Quick Answer

Start by determining whether you actually had an FBAR filing obligation and whether all related foreign income was reported and taxed. If the accounts exceeded $10,000 in aggregate, the failure was non-willful, and the IRS has not contacted you, Delinquent FBAR Submission Procedures may fit. If income reporting, tax payment, or willfulness is an issue, use the IRS path that matches those facts instead of filing late forms ad hoc.

Finding a missed FBAR filing is unsettling, especially if you are usually careful. In most cases, though, this is a sequencing problem, not a guessing game. The cleanest fix is to classify the facts, choose the right IRS path, and file a record that stays consistent from start to finish.

This guide follows that sequence in three phases: Triage and Diagnosis, Strategic Path Selection, and Flawless Execution. The goal is simple: understand what happened, pick the right correction route, and close the issue without creating a bigger one.

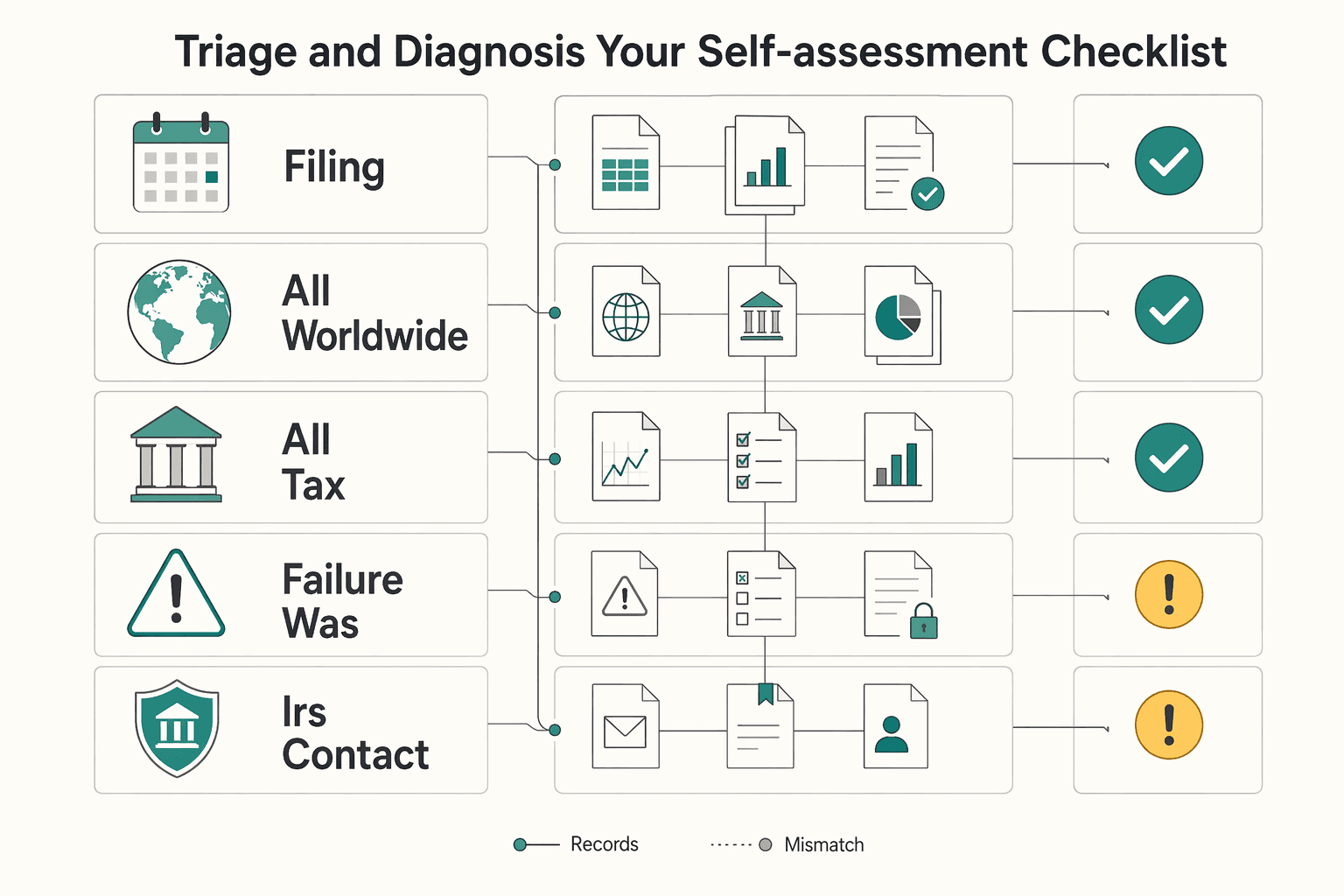

Phase 1: Triage & Diagnosis - Your Self-Assessment Checklist#

Start by classifying the facts before you choose a filing path. Pull your filed U.S. returns, foreign account statements, and payment records year by year so you are working from documents, not memory.

| Question | Verify | If no |

|---|---|---|

| FBAR filing obligation for that year | Whether combined covered accounts went over $10,000 at any point; include accounts you could control by signature authority | Keep your calculation and stop this process for that year |

| All worldwide income tied to those accounts reported | What was actually filed for wages, tips, and other income | Move to a path that includes amended returns, not a late-FBAR-only fix |

| All U.S. tax due on that income paid | Return and payment records, and transcripts or account records if needed | Use a path that addresses both return corrections and tax due |

| Failure was non-willful | Facts about what you knew, what you gave your preparer, and when you learned FBAR might apply | Skip ahead to the red-line section and get legal advice before filing |

| No IRS contact, civil exam, or criminal investigation | Whether the IRS has already contacted you or initiated certain actions | Phase 2's standard routes may not apply |

FBAR is FinCEN Form 114. The trigger is whether the aggregate value of covered foreign accounts exceeded $10,000 at any time during the calendar year. This is a combined-value test, not a per-account test. It can include bank accounts, brokerage accounts, mutual funds, and accounts where you had signature or other authority. Whether an account produced taxable income does not determine whether it is reportable for FBAR purposes.

- Did you have an FBAR filing obligation for that year?

Check each year separately. Confirm whether your combined covered accounts went over $10,000 at any point and whether you missed the April 15 due date, with the automatic extension to October 15. Include accounts you could control by signature authority, even if you did not think of them as "yours." If no: keep your calculation and stop this process for that year. If yes: go to Question 2.

- Did you report all worldwide income tied to those accounts on your U.S. return?

This is a reporting test first. Review what was actually filed for wages, tips, and other income. Do not assume that "I paid something" means reporting was complete. If yes: go to Question 3. If no: move to a path that includes amended returns, not a late-FBAR-only fix.

- Did you pay all U.S. tax due on that income?

Reporting and payment are separate checks. You can report income and still have unpaid tax because of an error or incomplete payment. Validate this with your return and payment records, and transcripts or account records if needed. If yes: go to Question 4. If no: use a path that addresses both return corrections and tax due.

- Was the failure non-willful, or do facts suggest deliberate concealment?

Be disciplined here. Non-willful means negligence, inadvertence, mistake, or good-faith misunderstanding. Willfulness points to intentional or deliberate concealment. Stick to facts about what you knew, what you gave your preparer, and when you learned FBAR might apply. If clearly non-willful: go to Question 5. If concealment risk exists: skip ahead to the red-line section and get legal advice before filing.

- Has the IRS already contacted you, or are you already under IRS civil exam or criminal investigation?

Timing affects eligibility. Delinquent FBAR and streamlined options have limits if the IRS has already contacted you or initiated certain actions. Silence is not a safety signal. Late FBAR filings are not automatically audited, but they can still be selected for audit. If no contact, no exam, and no investigation: voluntary resolution paths may still be available in Phase 2. If yes: your options narrow, and Phase 2's standard routes may not apply.

If every answer is yes, you are in the simplest bucket: FBAR required, all income reported, all tax paid, non-willful, and no IRS contact. If any link in that chain breaks, you likely need a different correction path, not a late FBAR alone.

You might also find this useful: What is 'Willful Blindness' in the Context of FBAR Penalties?.

Phase 2: Strategic Path Selection - Mapping Your Diagnosis to the Right IRS Program#

Once you know your fact pattern, the program choice usually becomes clearer. Pick the official IRS path that matches your Phase 1 answers, and do not improvise with ad hoc late filings.

If your income reporting, tax payment, and IRS-contact checks are clean, DFSP may fit. If not, verify whether another official route, such as Streamlined Filing Compliance Procedures or IRS Criminal Investigation Voluntary Disclosure Practice, fits your facts.

Choose the route that fits your facts#

| IRS path | Choose this if your Phase 1 answers say... | What you will need to file | Penalty posture | Stop and do not proceed alone if... |

|---|---|---|---|---|

| Delinquent FBAR Submission Procedures (DFSP) | You had an FBAR obligation, and you already reported related foreign-account income on your U.S. returns and paid all related tax. You are not under IRS civil examination or criminal investigation, and the IRS has not already contacted you about the delinquent FBARs. | File delinquent FBARs electronically through FinCEN's BSA E-Filing System. On the electronic form cover page, select a reason for filing late and include a statement explaining why you are filing late. | IRS relief language is conditional on proper income reporting, tax payment, and prior-contact conditions. Verify current penalty treatment before filing. | You find unreported income, unpaid tax, prior IRS contact about delinquent FBARs, or prior contact regarding an income tax examination. |

| Streamlined Filing Compliance Procedures | DFSP may not fit, and you may need to address delinquent or amended returns for additional tax. | Verify current IRS streamlined requirements and submission scope before filing. | Verify current penalty treatment. | Your eligibility facts are unclear or any IRS contact has already happened. |

| IRS Criminal Investigation Voluntary Disclosure Practice | DFSP may not fit, and this appears to be the relevant IRS offshore compliance route for your facts. | Verify the current filing scope and submission steps before filing. | Verify current penalty treatment. | Treat this as a counsel-first lane before any submission. |

DFSP is narrower than it sounds#

DFSP is not just "I filed late." It is for taxpayers who do not need Streamlined Filing Compliance Procedures or IRS Criminal Investigation Voluntary Disclosure Practice to fix delinquent or amended returns for additional tax.

Use this checkpoint before you choose DFSP: you are correcting the FBAR filing itself, not unresolved income-tax return issues. If you identify unreported account-related income or unpaid related tax, stop and re-check whether DFSP is still the right path.

Streamlined routes address more than the FBAR form#

If Phase 1 showed missing income reporting, unpaid tax, or both, your issue is broader than FinCEN Form 114. In that case, verify current streamlined eligibility first, then build the filing package to match the official route. Do not self-classify by intuition. Verify the eligibility rules first, then file through the official channel that fits.

Do not use quiet disclosure#

If your facts point to Streamlined Filing Compliance Procedures or IRS Criminal Investigation Voluntary Disclosure Practice, do not send late FBARs or amended returns outside the official route for your situation. Late FBARs are not automatically audited, but they may be selected for audit through existing audit selection processes.

Use the formal program that matches your facts and keep your documentation coherent. That gives you a clear, defensible filing narrative instead of a patchwork record. If you want more background on the streamlined route, see A Guide to the IRS Streamlined Filing Compliance Procedures. Before you lock in a filing path, run the FBAR calculator to organize account balances and catch documentation gaps.

Phase 3: The Flawless Execution Action Plan#

Execution matters because inconsistencies create avoidable problems. Build one consistent record so account scope, balances, explanations, and forms line up year by year before you submit anything.

1) Build the account file before you touch forms#

Before you touch the forms, build an inventory for each year in the applicable review period. Include potentially reportable foreign financial accounts such as traditional bank and brokerage accounts, joint accounts, signature-authority accounts, and multi-currency fintech wallets that may require review. Include foreign-entity accounts that need review based on your financial interest or authority. Do not assume every wallet, app balance, or entity account is automatically reportable.

| Deliverable | What to include |

|---|---|

| Year-by-year account list | Institution, account number, country, owner, and your connection, whether direct, joint, or signature authority |

| Statements or transaction records | Support each year's highest balance |

| Filed U.S. returns and Forms 8938 | Copies of filed U.S. returns and any Forms 8938 |

| Income and tax support | Support that related foreign income was reported and tax paid if you are using DFSP |

| Status memo | Whether there has been any IRS contact, civil exam, or criminal investigation |

As you build the file, keep these control points in mind:

- For reportable joint accounts, each holder generally reports the full account value unless an exception applies.

- If you plan to use a spousal single-filer position, confirm Form 114a conditions before you rely on one filing.

2) Normalize balances in one workbook#

Do this in one spreadsheet, not across scattered notes and downloaded PDFs. Use one row per account per year: highest balance in native currency, USD conversion, and a link to the supporting record. Apply one conversion approach consistently using the currently instructed conversion source.

Keep this rule in view: if you had financial interest in, or signature or other authority over, at least one foreign financial account and aggregate value exceeded $10,000 at any point in the year, that year requires FBAR review.

Catch these common QA failures now:

- Using balances that do not reflect the highest value reached during the year

- Mixing conversion methods across accounts or years

3) Draft the late-filing explanation with a fixed structure#

If you are using DFSP, the electronic filing requires you to select a late-filing reason on the cover page. It also requires a statement explaining why you are filing late. Keep this brief, factual, and consistent with your records.

A practical structure is:

- Facts: which years and accounts were missed

- Cause: negligence, inadvertence, or mistake

- Corrective controls: what you changed to prevent recurrence

- Consistency with prior filings: how income reporting and tax payment align with filed returns

This is a practical structure, not an IRS-mandated format.

4) Run pre-submission controls before filing#

Before you file, make sure the package tells one story across all years and forms. If you are in a streamlined lane, confirm the current covered periods and required components before submission. For SDOP, verify the covered period is the most recent 3 years for tax returns and most recent 6 years for FBARs where due dates have passed.

| Control | What to confirm |

|---|---|

| FBAR filing method | FBARs are filed electronically through FinCEN's BSA E-Filing System |

| Tax return attachment | FBARs are not attached to federal tax returns |

| Form 8938 consistency | Form 8938 and FBAR positions are consistent, and Form 8938 is not treated as a replacement for FinCEN Form 114 |

| Data alignment | Account numbers, ownership labels, balances, and country coding align across forms and years |

| Joint-account support | Joint-account treatment and any Form 114a position are supported |

| Explanation support | Your explanation matches what returns and statements show |

If any of these points do not line up, fix the record before you file.

Escalate before filing if you find unreported income, prior IRS contact, possible willful facts, or unclear entity or signature-authority classification. After filing, keep forms, confirmations, statements, workbook, and explanation records for 5 years from the FBAR due date.

Red Line Scenarios: When to Immediately Consult a Tax Attorney#

Some facts take this out of the self-filing category. If your situation is unclear or potentially sensitive, stop and talk to a tax attorney before you submit anything.

Use this red-line test:

- Potential willfulness: You cannot clearly support a non-willful explanation (negligence, inadvertence, or a good-faith misunderstanding), or you are considering signing a non-willfulness certification, including Form 14654, with facts that may be challenged.

- Program-selection risk: Your issue is not just late FBARs, and choosing among Delinquent FBAR, Streamlined, or Voluntary Disclosure is not a simple filing choice.

- Unclear reportability facts: Your ownership or account-authority facts are unclear enough that year-by-year FBAR reportability is uncertain.

Stop and escalate now#

- Pause filings. Do not submit late FBARs just to get something on file.

- Build a filing timeline before forms: account openings, control or authority changes, income reporting, and when you learned of the FBAR duty.

- Gather records before drafting anything: statements, account-opening documents, prior returns, and related communications.

- Contact a U.S. tax attorney who handles offshore compliance and share that timeline first.

Once the facts and remediation path are settled, a preparer can help execute the filing steps. If legal strategy or willfulness risk is unclear, a tax attorney should be the first call.

For a step-by-step walkthrough, see The Difference Between 'Willful' and 'Non-Willful' FBAR Penalties.

Conclusion: From Anxiety to Agency#

You can close this cleanly by following the same sequence each time: diagnose the facts, choose the correct filing path, and execute with documentation. In practice, that means confirming there is no existing IRS civil or criminal action and no prior IRS contact about delinquent FBARs. It also means confirming related income was properly reported and taxed, filing through FinCEN's BSA E-Filing System, including your late-filing explanation, and selecting the appropriate late-filing reason on the electronic form. Keep the full record set because penalty relief is conditional, and late FBARs can still be selected for audit.

For ongoing compliance, make the annual review mechanical. Pull account records, value each foreign account separately, then aggregate those values and test whether the total exceeded $10,000 at any point in the year. If you have fewer than 25 accounts and cannot determine whether aggregate maximum values exceeded the threshold, use item 15a ("amount unknown") and still complete the account-level information.

Use this next-cycle checklist:

- Record a reasonable approximation of each foreign account's greatest value during the year, separately for each account.

- Aggregate those maximum values and test the $10,000 filing threshold.

- Store your valuation workpapers, prior FBAR copies, explanation statements for any late filings, and BSA E-Filing confirmations in one folder.

- Once the filing deadline for the year is confirmed, add it to your calendar and set advance reminders.

- If you use a tax professional, send an annual briefing before return prep: new accounts, closed accounts, and related foreign-income reporting items.

- If you file late, keep your explanation statement and BSA E-Filing confirmation with the same records.

Self-manage when the facts are clean, income reporting is complete, records are strong, and the filing path is clear. Escalate to a qualified tax attorney or specialist when willfulness is a concern, IRS contact already exists, records are thin, account facts are complex, or the right path is still uncertain.

We covered this in detail in How to Document 'Reasonable Cause' for IRS Penalty Abatement. If you need operational support, use Contact Gruv to confirm whether this workflow is supported for your program.

Frequently Asked Questions

How should you think about willful vs non-willful?

Treat this as a facts-and-evidence test, not a label. Streamlined eligibility requires non-willful conduct, while willfulness refers to intentional conduct rather than a simple mistake. If your facts suggest intentional conduct, pause and get legal advice before filing.

Which disclosure path usually fits your facts?

Start by asking whether all foreign income was properly reported and taxed and whether the IRS has already contacted you. DFSP may fit if income reporting was complete and you are not under IRS civil exam or criminal investigation. If returns need correction and you can support non-willfulness, streamlined may fit. If willfulness is a live issue, discuss VDP first.

What makes a reasonable-cause or non-willful explanation credible?

A credible explanation is specific, dated, and supported by records. Build a timeline using statements, account-opening records, prior returns, adviser communications, and evidence of when you learned of the filing obligation. If you are certifying non-willfulness, give specific reasons for what was missed and avoid generic statements that are not backed by documents.

How do you calculate the SDOP 5 percent penalty?

Use a documented checklist and verify current instructions before filing. Confirm the covered filing periods, identify the foreign financial assets included in the penalty base, compute the highest aggregate balance or value across that period, and use the required currency-conversion method. Then apply the 5 percent rate to that highest aggregate balance or value base and keep the supporting workpapers.

Does filing late FBARs trigger an audit?

Not automatically, but audit risk still exists. DFSP filings may be selected through normal audit processes, and streamlined submissions can also be examined with additional penalties if warranted. A complete, consistent filing package is better protection than a bare late filing.

What should you avoid if you want to fix this cleanly?

Avoid treating a late FBAR by itself as a complete fix if you also have unreported income or missing information returns. Do not use DFSP or streamlined if you are already under IRS civil exam or criminal investigation, and do not treat quiet disclosure as equivalent to formal program entry. If prior penalty assessments already exist, plan for those to still be payable.

When should you escalate to a qualified tax attorney or specialist?

Escalate when the facts are hard to explain cleanly or the program choice is uncertain. Common triggers include possible intentional conduct, incomplete income reporting, complex ownership or signature authority, uncertain SFOP residency status, or a weak documentation trail. If VDP may be in play, involve counsel early and choose the filing path with professional tax or legal guidance.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Portugal NHR vs Spain Beckham Law for High-Earning US Expats in 2026

Start with documentation, not tax projections. In the portugal nhr vs spain beckham law decision, the safer first move is to choose the path you can prove from end to end before you optimize for headline outcomes.

IRS Streamlined Filing Decisions for Freelancers With Foreign Accounts

Make one decision before you touch forms: either your facts map cleanly to the primary IRS text, or you pause and clarify them first. That single choice prevents avoidable filing mistakes.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.