Quick Answer

Document it by building a dated, verifiable case file that shows ordinary business care and prudence. Start with the IRS notice, confirm the penalty, period, and response path, then create a fact-only timeline, collect matching proof, record mitigation attempts, and organize everything in one indexed folder. Your request should tie each key statement to a supporting exhibit and follow the notice instructions or Form 843 route if needed.

An IRS penalty notice is not a verdict. It is a business problem you can manage with the right systems.#

Step 1: Build Your 'Anti-Penalty' System#

Your reasonable-cause case starts before anything goes wrong. The goal here is routine proof that you exercised ordinary business care and prudence, not trying to write a better story after a miss. Reasonable cause is reviewed case by case, and you carry the burden to substantiate it.

For a solo consultant or small firm, four practical controls can carry most of the load: payment readiness, contemporaneous records, notice-response discipline, and clear responsibility. Each one should reduce failure risk, create dated evidence, and show who did what.

1. Separate filing readiness from payment readiness#

Treat filing and payment as two separate jobs. An extension to file is not an extension to pay, so payment risk still sits on the original due date.

Set up one primary payment method and one tested backup funding path. If you use EFTPS, you can schedule federal tax payments up to 365 days in advance. A conservative pre-scheduled payment helps show you were preparing to comply.

This control can reduce last-minute failures, including system issues that delay timely electronic filing or payment. It also matters when cash is tight, because lack of funds alone is not reasonable cause. Once a quarter, confirm you can log in, view scheduled payments, and retrieve confirmation details quickly.

2. Make recordkeeping automatic and time-stamped#

A workable recordkeeping system is better than an elaborate one you do not use. Use any system that clearly shows income and expenses. Electronic records are fine, but they must meet the same standards as paper records.

Create one tax archive that captures returns, payment confirmations, IRS notices, invoices, receipts, contracts, information returns, and advisor communications. Keep capture simple and consistent. For example, auto-route tax payment confirmations into a Tax Payments folder and save the PDF or screenshot the same day.

This gives you documentary support if you need to substantiate a reasonable-cause request. If you have payroll, keep employment tax records for at least 4 years.

Checkpoint: if you cannot pull last quarter's payment confirmation, extension confirmation, and latest IRS notice quickly, tighten the system.

3. Build a notice-response habit, not a mailbox gamble#

Penalties can get worse when notices are missed or answered late. The fix is routine, not heroics. Treat every IRS letter the day it arrives: capture it, log it, and assign the response date.

Keep copies of all IRS correspondence. If a notice asks for a response, act by the due date. If you dispute it, include your information and copies of supporting documents.

Use one intake lane, such as one email label plus one mail-scan folder. Each notice should produce the same basic record: the notice copy, received date, requested action, response copy, and supporting documents sent. If you later receive a rejection, calendar the deadline immediately because you generally have 30 days to request an appeal.

4. Write down who owns filing, payment, and follow-up#

Shared responsibility is where many preventable misses begin. If someone else helps with tax work, define roles before deadlines. For businesses, responsibility is tied to the person authorized to submit the return, make the deposit, or pay the tax.

Do not rely on "my preparer handles it" as your default defense. You remain generally responsible for compliance. What helps more is a clear trail: written instructions, approval, filing submission and acceptance, and payment confirmation.

| System control | Likely failure mode | Documentation artifact it should create |

|---|---|---|

| Payment readiness | Missed payment date, trapped funds, e-payment issue | EFTPS confirmation, scheduled payment record, bank transaction record, calendar entry |

| Automatic recordkeeping | Missing proof of filing, payment, income, or expenses | Time-stamped PDFs, synced folder history, saved receipts, return copies |

| Notice-response discipline | Missed IRS due date, incomplete dispute response | Notice log, scanned letters, response draft, copy of supporting documents sent |

| Role clarity | "I thought my preparer handled it" | Written responsibility note, advisor emails, approval trail, filing acceptance record |

Use this quick implementation checklist to put the system in place:

- Test your payment method now, and pre-schedule federal payments in EFTPS when relevant.

- Create one tax archive with folders for returns, payments, notices, and support.

- Add an email rule or scan routine so records are captured the same day.

- Start a notice log with received date, response date, and status.

- Write down who prepares, approves, submits, and confirms.

Guardrail: if you have major setup gaps, cross-border complexity, repeated control failures, or a penalty type that may not fit the reasonable-cause lane, get professional tax advice early.

Related: What is IRS Penalty Abatement and How to Request It.

Step 2: The CEO's Playbook for Building an Unassailable Case File#

Once your controls are in place, the next job is turning a missed deadline into a defensible record. The IRS reviews facts and circumstances case by case, so your file needs to show ordinary care and prudence with evidence a reviewer can verify quickly.

1. Verify the notice before you draft anything#

Start with the IRS notice, not memory. Confirm the points below before you draft.

| Notice item | What to verify | Practical note |

|---|---|---|

| Penalty type | The exact penalty at issue | Match your relief reason to the specific penalty at issue. |

| Tax year or period | The affected tax year or period | Answer from the notice itself which period is involved before writing your explanation. |

| Late, missing, or incorrect item | What the notice says was late, missing, or incorrect | Start with the IRS notice, not memory. |

| Response path | Whether the notice tells you to call first | Some requests may be handled by phone; if not, you may need to request relief in writing on Form 843. |

| Rejected e-file | The rejection notice and timing | A timely, processable e-file can still be treated as timely if you re-sent or mailed it within 10 days of the initial rejection notice. |

Use the notice instructions first. Some requests may be handled by phone. If not, you may need to request relief in writing on Form 843. Match your relief reason to the specific penalty at issue. If this involves a rejected e-file, preserve the rejection notice immediately. A timely, processable e-file can still be treated as timely if you re-sent or mailed it within 10 days of the initial rejection notice.

Checkpoint: before writing your explanation, answer from the notice itself what penalty is at issue, for which period, and which response path to use.

2. Build a fact-only event log (facts separate from assumptions)#

A solid event log does two things at once: it helps you think clearly, and it keeps later storytelling from drifting away from what you can prove. Open your log when you discover the problem. Your first entry should record when you learned of it, which obligation was affected, and what objective source confirmed the issue.

| Log element | What to record | Practical note |

|---|---|---|

| Opening entry | When you learned of it, which obligation was affected, and what objective source confirmed the issue | Open your log when you discover the problem. |

| Date and time | Exact date and time, plus time zone if relevant | If timing is uncertain, use timestamp bounds. |

| What happened | What happened | Keep facts and assumptions on separate lines. |

| How verified | How you verified it | Use the objective source that confirmed the issue. |

| Next step | What you did next | Each later entry should include what you did next. |

| Proof location | Where the proof is stored | Store it where Step 3 can cite it quickly. |

| Assumptions | Any assumption on a separate line | Say so plainly when timing is uncertain. |

At a minimum, each later entry should include:

- Exact date and time, plus time zone if relevant.

- What happened.

- How you verified it.

- What you did next.

- Where the proof is stored.

Keep facts and assumptions on separate lines. Fact: "Portal showed payment failure message." Assumption: "Bank likely blocked the transaction." If timing is uncertain, say so plainly and use timestamp bounds.

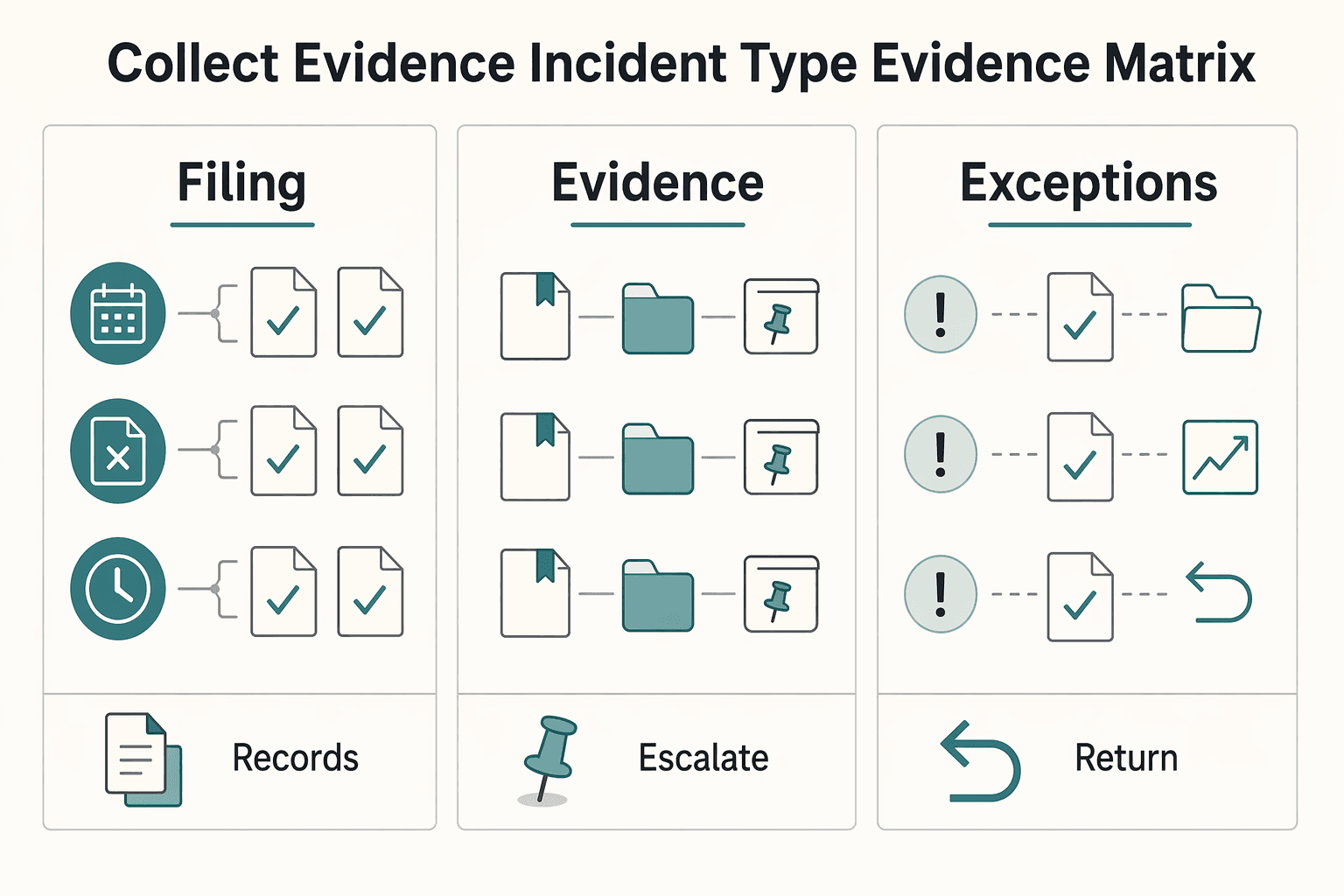

3. Collect evidence by incident type with an evidence matrix#

Do not collect records at random. Capture the proof that matches the incident, then store it where Step 3 can cite it quickly.

| Incident type | Proof to capture | Storage location | Why it matters |

|---|---|---|---|

| E-filing or e-payment system issue | Error screenshots, official outage/status notices, submission attempt confirmation | 03 System Notices, 04 Mitigation Attempts | Helps document that system issues may have delayed timely electronic filing or payment, along with your compliance attempts |

| Bank or processor restriction | Restriction notices, failed transaction messages, support emails, ticketed call notes, transaction history | 02 Third-Party Communications, 05 Transaction Proof | Documents an external barrier, not just a narrative |

| Rejected timely e-file | Rejection notice, original submission confirmation, proof of re-send or mailing within 10 days, acceptance/delivery proof | 01 Timeline, 05 Transaction Proof | Preserves a timeliness argument after rejection |

| Incorrect written IRS advice route | Copy of written IRS advice and your reliance explanation | 02 Third-Party Communications | Required for that separate statutory-exception path |

| Filing/payment channel details | Record the filing or payment route you actually used, plus any notice instructions you relied on | 00 Case Index | Reduces channel errors in your narrative |

Use exhibit filenames that map to your timeline entries so retrieval is immediate.

4. Document mitigation across primary and backup attempts#

What you did after the problem appeared can matter as much as the problem itself. Record attempts through your primary route and, when available, a verified backup route. For each attempt, capture the details below.

| Attempt detail | What to capture |

|---|---|

| Timing and channel | Date, time, and channel used |

| Contact reached | Who or what system you reached |

| Reference number | Ticket or confirmation number |

| Requested action | Action requested |

| Promised next step | Promised next step |

| Outcome | Outcome and failure reason, if any |

| Follow-up deadline | Follow-up deadline |

Avoid leaning on two arguments that are weak by themselves: reliance on a tax professional for filing or payment deadlines, and lack of funds alone. Your file should instead show documented attempts, barriers, and follow-through.

5. Consolidate one case folder with a clean index#

If your file is hard to work through, your explanation will feel weaker than it is. One practical incident-folder structure:

00 Case Index01 Timeline02 Third-Party Communications03 System Notices04 Mitigation Attempts05 Transaction Proof

In 00 Case Index, map each timeline entry to exhibits. That makes Step 3 faster whether you call, submit in writing, or escalate after a rejection letter. Final check: another person should be able to trace any timeline statement to supporting proof quickly.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025. Before you finalize your case file, centralize your timeline notes and cross-border movement records in the Tax Residency Tracker.

Step 3: Presenting Your Case to the IRS#

With the file built, your job is to make it easy for the reviewer to follow. Your request should read like a factual record of what happened, what you did, and why those facts support reasonable cause.

Verify readiness before you draft#

Start with the notice and your records, not memory. The IRS says to verify notice details and follow notice instructions first. Some requests may be handled by phone. If relief is not approved by phone, you may request it in writing with Form 843. Before you draft, confirm:

- notice number, penalty type, tax year or period, and amount

- whether the notice route is phone first or written request

- whether you are using reasonable cause or a separate lane, such as First Time Abate

- whether the penalty type is eligible for reasonable-cause analysis, since reasonable cause does not apply to certain penalties, including estimated tax penalty

- the filing and payment facts for the affected period that you can document

If you are evaluating First Time Abate, treat it as a separate administrative waiver path. Check the compliance-history requirements separately. That includes filing the same return type for the past 3 tax years and no penalties in the prior 3 years, unless removed for an acceptable reason other than FTA.

Checkpoint: You should be able to state, from documents in front of you, which penalty you are contesting and which relief path you are using. You should also be able to explain why your account facts fit that path.

Draft the request in a practical sequence#

Keep the structure simple enough that it works for a phone call, call notes, or a written submission. One practical sequence is:

- Issue statement: identify the penalty, period, notice number, and relief basis.

- Facts summary: give a short, objective summary of what happened.

- Timeline with exhibits: present events in date order and tie each material fact to supporting exhibits.

- Closing connection: state that you exercised ordinary business care and prudence but were still unable to file or pay on time, based on the documented facts.

If system issues delayed timely e-file or e-pay, say that directly and point to objective proof.

Replace weak language with verifiable language#

Use wording a reviewer can test quickly.

| Weak wording | Stronger wording | Why it works |

|---|---|---|

| "Everything fell apart and I could not handle it." | "My filing or payment attempt failed on a specific date, and I kept the system or bank message. I took follow-up steps and attached the related exhibits." | It gives verifiable facts, actions, and proof. |

| "My preparer caused this problem." | "I used a preparer for support, but this request is based on documented facts showing an external barrier or event. The supporting exhibits are attached." | Reliance on a tax professional alone generally does not qualify. |

| "I did not have enough money." | "Funds were unavailable because of a documented circumstance, and I kept proof of the payment attempt and timing. The supporting exhibit is attached." | Lack of funds by itself is generally not enough; cause and response must be documented. |

Attach the appendix and cross-reference it cleanly#

The body should stay readable. Put the supporting detail in an appendix with consistent exhibit labels, then cite those labels where the facts matter. Use one labeling method throughout, for example notice records, timeline proof, third-party communications, and transaction proof.

Simple rule: each material claim should point to support. For example, state when the electronic submission failed, when you retried, and which exhibits prove each step.

This structure also prepares you for Appeals if needed. If relief is denied, you generally have 30 days from the rejection letter date to request an appeal, and Appeals asks for detailed facts and circumstances.

You might also find this useful: The Difference Between 'Willful' and 'Non-Willful' FBAR Penalties.

Conclusion: From Penalty Anxiety to Proactive Control#

You cannot control the IRS decision, but you can control the record they review. The practical path is straightforward: choose the right relief lane, keep dated proof, and show what you did to fix the issue.

Start by separating the relief path before you draft anything. First-Time Abate is an administrative waiver, and reasonable cause is a facts-and-circumstances analysis. If you qualify for First-Time Abate, the IRS may apply it even if you requested reasonable-cause relief. Verify the basics first, including the same return type filed for the past 3 tax years and no penalties in the prior 3 years. If you proceed under reasonable cause, your file needs to show ordinary business care and prudence: you acted responsibly but still could not comply because circumstances were outside your control. Also remember that reasonable cause does not apply to every penalty type, including certain estimated tax penalties.

Use this closeout checklist every time:

- keep compliance records current instead of rebuilding them later

- preserve a time-ordered evidence trail for filing attempts, payment attempts, notices, errors, and third-party communications

- document corrective actions immediately, including when the issue was fixed and what changed to prevent repeat failures

- confirm each key statement in your request maps to a dated exhibit

Decide your escalation line early. You may represent yourself, and that can be practical when your facts are straightforward and your evidence is organized. Escalate to a CPA, EA, or attorney when facts are complex, international information reporting penalties are involved, or you receive a rejection. In that situation, you may need to prepare an appeal in the general 30-day window and provide detailed facts and circumstances. Some requests may be handled by phone. If phone resolution is not available, you may be routed to Form 843.

Run the same control loop each cycle: prepare, document, present, review. That repeatable loop gives you durable control, not just a one-time shot at relief.

For a step-by-step walkthrough, see How to Pay Estimated Taxes for an LLC. If you want to reduce future penalty-risk documentation scramble, discuss a compliance-first money workflow with Gruv here.

Frequently Asked Questions

What does reasonable cause for penalty abatement mean in plain English?

It means asking the IRS to remove a penalty based on documented facts and circumstances. This article presents practical guidance, not a complete rule statement. A stronger file lets a reviewer quickly verify what happened, when it happened, and what you did next from time-stamped records.

Which path should you evaluate first?

Evaluate First-Time Abatement separately if prior compliance history may matter, and verify current eligibility before choosing it. If you have a specific, documented event tied to the penalty period, a facts-based claim may be the better first path. If multiple periods or mixed issues are involved, review both routes before filing.

What is the minimum evidence package you should send or keep ready?

There is no IRS-required minimum evidence package in the excerpt. Keep the IRS notice, a dated event log or timeline, third-party proof, filing or payment attempt records, and your final request document ready. You are in better shape when every key statement in the request points to a matching record.

What usually weakens a case?

A case is usually weaker when the explanation is only "I forgot," "I was busy," or "my preparer handled it" without objective records. Repeated failures across periods can also make the issue harder to present as one documented event. Get professional advice if the pattern repeats, overlaps with foreign filings, or the issues are hard to separate.

What should you watch for after you submit?

Keep tracking every IRS response in the same case file after you submit. Watch for signature, no-consideration, disallowance, appeals, and Letter 105C or 106C issues referenced in the claims procedures discussed in the article. Get professional advice if the response does not match what you requested or you do not understand the letter you received.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

What is IRS Penalty Abatement and How to Request It

If you run a business of one, you want to reduce a tax penalty without creating a second problem. That second problem usually shows up when claims are weak, penalty types get mixed, or the submission path is wrong. This guide gives you safe defaults within the Internal Revenue Service framework so you can move in order instead of improvising.

The Difference Between 'Willful' and 'Non-Willful' FBAR Penalties

For modern global professionals, FinCEN Form 114, or the FBAR, creates a familiar kind of stress. You use platforms like Wise, Deel, and Revolut because they make your work easier and your finances more flexible. That flexibility is useful, but it also creates compliance complexity and, with it, the risk of a serious mistake. The line between an honest error and a willful violation can feel uncomfortably thin, and the penalties are not something to take lightly.