Quick Answer

Start with Stripe-hosted Checkout when speed and lower maintenance are the priority, then move to embedded or custom only for a specific in-app control requirement. In hosted checkout vs custom checkout decisions, the practical breakpoint is ownership of return-path handling, signed webhook confirmation, and reconciliation evidence, not just page design.

How to Choose Between Hosted and Custom Checkout#

The real choice is not just launch speed. It is whether you want to ship payments quickly now, or take on more control and day-to-day ownership later. For many platform teams, that tension shows up as soon as product wants a tighter in-app experience while engineering and finance ops are still trying to keep the first payment path stable.

This guide is an implementation-focused comparison of hosted checkout vs custom checkout. It is not a generic pros and cons list, and it does not treat "checkout" like a single product category with the same boundaries everywhere. The point is to help you decide what you are actually buying into: who owns the payment UI, who carries more maintenance, and what costs or constraints show up after the first successful transaction.

A useful anchor comes from Stripe’s own positioning. Stripe Connect pricing page frames the choice as a spectrum between offloading maintenance and taking "full control and ownership of payments." That is the split most teams actually care about. A hosted option usually cuts what your team has to build and maintain up front. A more custom approach gives you tighter product control, but it also shifts more responsibility onto your team over time.

If you are early and trying to get live quickly, published pricing can make the hosted path look straightforward. Stripe Standard, for example, advertises simple pay as you go pricing with "No setup fees, monthly fees, or hidden fees," and a domestic card price of 2.9% + 30¢ per successful transaction. That can be a real advantage when you need a clean first launch. It is not, by itself, a full answer on long-run ownership, because total effort depends on what your team must operate after launch, not just the initial fee line.

Before you compare vendor pages too literally, remember that similarly named checkout products can still draw different lines between provider-managed experience and platform-owned experience. In practice, you should verify that boundary before committing, especially if your roadmap assumes deep branding, in-app continuity, or provider-managed maintenance.

You should also be skeptical of broad claims about conversion lift or total cost. Consumer-law research warns that firms can exploit confusion, which makes clear UX and clear decision criteria important. The comparison that follows stays close to what teams can actually evaluate before go live: effort, ownership, and what breaks or gets expensive once volume and exceptions show up.

Hosted checkout vs custom checkout at a glance#

If you need a practical default, start with the most provider-managed option you can tolerate. In this source set, Stripe frames the core tradeoff clearly: offload maintenance to Stripe, or take full control and ownership of payments.

| Option | Setup effort | UX and branding control | Customer-flow mechanics | webhooks and idempotency | Ongoing ownership |

|---|---|---|---|---|---|

| Stripe-hosted Checkout | Lowest team ownership burden in this source set when you choose to offload maintenance | Exact branding depth is not established here | Do not assume hosted payform redirect behavior, return URL, success URL, or built-in success handling from this section alone | Not documented in these sources; treat both as implementation checks | Positioned at the "offload maintenance" end |

| Embedded Checkout | Hosted/embedded options are documented, but exact build scope is not specified here | More in-product continuity may be possible, but control boundaries are not established in this source set | Exact completion flow and built-in success state availability are not supported here | Not documented in these sources | Shared boundary; confirm what Stripe manages vs what your team owns |

| Bambora Checkout | Not established in this source set | Not established in this source set | Do not assume hosted payform, redirect, return URL, success URL, or built-in success behavior without Bambora docs | Not established in this source set | Verify directly with Bambora documentation and terms |

| Custom Checkout | Highest team-owned effort is the practical implication when you choose full control and ownership | Highest potential control because your team defines the experience | Completion path and success handling are team-defined in practice; specifics are not documented in this source set | Team-owned in practice; specifics are not documented in this source set | Full maintenance responsibility sits with your team |

| Unknowns | No validated cross-provider benchmark here for launch effort over time | No validated cross-provider benchmark for branding impact on outcomes | No validated cross-provider benchmark for conversion lift or abandonment impact | No validated cross-provider benchmark for reliability differences | No validated cross-provider benchmark for long-run maintenance cost |

What matters most in the first pass#

For founders and finance ops, the strongest signal is ownership, not checkout screenshots. Stripe’s Connect pricing page positions the decision as offloading maintenance versus taking full control and ownership, and that usually predicts long-run team load better than launch-speed claims.

There is also a pricing boundary to check early. Stripe states that when Stripe handles pricing for your users, you do not incur additional account, payout-volume, tax-reporting, or per-payout fees. When the platform handles pricing, Stripe lists $2 per monthly active account and 0.25% + 25¢ per payout sent. Separately, Stripe pricing lists 2.9% + 30¢ per successful domestic card transaction, and Managed Payments adds 3.5% per successful transaction on top of standard processing fees.

The checks you should not skip#

Do not fill provider-doc gaps with assumptions. Before you approve scope, verify:

- whether checkout redirects to a hosted payform or stays in your app

- whether you must provide a

return URLorsuccess URL - whether a built-in success state exists

- what event trail your team treats as proof that payment completed

Choose hosted first when speed and reduced maintenance are the goal. Move to embedded or custom only when owners for completion-state verification, webhooks, and idempotency are named before build starts. Related: Making Your Checkout Agent-Ready: Pricing Metadata Receipts and Policy Controls for AI Buyers.

What each model actually means in production#

In production, these labels are only useful if they map to a verified ownership split, not assumed vendor behavior. For this section, the available Stripe excerpt is access-limited and one comparison source is unavailable, so treat all model definitions as working hypotheses until you confirm them in live docs.

- Hosted payform: treat as the provider-managed end of the spectrum until verified. Confirm the exact customer path (

redirector direct link), whetherreturn URLorsuccess URLis required, and what completion state is actually reliable. - Custom Checkout: treat as the team-managed end of the spectrum, where your product and engineering teams own more of the payment experience and completion handling.

- Embedded Checkout: treat as a placement pattern, not proof of full ownership. Do not assume “embedded” automatically means fully custom front-end or risk logic without provider documentation.

Before you approve scope, document three answers in writing: who owns the UI boundary, what event confirms payment completion, and what your app does when page success and payment state do not match.

Hidden costs most comparison pages skip#

The hidden cost is ownership: as you move away from hosted checkout, your team takes on more maintenance, reliability work, and operational cleanup. Stripe Connect frames this directly as a choice to offload maintenance to Stripe or take full control and ownership of payments.

| Cost area | Closer to Stripe-hosted Checkout | More owned checkout path | What to verify before go-live |

|---|---|---|---|

| Feature requests | You work within provider page limits and release cycles | Your team builds and maintains more UX behavior | List the checkout states you must control, not just the happy path |

| QA cycles | Fewer page-level regressions in your app | Every copy, layout, and state change can reopen payment testing | Test success, cancel, timeout, and browser-back behavior |

| Regression risk | Lower surface area in your code | More ways to break redirects, event handling, and completion logic | Compare browser landing state with the provider event state |

| Incident response | Provider owns more of the hosted page behavior | Your team owns more triage across product, engineering, and ops | Define who responds when a customer sees “paid” but your app does not |

Fee pages can hide this shift if you only scan headline rates. Stripe Standard says there are no setup, monthly, or hidden fees, and lists domestic cards at 2.9% + 30¢ per successful transaction. In Connect models where you handle pricing for your users, Stripe also lists $2 per monthly active account and 0.25% + 25¢ per payout sent. Managed Payments adds 3.5% per successful transaction on top of standard processing fees. Country-specific pricing can supersede listed fees.

When you own more of the flow, treat redirect and event handling as separate reliability checks. Broken return URL handling, incomplete webhooks, and non-idempotent retries can all create cleanup work even when checkout appears complete to the customer.

The operating load also shifts by function. Product owns UX and completion-state decisions. Engineering owns idempotency, webhook replay handling, and one-payment-to-one-record integrity. Finance ops owns reconciliation and exception queues, especially once payout and account-level fees are in play.

A practical rule: stay closer to hosted until ownership is explicit. Before launch, require three artifacts: a redirect map for every return URL state, a webhook event checklist with retry and replay tests, and a reconciliation view that ties provider references to your internal records.

You might also find this useful: The Best Ways to Accept Payments on Your Website.

Compliance, tax, and policy gates that change the decision#

If auditability is the main risk, pick the checkout path that gives you the cleanest evidence trail, not the most flexible UI. The decision should be driven by whether you can consistently prove who paid, what you collected, and how that record supports later tax and policy reviews.

Where the compliance burden actually lands#

For PCI scope (including any SAQ-A assumption), this section’s sources do not provide provider-specific outcomes, so treat scope as an integration-specific validation step with your provider and compliance advisor. The same caution applies to KYC, KYB, AML, and payout gating mechanics: verify your exact flow rather than relying on generic claims.

Use this minimum evidence checklist before build:

- payment reference continuity from checkout into your internal account record

- exact identity and tax fields captured and retained

- the record path used when a payout is held, released, or investigated

If that trace breaks between payment and payout, extra checkout customization will not fix the operational risk.

Tax-adjacent workflows follow the same rule. If you support W-8, W-9, and 1099 processes, preserve clear linkage across payer, payee, payment, and classification records. For cross-border cases, FEIE rules show how specific recordkeeping can get: eligibility can require foreign earned income, a foreign tax home, and (under the physical presence test) 330 full days abroad in a 12-month period; those 330 days do not need to be consecutive; and excluded income is still reported on a U.S. tax return. For tax year 2026, the maximum FEIE is $132,900 per person.

FBAR is another reminder to design for traceability beyond checkout completion. FinCEN’s FBAR page includes official filing due-date resources, so your records need to stay usable after the transaction lifecycle ends.

The practical default is simple: if your team cannot already define the records needed for compliance review, tax support, and payout-policy decisions, start with the lower-ambiguity path and harden traceability first. For a step-by-step walkthrough, see How to Choose the Right Business Structure for Your Freelance Business. Want a quick next step for “hosted checkout vs custom checkout”? Try the free invoice generator.

Implementation checkpoints from first payment to reconciled ledger#

You are not go-live ready until one payment story runs end to end: initiation, asynchronous confirmation, and a canonical ledger state your finance team can reconcile. The checkout UI starts that story, but it is not the source of truth.

Order of operations to lock before go-live#

A reliable setup has clear ownership across three layers: payment initiation, payment confirmation, and business activation.

- Initiate payment: create your internal order/intent/session record first, then render or redirect to checkout to collect payment details.

- Confirm payment: treat confirmation as asynchronous; process provider webhook events, verify signatures, and persist one canonical outcome in your system (

paid,failed, orrefunded). - Activate business state: grant access, issue credits, and send notifications only after confirmed status is written.

If you activate from a browser return alone, you will eventually mark unconfirmed payments as complete.

| Stage | Primary trust signal | Pre-launch check | Red flag |

|---|---|---|---|

| Payment initiation | Internal order/session record | Every attempt is traceable before redirect/render | Provider charge cannot be matched to your internal record |

| Customer auth step | Provider status + internal pending state | Test flows with and without extra customer verification | Team assumes browser completion equals payment completion |

| Confirmation | Signed webhook + canonical ledger write | Replay events and confirm one final financial state | Return URL marks payment paid before webhook confirmation |

| Business activation | Post-confirmation app logic | Entitlements/receipts/alerts fire only after confirmation | Duplicate access, duplicate messages, or missing entitlements |

Verification checkpoints to force in test#

Treat success URL / return URL as customer experience, not accounting truth. In sandbox, test immediate return, no return, and delayed return; all should resolve to the same final internal state after webhook processing.

Run webhook delivery and replay tests directly. PayPal developer docs expose a Webhooks area plus Sandbox testing guide and Negative testing resources; use that to prove signature verification, duplicate-event safety, and alerting when confirmation is missing.

For retries and repeated submits, validate that your system still produces one canonical payment outcome and one downstream financial posting path.

Reconciliation artifacts finance ops should require#

Before go-live, require an evidence pack for each settled path:

- provider transaction/reference ID on the payment record

- linked internal order/invoice/account record

- journal or ledger posting reference for the financial entry

- explicit exception states (

pending,failed,refunded,challenged,manual review) - internal trace from confirmed payments to downstream payout decisions or payout batches, where applicable

If you cannot prove return handling, webhook replay handling, and retry safety all converge to one canonical ledger record, stay closer to hosted until that reliability baseline is in place.

For a deeper implementation view, see 3D Secure 2.0 for Platforms: How to Implement SCA Without Killing Checkout Conversion.

Scenario-based recommendations for service platforms#

Once your confirmation and ledger flow is reliable, decide based on the constraint that is binding now, not the most flexible architecture on paper. For most service platforms, that means choosing the path that gets you live without adding avoidable ownership and payout complexity.

| Your main constraint | Recommended choice | Why this usually wins | What to verify before you commit |

|---|---|---|---|

| You need to launch fast with a lean team | Stripe-hosted Checkout or another hosted payment page | Stripe defines a hosted payment page as third-party hosted secure checkout, positions prebuilt UIs as a way to save engineering time, and Stripe Standard pricing states no setup, monthly, or hidden fees. | Confirm internal order ID, provider reference, and final payment status are stored in your own records, not inferred from a success page. |

| You need deep UX control and in-app continuity | Embedded Checkout or Custom Checkout | This is the better fit when payment is part of core product UX. The tradeoff is more testing scope and ongoing maintenance. | Test delayed confirmation, retries, and step-up authentication in the exact flow you plan to ship. |

| You run a marketplace or contractor platform where payout orchestration is central | Choose the option that keeps pricing ownership and payout handoffs clear, even if checkout UI is simpler | Connect pricing changes with ownership: Stripe can handle pricing for connected users, or you can handle pricing and fee responsibility. | Verify each confirmed payment can be traced through connected-user records and into later payout decisions. |

| You may add non-card collection paths later | Keep checkout architecture modular, even if you start hosted | Method expansion is easier when initiation, confirmation, and ledger posting are shared components. | Check that customer, order, and payout metadata can pass through more than one collection path. |

Start hosted when speed is the real goal#

If your immediate goal is faster launch with limited engineering bandwidth, start with Stripe-hosted Checkout. It reduces build scope while still supporting clean reconciliation artifacts in your own system. Move away from hosted only after volume and exception handling are stable enough to justify extra ownership.

Go custom only when you can name the control you need#

Choose custom or embedded only when you can point to a specific in-product control requirement. Stripe frames the integration approach as a choice between offloading maintenance and taking full control of payments. If you choose control, budget for QA and incident response, not just implementation.

Model payout economics before polishing checkout#

For service platforms, payout economics often matter more than checkout polish. Stripe’s published pricing examples include 2.9% + 30¢ per successful domestic card transaction, and Connect pricing differs by ownership model. In the platform-handles-pricing model, Stripe lists fees including $2 per monthly active account and 0.25% + 25¢ per payout sent, and says you are responsible for Stripe processing fees; in the Stripe-handles-pricing model, Stripe says it sets and collects processing fees from your users and that you do not incur additional account, payout-volume, tax-reporting, or per-payout fees. Managed Payments also has a separate 3.5% fee layer in addition to standard Stripe processing fees.

We covered this in detail in How to Create a Productized Service for Your Freelance Business.

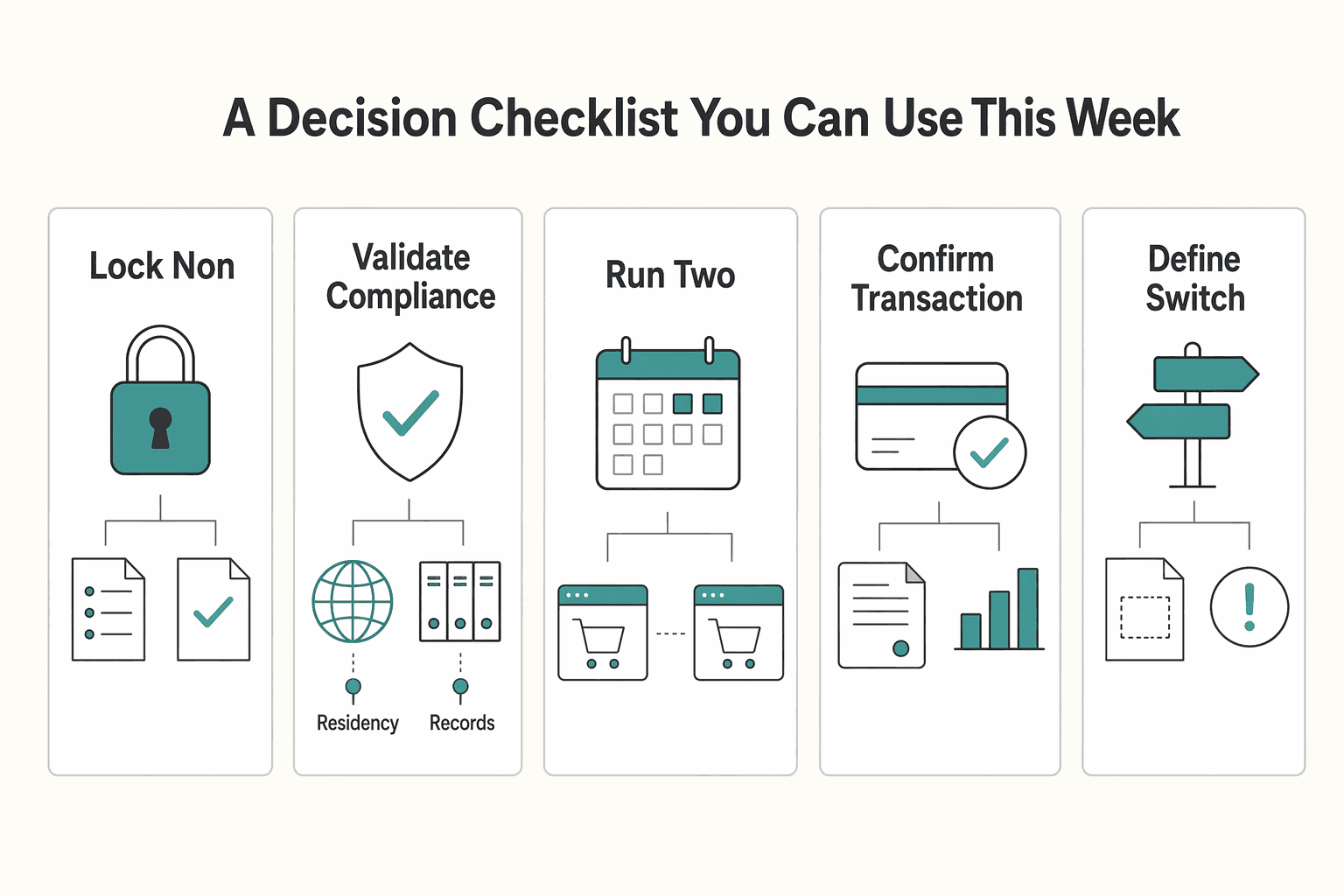

A decision checklist you can use this week#

Use a one-week test, not a long debate: start hosted if speed is the binding constraint, and move to embedded or custom only when you can name the exact control you need.

- Lock non-negotiables in writing.

If you need full in-app continuity and deeper UI control, state that upfront. If speed is the priority, Mastercard's Hosted Checkout docs position it as secure and fast to deploy, with a gateway-hosted payment UI so you do not have to invent the first comparison baseline yourself.

- Validate compliance assumptions before build decisions.

Do not assume a hosted page automatically means the lightest PCI path. SAQ A-EP is described for merchants that outsource processing but still keep some control of the payment experience, and scope can include third-party hosted pages and iframe-based embeds. Document your assumed PCI posture, who validated it, and whether KYC, KYB, or AML policy gates affect activation or payout.

- Run two pilots with explicit pass/fail rules.

Test one hosted flow and one embedded/custom flow. Pass only if each path reliably produces the same finance-critical records and clear exception states, with acceptable support load.

- Confirm transaction handling boundaries now.

For payer-participation transactions, Hosted Checkout uses a checkout session to display a Hosted Payment Page. For subsequent transactions without payer participation, Mastercard says you send a server-side API request.

- Define switch triggers before launch.

Set clear triggers to change models later: volume growth, hard UX limits, conversion testing needs, or rising audit and reconciliation complexity.

Related reading: Portugal D7 vs. D8 Visa: Which is Right for You?.

Conclusion#

The right hosted checkout vs custom checkout answer is usually the one that removes your current bottleneck, not the one that satisfies every future feature idea. If your constraint is launch speed, limited engineering bandwidth, or limited appetite for deeper technical and security ownership, a hosted path is the practical choice. If your constraint is in-product continuity, tighter branding control, or keeping payment on your site, then API integration or embedded checkout is the right direction.

That split is not cosmetic. Hosted checkout sends customers to third-party payment pages, and the provider develops, maintains, and hosts that experience. Decta’s comparison makes the tradeoff plain. Hosted is quick, easy, secure, and lighter on coding, but you give up branding control. API integration gives full control over user experience and branding, but requires more technical skill and stronger security compliance ownership. That is the decision to anchor on. Do not buy complexity early just because you may want it later.

For many platform teams, the sensible move is staged. Start with the option that requires lower initial integration work, then reassess as needs grow. Stripe Checkout docs are a good example of why this can work. Stripe positions Checkout as a prebuilt payment page with its own hosted flow, which lets you get live without hard-coding every payment-state edge case on day one.

A good trigger to move off hosted is not vague ambition. It is something you can point to: the redirect now breaks core product flow, branding limits are blocking a required experience, or your team is already staffed to own the added technical and security burden. The red flag in the other direction is just as clear. If nobody can name who owns payment-page behavior, compliance assumptions, and ongoing maintenance, do not choose on-site integration yet.

Your next step should be concrete. Align product, engineering, and finance ops on one checklist, then run a time-boxed implementation decision sprint with a hard end date. At minimum, that sprint should produce:

- one agreed success criterion for the customer experience

- one written decision on the exact integration pattern: hosted redirect, embedded Checkout, or on-site API integration

- one evidence pack for go-live signoff, including the implementation pattern shipped, the owner for technical and compliance questions, and the operational checks that must pass

If you cannot get those three groups to sign the same decision, the problem is not the checkout model. It is unresolved ownership.

Frequently Asked Questions

What is the practical difference between hosted checkout and custom checkout for a service platform?

The practical split is ownership. Hosted checkout usually redirects the buyer from your site to a provider-hosted payment page, while a custom build generally keeps more of the payment experience under your product and engineering team. For a service platform, that changes who owns UI control and redirect/event handling when payment status is finalized.

Which option is usually faster to launch for a small engineering team?

Hosted is often treated as the faster path, because the provider hosts the payment page and handles payment-data collection on that page. Your team still needs to wire up the redirect, the return path back to your site, and webhook notifications for payment events. Do not treat the customer return alone as proof of payment before your event handling confirms final status.

Which model gives more control over branding and in-product UX?

Custom usually gives you more control over layout, copy, and how payment fits into the rest of your product. Hosted pages vary by provider, but Mastercard explicitly says its Hosted Checkout cannot be customized beyond your merchant-specific name and logo. If matching an exact in-app experience matters more than launch speed, that is a real reason to move away from a redirect flow.

Can hosted checkout and custom checkout both support PCI-compliant implementations?

Potentially, but the scope is not identical and should never be guessed. Hosted flows can reduce PCI DSS burden because the provider handles payment data collection on the hosted page, but that does not mean all PCI responsibility disappears. The verification step that matters is simple: document your assumed scope, confirm it with your compliance owner or assessor, and keep evidence of the exact integration pattern you shipped.

Should we embed a hosted checkout page in an iframe?

Do not assume an embedded iframe is automatically cleaner or lower risk than a redirect. Check whether your provider explicitly supports that pattern and how it affects return handling, event delivery, and customer recovery if the frame fails or is blocked. If you cannot clearly prove the success path, the cancel path, and the webhook path in testing, use the standard hosted redirect instead.

What is the difference between a hosted page and an embedded prebuilt option like `Embedded Checkout`?

From this grounding, a hosted page is provider-hosted UI typically reached through a redirect, with a return path back to your site. This grounding does not establish the behavior of embedded prebuilt options, so treat those as provider-specific and verify them in the provider's own documentation before deciding architecture.

Can we run both models at the same time for different customer segments?

It can be done, but this grounding does not provide benchmark data on outcomes by segment. If you run both, keep records consistent across paths: your internal order ID, the provider reference, final payment status, and a clear exception state. If finance cannot reconcile both paths the same way, dual-track checkout can add operational risk.

Try a related tool

Avery writes for operators who care about clean books: reconciliation habits, payout workflows, and the systems that prevent month-end chaos when money crosses borders.

Sources

- cfo.asu.edu/cfo-pdf-site-maptrusted

- cisa.gov/news-events/bulletins/sb25-021trusted

- congress.gov/113/chrg/CHRG-113hhrg87150/CHRG-113hhrg87150...trusted

- docs.stripe.com/payments/checkout/how-checkout-workstrusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- lawreview.uchicago.edu/sites/default/files/04%20Willis_ART_Online%2...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Implement 3D Secure 2 for Platforms Without Losing Checkout Conversion

Treat 3D Secure 2 as an architecture choice, not a compliance box to tick. For a platform, the way you introduce 3DS2 changes how you meet Strong Customer Authentication requirements in Europe. It also changes how often customers get interrupted and how much payment logic you tie to a single checkout surface.

Making Your Checkout Agent-Ready for AI Buyers

`agent-ready checkout` is not a prettier pay button. It is a control problem. Can an AI agent complete a purchase through your API and payment gateway without breaking purchase confirmation, fraud handling, reconciliation, or customer trust? When the answer is no, the issue is usually not the model. It is the gap between authorization, payment events, and finance close.

The Best Ways for Freelancers to Accept Payments on a Website

Choose the payment setup your team can run cleanly from request to paid, not the one with the longest feature page. Late payments and disputes usually come from fuzzy terms, unclear ownership, and weak follow-through, not just from tool choice.