Quick Answer

Start by sorting failures into decline, expired card, insufficient funds, and payment or gateway error, then assign a different next action to each. Use capped retries, a clear payment-update path, and a written switch to escalation when the reminder window closes. For a 20-day campaign, measure on day 21 instead of mid-campaign, and review recovery with involuntary churn before expanding automation.

Why Failed Payment Recovery Needs Structure#

Failed payments create two problems at once: cash flow pressure and a retention decision. In subscription businesses, the same recovery step can either bring revenue back or push a customer closer to canceling.

Dunning is the process of asking customers to pay what they owe after a payment fails, including cases like declined cards, insufficient funds, or payment errors. In practice, it is a staged flow with early reminders, follow-ups, and then a final notice before escalation when needed. The goal is to protect cash flow without damaging the customer relationship, because heavy-handed outreach can feel invasive or intimidating.

This guide walks through seven strategies and shows how to implement them in a way teams can actually run. Use the ranking as decision support, not as a universal playbook. Timing, tone, and escalation norms vary by segment, market, and program.

For subscription and SaaS billing, success is broader than collecting one overdue invoice. You are trying to recover revenue while protecting customer relationships and keeping AR operations steady.

Before you change reminders or escalation language, confirm why payments are failing. Declined cards, insufficient funds, and payment errors are different triggers, and teams often handle them differently through the dunning process. For a deeper definition, see A Guide to Dunning Management for Failed Payments.

What dunning management is actually responsible for#

Dunning management owns the operating choices after a payment fails: how you use customer communication, retry logic, and escalation policy to recover revenue without damaging retention.

| Failure cause | Guidance |

|---|---|

| Credit card decline | Use available failure details before retrying blindly |

| Insufficient funds | Retries can work, but timing design matters more than retry volume |

| Payment method needs update | Prioritize a clear update-payment action |

| Payment or gateway error | Confirm the failure status before continuing reminders |

The work starts when a charge fails, including declines, insufficient funds, and payment or gateway errors. From there, you have two main levers: retry the current payment method, or ask the customer to provide a new one. Which path makes sense depends on the failure cause. Some cases respond to retry timing. Others require customer action. Keep the causes separate before you choose tactics:

- Credit card decline: use available failure details before retrying blindly.

- Insufficient funds: retries can work, but timing design matters more than retry volume.

- Payment method needs update: prioritize a clear update-payment action.

- Payment or gateway error: confirm the failure status before continuing reminders.

If failure-reason data is unclear, start with neutral customer-action messaging, typically by email, asking the customer to review or update payment details. Escalate channels only when needed. Dunning is an escalating reminder process, but it still has to protect the customer relationship and avoid aggressive patterns that create legal and experience risk.

Do not treat dunning performance as "more retries = better results." Measure recovery with a defined window and checkpoint. If you run a 20-day recovery campaign, evaluate performance after the window closes on day 21.

We covered this in detail in What Is Dunning? A Platform Operator's Guide to Recovering Failed Recurring Payments.

How to rank the 7 dunning strategies before you implement anything#

Before rollout, rank your options on two axes: expected recovery impact and involuntary churn risk. Start with lower-pressure moves, then add pressure only where earlier stages fail.

Use the table as a working model, not a fixed sequence. Dunning workflows can follow rules and still be customized. Final priority should follow your business model and actual failure-signal data.

| Strategy | Trigger | Customer message intent | Retry/escalation rule | KPI | Main risk/caveat |

|---|---|---|---|---|---|

| CTA optimization | Failures where customer action is likely required | Make the next step clear (update details, review billing, contact support) | Keep pressure low until the action path is easy to complete | Action completion rate; recovered invoices after notice | Reminder volume alone will not fix a confusing action path |

| Smart retries | Failures that may recover without immediate manual intervention | Set expectations and reduce confusion | Use clear retry rules; shift to customer-action prompts when needed | Retry recovery rate; time to recovery | Repeating retries on the wrong cases can add friction with little gain |

| Reminder sequencing | First notice through final notice | Progress from informative to urgent in clear stages | Escalate gradually by stage instead of jumping straight to high pressure | Recovery by notice stage; action rate per notice | High-pressure sequencing can put stress on customer relationships |

| Segmentation | Meaningful differences across customer cohorts | Match tone, urgency, and path by cohort | Use cohort-specific notice and escalation paths | Recovery and churn by segment | One-size-fits-all tactics can miss business-model differences |

| Grace-period policy | Failed payments where short continuity is a retention lever | Prompt action while preserving near-term continuity | Apply a defined grace window before tougher enforcement | Recovery during grace period; retention after recovery | Weak boundaries can delay collections and affect cash flow |

| Channel escalation | Repeated non-response after standard notices | Increase visibility when initial notices stall | Escalate only after earlier stages fail | Response after escalation; complaint rate | Overly aggressive escalation can put stress on customer relationships |

| Automation depth in dunning management software | Growing invoice volume or inconsistent manual handling | Keep execution consistent and documented | Automate standard paths; keep exceptions reviewable | DSO trend; manual touch volume; process completeness | Automation scales bad rules if policy quality is weak; notice content may need specific details when notices function as legal documents |

How to turn this into a real priority order#

One possible starting hypothesis is to fix the customer action path first, then improve timing and escalation:

- CTA optimization

- Smart retries

- Reminder sequencing

- Segmentation

- Grace-period policy

- Channel escalation

- Automation depth (after core rules are stable)

Treat this as a starting hypothesis, not a validated benchmark ranking.

Issue-led checks before rollout#

Use your own failure-signal data to adjust the order. If the biggest bottleneck is customer action, for example updating payment details, prioritize action-path clarity first. If accounts keep staying unresolved over time, prioritize timing, sequencing, and escalation controls first.

Before launch, review notice templates and exception handling. If a notice in your process functions as a legal document, make sure required details are present, including fees and goods or services rendered, before you scale automation.

If you want a deeper dive, read Smart Dunning Strategies: How to Sequence Retry Logic for Maximum Recovery.

Build retry logic by failure type instead of one generic sequence#

A single retry schedule is easy to run, but it is often the wrong operating choice. A fixed 3/7/14-day pattern applies one schedule to very different failure causes, and those causes can need different next actions.

Retry timing is a tradeoff. Too aggressive and you can frustrate customers; too slow and you can lose momentum. In subscription billing, retry rules are not just collections mechanics. They directly affect involuntary churn.

Start with a failure matrix, not one schedule#

Key retry logic to the failure categories your system can reliably detect. At minimum, separate credit card decline, expired card, and insufficient funds.

| Failure category | What it usually signals | Retry posture | Customer action posture | Stop condition |

|---|---|---|---|---|

| Credit card decline / bank-flagged charge | Issuer or network rejection, cause may be unclear | Limited retries while reviewing available signals | Neutral guidance if action is unclear | End retries at your policy cap, then escalate |

| Expired card | Stored method is no longer valid | Don't rely on repeated blind retries | Move quickly to payment-method update with a clear CTA | End retry-led handling early if no update |

| Insufficient funds | Temporary funding constraint | Retry can help, but timing matters | Explain update or pay options clearly | End retries at policy limit, then escalate |

In practice, "failed payment" is too broad for one treatment. Expired cards, bank-flagged charges, and insufficient funds should not follow the same sequence.

Set rules that match likely cause#

Two rules deserve to be explicit from the start. For expired cards, shift quickly to an update flow. More attempts on an outdated method may add delay without resolving the issue. The CTA should make the next step obvious.

For broader decline cases, treat the first failure as ambiguous unless you have better signals. If available, use decline-code and behavior signals to tune timing. If not, add a simple review checkpoint before repeating attempts.

Coordinate handoffs across the payment-failure lifecycle. Charge attempts, reminders, and account state should stay aligned so tactics do not conflict. Once payment succeeds, retries and reminders should stop for that payment path.

Add stop conditions before scaling automation. Retries should end by policy, not drift. Define per-category caps, then define the next step: escalation messaging, channel change, service-access decision, or manual review.

The failure mode to avoid is silent repetition. Better recovery comes from matching retry behavior to failure type, making the customer ask clear, and coordinating handoffs across the payment-failure lifecycle. If you change one thing first, map each failure type to a distinct next action before you tune timing.

Design reminder cadence and messaging that customers will actually act on#

Once retry rules are set, reminder design becomes the next lever. Recovery can improve when reminders follow a staged cadence with a clear purpose at each step, instead of repeating the same generic notice.

Match the copy goal to the stage#

Use a simple progression across your dunning window, for example:

| Stage | Goal | Detail |

|---|---|---|

| Inform | Friendly notice | Payment did not go through |

| Nudge | Short follow-up | Focus on the next action |

| Urgency | Clear reminder | Practical risk if unresolved, including possible service interruption |

| Final notice | Last reminder | Before your next policy step |

Run this cadence across the channels you already use, such as email, SMS, and in-app notifications, so customers can act from where they are.

Keep the tone human. Persistence works better when it stays empathetic. Cold or robotic reminders can feel accusatory, while personalized language tied to the customer's situation is more likely to earn a response.

Set escalation policy and service-access rules before the first failure hits#

Define escalation before the first failed payment lands, not during incident pressure. Once retries and reminders stop working, the team needs a written rule for when an account stays in automated recovery and when it moves to action-required escalation.

A strong policy is short and operational. It should define when retries continue and when you escalate from email to other channels such as SMS, in-app, or portal notifications where supported and enabled. It should also define when the grace period starts and ends, and when suspension becomes the last-resort access action.

Put the switch point in writing#

Use a clear if/then handoff: if retries fail and no billing update happens by your defined reminder window, move from retry-led recovery to action-required escalation.

At minimum, document:

- the trigger that moves an account from retries to escalation

- the channels allowed at each stage

- the grace period before any access change

- the access action at each escalation stage

- the reactivation path, including whether updating payment details can restore access in your billing setup

Also test these state changes end to end. If your process assumes self-reactivation after payment update, confirm your billing system actually supports it.

Match pressure to account value and churn risk#

Too much pressure, too early, can damage goodwill and future business. Too little pressure can reduce recovery odds and raise collection cost. In overdue-invoice data, recovery has been reported at 90%+ before 30 days overdue and below 15% after 180 days, which suggests long, open-ended delays can hurt recovery odds.

You can segment the policy by account context. One segment may stay on an automation-first path with clear update-payment prompts and a defined grace window, while another may trigger earlier human outreach before a full suspension.

Treat suspension as a last resort after the grace period. Where supported, keep a clear path for customers to reactivate by updating payment details.

Check channel and program constraints before launch#

Channel escalation only works when channels are actually supported and enabled. If market or program constraints affect communication channels or automated account actions, include those caveats directly in the policy.

Before rollout, verify:

- which channels are enabled by cohort

- whether suspension and reactivation behavior works in your billing stack

- who approves exceptions when access changes create outsized customer risk

Assign ownership so product, finance, and ops do not work at cross-purposes#

Clear ownership matters. If no one owns the decision, product, finance, and ops can optimize in different directions, and the policy can drift into case-by-case judgment.

One possible internal split is:

- Product may own flow design and customer-facing choices, including timing, messaging path, update-payment UX, and escalation flow design.

- Finance may sign off when a change affects reporting treatment, RevRec assumptions, or cancellation timing.

- Ops may own exception handling inside the published escalation policy.

Treat that as an operating model, not a universal rule. Document it as your internal standard.

Fix the handoff between AR and messaging#

Execution conflicts can happen when accounts receivable pressure and customer messaging timing are managed separately. If that risk exists in your process, define one shared handoff rule before manual outreach or overrides so customers do not get mixed signals.

Before an override or manual action, confirm in one shared record:

- current failure reason and retry state

- last message sent and next scheduled message

- current access and grace-period state

- open support context or account notes

- whether Finance approval is needed when accounting treatment is affected

Review exceptions as policy signals#

Consider a recurring cross-functional review of top failure reasons, retry outcomes, and escalation exceptions. Use it to check whether outcomes still reflect the intended balance of recovery, retention, and brand trust, and whether exceptions are quietly becoming the real policy.

Also challenge inherited defaults. If you still run a fixed 14-day dunning period, treat it as a choice to re-justify, not a permanent baseline. Keep metric integrity explicit. Honest metrics beat inflated promises.

Document override authority and required evidence in writing. Log each override with reason, approver, temporary rule change, and expiry date so decisions remain auditable.

Instrument KPIs that show quality, not just collections pressure#

A good scorecard should tell you whether recovery is getting healthier or just harsher. Recovered cash alone can hide process drift if risk visibility and process controls are moving the wrong way.

Use a balanced KPI set:

- Track recovery outcomes, then pair them with

CEIand root-cause analysis so you can tell whether results come from a healthier process or short-term pressure. - Review prioritization logic regularly. Age- or value-only queues can leave current high-risk receivables unworked until they roll into past-due buckets.

- Monitor whether reminders are running on the intended rules and intervals, since consistent, timed communication is a core control in a structured dunning process.

- Run a monthly checkpoint. If collections improve while portfolio risk worsens, rebalance cadence and escalation before the drift compounds.

Connect your dunning system to billing infrastructure without creating new risk#

Integration is where sound policy often breaks. Your billing engine, dunning workflow, CRM, and finance reporting should stay aligned from failure to outcome.

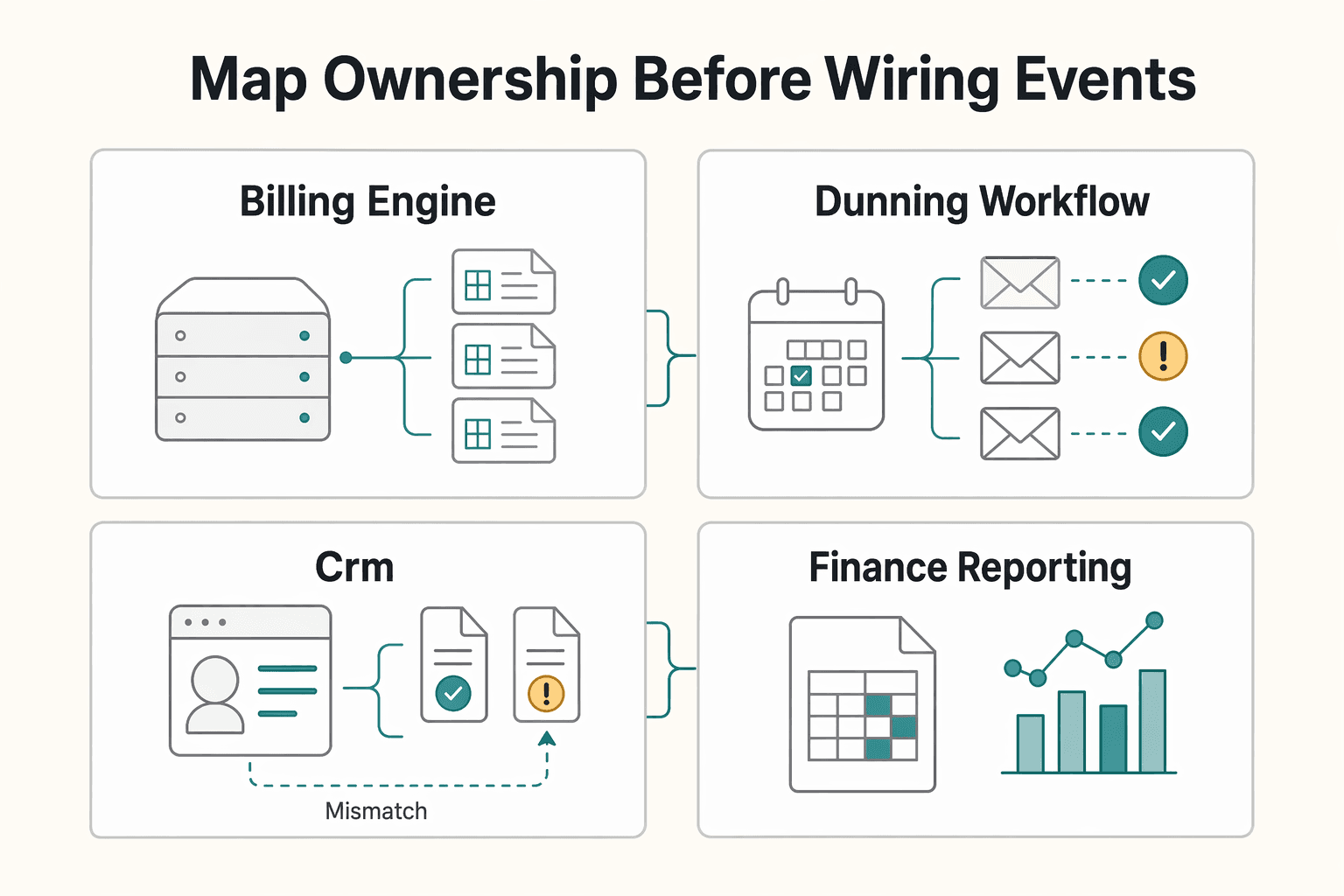

Map ownership before wiring events#

Use clear system roles so retries and messaging stay coordinated:

| System | Primary job |

|---|---|

| Billing engine (for example, Stripe Billing) | Track payment and invoice status |

| Dunning workflow | Orchestrate retry timing and customer messaging after failure |

| CRM | Reflect customer-facing communication and account context |

| Finance reporting | Show recovery and non-recovery outcomes |

If you run multiple billing models, for example recurring, usage-based, or sales-negotiated contracts, avoid one default flow for all of them. A failed payment can require different retry and message handling by model.

Define one visible event flow. A practical flow is:

- Payment failure event is received.

- Retry decision is made.

- Customer message is triggered with a secure path to update billing details.

- Customer billing update is recorded, if provided.

- Payment settlement, or non-recovery, is recorded.

This keeps the two core dunning components working together: payment retries and customer messaging.

Keep reliability and risk in view. Automated retries can help collect failed payments, but retry pressure can also create risk. In particular, retrying every 24 hours can backfire. Schedules such as 3, 7, and 14 days after failure are a common alternative pattern.

Keep operational tracking tight so teams can trace recovery and non-recovery outcomes across systems.

The failure modes that quietly destroy recovery performance#

Most recovery breakdowns are not mysterious. They come from generic decisions: vague messaging, one-size-fits-all retries, weak segmentation, and unclear escalation rules. The fix is to make each failed-payment path explicit by decline reason and customer segment.

Weak prompts waste the reminder cadence#

Frequent reminders can underperform if the message does not ask for one clear next step. Generic copy like "payment issue detected" can delay action when the customer needs a specific prompt, such as updating card details or contacting support. Keep each message focused on one action, and make sure the CTA lands on the correct billing-update path with minimal friction.

Poorly timed or overly aggressive outreach can also reduce recovery by pushing customers away. That risk can appear even when the underlying issue is straightforward, like an expired card, if the tone feels like collections.

Static retries create noise, not recovery#

Different decline reasons should not run through one static retry sequence. Expired cards, insufficient funds, and other failure types behave differently, so repeated retries on persistent failures can add noise without improving recovery. If the same reason keeps failing, time alone is not a strategy.

Define controls before optimization: retry limits, grace periods, and escalation rules. Then track recovery patterns by failure reason and adjust when retry volume is high but recovery stays low.

No segmentation means no policy#

Treating every failed-payment account the same hides where churn risk is highest. Segment communication by customer value, history, and failure reason, and move selected high-value cases to human outreach sooner. For API businesses, this matters because customers may not notice billing-related access degradation until production is affected.

Policy failures are often clarity failures. Set written rules for who gets a grace period, when service changes, and when automation escalates to a person. That way teams apply one consistent policy instead of making ad hoc decisions.

For a step-by-step walkthrough, see The $1 Billion Revenue Recovery Opportunity in Subscription Dunning.

30-day rollout checklist for a production-ready dunning campaign#

Use this 30-day plan as an execution rhythm, not as a promise. If gateway initiation is not already underway, start there first since it can take up to 45 days and delay everything else.

| Week | Focus | Key checks |

|---|---|---|

| Week 1 | Lock a baseline and classify failed payments | Validate from your own logs and support history; keep baseline records outside sandbox data; create a sandbox site and enable development mode if required by your vendor |

| Week 2 | Turn strategy into documented rules | Complete a sandbox signup and confirm the account and subscription were created correctly; test upgrades, downgrades, cancellations, and refunds; publish the policy in final form |

| Week 3 | Put the customer-facing flow under pressure | Treat reminder cadence or message variants as internal experiments; check the full CTA path end to end; train customer service before broader rollout |

| Week 4 | Review outcomes against the Week 1 baseline | Inspect exception logs; prioritize by failure type and customer segment using your own data; document every rule change; narrow or revert rules that are not working for a cohort |

This section is about sequencing the work, not pretending every team moves on the same calendar. The right pace will vary by your size, budget, and business needs.

Week 1#

Start by locking a baseline you can compare against later, then classify failed payments into a taxonomy your team can actually use. Do not assume the top drivers in advance. There is no universal ranking of failure drivers, so validate from your own logs and support history before you rank priorities.

If you are rolling out on a new billing stack, keep baseline records outside sandbox data. Sandbox customer accounts, transactions, and invoices are wiped when you go live. Complete environment setup this week: create a sandbox site and, if required by your vendor, enable development mode before deeper testing.

Week 2#

This is the week to turn strategy into documented rules for your team. If you define retry branches or escalation paths, treat them as internal policy decisions rather than vendor-validated defaults.

Validate full subscription behavior, not just first-charge flow. Complete a sandbox signup, confirm the account and subscription were created correctly, then test upgrades, downgrades, cancellations, and refunds. Publish the policy in final form so support, finance, and product make consistent decisions on the same case.

Week 3#

Now put the customer-facing flow under pressure. If you run reminder cadence or message variants, treat them as internal experiments, not validated best practices.

Check the full CTA path end to end. If the message asks for a payment update, the link and post-submit flow must complete that task cleanly. Train customer service before broader rollout so they can manage accounts and subscriptions and handle escalations from automation.

Week 4#

Use the final week to review outcomes against the Week 1 baseline, then inspect exception logs before making broader rule changes. Prioritize what is happening by failure type and customer segment using your own data.

Use exceptions to find routing mistakes and cases that required manual repair. Document the reason for every rule change so later reviews are traceable, especially as vendor documentation can change without notice and is not guaranteed to be error-free.

If internal results show a rule is not working for a cohort, narrow or revert it instead of scaling it across all accounts. Related: How to Build a Dunning Campaign for Your Platform: Sequence Timing and Messaging. If you're turning this checklist into production flows, use the Gruv docs to map idempotent retries, webhook events, and payout status handling.

What to do next with your dunning strategy#

The next step is to put your policy into practice with automation, retries, and follow-up messaging so teams can execute it consistently. Keep recovery work focused on getting customers back to a successful charge while managing involuntary churn risk.

Build the rules your team will actually use#

Start by documenting the tactics you already chose, and prioritize them by expected recovery impact and churn risk in your business. Use your failure mix to set priority. If expired cards, bank declines, or billing errors drive most failures, prioritize card-update messaging, retry timing, and clear follow-up messages ahead of lower-impact tweaks.

Set retry rules by failure type. Define when to retry, when to ask for a new payment method, and when to pause retries until the issue is resolved.

Roll out carefully and tune messaging#

Track whether follow-ups are moving customers back to a successful charge, and watch how changes affect involuntary churn. Recurly cites 3 to 4 messages over a 28-day period as a common checkpoint, not a universal rule. Too many reminders can create fatigue, and generic or inconsistent messaging can reduce campaign effectiveness.

Review it as a product and finance system#

Treat dunning as an operating discipline across billing behavior, customer trust, and revenue outcomes, not just as email automation. Review rules on a regular cadence, check what actually changed, and adjust when recovery gains come with higher churn pressure.

Keep the goal explicit: sustainable revenue recovery with lower involuntary churn. Recurly's 53% involuntary churn figure is a useful scale signal for failed-payment risk, not a guarantee for your customer base.

Need a second set of eyes on your recovery flow design and rollout constraints? Talk to Gruv.

Frequently Asked Questions

What is a dunning strategy, and how is it different from general collections?

A dunning strategy is a structured failed-payment recovery process that uses reminders, retries, and follow-up communication to recover payment and reduce passive churn risk. In subscription businesses, the goal is usually to keep active subscriptions from being lost to unresolved payment issues, not just collect one overdue charge. The provided sources define dunning as this failed-payment sequence; in this context, treat general collections as broader account-recovery work beyond that sequence.

What should every dunning sequence include before adding advanced automation?

Start with a clear reminder series, retries on the current payment method, and a direct path for the customer to add a new method. Those are the two core recovery paths after a failed payment: retry the current method or request a new one. Add written stop and escalation rules so your team does not keep retrying or messaging without a decision.

How many reminders should I send, and over what time window?

There is no universal best reminder count or single time window for every business. Use a defined sequence that starts polite and becomes firmer only if the issue stays unresolved. If your campaign runs 20 days, evaluate recovery on day 21, not mid-campaign.

When should I stop retrying and escalate instead?

Stop retrying when retries are no longer the best recovery path or your final reminder window closes without an update. Then move to action-required escalation instead of silently repeating failed attempts. If email is ineffective, a channel change can help, and SMS is one cited escalation option.

Which metrics best prove a dunning program is working?

Recovery rate is a core metric, but it is only reliable when measured after the campaign window and reviewed with rolling periods. Track all post-failure outcomes, not only recovered payments. If you report only recoveries and ignore passive churn, you can miss the true program impact.

Should I use one dunning policy for all customers or segment by account type?

Do not force every failed payment into one generic sequence. Card expirations, bank declines, and billing errors are different failure causes, so segmenting by failure cause is a practical baseline. Keep a shared core policy, then vary timing, messaging, or escalation where your data supports it.

What should I verify before rolling out dunning changes across all subscriptions?

Verify that each failure type maps to a clear decision: retry the current method, request a new method, or escalate. Confirm that every reminder drives the right customer action and that you can track outcomes after failure, including recovery and churn. Roll out carefully, since small recurring-payment errors can compound into meaningful revenue loss over time.

Try a related tool

Ethan covers payment processing, merchant accounts, and dispute-proof workflows that protect revenue without creating compliance risk.

With a Ph.D. in Economics and over 15 years of experience in cross-border tax advisory, Alistair specializes in demystifying cross-border tax law for independent professionals. He focuses on risk mitigation and long-term financial planning.

Sources

- cisa.gov/news-events/bulletins/sb25-356trusted

- clsbluesky.law.columbia.edutrusted

- ftc.gov/sites/default/files/documents/public_events/...trusted

- ndupress.ndu.edu/Portals/68/Documents/Books/CTBSP-Exports/Cha...trusted

- nlp.stanford.edu/~lmthang/morphoNLM/cwCsmRNN.wordstrusted

- pmc.ncbi.nlm.nih.gov/articles/PMC7243414trusted

- scholarcommons.sc.edu/cgi/viewcontent.cgitrusted

- snap.berkeley.edu/project/12206725trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Smart Dunning Strategies to Sequence Retry Logic for Maximum Recovery

If you treat retry logic as a billing setting, you may get some upside and still create hidden operational gaps. A better starting point is shared ownership across teams. Product decides customer treatment. Engineering controls retry execution and event integrity. Finance ops owns reconciliation and audit-trail review.

A Guide to Dunning Management for Failed Payments

If you run recurring invoices, failed payments are not back-office noise. They create cashflow gaps, force extra follow-up work, and increase **Involuntary Churn** when good clients lose access after payment friction.

Build a Platform Dunning Campaign With Timing You Can Defend

Build this as an operating sequence, not a template library. In practice, dunning starts after a recurring auto-collection attempt fails and combines payment retries with customer notices. Your job is to recover revenue from failed recurring payments without pushing good customers into churn or creating customer confusion.