Quick Answer

Choose BVI when you want an efficient holding setup with lower operational friction, and choose Cayman when institutional credibility or fund-facing expectations are central to your plan. In bvi vs cayman for holding company decisions, the critical test is operational fit after formation: governance discipline, filing ownership, and bank-ready documentation. If U.S. persons are involved, check Form 5471 and CFC implications early, and plan for CRS-driven reporting transparency rather than secrecy assumptions.

As your work grows, the financial side gets harder to manage casually. What starts as straightforward invoicing can turn into retained capital, liability exposure, and enterprise clients with stricter requirements. At that point, a more formal company structure is not just optional. It becomes a strategic decision. The comparison often narrows to two leading jurisdictions: the British Virgin Islands and the Cayman Islands.

The mistake is to start with fee schedules and treat this like a shopping exercise. Use a simple three-stage process instead: get clear on why the company exists, match that purpose to the right where, then commit to the how of running it properly. When those pieces line up, the structure can support asset protection, cleaner operations, and growth.

Stage 1: The 'Why' Audit - Defining Your Holding Company's Primary Job#

Start here: before you compare BVI and Cayman, decide the one primary job your holding company must do. If you skip this step, you can end up paying for complexity you do not need, or overlooking reporting obligations you do need.

One company can support more than one goal, but you still need a lead objective. That objective should drive your jurisdiction choice in Stage 2.

Pick the job before you pick the jurisdiction#

Use this table as your decision filter:

| Primary job | When this is your real priority | What to verify now | Common mistake |

|---|---|---|---|

| Liability ring-fencing | You want contracts, receivables, and assets held by a separate legal person | Identify exactly which contracts, accounts, and assets move into the company, and who signs going forward | Incorporating, then continuing to contract and operate in your personal name |

| Centralized investing | You want one entity to hold retained profits and investments | Confirm bank or broker onboarding requirements, including beneficial owner and tax documentation | Assuming privacy means invisibility to tax authorities |

| Compliant tax treatment | You want reporting handled correctly from day one | Map ownership and control, and assign responsibility for foreign-corporation filings | Forming first, then discovering CFC or Form 5471 issues late |

| Enterprise-facing credibility | You need a company that works for procurement, larger clients, or future fund-facing activity | Clarify whether you only need a corporate counterparty or regulated or institutional features | Choosing a heavier structure when a simpler operating company would do |

Liability ring-fencing#

If separation is the point, make the separation real. The company needs to hold the contract, account, or asset in practice, not just in your org chart. For BVI pathways, the BVI Business Company (BVIBC) is the core legal-person vehicle, and setup requires a registered agent.

Centralized investing#

If the main goal is to centralize ownership of capital, a holding company can make operations cleaner. It does not remove your home-country tax obligations. Be careful with the word "privacy." CRS is built on annual automatic exchange of financial account information between jurisdictions, and transparency frameworks still apply.

Compliant tax treatment#

If U.S. persons are involved, test this early. A foreign corporation is a CFC when U.S. shareholder control is more than 50 percent. Form 5471 is used by certain U.S. persons to satisfy reporting under IRC sections 6038 and 6046.

| Topic | Article detail | Value |

|---|---|---|

| CFC threshold | A foreign corporation is a CFC when U.S. shareholder control is more than 50 percent | >50 percent |

| Reporting form | Form 5471 is used by certain U.S. persons under IRC sections 6038 and 6046 | IRC 6038 and 6046 |

| Initial penalty | IRS guidance states an initial penalty may be assessed per Form 5471 per year | $10,000 |

| Continuation penalty | Continuation penalties may be assessed per form | Up to $50,000 |

Form 5471 does not apply to every owner in every case. But if your facts trigger filing, penalties can be material. IRS guidance states an initial $10,000 per Form 5471 per year may be assessed, with continuation penalties up to $50,000 per form.

Enterprise-facing credibility#

This becomes the lead objective when your company needs to satisfy procurement, support larger counterparties, or credibly sit in a fund-facing structure. In fund contexts, Cayman's framework matters. CIMA regulates certain fund categories under the Mutual Funds Act, and its Registered Fund criteria include a minimum aggregate equity interest figure of CI$80,000 (US$100,000). Cayman's Economic Substance regime has been in force since 1 January 2019.

Before you move to Stage 2, write down your answers to these five points:

- Your primary job for the next 24 months: ring-fencing, investing, compliant tax treatment, or enterprise credibility.

- Whether any U.S. person will own or control the company, and whether the more than 50 percent CFC threshold could be met.

- Which contracts, accounts, and assets will sit in the company on day one.

- Whether your plan assumes secrecy, despite CRS and beneficial-ownership transparency rules.

- Whether you need only a corporate counterparty or genuinely need fund or investor-facing capability.

If you want a deeper dive, read US LLC and BVI Company Blueprint for Asset Protection.

Stage 2: The 'Right-Sizing' Matrix - Matching Jurisdiction to Ambition#

Use this rule: match your jurisdiction shortlist to who needs to trust your company in the next 24 months. Treat early BVI or Cayman preferences as hypotheses, then verify them in writing before you decide.

That is a sizing decision, not a status decision. What you are really choosing is the level of governance, documentation discipline, and recurring administration your plan can support.

| Selection question | If BVI is on your shortlist | If Cayman is on your shortlist |

|---|---|---|

| Typical use case | Write your intended use case first, then ask whether a BVI structure fits that exact plan. | Use the same written use case, then ask whether a Cayman structure fits that exact plan. |

| Legal form fit | Ask for the exact legal form in writing, why it fits your stated use case, and which annual obligations come with it. | Ask for the same written form-fit memo, and require a clear reason beyond optics. |

| Banking and investor expectations | Expect full KYC and a coherent activity narrative; simplicity does not remove scrutiny. | Expect full KYC and a coherent activity narrative; if institutional counterparties are likely, prepare a fuller evidence pack on control, purpose, and operations. |

| Compliance workload | Request a dated annual compliance calendar before filing, including ownership updates and recurring filings; ask whether your model may trigger extra-territorial requirements or other cross-border obligations. | Request the same dated annual compliance calendar and ask whether your model may trigger extra-territorial requirements or other cross-border obligations. |

| Cost band | Current cost range pending provider, legal, or source-record verification. Compare all-in first-year and recurring costs, not just formation fees. | Current cost range pending provider, legal, or source-record verification. Use the same all-in template so the comparison is like-for-like. |

Why institutional context can matter#

If your path includes institutional conversations, check whether your structure will read clearly in that environment. One practical signal is how active and recurring the fund-finance network is. The Fund Finance Association describes its events as bringing together investors, fund managers, bankers, service providers, and lawyers, with annual events in Miami, London, and Asia. Its Global Symposium ran February 02 to 04, 2026, with listed individual passes at $3,000.

That does not prove one jurisdiction is always better. It does show the level of documentation and operating discipline institutional participants tend to expect.

Before anyone files, use a written verification checklist#

Have each provider answer the same questions in writing:

| Verification item | Question |

|---|---|

| Entity proposal | What exact entity are you proposing, and why does it fit my stated use case? |

| Cost | What is the full first-year and recurring annual cost, itemized? |

| Onboarding documents | What onboarding documents do you need from me now? |

| Annual deliverables | What annual deliverables will I own, and on what timetable? |

| Regulatory review | Could my planned activity trigger licensing or other regulatory review? |

Do not hand this off to loosely coordinated third parties and assume the details will settle themselves. Process control matters, and fragmented handoffs create avoidable failures.

Split the digital-asset use case early#

Digital assets are a good example of why you should separate use cases early. If the company will hold only your own digital assets, treat it as a proprietary holding setup. Keep your documentation clear on ownership, funds flow, and service-provider relationships.

| Activity | How the article frames it | What to do |

|---|---|---|

| Hold only your own digital assets | Treat it as a proprietary holding setup | Keep documentation clear on ownership, funds flow, and service-provider relationships |

| Touch client assets | Flag it for jurisdiction-specific regulatory review rather than assuming a standard setup | Get jurisdiction-specific advice before incorporation and before account opening |

| Execute for others | Flag it for jurisdiction-specific regulatory review rather than assuming a standard setup | Get jurisdiction-specific advice before incorporation and before account opening |

| Pool outside capital | Flag it for jurisdiction-specific regulatory review rather than assuming a standard setup | Get jurisdiction-specific advice before incorporation and before account opening |

| Provide exchange-like or custody-like activity | Flag it for jurisdiction-specific regulatory review rather than assuming a standard setup | Get jurisdiction-specific advice before incorporation and before account opening |

If the business may touch client assets, execute for others, pool outside capital, or provide exchange-like or custody-like activity, flag it for jurisdiction-specific regulatory review rather than assuming a standard setup. Get jurisdiction-specific advice before incorporation and before account opening.

If that distinction points you in a direction, use it as a verification prompt, not a conclusion. Then move to Stage 3 and pressure-test that choice through execution: KYC, beneficial-ownership records, and recurring filings.

For a step-by-step walkthrough, see Why Banking a Cayman or BVI Company Gets Complicated.

Stage 3: The 'Compliance-First' Checklist - An Action Plan for Peace of Mind#

Once the company is live, execution becomes the real risk. Run one written checklist, one owner map, and one live calendar from day one.

| Workstream | What you must do | BVI | Cayman |

|---|---|---|---|

| Filing type confirmation | Confirm the filing is framed as Form 6-K (Report of Foreign Private Issuer) and keep that label explicit in your internal workflow. | Jurisdiction-specific follow-on requirements are not established in this excerpt; verify locally. | Jurisdiction-specific follow-on requirements are not established in this excerpt; verify locally. |

| Annual report form path | Document the check-mark decision on whether annual reports are filed under Form 20-F or Form 40-F, and assign a clear owner. | Local implications are not established in this excerpt; verify locally. | Local implications are not established in this excerpt; verify locally. |

| Exhibit control | Track that Exhibit 99.1 (2018 Annual Report, dated April 11, 2019) and Exhibit 99.2 (2018 Sustainability Report, dated April 11, 2019) are listed and retrievable. | Any local exhibit or registry requirements are not established in this excerpt; verify locally. | Any local exhibit or registry requirements are not established in this excerpt; verify locally. |

| Forward-looking statements review | Treat forward-looking language as explicitly uncertain and risk-bearing, and route it for review before sign-off. | Jurisdiction-specific treatment is not established in this excerpt; verify locally. | Jurisdiction-specific treatment is not established in this excerpt; verify locally. |

| Filing metadata log | Record key submission metadata (for example, filed-as-of date 20190412 and public document count 220) in your tracker. | Any local filing-calendar overlays are not established in this excerpt; verify locally. | Any local filing-calendar overlays are not established in this excerpt; verify locally. |

Start with your filing map#

Do not wait until year-end to sort filing responsibilities. Ask your adviser for a one-page workflow that names who prepares each input, who reviews it, and who files it. Where a trigger, deadline, or penalty is not stated in this excerpt, label it clearly as "verify before filing season."

Confirm the annual report form path early#

Before filing season, make an explicit call on the Form 20-F versus Form 40-F path and document who owns that check-mark decision. If your team cannot explain that decision clearly and in writing, pause and resolve the gap first.

Plan for exhibit and record hygiene#

Keep the listed exhibits and dated versions easy to retrieve, and keep your filing log current. Clean records reduce friction during review cycles and make cross-checking faster when filing questions come up.

Set execution order now#

Set the order now so things do not drift later: assign responsible owners, maintain the filing calendar, centralize core filing artifacts, and run an annual review. Jurisdiction-specific obligations for BVI or Cayman are not established in this excerpt and should be verified separately. If you want a related example, see Cayman Islands LLC for Global Solopreneurs Who Want Fewer Compliance Surprises.

Before you lock your compliance workflow, organize your cross-border reporting assumptions in one place with the Tax Residency Tracker.

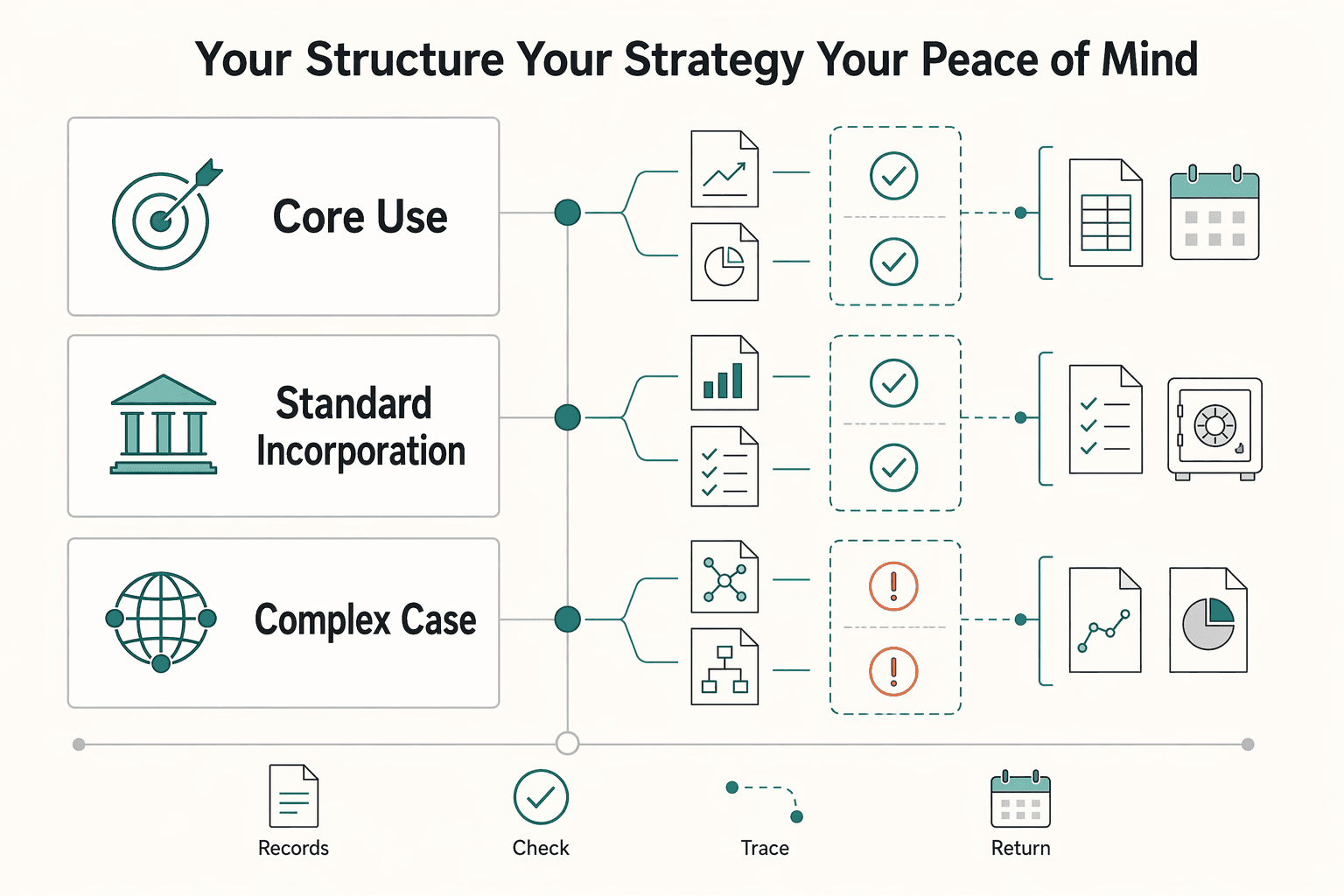

Your Structure, Your Strategy, Your Peace of Mind#

For many independent professionals, the decision becomes clearer once the job is clear. Choose BVI for an efficient, lower-friction holding setup. Choose Cayman when access to a stronger funds/fintech network and globally recognized regulatory standards is central to your plan. In practice, bvi vs cayman for holding company is a fit decision, not a branding decision.

Both jurisdictions are commonly described as having no direct corporate income tax, but that alone will not make the structure work. The outcome still depends on how consistently you handle governance, reporting requirements, and record-keeping after the company is live.

| Decision driver | BVI | Cayman | Usually fits best |

|---|---|---|---|

| Core use case | Popular hub for holding companies and SMEs with cost-efficient maintenance | Strong funds and fintech network with globally recognized regulatory standards | BVI for operational efficiency; Cayman for funds/fintech and institutional-facing needs |

| Standard incorporation | Approx. US$1,000-1,500 and 1-3 working days | Approx. US$3,500-6,000 and 3-7 working days | BVI if speed and budget are primary |

| If complexity increases | Banking and compliance can extend total setup time up to 3 months | If licensing or Cayman Enterprise City physical presence is required, expect about 4-6 weeks; CEC packages start around US$14,000+ | Cayman when added cost and timeline support your business case |

A common breakdown point comes after incorporation. Legal address setup, director and shareholder records, bank account opening, annual reporting where required, and follow-up compliance requests often get left without clear ownership. That is how a fast formation turns into a delayed launch.

To prevent that, do four things:

- Confirm your strategy in one line: an operationally efficient holding vehicle or an institutional-facing vehicle.

- Align entity setup, budget, and timeline to that strategy before filing.

- Assign one owner for ongoing compliance, records, and banking follow-up requests.

- Set a periodic review so the structure still matches what the company actually does.

If the structure fits your real objective and you run it with compliance-first habits, you can move forward with practical confidence. You might also find this useful: BVI Corporate Law for Independent Professionals. When you are ready to run collections, balances, and payouts with traceable controls, start with the Gruv docs.

Frequently Asked Questions

Is a BVI company safe for you as a U.S. person?

A BVI company can work if you run it as a compliance system, not a secrecy product. A key risk is U.S. reporting: a foreign corporation can be a CFC when U.S. shareholder ownership is over 50%, and certain Form 5471 failures can start at $10,000 per form per year. Your next step is to have your adviser confirm your exact CFC or Form 5471 position before filing season, since Form 5471 is attached to your federal return and follows that return’s due date, including extensions.

Do you also need FBAR for a BVI or Cayman setup?

You may need FBAR, so treat it as an early-year check, not a last-minute guess. The trigger is aggregate foreign account value over $10,000 at any point in the year, with FBAR due April 15 and an automatic extension to October 15. Your next step is to keep a live list of all foreign accounts tied to the company and confirm filing mechanics with your adviser or this FinCEN explainer.

What does economic substance mean for your one-person holding company?

If you are truly a pure equity holding vehicle, substance treatment is narrower, but it is not a blanket exemption. Cayman applies a reduced economic substance test to pure equity holding companies, while BVI applies substance requirements by relevant activity and can require compliance for each relevant activity you carry on. Your next step is to document your activity classification in writing and confirm it with your agent or local counsel before adding services, contracts, staff, or active management.

Is a Cayman company overkill for your solo consulting business?

It can be, unless you already need fund-facing or institutional counterparty credibility. A Cayman exempted company is designed for activities mainly outside Cayman, and certain fund activity sits in a formal CIMA regulatory framework that a simple solo holding setup may not need. Your next step is to use the simpler route for passive holding, see the BVI incorporation guide, or move directly to Cayman if investor diligence is already central, see the Cayman incorporation guide.

For holding crypto, is BVI or Cayman better?

For passive treasury holding of your own digital assets, either jurisdiction can work, and a lower-friction path may be enough. If you provide virtual asset services to others, you move into a regulated perimeter: BVI’s VASP Act has applied since 1 February 2023 and Cayman uses a CIMA registration or licensing route for VASPs. Your next step is to define your activity in one line, proprietary holding versus services for others, and avoid handling third-party assets until local scope is confirmed.

What is the real cost to maintain a BVI or Cayman holding company?

Do not rely on a single headline number, because setup and maintenance costs split into one-time and recurring items. One-time costs can include incorporation and onboarding, while recurring costs can include annual government fees, registered agent or office, annual filings, bookkeeping, and ongoing compliance support. Current cost ranges should be verified from provider quotes, official Registry fee schedules, legal advice, or source records before use. Your next step is to request a written quote that separates one-time versus recurring items and, for Cayman, verify the current Registry fee schedule plus the January annual fee or return cycle, practically due by the last business day of March.

How private is a BVI or Cayman company now?

Assume privacy from casual public view, not secrecy from tax authorities. CRS is built for annual automatic exchange of financial account information, Cayman guidance requires annual reporting by financial institutions for exchange, and BVI self-certification materials state account information may be shared with the BVI International Tax Authority; Cayman’s amended CRS or CARF framework takes effect from 1 January 2026. Your next step is to keep tax residency, beneficial ownership, and bank self-certification data consistent across records to reduce review friction.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- bvi.gov.vg/economic-substance-legislationtrusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/forms-pubs/about-form-5471trusted

- oecd.org/en/publications/consolidated-text-of-the-com...trusted

- sec.gov/Archives/edgar/data/1117795/0001564590190114...trusted

- sec.gov/Archives/edgar/data/2018222/0001641172250144...trusted

- uscode.house.gov/view.xhtmltrusted

- assets.kpmg.com/content/dam/kpmg/ky/pdf/2024/09/infrastructu...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Incorporate a Company in the British Virgin Islands (BVI)

A BVI company can be useful for a solo operator, but only in a narrow set of circumstances. If your business is genuinely cross-border, your clients are comfortable contracting with an entity, and you are prepared for real compliance and documentation work, it can be a strong tool. If you are looking for a shortcut on tax, admin, or banking, it is usually the wrong one.

How to Incorporate a Company in the Cayman Islands

**Start with fit, not forms.** If you're considering a Cayman company, first test whether it solves a real cross-border problem in your business. Do not start with whether it sounds sophisticated. A Cayman structure may be useful in some cases, but the excerpt here is not enough on its own to confirm legal or tax specifics.

What Is FinCEN for Freelancers and FinTech Users

If you are asking **what is fincen**, focus first on the decision in front of you. FinCEN, the Financial Crimes Enforcement Network, is tied to FBAR filing through FinCEN Form 114 when foreign financial accounts create reporting duties. By the end, you should know whether to act now, gather records, or escalate.