Quick Answer

Start by using broad labor context, then convert it into operating policy in stages. For fitness platform operators pay personal trainers class instructors scale decisions, the article recommends anchoring on OEWS SOC 39-9031, separating one-on-one CPT work from group classes, and selecting a model by utilization reality: per-class guarantee for volatility, revenue-share for stable bookings, and tiers only when data quality is reliable. Launch country by country with written fallback payout paths and hard compliance release gates.

Why Trainer and Instructor Payouts Get More Complex at Scale#

Public wage benchmarks are useful guardrails, not payout policy. They show labor-market context in broad terms. They do not, by themselves, set per-class guarantees, trainer earnings structures, or payout controls.

Step 1 Treat public wage data as a starting point#

Start by putting wage sources in the right role. The Bureau of Labor Statistics publishes labor-force statistics through the Current Population Survey, and those tables are meant to describe market context. The page shows fields such as "Number of workers" and "Median weekly earnings." In the 2025 table, the row for total full-time wage and salary workers shows 121,470 workers and median weekly earnings of $1,204. That is useful context, but it is not a payout rule for your platform.

The same caution applies to public salary pages generally. They can help you understand how the market describes work, but they are still external benchmarks with their own scope, labels, and sampling limits. If you treat any of these sources like a ready-made compensation plan, you blur the line between market signal and operating policy.

Verification point: if a source gives you broad earnings context, worker counts, or salary-style summaries, you are still at the benchmark stage. You are not ready to lock a per-session rate, revenue share, or class guarantee.

Step 2 Define the operator decision you actually need to make#

This guide is for operators making three decisions: where to launch next, how to pay trainers and instructors, and what controls to set before scale turns minor payout issues into recurring risk. Those decisions connect, but they are not the same.

A common failure mode is pulling one number from a wage page and carrying it straight into product, pricing, and finance. That often breaks once you hit real operating conditions such as uneven utilization, different service formats, or market-specific payment constraints. Broad wage data may tell you whether a market looks expensive or inexpensive. It does not, on its own, tell you whether your unit economics support a guaranteed payout, whether your cancellation rules work, or whether your payout rail coverage is strong enough to launch.

Step 3 Follow a repeatable sequence instead of improvising#

Use a repeatable sequence instead of making case-by-case exceptions. Start with baseline wage context, layer narrower sources carefully, prepare the market inputs that matter operationally, choose a compensation model, and then add execution checks that keep payouts accurate as volume grows.

Expected outcome: by the end, you should be able to explain not just what you plan to pay, but why, in which market, and under what assumptions. That is the difference between using wage data responsibly and letting it make decisions it was never built to make.

Start with the wage baseline and separate signal from noise#

Use a coverage-first rule: start with the broad occupational baseline, then layer narrower sources only when they match your market and service format. If two sources conflict, prioritize broader occupational coverage first and adjust with local evidence second.

| Source | Role | Key note |

|---|---|---|

| OEWS / SOC 39-9031 Exercise Trainers and Group Fitness Instructors | Broad occupational baseline | Treat as market context for the occupation, not as a ready-made class rate or payout policy |

| NASM CPT Salary Guide | Directional overlay | Useful for narrower role context only after the broad baseline is set |

| Indeed / Group Fitness | Directional overlay | Useful for narrower role context only after the broad baseline is set |

| Fitness Industry Award [MA000094] (Australia, via Rippling) | Local pay-rule layer | Employee minimum-pay rules for gyms and similar facilities; rates are affected by classification, age, employment type, and time/day penalties, with a stated 25% casual loading for casual workers |

Step 1 Anchor on the broad occupational baseline#

Start with Occupational Employment and Wage Statistics (OEWS) and SOC 39-9031 Exercise Trainers and Group Fitness Instructors. Treat this as market context for the occupation, not as a ready-made class rate or payout policy.

Before you use any figure, label it by jurisdiction, worker type, service format, and source coverage. If any of those are unclear, keep it as context, not a decision input.

Step 2 Layer narrower sources as directional overlays#

Use sources like NASM CPT Salary Guide and Indeed / Group Fitness as directional overlays, not as primary truth. They can be useful for narrower role context, but only after your broad baseline is set.

Keep jurisdiction rules separate from market wage context. In Australia, Rippling describes the Fitness Industry Award [MA000094] as employee minimum-pay rules for gyms and similar facilities, including employed instructors and personal trainers, with rates affected by classification, age, employment type, and time/day penalties, and a stated 25% casual loading for casual workers. That is a local pay-rule layer, not a substitute for a broad occupational baseline.

Step 3 Keep one-on-one CPT and group-class economics separate#

Do not treat one-on-one CPT rate context as interchangeable with group-class delivery economics. They reflect different service formats and different utilization patterns.

Keep separate lines in your model for one-on-one, small-group, and larger class formats. If sources disagree, return to the same rule: broad OEWS occupation first, then local evidence that matches your exact format and jurisdiction.

Related reading: How Platform Operators Pay Contractors in Indonesia With GoPay, OVO, DANA, or BI Fast.

Prepare the inputs before you pick a payout model#

Before you choose a payout model, lock the market inputs you will use to make that decision. Keep gyms and fitness centers, corporate wellness programs, and independent personal trainer supply as separate inputs so you are not pricing different supply pools as if they were one.

Step 1 Define the service mix for each launch market#

Create a short market note for each launch country and list the formats you plan to buy first: one-on-one training, small group, or scheduled classes. Then map likely supply by channel: gyms and fitness centers, corporate wellness programs, or independent trainers.

Step 2 Build a minimum evidence pack before launch#

Use one document per market with four fields: target role mix, expected utilization, cancellation behavior, and market-specific payment constraints. Keep sources relevant to fitness payout operations, and filter out off-topic pages such as education-focused tool roundups.

When you rely on official requirements, prioritize stronger trust signals in source selection, including official-site domains such as .gov where applicable and HTTPS.

Step 3 Pre-select payout rails and your fallback path#

Choose your primary payout route and define the fallback path before launch. Then document where your own stack or provider setup introduces differences in integrations, pricing, or feature coverage, because those differences can change rollout risk by market.

Checkpoint: before launch, your team should be able to answer in writing how trainers are paid in the normal path and what the fallback path is if that route is unavailable.

If you are mapping Latin America rollout details, this pairs well with How Platform Operators Pay Contractors in Colombia with PSE Nequi and DIAN Controls.

Choose a compensation model by session type and utilization reality#

Pick the model that matches real utilization, not forecast assumptions. If demand is still noisy, begin with a per-class guarantee floor. If demand is consistently measurable, a revenue-share model can better tie earnings to booked revenue.

Step 1 Compare the three core models on one page#

Use one decision view for product, ops, and finance so the tradeoffs stay explicit.

| Model | Best starting fit | Main upside | Main risk | Verify first |

|---|---|---|---|---|

| Revenue-share model | Stable booking and billing patterns | Earnings scale with booked revenue | Earnings volatility when attendance or cancellations are unstable | Session-level attendance, billing, and cancellation data quality |

| Per-class guarantee | Early-stage or volatile utilization | Clear earning floor for instructor supply | Platform downside during weak class performance | Ability to fund guarantees through low-occupancy periods |

| Tiered payout model | Repeat volume with reliable performance data | Rewards stronger outcomes without constant model changes | Disputes when tier inputs are unclear | Transparent, auditable metrics across multiple payout cycles |

Fitness businesses already use multiple pay structures, and compensation design affects business outcomes. The goal is fit by format, not one universal rule.

Step 2 Separate one-on-one from group-class payout logic#

Do not force one payout rule across all session types. In practice, you often need different logic by format, and some gyms already separate pay between non-training hours and personal-training hours.

For one-on-one services, set terms with instructor-level variation in mind, since rates can differ by qualifications, experience, and volume. For group classes, use class-level performance signals only when your attendance and payout data are dependable. If both formats are blended in reporting, fix that before you standardize compensation.

Step 3 Choose a starting model by utilization reality#

When utilization is volatile, start with a per-class guarantee and defer tiers until your operating signals settle. When utilization is stable, a revenue-share model is easier to govern because payout moves with booked demand.

Use a tiered payout model only after your inputs are consistently reliable. Otherwise, you are tiering on noise and creating preventable payout disputes.

Step 4 Define trigger rules before launch#

Do not change models ad hoc. Document the trigger framework in advance: metric, source of truth, review cadence, and approver.

You can use signals like fill rate, retention trend, and cancellation stability, but keep cutoffs as internal operating decisions and record them clearly before rollout. If the switch logic is not written down, the model is not ready to scale.

For the finance side of that transition, see Finance Automation and Accounts Payable Growth: How Platforms Scale AP Without Scaling Headcount.

Design country rollout in waves instead of one global policy#

Once your payout model is set by session type, decide rollout shape next: launch in waves, not as one global policy. Keep one shared payout architecture, and use a country matrix to test whether each market is operationally ready before launch.

Step 1 Build a country matrix before approving a market#

Use the same matrix for every market so your product, ops, and finance teams evaluate launch readiness on the same fields.

The segmentation view you already used supports this approach. One fitness market report segments by mode, end use, and region, and another segments virtual fitness by channel and region. In practice, that means markets can start from different operating shapes, so write those assumptions down instead of defaulting to one-size-fits-all.

| Matrix field | What you record | Why it matters |

|---|---|---|

| Service mix | One-on-one, group, online, in-person, hybrid | Keeps payout logic aligned to delivery model |

| Compensation model | Starting model and model-change triggers | Prevents ad hoc local payout rules |

| Payout setup | Planned payout method and exception path | Confirms payout operations are defined before launch |

| Onboarding setup | Required onboarding inputs and review owner | Clarifies readiness for supply onboarding |

| Reconciliation ownership | Finance owner and ledger path | Keeps payout records auditable and reviewable |

Step 2 Gate each country on operational readiness, not demand alone#

Treat launch as an operations decision, not just a market-interest decision. Before you open a country, make sure onboarding, payout handling, exception handling, and reconciliation ownership are clearly defined and testable in your workflow.

If exception handling is still informal, pause the launch. Reconciliation and accounting controls are there to verify internal consistency, completeness, and accuracy, not to clean up preventable payout process gaps later.

Step 3 Keep one payout architecture and parameterize local variance#

Use one core payout flow across markets, then adjust local parameters inside that structure. That lets you vary service mix and compensation choices by market without forking your entire system.

Set a hard no-go rule for your team: do not open a market until payout-failure and hold-handling paths are explicitly defined. This keeps expansion comparable across countries and reduces avoidable payout debt.

Set tax and compliance controls before first payout#

Set compliance gates before payout release, not after onboarding starts. If eligibility goes live before tax collection, validation, and escalation are defined, issues move downstream to finance and support instead of being blocked at the right point.

Step 1 Define the collection set and tie each item to payout eligibility#

Define, per market, what you collect, what you validate, and which payout rule each item controls. Each requirement should lead to one clear outcome: release, hold for review, or reject until corrected.

Use a control sheet with three fields for every requirement: who provides it, what check is run, and what happens on failure. If a required item is missing or mismatched, route the worker to a named exception queue with a reason code and owner instead of leaving them in open-ended manual review.

Do not start accruing earnings before required tax and compliance items are gated. That is how pending balances and one-off exceptions pile up.

Step 2 Pre-document cross-border steps before they become support issues#

For cross-border launches, document whether the payout design creates FATCA, Form 8938, FBAR, or FinCEN steps, who owns review, and what worker-facing copy can say. Keep product copy narrow: escalation path, not filing instructions.

For Form 8938 specifically, anchor controls to what the IRS actually states:

| Form 8938 point | What to encode in controls |

|---|---|

| It is the Statement of Specified Foreign Financial Assets | Use the correct form name in internal playbooks and support scripts |

| Reporting may apply when thresholds are exceeded | Treat threshold checks as filer-context dependent, not one universal trigger |

| IRS references an aggregate value exceeding $50,000 in guidance | Keep this as a context-specific signal, not a blanket rule |

| Instructions reference $50,000 (last day of tax year) and $75,000 (any time during tax year) for certain specified domestic entity contexts | Preserve those values with context labels so teams do not overgeneralize |

| Form says Attach to your tax return | Do not imply the platform files Form 8938 for payees |

| If no income tax return is required for the year, Form 8938 is not required | Add this to internal decision notes to avoid overstatement in support replies |

Step 3 Publish narrow worker guidance and hard-stop release logic#

Give workers concise, general guidance that self-employment tax questions can include Schedule SE context, and keep the boundary explicit: general information only, not tax advice.

Then enforce one release rule: no payout moves from pending to released until required market gates pass. Validate with two pre-launch tests: one worker who passes all gates and one who fails a required item. The fail path should remain blocked with a visible hold reason, the missing or mismatched item, and the owning exception queue.

For a deeper dive on payout architecture and classification boundaries, read How EdTech Platforms Pay Tutors and Instructors at Scale: Tax Classification and Payout Architecture.

Implement the payout execution sequence in product and ops#

Once your compliance gates are working, execution drift becomes an operations problem. Keep payout processing structured so records can be reconciled quickly and corrections can be explained without rebuilding history from scratch.

Step 1 Build a visible sequence from request to resolution#

Use clear, separate payout states instead of one opaque "paid" event. A practical structure is request intake, policy checks, provider routing, execution, reconciliation, and exception resolution, with ownership defined at each stage.

Your checkpoint is simple: for any instructor payout, the record should show what was requested, what checks were applied, what happened in execution, and how exceptions were handled. If support or finance cannot answer that from the record, your process is too thin.

Step 2 Make reconciliation checks part of normal execution#

Treat reconciliation as a core control, not a cleanup step. Accounting operations include balancing and reconciling accounts and verifying accounting documents for internal consistency, completeness, and mathematical accuracy.

This is where many teams lose time: policy holds, execution failures, and reconciliation issues get mixed together. Keep those failure classes separate so each one goes to the right owner and resolution path.

Step 3 Design correction and review paths before launch#

Build records so finance can trace a payout from request to ledger posting to export package. When corrections are required, your process should support journal vouchers and adjustment entries as part of normal accounting handling.

| Owner | Handles |

|---|---|

| Operations | Provider-facing issues and missing details |

| Finance/accounting | Reconciliation and adjustments |

| Engineering | Execution defects |

| Compliance | Holds tied to onboarding or review |

Set this ownership before launch. Completed work should be reviewed for both accuracy and procedural compliance, not only for whether money moved.

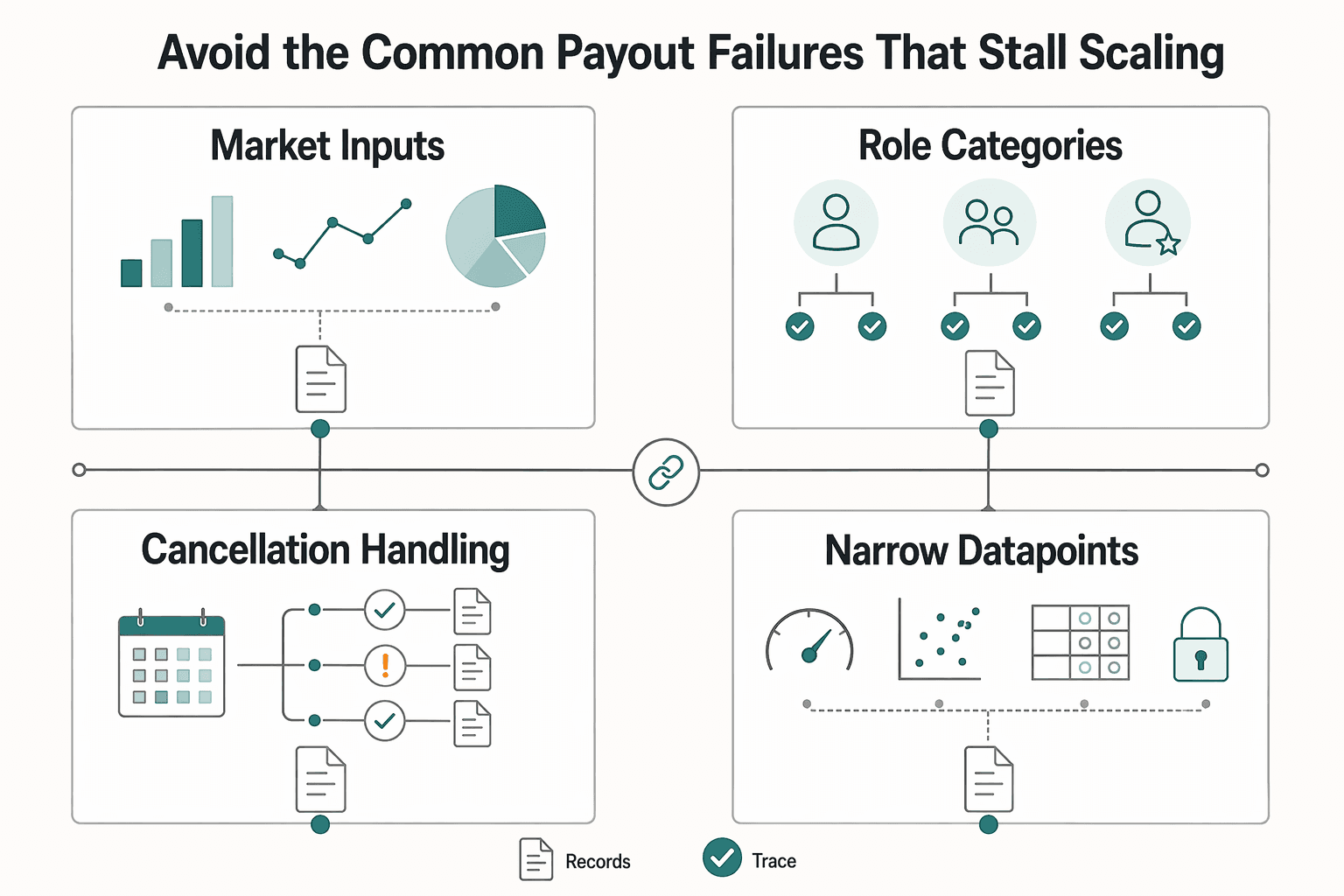

Avoid the common payout failures that stall scaling#

Most scaling failures start before money moves: in category design, policy logic, and exception handling. Keep market signals separate from payout rules, keep role definitions consistent, and make exceptions reviewable from the record.

| Failure area | Control |

|---|---|

| Market inputs vs payout policy | Use market data as input, not as an automatic payout rule |

| Role categories | Standardize categories before pricing and cross-match them to functional responsibilities and the Standard Occupational Classification model |

| Cancellation handling | Treat cancellation decisions as policy and capture the policy version, cancellation context, and review path on the payout record |

| Narrow datapoints | Re-weight with broader role coverage and local pilot evidence, then sample payouts and verify document consistency, completeness, and mathematical accuracy before expanding |

- Separate market inputs from payout policy.

Use market data as an input, not as an automatic payout rule. Your policy should stand on a clear compensation model and explicit guardrails, with a record of what input informed each rate decision.

- Standardize role categories before pricing.

Do not merge distinct trainer or instructor formats into one payout category just because they sit under fitness. A standardized category structure cross-matched to functional responsibilities and the Standard Occupational Classification model improves pricing management, reporting, and quality assurance.

- Define cancellation handling as formal policy.

Treat cancellation decisions as policy, not ad hoc support judgment. Capture the policy version, cancellation context, and review path on the payout record so each outcome is traceable.

- Do not overfit to a narrow datapoint.

A single company example can be directional, but it is not enough for platform-wide assumptions. Re-weight with broader role coverage and local pilot evidence, then sample payouts and verify document consistency, completeness, and mathematical accuracy before expanding.

Make expansion decisions with a payout checklist you can execute#

Use one go/no-go payout checklist for every new market. If an owner, required document, or fallback path is missing, pause launch until it is resolved.

- Set the wage band from the broadest baseline first.

Start with BLS OEWS SOC 39-9031 Exercise Trainers and Group Fitness Instructors, then use NASM and Indeed as directional overlays. If the narrower sources diverge, check whether you are mixing one-on-one, group, and sales-weighted roles before changing policy. Verification point: your launch doc shows baseline source, secondary overlays, and why ranges differ by format.

- Choose the payout model from session economics, not headline pay.

Use a per-class guarantee when attendance is volatile or supply is unproven. Use a revenue-share model when fill rates and retention are stable enough to forecast class economics. Use a tiered payout model when you need a floor first, then upside after preset targets. Define switch triggers before launch: which checkpoint changes the model, and who approves it.

- Validate market readiness before opening the country.

Confirm country rollout constraints and market-specific payment constraints before recruiting instructors. You need required onboarding documents, supported payout methods, and a fallback path for failed or held payouts. If reconciliation ownership is unclear, readiness is incomplete. Evidence pack: onboarding requirements, supported payout rail, fallback process, exception owner, reconciliation owner.

- Finalize tax and compliance gates before first release.

For U.S. workflows, document where FATCA, Form 8938, FBAR, FinCEN, and Schedule SE context may require review. The concrete gate here is Form 8938: IRS materials state it is used to report specified foreign financial assets, is attached to the annual income tax return, and applies when value exceeds the applicable reporting threshold. IRS materials also reference $50,000 for certain taxpayers and, for certain specified domestic entities, $50,000 on the last day of the tax year or $75,000 at any time during the year. Keep worker-facing guidance operational and route tax determinations to tax review.

- Launch in waves and expand only after weekly controls stay stable.

Start with one market or provider cohort, then review payout accuracy, reconciliation completion, and exception handling weekly. Pause expansion if duplicate-risk retries appear, exceptions age without owners, or finance cannot trace payouts to policy version and attendance records. Scale when the payment path is stable, not just when early demand is strong.

If you're working through "fitness platform operators pay personal trainers class instructors scale" for a specific country or program, Talk to Gruv.

Frequently Asked Questions

What do fitness instructors and trainers earn on average in the United States?

Use caution with the word average. The excerpts in this pack do not establish a single U.S. national average. One source says there are five common trainer pay structures, including a low hourly W2 model, and notes that bonuses/commissions are common in some setups. If you mix role types, one number can mislead.

What is a realistic starting pay range to budget when entering a new fitness market?

Budget by pay structure, not a headline number. Set separate ranges for hourly wage roles and variable-pay roles (for example, bonus/commission-heavy setups), then refine after pilot performance.

How should I use BLS data versus NASM and Indeed salary pages?

This grounding pack does not include BLS, NASM, or Indeed wage figures, so treat those as separate research inputs. It does show mixed freshness across excerpts: one page was updated Oct. 29, 2025, one is dated July 21, 2024, and one is dated June 28, 2021.

Can I use one company salary page to set platform-wide payout policy?

No, not by itself. A single page may reflect a different role scope and compensation structure than your model. Use it as one input, then validate against your own economics and operating rules.

When should I choose revenue share instead of a per-class guarantee?

Choose revenue share when class economics are predictable enough for both sides to plan confidently. Start with a per-class guarantee when demand is still uncertain and you need a clearer floor during early testing.

Why is wage data alone not enough to design payout architecture at scale?

Wage data is context, not a full payout design. You still need explicit rules for structure and exceptions, especially because trainer compensation can combine hourly wages with variable elements like commissions or bonuses.

What key unknowns should I validate first for cross-border fitness payouts?

These excerpts do not provide validated cross-border tax or compliance thresholds. Before launch, confirm required onboarding documents, payout-method support, and who owns payout-failure and exception handling.

Try a related tool

Connor writes and edits for extractability—answer-first structure, clean headings, and quote-ready language that performs in both SEO and AEO.

Sources

- acces.nysed.gov/sites/acces/files/vr/crsguide2024-28.pdftrusted

- bls.gov/cps/cpsaat39.htmtrusted

- chandlerazpd.gov/wp-content/uploads/2024/12/A00-GO-Public-Web...trusted

- congress.gov/117/plaws/publ103/PLAW-117publ103.htmtrusted

- dol.gov/sites/dolgov/files/WHD/legacy/files/SCADirec...trusted

- ecfr.gov/current/title-29/subtitle-B/chapter-XVII/par...trusted

- fda.gov/food/food-safety-modernization-act-fsma/freq...trusted

- iowacentral.edu/pdfs/Student_Handbook.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How EdTech Platforms Pay Tutors: Tax and Payout Architecture

If you are deciding whether to open a new tutor market, set your operating model before you localize pricing, onboard tutors, or connect payout rails. You should treat classification, tax ownership, and payout architecture as launch decisions, not cleanup work for after go-live.

How Logistics and Freight Platforms Pay Carriers and Owner-Operators at Scale

If you are sizing a freight payout product from owner-operator pay headlines alone, pause. Those figures can tell you the market is active, but they cannot tell you whether your payout design will hold up when contractor mix, lane economics, and country constraints can all shift.

How Platform Teams Scale AP Volume Without Adding Headcount

Use this as a decision list for operators scaling Accounts Payable, not a generic AP automation explainer. In these case-study examples, invoice volume can grow faster than AP headcount when the platform fit is right, but vendor claims still need hard validation.