Quick Answer

For portugal d7 vs d8, choose the route your documents can defend most clearly right now. D7 is framed as the passive-income path, while D8 is framed as the remote-work path. The safest approach is to run a 10-minute decision framework, build one primary evidence narrative, and keep a fallback path ready if your proof weakens before filing.

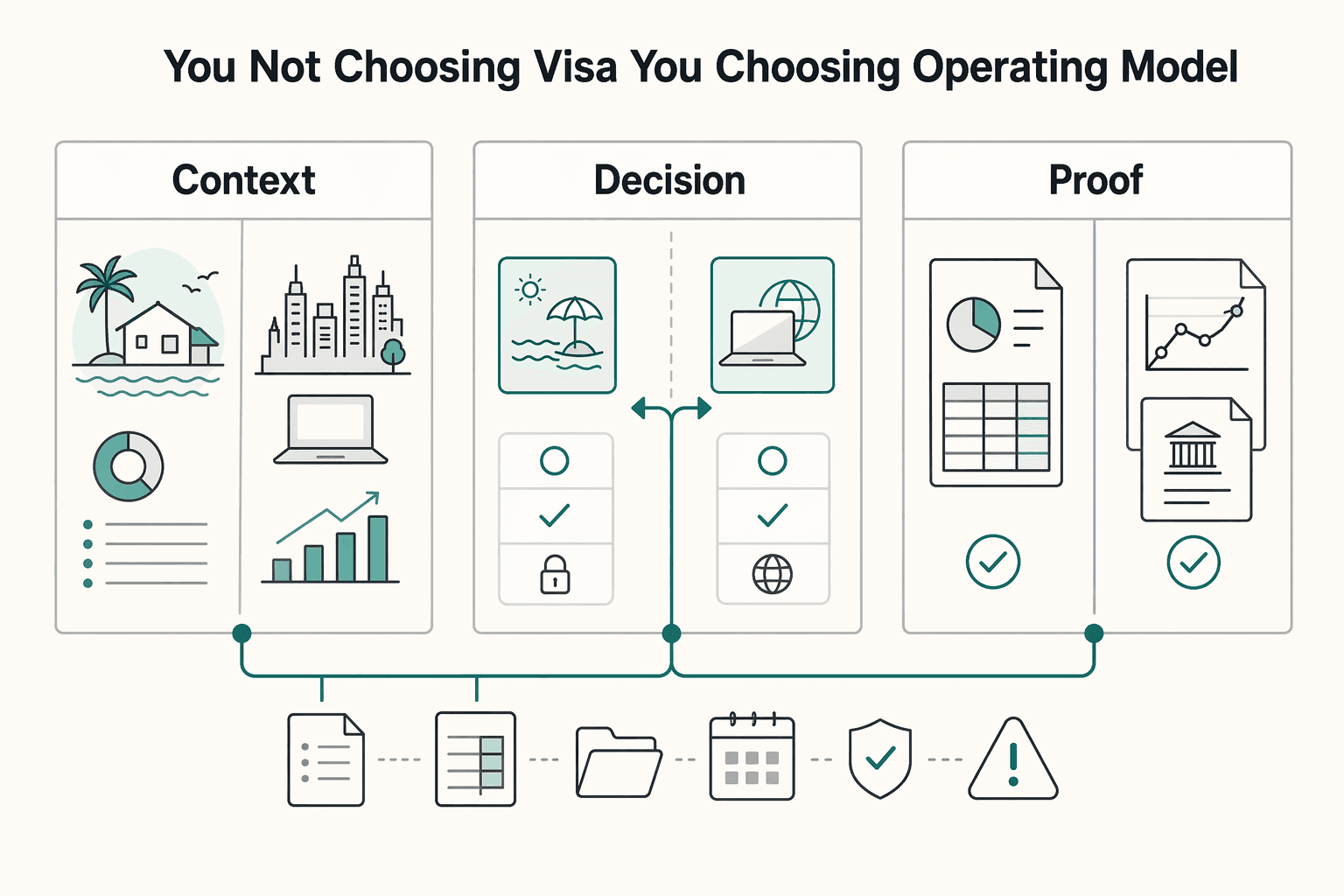

You are not choosing a visa you are choosing an operating model for your move#

Treat Portugal D7 vs D8 as an operating decision first, then choose the visa that matches your income narrative and proof quality. If you treat this like form-filling, you will collect the wrong evidence and end up in a rework loop. If you treat it like operations, you set a default path early, sequence documents on purpose, and keep a fallback ready.

In practice, people usually frame the split this way. The D7 visa fits a passive income narrative. The D8 visa fits active remote-work income (sometimes labeled online as a "digital nomad" option).

The first issue is trust. Some widely shared materials block key details behind sign-up walls. Some pages surface cookie-consent interface text instead of guidance. One visible D8 explainer shows up in a tax residency context with a late-2025 date stamp. Use that reality to set stricter trust rules before you do anything else.

Apply trust rules before paperwork#

| Confirmed from current captures | Verify before filing |

|---|---|

| Some pages hide full guidance behind access gates. | Exact current eligibility thresholds for D7 and D8. |

| Some pages present mostly cookie-consent interface text. | Program-specific legal criteria for your filing context. |

| One D8 explainer appears under tax residency and shows a December 10, 2025 date. | Current rules on timelines, rights, and downstream status outcomes for your case. |

Run the 10 minute decision framework now#

| Minutes | Action |

|---|---|

| Minute 1 to 3 | Pick your primary income story. Lead with one model only, either passive-income-first or active-remote-income-first. |

| Minute 4 to 6 | Match evidence to that story. Keep only documents that prove continuity, ownership, and legitimacy of that income type. |

| Minute 7 to 8 | Choose a safe default route, then define a fallback route if your primary evidence weakens. |

| Minute 9 to 10 | Build your timeline and checklist in one tracker with clear gates: proceed, pause to verify, or switch path. |

Example: a mixed-income operator invoices clients and also receives investment distributions. The clean move is to pick one primary narrative, build the strongest pack for that route, and keep the other route as a documented fallback. The goal is simple: one safe default path, one fallback plan, and no guesswork once you start filing.

Which visa fits your income model in 10 minutes?#

Choose D7 when your strongest proof is stable passive income. Choose D8 when your strongest proof is remote work income you can document cleanly. This section turns that principle into a quick decision engine so your visa path follows evidence strength, not preference.

Run these three inputs in order, then pick your branch. Use this flow whenever the choice feels close:

- Passive income stability

- Remote income continuity (employee salary or freelancer contracts)

- Your intended work setup in Portugal (your day-to-day model changes what you must defend)

| Income model signal | Likely visa path | Confidence label | What to prove now | Fallback trigger |

|---|---|---|---|---|

| Stable recurring passive income, with limited reliance on active client work | D7 Visa (commonly described as a passive-income route) | High confidence | Show durable passive income history and clean fund trail | Passive stream looks irregular or too recent |

| Active remote salary or freelancer revenue as the core model | D8 Visa (Portugal Digital Nomad Visa) | Verify before filing | Show ongoing remote income continuity and role setup | Contract continuity weakens or employer setup creates ambiguity |

| Mixed model with both passive income and active remote earnings | Pick one primary path, keep the other as backup evidence | Specialist review needed | Build two evidence packs, then lead with the stronger narrative | Primary pack fails consistency checks |

Use threshold numbers carefully. You may see secondary figures such as EUR 920 per month and EUR 12,000 per year for D7, plus 50 percent for a spouse and 30 percent for a dependent child in one source set. One source also states that only passive income qualifies for D7. Another source ties review to the minimum wage in force at your appointment date and references January 2026 updates. Treat these as directional, then verify before filing.

Example: a freelancer with dividend income chooses D8 as the primary route because contract continuity is easier to prove. They keep a D7-ready passive-income file as backup. This reduces delay risk if a reviewer pushes back.

If you want deeper D8 prep after choosing your branch, use Portugal Digital Nomad (D8) Visa: A Complete Guide. The operating rule stays the same: pick what you can prove cleanly today, and keep a documented Plan B.

What does the at a glance comparison say before you gather paperwork?#

Use this Portugal D7 vs D8 snapshot to sanity-check your choice before you build a full document pack. The point is not to memorize requirements from summaries. It is to avoid assembling evidence for the wrong narrative, then discovering the mismatch after submission.

| Criteria | D7 Visa (Portugal Passive Income Visa) | D8 Visa (Portugal Digital Nomad Visa) | Confidence label |

|---|---|---|---|

| Income type fit | Best fit when stable passive income carries your case. | Best fit when remote work income (salary or self-employed/freelance) carries your case under a digital nomad model. | High confidence |

| Work model signal | Supports a passive-income-first story. | Supports a remote professional story, often framed as the Digital Nomad Visa. | High confidence |

| Residency outcome signal | Secondary comparisons frame both routes as long-term residence paths in Portugal for non-EU/EEA/Swiss citizens. | Secondary comparisons also frame a legal path to live in Portugal long-term, and eventually citizenship. | Verify before filing |

| Complexity signals | Secondary content shows a lower headline income benchmark for D7, including references to EUR 920 per month in 2026 context. | Secondary content shows a higher D8 benchmark, including EUR 3,680 per month (net, last three months), plus at-a-glance notes like 1 to 4 months processing and an initial 2-year permit. | Verify before filing |

| Known uncertainty | These excerpts do not confirm exact official thresholds or filing-context rules. | These excerpts do not confirm non-Portuguese company work assumptions or final threshold enforcement. | Specialist review needed if your case looks complex |

| Shared outcomes check | Family reunification and Schengen Area mobility often appear in broader discussions, but this evidence set does not confirm specifics. | A secondary panel references a citizenship path after five years, but you still need current official confirmation. | Verify before filing |

| Safe default when profile is borderline | Choose the route with cleaner, more consistent proof right now. | Keep the alternate route as backup evidence if your primary narrative weakens. | High confidence |

If you earn rental income and freelance revenue, do not submit a blended narrative that forces the reviewer to guess what you are applying under. Choose one primary story and keep the second as backup evidence.

Verdict: pick the visa your documents can defend today. If proof quality is truly a tie, pause and get a specialist review before you submit anything.

Is D8 actually harder than D7 and where do applicants get blocked?#

From the evidence here, you cannot verify that D8 is "harder" than D7. Treat any D7 vs D8 difficulty talk as directional until you confirm current official requirements for your exact filing path. What matters is where files break under review pressure so you can design controls upfront.

The strongest risk signal here is operational. Portugal visa processing through AIMA or SEF and consulates can move slowly. Applicants underestimate appointment waits, document validity windows, authentication steps, and background check delays.

That risk exists on both routes. In practice, the win is to plan for timing friction and keep your story and documents tight.

| Block point | Where it usually breaks | Control move you should make now |

|---|---|---|

| Income evidence clarity | Reviews bog down when income proof is unclear, incomplete, or hard to trace | Build a clean income trail with consistent statements, source/ownership proof where relevant, and translation or authentication readiness |

| Narrative coherence | Files slow down when the story does not match the documents (or mixes models without a clear primary) | Write one primary narrative and align every document to it; keep any "extra" income as clearly secondary support |

| Work/setup clarity | Applicants hit ambiguity when reviewers cannot quickly map the setup to the narrative | Prepare role/context documents (letters, contracts, explanations) that make your setup easy to understand |

| Timing discipline | Strong files stall when documents expire before appointments | Start prep 2 to 4 months before your move and track validity windows in one checklist |

| Basic setup prerequisites | People get blocked when they skip foundational setup | Secure your NIF number early and sequence downstream tasks around it |

Run this risk control checklist before submission#

| Checklist item | Details |

|---|---|

| Verify now | Current requirements for your route, appointment timing, and any timing constraints around background checks, authentication, and document validity windows. |

| Document now | One primary narrative and a dated checklist for validity windows. |

| Escalate now | Mixed-income cases or any situation where advisors give conflicting interpretations. |

If you need deeper route setup, use Portugal Digital Nomad (D8) Visa: A Complete Guide.

What timeline should you run from planning to arrival?#

Run a five phase operating timeline with a decision gate at each step, and switch paths early when your evidence weakens. This is an execution plan, not a legal checklist.

Use public guides as directional context, then verify current filing rules before you submit. If a page returns a 404, discard it. If a page pushes a promotional checklist, treat it as marketing support, not final authority.

| Phase | Core artifacts for D7 Visa path | Core artifacts for D8 Visa path | Decision gate |

|---|---|---|---|

| Planning | One page narrative that defines your financial means story, fallback trigger, and file owner | One page narrative that defines your D8 story under the Portugal Digital Nomad Visa frame | Proceed if one narrative reads cleaner than the other. Pause if both look mixed. |

| Evidence assembly | Evidence pack that supports your chosen story, with a clear ownership trail and clean account history | Evidence pack that supports your chosen story, with continuity across contracts, invoices, and role setup (if applicable) | Proceed if documents align with one story. Switch if your stronger proof sits in the other path. |

| Submission prep | Versioned checklist, document validity tracker, translation or authentication tracker | Same control stack, plus consistency checks across all files | Proceed when every file supports the same narrative. Pause on any contradiction. |

| Post approval setup | Arrival task list, banking and housing admin tracker, first month compliance reminders | Arrival task list, continuity tracker, first month compliance reminders | Proceed if your live setup still matches filed evidence. Escalate if your circumstances change. |

| First months in Portugal | Monthly evidence log that preserves your D7 narrative for renewals | Monthly evidence log that preserves your D8 narrative for renewals | Proceed with steady recordkeeping. Switch strategy only with specialist input. |

Run safeguards from day one#

| Safeguard | Details |

|---|---|

| Document folder | Version controlled document folder with dated filenames and change notes. |

| Submission log | Submission log with status, owner, next action, and blocker. |

| Follow up tracker | Follow up tracker so no appointment, expiration, or request slips. |

Example: a freelancer starts on a D8 track, then loses income continuity before filing. Hit the gate, pause, and pivot only if the other path's evidence pack is clearly stronger. That is disciplined switching, not panic switching.

If you need a deeper path-specific checklist next, review A Guide to Portugal's D7 Visa.

Which hidden tradeoffs matter after approval?#

The biggest post-approval risk is not paperwork. It is acting on assumptions your approved status does not actually support. Once you arrive, the job becomes keeping your real life aligned with the story your file was built on.

Most hidden costs show up when you relax controls. That includes rework cycles, document refreshes, and avoidable delays when your situation drifts from your filed narrative. This can hit both a passive-income story and a remote-work story.

| Hidden tradeoff | What can go wrong | Safe control |

|---|---|---|

| Local work flexibility assumptions | You act on forum shorthand and create a mismatch with your visa narrative | Treat every new work change as a verification event before you execute |

| Remote employee constraints | Employer setup or role scope changes, but your file logic does not | Keep an active role evidence log and review it before each major admin step |

| Family reunification timing assumptions | You sequence housing, school, or travel around unverified timing | Build plans with buffers and confirm timing rules before commitments |

| Cross program confusion | You apply Golden Visa cultural-route figures some publishers cite (like €250,000 or €200,000) to non-Golden-Visa decisions | Separate program types in your tracker and block cross-use of thresholds |

| Publisher and community noise | Community threads or polished guides sound certain without full context | Mark each claim as official rule, publisher interpretation, or anecdote |

Run a signal filter every month#

- Verify high-impact claims against current official requirements before action.

- Keep one change log for visa narrative, household plan, and work model updates.

- Escalate when two sources disagree, especially when neither is an official rulebook.

- Archive outdated guidance and remove it from your operating checklist.

Even formal policy papers often state that author opinions may not reflect official institutional views. Apply the same discipline here.

Example: a remote employee reads a social post, assumes it applies to their visa category, and shifts work structure too early. The better move is simple: pause, verify, then execute.

If your profile looks like this which visa is the safe default?#

In Portugal D7 vs D8, default to the route backed by your strongest evidence today. Switch only if that evidence stops holding up. This is profile-based guidance, not a substitute for confirming the current filing requirements before you submit.

| Profile | Choose this now | Switch if evidence weakens | Why this default is safe |

|---|---|---|---|

| Retiree living on passive income | D7 Visa | Switch to D8 Visa only if active remote work becomes your primary income story and your D8 work documents are stronger | If you are not anchoring your application on remote/freelance work, D7 can keep the narrative simpler (confirm eligibility and requirements) |

| Consultant freelancer with active client contracts | D8 Visa | Switch to D7 Visa if contract continuity turns unclear and your non-work income documents become stronger | D8 aligns with freelancer and remote work visa positioning |

| Remote employee at a non-Portuguese company | D8 Visa | Switch to D7 Visa if employer documentation cannot clearly support your remote setup and you hold stronger non-work income proof | D8 fits the Portugal Digital Nomad Visa track for remote workers, but document quality decides the safer path |

| Mixed-income household | Start with D7 Visa when non-work income evidence leads, or D8 Visa when active remote earnings lead | Switch the primary route if the lead income narrative loses clarity before filing | One primary narrative lowers contradiction risk across the household |

| Uncertain earners with unstable income story | Choose the route, D7 Visa or D8 Visa, with the cleanest recurring document trail right now | Pause and rebuild evidence before any switch driven by preference alone | Document strength beats preference every time |

Example: one partner earns mostly from contracts while another relies on passive income. You can still run a safe plan by choosing one primary narrative and keeping the other income stream as backup evidence, not competing logic inside the same story.

If you plan to include dependents or pursue family reunification, sequence operations early, but treat timing and steps as jurisdiction- and case-dependent:

- Lock the primary applicant and visa narrative before you book major commitments.

- Build dependent files from the same evidence timeline as the main file.

- Add buffers in case administrative timelines shift so housing, school, or travel plans are not forced into last-minute changes.

- Recheck narrative consistency before each submission event.

If you lean toward D8, use Portugal Digital Nomad (D8) Visa: A Complete Guide to tighten your checklist.

If you want a deeper dive, read The 2025 Global Digital Nomad Visa Index: 50+ Countries Compared.

Use this decision checklist to move from confusion to execution#

Choose model fit first, validate evidence second, then lock a timeline with explicit decision gates. The goal is controlled speed. Move fast only where the proof is already clean, and slow down where uncertainty can force rework.

| Decision gate | Action now | Proceed when | Pause when |

|---|---|---|---|

| Pick your primary path | Choose one lead path, D7 Visa or D8 Visa, and write a one line income narrative | Your narrative and your current documents tell the same story | Your file mixes competing stories and you cannot defend one clearly |

| Validate evidence | Build one document pack tied to your lead narrative | Every material claim maps to a document you can present consistently | Key claims rely on assumptions, screenshots, or informal summaries |

| Resolve uncertainty flags | List unresolved rules and assign an owner for each verification | Each open question points to an official, secure source before action | You still rely on social posts, recycled checklists, or conflicting summaries |

| Lock your timeline | Set submission milestones and fallback triggers in advance | You can state exactly when to proceed, pause, or switch path | You have dates but no decision triggers or contingency path |

Use this immediate checklist before you execute:

- Confirm your income narrative in plain language.

- Assemble your document pack in one controlled folder with version history.

- Mark uncertainty flags as open, in review, or resolved.

- Define a fallback path and the exact trigger that activates it.

Trust rules protect you from preventable delays when program rules vary by filing context:

- Treat official domains as your highest trust source. In U.S. context,

.govindicates an official government organization. - Share sensitive information only on official, secure websites and confirm

https(or the lock indicator) before you upload documents. - If two sources disagree, escalate and verify before you act.

Example: a mixed-income household wants to submit fast. They pause for a week, tighten one narrative, remove conflicting evidence, and then file with a clear fallback trigger. That short pause can prevent a long rework cycle.

If you want extra structure, read our Portugal D7 guide. You can also talk to a specialist to confirm what's current for your situation.

Frequently Asked Questions

D7 vs D8 which visa is for passive income and which is for remote work?

D7 is the passive income route. D8 is framed in one advisory source as the Digital Nomad (D8) route, and you should verify what income and documentation it expects based on your exact situation. For D7, build around stable, recurring, verifiable passive income.

Is D8 harder to qualify for than D7 in practice?

Do not anchor your plan to a single published number. The excerpts here signal a higher income bar for D8, but they do not confirm a complete, current threshold for every filing context. Verify before you lock dates.

Can both D7 Visa and D8 Visa lead to Portuguese citizenship?

Treat both routes as residency pathways first, not automatic citizenship tracks. D7 commonly starts with a 1 year grant and renewals, and long term outcomes depend on ongoing compliance. Confirm citizenship eligibility rules separately before you make long-horizon promises to yourself or your family.

Do both routes support family reunification and Schengen Area access?

Use family reunification and Schengen mobility as planning goals, not guarantees. Conditions can vary with file quality, timing, and current rules. Verify requirements before submission, then re-verify before each major dependent or travel step.

Can D7 holders work in Portugal and does D8 require a non-Portuguese company setup?

Do not run this decision from forum shortcuts. Keep D7 focused on passive income evidence, since advisory guidance flags salary, remote work earnings, and active business profits as a refusal risk for a D7 narrative. For D8, validate your exact employer or freelancer setup against current official criteria before filing.

What should I do if my income is mixed between passive income and freelancer work?

Pick one primary narrative and one backup narrative. If passive income documents are stronger and more stable, lead with D7. If your situation fits D8 more cleanly, lead with D8. Keep the secondary stream as supporting context, not competing logic.

What can I verify this week to reduce application delay risk?

Audit your income evidence for consistency, stability, and recurrence, and make sure it is verifiable through official documents. Check current threshold language because published D7 amounts can change, and D8 figures vary by source. If you face higher scrutiny risk, especially as noted for some regions, tighten completeness before you submit.

Try a related tool

Having lived and worked in over 30 countries, Isabelle is a leading voice on the digital nomad movement. She covers everything from visa strategies and travel hacking to maintaining well-being on the road.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The 2026 Global Digital Nomad Visa Index for 50+ Countries

Start with legal fit, not lifestyle filters. The practical order is simple: choose a route you can actually document, then decide where you want to live. That single change cuts a lot of wasted comparison work and stops you from falling in love with places that were never a real filing option.

Portugal Digital Nomad Visa Decisions That Prevent D8 Delays

Start with verification, not paperwork. In this research set, some material is useful only as EU VAT context, not as D8 instruction, and mixing those categories is one of the fastest ways to build the wrong plan. We use the same separation rule in [Global Digital Nomad Visa Index](/blog/global-digital-nomad-visa-index) comparisons.

A Guide to Portugal's D7 Visa for Passive Income Earners

**Run your D7 process like an operating plan with decision gates, not a one-time application.**