Quick Answer

Start with an eligibility decision, then draft. An FBAR reasonable cause letter template should organize dated facts for each late FinCEN Form 114 year, explain why filing was late, and match what is submitted in the BSA E-Filing System. Use the delinquent path only when exam/contact and tax-reporting conditions are clean. Keep the filing evidence bundle, because submissions can still be reviewed and relief is conditional, not automatic.

When a Reasonable Cause Letter May Help With a Late FBAR#

Start with eligibility, not wording. For a late Report of Foreign Bank and Financial Accounts, the biggest risk is choosing the wrong procedure before you confirm the filing fits the IRS lane for delinquent FBARs.

That lane is narrow. It is for taxpayers who do not need Streamlined Filing Compliance Procedures or IRS Criminal Investigation Voluntary Disclosure Practice, are not under IRS civil examination or criminal investigation, and have not already been contacted by the IRS about delinquent FBARs. It also ties penalty non-imposition to proper U.S. return reporting and tax payment on related foreign-account income. If that point is unclear, pause and validate the filing path before you draft anything.

Set expectations for the document itself. The IRS requires a statement explaining why the FBARs are late, and the electronic cover page requires a late-filing reason. The guidance sets required filing elements rather than a single fill-in letter format. If you came looking for an FBAR reasonable cause letter template, use a fact-based structure you can adapt, then test it against the eligibility rules and your records.

Reasonable cause is evaluated case by case based on facts and circumstances, so polished wording will not fix a bad eligibility call. Filing late with a statement also does not guarantee relief or remove audit risk.

Treat this as operational guidance for compliance, legal, finance, and risk owners building a defensible late-FBAR process. It is not individualized legal advice. If facts are mixed, incomplete, or potentially adverse, use this structure to organize the file quickly and escalate before filing.

Related reading: How to Determine the Maximum Value of a Foreign Bank Account for FBAR.

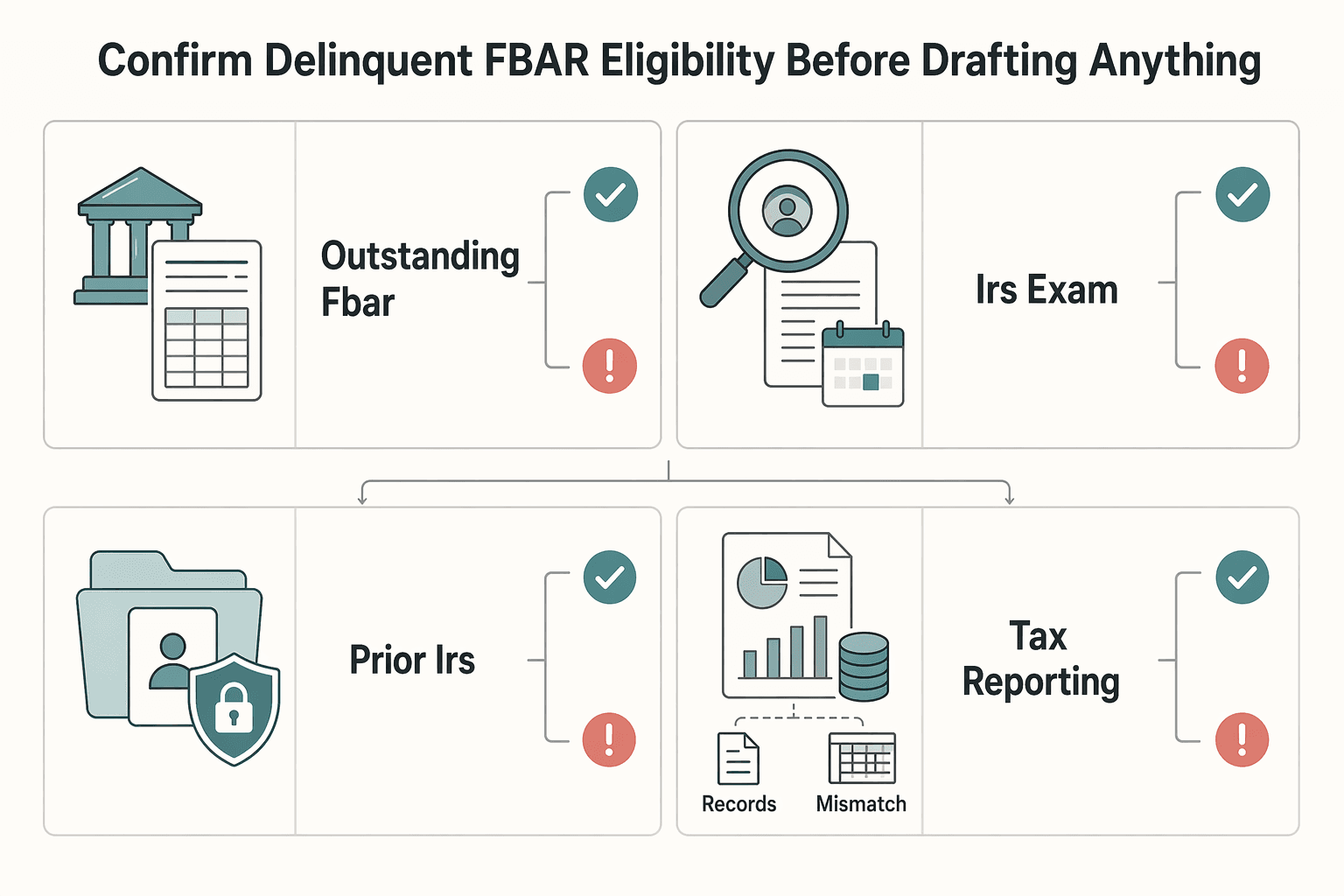

Confirm Delinquent FBAR eligibility before drafting anything#

Make a clear go or no-go decision on Delinquent FBAR Submission Procedures before you draft the statement. If foreign-account income was not properly reported on U.S. returns and all related tax was not paid, this path may not support penalty non-imposition. Pause and evaluate other options before filing through the BSA E-Filing System.

This lane applies only to delinquent FinCEN Form 114 filings. The taxpayer must not need Streamlined Filing Compliance Procedures or IRS Criminal Investigation Voluntary Disclosure Practice, must not be under IRS civil examination or criminal investigation, and must not already have been contacted by the IRS about the delinquent FBARs.

| Eligibility gate | Confirm internally | Pause if |

|---|---|---|

| Outstanding FBAR exists | One or more FinCEN Form 114 filings are still missing, and the year crossed the FBAR threshold (aggregate foreign account value over $10,000 at any time during the calendar year) | The year was already filed, or the threshold was not met |

| No IRS exam or investigation | No current IRS civil exam or criminal investigation for the filer | Any active exam or investigation, or status is unclear |

| No prior IRS contact on delinquent FBARs | No IRS notice, letter, or direct contact on the specific delinquent FBAR issue | IRS has already contacted you about the late FBARs |

| Tax reporting was complete | Foreign-account income was properly reported and tax was paid | Unreported income, unpaid tax, or returns may need amendment |

Document how each gate was checked before you draft the late-filing statement. Keep enough detail that another reviewer could reconstruct the decision from the file. For internal control, retain:

- filer name and FBAR years at issue

- gate-by-gate status and what was reviewed

- decision date

- who made the eligibility call

If any gate is uncertain, treat that as a stop signal. Delinquent submission does not guarantee penalty relief, and filings may still be selected for audit.

For a step-by-step walkthrough, see FBAR for a Foreign-Owned US LLC and the Filing Path That Works.

Choose the right path when Delinquent FBAR is not a fit#

When Delinquent FBAR is not a clean fit, the next step is not better drafting. It is choosing the right lane based on the full scope of the problem.

The bigger risk is not weak language in a statement. It is filing under a procedure that does not match the facts.

| Lane | Use only after confirming | What it addresses | Main mismatch risk |

|---|---|---|---|

| Delinquent FBAR Submission Procedures | Year-by-year review supports an FBAR-only filing gap | Late FinCEN Form 114 filings | You treat an FBAR gap as the full issue when returns or other international forms may also need work |

| Streamlined Filing Compliance Procedures | Separate eligibility review is complete outside this section | Requires separate program-specific analysis | You choose a path before the facts are complete |

| IRS Criminal Investigation Voluntary Disclosure Practice | Separate eligibility review is complete outside this section | Requires separate program-specific analysis | You choose a path before the facts are complete |

| Delinquent International Information Return Submission Procedures | Separate eligibility review is complete outside this section | Requires separate program-specific analysis | You fix FBARs but leave the return package incomplete |

These program names are not interchangeable. If facts are mixed or incomplete, escalate early instead of guessing.

Run the FATCA/Form 8938 checkpoint before selecting a lane#

Form 8938 and FBAR are separate requirements, so filing one does not satisfy the other. Before you settle on a path, use the IRS Form 8938 vs FBAR comparison chart as a required checkpoint.

Review year by year and verify what was required and what was actually filed:

- Check whether an income tax return was required for that year.

- If a return was required, confirm whether Form 8938 should have been attached and filed by that return's due date, including extensions.

- Confirm whether FBAR was filed separately, since Form 8938 does not replace FinCEN Form 114.

- Confirm asset scope, not just account count. Form 8938 can include specified foreign financial assets beyond bank accounts, including certain foreign-issued securities held for investment.

- Apply filer profile before concluding thresholds, because higher Form 8938 thresholds can apply to joint filers and taxpayers residing abroad.

Keep the grounded threshold details in your review file:

- Baseline Form 8938 threshold cited for certain U.S. taxpayers: aggregate value exceeding

$50,000. - For specified domestic entities: more than

$50,000on the last day of the tax year or more than$75,000at any time during the tax year. - If no income tax return was required for the year, Form 8938 is not required for that year.

- Form 8938 reporting applies to taxable years starting after

March 18, 2010with most individuals starting on the2011return year.

Keep FBAR cleanup separate from non-FBAR return cleanup#

Do not stop once you identify missing FBAR years. If non-FBAR international information returns are also missing, treat that as a separate lane decision, not as an FBAR-only narrative.

A simple year-by-year matrix helps reviewers and counsel see the same facts quickly:

- Income tax return required or filed

- Form 8938 required or attached

- FBAR required or filed

- Other international information returns potentially missing

- Asset types involved, including accounts and non-account assets

- Open factual gaps

Also check entity scope. Certain domestic corporations, partnerships, and trusts can be specified domestic entities for Form 8938 purposes, so the review may need to cover entities, not only individuals.

Escalate early when facts are mixed#

Use a simple rule here. If you cannot clearly show this is only a late-FBAR issue, escalate to tax counsel before filing anything.

Escalate immediately when return history is incomplete, foreign asset classification is unclear, Form 8938 status is uncertain, or non-FBAR international forms may also be missing. Working rule: use the narrow lane only when facts are clean. When facts are mixed, get legal and tax review first.

If you have never filed an FBAR before, read What to Do If You've Never Filed an FBAR (Delinquent FBAR Procedures).

Assemble the evidence pack that supports reasonable cause#

Start with evidence, not prose. For late FinCEN Form 114 filings, the statement is strongest when a reviewer can follow dated facts from discovery to correction.

Gather the four inputs before drafting#

Build one file per late FBAR year, plus a short cross-year index.

| Input | What to collect | Key detail |

|---|---|---|

| Filing timeline | Each delinquent year | When the FBAR should have been filed, when it will be filed through the BSA E-Filing System, and a statement explaining why the FBARs are late |

| Account discovery timeline | Account history and authority | When the accounts existed, when you had financial interest or signature authority, and when the filing gap was identified, with dated support |

| Prior tax return status | Year-by-year return status | Whether U.S. returns were filed and whether foreign-account income was properly reported and taxed |

| Correspondence tied to the late years | Related communications | Preparer communications, internal reminders, prior filing instructions, bank communications, and any IRS correspondence |

Use that table as your drafting checklist. If one of the four inputs is thin or missing, fix the record before you write the narrative.

Map facts to the reasonable-cause standard#

The evidence file should do more than explain lateness. It should show ordinary care and prudence, what prevented timely filing, and what you did once the issue was found.

Keep conclusions out of the evidence layer. "We did not know" is a conclusion. Dated records showing what happened and what changed are the proof. If legal wants a policy crosswalk, build it from the same record.

Reliance on a tax professional is generally not enough on its own. If a preparer is part of the timeline, document what information you provided, what was asked, and what corrective actions followed.

Keep facts separate from narrative and log adverse facts#

Use a two-layer approach: evidence pack first, then the Reasonable Cause Statement. This makes unsupported language easier to spot and keeps the narrative aligned with the record.

Log adverse facts explicitly, including prior reminders, inconsistent filings, earlier related disclosures, or IRS contact about the delinquent FBARs. Do not bury those points. Address them directly in legal review. Delinquent FBAR procedures require that you have not already been contacted by the IRS about those delinquent FBARs, and delinquent FBAR submissions can still be selected for audit.

For a broader framework on building your support file, see How to Document 'Reasonable Cause' for IRS Penalty Abatement.

Build the reasonable cause letter template section by section#

Use one practical structure and keep it evidence-led. A strong statement lets a reviewer quickly see ordinary care, what interrupted timely filing, and what you did after discovery.

Use five core blocks in a consistent order#

Keep these core blocks in this order as a drafting default, even though the facts will vary:

| Block | What to include | Drafting note |

|---|---|---|

| Taxpayer context | Identify the filer, the role that created the filing obligation, and the affected late-FBAR years | For business fact patterns, name the person with authority over filing decisions |

| Filing lapse timeline | List each delinquent year, when the FBAR should have been filed, when the gap was identified, and when the late filing was or will be submitted | Keep this as dated chronology, not argument |

| Cause narrative | Explain what happened, how it prevented timely filing, and why the issue persisted until discovery | Tie it to ordinary care and prudence and to case-by-case facts and circumstances |

| Corrective actions | State the review steps, account reconciliation, filing preparation, and process fixes | Name what was corrected and for which years |

| Attestation of accuracy and good faith | Close with a short good-faith statement | State that facts are true to the signer's knowledge |

This five-block order is a practical structure, not an IRS-mandated paragraph format.

Tie each block to recognized standards#

Use the standards as drafting checks, not as labels. Reasonable cause is evaluated on all facts and circumstances. Relief is framed around reasonable cause, good faith, and ordinary care and prudence, and Policy Statement 3-2 is an additional IRS reference point. Penalty relief is possible, but not automatic.

Draft against weak conclusions. If you say the requirement was missed, show dated facts: what accounts existed, who had authority, what controls existed, and what event exposed the gap. If adverse facts exist, address them directly in the narrative or escalate for legal review before filing.

If your team references "willful neglect" or 26 CFR 301.6724-1 internally, treat that as internal framing only here, not as an FBAR-specific template rule from these materials.

Apply minimum viable content rules#

At minimum, include:

- Specific dates or date ranges for account authority, gap discovery, and late-filing actions

- A clear causal chain from event to delay to correction

- An explicit correction statement listing what was filed and which years were covered

Then verify each line against your evidence pack and filing records. Conclusory language is the common failure mode, especially a standalone reliance-on-preparer statement without fact detail.

Add optional blocks only when facts require them#

Keep one narrative for multi-year late filings when one cause explains all years and remediation was coordinated. Split by year when causes, accounts, or adverse facts differ.

For multi-entity operations, use one narrative only when control failure, responsible personnel, and remediation are shared. Use separate statements when authority differs, when third-party electronic filing is involved for only some entities, or when facts do not align.

Also confirm filing-path mechanics where relevant: separate IRM procedures for 25 or More Accounts, consolidated filing, third-party electronic filing, and the aggregate value over $10,000 checkpoint. These mechanics do not replace the narrative, but the statement should match the filing path actually used.

Related: Filing FBAR Late: Reasonable Cause Statements and Delinquent Submission Procedures.

Use language that is specific, factual, and non-defensive#

Write this like an evidence record, not a plea. For a late Report of Foreign Bank and Financial Accounts, the most credible language explains the ordinary care you used, what interrupted compliance, and what you did after discovery.

Replace conclusions with dated facts#

Lead with facts your records can support. The IRS says reasonable cause is determined case by case based on all facts and circumstances, so broad conclusions without dates, documents, and corrective action can weaken credibility.

| Weak claim | Stronger factual statement | What should back it up |

|---|---|---|

| "I was unaware of the FBAR requirement." | "Until March 2025, I believed my foreign accounts were not reportable because they were opened for local payroll use. During a 2025 compliance review, I learned FinCEN Form 114 applied to the 2022 through 2024 years, and I began preparing the late filings that week." | Review notes, account records, dated discovery email, filing timeline |

| "My preparer never told me." | "I used a return preparer for income tax filings, but I did not provide the foreign account information needed to evaluate FBAR reporting. After identifying that omission on April 8, 2025, I collected the account data and completed the delinquent filings." | Organizer, prior intake documents, emails, account list |

| "The filing was late due to an oversight." | "The employee responsible for foreign account reporting left in June 2023, no handoff occurred, and the missed filing was identified during a control review in February 2025. We then reconciled all reportable accounts and submitted the delinquent FBARs." | Departure records, control review notes, reconciliation file |

Phrases that usually need rewriting#

Vague or defensive lines usually hurt more than they help. Rewrite phrases like "I relied on my accountant," "this was an innocent mistake," or "penalty relief should apply." Reliance on a tax professional is generally not enough by itself, and taxpayers are generally responsible for complying with tax law. Show your own ordinary care instead: what you provided, what you reviewed, and what you did once the issue was found.

Use a hard drafting rule: if you cannot prove a claim with records, rewrite it as a narrower fact statement or remove it. For example, replace "I always tried to comply" with "I timely filed my income tax returns for the same years and submitted the delinquent FBARs promptly after discovery."

Keep the tone sober and verifiable. Under Delinquent FBAR Submission Procedures, include a statement explaining why the filing is late and select a reason for filing late on the electronic cover page. Do not promise automatic penalty relief or assume there will be no further review.

If you live abroad, see FBAR and FATCA Reporting for US Expats for the broader reporting context.

Execute filing in the right order inside FinCEN systems#

Once the statement is ready, execution should be mechanical. Finalize the late-filing statement first. Then file each delinquent FinCEN Form 114 through the BSA E-Filing System, select the late-filing reason on the electronic cover page, and verify every intended year was submitted.

| Phase | Required action | Record or check |

|---|---|---|

| Before data entry | Finalize the late-filing statement first | Confirm it matches the delinquent years and the late-filing reason before filing |

| Electronic submission | File all delinquent FinCEN Form 114s in the BSA E-Filing System and select a reason for filing late on the electronic cover page | Track missing years year by year and do not close the task after a partial submission |

| If e-filing is blocked | Inquire with FinCEN Regulatory Help to determine possible alternatives to electronic filing | Log the date and time, error summary, screenshots if available, and any case number, email trail, or secure message |

| After submission | Confirm every intended delinquent year was filed and retained records match the final statement text and filed data | Save the submission confirmation for each year, a copy of filed FinCEN Form 114 data, the exact statement text submitted, and the internal checklist and reviewer signoff |

| If a correction is needed | Complete a new FBAR and check Amend in Item 1 | Keep any Prior Report BSA Identifier with the amended filing record |

Finalize the statement before data entry#

Lock the statement before anyone enters FBAR data. Under delinquent FBAR procedures, you must include a statement explaining why the FBARs are late, so last-minute edits can create mismatches between your narrative and what was actually filed.

Before submission, confirm the statement matches the delinquent years and late-filing reason. If those do not align, correct them before filing.

Submit all delinquent FBARs in the BSA E-Filing System#

File all delinquent FBARs electronically in FinCEN's BSA E-Filing System. On the electronic cover page, select a reason for filing late, and treat that selection as separate from the required statement explaining why the filing is late.

If multiple years are missing, track them year by year and do not close the task after a partial submission.

Route blocked electronic filing to FinCEN Regulatory Help#

If electronic filing is blocked, do not guess at alternatives. IRS guidance says you may inquire with FinCEN Regulatory Help to determine possible alternatives to electronic filing.

For internal tracking, log the exception path the same day: date and time, error summary, screenshots if available, and any case number, email trail, or secure message.

Verify every year and preserve the evidence trail#

After submission, reconcile before marking the matter complete. Confirm every intended delinquent year was filed and that retained records match the final statement text and filed data.

Delinquent FBARs are not automatically subject to audit, but they may be selected for audit, so keep a complete evidence trail. For internal recordkeeping (not a stated IRS/FinCEN required package format), save:

- submission confirmation for each filed year

- copy of filed FinCEN Form 114 data for each year

- exact statement text submitted with the late filing

- internal year-by-year checklist and reviewer signoff

If you find a correction issue after filing, use the amendment path: complete a new FBAR and check Amend in Item 1. Keep any Prior Report BSA Identifier with the amended filing record.

Run sanity checks before final submission#

A filing confirmation is not the last control. Before you close the matter, run one final consistency check across the Reasonable Cause Statement, the tax return file, and the foreign-account record.

Reconcile the statement to your records#

Start by validating each concrete sentence in the statement against your working papers. The tax years, filer identity, and account history should all align with what was actually filed and documented.

Use year-activity facts as a practical cross-check. Confirm whether an income tax return was required and filed, and whether any foreign assets or accounts were acquired, sold, or closed during the year. If a sentence cannot be supported, narrow it or remove it.

Check Form 8938 and FBAR consistency before submission#

Do not treat Form 8938 as a substitute for FBAR. Filing Form 8938 does not remove the need to file FinCEN Form 114 when FBAR applies.

Run this quick check:

- Confirm whether Form 8938 was required for the filer and year you are reviewing.

- For specified domestic entities, check the stated thresholds: more than

$50,000on the last day of the tax year or more than$75,000at any time during the year. - If required, confirm Form 8938 was attached to the related income tax return, not just prepared.

- If no income tax return was required for that year, document that Form 8938 is not required even if foreign assets exceed the threshold.

- Use the Form 8938 instructions' comparison chart for Form 8938 vs. FBAR requirements, and reconcile account treatment so the same account is not described inconsistently.

Pause and escalate if the file is still inconsistent#

If tax-return facts and foreign-account facts still do not reconcile, stop before submission. A late FBAR package alone does not resolve unresolved tax-return inconsistencies.

Consider dual review and log the decision#

If your team uses a final two-person review before filing, assign one reviewer for filing accuracy and evidence completeness and one for tax-return linkage and issue spotting. Record names, roles, date and time, years reviewed, what was checked, including Form 8938 where relevant, and how mismatches were resolved. If an issue remains open, keep the file in escalation rather than filing incomplete.

Before sign-off, run your account-year exposure check in the FBAR calculator and attach the output to your review packet.

Plan post-filing monitoring and escalation#

After you file, treat the matter as still live. Relief is possible, but not automatic, reasonable-cause determinations are case by case, and delinquent FBAR submissions can still be selected for audit through existing IRS selection processes.

- Set expectations immediately after submission.

Under the Delinquent FBAR Submission Procedures, the IRS says it will not impose a failure-to-file penalty when the stated reporting and payment conditions are met. Treat that as conditional relief, not blanket clearance. Confirm your file includes the exact late-filing explanation statement submitted and that the late-filing reason selected on the BSA E-Filing cover page matches your internal record.

- Define escalation triggers before any follow-up arrives.

Escalate if you receive an IRS notice, information request, or other examination contact. If electronic filing is not possible, use FinCEN Regulatory Help to identify alternatives. Escalate the same way if your team discovers new facts after filing that conflict with what was submitted. When that happens, pause informal fixes and route the file to tax or legal review with a dated memo covering what changed, who identified it, and which years are affected.

- Keep a response-ready retention bundle.

Maintain one bundle with the filed statement, submission confirmations, filed FBAR data by year, supporting evidence, and the decision log. Use a simple test: can a new reviewer reconstruct why this path was used and what supports it without re-interviewing the filer? If not, strengthen the file before you need to respond.

For teams that already run post-mortems, apply the same documentation discipline here: How to Conduct a Payment Platform Post-Mortem: Root Cause Analysis for Outages and Errors.

Operationalize this as a repeatable control in your payments stack#

Treat delinquent FBAR handling as a standing control, not a one-off cleanup task. The goal is to make eligibility decisions, drafting, filing, and documentation repeatable under pressure.

Put the checkpoint where tax evidence already moves#

Put the FBAR checkpoint in the same compliance lane where your team already handles tax documents, exception explanations, and audit-ready exports. Trigger that checkpoint when you identify an unfiled FBAR or a filing mismatch that points to a missed year.

Before drafting, set a clear go or no-go gate for the Delinquent FBAR Submission Procedures. Your intake should confirm whether the filer has already been contacted by the IRS about the delinquent FBARs, whether foreign-account income was properly reported, whether all tax was paid, and whether the case needs a different route (such as Streamlined procedures or CI voluntary disclosure). If those facts are unclear, pause this path and escalate before drafting.

Assign ownership before the fire drill#

Named ownership keeps decisions from becoming ad hoc. One workable model is:

- Finance or tax operations owns intake and fact collection.

Capture filing years, account facts, prior return status, and records needed for the late-filing explanation statement.

- Legal or tax review owns the eligibility decision.

Approve whether the facts fit the delinquent FBAR path or require a different route.

- Compliance or risk owns submission control and recordkeeping.

Verify filing through FinCEN's BSA E-Filing System, confirm the cover-page late-filing reason is selected, and retain the submission confirmation.

Make approval visible in the record#

Use policy gates that produce a simple audit trail with date, reviewer, decision, and facts reviewed.

| Control point | What must be confirmed | Evidence to retain |

|---|---|---|

| Eligibility approval | No prior IRS contact about the delinquent FBARs; facts support this procedure | Dated reviewer sign-off and intake checklist |

| Draft approval | Late-filing explanation statement matches documented facts | Final approved statement text |

| Submission approval | FBARs filed through BSA E-Filing; late-filing reason selected on the cover page | Submission confirmation and filed data export |

| Exception handling | E-filing not possible | FinCEN Regulatory Help inquiry log or escalation memo |

As a final check, compare the exact statement text stored internally with what was submitted, and confirm each intended year was filed.

Keep sensitive data out of casual review paths#

As an internal control choice, limit exposure of sensitive taxpayer data in drafting and review artifacts. Mask details in shared review materials when full values are not required, and restrict unmasked records to the people preparing or submitting the filing.

Keep the full evidence pack in a controlled location, including the final statement, filed FBAR data, and submission confirmations. This supports a cleaner response if the filing is later selected for audit and reduces avoidable data-handling risk.

Conclusion#

The safest approach is procedural, not rhetorical: verify eligibility, file correctly, and keep an audit-ready record. If you confirm an FBAR was required, confirm Delinquent FBAR Submission Procedures fit your facts, file the delinquent FBARs correctly, and preserve what you submitted. That helps reduce avoidable penalty risk without creating a larger compliance error.

Use this closeout checklist before relying on any template or internal draft:

- Start with threshold and eligibility facts

Confirm an FBAR filing obligation existed. FinCEN's threshold is foreign accounts that exceeded $10,000 in maximum value or aggregate maximum value during the year. Then confirm IRS entry conditions for the delinquent path: no IRS civil exam or criminal investigation and no prior IRS contact about delinquent FBARs. Also verify whether foreign-account income was properly reported on U.S. returns with related tax paid, because IRS non-penalty treatment is conditioned on that. If any of those facts is uncertain, stop treating this as a routine late-file case.

- Draft a factual statement, not a defensive one

The IRS requires a statement explaining why the FBARs are late. Keep it factual and consistent with the filing years, account history, and return history. Before submission, compare the narrative against the electronic FBAR form data and your tax-return file. If you cannot document a point, narrow it or remove it.

- Execute the filing exactly as required

File all delinquent FBARs electronically through FinCEN's BSA E-Filing System, and select a late-filing reason on the electronic cover page. Treat that as a required checkpoint. After filing, save the submission confirmation, filed data for each year, and the exact statement text submitted.

- Keep an audit-ready record and escalate ambiguity early

Delinquent FBAR submissions are not automatically audited, but they may still be selected through normal audit processes. Keep the eligibility decision, supporting evidence, final statement, filed FBAR records, and submission confirmations together. If e-filing is blocked, use FinCEN Regulatory Help and record the inquiry and outcome. If facts become unclear, escalate before taking another filing step.

Use a controlled sequence, not a generic template, as your main protection. When facts are clean, this keeps remediation efficient. When facts are mixed, it gives you an early signal to involve tax or legal review before the wrong path hardens into a bigger problem.

If you need to turn this playbook into a controlled workflow with approvals, audit logs, and retention, contact Gruv.

Frequently Asked Questions

Is there an official IRS FBAR reasonable cause letter template?

The IRS delinquent FBAR guidance does not provide a fill-in template. It instructs filers to include a statement explaining why the FBARs are late and to select a late-filing reason on the electronic form cover page.

Who qualifies to use Delinquent FBAR Submission Procedures?

This path is for filers who are not under IRS civil examination or criminal investigation, have not already been contacted by the IRS about the delinquent FBARs, and do not need CI voluntary disclosure or Streamlined Filing Compliance Procedures. IRS also states it will not impose a failure-to-file penalty when stated conditions are met, including proper U.S. return reporting and payment of tax on foreign-account income. If you cannot confirm those facts, pause and escalate.

What must a Reasonable Cause Statement include for a late FinCEN Form 114 filing?

At minimum, include a statement explaining why the FBARs are late. The IRS guidance cited here does not specify a required paragraph structure, so keep the statement factual and consistent with your records. Before submission, verify it matches the tax returns, account history, and exact filing years on FinCEN Form 114.

Does filing a late FBAR with a statement guarantee penalty relief?

No. A late-filing statement alone does not guarantee relief in every case. The IRS says it will not impose a failure-to-file penalty for delinquent FBARs when the stated conditions are met, including proper U.S. return reporting and payment of tax on foreign-account income.

Can delinquent FBAR submissions still be audited after filing?

Yes. The IRS says delinquent FBARs are not automatically audited, but they may still be selected through normal audit selection processes. Keep your filing records, including the BSA E-Filing confirmation, for each year.

How do FBAR and FATCA Form 8938 relate when fixing late international reporting?

They can overlap, but they are not interchangeable. Form 8938 is attached to the annual tax return and filed by that return’s due date, including extensions, and certain taxpayers may need it when aggregate asset value exceeds $50,000, with higher thresholds in some cases. Filing Form 8938 does not remove a separate FinCEN Form 114 obligation when an FBAR is otherwise required.

When should a team use Streamlined Filing Compliance Procedures instead of Delinquent FBAR procedures?

Do not force the delinquent FBAR lane when you need to file delinquent or amended tax returns to report and pay additional tax, or when facts are otherwise mixed. The IRS frames the Delinquent FBAR path for taxpayers who do not need Streamlined procedures or CI voluntary disclosure. If eligibility is unclear, get legal or tax review before filing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- fincen.gov/system/files/shared/FBAR%20Line%20Item%20Fil...trusted

- irs.gov/individuals/international-taxpayers/delinque...trusted

- irs.gov/payments/penalty-relief-for-reasonable-causetrusted

- taxpayeradvocate.irs.gov/wp-content/uploads/2024/12/ARC24_MSP.pdftrusted

- taxpayeradvocate.irs.gov/wp-content/uploads/2020/08/ARC16_Volume3_03_...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Missed an FBAR Filing? When Delinquent FBAR Procedures Fit and When They Do Not

Finding a missed FBAR filing is unsettling, especially if you are usually careful. In most cases, though, this is a sequencing problem, not a guessing game. The cleanest fix is to classify the facts, choose the right IRS path, and file a record that stays consistent from start to finish.

Filing FBAR Late: Reasonable Cause Statements and Delinquent Submission Procedures

Late FBAR filing can be a controls issue, not just a tax cleanup task. For teams managing cross-border accounts, it can expose gaps in ownership, recordkeeping, and escalation at the same time.

How to Document 'Reasonable Cause' for IRS Penalty Abatement

Your reasonable-cause case starts before anything goes wrong. The goal here is routine proof that you exercised ordinary business care and prudence, not trying to write a better story after a miss. Reasonable cause is reviewed case by case, and you carry the burden to substantiate it.