic admin setup and record-keeping standards | More documentation and coordination discipline from day one |

| Ongoing admin effort | Lower at the start | Higher ongoing coordination and review workload |

| Tax treatment framing | Business income generally flows through to personal income tax treatment | Tax and reporting obligations differ from sole trader treatment |

| Switching later | You can switch later, but expect extra cost, complexity, and possible tax consequences | Late changes can still create cleanup work, extra cost, and possible tax consequences |

Use this fill-in budget template before you commit:

| Line item | Applies to | Timing | Your estimate | Owner |

|---|---|---|---|---|

| ABN setup | Sole trader | One-off | ||

| Business name registration | As needed | One-off | ||

| Company setup and registration steps | Company path | One-off | ||

| Bookkeeping software | Both | Recurring | ||

| Bookkeeping and reconciliation time | Both | Monthly | ||

| Advisor review time | Both | As needed |

If you start as a sole trader, you can still switch later. Expect extra cost and extra admin. There may also be tax consequences during transition.

Rule to run: pick the Australian business structure you can run reliably now. Review at fixed checkpoints instead of waiting for stress to force the move.

How much monthly admin can you actually run without breaking your workflow?#

If you cannot run a consistent monthly admin rhythm, choose the simpler structure you can execute without misses.

| Control | Practical standard |

|---|---|

| Traceable approvals | Log who approved pricing changes, write-offs, and payment exceptions. |

| Reconciliation pack | Store bank match reports, aged receivables, and open obligations in one monthly folder. |

| Clean handoff artifacts | Maintain concise summaries and source files your advisor can review quickly. |

| Formal obligations list | Maintain a formal obligations list before owner draws. |

| Payment approvals and release | Separate payment approvals from payment release where supported. |

You have priced setup and costs. Now test operational capacity. Missed admin creates real risk even when your structure looks correct on paper.

In freelance work, structure changes how you take pay and how you are taxed on that pay. Your monthly system has to match reality.

| Monthly control | Sole trader workflow | Company workflow |

|---|---|---|

| Records | Keep one source of truth for invoices, expenses, and contracts. | Keep the same core records, then separate company records from personal activity clearly. |

| Reconciliations | Reconcile bank activity and receivables monthly. | Reconcile monthly, with clear segregation and documented follow-up actions. |

| Invoicing | Issue, chase, and close invoices on a fixed weekly cadence. | Run the same cadence, with approval checks before write-offs or credits. |

| Owner pay handling | Draw cash withdrawals, then track them so year-end tax treatment stays accurate. | Run a planned owner pay mix, often salary and potentially dividends, with documented decisions. |

| Review cadence | Run one monthly owner review and log actions. | Run one monthly company review and keep clear notes on key decisions. |

Use this decision lens for admin capacity:

- If you routinely miss reconciliations, start with sole trader controls and harden them before adding company complexity.

- If you already run clean monthly packs, a company structure can be sustainable now.

Use the controls above as your baseline. For payment risk, keep execution practical:

- Maintain a formal obligations list before owner draws.

- Separate payment approvals from payment release where supported.

Picture a solo operator who adds more clients without changing review discipline. Cash arrives, but one missed reconciliation hides a payment gap. Choose the structure you can run monthly without drift, then add complexity only after your control routine holds.

When should you switch from sole trader to Pty Ltd?#

Switch from sole trader to Pty Ltd when liability, reporting obligations, and business complexity start to exceed what a simple structure can handle.

| Situation | Suggested move | Note |

|---|---|---|

| Simplicity and speed are your priority | Start sole trader | Keep setup lean. |

| Liability, reporting, and compliance demands are rising | Switch to company earlier | Move when you can reliably manage company-level obligations. |

| Records stay inconsistent | Fix operations before you incorporate | Add company complexity when your operating discipline can support it. |

| Older figures such as 27.5% company tax (2018/2019) or the $108,750 "magic number" | Do not use as current advice | The article says they were time-specific. |

You know what monthly admin you can run. Use that same operational lens to time the move, because structure only helps when your controls can support it.

Do not chase a single tax myth or one income number. Guidance on the two models compares costs, liability requirements, and reporting obligations. It also warns you to understand legal, reporting, and tax obligations before you switch.

| Switch signal | What you are seeing now | Practical move |

|---|---|---|

| Liability exposure | A dispute or contract issue would be harder to manage under your current setup | Consider moving earlier to a Pty Ltd structure |

| Reporting obligations | Your reporting and compliance needs are becoming heavier | Move when you can reliably manage company-level obligations |

| Admin maturity | You can run reconciliations, records, and regular reviews without misses | Add company complexity when your operating discipline can support it |

| Cost and setup tradeoff | You still need the leanest possible setup and minimal compliance | Stay sole trader while simplicity is the priority |

| Tax implications | You want to review tax options, noting sole trader income is taxed at personal income tax rates | Review with an advisor, and avoid universal income thresholds |

Use this rule set:

- If simplicity and speed are your priority, start sole trader and keep setup lean.

- If liability, reporting, and compliance demands are rising, switch to company earlier.

- If your records stay inconsistent, fix operations before you incorporate.

Historical tax examples are not current rules. Older figures such as 27.5% company tax (2018/2019) and the $108,750 "magic number" were time-specific and should not be used as current advice.

If you want the simplest default: start as a sole trader when simplicity and speed matter. Switch to Pty Ltd before liability, reporting, and complexity outpace your current controls.

The 90 day decision checklist you can execute this week#

Run a 90 day checklist that sets priorities early, then tightens controls before you scale.

| Window | Focus | Key actions |

|---|---|---|

| Week 1 | Priorities and setup | Choose your track for this cycle and document why; write a one page decision note with current setup, main risk, review date, and trigger for switching. |

| Week 2 to 4 | Control setup and delivery protection | Set one invoicing routine and follow it every week; standardize onboarding with scope, out of scope, approvals, and payment terms in writing; log approval changes and reprice before extra work starts. |

| Week 5 to 8 | Reporting cadence and escalation triggers | Run a regular records capture and reconciliation cadence; keep a clean reporting folder with invoices, expenses, contracts, and approval trail; escalate to a qualified advisor when records do not reconcile, reporting implications are unclear, or operating complexity jumps. |

| Week 9 to 12 | Scale readiness and switch review | Recheck whether your current structure still matches risk and growth; document a formal transition plan if contract pressure or role complexity rises; enforce audit-ready recordkeeping with traceable approvals, versioned contracts, and invoice to delivery linkage. |

Turn the decision into phased execution so your setup stays aligned with real client work, risk, and admin capacity.

Treat this as an operator playbook, not a rigid script. Adapt it to your workload, but keep the sequence: priorities first, controls next, review points after that.

- Week 1: priorities and setup

- Choose your track for this cycle and document why. * Write a one page decision note: current setup, main risk, review date, and trigger for switching. * If you need a refresher before deciding, read A Guide to Australia's ABN for Sole Traders.

- Week 2 to 4: control setup and delivery protection

- Set one invoicing routine and follow it every week. * Standardize onboarding: scope, out of scope, approvals, and payment terms in writing. * Log approval changes and reprice before extra work starts. * Keep contract hygiene tight, because weak onboarding drives scope creep, unpaid work, and expectation gaps.

- Week 5 to 8: reporting cadence and escalation triggers

- Run a regular records capture and reconciliation cadence. * Keep a clean reporting folder: invoices, expenses, contracts, and approval trail. * Escalate to a qualified advisor when records do not reconcile, reporting implications are unclear, or operating complexity jumps.

- Week 9 to 12: scale readiness and switch review

- Recheck whether your current structure still matches risk and growth. * If contract pressure or role complexity rises, document a formal transition plan. * Enforce audit-ready recordkeeping: traceable approvals, versioned contracts, and invoice to delivery linkage.

Imagine a freelance operator wins a larger retained brief and starts coordinating outside contributors. If controls hold and records stay clean, continue on plan. If risk concentration rises and documentation slips, trigger a formal structure review.

One page printable decision checklist#

| Gate | Yes | No |

|---|---|---|

| Chosen structure fits next 90 days | Execute current path this week | Decide now before taking new work |

| Core setup details are clear | Record status and move to controls | Resolve open setup questions first |

| Onboarding and contracts are standardized | Start every client with the same workflow | Pause new work until scope and approvals are fixed |

| Invoicing and records cadence is stable | Keep reporting pack current | Simplify workflow and restore consistency |

| Reporting questions are clear | Continue with internal cadence | Book a qualified advisor check-in |

| Scale signals justify a structure change | Start transition planning | Keep current setup and review again next cycle |

If you want a deeper dive, read Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

Choose the structure you can run well and review it on a schedule#

Pick the structure that matches your risk, growth plan, and operating discipline now, then review it on a schedule because switching can add cost, complexity, and potential tax consequences.

You have the decision points and the execution plan. Use them to make one clear call today, then stop relitigating it every week.

Treat this as an operating decision, not an identity decision. Both paths can work. The right choice depends on your goals, risk profile, and growth plans, and you can change later if you plan the move carefully.

| Decision lens | Stay sole trader now | Move to company (Pty Ltd) now |

|---|---|---|

| Legal position | You trade as an individual in your own legal capacity. Registering a business name does not create a separate legal person. | A proprietary limited company is a separate legal entity set up with ASIC. |

| Setup cost signals | Generally lower setup complexity, with fewer moving parts to coordinate. | Generally higher setup complexity, with more formal registrations and ongoing requirements. |

| Obligation profile | Simpler structure, but you still must run clean records and meet your obligations. | More complex reporting, legal, and tax obligations that require tighter controls. |

| Fit for your stage | Can fit when operations stay straightforward and risk remains manageable. | Can fit when risk, contract pressure, or growth plans justify added structure. |

If your delivery model is still simple, a sole trader setup can be a practical start. If your risk exposure and growth intent are rising, a Pty Ltd path can better match that next stage. Only do it if you can run the added compliance load.

One-line playbook: choose your structure, run it cleanly, and set clear triggers to reassess if risk, growth plans, or obligations change.

For next steps, review your ABN setup with A Guide to Australia's ABN for Sole Traders. Then review tax residency implications if your work spans borders. If cross-border workflow requirements matter, confirm fit and requirements before you commit.

Frequently Asked Questions

Should an Australian freelancer start as a sole trader or a company?

Start as a sole trader when you want the simplest setup and you can tolerate more personal exposure while you validate your offer. Choose a company when you need a separate legal entity for how you run the business and you can handle the added complexity and admin. Treat this as an operating decision, not a one-time identity choice.

At what point should I move from sole trader to Pty Ltd?

There is no universal revenue or profit trigger. Move when your business size, risk profile, or operating model starts to outgrow your current setup, and when growth may trigger different tax rules and liabilities. Plan the change carefully so your records and processes can support it.

What are the true setup and ongoing admin differences between a sole trader and a company?

A sole trader is simpler because one person owns the business and makes decisions. A company is a separate legal entity and is more complex to run, so admin and compliance are often heavier. If you trade under a name that is not your personal name, you must be on the business names register.

How does unlimited personal liability change day-to-day risk in freelance work?

As a sole trader, personal exposure is generally higher in day-to-day operations. That should change how you scope projects, approve changes, and manage payment risk. A company can help limit liability, but liability protection is not absolute in every scenario.

What records should I keep from day one to stay compliant in Australia?

Keep clear records of what you agreed, delivered, invoiced, and collected. Exact compliance requirements vary by structure and how you trade, and ASIC register obligations depend on your structure and the names you use in business. If you trade under a name other than your personal name, you must be on the business names register.

Is a company always better for tax outcomes than a sole trader?

No. Structure can affect tax, asset protection, and setup costs, and higher turnover may trigger different tax rules and liabilities. Choose based on your full business position and consult a tax professional as obligations evolve.

Can I start as a sole trader and switch later without major disruption?

You can start as a sole trader and switch later, but do not assume the move is frictionless. The level of disruption depends on planning, timing, and record quality. Keep documentation clean from day one so any transition is controlled.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- business.gov.au/planning/business-structures-and-types/busin...trusted

- dentons.com/en/insights/articles/2024/november/18/establ...external

- myob.com/au/blog/sole-trader-vs-company-key-differencesexternal

- nab.com.au/business/small-business/sole-trader-resource...external

- sleek.com/au/resources/company-or-sole-traderexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

Australia Tax Residency for Digital Nomads With GST and ABN Checkpoints

The goal is a defensible, low-drama position the Australian Taxation Office (ATO) can follow from your records, not a clever workaround. For a digital nomad, that usually means keeping two tracks straight: residency and GST/ABN admin. Consistency is what holds up over time: use real facts, take steps in a clear order, and keep documents that still match months later.

How Sole Traders Can Get an ABN in Australia and Stay Compliant

If your goal is to get an ABN in Australia without avoidable rework, use this section as your operating base, not as your eligibility ruling or form guide. The later sections cover the entitlement test, the ABR application itself, and what to do if you receive a reference number or a refusal.