Quick Answer

Form an LLC when your risk and operations warrant a legal boundary - rising client volume, larger scopes, or planned hiring. Keep tax strategy separate: an LLC does not change federal taxes by default. Obtain an EIN, open a business bank account, and use the LLC name on invoices to preserve the corporate veil and clean records.

Introduction: What "Upgrading to an LLC" Really Means#

Forming an LLC is usually an operations decision before it is a tax decision. If you are weighing a move from sole proprietor status to an LLC, start with exposure, contract risk, and how money moves through the business. Treat federal tax treatment as a separate choice, and verify it through IRS guidance instead of assumptions.

That framing matters because the real upgrade is not a nicer label or a more polished business name. It is a firmer boundary between business activity and personal activity. That boundary only holds if your day-to-day habits support it. If your work is still simple and low risk, waiting can be reasonable. If scopes, client demands, and obligations are growing, delay often creates more friction than it saves.

Before you file anything, do a quick reality check on the setup you already have. Pull recent contracts, look at your invoice flow, and trace where client money lands today. If personal and business details are mixed across documents and payments, the LLC question is less about branding and more about reducing avoidable confusion before it gets expensive.

A practical place to anchor the decision is the IRS Self-employed Individuals Tax Center. It pulls together the pages most freelancers need and gives you a reliable starting point before you form anything. The pages worth reviewing first are:

- Self-employed Individuals Tax Center

- Business structures

- Information return

- Who is self-employed?

Read those before you create an entity. They help clarify what changes when you form an LLC and what stays the same.

Two habits keep this decision grounded. First, verify before you file. Open the IRS Self-employed Individuals Tax Center, review the Business structures page, and bookmark Information return so payer reporting rules are easy to check later. If you want a practical warning list, compare your current setup against these freelance red flags. Second, write your reason for forming now in one sentence. Larger scopes, vendor onboarding pressure, or near-term hiring plans are concrete reasons. "It sounds more professional" usually is not enough on its own.

That sentence is not busywork. It becomes your quality check after the switch. Six months later, you should be able to point to cleaner contracts, cleaner payment records, or easier onboarding and say the change solved a real operating problem.

Keep one distinction clear from the start. Forming an LLC does not automatically change federal tax treatment. Use IRS materials to understand default treatment first, then evaluate any optional tax path separately. If you want a focused walkthrough of that separate decision, see The S-Corp Election for LLCs: A Tax-Saving Strategy for High-Earning Freelancers.

With that framing in place, the decision gets much easier: look at risk, look at operations, and then decide whether the legal wrapper is doing real work for you now.

The Upgrade Decision at a Glance#

Here is the short version: make this call based on liability exposure and operating reality, not on hopes of immediate tax savings. As a sole proprietor, you and the business are the same legal person by default. As client load and contract scope grow, an LLC can create a clearer legal boundary, but only if you actually run the work as a separate business.

If tax reduction is your only reason, pause and split the choice into two steps. First decide whether the legal boundary is useful now. Then evaluate tax options with a professional as a separate move. That sequencing keeps the decision cleaner and lowers the chance that you form for the wrong reason.

Use the IRS Business structures overview to orient yourself, then confirm the formation and maintenance basics in your state portal before you commit. Your reasoning should stay simple enough that you can explain it in one sentence six months from now.

| Trigger | What you are seeing | Action |

|---|---|---|

| More clients and larger scopes | Multiple active projects and broader terms | Form an LLC and operate as a separate business across contracts and records. |

| Only goal is tax savings | No meaningful change in risk or exposure | Stay a sole proprietor for now and revisit tax strategy later. |

| Clients treat you as a vendor or company | Onboarding packets and contracts expect a business name | Consider an LLC to align contracts, invoicing, and vendor records. |

| Planning to pay others for project work | You expect to engage subcontractors on deliverables | Consider whether an LLC helps keep obligations, payments, and records distinct from personal activity. |

Before you act, run two quick checkpoints.

The first is decision quality. Review the IRS Business structures page, then visit your secretary of state portal and confirm the basic formation and maintenance requirements. Capture your reason in a short note, such as a clearer liability posture for larger statements of work. That gives you something concrete to test later. Did the change actually improve how you contract, bill, and maintain records?

The second is execution readiness. If you formed tomorrow, could you keep the entity name consistent across contracts, invoices, and bank records without monthly cleanup? If not, spend a short cycle fixing naming and account habits first. That prep work usually prevents more friction than it creates.

The most common failure mode is simple. Someone files the LLC and then keeps operating as if nothing changed. Mixing personal and business behavior weakens the line created on paper. Use the entity name in agreements, keep records consistent, and stop letting personal details spill into business documents unless they are truly required.

If your work is still small and low risk, staying a sole proprietor while you monitor exposure is a valid choice. If you want a deeper side by side comparison, see Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers. If your next move is implementation, run a quick account and contract separation check and then browse Gruv tools if you need help putting it into practice.

The first place to pressure-test that choice is client and contract risk.

Liability and Client-Risk Triggers You Shouldn't Ignore#

If your contracts are getting bigger, broader, or more one-sided, waiting gets harder to justify. A sole proprietor has no legal separation between business obligations and personal assets. An LLC can strengthen that separation, but only when contracts, billing, and banking all match the entity in daily practice.

In practice, the warning signs usually show up before any major dispute does. You may be signing larger statements of work, managing more clients at once, or accepting terms that shift more responsibility onto you. Each step increases the chance that a routine disagreement becomes a serious distraction.

Track exposure in three places.

- Broader work and more clients: Larger scopes and concurrent projects increase the surface area for missed expectations, delays, and payment disputes.

- Contract red flags: Risk-shifting language deserves close review. Non-compete clauses in contractor agreements can also raise classification concerns and should trigger a second look before you sign.

- Operations and money flow: Use an EIN to open a business bank account, route client receipts there, and build business credit under the entity. Use the LLC name on invoices and vendor profiles so the record tells one consistent story.

The goal is not to predict every worst case. It is to reduce routine points of confusion that make disputes harder to resolve. When the name on the contract, the invoice, and the bank record all match, you spend less time defending basic facts and more time resolving the actual issue.

Before you decide, test whether you can actually operate the way the entity requires. Good intentions are not enough. Use these checkpoints:

- Contracts checkpoint: Review active agreements for risk-shifting terms and non-compete language, then request edits or narrower language where needed.

- Evidence pack checkpoint: Gather current scopes of work and the past year of Form 1099 patterns to identify concentration risk and payer dependency.

- Banking separation checkpoint: Issue a small invoice under the LLC name and EIN, deposit it to the business account, and reconcile it in your books.

Treat these as go/no-go tests, not documentation theater. If you cannot pass them now, the timing may be early. If you can pass them quickly, you are usually in a much stronger position to make the switch and keep it clean.

A few failure modes repeat. The first is forming the entity while continuing to mix personal and business activity, which weakens separation. The second is signing new scopes without reviewing the risk terms, which leaves exposure mostly unchanged in practice. The third is treating LLC status as full protection even though the supporting documents are inconsistent.

If your work is narrow and low stakes, document that assessment and continue as a sole proprietor while you monitor the triggers above. If those triggers are already present, form the LLC, adopt EIN-based banking, and keep a clean contract and payment trail so the line holds when it matters.

Once exposure justifies the legal boundary, the next question is tax treatment, and that needs its own analysis.

Tax Reality vs. Myths for Freelancers#

Most bad LLC decisions start with a tax myth. The core tax truth is simple: an LLC does not change taxation by default. For a single-member LLC, business income is generally reported on Schedule C with Form 1040. Any potential savings usually come only after a separate S-corp election with the IRS, and that election adds payroll and compliance obligations that do not disappear after setup.

Keep the concepts separate in both your thinking and your process. The LLC is the legal wrapper. The S-corp election is a tax choice you may apply to that wrapper. When people blur those together, they mis-time decisions, assume savings that are not there, and add administrative weight before the business is ready.

That confusion creates practical problems. Someone hears that an LLC helps taxes, files the entity, and assumes the tax side is handled. Filing season arrives, and they discover their default treatment never changed. The cost is not just money. It is also rushed decisions, messy cleanup, and avoidable stress.

Once an S-corp election is in place, you are expected to run payroll and pay yourself a reasonable W-2 salary. That means recurring process, cost, and accountability. For freelancers with steady profits, the tradeoff can be worth it. For businesses with variable income, the added overhead can outweigh the upside for long stretches.

| Myth | Reality |

|---|---|

| An LLC automatically lowers taxes | A single-member LLC reports on Schedule C with Form 1040 by default. |

| S-corp is a different business entity | S-corp is a tax election applied to an LLC or corporation. |

| Forming in the right state avoids taxes | State selection does not eliminate tax obligations, so avoid state-shopping for tax alone. |

Before making any tax move, run three practical checks.

- Return check: Open last year's Form 1040. If your LLC has no election, you should see Schedule C treatment reflected there.

- Election readiness check: If you and a CPA are considering S-corp, map payroll setup, recurring filings, and clear task ownership.

- Income stability check: If most revenue is variable 1099 income, model more than one scenario before committing to salary obligations that run on a fixed schedule.

These checks force realistic planning. If payroll ownership is unclear, that is a warning sign. If income swings heavily, that is another. You can choose the election later, but it should happen when you can meet the ongoing requirements without scrambling.

The mistakes here are predictable. One is forming an LLC and assuming taxes already changed, then discovering at filing time that default treatment never moved. Another is electing S-corp and failing to run payroll consistently, which turns an intended benefit into a compliance problem. If profits are still uneven, keeping Schedule C treatment for now can be the cleaner move until the numbers and the process stabilize.

If you want a focused walkthrough of the separate election decision, see The S-Corp Election for LLCs: A Tax-Saving Strategy for High-Earning Freelancers.

Even if you keep default treatment, the upgrade can pay off through cleaner administration. That is where most of the day-to-day value shows up.

Operational Signals: EIN, Banking, and Hiring Readiness#

If you cannot keep identity and money flow clean, the upgrade stays mostly on paper. The practical gains come from a dedicated business identity, clearer books, and smoother client onboarding. By default, taxes still follow sole proprietor treatment unless you make a separate election later, so the immediate value here is operational clarity.

Clients usually respond well when vendor records are consistent. In practice, that means the company name, invoices, payment flow, and onboarding details all point to the same entity without repeated explanations or monthly cleanup.

This matters more as your client base grows. Every onboarding packet becomes a small stress test. If names and tax details are inconsistent, those tests fail in slow, annoying ways that delay payment and force retroactive fixes.

Start with the basics and get them right before you optimize anything else:

- Open a dedicated business bank account in the LLC name and route business income and expenses through it.

- Use that same name across invoices, onboarding forms, and agreements.

- Use an EIN for business records and banking, and keep that record ready if payroll or vendor requests show up later.

- Run a verification check by sending a test invoice with the LLC name, confirming the deposit to the business account, and reconciling the entry in your books.

Hiring readiness is one of the clearest operational thresholds because it forces discipline. If you expect to pay contractors or bring on an employee, keep agreements, approvals, and payment records under the entity so the documentation matches how money moves.

Two guardrails matter. First, do not assume tax savings from formation alone. A single-member LLC remains taxed like a sole proprietorship by default unless you make a separate election. Second, do not commingle personal and business spending. Clean books and business-first behavior are what make the upgrade meaningful in real life.

When those basics are working, the next risk area is state administration. That is where a lot of otherwise solid setups start to drift.

State Formation and Maintenance Differences#

A clean entity setup can become messy if state upkeep gets treated as an afterthought. Formation and maintenance are controlled by state rules, so your best source is always your state's official portal. Use that portal as the authority for filings, deadlines, and status details, then make sure bank and client records match the state record exactly.

Start with primary sources and keep a clean trail from day one. Your secretary of state site explains how to form and maintain the entity, and the SBA registration guide can help you find the right state links if you need orientation. Avoid relying on secondhand summaries for due dates or filing obligations. As you move through setup, record the exact entity name, the portal URL, the approval documents, and any entity ID issued by the state.

That discipline matters because maintenance is not uniform, and those differences affect operations quickly. Common obligations include a periodic report, a public contact or agent record, and local licensing touchpoints. Treat these as recurring calendar obligations, not one-time setup noise. A missed filing can trigger unnecessary re-verification work with banks, platforms, and clients.

A practical way to stay ahead is to create a small compliance calendar with owners and due months. Keep it close to your banking and vendor setup files so annual tasks are visible where daily work already happens. The point is not process for its own sake. The point is to avoid rushed fixes when a client or bank asks for updated status.

If your services or clients span multiple states, track facts before you interpret rules. Keep an operations log that notes where services are performed and where business addresses or office space are maintained. That gives you neutral input for advisor conversations if registration questions arise later.

For orientation only, you can review how a state such as Texas structures filing categories to understand what these portals commonly ask for. Then confirm every action in your own state's site before you submit anything.

Use this file and calendar checkpoint once formation is approved:

- Download and store the formation approval with banking and onboarding records, labeled with your entity ID if one is assigned.

- Open or update your business bank account so the entity name matches state approval exactly.

- Add reminders ahead of the due months listed on your portal for recurring submissions.

- Keep a one-page state summary with formation notes and maintenance obligations near vendor W-9s and client setup files.

That state-first habit reduces admin drag later. It also keeps identity consistent across state records, payables, and onboarding. If you want a structural refresher before filing, see Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

Once the state record is clean, the switch itself becomes much easier to execute without rework.

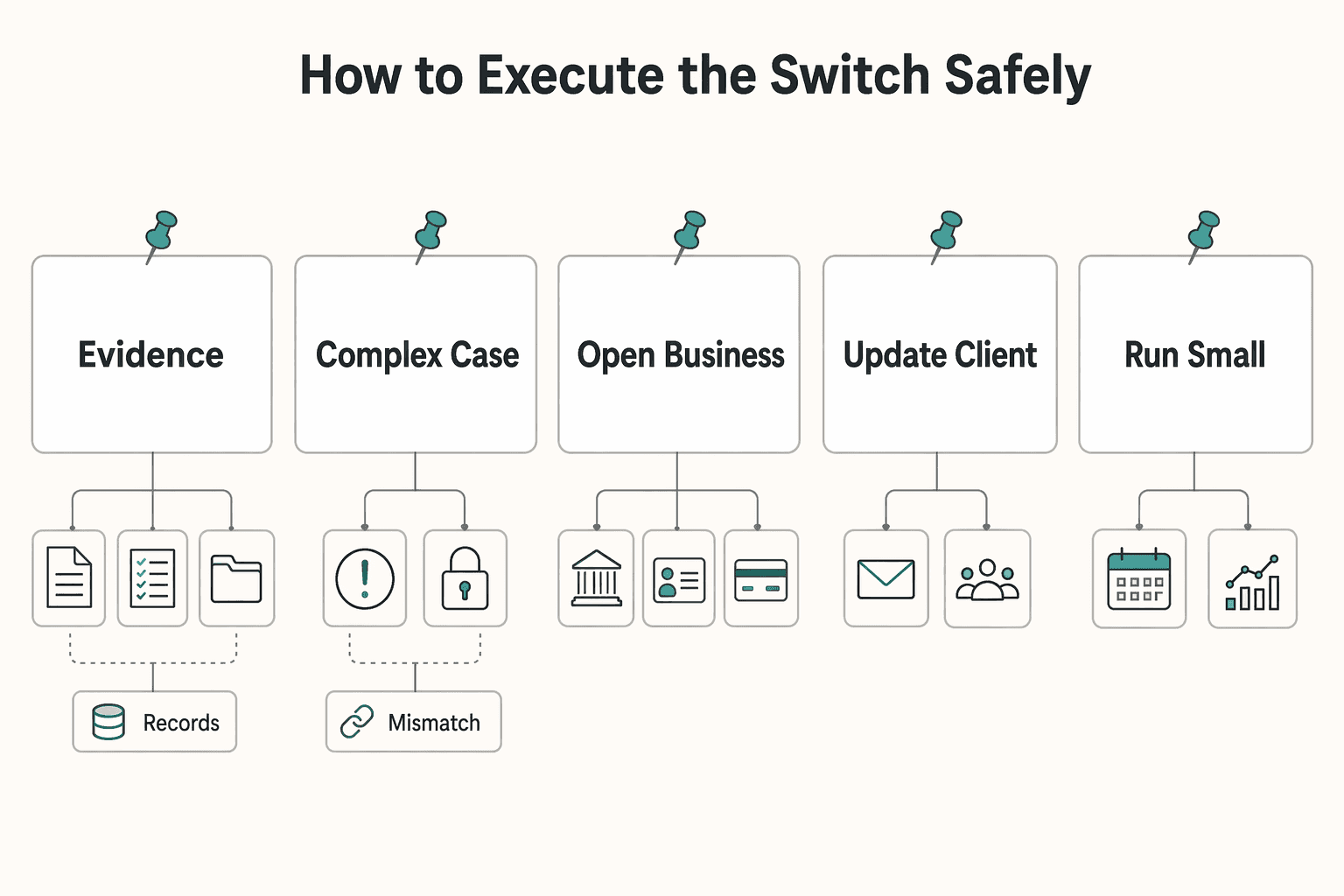

How to Execute the Switch Safely#

Once you decide to form, order matters more than speed. A clean switch is mostly about sequence and record discipline. Move in a way that keeps the entity name, EIN, banking, and client records aligned from the start. Tax planning can run in parallel, but it should not block the core setup.

| Step | Action | Key detail |

|---|---|---|

| 1 | Choose an LLC name you can keep consistent across state records, bank setup, invoices, and vendor profiles. | Keep the name consistent across records. |

| 2 | File formation with your state and store the approval documents and entity ID in one place. | Store approval documents and entity ID together. |

| 3 | Obtain an EIN from the IRS for the LLC to support account setup, payer records, and hiring when needed. | Supports account setup, payer records, and hiring. |

| 4 | Open a business bank account in the LLC name and route client payments there. | Keep client payments in the business account. |

| 5 | Update client onboarding data and invoice templates to show the LLC name and EIN. | Use the LLC name and EIN in client records. |

| 6 | If you may evaluate S-corp later, coordinate the timing with your accountant and keep that tax decision separate from entity setup. | Keep tax election timing separate from entity setup. |

If you want the same sequence in checklist form:

- Choose an LLC name you can keep consistent across state records, bank setup, invoices, and vendor profiles.

- File formation with your state and store the approval documents and entity ID in one place.

- Obtain an EIN from the IRS for the LLC to support account setup, payer records, and hiring when needed.

- Open a business bank account in the LLC name and route client payments there.

- Update client onboarding data and invoice templates to show the LLC name and EIN.

- If you may evaluate S-corp later, coordinate the timing with your accountant and keep that tax decision separate from entity setup.

That sequence is practical guidance, not a legal mandate. Its value is simple: each step supports the next and reduces rework. If records drift during setup, cleanup often takes longer than the original switch.

A safe switch also includes legacy cleanup. Update old invoice templates, contract templates, and vendor profiles that still use personal details. If old and new records coexist for too long, clients and platforms tend to use whichever version they saw first, and you can spend months untangling mismatches that were easy to prevent.

Before you treat the transition as complete, run a small live test and tighten the file set:

- Run a small client payment through the business account and confirm it reconciles in your books.

- Verify that the bank account title exactly matches the state approval.

- Store the formation approval, EIN assignment notice, and bank onboarding documents with client setup files.

- At year-end, track which clients issue Form 1099s and confirm those records reflect the LLC details used in onboarding.

Watch for a few failure modes here, because they are easy to miss when you are focused on setup:

- Opening the business account but continuing to run personal spending through it.

- Leaving your SSN in legacy vendor records after moving operations to EIN-based business records.

- Letting names drift across state records, bank profile, and invoices, which can trigger re-verification or delayed payments.

Handled this way, the switch produces immediate operational gains: cleaner payer records, cleaner bookkeeping, and a stronger business identity for contracts and hiring. Keep monthly reconciliation tight, keep naming consistent, and calendar state maintenance items as soon as they appear in your portal.

For a deeper view of tax election timing after setup, see The S-Corp Election for LLCs: A Tax-Saving Strategy for High-Earning Freelancers.

Common Mistakes and Red Flags to Avoid#

Most LLC problems are behavior problems, not filing problems. The paperwork rarely fails on its own. Drift does. Liability protection depends on whether you actually operate as a separate business after formation. The fastest way to weaken your position is to treat that separation as optional in everyday transactions.

Drift usually starts quietly during busy periods. A personal card gets used for a business charge, an old invoice template gets reused, or a vendor file keeps legacy tax details because updating it feels low priority. None of those choices looks serious in isolation, but together they erode the consistency that makes the entity useful.

The core controls are simple, but they only work when followed consistently:

- Separate money: Use a business bank account titled in the LLC name and route client payments there. Avoid paying personal expenses from business cards, and avoid casual transfers that blur purpose.

- Match the entity name exactly: Keep the approved name consistent across the state approval, bank profile, invoices, and vendor records.

- Do not mix up entity formation and tax treatment: Formation alone does not change default federal tax treatment. Coordinate any election and related compliance work with an advisor.

- Update W-9 records: When payers request Form W-9, provide the LLC name and EIN so reporting points to the business record.

- Store formation records cleanly: Confirm approval details and entity ID early so you can answer client and bank verification requests quickly.

Red flags usually show up long before they become expensive:

- Client deposits landing in a personal account.

- Personal charges appearing on the business account.

- A payer file showing SSN-based W-9 details after you moved operations to the LLC.

- Mismatched entity names across the state portal, bank profile, and invoice templates.

- Missing or incorrect details on formation approval documents.

A short monthly review catches most of this drift:

- Send one test invoice from the LLC profile, verify the deposit to the business account, and reconcile it to the invoice number.

- Check at least one active client vendor profile to confirm the LLC name and EIN are on file.

- Keep the formation approval and EIN assignment with current vendor W-9s so re-verification takes minutes, not days.

If this sounds strict, that is the point. Consistency turns LLC status into practical protection and smoother payment operations. Sloppy records create preventable disputes. Clean records make your position boring, clear, and easier to defend.

For a deeper comparison before or after cleanup, see Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

30-60-90 Day Upgrade Pilot#

If timing still feels fuzzy, run a 90-day pilot before filing. For example, we recommend a simple tracker for contract risk, invoice flow, and onboarding friction so you can test the upgrade with real operating evidence. By day 30, day 60, and day 90, your notes should show whether the LLC would remove recurring rework. We are not trying to predict every outlier; we are trying to measure real operating friction. Otherwise, you can delay with confidence instead of guessing.

Risk and Revenue Signals#

Specifically, flag any month where one client exceeds 40% of revenue, or where one contract exposes more than $10,000 in potential rework. In contrast, if no client is above 20% and scopes stay narrow, you may stay a sole proprietor while you keep monitoring. We use this threshold approach because it helps you make a cleaner call before urgency takes over.

Operations Readiness Signals#

Meanwhile, track whether you can run your process in the business name without cleanup: invoice template, vendor profile, and bank deposit trail. Additionally, log how much time your admin cleanup takes each month. If the cleanup load stays above 2 hours, the boundary is likely already needed. Therefore, if your cleanup drops below 30 minutes and naming stays consistent, you can revisit later with less risk.

- Target 1: keep at least 90% of invoices in the exact legal name you plan to register.

- Target 2: keep personal spend at $0 on the business card during the pilot window.

- Target 3: keep vendor re-verification caused by name or tax-ID mismatch below 1 request per quarter.

Conclusion: Make the Upgrade When Risk and Operations Warrant It#

The right time to upgrade is when exposure and operating complexity justify a stricter boundary, not when the label simply sounds more professional. Forming the entity is the easy part. The value comes from running contracts, banking, and records in a way that keeps business activity separate from personal activity.

If several of the following are already true, your case for forming is stronger:

- You are signing larger statements of work with indemnity, IP, or privacy obligations.

- You are managing multiple active clients and invoice volume is rising.

- You plan to hire contractors or occasional employees and need cleaner onboarding and payment records.

- Clients request forms that require a business name or EIN.

- You want client receipts and vendor payments fully outside personal accounts.

Use these triggers as a decision checkpoint, not as a scorecard. You do not need every signal to be present. You need enough operating complexity that separation solves real problems and enough discipline to maintain that separation after formation.

Keep tax strategy on its own track. An LLC can elect S-corp taxation, but that decision only works when expected savings justify the added payroll and compliance work. If profit is still uneven, default treatment may be the simpler option until the numbers stabilize and your process can support extra obligations.

Before you call the switch complete, use one final checkpoint:

- Obtain an EIN and open a business bank account in the exact LLC name.

- Update invoices and vendor records to reflect that name and EIN.

- Run a small payment through the business account and reconcile it in your books.

- Store the formation approval, entity ID, and EIN notice in one place for fast verification responses.

The main red flag to avoid is commingling. When personal and business money paths overlap, the practical benefits of the entity weaken quickly. Keep separation tight, reconcile monthly, and maintain naming consistency across operational touchpoints.

If you are still early, low risk, and building baseline revenue, staying a sole proprietor is fine. Keep records clean, save tax forms, and revisit the upgrade triggers as scopes and obligations expand. For many freelancers, the most reliable rule is simple: upgrade when liability, client complexity, or hiring plans increase and you are ready to operate with consistent separation and disciplined recordkeeping.

For a deeper side by side on structure tradeoffs, see Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers. If you want help applying this checklist to your setup, talk to Gruv.

Frequently Asked Questions

Does an LLC save taxes for freelancers?

No. An LLC is a legal structure and, by default, you report taxes much like a sole proprietorship. Any different tax treatment would come from a separate S-corp election with the IRS, not from forming the entity itself. Keep entity choice and tax strategy as separate decisions.

When is the right time to form an LLC as a freelancer?

Use operational signals. If client volume is rising, you want a business identity, you want to open a business bank account and build business credit (an EIN helps), or you plan to hire, forming an LLC can be practical. If you are wondering when to form an llc for freelance work, move when those needs appear and you can maintain clean records from day one.

Do I need an EIN if I’m a single-member LLC?

It is useful. An EIN helps you open a business bank account, build business credit, and supports hiring. Store the EIN notice with your formation approval so you can share it quickly during vendor checks.

What’s the difference between an LLC and an S-corp election?

An LLC is the legal entity. An S-corp is a tax designation you may elect for that entity; it is not a separate company. You can run as a single-member LLC without the election, then evaluate the election later with your accountant. For a deeper look at that choice, see The S-Corp Election for LLCs: A Tax-Saving Strategy for High-Earning Freelancers.

Is staying a sole proprietor fine when I’m just starting?

Yes. If you have not formed an LLC, you are a sole proprietor by default, and you can begin that way. Keep clean books and save client tax documents you receive.

Which state should I form my LLC in?

Requirements differ by state. Verify the process on your state’s official portal and file the Articles of Organization as directed. After approval, open banking in the LLC’s legal name and keep the approval and EIN notice together.

Can I hire contractors under a single-member LLC?

Yes. With an EIN, you can pay contractors under the business identity. Keep agreements and payments in the LLC’s name.

Watch

When Should a Freelancer Form an LLC?

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- irs.gov/businesses/small-businesses-self-employed/se...trusted

- devlinpeck.com/content/red-flags-for-freelancersexternal

- healthjournalism.org/blog/2025/09/should-freelance-journalists-ge...external

- mylance.co/post/should-you-set-up-an-llc-for-your-freel...external

- oboe.com/learn/forming-an-llc-for-freelancers-1rkx9fh...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

S-Corp Election for LLCs for High-Earning Freelancers

Make this a practical go-or-no-go checkpoint, not a promise of outcomes. Proceed only if you can run the ongoing admin consistently, not just file paperwork once. If execution will happen "later, when things calm down," treat that as a no for now.

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.